Metal Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

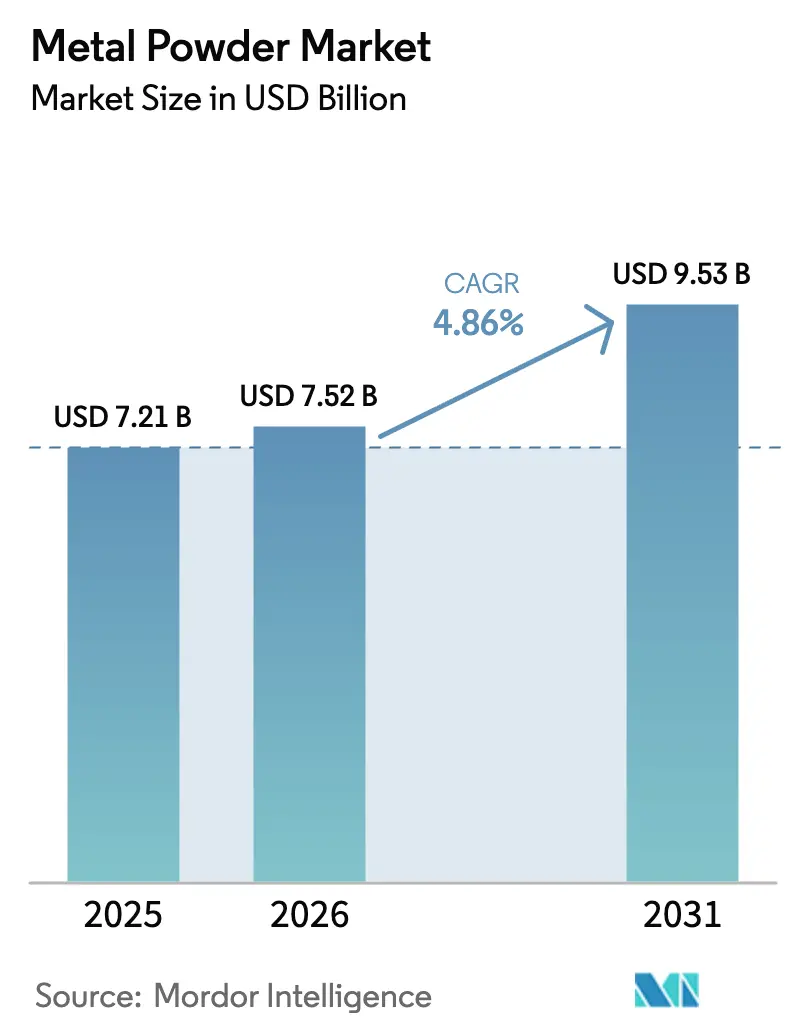

| Market Size (2026) | USD 7.52 Billion |

| Market Size (2031) | USD 9.53 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Powder Market Analysis by Mordor Intelligence

The Metal Powder Market size is projected to expand from USD 7.21 billion in 2025 and USD 7.52 billion in 2026 to USD 9.53 billion by 2031, registering a CAGR of 4.86% between 2026 to 2031. Electrification of vehicles, rapid industrialization of binder-jet additive manufacturing, and hydrogen-based direct-reduced-iron (DRI) projects are reshaping demand patterns across process technologies and alloy types. Atomization continues to dominate high-volume automotive and appliance applications, yet hydrometallurgical routes enjoy faster growth because they deliver energy savings. Titanium and refractory-alloy powders gain traction as medical-implant makers and hypersonic-weapon programs require near-net-shape components with ultra-low oxygen content. Asia-Pacific anchors both volume and growth as China and India scale hydrogen-DRI capacity alongside government incentive schemes, while North America protects domestic aerospace and defense supply chains through production credits and Title III funding.

Key Report Takeaways

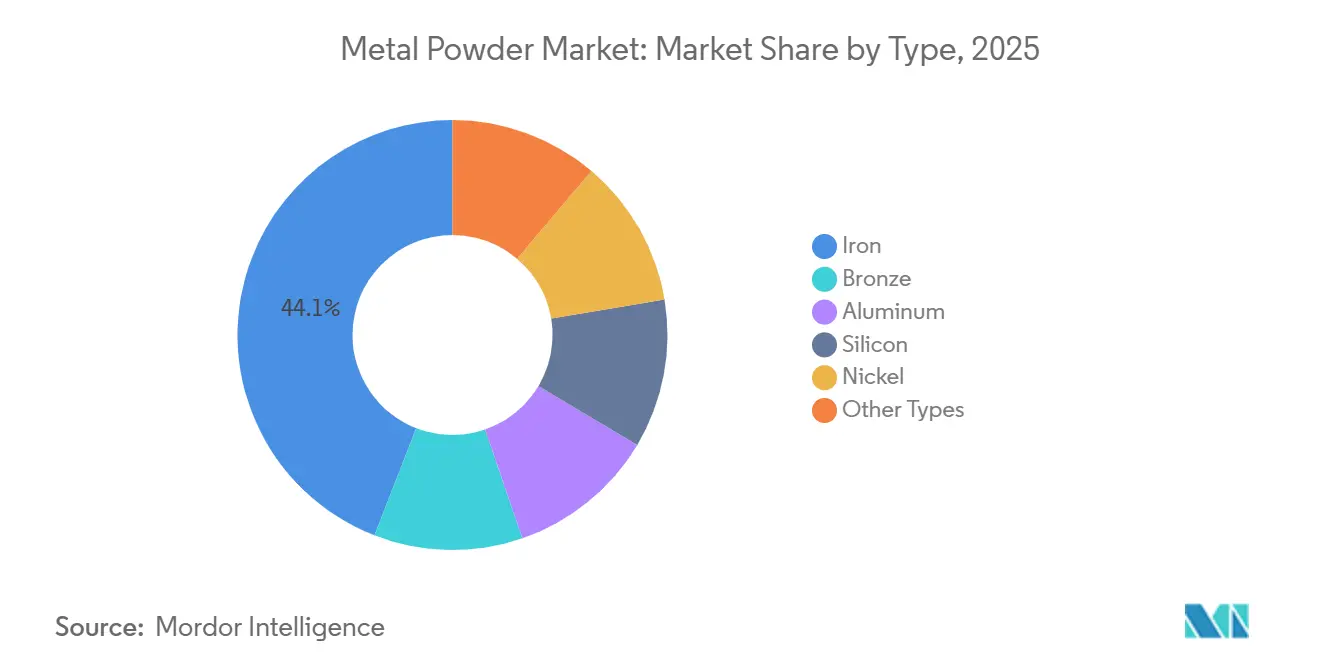

- By type, iron powders captured a 44.08% share in 2025, while "other types" are forecast to expand at a 5.85% CAGR to 2031.

- By process, atomization held 69.79% of the metal powder market share in 2025; other processes are projected to advance at a 5.38% CAGR through 2031.

- By manufacturing method, press-and-sinter commanded 91.18% share in 2025; additive manufacturing is predicted to achieve a 6.10% CAGR through 2031.

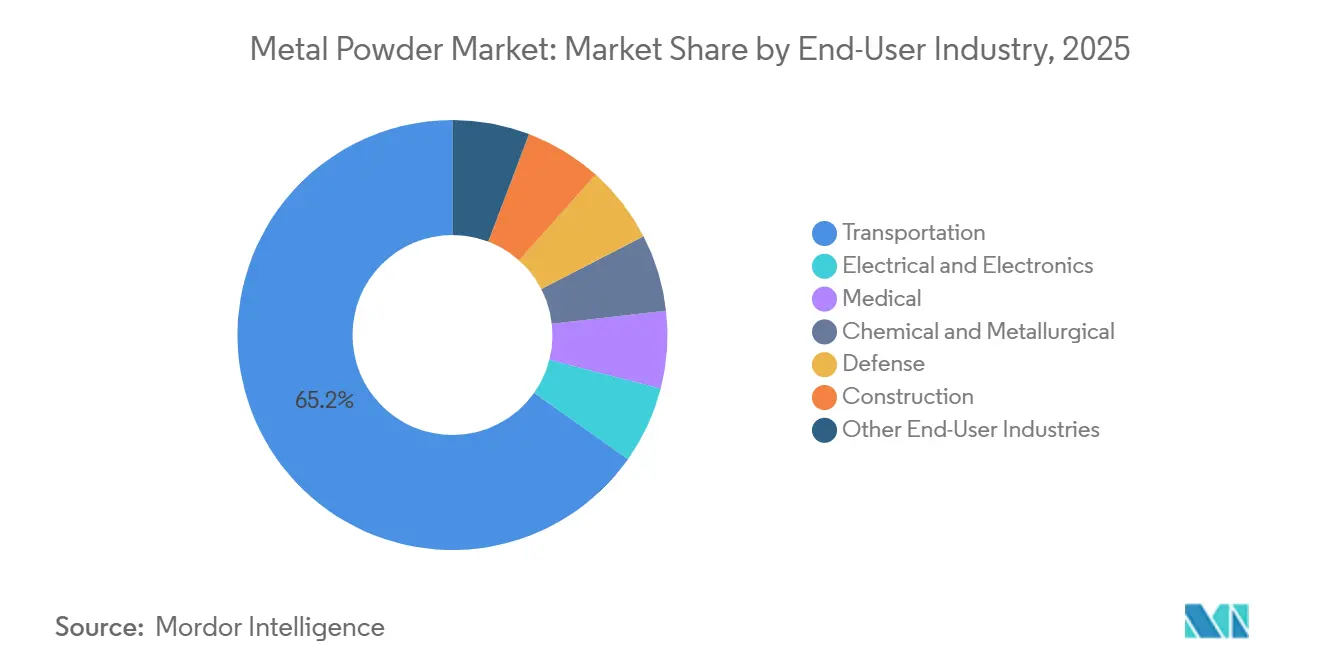

- By end-user industry, transportation led with a 65.21% share in 2025, and medical applications are set to post a 6.26% CAGR to 2031.

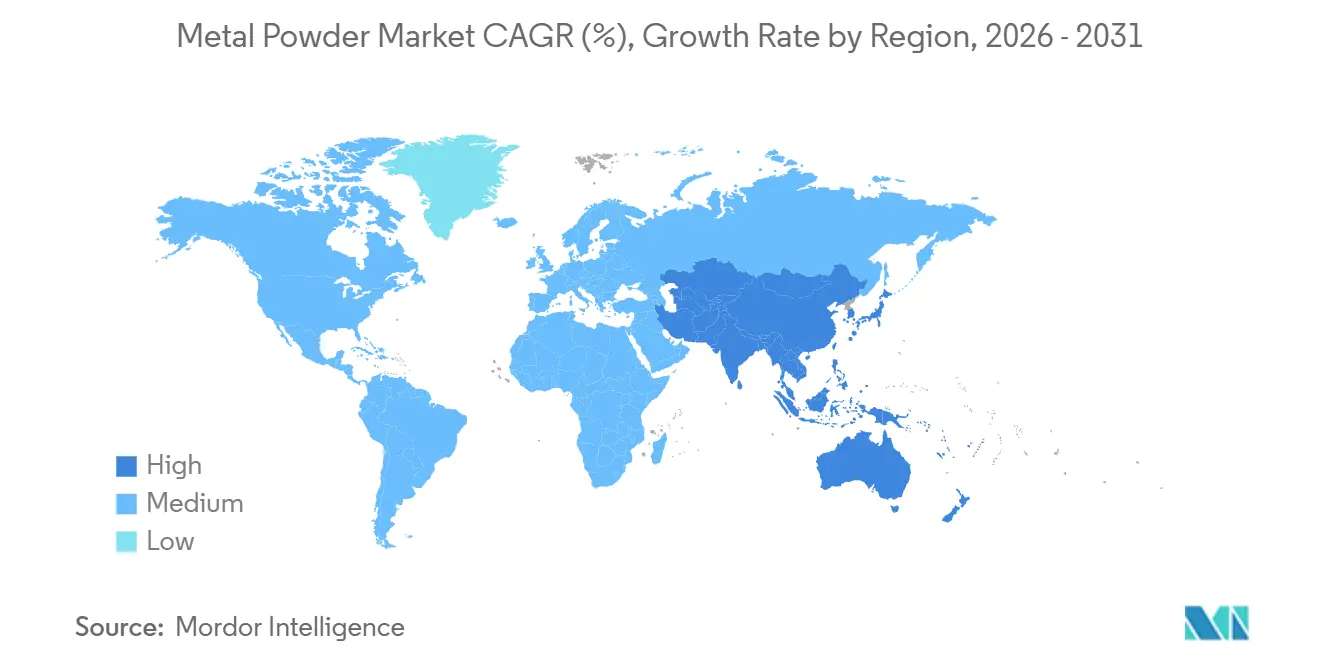

- By geography, Asia-Pacific accounted for a 44.26% share in 2025 and is expected to grow at a 5.48% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metal Powder Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in automotive and aerospace lightweighting programs | +1.2% | Global, with concentration in North America, Europe, and China | Medium term (2-4 years) |

| Rapid industrialization of binder-jet additive manufacturing | +0.9% | North America and Europe core, APAC adoption accelerating | Medium term (2-4 years) |

| Electronics densification driving ultra-fine powder demand | +0.6% | APAC (China, South Korea, Taiwan), spill-over to North America | Short term (≤ 2 years) |

| Rise of hydrogen-based DRI routes creating high-purity Fe powders | +0.8% | China, India, Middle East (Saudi Arabia, UAE) | Long term (≥ 4 years) |

| Defense-grade refractory alloys for hypersonic systems | +0.5% | United States, Europe (France, UK), China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Automotive and Aerospace Lightweighting Programs

Automotive and aerospace manufacturers are increasingly turning to powder metallurgy for components like gears, connecting rods, brackets, and hydraulic manifolds. This shift not only reduces the mass of vehicles and aircraft but also leads to significant cuts in lifecycle emissions and fuel consumption. For instance, General Motors has integrated press-and-sinter gears into its Ultium electric-vehicle platform, achieving a reduction in component mass while retaining fatigue life over 200,000 cycles. Similarly, Airbus has adopted aluminum-silicon powder brackets for its A320neo, resulting in a weight reduction and a significant reduction in lead times. These achievements have paved the way for multi-year powder supply contracts, tightening atomization capacity. Consequently, prices for aerospace-grade aluminum powder are projected to rise in 2025. With regulatory pressures from CAFE and Euro 7 pushing for lightweighting, powder suppliers holding aerospace certifications stand to gain margin premiums, a privilege not extended to commodity iron-powder vendors.

Rapid Industrialization of Binder-Jet Additive Manufacturing

Desktop Metal's P-50 system has propelled binder-jet technology from mere prototyping to full-scale serial production. This advancement allows automotive suppliers to competitively price their offerings, matching the cost-efficiency of metal-injection molding for unit batches. In a significant endorsement, GE Aerospace has approved binder-jet titanium for its RISE engine program, noting a sintered density surpassing wrought materials. While the demand for powder is increasingly leaning towards a highly spherical titanium feedstock, a bottleneck emerges: a scarcity of high-temperature vacuum furnaces is extending lead times to a year. This situation is advantageous for vertically integrated firms that possess both powder and sintering capabilities.

Electronics Densification Driving Ultra-Fine Powder Demand

In 2025, South Korean and Taiwanese capacitor manufacturers secured long-term supply agreements, driving a year-over-year surge in demand for dendritic electrolysis nickel powder. Advanced smartphones and data-center hardware now rely on multilayer ceramic capacitors, enhanced by sub-micron nickel and copper powders for superior dielectric performance. As a result, powder producers with electrorefining capabilities have outshone atomizers, who struggle to economically produce powders under 5 µm, redirecting profit margins towards specialty suppliers in East Asia.

Rise of Hydrogen-Based DRI Routes Creating High-Purity Fe Powders

China Baowu and JSW Steel have launched hydrogen-DRI lines, producing sponge iron with an oxygen content below a specification unachievable through traditional blast furnaces. A portion of this sponge iron is set aside for powder atomization, fetching a premium due to its enhanced sintered density and surface finish from the lower oxygen content. Meanwhile, producers in the Middle East, capitalizing on affordable renewable energy, export their high-purity powder to Europe. There, the CBAM tariffs provide a cost edge to green-iron feedstock[1]European Commission, “Carbon Border Adjustment Mechanism Guidance,” ec.europa.eu .

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Respiratory and explosion hazards in nano-scale production | -0.7% | Global, acute in North America and EU due to enforcement | Short term (≤ 2 years) |

| Quality drift in recycled feedstock streams | -0.6% | North America and Europe (aerospace certification requirements), spill-over to APAC | Medium term (2-4 years) |

| Energy-intensive atomisation impacting sustainability metrics | -0.5% | Europe (carbon pricing), China (dual-control policy), North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Respiratory and Explosion Hazards in Nano-Scale Production

In January 2025, OSHA mandated enclosed handling and live particulate monitoring for powders smaller than 10 µm[2]Occupational Safety and Health Administration, “Combustible Metal Dust Guidance 2025,” osha.gov. This requirement has raised compliance costs significantly for each production line. Meanwhile, European ATEX regulations are pushing smaller producers away from nano-powder lines due to the high costs of retrofitting for explosion-proof electrics and inert-gas blanketing. Following a series of dust explosions in 2024, insurance premiums have increased. This spike has led to a concentration of supply among integrated players, who can spread the burden of safety investments across their broader portfolios.

Energy-Intensive Atomization Undermining Sustainability Metrics

Gas atomization, consuming significant energy per kilogram, clashes with net-zero commitments. Starting in 2026, this energy consumption will lead to CBAM tariffs, increasing import costs in Asia. Both Höganäs and Rio Tinto have pledged substantial investments towards hydrogen-plasma and renewable-electricity retrofits. Their goal is to achieve a carbon footprint of less than 1 kg CO₂ per kg of powder by 2027. Meanwhile, smaller atomizers are feeling the pinch. As automotive and aerospace clients enforce Scope 3 caps, those using high-carbon feedstock face penalties, tightening margins for these smaller players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Iron Dominates Volume, Titanium and Specialty Alloys Lead Growth

Iron accounted for a 44.08% share in 2025, reflecting its role in high-volume gears, bearings, and structural components, but commoditization continues to suppress margins. "Other Types" are forecast to grow 5.85% annually as orthopedic and dental implants, hypersonic systems, and semiconductor thermal-management parts demand ultra-clean powders. Iron suppliers hedge margin risk by capturing vehicular electrification volumes in EV battery trays, while premium-alloy producers secure long-term take-or-pay contracts with medical and defense customers that insulate pricing.

By Process: Atomization Anchors Volume, Hydrometallurgy Targets Purity

Atomization delivered 69.79% of the metal powder market share in 2025 because decades of investment locked in low-cost production for press-and-sinter iron and aluminum powders. "Other Processes" will expand at a 5.38% CAGR through 2031 as fluidized-bed electrolysis and hydrogen reduction slash energy use and accept lower-grade ores, tightening the metal powder market size cost gap versus traditional atomization. Atomization incumbents leverage scale, captive scrap, and tolling deals with automotive tier-ones, yet they invest in plasma and hydrogen-plasma upgrades to defend share. Electrochemical challengers focus on titanium, copper, and nickel powders for electronics and aerospace, where purity and morphology command premiums, avoiding head-on volume battles until cost parity approaches at smaller batch sizes. Competitive intensity, therefore, pivots on energy economics and feedstock flexibility rather than throughput alone.

By Manufacturing Method: Press-and-Sinter Defends Economics, Additive Gains Certification Traction

Press-and-sinter retained 91.18% share in 2025, offering lower part costs at scale compared to binder-jet. This cost advantage solidifies its lead in transmissions and drivetrain components. As approvals accumulate, additive manufacturing will post a 6.10% CAGR through 2031, subsequently boosting the metal powder market for additive-grade feedstock. The economic crossover threshold is set below specific part batch sizes or for geometries that can shave off significant costs post-machining. Consequently, additive vendors are focusing on aerospace brackets, orthopedic implants, and tooling inserts, steering clear of bulk powertrain components. In response, press-and-sinter operators are diversifying with multi-material stacks and warm compaction techniques to fortify their market position.

By End-User Industry: Transportation Anchors Volume, Medical Commands Margin

Transportation absorbed a 65.21% share in 2025, driven by sustained iron-powder demand for gears and structural cast-replacement parts amidst rising EV adoption. Meanwhile, medical devices emerge as the fastest-growing consumer, with a robust annual growth rate fueled by trends in joint replacements and protocols for single-use surgical instruments. Medical devices, however, are the fastest-growing consumer, advancing 6.26% annually on the back of joint-replacement demographics and single-use surgical-instrument protocols. Powder producers boasting ISO 13485 certifications and a history with the FDA enjoy a price premium over standard commodity grades, a gap likely to widen as regulatory scrutiny sharpens.

Geography Analysis

Asia-Pacific held 44.26% of the metal powder market share in 2025 and is projected to post the fastest 5.48% CAGR to 2031. This growth is largely fueled by initiatives in China and India, notably in hydrogen-DRI production and the expansion of electric vehicle platforms. Chinese industry leader Baowu is reaping significant cost advantages over Western counterparts by seamlessly integrating upstream sponge iron with water-atomization. Meanwhile, India's Production-Linked Incentive (PLI) scheme unveiled a significant boost in press-and-sinter capacity in 2025. Both Japan and South Korea have carved a niche, specializing in ultra-fine copper and silver powders tailored for multilayer ceramic capacitors, solidifying their export dominance in the Americas and Europe.

North America accounted for a substantial portion of the 2025 market volume, propelled by robust demand from the aerospace, defense, and electric vehicle sectors. Domestic titanium-powder production lines received a boost from Title III grants, while the Inflation Reduction Act's advanced-manufacturing credit is driving green-powder production, essential for EV motors and wind turbine gearboxes. Leveraging its hydropower advantage, Quebec's cluster is positioning giants like Rio Tinto Metal Powders and Tekna as prime low-carbon suppliers to both the U.S. and Europe.

Europe, holding a significant share of the market in 2025, faced growth constraints due to stagnant light-vehicle output. However, the region found momentum in scope-3 decarbonization incentives, which favor low-CO₂ powders. Companies like Höganäs and Metalysis are racing ahead, fast-tracking hydrogen-plasma and electrolysis technologies, eyeing market leadership as CBAM tariffs push import prices higher. Meanwhile, smaller atomizers in Germany and Italy are honing in on aerospace and luxury tooling powders, strategically safeguarding their profit margins. Though South America and the Middle-East and Africa collectively account for a smaller portion of the market, there's potential for growth, especially with Brazil's automotive ambitions and Saudi Arabia's push towards renewables and hydrogen-DRI strategies.

Competitive Landscape

The metal powder market is moderately fragmented. Competitive intensity, therefore, bifurcates: scale economics continue to dominate commoditized press-and-sinter iron, while certification moats and novel process IP shield margin pools in aerospace, medical, and defense alloys. Over the forecast window, incumbents that fail to secure low-carbon energy or proprietary atomization upgrades risk erosion of both share and EBITDA.

Metal Powder Industry Leaders

Höganäs AB

GKN Powder Metallurgy

Sandvik AB

ATI

Kymera International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Outokumpu entered the metal powder market for additive manufacturing in 2023. As of May 2025, the company is expanding its operations into the aerospace and aviation sectors. It has successfully delivered the industry's first batch of a new stainless steel powder grade designed for a specialized 3D printing application.

- April 2025: Epson Atmix Corporation, a subsidiary of Seiko Epson Corporation, collaborated with Epson Europe Electronics GmbH to establish a sales office in München, Germany. This initiative aims to strengthen and expand Atmix's metal powder business in Europe.

Global Metal Powder Market Report Scope

Metal powder is defined as finely divided metal particles, ranging from micrometers to sub-millimeters, that serve as essential raw materials in powder metallurgy. These powders are primarily produced through atomization, reduction, and electrolysis, with iron being the predominant material, alongside bronze, aluminum, nickel, and titanium. They are processed using techniques such as press-and-sinter, metal injection molding, and additive manufacturing, supporting industries like automotive, aerospace, and electronics.

The Powder Metallurgy market is segmented by type, process, manufacturing method, end-user industry, and geography. By type, the market is segmented into iron, bronze, aluminum, silicon, nickel, and other types (e.g., titanium). By process, the market is segmented into atomization, reduction of compounds, electrolysis, and other processes (e.g., hydrometallurgical routes). By manufacturing method, the market is segmented into press and sinter (conventional PM), metal injection molding, additive manufacturing/3D printing, and other methods (e.g., hot isostatic pressing). By end-user industry, the market is segmented into transportation, electrical and electronics, medical, chemical and metallurgical, defense, construction, and other end-user industries (e.g., additive manufacturing service bureaus). The report also covers the market size and forecasts for the market in 28 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Iron |

| Bronze |

| Aluminum |

| Silicon |

| Nickel |

| Other Types (Titanium, etc.) |

| Atomization |

| Reduction of Compounds |

| Electrolysis |

| Other Processes (Hydrometallurgical Routes, etc.) |

| Press and Sinter (Conventional PM) |

| Metal Injection Molding |

| Additive Manufacturing/3D Printing |

| Other Methods (Hot Isostatic Pressing, etc.) |

| Transportation |

| Electrical and Electronics |

| Medical |

| Chemical and Metallurgical |

| Defense |

| Construction |

| Other End-User Industries (Additive Manufacturing Service Bureaus, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Philippines | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle-East and Africa |

| Type | Iron | |

| Bronze | ||

| Aluminum | ||

| Silicon | ||

| Nickel | ||

| Other Types (Titanium, etc.) | ||

| Process | Atomization | |

| Reduction of Compounds | ||

| Electrolysis | ||

| Other Processes (Hydrometallurgical Routes, etc.) | ||

| Manufacturing Method | Press and Sinter (Conventional PM) | |

| Metal Injection Molding | ||

| Additive Manufacturing/3D Printing | ||

| Other Methods (Hot Isostatic Pressing, etc.) | ||

| End-User Industry | Transportation | |

| Electrical and Electronics | ||

| Medical | ||

| Chemical and Metallurgical | ||

| Defense | ||

| Construction | ||

| Other End-User Industries (Additive Manufacturing Service Bureaus, etc.) | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the metal powder market in 2031?

Global consumption is USD 7.52 billion in 2026 and is projected to reach USD 9.53 billion by 2031, reflecting a 4.86% CAGR.

Which process currently dominates global metal powder output?

Atomization leads with 69.79% share, driven by established gas- and water-atomized lines.

Which end-user segment is expected to grow the fastest through 2031?

Medical devices are projected to record a 6.26% CAGR, outpacing all other industries.

How will CBAM influence European metal powder sourcing?

The tariff raises Asian import costs, encouraging European buyers to shift toward regionally produced low-carbon powder.

Page last updated on: