Middle East And Africa Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

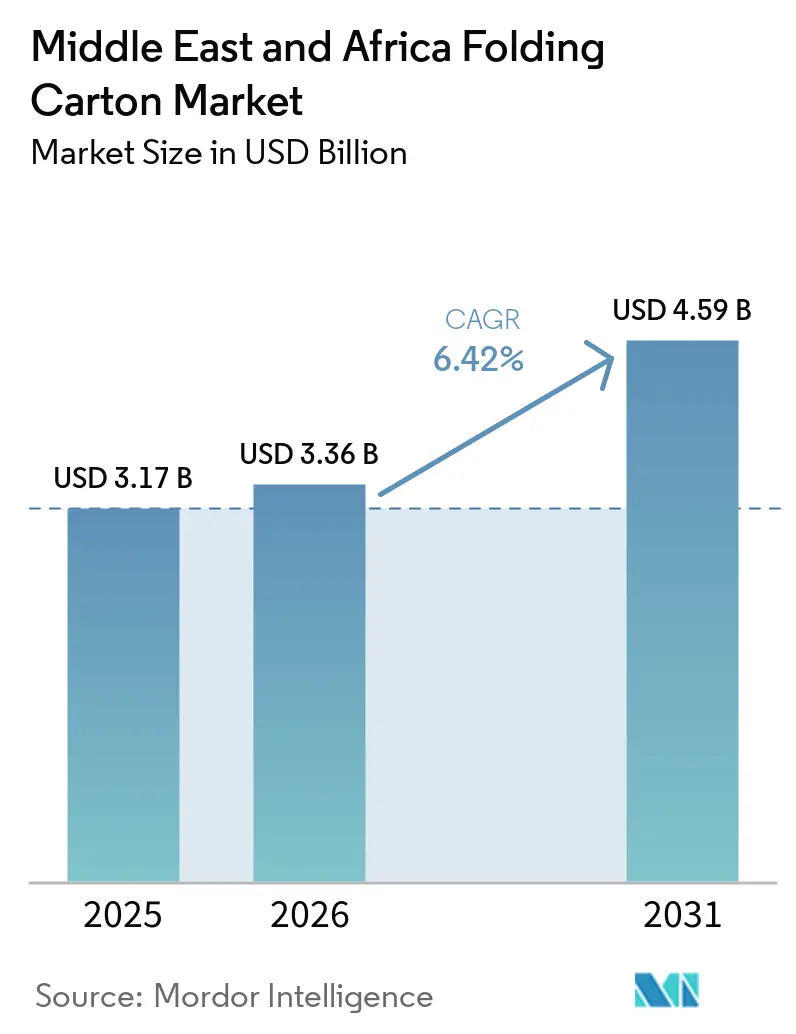

| Base Year Market Size (2025) | USD 3.17 Billion |

| Market Size (2026) | USD 3.36 Billion |

| Market Size (2031) | USD 4.59 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

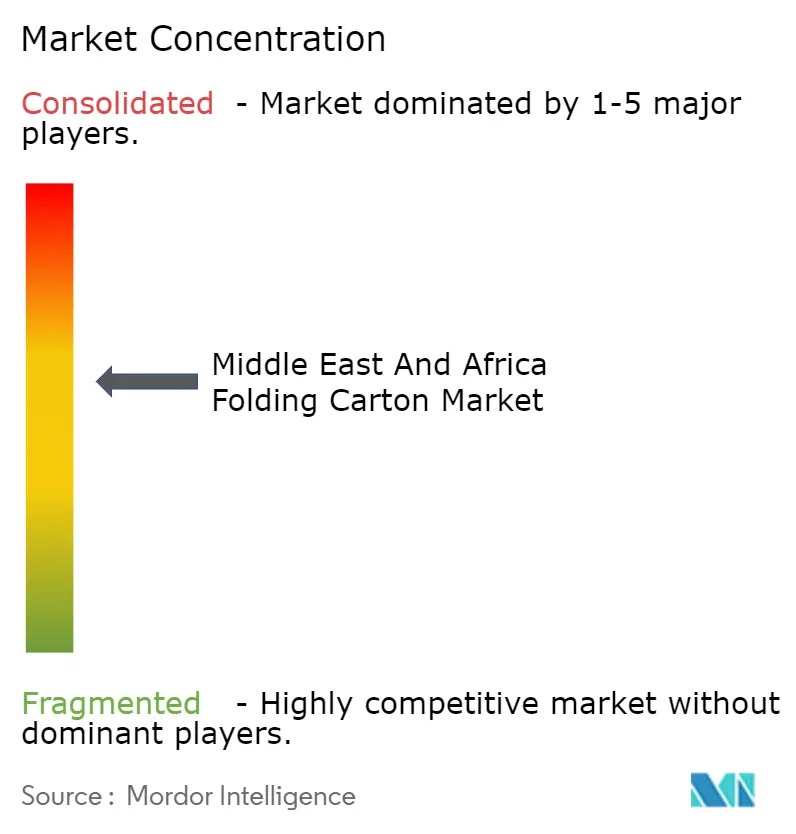

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Folding Carton Market Analysis by Mordor Intelligence

The Middle East and Africa folding carton market size is expected to increase from USD 3.17 billion in 2025 to USD 3.36 billion in 2026 and reach USD 4.59 billion by 2031, growing at a CAGR of 6.42% over 2026-2031. Rapid shifts toward paper-based formats, rising e-commerce parcel volumes, and pharmaceutical cold-chain expansion are accelerating demand across consumer goods, healthcare, and retail channels. Brand owners are adopting digitally printed short-run cartons that support SKU proliferation and personalized promotions, while regulatory bans on single-use plastics in Gulf Cooperation Council markets create mandated substitution tails. Converters that combine integrated substrate sourcing with high-speed digital press fleets are positioned to defend margins against pulp price volatility and consolidate share. Competitive intensity is moderate to high as global leaders scale up through mergers and divestitures, while regional converters invest in specialty grades and finishing capabilities. Smurfit Westrock’s USD 34 billion combination in 2024 heightened scale-based rivalry, yet International Paper’s planned spin-off of its EMEA business in 2026 may open acquisition pathways for regional players.

Key Report Takeaways

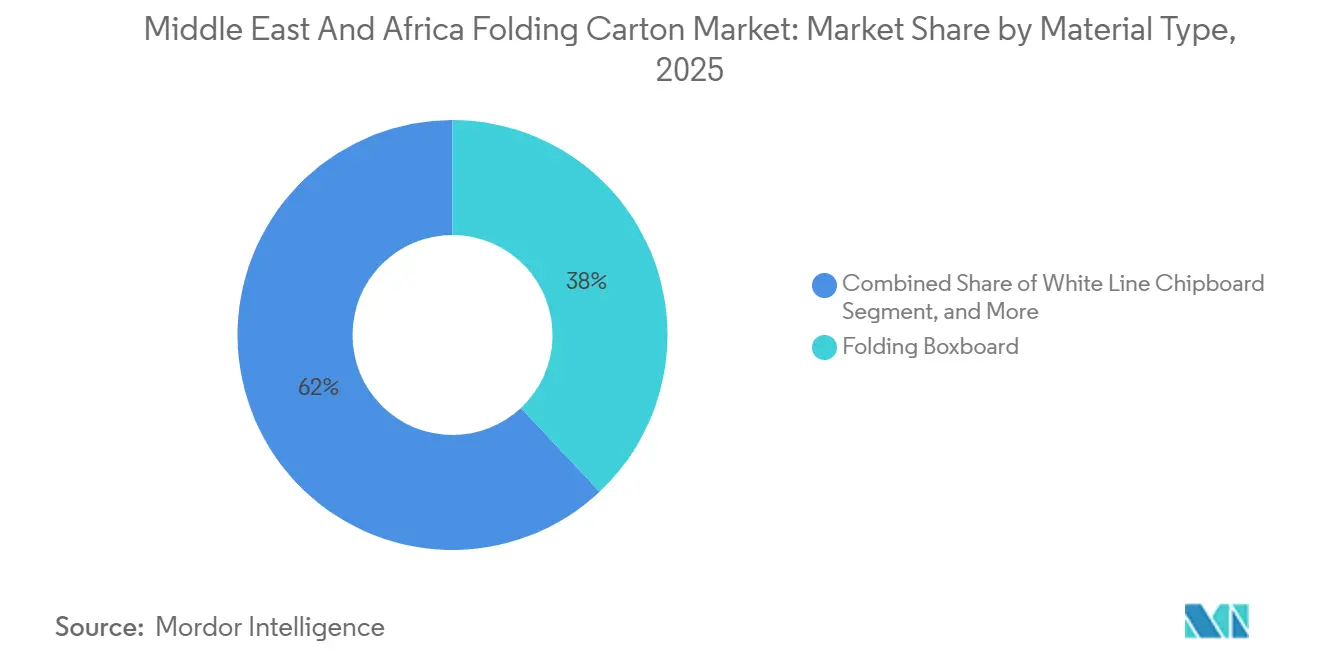

- By material type, folding boxboard accounted for 38.0% of the Middle East and Africa folding carton market share in 2025.

- By printing technology, the Middle East and Africa folding cartons market size for the digital printing segment is forecast to advance at a 12.8% CAGR through 2031.

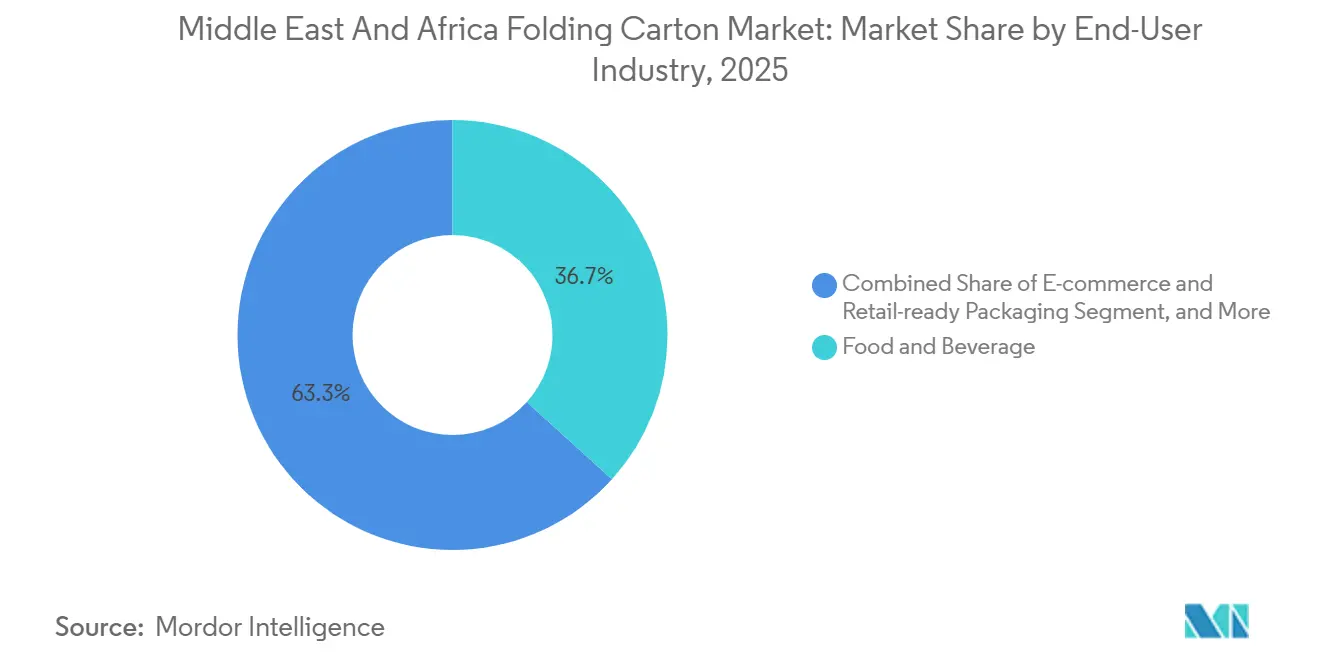

- By end-user industry, food and beverage captured 36.7% of the Middle East and Africa folding carton market share in 2025.

- By geography, the Middle East and Africa folding cartons market size for Nigeria is forecast to advance at an 11.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urbanization Driving Packaged Food Consumption | +1.2% | Saudi Arabia, UAE, Egypt, Nigeria, Kenya | Medium term (2-4 years) |

| E-Commerce Expansion Requiring Lightweight Transit Packs | +1.5% | Saudi Arabia, UAE, Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| Government Plastic-Reduction Policies Favoring Paper-Based Packaging | +1.0% | UAE, Saudi Arabia, Egypt, South Africa | Short term (≤ 2 years) |

| Pharmaceutical Cold-Chain Growth Requiring Barrier-Coated Cartons | +0.8% | Saudi Arabia, UAE, Egypt, South Africa | Medium term (2-4 years) |

| Investment In High-Speed Digital Presses Enabling Short-Run SKUs | +0.6% | Saudi Arabia, UAE, Egypt, South Africa | Medium term (2-4 years) |

| Rise Of Halal-Certified Food Exports From GCC | +0.5% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization Driving Packaged Food Consumption

Urban populations are swelling across the Middle East and Africa, prompting modern grocery formats to replace open-air markets in secondary cities. Supermarket chains in Nigeria, Egypt, and Kenya prioritize shelf-ready folding cartons for cereals, biscuits, and powdered beverages because the packs stack neatly, carry large branding areas, and withstand humid distribution corridors. Rising middle-class incomes in Gulf Cooperation Council cities are boosting demand for premium graphics, resealable closures, and certified sustainable substrates that folding cartons can deliver. Local converters are upgrading pre-press workflows and offset lines to meet brand owner requirements for color accuracy, while import substitution programs in Saudi Arabia encourage domestic sourcing of cartonboard grades. As migration concentrates purchasing power in urban hubs, folding-carton volumes grow faster than population because consumers favor portion-controlled, hygiene-sealed formats over loose goods.

E-commerce Expansion Requiring Lightweight Transit Packs

Online retail penetration is escalating, with platforms such as Noon, Jumia, and Amazon scaling fulfillment networks in Riyadh, Dubai, Lagos, and Nairobi. Brand owners choose folding cartons over heavier corrugated boxes for cosmetics, electronics accessories, and over-the-counter medicines, where structural rigidity is achievable with 250-350 gsm solid bleached sulfate. Variable-data digital presses allow converters to print order-specific graphics, QR codes, and seasonal artwork without makeready waste, minimizing inventory obsolescence. Subscription boxes for beauty and health products rely on litho-laminated folding cartons that optimize dimensional-weight tariffs, lowering last-mile costs. The surge of cloud kitchens and quick-commerce grocery apps in Gulf capitals drives demand for grease-resistant cartons that preserve food integrity and brand aesthetics during delivery.

Government Plastic-Reduction Policies Favoring Paper-Based Packaging

The United Arab Emirates enforced its single-use plastic ban on January 1, 2026, spurring foodservice operators to shift cutlery-overwraps, confectionery trays, and QSR meal boxes to paperboard formats.[1]UAE Ministry of Climate Change and Environment, “Single-Use Plastic Ban,” moccae.gov.ae South Africa’s Extended Producer Responsibility rules allocate end-of-life costs to producers, increasing the appeal of folding cartons that integrate smoothly into established curbside recycling. Egypt’s waste-management reforms incentivize pack designs with high fiber recoverability, nudging multinational brand owners to harmonize carton specifications across regional markets. Although enforcement intensity varies, global consumer-goods companies apply the strictest standards to streamline procurement, effectively exporting Gulf compliance norms to North and sub-Saharan Africa. These mandates set a regulatory floor for carton demand, even in jurisdictions with limited inspection capacity.

Pharmaceutical Cold-Chain Growth Requiring Barrier-Coated Cartons

Public-health agencies in Saudi Arabia, the UAE, and South Africa invest in temperature-controlled logistics for vaccines and biologics, spurring the need for secondary packs that resist condensation, UV-light, and oxygen. Converters laminate aqueous or extrusion coatings on solid bleached sulfate to meet moisture-vapor-transmission targets while preserving board recyclability. Validation protocols require stability data under 25-45 °C cycles, raising the technical bar and favoring suppliers that partner with resin and dispersion innovators. Tetra Pak’s high-renewable barrier technology, adapted from aseptic beverage lines, demonstrates scalability for pharmaceutical formats and may reduce aluminum foil dependency by more than 40%. Contract packagers view barrier-coated cartons as a way to reduce plastic thermoform use, improve pack density, and simplify cold-chain validation paperwork.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Pulp Prices Compressing Converter Margins | -0.9% | Region-wide exposure to global supply | Short term (≤ 2 years) |

| Under-Developed Collection Systems Limiting Recycled Fiber Availability | -0.6% | Nigeria, Kenya, Egypt, Rest of Africa | Long term (≥ 4 years) |

| Growing Plastic Barrier Films In Aseptic Cartons | -0.4% | Middle East, North Africa | Medium term (2-4 years) |

| Political Instability Affecting Cap-Ex Decisions In Parts Of Africa | -0.5% | Sudan, Ethiopia, Nigeria, Kenya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Pulp Prices Compressing Converter Margins

Northern Bleached Softwood Kraft prices climbed to USD 1,710 per tonne in early 2026 after energy-cost spikes and Scandinavian supply constraints.[2]Pulp and Paper Chronicle, “Global Paper Industry Update – February 2026,” pulpandpaperchronicle.com Folding-carton converters, many of which are reliant on imported virgin fiber, endure 60-90-day lags before contract price adjustments, eroding working-capital buffers. Currency depreciation in Nigeria and Egypt amplifies landed-cost inflation, while smaller converters lacking hedging facilities risk rapid margin compression. Although Saudi Arabia’s MEPCO is doubling capacity to 900,000 tonnes per year, the mill targets tissue and specialty grades rather than the coated boxboard essential for high-graphics food cartons. Cost pass-through resistance from retailers dampens investment appetite for new litho lines, nudging converters toward lightweighting and digital workflows that cut substrate usage.

Under-Developed Collection Systems Limiting Recycled Fiber Availability

South Africa achieves a 63.3% paper recovery rate, yet most sub-Saharan markets collect under 30% of post-consumer fiber.[3]Paper Recycling Association of South Africa, “South Africa Paper Recycling Statistics 2025,” prasa.co.za Informal pickers focus on PET bottles and aluminum cans, leaving paperboard streams contaminated with food residues that hinder de-inking yields. Converters in Lagos and Nairobi import recovered fiber from Europe or South Africa, adding freight and fumigation costs that narrow the price gap with virgin pulp. Extended Producer Responsibility frameworks in Kenya and Egypt mandate producer-funded collection, but municipal capacity shortfalls delay infrastructure roll-out. The scarcity of clean recovered board limits the ability to meet brand-owner commitments for 50% recycled content by 2030, thereby restricting the circular-economy narrative that underpins premium price positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Grades Rise as Barrier Needs Intensify

Solid statistics underscore the scale of this shift. Folding Boxboard held a 38.0% slice of the Middle East and Africa folding carton market in 2025, while Solid Bleached Sulfate is set to grow at a 9.4% CAGR through 2031. Multinational confectionery and skincare brands prefer the latter for its brightness, odor neutrality, and compatibility with aqueous dispersion barriers. Pharmaceutical blisters and nutraceutical sachets are migrating from PVC wallets to SBS cartons that pass accelerated-aging tests, reinforcing premium substrate adoption.

Growth trajectories diverge across value chains. Cost-sensitive household detergent packs in Egypt retain white-lined chipboard, yet Gulf cosmetics marketers pay premiums for FSC-certified SBS paired with tactile varnishes. Recycled grades, such as RDM’s Vincicoat PLUS, which deliver 15-20% higher tensile strength, enable brand owners to claim recycled content without downgrading graphics. This bifurcation rewards converters that can source both low-cost mixed-waste boards and high-performance virgin fiber, sustaining service breadth for diverse customer tiers.

By Printing Technology: Digital Presses Unlock SKU Agility

Lithographic equipment secured 42.5% of the Middle East and Africa folding carton market size in 2025, but Digital Printing is pacing growth at 12.8% CAGR through 2031. HP Indigo 200K installations in Dubai and Johannesburg achieve 130 linear meters per minute, slashing turnaround from weeks to hours for cosmetics launch kits. Brand owners use digitally printed micro-batches to A/B-test flavors and fragrances, interpreting sell-out data before committing capital to long litho runs.

Hybrid workflows marry litho economics with digital personalization. A base graphic prints offset at 18,000 sheets per hour, then passes through a single-pass inkjet unit to apply variable QR codes and language versions. Flexographic and gravure presses maintain niches in tobacco inner frames and confectionery gift boxes, yet the capital expenditure case weakens as inkjet resolution surpasses 1,600 dpi. As consumable costs fall, converters translate savings into competitive pricing, widening digital adoption across mid-tier accounts.

By End-User Industry: E-Commerce Jumps From Niche to Core Channel

Food and Beverage dominated the Middle East and Africa folding carton market with a 36.7% share in 2025, supported by cereals, biscuits, and dairy powders that require stackable, moisture-resistant board. E-commerce and Retail-ready Packaging is sprinting ahead at a 13.7% CAGR to 2031, buoyed by smartphone penetration and last-mile platform investment. Quick-commerce grocery services in Riyadh and Dubai prefer grease-proof SBS cartons for ready-to-eat meal kits, while electronics vendors adopt shock-absorbent paperboard inserts that displace plastic bubble sleeves.

Pharmaceutical demand accelerates as Ministries of Health expand vaccine schedules and expand access to chronic-disease drugs. Barrier-coated cartons replace cold-chain plastic clamshells, meeting recyclability mandates and reducing pack weight by up to 30%. Personal-care brands leverage digital embellishments, such as holographic foils and raised UV, to differentiate their shelf presence. Mature segments like tobacco plateau as regulation tightens display restrictions, pushing carton value toward tax-stamp security features rather than volume expansion.

Geography Analysis

Saudi Arabia anchors the Middle East and Africa folding carton market with an 18.4% share in 2025. Vision 2030 programs subsidize agrifood self-sufficiency, stimulating domestic carton demand for poultry, flour, and dairy. MEPCO’s upstream pulp expansion aims to localize fiber sourcing, counter freight volatility, and secure board supply for Riyadh’s converter cluster. The kingdom’s halal-certified dairy exporters deploy barrier-coated SBS cartons to access Southeast Asian markets, reinforcing premium-grade momentum.

The United Arab Emirates accelerates substitution toward paperboard following its single-use plastic ban, creating lift in foodservice sleeves, QSR meal boxes, and pharmacy blister cartons. Dubai Airport’s duty-free channel favors high-graphics gift packs for confectionery and cosmetics, raising per-unit value. Qatar’s hospitality pipeline, fueled by cultural and sporting mega-events, drives demand for rose-gold metallic cartons that satisfy luxury presentation norms. Turkey functions as a transshipment node linking European cartonboard mills with Gulf converters, although domestic folding-carton capacity remains thin.

Nigeria charts the fastest trajectory at an 11.9% CAGR through 2031. Organized retail chains expand shelf footage for packaged snacks and breakfast cereals, while fintech-enabled e-commerce players distribute consumer electronics in SBS clamshell cartons. Infrastructure gaps in fiber recovery hinder recycled-content options, steering converters toward lightweight virgin grades. Kenya’s producer-responsibility rules nudge urban supermarkets to specify recyclable folding cartons, yet informal waste systems delay broad compliance. South Africa retains a mature recycling ecosystem that supplies recovered board across the region, but load-shedding and tepid GDP growth cap upside in volume.

Competitive Landscape

Global majors and regional independents vie for a share in a moderately fragmented arena. Smurfit Westrock’s formation in 2024 bolstered purchasing leverage on pulp and print consumables, pressuring mid-tier converters to seek niche differentiation or strategic investors.[4]Reuters, “Smurfit Kappa, WestRock Complete Merger,” reuters.com International Paper’s plan to carve out its EMEA division in 2026 could trigger regional roll-ups by private equity funds attracted to emerging-market growth.

Mondi earmarked EUR 1.2 billion (USD 1.36 billion) for global expansion, bolstering its position in sustainable kraft bags while maintaining a limited footprint in folding cartons. Nampak exited liquid cartons to focus on metal cans, ceding share in South African board conversions. Emirates Printing Press adds value through inline cold-foil and lenticular finishing that resonates with Dubai’s luxury retail brands.

Strategic white spaces reside in barrier-coated pharmaceutical cartons, halal-certified aseptic dairy packs, and digitally printed micro-runs for influencer-led cosmetic lines. Abu Dhabi’s 2PointZero Group acquired Italy’s ISEM Packaging for AED 704 million (USD 192 million) in 2026, importing luxury carton expertise and AI-driven workflow software to Gulf plants. Wyda Packaging’s buyout of Hulamin Containers in April 2026 quadrupled press capacity and introduced FSC chain-of-custody certification, signaling a pivot from foil trays into paperboard solutions

Middle East And Africa Folding Carton Industry Leaders

International Paper Company

Smurfit Westrock plc

Mondi plc

Graphic Packaging Holding Company

Rengo Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Wyda Packaging acquired Hulamin Containers’ operational assets, boosting press capacity by 340% to 22 presses and mould library by 400% to more than 250, positioning the company as one of sub-Saharan Africa’s largest aluminum-foil container manufacturers with diversification into paper-based packaging solutions and FSC certification.

- March 2026: 2PointZero Group completed a 60.8% acquisition of Italy’s ISEM Packaging for AED 704 million (USD 192 million), adding packaging as its sixth consumer vertical with AI and digital technology deployment plans.

- February 2026: Tetra Pak expanded its paper-based barrier technology to high-speed A3/Speed aseptic lines, reaching 24,000 packs per hour and 87% renewable content for Maeil Dairies.

- February 2026: SIG launched camel milk in 125 ml aseptic cartons under the Sawani brand in Saudi Arabia, demonstrating barrier-coated paperboard viability for culturally significant dairy.

Middle East And Africa Folding Carton Market Report Scope

The Middle East And Africa folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into cartons for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The Middle East And Africa Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries), and Geography (United States, Mexico, Canada). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Turkey | |

| Rest of Middle East | |

| Africa | Egypt |

| South Africa | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Material Type | Solid Bleached Sulfate | |

| Folding Boxboard | ||

| Coated Unbleached Kraft | ||

| White Line Chipboard | ||

| Other Material Types | ||

| By Printing Technology | Lithographic Printing | |

| Flexographic Printing | ||

| Digital Printing | ||

| Gravure Printing | ||

| Other Printing Technologies | ||

| By End-User Industry | Food and Beverage | |

| Healthcare/Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Electrical and Electronics | ||

| Household and Industrial Goods | ||

| Tobacco | ||

| E-commerce and Retail-ready Packaging | ||

| Other End-User Industries | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| South Africa | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the Middle East and Africa folding carton market?

The market stands at USD 3.36 billion in 2026 and is projected to reach USD 4.59 billion by 2031.

Which end-user segment is growing fastest in folding carton across the region?

E-commerce and retail-ready packaging is expanding at a 13.7% CAGR through 2031 as online platforms scale fulfilment networks.

How will single-use plastic bans affect carton demand?

Plastic-reduction policies in Gulf Cooperation Council countries are driving accelerated substitution toward paperboard, underpinning steady volume growth.

What technology trend is reshaping carton production economics?

High-speed digital printing enables short-run, variable-data jobs that cut inventory and support rapid SKU proliferation for consumer brands.

Which material type is expected to gain the most share?

Solid Bleached Sulfate is set to grow at a 9.4% CAGR thanks to premium food, cosmetics, and pharmaceutical adoption of high-barrier, high-brightness boards.

How exposed are converters to pulp price swings?

High reliance on imported virgin fiber and thin hedging capacity means pulp price volatility remains the biggest near-term margin risk for regional converters.

Page last updated on: