Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

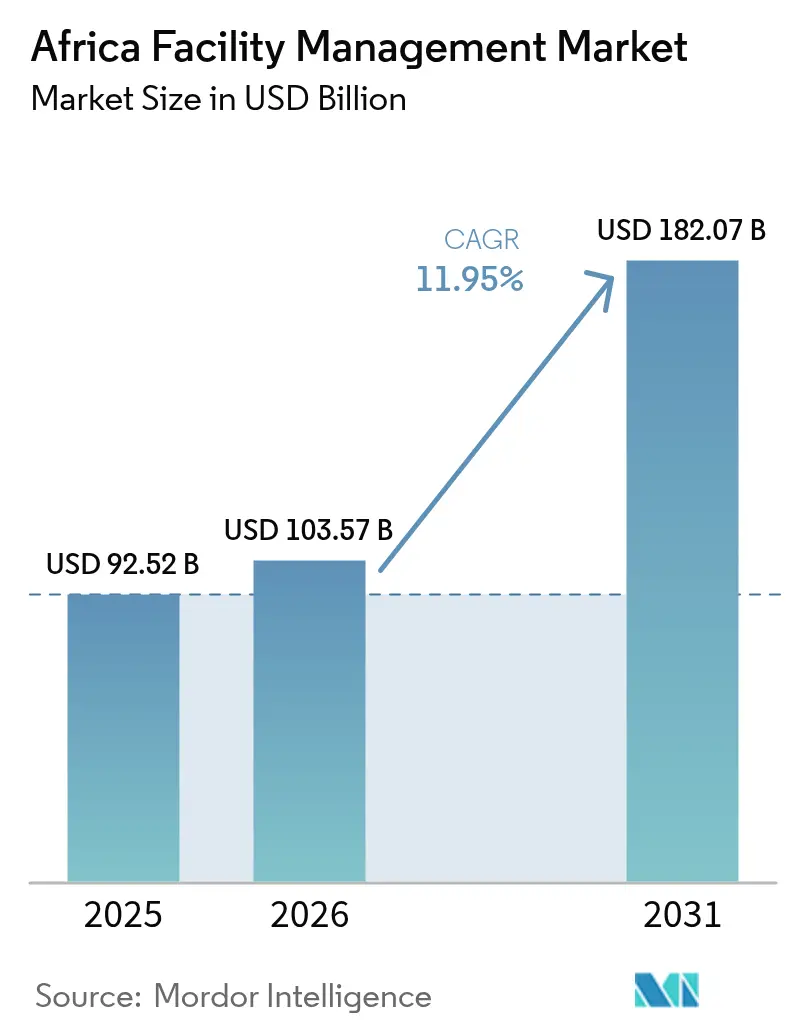

| Base Year Market Size (2025) | USD 92.52 Billion |

| Market Size (2026) | USD 103.57 Billion |

| Market Size (2031) | USD 182.07 Billion |

| Growth Rate (2026 - 2031) | 11.95% CAGR |

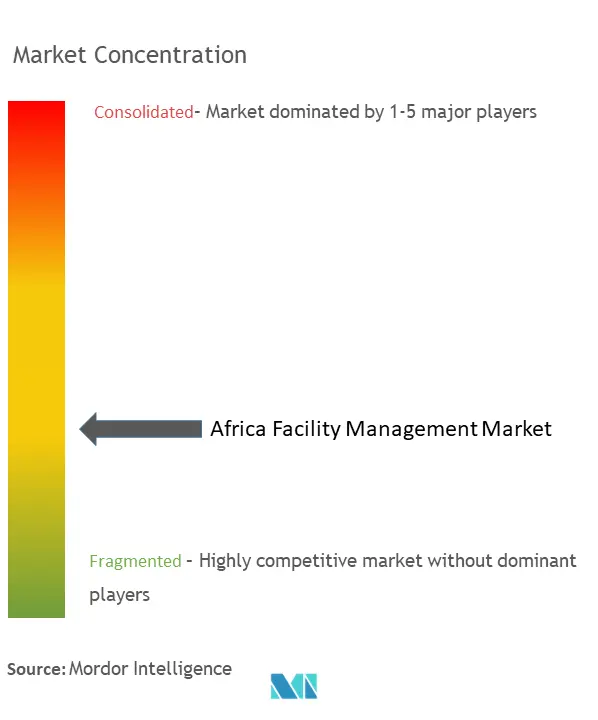

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Facility Management Market Analysis by Mordor Intelligence

Africa Facility Management Market size in 2026 is estimated at USD 103.57 billion, growing from 2025 value of USD 92.52 billion with 2031 projections showing USD 182.07 billion, growing at 11.95% CAGR over 2026-2031. This momentum reflects accelerating infrastructure investment, the growing preference for outsourced service models, and tightening regulatory frameworks that reward professional standards in building operations. Nigeria’s 29.47% share gives it an outsized influence on regional demand, while South Africa and Egypt provide scale, financing depth, and policy stability that attract international providers. Outsourced contracts now account for 67.3% of value thanks to cost-saving synergies and performance guarantees that appeal to private and public owners alike. The commercial segment remains the largest end-user at 40.2% share, though industrial and process facilities are expanding fastest as mining and energy projects add complex sites that demand specialized technical expertise. Technology integration, particularly IoT-enabled building management systems and AI-driven predictive maintenance, underpins margin protection in an inflationary cost environment and positions early adopters to win outcome-based tenders across the Africa facility management market.

Key Report Takeaways

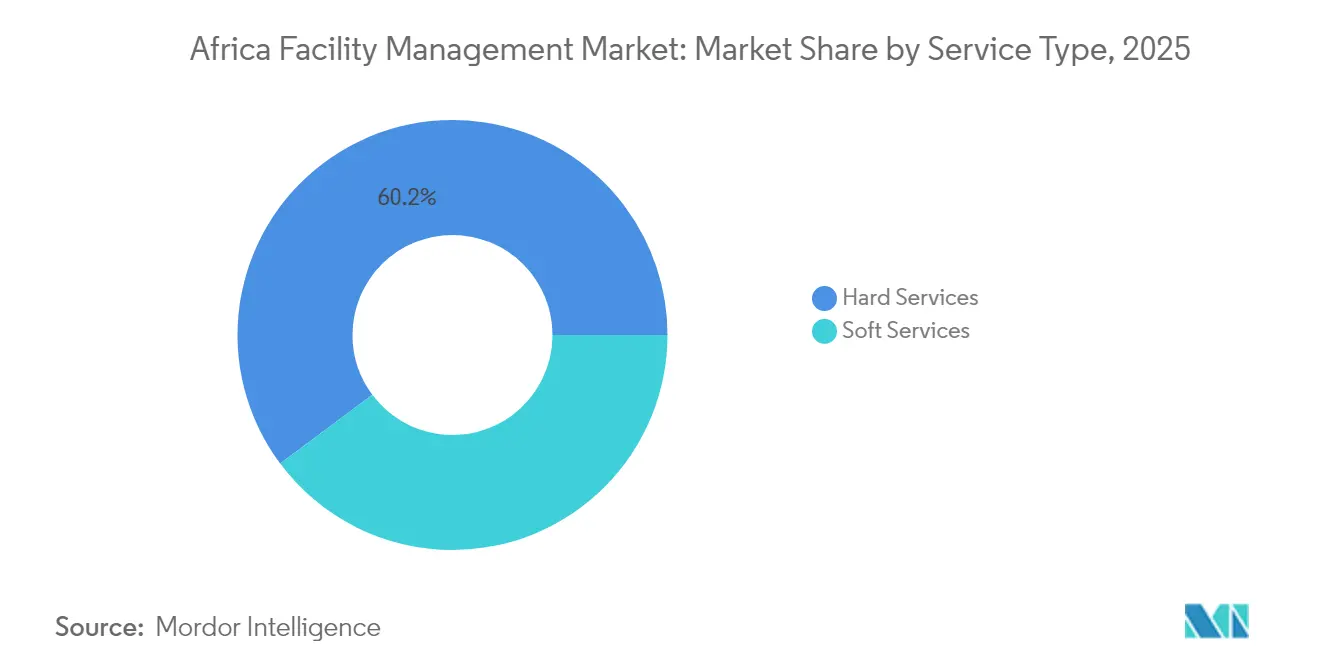

- By service type, hard services led with 60.20% of the Africa facility management market share in 2025; soft services are growing at a 14.54% CAGR and are on course to narrow the gap during the forecast period.

- By offering type, outsourced models accounted for 66.70% of 2025 revenue while expanding at a 13.88% CAGR through 2031. Integrated FM solutions delivered the fastest growth within outsourced models, reflecting demand for single-provider accountability.

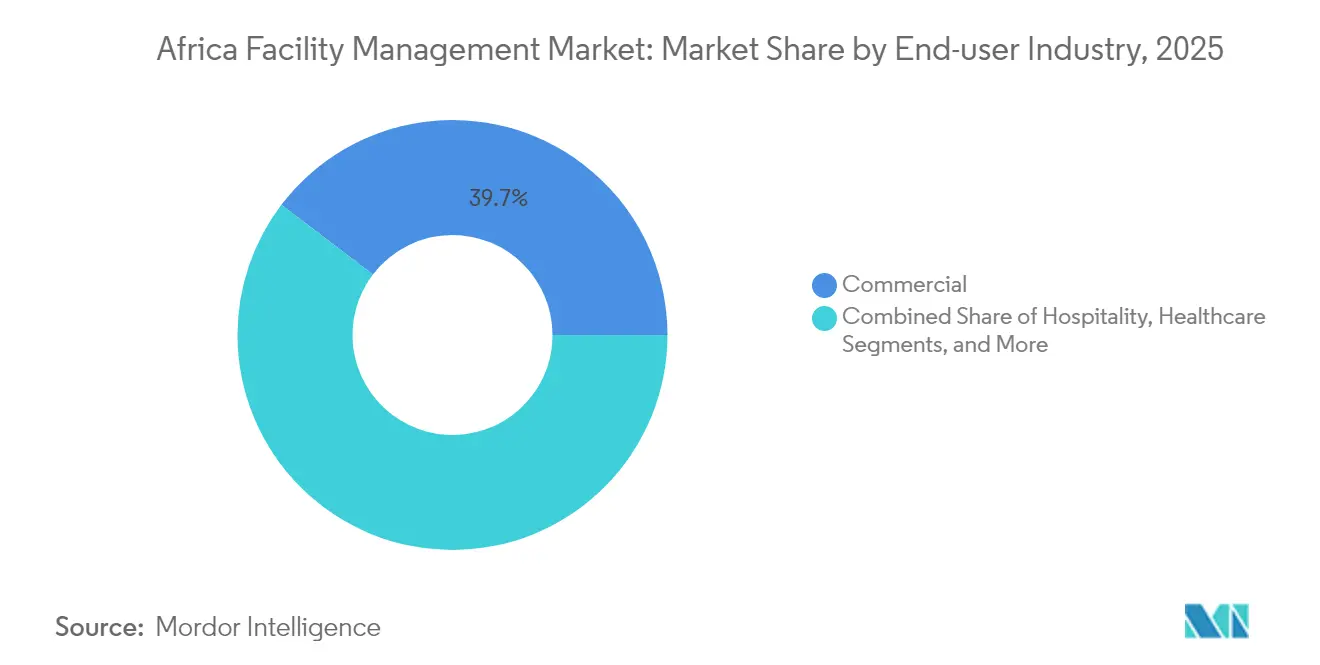

- By end-user industry, commercial facilities held 39.65% share of the Africa facility management market size in 2025, whereas the industrial and process segment recorded the highest projected CAGR at 14.27% through 2031.

- By country, Nigeria retained the largest national position at 29.10% and is expected to sustain a 14.02% CAGR, underpinning continental expansion.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing momentum | +3.2% | Nigeria, South Africa, Egypt | Medium term (2-4 years) |

| Technology integration | +2.8% | South Africa, Nigeria, Egypt | Long term (≥ 4 years) |

| ESG-aligned solutions | +2.1% | South Africa, Egypt, Rest of Africa | Long term (≥ 4 years) |

| Demand for integrated FM | +1.9% | Nigeria, South Africa, Egypt | Medium term (2-4 years) |

| Expansion of Special Economic Zones | +1.4% | Nigeria, Egypt, Rest of Africa | Medium term (2-4 years) |

| Insurance-driven compliance mandates | +1.0% | South Africa, Nigeria, Egypt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Outsourcing Momentum

Organizations across the continent increasingly outsource non-core building operations to unlock capital, standardize processes, and access specialized talent pools. Nigeria’s 2024 Presidential Directive on Local Content Compliance rewards bidders that demonstrate domestic workforce development, encouraging local FM firms to form joint ventures with global specialists.[1]Bola Ahmed Tinubu, “Presidential Directive on Local Content Compliance Requirements, 2024,” nuprc.gov.ng Botswana’s experience with hospital service outsourcing illustrates measurable gains in quality metrics that offset incremental cost, reinforcing the case for managed contracts in public health infrastructure. Contracting models have shifted toward multi-year agreements that bundle technical and support services under performance guarantees, subsequently reducing renegotiation friction and improving budget predictability for asset owners. Facility managers now embed service-level-based key performance indicators that align payment schedules with uptime, energy savings, and user comfort, promoting transparent value delivery. As success stories circulate across peer networks, more boards view outsourcing as a strategic lever rather than a cost-cutting experiment, driving deal volumes in the Africa facility management market.

Technology Integration

IoT sensors, cloud analytics, and AI diagnostics enable remote monitoring, automated fault detection, and predictive maintenance that extend asset life while curbing unplanned downtime. Field evidence shows smart building controls can cut average site energy draw by 36.8 kW during sensor failure scenarios, mitigating utility volatility.[2]Hakilo Sabit and Thit Tun, “IoT Integration of Failsafe Smart Building Management System,” mdpi.com South African pilots using energyAI’s software recorded 10-15% operating cost savings by combining equipment telemetry with weather and tariff feeds to optimize HVAC cycles. Providers that embed digital twins and mobile work-order platforms differentiate by offering live dashboards, automated compliance logs, and data-backed capital planning recommendations. However, the limited pool of technicians versed in data analytics and OT-IT convergence slows large-scale rollouts outside major metros. Training alliances with technical universities and vendor academies are therefore emerging as competitive necessities for firms intent on capturing technology-weighted contracts within the Africa facility management market.

ESG-Aligned Solutions

Sustainability and governance criteria are moving from optional add-ons to baseline procurement requirements. The South African Treasury mandates 90% local sourcing from suppliers with Level 4 B-BBEE ratings by 2025, tying social impact targets to contract eligibility. Data-center operator Digital Realty channels 64% of its African power mix through renewables, signaling that green credentials affect hyperscale site selection. Healthcare facilities such as George Regional Hospital deploy biodegradable consumables and preferentially award janitorial contracts to local SMEs, creating replicable ESG frameworks that influence future tenders. Environmental rules also tighten around refrigerants, wastewater discharge, and solid-waste diversion, compelling FM partners to document science-based reduction targets. As regulators harmonize reporting standards, service bids increasingly request audited ESG scorecards, nudging laggards to upgrade processes or exit the Africa facility management market.

Demand for Integrated FM

Clients are consolidating discrete hard and soft service lines under single contracts to eliminate coordination gaps and unlock procurement scale. An integrated model streamlines governance as one provider becomes custodian of building assets, occupant wellbeing, and sustainability dashboards. Bundled scope also supports outcome-based payments that reward uptime, space utilization efficiency, and carbon mitigation instead of task completion. The trend resonates most in multi-site commercial portfolios seeking consistent brand experience, and in campuses where complex systems require synchronized preventive maintenance and cleaning rotations. FM firms therefore invest in multi-disciplinary teams and cross-skilling programs that allow flexible crew deployment against variable daily demand, boosting utilization rates and contract margins across the Africa facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising operational costs | -2.4% | Nigeria, Egypt, Rest of Africa | Short term (≤ 2 years) |

| Cultural resistance to outsourcing | -1.8% | Nigeria, Rest of Africa | Medium term (2-4 years) |

| Skills gap in digital FM technologies | -1.5% | Nigeria, South Africa, Egypt | Long term (≥ 4 years) |

| Volatile foreign-exchange rates impacting contract viability | -1.3% | Nigeria, Egypt, Rest of Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Operational Costs

Currency devaluation and imported material reliance have pushed Nigerian construction input prices up by 200% since 2023, squeezing FM service margins and forcing renegotiations of long-term contracts. Cement, steel, and skilled labor rates doubled over the same period, while utilities tariffs escalated due to global energy volatility. Providers answer with dynamic pricing clauses, bulk-buy partnerships, and substitution of locally sourced consumables to limit pass-through risk. Some firms leverage remote supervision and sensor-based inspections to lower technician travel expenses, partially offsetting inflation pressure in the Africa facility management market. Yet, persistent logistics bottlenecks and fuel cost spikes threaten cash-flow predictability and limit smaller vendors’ ability to fund tech upgrades.

Cultural Resistance to Outsourcing

Organizational preference for in-house teams remains prevalent, particularly in public institutions where employment protection and institutional knowledge retention are prized. The South African discourse around “consultocracy” highlights concerns over overreliance on external advisers and perceived accountability dilution. FM proponents counter with pilot programs that demonstrate higher service uptime, transparent KPI dashboards, and structured workforce transition plans that absorb existing staff under improved training paths. Over time, evidence-based performance reporting and peer endorsements help erode skepticism, although resistance still lengthens bidding cycles and dampens immediate outsourcing uptake across parts of the Africa facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Revenue While Soft Services Accelerate

Hard services retained a 60.20% share of the Africa facility management market in 2025, anchored by mechanical, electrical, and plumbing maintenance that ensures operational uptime for critical building systems. Mandatory fire-life-safety testing, HVAC optimization, and elevator inspections position technical trades as non-discretionary budget items across commercial towers and industrial plants. Asset owners prioritize hard services when pursuing occupancy certificates and insurance renewals, supporting stable demand even during economic slowdowns. Meanwhile, digital asset registers and condition-based monitoring bolster recurring revenue streams by embedding data-centric workflows into maintenance cycles.

Soft services chart the fastest trajectory with 14.54% CAGR as employers link workplace experience to talent retention and brand perception. Security and office support top growth subsectors because rising urban crime rates and hybrid work models heighten the need for access control, reception management, and concierge services. Cleaning and waste services integrate green chemicals and robotics to meet ESG benchmarks while cutting manual labor intensity. Predictive scheduling triggered by occupancy sensors minimizes overtime, keeps air-quality metrics within health guidelines, and lifts satisfaction scores. This convergence of wellness and efficiency pulls a larger spending envelope toward soft services, gradually narrowing the revenue gap with hard services in the Africa facility management market size.

By Offering Type: Outsourced Models Reshape Market Dynamics

Outsourced contracts commanded 66.70% of 2025 revenue due to a 13.88% growth that far outpaced in-house program budgets. Boards prefer shifting fixed payroll and asset replacement risk onto specialist partners who guarantee uptime and document regulatory compliance. Single-service contracts remain common among cost-conscious SMEs requiring ad-hoc repairs or security patrols, but bundled and integrated FM models together now generate the majority of outsourced revenue as they unlock cost efficiencies of scope and streamline governance. Integrated FM further benefits from technology-enabled reporting that unifies KPIs across disciplines, delivering real-time scorecards valued by risk committees.

In-house teams retain footholds in sectors with sensitive data or statutory staffing mandates, such as defense campuses and select healthcare facilities. Even here, hybrid structures are emerging where proprietary staff oversee strategy while third-party technicians handle peak-load tasks and specialist trades. Nigeria’s local content rules accelerate domestic provider formation and joint ventures, driving knowledge transfer and capitalizing on the Africa facility management market share of indigenous firms. Across the continent, decision makers increasingly evaluate life-cycle value rather than headline labor costs, a shift that reinforces outsourced contract momentum.

By End-user Industry: Commercial Leadership Faces Industrial Challenge

Commercial facilities, spanning offices, telecom hubs, retail complexes, and distribution centers, accounted for 39.65% of the Africa facility management market in 2025. Continuous IT uptime, occupant comfort, and brand-aligned aesthetics drive large service envelopes for cleaning, MEP, and security functions. The e-commerce surge expands warehousing footprints that demand integrated loading-dock management, fleet coordination, and energy-efficient lighting retrofits. Financial institutions and technology parks anchor multi-year service agreements that emphasize cyber-physical security integration and regulatory reporting.

Industrial and process facilities deliver the highest projected growth at 14.27% CAGR as mining companies, refiners, and FMCG manufacturers expand capacity to meet export demand. These plants require 24/7 maintenance of heavy equipment, on-site utilities, and hazard-control systems, translating into complex hard-service contracts that carry above-average margins. Sustainability commitments such as Exxaro’s carbon-neutral roadmap embed renewable transition projects and waste-heat recovery tasks into the FM scope. Healthcare, hospitality, and educational campuses add niche requirements—from clinical waste disposal to guest-experience protocols—that encourage providers to develop sector-specific playbooks, broadening clientele across the Africa facility management market.

Geography Analysis

Nigeria leads the Africa facility management market with a 29.10% share in 2025 and maintains a forecast 14.02% CAGR through 2031, buoyed by mega-city expansion, SEZ development, and local-content policies that favor domestic bidders. Lagos State’s Infrastructure Asset Management Agency exemplifies official support for professionalized upkeep of public assets, while oil-and-gas majors outsource MEP services to ensure compliance with stringent safety guidelines. Currency headwinds elevate cost-control urgency, prompting building owners to adopt condition-based maintenance that lowers spare-parts spend and reduces unplanned downtime. Rising operational costs, however, constrain cash flow for small providers, intensifying competition for dollar-denominated contracts and increasing consolidation prospects within the Africa facility management market size.

South Africa ranks second in value and provides a mature regulatory environment that anchors multinational FM headquarters. The 2024 Public Procurement Act introduces a centralized tender portal that improves transparency and encourages cross-border entrants, thereby widening supplier pools and narrowing bid spreads. Government commitment of R1 trillion to infrastructure delivery through 2025 unlocks projects that require turnkey FM once commissioned, ranging from transport hubs to student housing. Domestic champions like Bidvest Facilities Management leverage national scale to fund R&D in smart-building analytics and to expand northward via franchise alliances, reinforcing technology leadership across the Africa facility management market.

Egypt records double-digit growth underpinned by a LE 2 trillion public-investment roadmap emphasizing transport corridors, new-city developments, and industrial estates. Private capital participation reached 63.5% of total project funding in FY 2024/2025, demonstrating investor confidence in stable FM outsourcing frameworks. Growth opportunities concentrate in Greater Cairo, Suez Canal logistics zones, and emerging knowledge cities where premium facilities seek LEED and EDGE certifications. The broader Rest of Africa cluster adds diversity, with Kenya, Ghana, and Côte d’Ivoire advancing PPP pipelines that create first-time outsourcing prospects, and frontier markets adopting donor-funded hospital and education projects that stipulate international FM standards. Collectively, these regions lift the growth profile and risk-adjusted returns of the Africa facility management market.

Competitive Landscape

The Africa facility management market remains fragmented, as disparate regulatory regimes and high local-knowledge requirements foster numerous national and sub-regional specialists. Top regional groups such as Bidvest Facilities Management, Tsebo Solutions, and Servest Africa command extensive contract portfolios in South Africa, leveraging shared services centers and fleet synergies to compress unit costs. Nigerian contenders Alpha Mead Group and Broll Nigeria scale on the back of oil-and-gas and commercial-real-estate demand, while Egypt’s Contrack FM draws on construction pedigree to serve mixed-use mega-projects. Collective top-five revenue concentration stays below 30% of continental value, indicating ample room for consolidation.

Technology capability has become a decisive differentiator. Providers deploy IoT gateways, CAFM platforms, and AI-enabled diagnostic engines to promise energy savings, predictive asset replacement, and automated compliance logs. Intellectual-property filings related to heat-pump demand-response systems and smart-meter orchestration underscore rising R&D allocation. [4]Rheem Manufacturing Company, “Heat-Pump Systems Patent,” patents.google.com International entrants either acquire local license holders or form minority-position joint ventures that satisfy market-access quotas while granting operational oversight.

Margin pressure from input-cost inflation accelerates M&A as scale becomes essential for purchasing leverage, multi-site workforce deployment, and digital R&D amortization. Allied Universal’s 2025 acquisition spree signals heightened interest from global security majors repositioning as integrated FM suppliers. Strategic focus is shifting toward outcome-based agreements that bundle risk sharing, thereby rewarding firms with robust balance sheets and data-science talent capable of quantifying performance guarantees throughout the Africa facility management market.

Africa Facility Management Industry Leaders

Bidvest Facilities Management

Apleona GmbH

Tsebo Facilities Solution

Servest Africa

G4S Africa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The South African Treasury allocated R1 trillion over three years for infrastructure projects, releasing construction pipelines valued at R313.5 billion that will require downstream FM services once operational.

- March 2025: Allied Universal completed six global acquisitions totaling USD 240 million in annual revenue, signalling accelerated consolidation in security-led integrated FM offerings across Africa.

- January 2025: Egypt’s Ministry of Planning confirmed private-sector investments of LE 133.1 billion as part of a LE 2 trillion capital plan for FY 2024/2025, broadening the addressable infrastructure base for integrated FM.

- July 2024: South Africa’s new Public Procurement Act took effect, creating a Public Procurement Office and mandating technology-based tender systems that raise transparency in public-sector FM contracting. This policy is set to intensify competition and introduce digital compliance checkpoints across future bids.

Africa Facility Management Market Report Scope

Facility Management is the integration of processes within an organization to maintain and develop the agreed services that support and improve its primary activities' effectiveness. Facility Management covers two main areas: Space & Infrastructure (planning, design, workplace, construction, lease, occupancy, maintenance, and furniture) and People & Organization (catering, cleaning, ICT, HR, accounting, marketing, and hospitality). These two broad areas of operation are commonly referred to as hard facility management and soft facility management.

The Africa facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others), and country (South Africa, Egypt, Nigeria and Rest of Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Country

| South Africa |

| Egypt |

| Nigeria |

| Rest of Africa |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Country | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Africa facility management market?

The Africa facility management market size is valued at USD 103.57 billion in 2026.

How fast is the market growing?

The market is forecast to expand at a 11.95% CAGR between 2026 and 2031.

Which service category generates the most revenue?

Hard services, covering mechanical, electrical, and safety systems, hold 60.20% of 2025 revenue.

Why are outsourced models so dominant in Africa?

Outsourced providers offer performance guarantees and technology capabilities that reduce owner risk and capture 66.70% of the 2025 market value.

Which country leads regional demand?

Nigeria commands 29.10% of market share and is forecast to grow at 14.02% CAGR through 2031.

What technology trends are reshaping facility management?

IoT sensors, AI-driven predictive maintenance, and integrated digital dashboards cut energy consumption and improve compliance reporting, driving contract wins for tech-enabled providers.

Page last updated on: