Solid Sulphur Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

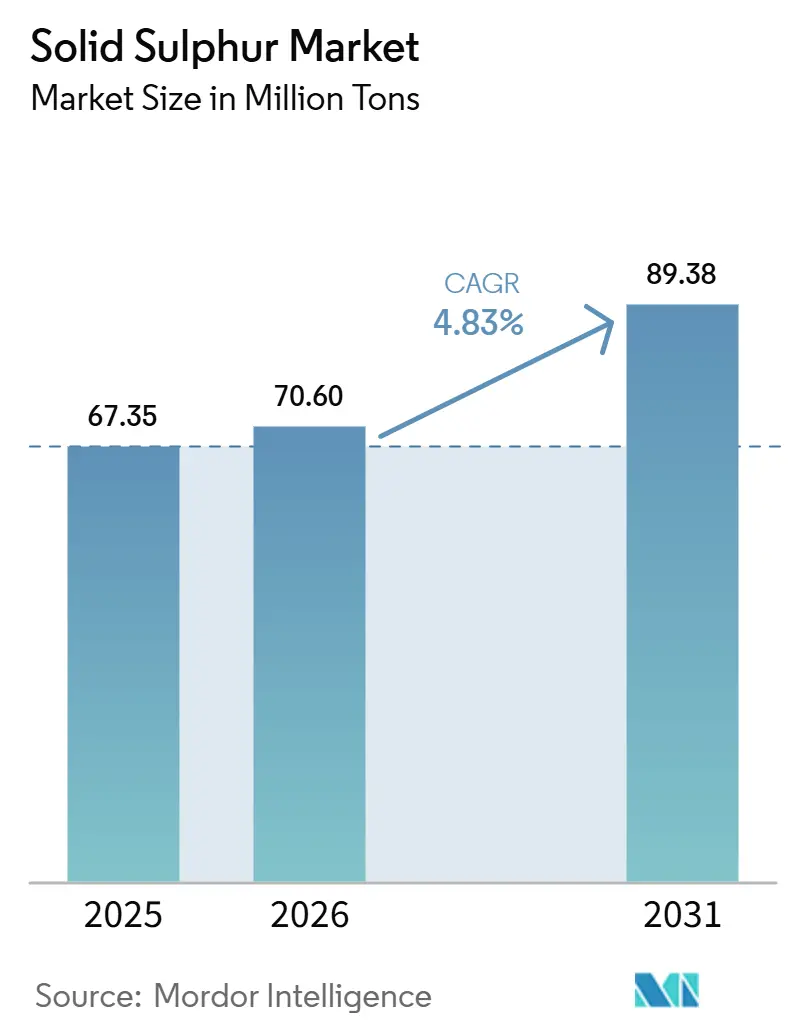

| Market Volume (2026) | 70.60 Million tons |

| Market Volume (2031) | 89.38 Million tons |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

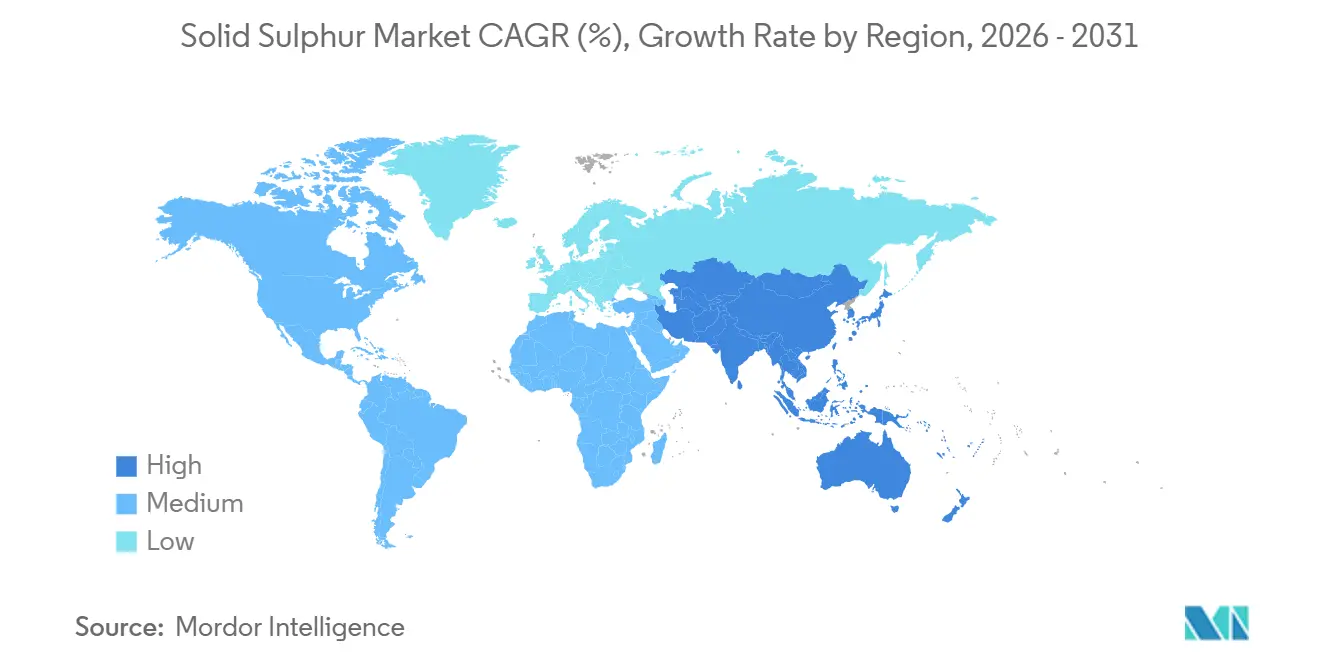

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solid Sulphur Market Analysis by Mordor Intelligence

The Solid Sulphur Market size is projected to expand from 67.35 Million tons in 2025 and 70.60 Million tons in 2026 to 89.38 Million tons by 2031, registering a CAGR of 4.83% between 2026 to 2031. The expansion reflects a structural shift in supply, as by-product sulphur from ultra-low-sulphur fuel regulations now competes with deliberate extraction, introducing price volatility that saw spot values spike to USD 528 per ton in December 2025, nearly triple late-2024 levels. Refinery desulphurization economics and surging demand from Indonesia’s nickel HPAL sector have decoupled sulphur availability from crude-oil recovery volumes, rendering legacy supply models unreliable. Integrated oil majors are investing in handling infrastructure. ADNOC’s Ruwais terminal can now move 27,000 tons per day to safeguard export competitiveness. Fertilizer producers in Brazil and China remain the largest buyers, yet emerging applications such as sulphur-extended asphalt and sulphur-based polymers hint at diversified long-term demand.

Key Report Takeaways

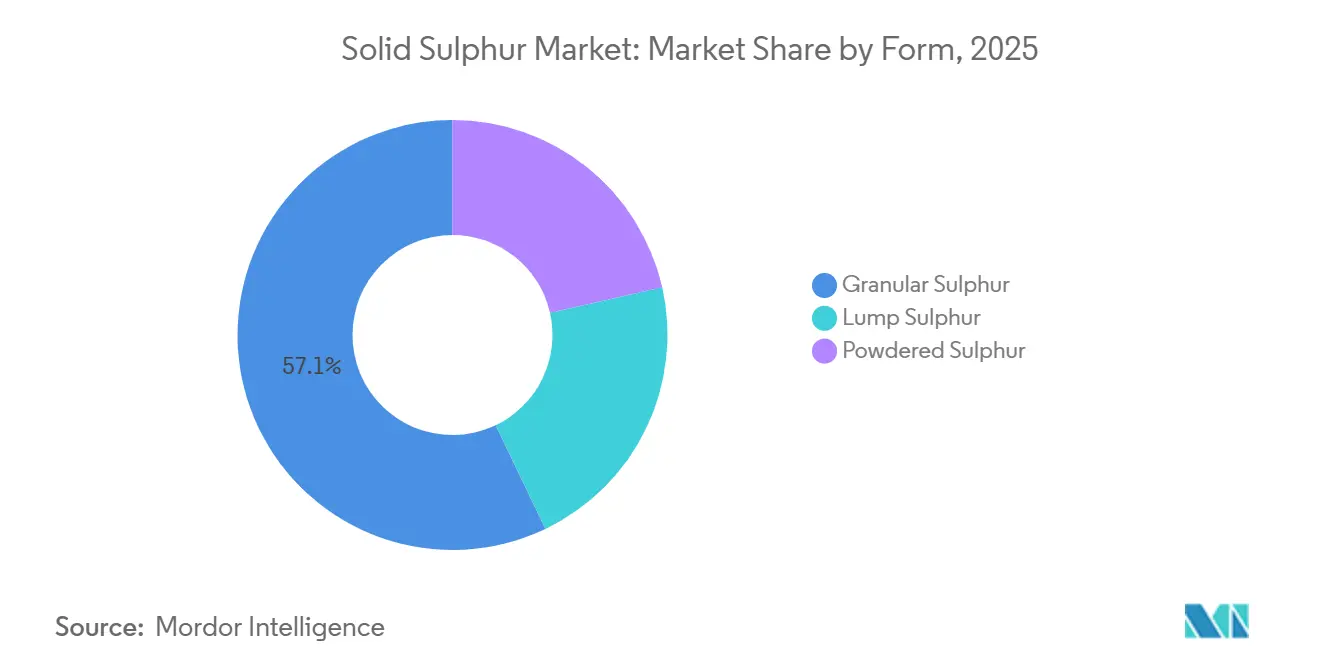

- By form, granular sulphur led with 57.11% of the Solid Sulphur market share in 2025, while powdered sulphur is projected to post the highest 5.25% CAGR during the forecast period (2026-2031).

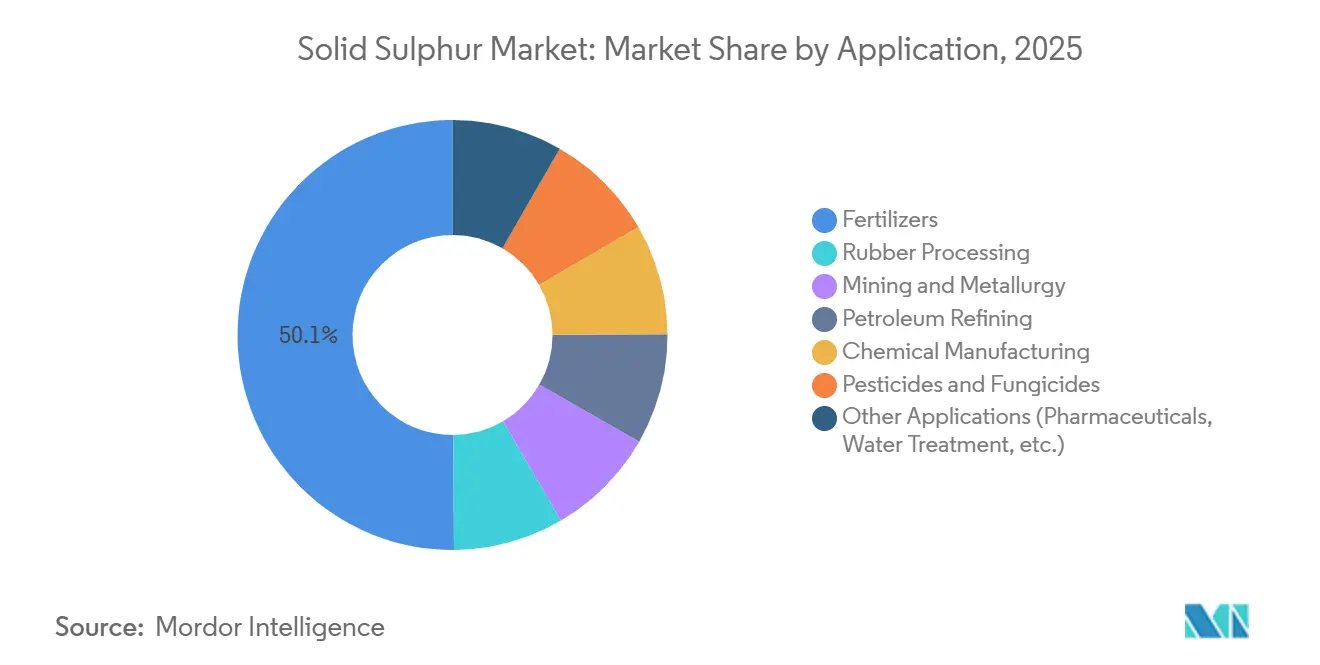

- By application, fertilizers accounted for 50.11% of the Solid Sulphur market size in 2025 and are expected to expand at a 5.51% CAGR from 2026 to 2031.

- By geography, Asia-Pacific captured 41.34% of the Solid Sulphur market share in 2025, and the region is forecast to advance at a 5.42% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solid Sulphur Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in ultra-low-sulphur-fuel regulations | +1.2% | Global refining hubs | Medium term (2-4 years) |

| Expansion of non-ferrous metal smelting capacity | +1.5% | Indonesia, China, Chile, Peru, DRC, Zambia | Medium term (2-4 years) |

| Increasing asphalt modification uses | +0.4% | North America, Europe, Middle East | Long term (≥4 years) |

| Commercialization of lithium-sulphur batteries | +0.3% | Global R&D hubs | Long term (≥4 years) |

| Circular-economy push for sulphur-based polymers | +0.5% | Europe, North America, Asia-Pacific pilots | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growth in Ultra-Low-Sulphur-Fuel Regulations

Tighter marine and on-road diesel limits have compelled refiners to add or upgrade desulphurization units, dramatically lifting solid sulphur output even as they sell cleaner fuels. KIPIC’s Al-Zour refinery produced 732,000 tons of granular sulphur across 2024-2025, saving USD 100 million annually by enabling low-sulphur fuel-oil production[1]Kuwait Integrated Petroleum Industries Company, “Annual Report 2024-2025,” kipic.com. This paradox of lower-sulphur fuels but higher elemental supply periodically depresses prices when fertilizer demand softens. North American majors responded by optimizing Claus units that now capture more than 99% of hydrogen sulphide, turning a former liability into a revenue stream, although capital intensity restricts the practice to integrated players.

Expansion of Non-Ferrous Metal Smelting Capacity

Copper, nickel, and zinc projects continue to increase sulphuric-acid intensity. Indonesia’s battery-grade nickel HPAL plants import roughly 75% of their sulphur feedstock from the Middle East, tightening global balances whenever Persian Gulf logistics slow. Chile’s copper leach operations consumed 8.2 million tons of acid in 2025, up sharply as ore grades declined, while Peru’s Tía María project will lift national acid demand by 800,000 tons per year after 2027. The Central African Copperbelt imports close to 2 million tons of solid sulphur annually for cobalt and oxide copper leaching, leaving regional output exposed to any Strait of Hormuz disruption.

Increasing Asphalt Modification Uses

Elemental sulphur can replace up to 30% of bitumen in road construction, lowering paving temperatures and improving rut resistance. Middle Eastern highway projects and North American resurfacing programs have rolled out sulphur-extended mixes, although adoption is gradual because contractors must invest in modified mixing equipment and monitor hydrogen-sulphide emissions. Academic trials confirm superior durability under thermal cycling, yet widespread commercial use still hinges on standardized specifications and end-user familiarity with sulphur-amended binders.

Commercialization of Lithium-Sulphur Batteries

Lithium-sulphur chemistry targets energy densities above 500 Wh/kg, potentially doubling the range of electric vehicles. Firms such as Lyten aim to start limited automotive deliveries in 2026, and Li-S Energy is collaborating with aerospace partners on lightweight aviation cells. Persistent issues with polysulphide shuttle and cycle life have confined production to pilot scale; sizeable industrial demand will only emerge if electrolyte and separator breakthroughs stabilize long-term performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil and gas recovery volumes | -0.8% | Global producing regions | Short term (≤2 years) |

| Slow ramp-up of blue-hydrogen Claus output | -0.3% | Europe, Middle East, North America | Medium term (2-4 years) |

| Logistics bottlenecks in molten-sulphur transport | -0.5% | Canada oil sands, remote refining sites | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil and Gas Recovery Volumes

Solid sulphur supply mirrors hydrocarbon activity. North American gas drilling retrenched in 2025, curbing output from sweetening plants in the Permian and Marcellus. OPEC+ production cuts also tightened Middle Eastern by-product availability even though desulphurization capacity was idle. With virtually no stand-alone sulphur mines, the market cannot respond quickly when fertilizer or metallurgical buyers suddenly increase orders, embedding chronic supply-demand mismatches.

Slow Ramp-Up of Blue-Hydrogen Claus Output

Blue-hydrogen projects were expected to bolster low-carbon sulphur supply, yet delays in carbon-capture financing and offtake agreements have postponed commercial start-ups in the U.S. Gulf Coast, the Netherlands, and the Middle East. Although SuperClaus retrofits have raised recovery rates at existing plants, incremental tonnage is insufficient to balance rising demand from battery metals and fertilizers, leaving the solid sulphur market tethered to traditional refining cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Granulation Dominates Bulk Handling

Granular grades commanded 57.11% of the solid sulphur market share in 2025 as fertilizer blenders favor their 2-6 mm spheres for dust-free pneumatic conveying. IPCO’s single-pass drum technology now cools and coats liquid sulphur into SUDIC-compliant granules, meeting stricter occupational health limits on hydrogen-sulphide exposure[2]Hydrocarbon Engineering, “IPCO SG20 Drum Technology,” hydrocarbon-engineering.com .

Powdered material, though smaller today, is projected to grow at a 5.25% CAGR through 2031, buoyed by micronized fungicide sprays and inverse-vulcanization feedstocks that require high surface area. Vineyards report better powdery-mildew control when sulphur powders are mixed with organosilicone surfactants, broadening adoption across specialty crops. Lump sulphur retains niche uses where slow dissolution suits alkaline soils, yet its irregular size complicates automated blending, reducing future share.

By Application: Fertilizer Demand Anchors Growth

Fertilizers represented 50.11% of the solid sulphur market size in 2025 and are forecast to log the highest 5.51% CAGR to 2031 as phosphate projects in Brazil and ammonium-sulphate expansion in China accelerate uptake. Brazil imported 2.3 million tons of elemental sulphur in 2025, with Serra do Salitre alone set to consume 330,000 tons annually at full capacity.

Rubber processing is the next-largest outlet, driven by insoluble sulphur gradings that prevent bloom in high-temperature tire curing. Metallurgy depends on sulphuric acid converted from solid feed; Chile’s leach operations now require 6.9 tons of acid per ton of copper, underscoring structural demand. Smaller but rising uses include sulphur dioxide preservatives, wastewater treatment and sulfur-coated urea that lowers nitrogen runoff.

Geography Analysis

Asia-Pacific held 41.34% of solid sulphur market share in 2025 and is projected to grow at 5.42% CAGR through 2031. Indonesia’s HPAL nickel, China’s soil-sulphur depletion, and India’s refinery upgrades underpin regional momentum. Indonesia sources 75% of its sulphur from the Middle East, exposing its balances to Persian Gulf shipping risks. China’s ammonium-sulphate boom lets farmers sidestep nitrogen export quotas, while India’s new desulphurization units will gradually substitute imports with domestic by-product.

North America remains a pivotal supplier. Canada’s oil-sands produced about 3 million tons in 2025, 63% of national output, while Suncor marketed more than 800,000 tons as molten and prilled product. Historical block remelting could add 1.5 million tons by 2030 if prices stay elevated, yet new facilities will not be fully online until 2026. U.S. output hinges on Gulf Coast refinery runs and Permian gas drilling, making supply sensitive to crude and gas price cycles.

Europe faces shrinking domestic production as aging refineries close and crude slates lighten. Germany, France, and Italy import growing volumes from Qatar, Saudi Arabia, and Russia, while policy focus on circular-economy solutions is spurring pilot projects in sulphur-based polymers. South America’s profile is shaped by Chilean copper and Brazilian fertilizers: Chile imported 3.8 million tons of sulphuric acid in 2025 after smelter outages, and Mosaic’s December 2025 shutdown of SSP production in Brazil highlighted pricing risk when spot sulphur tripled year-over-year. The Middle East remains the export hub, with ADNOC’s Ruwais terminal lifting capacity to 27,000 tons per day and KIPIC’s Al-Zour sending a record 52,000-ton shipment in January 2025.

Competitive Landscape

The Solid Sulphur market is moderately fragmented. White-space opportunities revolve around sulphur-based polymers, lithium-sulphur batteries and sulphur-extended asphalt, but commercialization depends on technical breakthroughs and standardization. No pure-play sulphur miners exist at scale, so prospective entrants must integrate either backward into refining or forward into specialty formulations.

Solid Sulphur Industry Leaders

Saudi Aramco

Suncor Energy Inc.

Shell plc

ADNOC

CNPC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: PT Pertamina Petrochemical Trading (Pertachem) successfully executed its first bulk shipment of 5,000 tons of solid sulphur to the Morowali area, Central Sulawesi, Indonesia.

- May 2025: Duqm Refinery installed three IPCO SG20 drum granulation units, each with a design capacity of 800 tonnes per day, which operated at 450 tonnes per day. These units convert liquid sulphur into granules compliant with Sulphur Development Institute Canada (SUDIC) standards for export.

Global Solid Sulphur Market Report Scope

Solid sulphur is a bright yellow, brittle, non-metallic chemical element that exists as a solid at room temperature. It is a crystalline substance, often found in nature around volcanic regions, that forms cyclic octatomic molecules.

The solid sulphur market is segmented by form, application, and geography. By form, the market is segmented into granular sulphur, lump sulphur, and powdered sulphur. By application, the market is segmented into fertilizers, rubber processing, mining and metallurgy, petroleum refining, chemical manufacturing, pesticides and fungicides, and other applications (pharmaceuticals, water treatment, etc.). The report also covers the market size and forecasts for solid sulphur in 17 countries across major regions. The market sizes and forecasts are provided in terms of volume (tons).

| Granular Sulphur |

| Lump Sulphur |

| Powdered Sulphur |

| Fertilizers |

| Rubber Processing |

| Mining and Metallurgy |

| Petroleum Refining |

| Chemical Manufacturing |

| Pesticides and Fungicides |

| Other Applications (Pharmaceuticals, Water Treatment, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Granular Sulphur | |

| Lump Sulphur | ||

| Powdered Sulphur | ||

| By Application | Fertilizers | |

| Rubber Processing | ||

| Mining and Metallurgy | ||

| Petroleum Refining | ||

| Chemical Manufacturing | ||

| Pesticides and Fungicides | ||

| Other Applications (Pharmaceuticals, Water Treatment, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the solid sulphur market in 2026?

The solid sulphur market stands at 70.60 million tons in 2026, on track for 4.83% CAGR growth to 2031.

Which form dominates global demand?

Granular grades led with 57.11% share in 2025 owing to superior bulk-handling properties.

Why is Asia-Pacific the fastest-growing region?

The region’s 5.42% CAGR is fueled by Indonesia’s nickel HPAL imports, China’s fertilizer consumption and India’s refinery build-out.

What caused the 2025 price spike in Brazil?

Spot prices tripled as Middle Eastern supply tightened and Indonesian battery-metal demand surged, prompting Mosaic to idle SSP plants.

Page last updated on: