Ghana Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

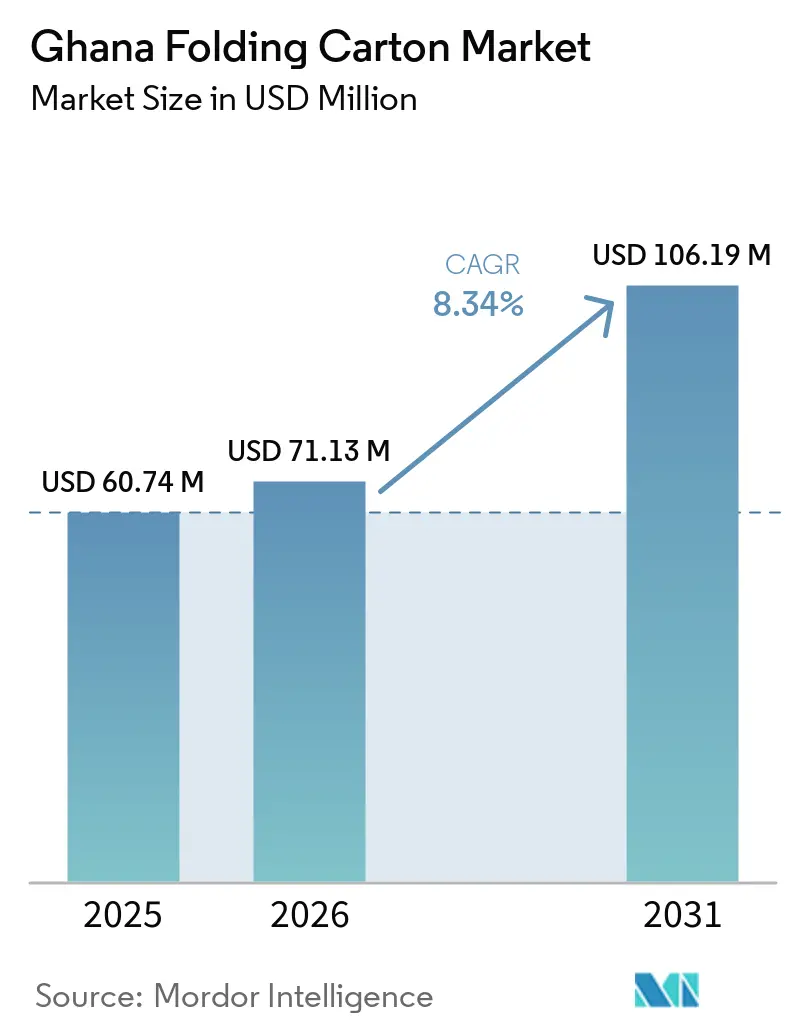

| Base Year Market Size (2025) | USD 60.74 Million |

| Market Size (2026) | USD 71.13 Million |

| Market Size (2031) | USD 106.19 Million |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

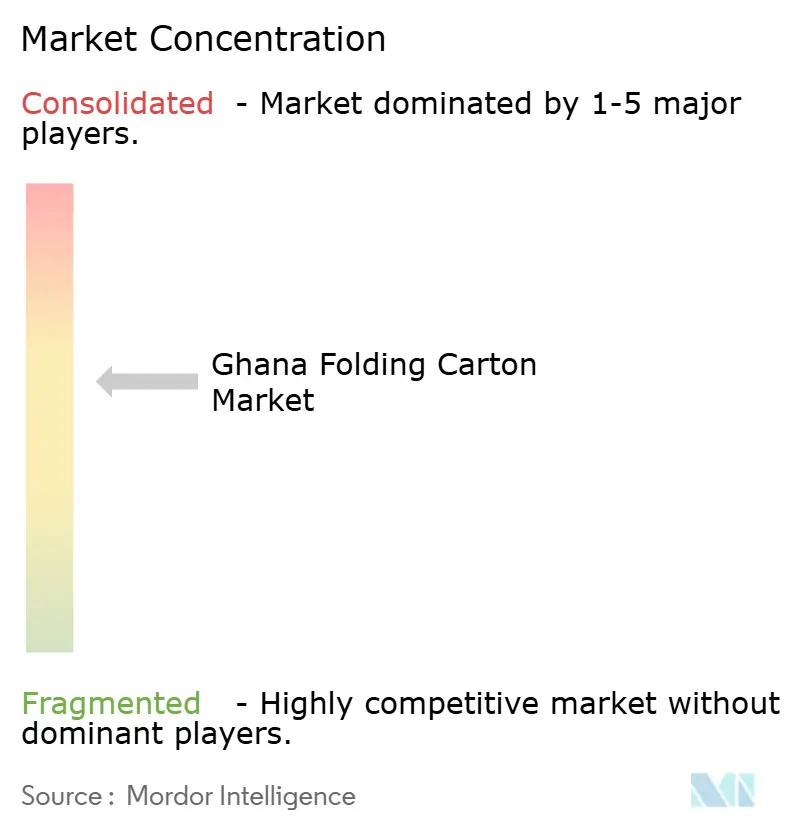

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ghana Folding Carton Market Analysis by Mordor Intelligence

The Ghana folding carton market size is expected to increase from USD 60.74 million in 2025 to USD 71.13 million in 2026 and reach USD 106.19 million by 2031, growing at a CAGR of 8.3% over 2026-2031. Demand is accelerating as pharmaceutical producers align with government vaccine-manufacturing goals, ready-to-eat food brands capitalize on urban convenience trends, and online retailers seek retail-ready secondary packs that withstand last-mile handling. Policy support through the Feed the Industry Program is improving local access to starches, fibers, and other upstream inputs, which lessens foreign-exchange exposure for converters. At the same time, duty-reduced intra-African trade under the African Continental Free Trade Area (AfCFTA) expands Ghanaian converters' customer base. Energy-efficient presses, automated die-cutters, and digital print engines are being installed to offset industrial-power tariffs, which rose 28.2% between January 2025 and March 2026. In addition, the 14% year-on-year cedi depreciation has encouraged converters to hedge inputs and explore home-grown fiber sources, strengthening supply-chain resilience.

Key Report Takeaways

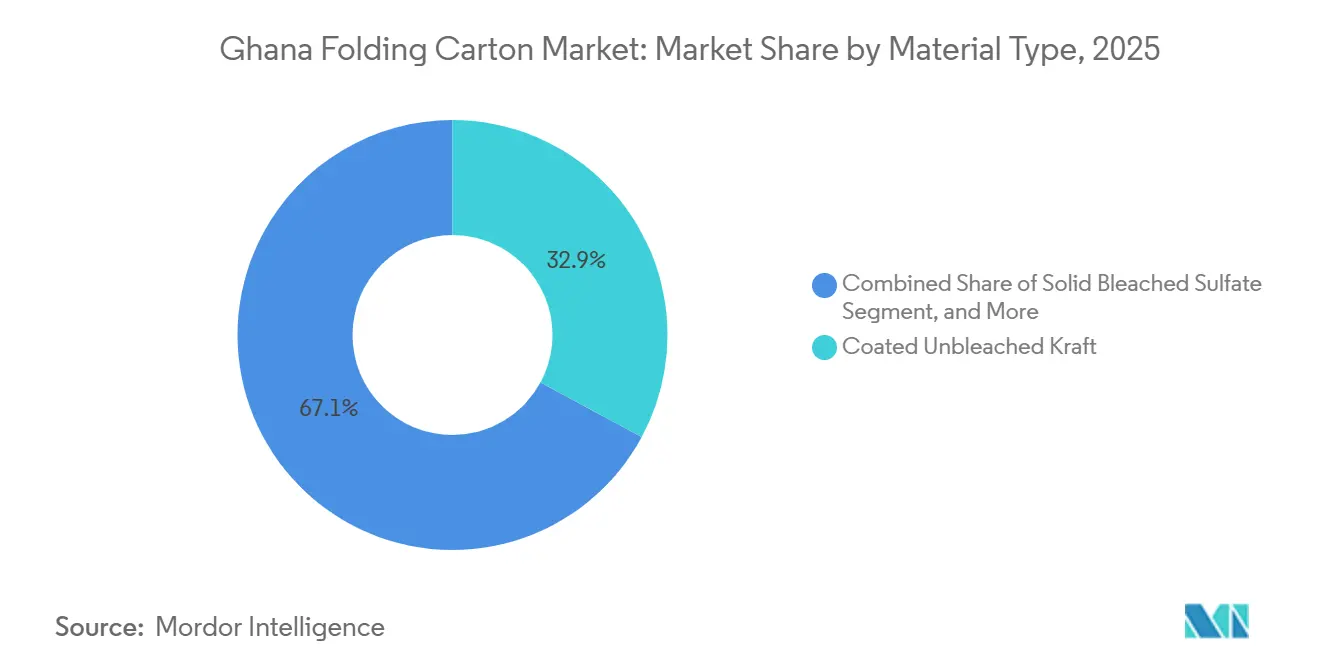

- By material type, coated unbleached kraft captured with 32.87% of the Ghana folding carton market share in 2025.

- By printing technology, the Ghana folding carton market size for digital printing is projected to grow at a 9.61% CAGR to 2031.

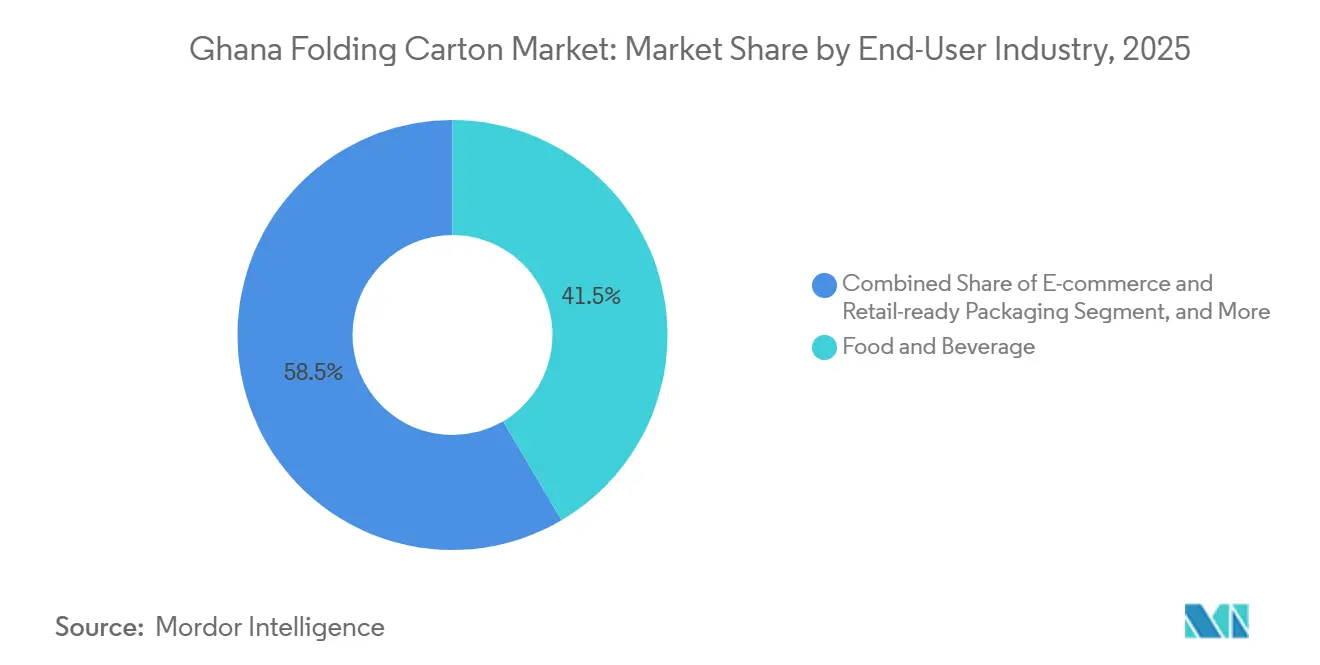

- By end-user industry, the food and beverage industry captured 41.54% of the Ghana folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ghana Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand from Ghana's Fast-Growing Ready-to-Eat Food Sector | + 2.5% | National, concentrated in the Greater Accra and Ashanti regions | Medium term (2-4 years) |

| Expansion of Pharmaceutical Manufacturing Under Government Incentives | + 2.0% | National, early gains in the Tema Industrial Area and the Accra-Tema corridor | Long term (≥ 4 years) |

| Surge in E-Commerce Packaging Requirements Post-COVID | + 1.8% | National, urban-led with spillover to regional capitals | Short term (≤ 2 years) |

| Shift Toward Sustainable Paper-Based Packaging Over Plastics | + 1.5% | National, accelerated by EU export compliance and domestic EPR policy | Medium term (2-4 years) |

| Investment in Automated Folding Carton Converting Lines by Local Converters | + 0.8% | Accra-Tema industrial corridor and Kumasi | Medium term (2-4 years) |

| Growing Popularity of Premium Personal-Care Brands Targeting the Middle Class | + 0.6% | Urban centers of Accra, Kumasi, and Takoradi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Ghana's Fast-Growing Ready-To-Eat Food Sector

Urban households spent USD 1.27 billion on imported processed food in March 2026, 2.5% higher than in 2024, reflecting a pivot toward convenience packs that require rigid secondary barriers for shelf stability. Hotels and restaurants valued at USD 3.2 billion in 2024 have adopted portion-controlled cartons to improve hygiene during service, reinforcing volume growth. Brands such as Niche Cocoa’s Daily Milk have validated aseptic carton formats with a 9-month shelf life, enabling rural distribution without refrigeration. Soft-drink consumption reached 1.05 billion liters in Q3 2024 and is forecast to climb 10.9% a year to 2029, supporting the Ghana folding carton market as beverage fillers seek brand differentiation on crowded shelves. Mandatory ingredient labeling under Legislative Instrument 1541 further lifts demand for high-resolution printing and variable-data capabilities.

Expansion of Pharmaceutical Manufacturing Under Government Incentives

The Health Ministry earmarked GHS 50 million (USD 3.2 million) in August 2025 for vaccine production and launched a National Vaccine Institute, prompting local converters to qualify for blister-carton supply with serialization features. Ghana’s pharmaceutical packaging imports, which accounted for 67% of material demand in 2023, now face substitution by domestic folding-carton suppliers able to meet Good Manufacturing Practice standards. AfCFTA allows duty-free entry into 53 markets if rules-of-origin criteria are met, creating scale economies for compliant Ghanaian converters. World Bank-backed transformation programs are also nurturing more than 6,000 start-ups, many in nutraceuticals, which require tamper-evident, leaflet-insert cartons for export readiness.

Surge in E-Commerce Packaging Requirements Post-COVID

Smartphone penetration reached 68% in 2026, and the national e-commerce market is forecast to touch USD 1.17 billion by 2028, expanding 10.9% annually. Online sellers prefer shelf-ready folding cartons that double as display trays, cutting corrugated use and lowering logistics costs. A new digital trade corridor with Rwanda and Zambia promises near-real-time payment settlement, enabling lean inventory for fulfillment centers. Women-led exporters trained by the Export Promotion Authority in February 2026 now specify digital-print cartons for low minimum order quantities, fueling the adoption of inkjet and toner presses. Ghana and Togo’s joint cargo-management system has already cut border dwell times by 60%, encouraging trade in packaged consumer goods along the Akanu-Noepe route

Shift Toward Sustainable Paper-Based Packaging Over Plastics

Plastic pollution costs Ghana USD 6 billion a year, or 11% of GDP, spurring the draft Extended Producer Responsibility Act that will impose recovery obligations on brand owners. EU rules effective July 2026 also oblige exporters to meet recycled-content thresholds, making paperboard an attractive alternative. Mohinani Group’s partnership with Norfund on 15,000-tonne rPET plants underscores investor appetite for circular materials, yet folding-carton converters must still secure certified recovered fiber. Tetra Pak’s 90% renewable-content barrier board provides a high-profile case study for carbon-reduction claims among Ghanaian dairy processors. Rising middle-class consumers, particularly in Accra and Kumasi, actively seek eco-friendly packaging, reinforcing momentum toward paper solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Imported Pulp Prices Affects Board Costs | - 0.5% | All converters dependent on imported fiber | Short term (≤ 2 years) |

| Limited Domestic Recycling Infrastructure for High-Quality Recovered Fiber | - 0.3% | National, constraining circular-economy models | Long term (≥ 4 years) |

| Power Supply Instability Increasing Operating Costs for Converters | - 0.2% | Accra-Tema and Kumasi industrial zones | Medium term (2-4 years) |

| Competition From Flexible Plastic Pouches in Low-Price Segments | - 0.2% | Sachet beverages and personal-care formats | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Imported Pulp Prices Affecting Board Costs

Pulp imports reached USD 3.01 million in June 2025 after peaking at USD 4.15 million in May, exposing converters to global market swings.[1]Trading Economics, “Ghana Imports of Pulp of Wood, Paper,” tradingeconomics.com A 14% cedi slide to GHS 13.90-15.30 per USD magnifies cost shocks, eroding margins for price-sensitive food-and-beverage contracts. Import duties benchmarked in dollars exacerbate the squeeze, pushing firms toward forward FX contracts and longer-term supply deals. Although some converters trial bagasse and cocoa-husk pulp, the absence of commercial-scale mills leaves the Ghana folding carton industry structurally reliant on imported fiber.

Limited Domestic Recycling Infrastructure for High-Quality Recovered Fiber

Less than 9% of Ghana’s 1.1 million tonnes of annual plastic waste is recycled, and recovery rates for post-consumer paperboard remain equally limited.[2]Graphic Online, “Cedi Depreciation Bites Hard,” graphic.com.gh World Bank plastic-reduction funds focus on polymers, meaning fiber loops receive little capital support. EU mandates on recycled content for imports after July 2026 force converters to procure costly certified board from offshore sources. A lack of national standards for recycled-content verification adds uncertainty, deterring investment in local sorting and pulping capacity. As a result, circular-economy ambitions risk falling short unless infrastructure spending broadens to include paper recovery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Substrates Anchor Strength-Critical Applications

Coated Unbleached Kraft captured 32.87% of material demand in 2025, underlining its popularity among beverage and canned-goods fillers that need superior burst strength and moisture resistance. The Ghana folding carton market for this grade has benefited from warehouse automation, which enables pallets to withstand higher stacking loads during distribution to Accra and Tema retailers. Solid Bleached Sulfate is projected to grow 10.1% a year through 2031 as premium cosmetics brands seek high-gloss surfaces that convey luxury and print multicolor graphics without surface treatment. Folding boxboard serves mid-tier applications, while white-lined chipboard remains confined to low-budget household goods where print fidelity is less critical.

Converters have begun blending virgin Kraft liners with recycled back panels to trim input costs and hedge against pulp volatility, an approach that protects Ghana's folding carton market share for strength-critical packs without sacrificing sustainability claims. Experiments with bagasse and cocoa-pod fiber offer long-term diversification, though food-contact certification is still pending. Enforcement by the Standards Authority and the Food and Drugs Authority obliges full traceability for medical and food clients, driving adoption of certified chain-of-custody systems. The coming Extended Producer Responsibility Act is expected to reward recycled-content board once domestic recovery improves, offering a new growth lever for converters positioned with dual-fiber supply chains.

By Printing Technology: Digital Gains Ground on Short-Run Flexibility

Lithographic presses supplied 45.93% of Ghana folding carton market demand in 2025, favored for long beverage and pharmaceutical orders that justify plate costs and demand strict color consistency. Yet digital presses are forecast to log a 9.6% CAGR to 2031 as e-commerce sellers, indie beauty brands, and export-oriented SMEs seek rapid artwork changes and serialized QR codes. The public sector reinforced this shift by opening a state-backed digital print center in January 2026 and facilitating local finance for inkjet equipment, lowering entry barriers for smaller converters.

ePac’s 15-business-day lead-time plant in Accra exemplifies how digital workflows reduce obsolete inventory and carbon footprint, themes that resonate with the Ghana folding carton industry’s sustainability narrative. Litho operators are countering by adding hybrid UV-inkjet units for versioning in long runs, while flexo houses are moving into post-print corrugated segments. The Ghana folding carton market size for gravure remains niche, restricted to ultra-long confectionery wraps. Across all platforms, the power-tariff spike is encouraging retrofits with energy-efficient drying and inline quality-control sensors, safeguarding margins amid rising operating costs.

By End-User Industry: Food Anchors Volume, E-Commerce Drives Growth

Food and beverage brands accounted for 41.54% of cartons shipped in 2025, reflecting steady population growth and a hotel-restaurant sector valued at USD 3.2 billion. Growing imports of processed food, flavored milk launches, and dairy aseptic lines sustain high-volume replenishment for litho converters. The Ghana folding carton market linked to e-commerce is set to expand at 9.9% annually, buoyed by digital payment adoption and improved border clearance that make door-to-door fulfillment viable beyond Accra.

Healthcare packaging is poised for double-digit gains as the vaccine-production roadmap and Good Manufacturing Practice enforcement take hold. Track-and-trace codes, tamper labels, and leaflet inserts draw on the Ghana folding carton market share of digital printers offering variable data. Cosmetics continue to ride a projected rise from USD 29.3 million in 2023 to USD 46.2 million in 2027, as premium formulations demand solid bleached substrates. Tobacco cartons require rotating 50-65% pictorial warnings, keeping volume intact while forcing converters to adopt high-efficiency artwork management to navigate frequent regulation-driven changes.

Geography Analysis

Accra-Tema remains the logistics hub of the Ghana folding carton market, combining proximity to Tema Port and Kotoka International Airport with a dense consumer base. The new 1,238-acre Afienya Export Processing Zone offers serviced plots and tax advantages that shorten go-to-market time for converters aiming to feed AfCFTA demand.[3]The Vaultz News, “Afienya EPZ: Ghana's Plug-and-Play Industrial Hub,” thevaultznews.com Kumasi is emerging as a parallel hub after Twellium and Sidel installed Africa’s fastest PET water line, attracting ancillary packaging investments. Such decentralization reduces trucking distances for clients in northern and central Ghana, lowering delivered-box costs and expanding the Ghana folding carton industry's footprint.

Further north, improved road links to Burkina Faso and Niger enhance prospects for carton exports under the Economic Community of West African States corridor. The Akanu-Noepe one-stop border post has already cut clearance from eight to roughly three hours, stimulating regional trade. Western port expansion at Takoradi and fresh warehousing in Sekondi further diversify supply-chain options, improving resilience in the face of recurring power outages along the Eastern Corridor.

The AfCFTA, the EU-Ghana Economic Partnership Agreement, and the African Growth and Opportunity Act grant duty-free access to continental, European, and United States buyers once the relevant standards are met. Consequently, converters are investing in ISO 9001, Forest Stewardship Council, and FSSC 22000 certifications to guarantee market entry. High inland freight charges remain a hurdle, yet falling electronic tolls and port-digitalization drives are narrowing Ghana’s cost gap with Côte d’Ivoire and Nigeria.

Competitive Landscape

The Ghana folding carton market is moderately fragmented, with eight to ten overseas majors serving multinationals and a wider field of local converters focused on rapid turnaround. International Paper, Mondi, and Graphic Packaging supply high-volume pharma and beverage lines, while Packrite Ghana, Xpresspak Ghana, and Printex Limited differentiate through custom runs and design services. FON Group’s corrugated start-up, which serves 80 fast-moving consumer goods companies, highlights local-scale success as multinationals localize sourcing.

Technology is the main battlefield. ePac’s carbon-neutral digital plant offers speed and low minimums, luring emerging food brands away from litho incumbents.[4]Packaging MEA, “ePac Flexible Packaging Opens New Plant in Accra,” packagingmea.com In response, Universal Investment and Industries ordered a second high-speed Theegarten-Pactec cartoner to double throughput to 2,800 products per minute. Strategic alliances with equipment vendors, exemplified by Tetra Pak’s work with Niche Cocoa and Sidel’s line for Twellium, give converters access to global technical support and co-innovation pathways.

White-space innovation is intensifying around shelf-ready cartons that eliminate restocking, aseptic packs for ambient dairy, and tobacco cartons with variable art mandated by regulators. Flexible-pouch suppliers are also chipping at low-price sachet niches, demonstrated by Mushplus Agri-Foods’ switch from paper cartons to pouches for extended shelf life. The resulting competitive mix supports moderate buyer choice while preventing any single vendor from dominating share.

Ghana Folding Carton Industry Leaders

Sonapack Ghana Ltd

Packrite Ghana Ltd.

FON Packaging Ventures

Tetra Pak (West Africa) Limited

Ghana Printing and Packaging Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Ghana Free Zones Authority opened the Afienya Export Processing Zone near Tema Port to speed investor onboarding.

- April 2026: The Environment Ministry forwarded an Extended Producer Responsibility Act to the Attorney-General, flagging future recycling obligations for converters.

- April 2026: Electricity Company of Ghana launched a GHS 3.46 billion (USD 223 million) power-reliability program.

- March 2026: Chroma Digital Solutions installed a Canon Colorado M5W wide-format printer, widening local digital capacity.

Ghana Folding Carton Market Report Scope

The scope of the report covers the analysis of the folding carton market in Ghana, focusing on its current trends, growth drivers, challenges, and opportunities. These cartons are lightweight, recyclable, and customizable, making them a preferred choice for packaging. The report provides insights into market dynamics, competitive landscape, and key developments shaping the folding carton market in Ghana.

The Ghana Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Ghana folding carton market?

The Ghana folding carton market size is projected at USD 71.13 million for 2026, rising toward USD 106.19 million by 2031 according to Mordor Intelligence.

Which material type holds the largest share of carton demand in Ghana?

Coated Unbleached Kraft leads with 32.87% of volume, favored by beverage and canned-food fillers for its high burst strength.

Which printing technology is growing the fastest?

Digital printing is forecast to post a 9.6% CAGR through 2031 as e-commerce and cosmetics brands demand rapid artwork changes and variable data.

How will AfCFTA influence folding-carton producers?

Duty-free intra-African access under AfCFTA expands the reachable customer base, enabling Ghanaian converters to scale automated lines for regional export.

What regulatory changes affect sustainable packaging?

A draft Extended Producer Responsibility Act and upcoming EU recycled-content mandates push converters toward higher recovered-fiber use and design-for-recycling features.

Which end-user segment is expected to grow quickest through 2031?

E-commerce and retail-ready packaging is expected to advance at a 9.9% CAGR, outpacing all other user groups as online retail spending rises.

Page last updated on: