Galvanized Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

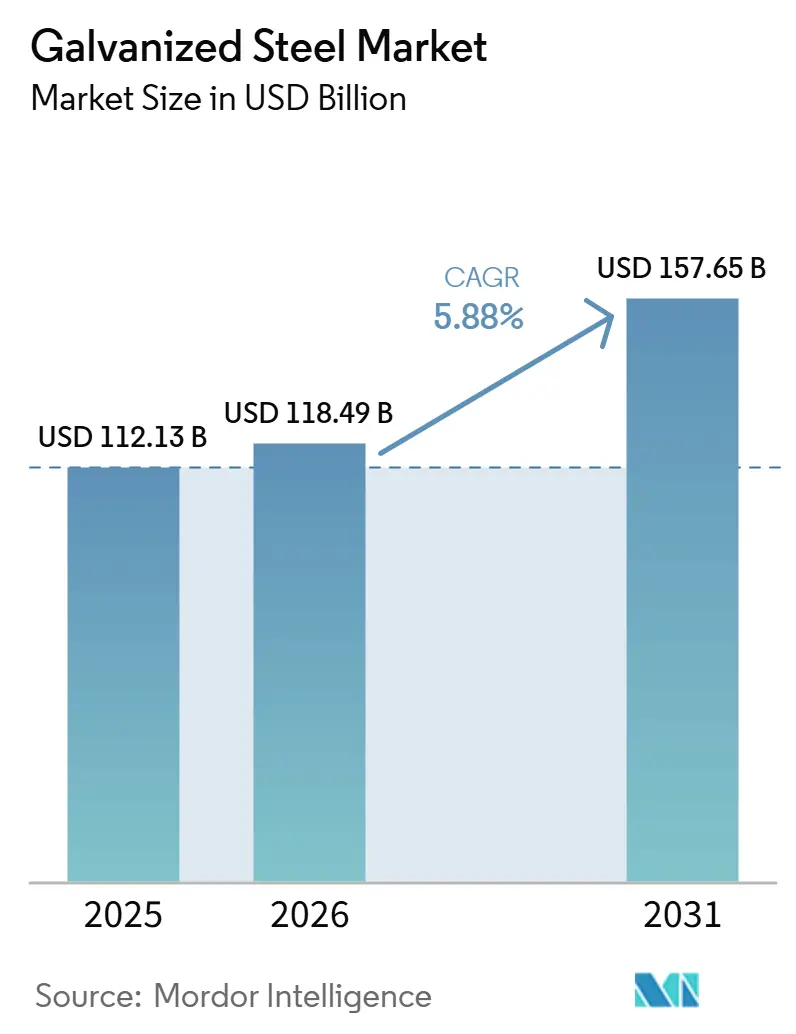

| Market Size (2026) | USD 118.49 Billion |

| Market Size (2031) | USD 157.65 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

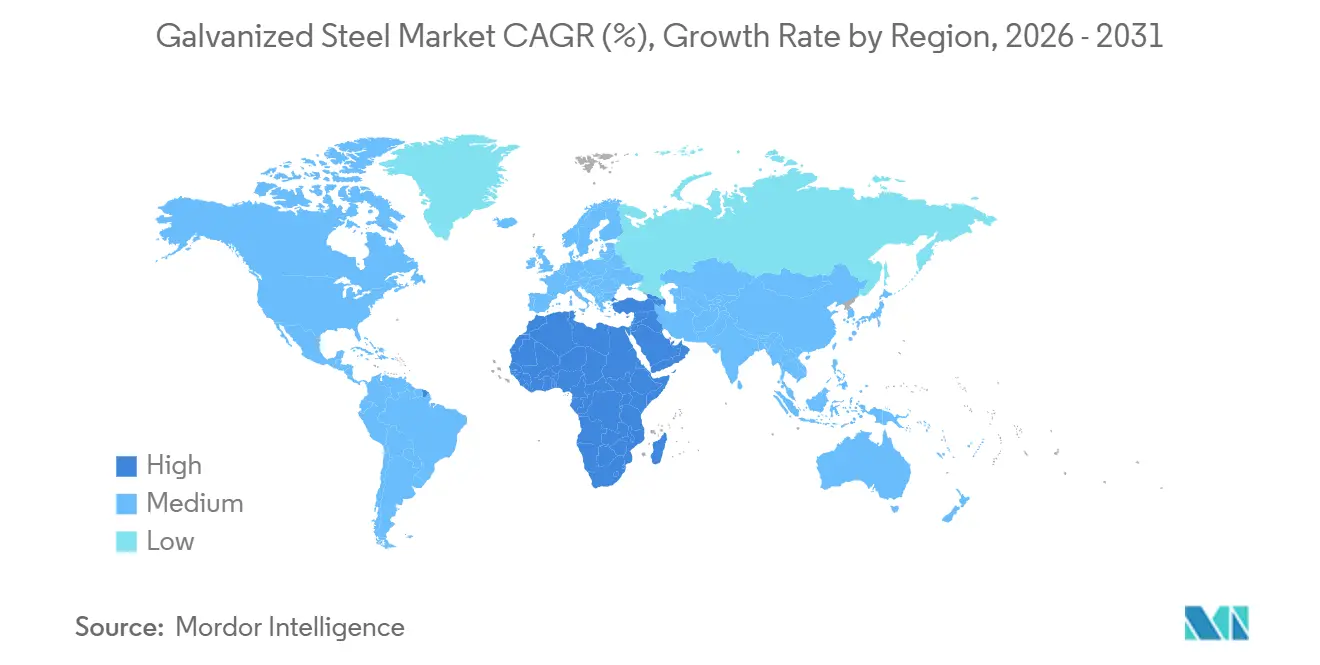

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Galvanized Steel Market Analysis by Mordor Intelligence

The Galvanized Steel Market size is projected to expand from USD 112.13 billion in 2025 and USD 118.49 billion in 2026 to USD 157.65 billion by 2031, registering a CAGR of 5.88% between 2026 to 2031. Rising demand for corrosion-resistant materials in construction, automotive electrification, and renewable-energy structures is driving consistent volume growth despite fluctuations in input costs. Stricter carbon-border regulations in Europe and North America are accelerating the transition to low-emission electric-arc-furnace supply chains. Additionally, artificial intelligence-based quality controls are enhancing coating consistency and minimizing scrap, providing competitive advantages. Alloy-coated products, such as zinc-magnesium-aluminum grades, are gaining traction in premium roofing and solar applications, while hot-dip galvanized substrates continue to dominate mainstream construction. Regionally, Asia-Pacific remains the largest production hub, while the Middle-East and Africa are experiencing the fastest growth due to significant greenfield capacity additions and large-scale project pipelines.

Key Report Takeaways

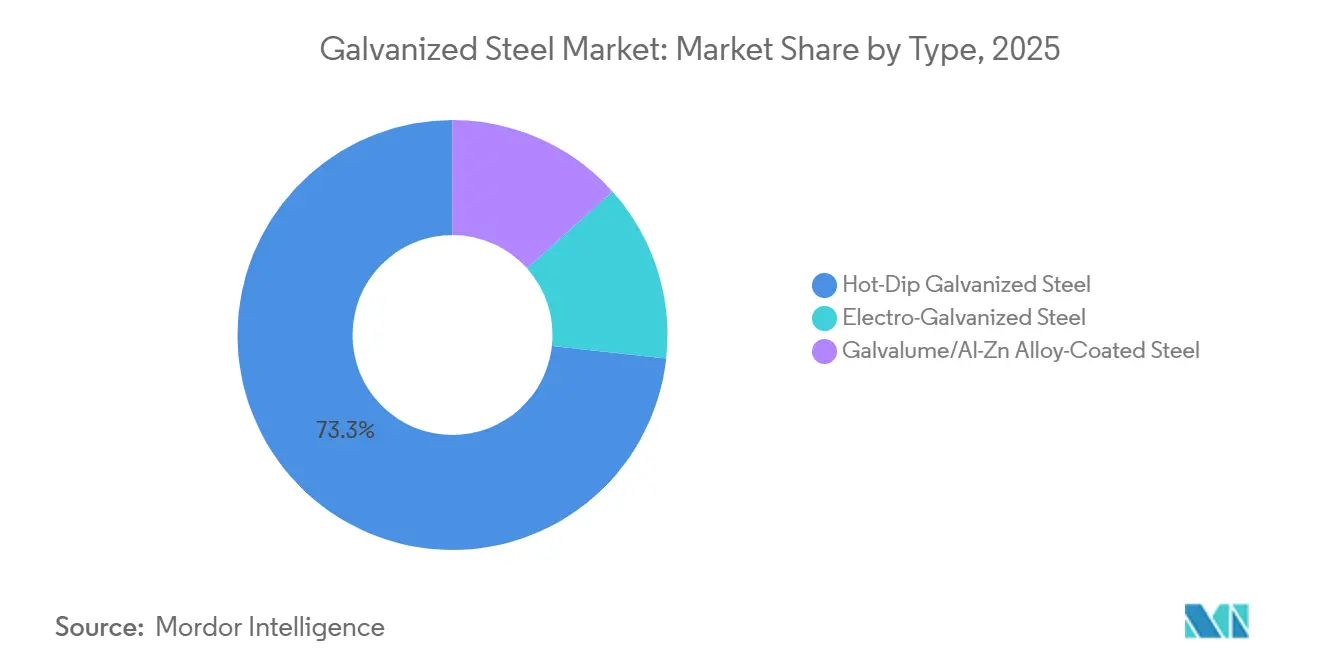

- By type, hot-dip galvanized steel led with 73.26% of the galvanized steel market share in 2025, whereas electro-galvanized steel is projected to record the highest 6.21% CAGR through 2031.

- By form, coils and sheets captured 46.50% of the galvanized steel market share in 2025, while pipes and tubes are forecast to expand at a 6.30% CAGR through 2031.

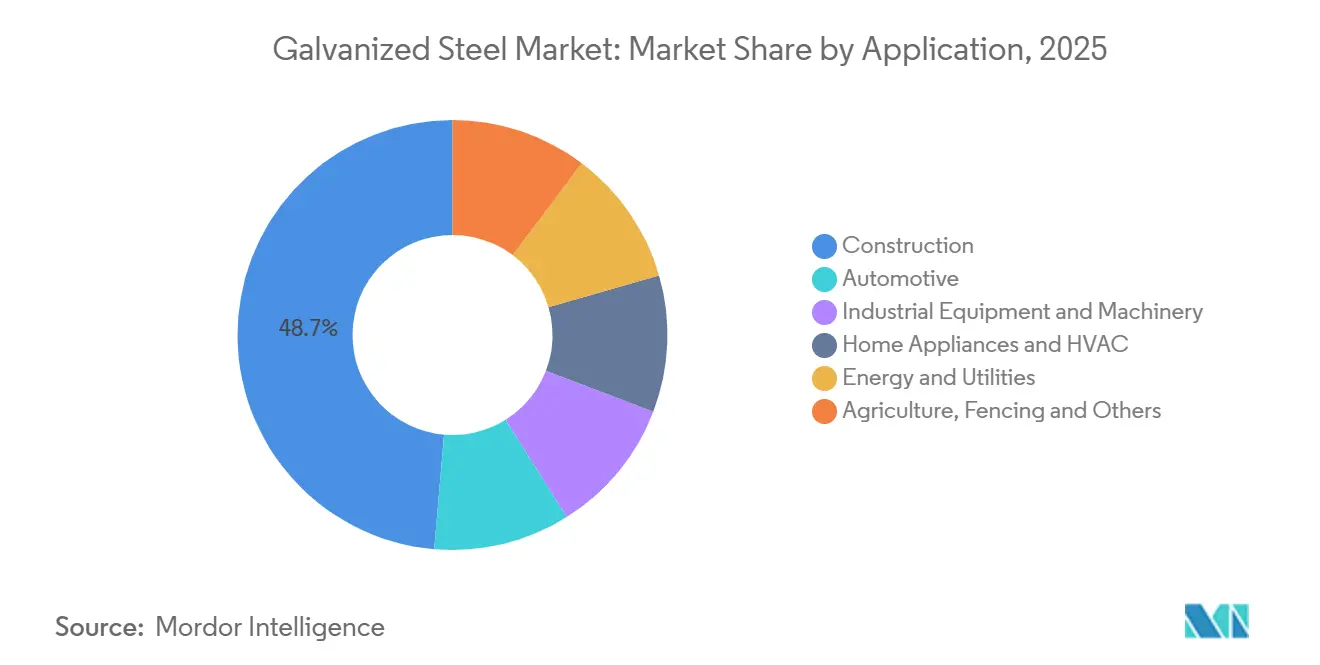

- By application, construction accounted for 48.65% of the galvanized steel market share in 2025, yet energy and utilities is advancing at the fastest 6.12% CAGR through 2031.

- By geography, Asia-Pacific held 55.18% of the galvanized steel market share in 2025, whereas the Middle-East and Africa is projected to grow at 6.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Galvanized Steel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from construction and infrastructure | +1.8% | Global, with peaks in Asia-Pacific and Middle-East and Africa | Medium term (2-4 years) |

| Automotive corrosion-resistance requirements | +1.2% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Renewable-energy structures (solar frames, wind towers) | +0.9% | Global, led by North America, Europe, and China | Long term (≥ 4 years) |

| Uptake of lightweight modules in off-site and modular housing | +0.6% | North America, Europe, urban centers in Asia-Pacific | Medium term (2-4 years) |

| AI-driven predictive-maintenance coating-quality systems | +0.4% | Global, early adoption in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Construction and Infrastructure

Large-scale transport corridors and mixed-use developments under Saudi Arabia’s Vision 2030 and the UAE’s diversification strategies are driving increased demand for coated steel, as evidenced by SeAH GSI’s USD 240 million Saudi plant and EMSTEEL’s AED 625 million UAE expansion. Egypt’s Suez Canal floating bridge utilized over 8,000 tons of hot-dip galvanized sections in 2025, showcasing the material’s suitability for marine environments. India’s highway and metro development programs are boosting domestic demand, while China’s Belt and Road Initiative is exporting coils and sheets to Southeast Asia and Africa. Middle-income economies continue to prefer galvanized beams and roofing for their durability, and government stimulus budgets in 2026 are expected to secure multi-year project pipelines. These factors collectively support sustained growth in the galvanized steel market.

Automotive Corrosion-Resistance Requirements

Twelve-year corrosion warranties, now standard in North America and Europe, mandate zinc coating weights of 60 g/m² or higher on body-in-white components. Innovations like Thyssenkrupp’s selectrify battery housing, which offers a 40% cost and 30% CO₂ reduction compared to aluminum, are gaining popularity in electric vehicle (EV) platforms. Schneider Electric introduced electro-galvanized enclosures for outdoor chargers in 2025, designed for industrial environments. Thailand’s EV production increased by 20% in 2025, driving demand for electro-galvanized sheets in Southeast Asian supply chains. High-strength galvanized grades are also being utilized to offset battery weight without compromising crash safety, reinforcing the market outlook for galvanized steel in the automotive sector.

Renewable-Energy Structures (Solar Frames, Wind Towers)

Hot-dip galvanized poles and lattice towers, with lifespans of up to 25 years, are critical for utility-scale solar and offshore wind farms. These structures align with funding initiatives such as the U.S. Grid Resilience and Innovation Partnerships program. In 2025, Chinese mills allocated 990 kilotons of new capacity, partly for domestic wind-tower and solar-frame applications. Galvalume coatings, which outperform pure zinc by up to five times in salt-spray tests, command a 15% premium in desert and coastal projects. European developers are specifying coatings of ≥ 85 microns for offshore applications, driving demand for thicker galvanizing baths. These trends are expanding the galvanized steel market’s role in the energy transition.

Uptake of Lightweight Modules in Modular Housing

Prefabricated galvanized frames reduce on-site labor by up to 50% while meeting 60-minute fire-rating requirements in dense urban areas. Labor shortages in North America and Europe are increasing the appeal of factory-built units, and tax incentives tied to LEED or BREEAM certifications favor recyclable steel. In China, policies promoting industrialized construction are driving demand for galvanized coils used in wall and floor cassettes, with companies like Shougang Group leading supply. The strength-to-weight ratio of galvanized steel enables multi-story modular construction without requiring deep foundations, making it advantageous for high-cost urban plots. This growing adoption is contributing to incremental growth in the galvanized steel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zinc and steel raw-material price volatility | -0.7% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Alternative metallic coatings (Al-Zn, Zn-Mg-Al) | -0.4% | North America, Europe, premium segments in Asia-Pacific | Medium term (2-4 years) |

| Carbon-border-adjustment tariffs on high-emission mills | -0.5% | Europe, spillover to North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Zinc and Steel Raw-Material Price Volatility

In the first quarter of 2026, zinc prices averaged USD 3,280-3,650 per ton, representing a 12%-18% increase compared to the previous year. This rise reduced galvanizer margins by 200-300 basis points. European hot-rolled coil prices reached EUR 713.57 per ton in March 2026, driven by energy cost inflation and stricter quota regulations. Lead times for tubing extended to 35 days as mills prioritized higher-margin automotive sheets. Smaller galvanizers without hedging capabilities are exiting low-margin segments such as fencing products. While price clauses provide some risk mitigation, volatility continues to challenge the galvanized steel market.

Carbon-Border-Adjustment Tariffs on High-Emission Mills

The EU Carbon Border Adjustment Mechanism, effective January 2026, imposes tariffs of approximately EUR 144 (USD 159) per ton on Chinese slab imports at current ETS prices, reducing their cost advantage[1]European Commission, “Carbon Border Adjustment Mechanism,” europa.eu. Indian and Indonesian coils face even higher tariffs, prompting buyers to shift toward EAF producers. Quota reductions and a 50% over-quota duty are reinforcing reshoring trends, while accreditation delays are forcing many importers to accept default emission values, increasing their liabilities. This policy is accelerating investments in low-carbon furnaces, such as ArcelorMittal’s EUR 1.3 billion Dunkirk EAF. However, compliance costs are adding pressure to certain segments of the galvanized steel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electro-Galvanized Steel Gains Automotive Traction

Electro-galvanized steel grades are anticipated to grow at a 6.21% CAGR through 2031, exceeding the average growth rate of the galvanized steel market. This growth is attributed to automakers' demand for thinner and smoother coatings for exposed panels and battery housings. In 2025, hot-dip galvanized steel captured 73.26% of the galvanized steel market share due to its cost-effectiveness and thicker coatings, which are well-suited for construction applications. The market for electro-galvanized sheets is supported by Schneider Electric’s outdoor charger enclosures and the increasing production of electric vehicles (EVs) in Southeast Asia. Aluminum-zinc alloy coatings are gaining traction in premium applications such as solar and marine roofing, driven by ArcelorMittal’s Optigal product launch. Together, the alloy and electro-galvanized segments are contributing to a more diversified galvanized steel industry.

Electro-galvanized steel is preferred for its weldability and paint adhesion, which drive its demand in appliances requiring DX51D to S220GD grades with 40-100 g/m² zinc coatings. Appliance manufacturers value its balance of formability and corrosion resistance, particularly in humid regions. Hot-dip galvanizing remains the standard for beams and roofing, where 80-120 g/m² coatings provide cost-effective solutions. While Galvalume adoption is increasing in North America and Europe, it remains slower in India and Southeast Asia. Consequently, the galvanized steel market is experiencing simultaneous growth in high-value precision coatings and high-volume traditional coatings.

By Form: Pipes and Tubes Surge on Energy Infrastructure

Pipes and tubes are projected to grow at a 6.30% CAGR through 2031, driven by grid-resilience projects in the U.S. and India, such as Fayetteville PWC’s order for 480 galvanized poles. The market size for galvanized steel pipes is expected to increase as SeAH GSI’s 150,000-tpy Saudi plant supports Vision 2030 pipeline projects. Coils and sheets accounted for 46.50% of the 2025 revenue, serving applications like cladding and appliance casings. Wires and rods cater to agricultural fencing and high-tensile cables, supported by advancements in in-line galvanizing technology.

Lead times for tubing are expected to extend to 35 days by early 2026, indicating supply constraints. Rising zinc costs are compressing margins, pushing smaller producers out of the commodity pole market. Continuous galvanizing lines for sheets, operating at 150-200 m/min, offer cost advantages over batch lines for tubes. Similarly, in-line wire galvanizing reduces handling costs, enhancing competitiveness in rural electrification programs. These factors contribute to dynamic form-factor trends within the galvanized steel market.

By Application: Energy and Utilities Outpaces Construction

The energy and utilities segment is forecasted to grow at the fastest rate of 6.12% CAGR through 2031, supported by U.S. Department of Energy (DOE) funding for galvanized transmission towers and offshore wind projects requiring ≥ 85-micron coatings. Despite this, construction remained the largest segment in 2025, accounting for 48.65% of sales, driven by demand for roofing and beams. Solar racking and wind-tower applications increasingly favor Galvalume for its 25-year durability under salt spray conditions. Grid upgrades tied to electrification goals are expected to further expand the galvanized steel market.

In the automotive sector, demand is rising due to extended corrosion warranties, as seen in Thailand’s 20% EV production increase and Thyssenkrupp’s cost-efficient battery housings. Industrial equipment applications include galvanized conveyor structures and chemical-resistant casings, while appliance manufacturers prefer electro-galvanized steel for refrigerators and HVAC units. Agricultural fencing and mesh provide steady, albeit cyclical, demand in emerging markets. Collectively, these applications sustain broad-based growth in the galvanized steel market.

Geography Analysis

Asia-Pacific accounted for 55.18% of 2025 revenue, driven by China’s 990-kiloton capacity addition and an additional 800 kilotons planned for 2026. Major producers like China Baowu and HBIS supply approximately 70% of global coated coil, benefiting from economies of scale. Shougang’s new Zn-Mg-Al line supports coastal infrastructure projects while utilizing over 50% scrap, aligning with EU emission standards. India’s metro and highway expansions boosted the local galvanized steel market in 2024-2025, while Southeast Asia saw increased consumption due to Vietnam’s 1.5 million-ton demand and Indonesia’s USD 50 billion infrastructure plan. RCEP tariff reductions further enhance intra-regional trade.

The Middle-East and Africa are expected to grow at the fastest rate of 6.19% CAGR through 2031, driven by megaprojects in Saudi Arabia and the UAE. Investments such as SeAH GSI’s USD 240 million pipe mill and EMSTEEL’s 200,000-tpy UAE expansion support localized supply. East Pipes Integrated’s SAR 78.5 million investment in coating lines and Egypt’s canal bridge project highlight marine-grade demand. Despite energy inflation in South Africa, tower and fencing orders provide stability, contributing to the region’s growing market share.

North America is adding over 6 million short tons of new capacity, led by Nucor’s West Virginia lines and California Steel’s 2027 startup. ArcelorMittal’s USD 1.2 billion electrical-steel plant in Alabama and U.S. Steel’s 1 million-ton Big River 2 galvanizing line reflect reshoring efforts supported by Buy America policies. Canada’s EAF proposals in Hamilton aim to reduce CO₂ emissions by 60% within seven years. These developments diversify supply and address carbon-border risks, strengthening the region’s galvanized steel market.

Europe faces EUR 80-85 per-tonne carbon prices and a record 29% import share in late 2025. ArcelorMittal is responding with a EUR 1.3 billion Dunkirk EAF producing low-CO₂ steel by 2029 and a PLN 40 million Optigal upgrade in Kraków. Quota reductions and 50% over-quota duties limit import access, while EUROFER forecasts a 2.4% consumption recovery in 2025. These measures aim to protect local market dynamics.

South America remains a smaller market, led by Brazil, where Gerdau is upgrading lines for appliance sheets. Economic volatility in Argentina limits imports, pushing buyers toward domestic mills. Many producers rely on batch galvanizers to serve construction roofing and farm machinery. Long-term growth depends on economic stabilization and infrastructure investments, but current conditions keep the market fragmented.

Competitive Landscape

The global galvanized steel market shows moderate concentration. Major players include China Baowu, ArcelorMittal, POSCO, Nippon Steel, and Tata Steel. Differentiation increasingly depends on carbon intensity, as seen in ArcelorMittal’s Dunkirk EAF, which targets one-third the CO₂ emissions of traditional blast furnaces. Schneider Electric’s electro-galvanized EV charger cabinets and Thyssenkrupp’s battery enclosures highlight high-margin niches. New entrants like Indonesia’s PT Tata Metal Lestari and Vietnam’s Hoa Sen are leveraging RCEP tariff benefits to expand alloy coating offerings.

Technological advancements are shaping the industry. POSCO’s AI-driven coating-weight control reduces zinc usage by 5%[2]POSCO, “AI Coating-Control Case Study,” posco.com, while SSAB’s predictive maintenance cuts rejects by 18%. The USD 7.7 billion Odisha joint venture between JSW and POSCO secures 6 million-tpy integrated capacity with downstream galvanizing. Vertical integration into captive zinc supplies or hedging strategies helps mitigate the impact of zinc price fluctuations expected in 2026. Certifications such as ISO 14001 and Environmental Product Declarations (EPDs) provide compliant mills with preferential access to automotive contracts, influencing future market dynamics.

Regional players are making significant investments. Nucor’s West Virginia facility will produce 1 million short tons of auto-grade coil by late 2026. U.S. Steel’s Big River 2 and Steel Dynamics’ Heartland expansions add diversified capacity. In ASEAN, POSCO-Krakatau’s USD 3.5 billion complex and Tata Metal’s 250,000-tpy alloy line are targeting growing demand in construction and solar applications. These developments reflect an evolving yet moderately concentrated galvanized steel industry.

Galvanized Steel Industry Leaders

ArcelorMittal

NIPPON STEEL CORPORATION

Tata Steel

POSCO

China Baowu Steel Group Corp., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Tata Steel inaugurated a new Continuous Galvanising Line (CGL-1) at its Kalinganagar plant in Odisha. The facility, designed to produce Advanced High Strength Steel (AHSS) for the automotive and appliance industries, was part of the Phase II expansion, which increased Kalinganagar's total capacity from 3 MTPA to 8 MTPA.

- July 2025: Jindal Steel & Power commissioned its first Continuous Galvanizing Line (CGL 1) at the Angul Integrated Steel Complex in Odisha. This development enhanced the company's capacity to produce value-added galvanized and galvalume products for the automotive, infrastructure, appliances, and construction industries.

Global Galvanized Steel Market Report Scope

Galvanized steel is carbon steel coated with a protective zinc layer to prevent rust and corrosion. The galvanization process forms a metallurgical bond between the zinc and steel, creating a durable barrier that can last for 50 to 100 years in moderate environments.

The Galvanized Steel market is segmented into type, form, application, and geography. By type, the market is segmented into hot-dip galvanized steel, electro-galvanized steel, and galvalume/Al-Zn alloy-coated steel. By form, the market is segmented into coils and sheets, pipes and tubes, and wires and rods. By application, the market is segmented into construction, automotive, industrial equipment and machinery, home appliances and HVAC, energy and utilities, and agriculture, fencing, and others. The report also covers the market size and forecasts for galvanized steel in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Hot-Dip Galvanized Steel |

| Electro-Galvanized Steel |

| Galvalume/Al-Zn Alloy-Coated Steel |

| Coils and Sheets |

| Pipes and Tubes |

| Wires and Rods |

| Construction |

| Automotive |

| Industrial Equipment and Machinery |

| Home Appliances and HVAC |

| Energy and Utilities |

| Agriculture, Fencing and Others |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Hot-Dip Galvanized Steel | |

| Electro-Galvanized Steel | ||

| Galvalume/Al-Zn Alloy-Coated Steel | ||

| By Form | Coils and Sheets | |

| Pipes and Tubes | ||

| Wires and Rods | ||

| By Application | Construction | |

| Automotive | ||

| Industrial Equipment and Machinery | ||

| Home Appliances and HVAC | ||

| Energy and Utilities | ||

| Agriculture, Fencing and Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the galvanized steel market?

The galvanized steel market stands at USD 118.49 billion in 2026 and is forecast to reach USD 157.65 billion by 2031.

Which type is expanding fastest through 2031?

Electro-galvanized steel leads with a 6.21% CAGR through 2031 thanks to rising automotive and appliance demand.

Why are pipes and tubes growing through 2031?

Grid-resilience and water-infrastructure projects are driving a 6.30% CAGR through 2031 for galvanized pipes and tubes.

What region shows the highest growth through 2031?

The Middle-East and Africa is projected to grow at a 6.19% CAGR through 2031 on the back of megaproject spending.

Page last updated on: