Kenya Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

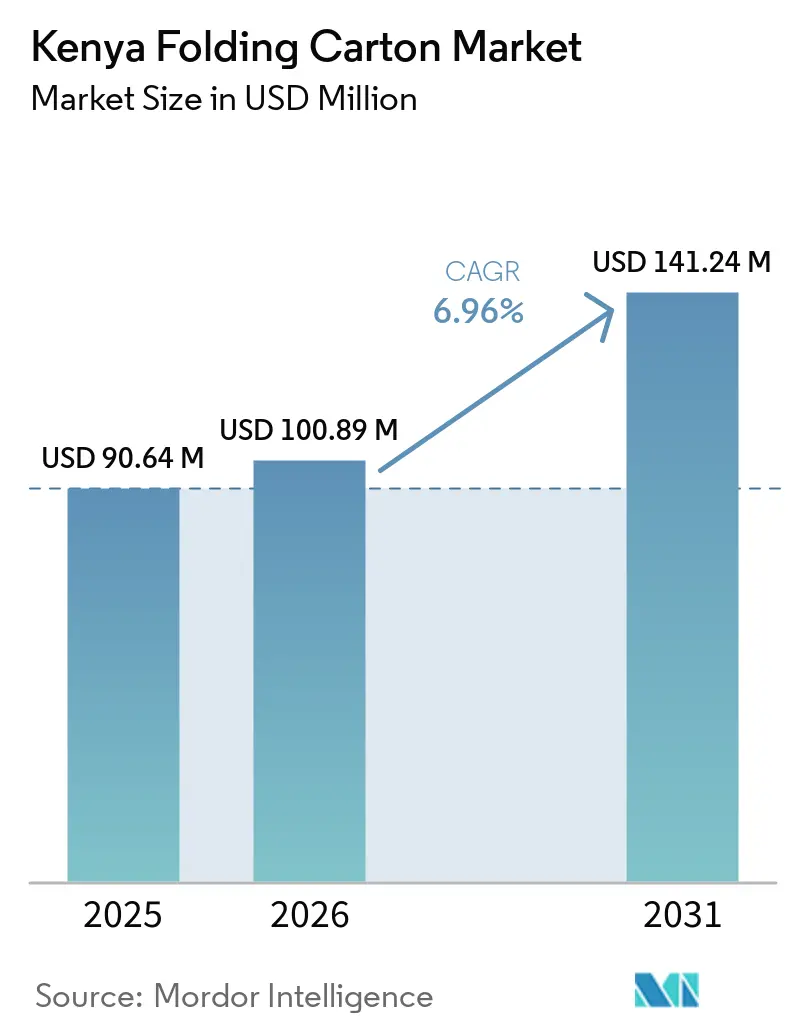

| Base Year Market Size (2025) | USD 90.64 Million |

| Market Size (2026) | USD 100.89 Million |

| Market Size (2031) | USD 141.24 Million |

| Growth Rate (2026 - 2031) | 6.96% CAGR |

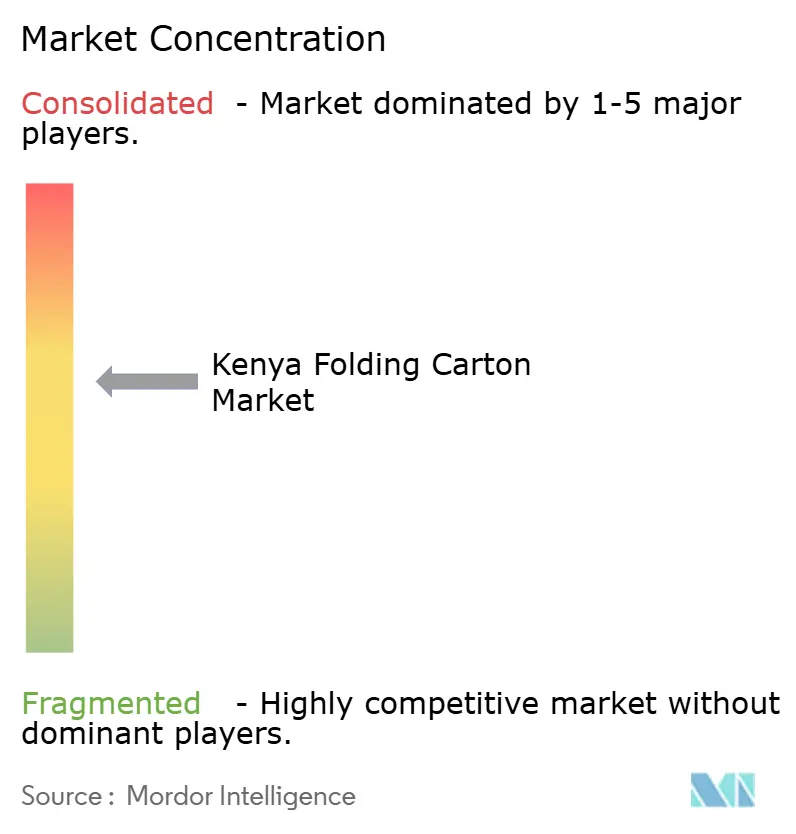

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya Folding Carton Market Analysis by Mordor Intelligence

The Kenya folding carton market size is expected to increase from USD 90.64 Million in 2025 to USD 100.89 Million in 2026 and reach USD 141.24 Million by 2031, growing at a CAGR of 6.96% over 2026-2031. Intensifying enforcement of the Sustainable Waste Management Act, the nationwide ban on single-use plastics under 30 microns, and rising import tariffs on non-recyclable packaging are steering brand owners toward paper-based formats. Parallel government directives that target 50% local pharmaceutical production by 2026 and mandate Extended Producer Responsibility (EPR) certification for all incoming packaging are expanding order volumes for converters that can meet serialized, tamper-evident, and food-contact safety specifications. Investment momentum is strong: Phase 1 of the Konza Biopharma Park alone attracted USD 57 Million, while multiple FMCG multinationals enlarged in-country capacity, anchoring demand for domestic folding cartons. On the technology front, converters are pivoting to short-run digital presses and automated cartoning lines that compress lead times and satisfy the SKU proliferation linked to urban single-serve, or “kadogo,” pack formats.

Key Report Takeaways

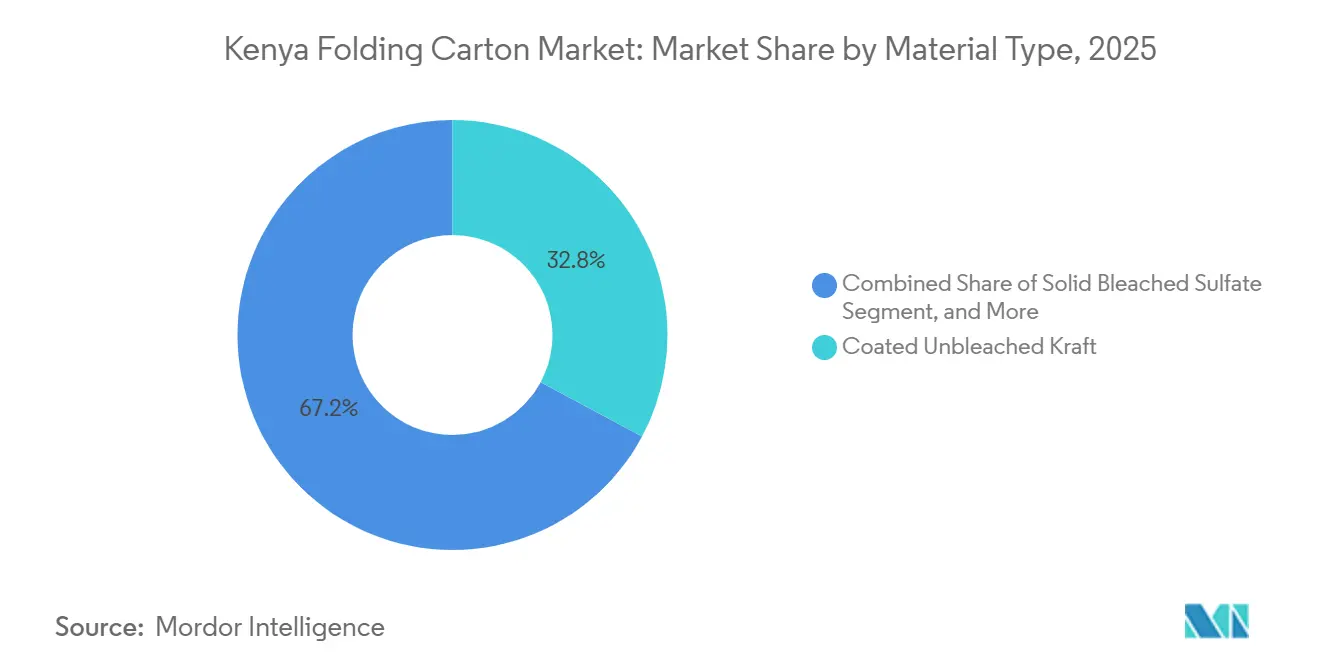

- By material type, coated unbleached kraft captured with 32.83% of the Kenya folding carton market share in 2025.

- By printing technology, the Kenya folding carton market size for digital printing is projected to grow at a 7.57% CAGR to 2031.

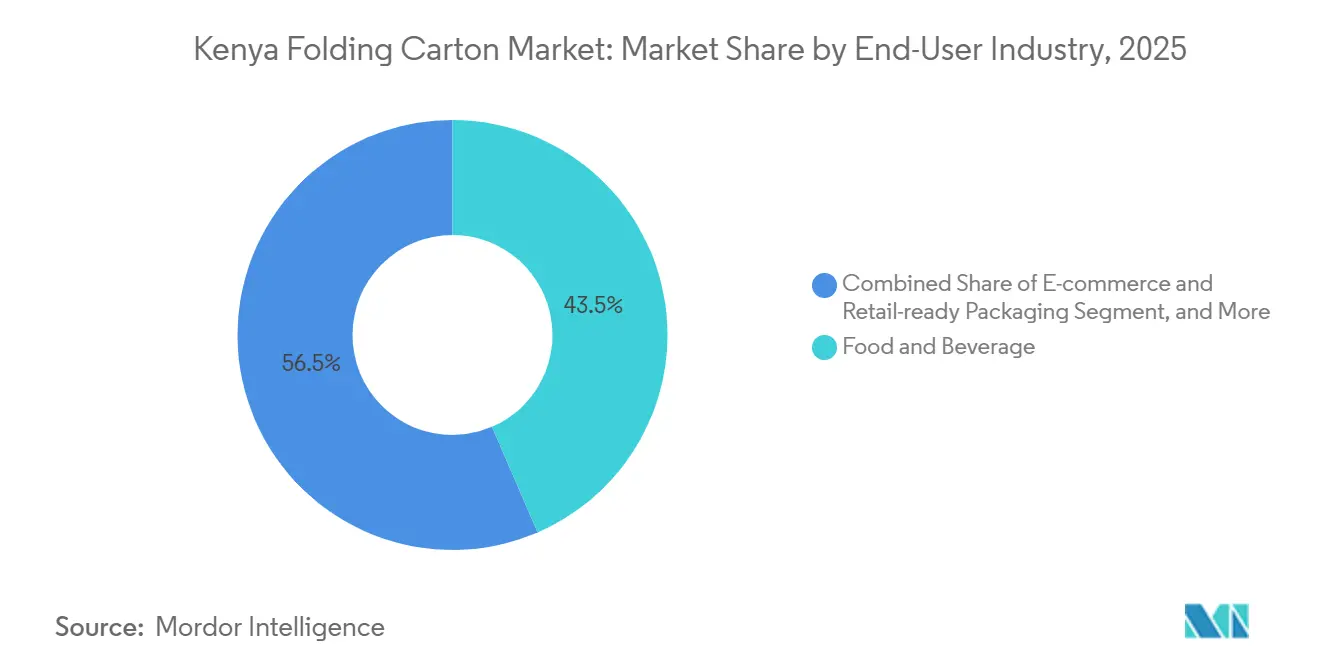

- By end-user industry, the food and beverage industry captured 43.52% of the Kenya folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kenya Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Penetration of Packaged Foods in Urban Centers | +1.2% | National, major cities | Medium term (2-4 years) |

| Accelerating Expansion of E-Commerce Fulfillment Networks | +1.4% | National, rural uptake | Short term (≤ 2 years) |

| Government Ban on Single-Use Plastics Driving Paper Substitution | +1.8% | Nationwide | Long term (≥ 4 years) |

| Growing Adoption of Automated Cartoning Lines Among SMEs | +0.9% | Nairobi Industrial Area and Athi River | Medium term (2-4 years) |

| Increasing Consumer Preference for Sustainable Packaging | +0.7% | Urban and Peri-urban | Long term (≥ 4 years) |

| Surge in Pharmaceutical Manufacturing Capacity in Kenya | +1.0% | National, Konza, and Murang’a | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Ban on Single-Use Plastics Driving Paper Substitution

Kenya’s Sustainable Waste Management Act and the EPR Regulations gazetted in 2024 obligate producers to recover post-consumer packaging, forcing brand owners to redesign away from flexible plastics.[1]Kenya Plastics Pact, “EPR Regulations Gazetted,” kpp.or.ke NEMA-enforced bans on carrier bags and new mandates for resin identification codes elevate folding cartons into default primary and secondary packs, especially for dry groceries and personal care. Chandaria Industries invested KES 5 Billion (USD 38.5 Million) in a recycling-backed mill that converts 4,000 tonnes per month, supplying converters with recycled-content board compliant with EPR thresholds. Multinationals now specify ISO 14001 and FSC chain-of-custody in tenders, reinforcing the shift. The policy certainty and green-label pull together account for a material +1.8% lift on the long-term CAGR.

Accelerating Expansion of E-Commerce Fulfillment Networks

Jumia Kenya recorded a 34% year-on-year revenue jump in Q4 2025 and operates over 300 pickup stations, 60% of which are in rural counties. Rural distribution demands lightweight, stackable cartons that withstand rough handling yet minimize dimensional-weight charges. E-commerce operators also insist on retail-ready formats that require no secondary repacking, raising per-parcel carton volumes. Sidel’s July 2026 opening of an East Africa office provides OEM-level line engineering, helping converters synchronize carton, label, and pallet configurations. These combined logistics and technology shifts are estimated to add +1.4% to market growth over the next two years.

Rising Penetration of Packaged Foods in Urban Centers

Kenya’s packaged-food retail value climbed from USD 5.1 billion in 2023 to a projected USD 7.3 billion by 2028, driven by 28% urbanization and the micronized “kadogo” format, which multiplies SKU counts. Brands such as Brookside and Bidco migrated from bulk packs to portion-controlled cartons, boosting unit orders per tonne of food. Secondary cities Kisumu and Nakuru are reporting double-digit growth in modern retail, with shelf-ready cartons featuring tamper-evident closures. Pending front-of-pack label regulations are expected to trigger a fresh redesign cycle that favors carton substrates for improved legibility. Collectively, these consumption and compliance factors add 1.2% to the medium-term CAGR.

Surge in Pharmaceutical Manufacturing Capacity in Kenya

The presidential target to localize 50% of pharmaceutical output by 2026 spurred USD 57 Million Phase 1 investment at Konza Biopharma Park and a KES 65 Billion (USD 500 Million) China-Kenya deal that mandates local carton printing with serialized barcodes. Pharmaceutical cartons require high-brightness Solid Bleached Sulfate, anti-tamper glue flaps, and variable data printing. Converters installing UV-curable digital presses can now meet 48-hour lead times, a necessary cadence for prescription stock-keeping. These capacity builds and compliance norms contribute roughly +1.0% to forecast CAGR through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Imported Pulp and Paperboard Prices | -0.8% | Nationwide | Short term (≤ 2 years) |

| Competition From Flexible Plastic Pouches in Low-Cost Segments | -0.6% | Nationwide | Medium term (2-4 years) |

| Fragmented Printing Infrastructure Limiting High-Quality Output | -0.5% | Nairobi and Mombasa | Medium term (2-4 years) |

| Limited Domestic Recycling Collection Systems | -0.4% | Rural counties | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Imported Pulp and Paperboard Prices

Kenya imported USD 425.5 million of board in 2024, relying on Scandinavia, South Africa, and Asia for Coated Unbleached Kraft and Solid Bleached Sulfate. Disruptions in the Red Sea during 2024 stretched lead times to 75 days and lifted container rates by as much as 60%, slicing converter margins by 200-300 basis points. Although Mondi’s European capacity additions may temper global virgin-fiber pricing by 2027, Kenya’s distance and reliance on spot markets dilute the benefit. Chandaria’s 4,000 tonne recycling line cushions some cost swings but cannot produce food-contact-grade SBS, keeping high-spec import reliance intact and imposing a -0.8% drag on near-term growth.

Competition From Flexible Plastic Pouches in Low-Cost Segments

Price-sensitive FMCG categories, from powdered detergents to fortified porridge, still gravitate toward flexible pouches that cost up to 30% less per fill than entry-level folding cartons. SME brand owners facing EPR-related cash deposits frequently default to laminated sachets to preserve working capital, despite looming compliance fees. While upcoming recycled-content mandates will erode some of plastic’s cost advantage, pouch converters are also investing in thinner laminates and recyclable mono-materials. This entrenched low-cost alternative absorbs about -0.6% of the market’s potential CAGR over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Cost-Efficient Kraft Holds Ground as Pharmaceutical-Grade SBS Accelerates

Coated Unbleached Kraft dominated the Kenya folding carton market with a 32.83% market share in 2025, driven by beverage multipacks and dry-food staples that prioritize stacking strength over aesthetics. The Kenya folding carton market for Solid Bleached Sulfate is projected to grow fastest at a 7.83% CAGR, driven by pharmaceuticals, cosmetics, and premium confectionery that specify virgin-fiber substrates that comply with FDA and Kenya Bureau of Standards migration limits. Pharmaceutical expansion at Konza Biopharma Park and bilateral manufacturing deals guarantee a captive pipeline for SBS, whereas Kraft remains the choice for cost-engineered SKUs in staples and industrial goods.

Converters are also exploring a hybrid Folding Boxboard that layers recycled inner plies with a virgin facing, offering a mid-priced option for the personal-care and snack sectors. Specialty grades such as holographic or metalized board still account for less than 5% of demand, but are rising in tobacco and spirits packs following Kenya’s 2025 excise stamp and anti-counterfeit regulations. Certification under FSC or PEFC has now become the baseline for export-oriented lots, aligning with global buyer audits.

By Printing Technology: Flexo Remains Workhorse While Digital Scales With SKU Proliferation

Flexographic presses preserved 39.53% share of the Kenya folding carton market in 2025, owing to cost-efficient plate technology and compatibility with water-based inks mandated by VOC caps. However, brand diversification into micro-batches is prompting the Kenya folding carton industry to install digital equipment capable of handling 1,000-unit runs with zero plate costs. Digital share is therefore projected to record a 7.57% CAGR through 2031, especially as EPR traceability rules call for variable QR codes and serialized numbering.

Hybrid presses that combine flexo decks with inkjet bars are emerging, letting converters toggle between mass and micro volumes without additional floor space. This modular philosophy underpins new Nairobi installations from Sky Labels and Digital Packaging Innovations Holdings, cutting standard lead times from seven days to as low as 48 hours.[2]Sustainability MEA, “Sky Labels Expands Operations,” sustainabilitymea.com Lithographic and gravure stations still anchor ultra-long runs for cigarettes and spirits needing 8-color metallic effects, yet their capital intensity deters most SMEs.

By End-User Industry: Food and Beverage Dominates as E-Commerce Cartons Post Quickest Lift

Food and Beverage represented 43.52% of the 2025 Kenya folding carton market, buoyed by Coca-Cola Beverages Africa’s USD 175 million multi-plant pledge and Unilever’s KES 17 billion (USD 131 million) Tatu City investment. Format shifts to shelf-ready trays and six-pack carriers stimulate larger-surface cartons that support both branding and recycling instructions. E-commerce and Retail-ready Packaging is forecast to outpace all others at an 8.16% CAGR, mirroring Jumia’s 300-station pickup lattice and rural order flow.

These shipments depend on lightweight cartons with puncture-resistant liners to survive unpaved routes while trimming volumetric weight charges. Pharmaceuticals follow closely, galvanized by the government’s 50% localization target that obliges tamper-evident, serialized, FSC-certified cartons. Personal Care, tobacco, and household chemicals round out the portfolio, each responding differently to evolving labeling and excise frameworks but collectively deepening the addressable Kenya folding carton market.

Geography Analysis

Nairobi and its satellite corridors, Athi River, Ruiru, and Thika, account for roughly 55-60% of national converting capacity, reflecting the clustering of FMCG headquarters, pharmaceutical labs, and e-commerce fulfillment hubs. Mombasa contributes an additional 15-20%, servicing coastal tourism and acting as the gateway for tea, coffee, and cross-border flows into Uganda and Rwanda. Introduction of the EPR import certificate, effective March 2026, lifts landed carton costs by up to 5% at the Kilindini terminal, indirectly favoring Nairobi-based producers, who are shielded from the levy.

Westward, Kisumu is emerging as a regional anchor, supplying the dairy and brewery corridors of Lake Victoria, yet it still relies on Nairobi presses for high-definition work. Secondary growth nodes Nakuru, Eldoret, and Nyeri are showing double-digit sales increases in modern retail but lack local board conversion, resulting in two-day transit times and elevated logistics buffers. Rural counties, newly served by Jumia’s network, reinforce the necessity for cartons that balance cube efficiency with durability on rough terrain.

Cross-border arbitrage within the East African Community shapes the competitive map. Kenyan converters leverage superior print infrastructure and port proximity to ship cartons into Tanzania, Uganda, and the Democratic Republic of Congo, countering each market’s divergent EPR fee timelines.[3]Pack-Lab, “Packaging Regulations in Africa: 2025 Updates,” packlab.gr The USD 57 Million Konza Biopharma Park, situated 60 kilometers from Nairobi, cements the capital’s magnetism for pharma-grade print jobs that must comply with Kenya Bureau of Standards serialization rules.

Competitive Landscape

Four leading firms, Chandaria Industries, Kenafric Packaging, Ramco Printing Works, and Carton Manufacturers, collectively held about 40% of available capacity in 2025, signaling moderate concentration that still leaves headroom for specialist entrants. Kenaf’s March 2025 integration of Economic Industries elevated its stationery share from 12.3% to 22.6%, setting a precedent for family-owned consolidations designed to amortize EPR compliance costs. Ramco Plexus’ buyout of Platinum Packaging added gravure and digital assets, opening new revenue lanes for tobacco and spirits.

International capital is equally active: Printcare PLC inaugurated a high-precision mono-carton plant in Nairobi in March 2025, in partnership with the Karimjee Group.[4]Packaging MEA, “Printcare Launches Advanced Packaging Facility in Nairobi,” packagingmea.com The operation injects world-class color management and sustainability reporting, raising competitive benchmarks. Sky Labels brought East Africa’s first AccurioLabel 230 digital press online, enabling 48-hour cosmetic runs that capture premium margins. Parallel to these moves, Sidel’s July 2026 engineering hub underscores OEM confidence in Kenya’s shift from manual to automated end-of-line carton systems.

Strategic gaps persist in backward-integrated recycled board and in specialty finishes. Chandaria’s 4,000 tonne mill offers partial security of supply but not enough to satisfy the mandated 30% recycled-content threshold by 2030. Anti-counterfeit features such as holographic foils, tactile varnish, and UV-reactive inks are gaining in tobacco and spirits sectors, pushing converters to partner with global security providers. ISO 9001, 14001, and FSC certifications now represent table stakes for multinational bids, leaving non-accredited SMEs increasingly restricted to low-margin domestic spot orders.

Kenya Folding Carton Industry Leaders

Tetra Pak Kenya Ltd

East African Packaging Industries Ltd

Statpack Industries Ltd

ASL Packaging Limited

Shri Krishana Overseas plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NEMA activated a mandatory EPR import-certificate workflow through Kenya’s Single Window System, imposing a KES 150 (USD 1.03) fee per outermost package.

- January 2026: COMESA launched a merger probe into Guala Closures’ plan to buy Metal Crowns Kenya, flagging potential regional competition impacts.

- March 2025: Printcare PLC commissioned a mono-carton and corrugated facility in Nairobi via alliance with the Karimjee Group.

- March 2025: Kenafric Packaging finalized the acquisition of Economic Industries, doubling its stationery share to 22.6%.

Kenya Folding Carton Market Report Scope

The scope of the report covers the analysis of the folding carton market in Kenya, focusing on its current trends, growth drivers, challenges, and opportunities. These cartons are lightweight, recyclable, and customizable, making them a preferred choice for packaging. The report provides insights into market dynamics, competitive landscape, and key developments shaping the folding carton market in Kenya.

The Kenya Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Kenya folding carton market size and how fast is it growing?

The market stood at USD 90.64 Million in 2025, is set to reach USD 100.89 Million in 2026, and is forecast to expand to USD 141.24 Million by 2031 at a 6.96% CAGR, according to Mordor Intelligence.

Which material type is gaining the fastest traction among converters?

Solid Bleached Sulfate is projected to register the quickest 7.83% CAGR through 2031 as pharmaceutical and cosmetics orders demand high-brightness, food-contact-compliant board.

How are EPR regulations reshaping packaging choices in Kenya?

The 2024 EPR Regulations impose post-consumer recovery obligations and a KES 150 (USD 1.03) import fee, pushing FMCG brands to substitute single-use plastic pouches with locally produced folding cartons.

Which end-user segment will deliver the highest growth by 2031?

E-commerce and Retail-ready Packaging is expected to post an 8.16% CAGR due to the expansion of rural pickup stations and rising parcel volumes.

What technology investments are converters making to stay competitive?

Firms are installing digital presses and automated cartoning lines to handle short runs, variable data printing, and quick changeovers, reducing lead times from a week to as little as 48 hours.

How concentrated is the supplier landscape?

The four largest players control around 40% of capacity, classifying the field as moderately consolidated, yet open for high-value niche entrants.

Page last updated on: