Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

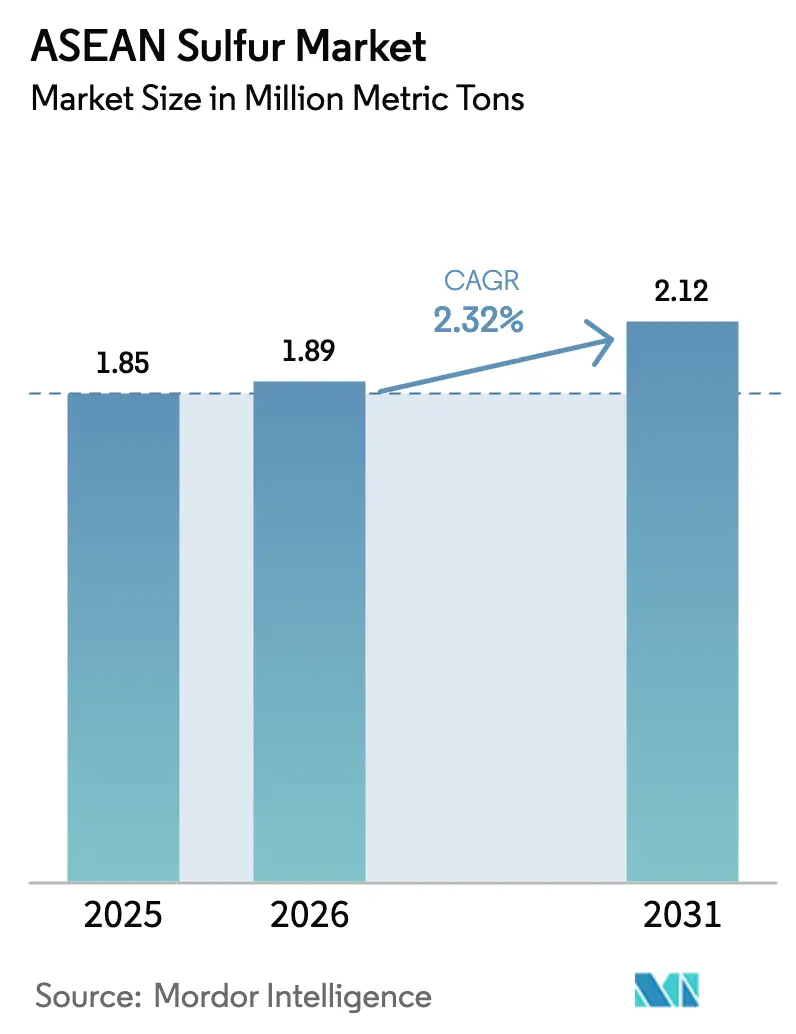

| Base Year Market Size (2025) | 1.85 Million metric tons |

| Market Volume (2026) | 1.89 Million metric tons |

| Market Volume (2031) | 2.12 Million metric tons |

| Growth Rate (2026 - 2031) | 2.32% CAGR |

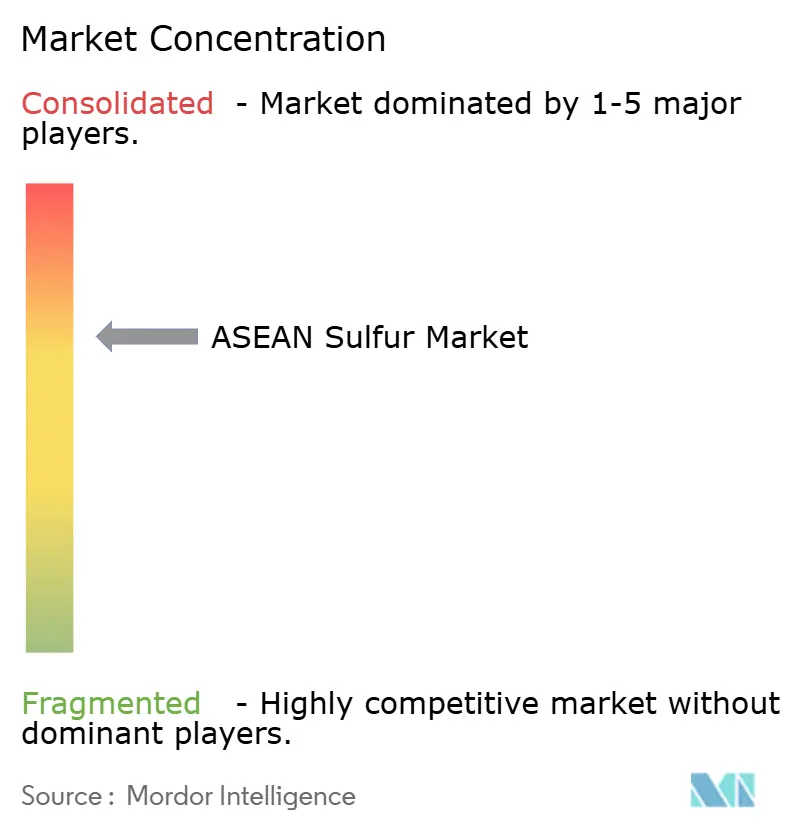

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Sulfur Market Analysis by Mordor Intelligence

The ASEAN Sulfur Market size is expected to grow from 1.85 Million metric tons in 2025 to 1.89 Million metric tons in 2026 and is forecast to reach 2.12 Million metric tons by 2031 at 2.32% CAGR over 2026-2031. Indonesia's increase in nickel high-pressure acid leach projects, constrained Middle-East supply routes, and stricter refinery desulfurization standards are altering trade flows and emphasizing the strategic value of captive acid capacity. While Middle-East exporters continue to lead in seaborne deliveries, vertical integration by Indonesian nickel producers and regional refiners is reducing dependence on imports by strengthening domestic supply. Additionally, Vietnam's phosphate fertilizer expansions and Thailand's stable ammonium-sulfate demand are supporting consistent agricultural consumption. These factors collectively maintain the ASEAN sulfur market in a structural deficit, despite limited overall demand growth.

Key Report Takeaways

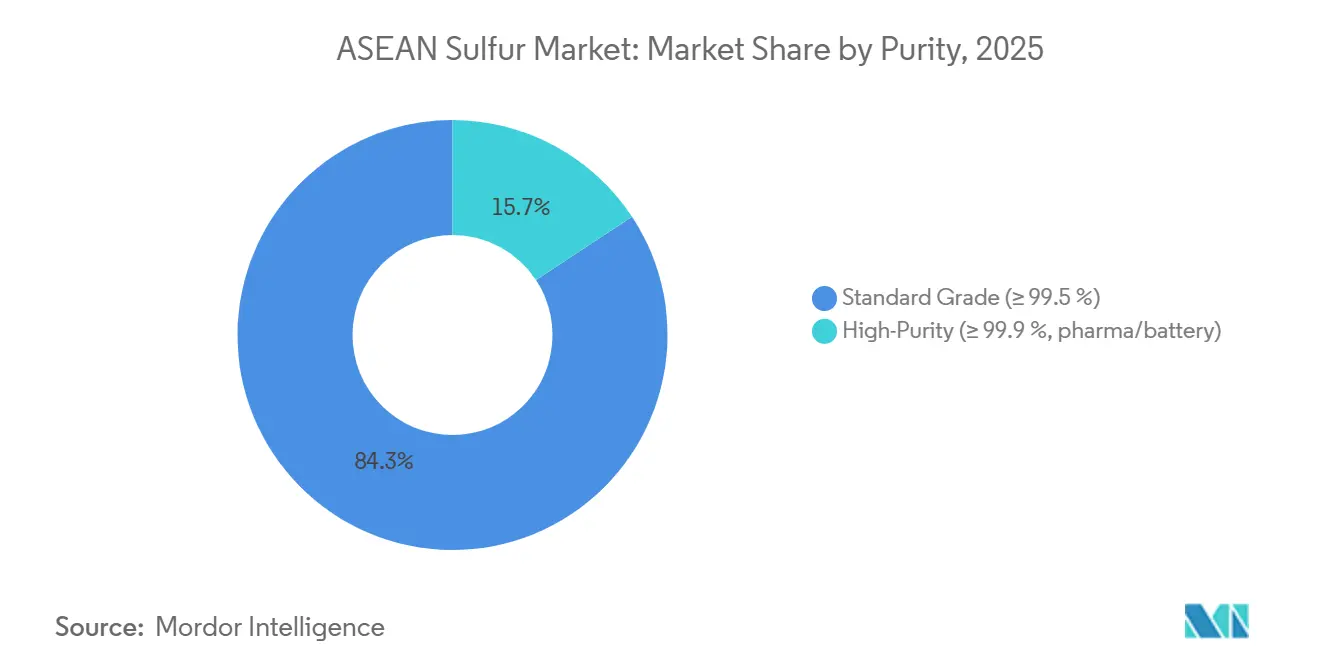

- By purity, standard grade (≥99.5%) led with 84.27% of the ASEAN sulfur market share in 2025, while high-purity sulfur (≥99.9%) is projected to expand at a 3.41% CAGR through 2031.

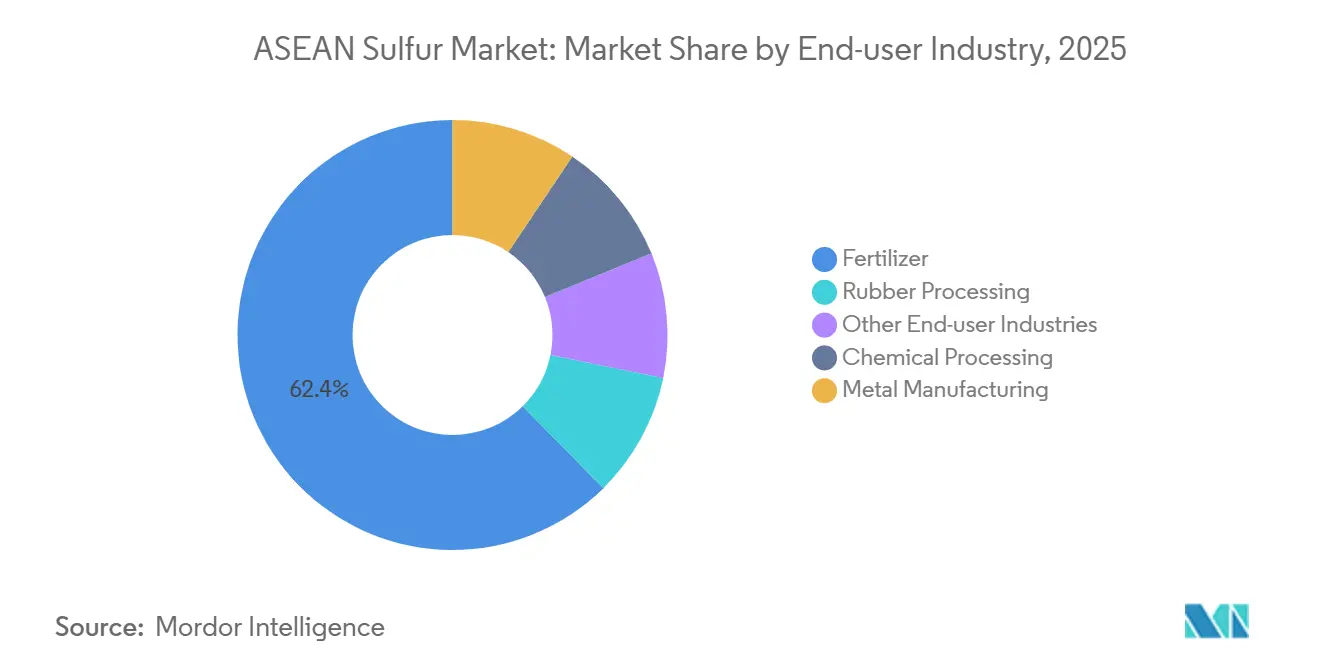

- By end-user industry, fertilizer captured 62.38% of the ASEAN sulfur market share in 2025, whereas chemical processing is projected to expand at a 3.34% CAGR through 2031.

- By geography, Indonesia held 29.46% of the ASEAN sulfur market share in 2025; Vietnam is projected to expand at a 3.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Sulfur Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fertilizer demand rebound across ASEAN rice and oil-seed belts | +0.6% | Vietnam, Thailand, Indonesia (Mekong Delta, Central Plains, Sumatra) | Medium term (2-4 years) |

| Nickel-HPAL projects in Indonesia and Philippines intensifying sulfuric-acid pull | +0.9% | Indonesia (Sulawesi, Maluku), Philippines (Palawan, Surigao) | Short term (≤2 years) |

| Stricter refinery desulfurization standards boosting regional sulfur recovery | +0.3% | Singapore, Thailand, Indonesia, Philippines | Long term (≥4 years) |

| Expansion of phosphate-fertilizer production capacities in Vietnam and Thailand | +0.4% | Vietnam (Lao Cai, Quang Ninh), Thailand (Rayong) | Medium term (2-4 years) |

| Rise of sulfur-based cathode R&D for low-cost grid batteries | +0.2% | Global, with early adoption in China, Japan, South Korea; spillover to ASEAN | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fertilizer Demand Rebound Across ASEAN Rice and Oil-Seed Belts

Southeast Asian growers increased fertilizer usage to 5.5 million tons in 2024, driven by higher crop prices and government subsidies that boosted application rates. The production of one ton of phosphoric acid requires nearly the same weight of sulfur, directly linking increased phosphate output to the ASEAN sulfur market. Ammonium sulfate, which contains 24% sulfur, averaged THB 11,139 per ton in Thailand during 2024 and remained a preferred fertilizer for rice and oil-seed rotations. Vietnam’s fertilizer consumption is growing, with the Mekong Delta’s rice paddies accounting for nearly 40% of national demand. This growth pattern suggests localized sulfur shortages may emerge first in areas with new phosphate production capacity, exacerbating price volatility during disruptions in Middle Eastern logistics. Import dependency remains significant, with 24% of Thailand’s ammonium sulfate sourced from Saudi Arabia in early 2025, leaving the ASEAN sulfur market vulnerable to global freight fluctuations.

Nickel-HPAL Projects in Indonesia and the Philippines Intensifying Sulfuric-Acid Pull

Indonesia increased mixed-hydroxide-precipitate (MHP) capacity to 850,000 tons of nickel in 2025, with each ton requiring approximately 11.8 tons of sulfur for HPAL (high-pressure acid leaching) processes. As a result, sulfuric acid demand surged from 5.17 million tons in 2024 to 7.12 million tons in 2025, marking a 40% increase that significantly impacted the ASEAN sulfur market. Sulfur now accounts for nearly 29% of HPAL operating costs when spot prices exceed USD 530 per ton. Producers have responded by installing on-site burners to convert elemental sulfur, reducing reliance on imported acid. In 2024, Tsingshan added approximately 5 million tons per year of new acid capacity, while QMB commissioned 660,000 tons per year, with an additional 1 million tons per year planned. This vertical integration is shifting trade flows from finished sulfuric acid to elemental sulfur, driving a 48% year-on-year increase in Indonesian sulfur imports to 5.35 million tons in 2025.

Stricter Refinery Desulfurization Standards Boosting Regional Sulfur Recovery

Regulations such as IMO 2020, which capped marine fuel sulfur content at 0.5%, and emission-control area limits of 0.1%[1]Maritime and Port Authority of Singapore, “Port Marine Circular 03/2024,” mpa.gov.sg, have driven stricter desulfurization standards. Thailand adopted Euro 5 fuel standards in 2024, Singapore enforces 10 ppm diesel, and Vietnam targets 50 ppm. Refiners have responded by upgrading hydrodesulfurization and sulfur-recovery units, capturing larger volumes of sulfur as a by-product. Pertamina’s USD 25 billion master plan aims to increase Indonesian refining throughput to 1.68 million barrels per day by 2025 and incorporates wet-sulfuric-acid technology to enhance elemental sulfur output. However, as refinery economics prioritize fuel-quality compliance over sulfur yield, recovered sulfur volumes are expected to grow gradually, leaving the ASEAN sulfur market reliant on imports for the foreseeable future.

Expansion of Phosphate-Fertilizer Capacities in Vietnam and Thailand

Vietnam’s Duc Giang Chemicals has expanded its single-superphosphate production lines, while Thailand is advancing sulfate-of-potash and muriate-of-potash projects. Each Mannheim or acidulation process secures multi-year sulfuric acid supply agreements, tightening spot market liquidity. Taiwan’s Green On increased sulfate-of-potash capacity by 25% for 2026, adding incremental demand that is less price-sensitive compared to commodity NPK fertilizers. These investments ensure stable demand across the ASEAN sulfur market, even during agricultural downturns, as farmers prioritize phosphate and sulfate nutrients for rice and plantation crops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Middle-East supply routes via Strait of Hormuz and Red Sea | -0.5% | Indonesia, Thailand, Vietnam, Malaysia (import-dependent markets) | Short term (≤2 years) |

| Growing adoption of sulfate-free LiFePO₄ battery chemistries | -0.1% | Global, with concentration in China, Japan, South Korea; indirect impact on ASEAN phosphate demand | Long term (≥4 years) |

| Tightening ASEAN port dust-emission limits raising handling costs | -0.2% | Singapore, Malaysia (Port Klang), Thailand (Laem Chabang), Indonesia (Tanjung Priok) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Middle-East Supply Routes Via Strait of Hormuz and Red Sea

The March 2024 closure of the Strait of Hormuz disrupted nearly half of global seaborne sulfur supply and caused freight costs to double due to conflict-related surcharges. By December 2025, Indonesia's CIF sulfur price had surged to USD 547 per ton, representing a 193% increase that significantly compressed HPAL margins. Furthermore, Russia's export ban in November 2025 removed an alternative supply source, while China's price-cap policy redirected domestic sulfur away from exports. With approximately 75% of Indonesian sulfur imports originating from the Gulf, each supply disruption adds price premiums, impacting the ASEAN sulfur market and encouraging further investment in captive-burner projects.

Growing Adoption of Sulfate-Free LiFePO₄ Battery Chemistries

LiFePO₄ battery packs are increasingly being adopted in electric two-wheelers and buses due to their cost and safety advantages. If the production of battery-grade iron phosphate moves away from traditional sulfuric acid-based processes, long-term phosphate consumption could become less reliant on sulfur demand. However, the immediate impact on the ASEAN sulfur market remains limited, as most cathode precursor plants are still based in China. Nevertheless, reduced sulfuric acid export availability from China could decrease the spot tonnage available for ASEAN fertilizer producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Purity: High-Purity Sulfur Gains as Battery R&D Accelerates

Standard Grade sulfur accounted for 84.27% of the projected 2025 volume, maintaining its position as the primary feedstock for fertilizers, base chemicals, and nickel HPAL leach circuits. High-Purity sulfur is anticipated to grow at a CAGR of 3.41% through 2031, driven by increased pharmaceutical production in Singapore and initial battery-material trials in Malaysia. Suppliers utilizing advanced Claus or wet-acid plants can enhance off-gas streams, improving realizations without expanding primary mining capacity.

In 2024, rubber industries in Vietnam and Thailand consumed approximately 250,000 tons of insoluble sulfur for tire vulcanization. Despite a 13% increase in feedstock prices, alternative curing methods like peroxide and radiation remain niche due to performance limitations. The Asia-Pacific region accounts for 55% of global insoluble sulfur consumption, ensuring stable demand even during economic slowdowns. While High-Purity sulfur cannot replace Standard Grade in these applications, increased captive burning in Indonesia may divert Standard Grade sulfur away from rubber processors, potentially tightening regional supply and supporting prices.

By End-user Industry: Metal Manufacturing Drives Fastest Absolute Growth

Fertilizers represented 62.38% of ASEAN sulfur volume in 2025, while chemical processing is projected to grow at a CAGR of 3.34% through 2031, as plants increasingly monetize by-product acid. For instance, Metso’s EUR 180 million equipment contract for a 1.1 million tons per year acid plant, expected to be operational by 2029, highlights this trend.

Vertical integration helps reduce sulfur disposal costs and provides a consistent revenue stream, leading to the inclusion of sulfuric-acid facilities in most new smelters. Fertilizer demand is further supported by efficiency improvements in application. Although rubber processing consumes smaller volumes, it remains highly price-sensitive, prompting users to mitigate exposure through long-term contracts during periods of market volatility in the ASEAN sulfur market.

Geography Analysis

Indonesia accounted for 29.46% of the 2025 sulfur volume, driven by 5.35 million tons of sulfur imports to support its nickel HPAL plants. Approximately 75% of these imports originate from Gulf suppliers, making the ASEAN sulfur market vulnerable to price spikes in the event of disruptions in the Strait. Domestic acid production from Freeport’s Manyar and AMNT copper smelters is expected to add around 3 million tons annually by late 2025. However, this increase will still fall short of projected HPAL growth, ensuring Indonesia remains a net importer.

Vietnam is projected to lead growth with a CAGR of 3.22% through 2031, fueled by phosphate-fertilizer expansion in regions like Lao Cai and Quang Ninh. Duc Giang Chemicals reported revenue of VND 2.8 trillion in 2025 and aims for VND 3.0 trillion in 2026, supported by higher sulfuric-acid utilization. Additionally, Vietnam’s growing electronics sector is driving demand for ultra-pure acid, diversifying end-use applications within the ASEAN sulfur market.

Thailand, Malaysia, and Singapore play critical roles in trade logistics. Thailand sources 24% of its ammonium sulfate imports from Saudi Arabia and 15.5% from China, linking local prices to global benchmarks. Malaysia’s sulfuric-acid consumption is expected to reach 525,000 tons by 2034, driven by palm-oil downstreaming and rubber industries. Singapore enforces stringent port-emission regulations, encouraging investments in enclosed bulk-handling infrastructure, which supports its role as a regional re-export hub in the ASEAN sulfur market.

Competitive Landscape

Middle Eastern exporters, including ADNOC, QatarEnergy, and Saudi Aramco, dominate Indonesian sulfur imports, anchoring regional seaborne trade. QatarEnergy’s long-term offtake agreement with OCP Nutricrops, signed in November 2024, covers up to 7.5 million tons and ensures export growth following the completion of North-Field expansions in 2027[2]QatarEnergy, “QatarEnergy and OCP Long-Term Sulfur Supply Agreement,” qatareenergy.qa. Saudi Aramco’s USD 25 billion Jafurah gas project incorporates significant sulfur-recovery modules, expected to boost global supply by 2028.

Regional players are increasingly integrating upstream operations. Pertamina, in collaboration with Topsoe, is developing a wet-acid unit scheduled for startup in 2029. Meanwhile, Tsingshan’s facilities in Weda Bay and Morowali produce approximately 5 million tons of acid annually. These initiatives reduce the tradable sulfur pool and contribute to price stability at higher levels within the ASEAN sulfur market. Opportunities remain in high-purity refining, where Japanese and Korean producers currently dominate. However, Singapore and Malaysia aim to capture market share by leveraging their pharmaceutical clusters.

Chinese traders continue to influence spot market dynamics despite export restrictions imposed in December 2025. When domestic demand weakens, surplus volumes are redirected to the ASEAN sulfur market, limiting extreme price fluctuations. The market remains fragmented, with no single producer accounting for more than 15% of regional volume, maintaining a balance of bargaining power between buyers and suppliers.

ASEAN Sulfur Industry Leaders

Petroliam Nasional Berhad (PETRONAS)

PT Pertamina (Persero)

Shell plc

Abu Dhabi National Oil Company (ADNOC)

QatarEnergy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Indonesian nickel producers faced production challenges due to disruptions in sulfur supply from the Middle-East, following conflicts in the Gulf region that impacted global shipping routes. The Indonesian nickel producers depended on the Middle-East for approximately 75% of the sulfur required in their production processes.

- March 2026: QatarEnergy halted all sulfur production, which totaled approximately 3.8 million tons per year, following drone strikes on its industrial facilities. The suspension affected the company's entire sulfur output capacity.

ASEAN Sulfur Market Report Scope

Sulfur (S, atomic number 16) is a nonmetallic element characterized by its bright yellow color and brittle solid form. It is essential for life, present in amino acids, and widely used in industrial, agricultural, and medical applications.

The ASEAN Sulfur Market is segmented by purity, end-user industry, and geography. By purity, the market is segmented into standard grade (≥ 99.5%) and high-purity (≥ 99.9%, pharma/battery). By end-user industry, the market is segmented into fertilizer, chemical processing, metal manufacturing, rubber processing, and other end-user industries. The report also covers the market size and forecasts for sulfur in 6 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of volume (metric tons).

By Purity

| Standard Grade (≥ 99.5%) |

| High-Purity (≥ 99.9%, pharma/battery) |

By End-user Industry

| Fertilizer |

| Chemical Processing |

| Metal Manufacturing |

| Rubber Processing |

| Other End-user Industries |

By Geography

| Malaysia |

| Indonesia |

| Thailand |

| Singapore |

| Philippines |

| Vietnam |

| Rest of ASEAN Countries |

| By Purity | Standard Grade (≥ 99.5%) |

| High-Purity (≥ 99.9%, pharma/battery) | |

| By End-user Industry | Fertilizer |

| Chemical Processing | |

| Metal Manufacturing | |

| Rubber Processing | |

| Other End-user Industries | |

| By Geography | Malaysia |

| Indonesia | |

| Thailand | |

| Singapore | |

| Philippines | |

| Vietnam | |

| Rest of ASEAN Countries |

Key Questions Answered in the Report

What is the volume of the ASEAN sulfur market?

The ASEAN sulfur market size stands at 1.89 million metric tons in 2026 and is forecast to reach 2.12 million metric tons by 2031 at a 2.32% CAGR over 2026-2031.

Which country commands the largest share of ASEAN sulfur consumption in 2025?

Indonesia held 29.46% of the 2025 volume due to its nickel HPAL surge.

Which end-user industry is expanding fastest through 2031?

Chemical processing, led by integrated copper and nickel smelters, is set to grow at a 3.34% CAGR through 2031.

How are Middle-East logistics risks influencing ASEAN buyers?

Recurrent Strait of Hormuz disruptions raise freight costs and push buyers toward on-site sulfur-burning capacity for supply security.

Page last updated on: