Insoluble Sulfur Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

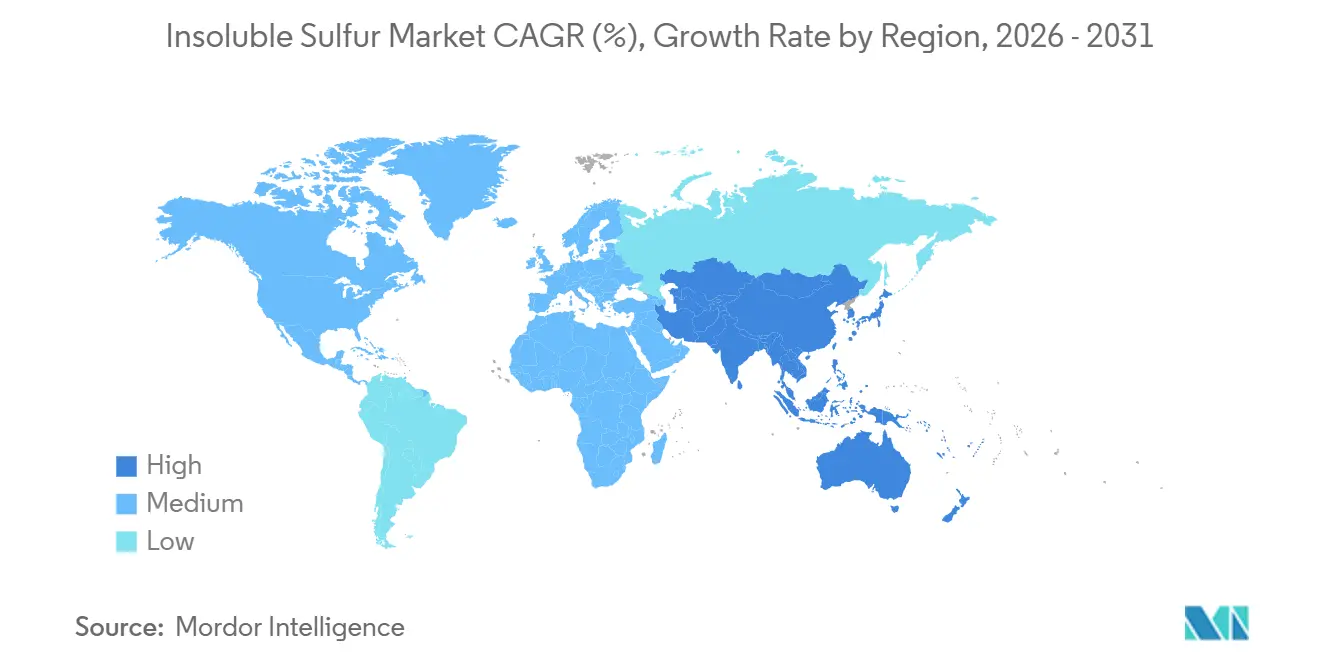

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insoluble Sulfur Market Analysis by Mordor Intelligence

The Insoluble Sulfur Market size is expected to increase from USD 1.16 billion in 2025 to USD 1.21 billion in 2026 and reach USD 1.49 billion by 2031, growing at a CAGR of 4.31% over 2026-2031. Tire radialization, higher electric-vehicle (EV) penetration, and the shift toward premium high-dispersion grades are reinforcing demand resilience despite margin pressure from elemental sulfur cost spikes. Capacity additions in China and the adoption of continuous-process manufacturing are reshaping cost curves, while Western suppliers focus on low-carbon, high-stability formulations to serve EV tires. Distributor-led sales are expanding as mid-tier compounders seek technical support and just-in-time delivery, and industrial rubber goods capitalize on mining and infrastructure spending. Regulatory scrutiny of carbon disulfide (CS₂) exposure and the search for sustainable feedstocks will keep capital requirements high and support long-term price discipline.

Key Report Takeaways

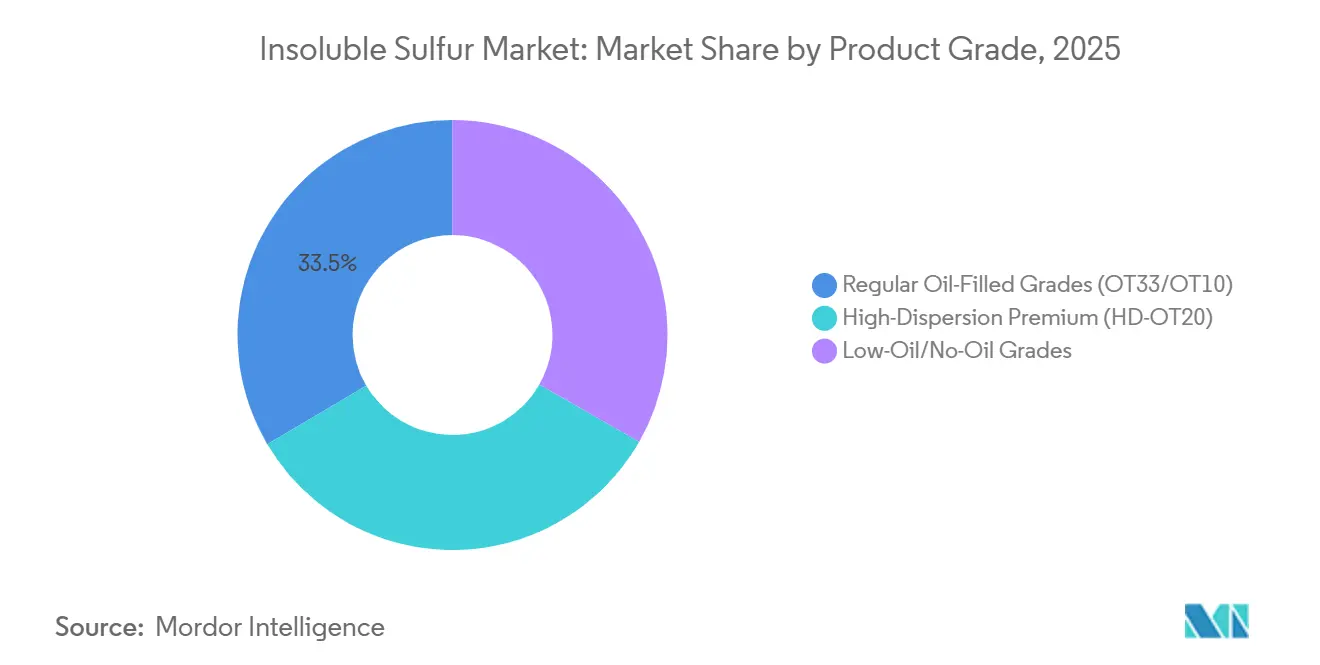

- By product grade, regular oil-filled (OT33/OT10) held 33.47% of the Insoluble Sulfur market share in 2025, while high-dispersion premium (HD-OT20) grades are expected to post the strongest 4.58% CAGR during the forecast period (2026-2031).

- By distribution channel, direct sales controlled 67.71% of the market in 2025, whereas specialty chemical distributors are advancing at 4.72% CAGR during the forecast period (2026-2031).

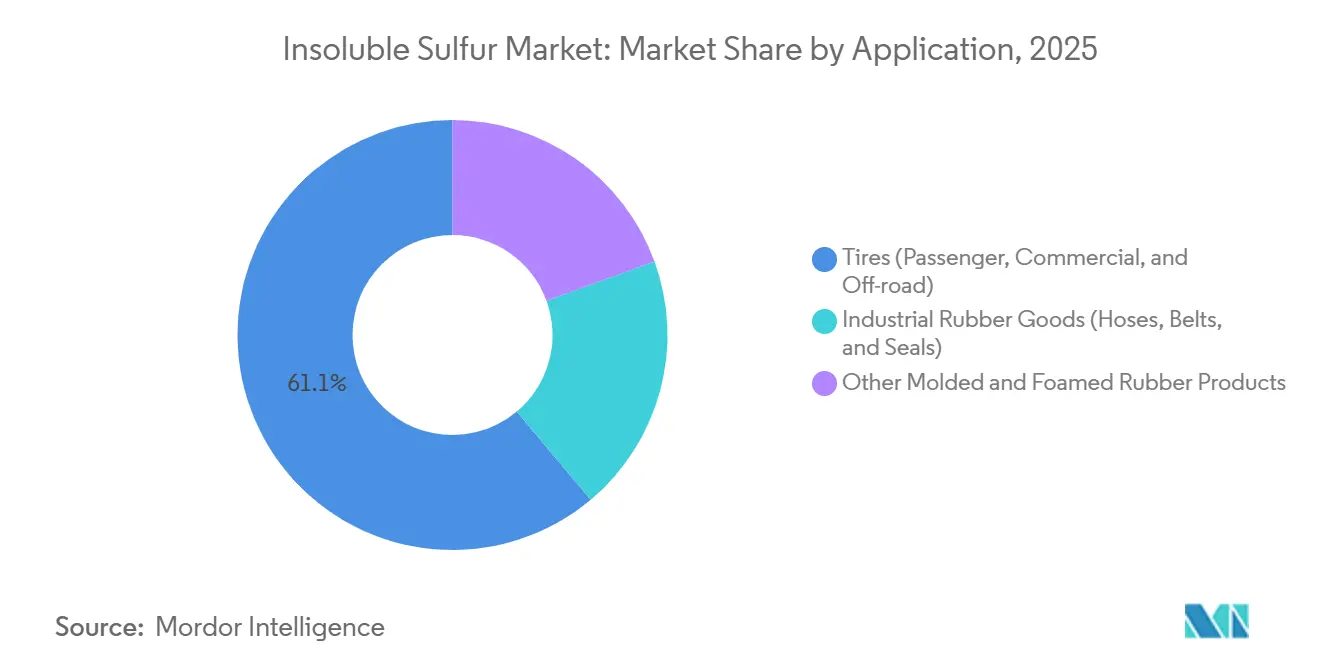

- By application, tires captured 61.11% revenue share in 2025; industrial rubber goods are projected to expand at 4.89% CAGR during the forecast period (2026-2031).

- By geography, Asia-Pacific commanded 56.25% of the market in 2025 and is set to register a 5.14% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Insoluble Sulfur Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global OEM and replacement tire production demand | +1.2% | Global, with concentration in Asia-Pacific (China, India, ASEAN) and spillover to North America | Medium term (2-4 years) |

| Shift to EV-specific low-rolling-resistance compounds | +0.9% | Global, led by China and Europe; early adoption in North America | Medium term (2-4 years) |

| Continuous-process IS manufacturing boosts capacity and consistency | +0.7% | Asia-Pacific (China, Japan); technology transfer to Europe and North America | Long term (≥ 4 years) |

| Rise of green high-dispersion, low-oil IS grades for sustainability | +0.6% | Europe and North America (driven by OEM sustainability mandates); Asia-Pacific following | Long term (≥ 4 years) |

| Industrial rubber goods capacity additions in mining and construction | +0.5% | Asia-Pacific, Middle East & Africa, South America (mining belts in Chile, Brazil, South Africa) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Global OEM and Replacement Tire Production Demand

China produced 1.19 billion tire units in 2024, an increase of 9.2% year on year, while replacement demand remained robust because aging vehicle fleets continue to clock higher mileage[1]China Sunsine Chemical Holdings, “Annual Report 2025,” sunsine.com. Southeast Asia’s dominance in tire exports, led by Thailand’s 40.38% share of US passenger-tire imports, keeps regional offtake solid. Radial tires need about 1.7 times more insoluble sulfur than bias-ply designs, reinforcing the volume pull from tire modernization. Tire makers relocating plants to circumvent tariffs are boosting chemical imports and accelerating international orders. Combined, these structural and cyclical forces underpin a sustained volume floor for the insoluble sulfur market.

Shift to EV-Specific Low-Rolling-Resistance Compounds

EV tires carry heavier loads and must deliver a longer range. They therefore rely on silica-rich, low-rolling-resistance compounds that demand insoluble sulfur to prevent bloom and ensure thermal stability[2]Continental Reifen Deutschland GmbH, “US20210163696A1,” continental-tires.com. Eastman’s Crystex Cure Pro, jointly developed with Double Coin, improves flow and dispersion, enabling shorter mixing times and lower cure temperatures, which saves energy and reduces emissions. Flexsys reports that its Cure Pro Malaysia grade has a 10% lower product carbon footprint than conventional HD-OT20, supporting OEM (original equipment manufacturer) scope-3 targets. Growing EV adoption in China, where new-energy vehicles reached a 41% sales share in 2024, positions premium insoluble sulfur grades for double-digit volume growth through 2031.

Continuous-Process IS Manufacturing Boosts Capacity and Consistency

Continuous production lifts sulfur atom utilization above 95% and recovers 91.78% of CS₂ via cryogenic separation at 12°C and 450 kPa, cutting unit costs by up to RMB 2,000 per tonne. Shandong Yanggu Huatai is the third global player to master the process, joining US and Japanese pioneers. China Sunsine’s Phase 2 line, finished in 2025, raises installed capacity to 60,000 tons per annum, yet utilization lags at 68% as margins remain compressed. Automation reduces labor needs, improves product consistency, and helps plants meet tightening CS₂ exposure limits. The technology’s capital intensity accelerates consolidation and raises barriers for new entrants.

Rise of Green High-Dispersion, Low-Oil Grades for Sustainability

Tire OEMs require life-cycle-assessment data under the European Union Corporate Sustainability Reporting Directive. Flexsys aims to supply fully circular insoluble sulfur by 2030 using bio-based oils and recycled pyrolysis oil, targeting net-zero emissions by 2040. Its German-made HD-OT20 grade has a cradle-to-gate footprint of 1.36 tons CO₂ equivalent per kilogram, 18% below the Malaysian equivalent. High-dispersion grades also cut mixing energy by up to 10% and command 10-15% price premiums. Suppliers investing in ISO 9001:2015 and ISCC PLUS certifications secure OEM approvals more quickly, supporting margin uplift even when commodity prices soften.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile elemental sulfur and CS₂ feedstock pricing | -0.8% | Global, with acute impact in Asia-Pacific (China import-dependent) and Europe | Short term (≤ 2 years) |

| Tightening occupational-exposure limits for dust and CS₂ | -0.4% | Europe, North America; gradual adoption in Asia-Pacific | Medium term (2-4 years) |

| Emerging peroxide/other non-sulfur cure systems in specialty elastomers | -0.3% | North America, Europe (specialty applications); limited tire-segment impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Elemental Sulfur and CS₂ Pricing

China’s FOB sulfur price hit USD 571 per ton in January 2026, quadrupling from January 2024, after Russia extended its export ban and Middle Eastern producers diverted tonnage to Indonesian nickel projects. Sulfur makes up over half of phosphate-fertilizer costs, so fertilizer demand competes directly with chemical feedstock buyers. LANXESS raised additive prices by up to 50% in March 2026 to preserve margins. Producers without long-term sulfur contracts face margin squeeze and working-capital strain.

Tightening Occupational-Exposure Limits for Dust and CS₂

The European Chemicals Agency is reviewing lower workplace limits for CS₂ vapor. Continuous plants, which operate under slight positive pressure and recycle solvent internally, inherently reduce emissions and worker exposure. Retrofitting batch units can cost more than USD 10 million per line, driving smaller firms out of the market. Consolidation will curtail future capacity growth and underpin pricing discipline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: HD-OT20 Commands Premium as Bloom Prevention Drives Adoption

Regular Oil-Filled Grades (OT33/OT10) hold 33.47% of the Insoluble Sulfur market share owing to cost advantages for bias-ply and replacement tires. The insoluble sulfur market size for regular grades remains the largest, yet premium grades capture incremental margin, especially where OEM sustainability mandates push for lower product carbon footprints. High-Dispersion Premium (HD-OT20) grades captured the fastest growth at a 4.58% CAGR, supported by EV tire needs for low bloom and superior thermal stability. Flexsys’s Crystex HD OT 20 specifies more than or equal to 72% insoluble sulfur and maintains stability at 105°C for 15 minutes. Eastman’s Cure Pro variant allows lower mixing speeds and saves up to 10% energy.

Low-oil and no-oil grades are gaining traction in high-silica EV compounds. LANXESS’s Aflux SD, launched in 2025, improves silica dispersion and wet grip. Flexsys’s XD grade posts cradle-to-gate emissions near 1.23 tons CO₂ equivalent per kilogram, reinforcing its positioning in low-carbon tires. Suppliers with continuous-process capability can switch between grades quickly, meeting diverse compounder requirements and optimizing asset utilization.

By Distribution Channel: Specialty Distributors Gain Share Through Technical Support and JIT Inventory

Direct contracts with global top-75 tire makers captured 67.71% of the Insoluble Sulfur market size in 2025. China Sunsine supplies over 75% of these OEMs and bundles accelerators and antioxidants to lock in share. Flexsys runs seven plants on four continents to support local-for-local delivery and slash transport emissions by 2.5 times. Direct supply secures volume but ties up working capital.

Specialty distributors, growing at 4.72% CAGR, aggregate demand from mid-tier compounders and industrial rubber goods manufacturers. Prisma Rubber Additives and R.E. Carroll offer multiple packaging formats and technical data sheets, helping smaller buyers comply with quality audits. Distributors charge a 5-10% markup for flexibility, which remains acceptable as buyers seek reduced inventory risk and faster response times.

By Application: Industrial Rubber Goods Outpace Tire Growth Amid Infrastructure Investment

Tires consumed 61.11% of the Insoluble Sulfur demand in 2025, anchored by China’s 1.19 billion-unit tire output and Thailand’s export leadership. Radial-tire complexity ensures per-unit sulfur use stays high, while EV penetration lifts demand for premium grades with tight bloom control. Replacement purchases account for roughly three-quarters of tire consumption, buffering cyclical swings in OEM output.

Industrial rubber goods are forecast to expand at a 4.89% CAGR, surpassing tire growth. Conveyor belts, hoses, and seals used in mining and construction rely on insoluble sulfur for consistent cure in thick sections. Indonesia’s metals boom and the accompanying sulfur imports support regional belt demand. Suppliers that bundle insoluble sulfur with accelerators secure stickier positions with belt makers, diversifying revenue away from the more volatile automotive sector.

Geography Analysis

Asia-Pacific held 56.25% of the 2025 value and will post a 5.14% CAGR to 2031, driven by China’s tire expansion and EV adoption. China Sunsine raised insoluble sulfur capacity to 60,000 tons per annum, but oversupply kept utilization near 68% in 2024. Shandong Yanggu Huatai’s 40,000 tons per annum addition in 2022 depressed average selling prices by 24% through mid-2024. Thailand’s natural-rubber supremacy and Vietnam’s rising tire plants fortify regional offtake. India is adding capacity to meet domestic auto growth, yet it relies on imports, offering investment headroom for new regional producers.

North America benefits from LANXESS’s Bushy Park expansion, which brought new processing-promoter lines online in November 2025. Local production cuts shipment times and enhances security amid geopolitical tension. Flexsys operates US plants that feed domestic OEMs pursuing lower scope-3 emissions. Mexican tire plants serve US automakers, and Canada remains a key sulfur exporter. Regional EV uptake is slower than in China, moderating demand growth but supporting higher-value, low-carbon grades.

Europe’s market reflects strict environmental norms and decarbonization mandates. LANXESS’s Vulkanox HS Scopeblue, ISCC PLUS-certified since 2024, evidences regional emphasis on bio-based inputs. Flexsys’s German HD-OT20 emits 18% less CO₂ than its Malaysian counterpart, appealing to European Union (EU) OEMs with aggressive CO₂ targets. Russian sulfur export bans and higher energy costs squeeze margins, encouraging process upgrades and local feedstock contracts. South America’s growth clusters in Brazil’s auto and agricultural equipment sectors, while Middle East and Africa depend on mining-related rubber goods, importing most insoluble sulfur from Asia.

Competitive Landscape

The Insoluble Sulfur market is moderately concentrated. China Sunsine, Shandong Yanggu Huatai, Flexsys, Eastman, and LANXESS dominate, leveraging vertical integration, proprietary technology, and direct OEM ties. China Sunsine’s MBT backward integration saves spending and shields earnings from feedstock volatility. Western suppliers hold pricing power for premium grades, while Chinese firms compete on scale.

Insoluble Sulfur Industry Leaders

China Sunsine Chemical Holdings

Eastman Chemical Company

OCCL Limited

SHIKOKU CHEMICALS CORPORATION

LANXESS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: India has imposed anti-dumping duties on insoluble sulphur imports from China and Japan, as well as vitamin-A palmitate from China, the EU, and Switzerland. Based on DGTR recommendations, these duties, effective immediately, will remain for five years to protect domestic industries from unfairly priced imports.

- June 2025: Flexsys has announced a USD0.25/kg price increase for Insoluble Sulfur products in India, effective July 1, 2025, or as per customer contracts. The hike is due to rising raw material costs, changing market conditions, and increased R&D investments in sustainable, high-performance products.

Global Insoluble Sulfur Market Report Scope

Insoluble sulfur is a high-molecular-weight polymeric form of sulfur used primarily as a superior vulcanizing agent in the rubber industry. It is insoluble in carbon disulfide, enabling it to remain dispersed within rubber compounds, prevent blooming, reduce scorch, and improve adhesive properties in tires and technical rubber products.

The Insoluble Sulfur market report is segmented by product grade, distribution channel, application, and geography. By product grade, the market is segmented into high-dispersion premium (HD-OT20), regular oil-filled grades (OT33/OT10), and low-oil/no-oil grades. By distribution channel, the market is segmented into direct to tire/rubber manufacturers and specialty chemical distributors. By application, the market is segmented into tires (Passenger, Commercial, and Off-road), industrial rubber goods (hoses, belts, and seals), and other molded and foamed rubber products. The report also covers the market size and forecasts for insoluble sulfur in 17 countries across major regions. The market forecasts are provided in terms of value (USD).

| High-Dispersion Premium (HD-OT20) |

| Regular Oil-Filled Grades (OT33/OT10) |

| Low-Oil/No-Oil Grades |

| Direct to Tire/Rubber Manufacturers |

| Specialty Chemical Distributors |

| Tires (Passenger, Commercial, Off-road) |

| Industrial Rubber Goods (Hoses, Belts, Seals) |

| Other Molded and Foamed Rubber Products |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Grade | High-Dispersion Premium (HD-OT20) | |

| Regular Oil-Filled Grades (OT33/OT10) | ||

| Low-Oil/No-Oil Grades | ||

| By Distribution Channel | Direct to Tire/Rubber Manufacturers | |

| Specialty Chemical Distributors | ||

| By Application | Tires (Passenger, Commercial, Off-road) | |

| Industrial Rubber Goods (Hoses, Belts, Seals) | ||

| Other Molded and Foamed Rubber Products | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Insoluble Sulfur market?

The Insoluble Sulfur market size is USD 1.21 billion in 2026 and is projected to reach USD 1.49 billion by 2031 at a 4.31% CAGR

Which product grade is growing fastest?

High-dispersion HD-OT20 grades are expanding at 4.58% CAGR because they curb bloom in EV and high-silica tire compounds.

Why are distributors gaining share?

Specialty distributors provide technical support, smaller lot sizes, and just-in-time inventory for mid-tier tire and industrial compounders.

How do elemental sulfur prices affect producers?

Feedstock costs quadrupled between 2024 and 2026, eroding margins for producers without long-term supply contracts.

Page last updated on: