Software Supply Chain Security Platforms Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

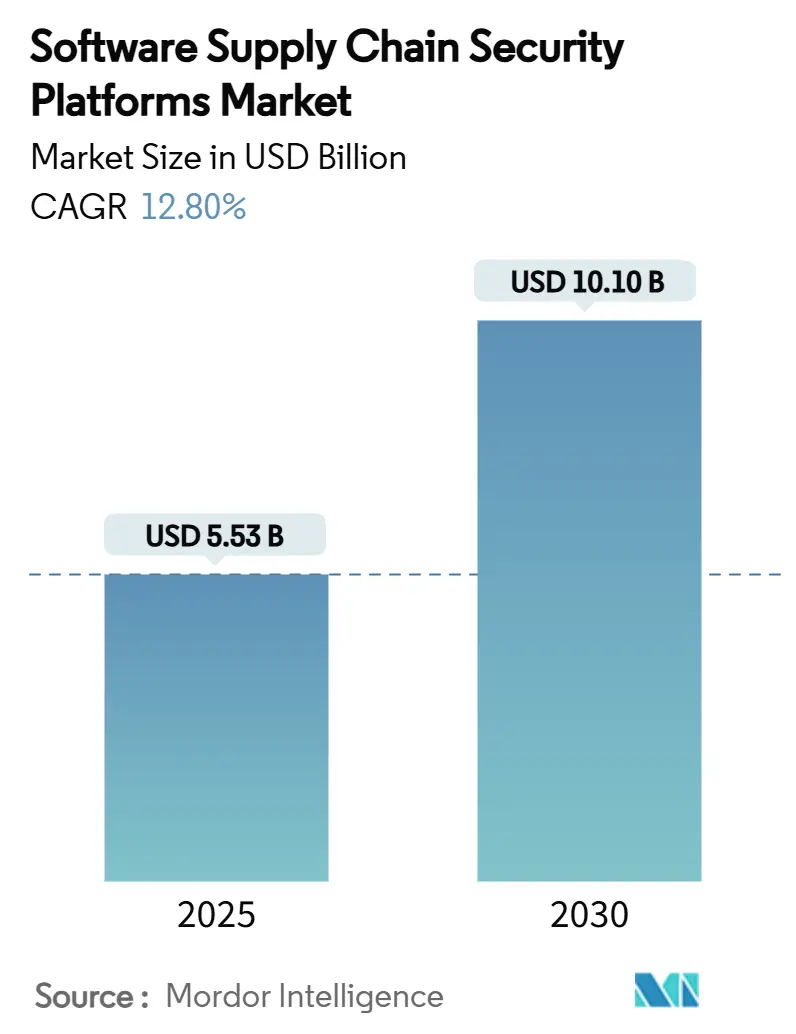

| Market Size (2025) | USD 5.53 Billion |

| Market Size (2030) | USD 10.10 Billion |

| Growth Rate (2025 - 2030) | 12.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software Supply Chain Security Platforms Market Analysis by Mordor Intelligence

The Software Supply Chain Security Platforms market size stands at USD 5.53 billion in 2025 and is forecast to reach USD 10.10 billion by 2030, reflecting a robust 12.8% CAGR over the period. This growth trajectory mirrors the urgency created by a 742% surge in software supply-chain attacks since 2020. [1]“Red Hat Introduces Red Hat Trusted Software Supply Chain,” Red Hat, redhat.com Regulatory mandates that compel the disclosure of a machine-readable Software Bill of Materials (SBOM) across U.S. federal procurements, coupled with the fact that open-source components now account for 75% of modern application code, are amplifying visibility and compliance pressures. Cloud-based, AI-enabled platforms that integrate seamlessly with DevSecOps pipelines increasingly dominate purchasing criteria, while cross-border regulations such as the EU Cyber Resilience Act extend adoption momentum beyond North America. Intensifying competition among established vendors and venture-backed challengers accelerates feature innovation, especially around automated vulnerability triage and binary provenance verification, thereby expanding the Software Supply Chain Security Platforms market opportunity across all customer segments.

Key Report Takeaways

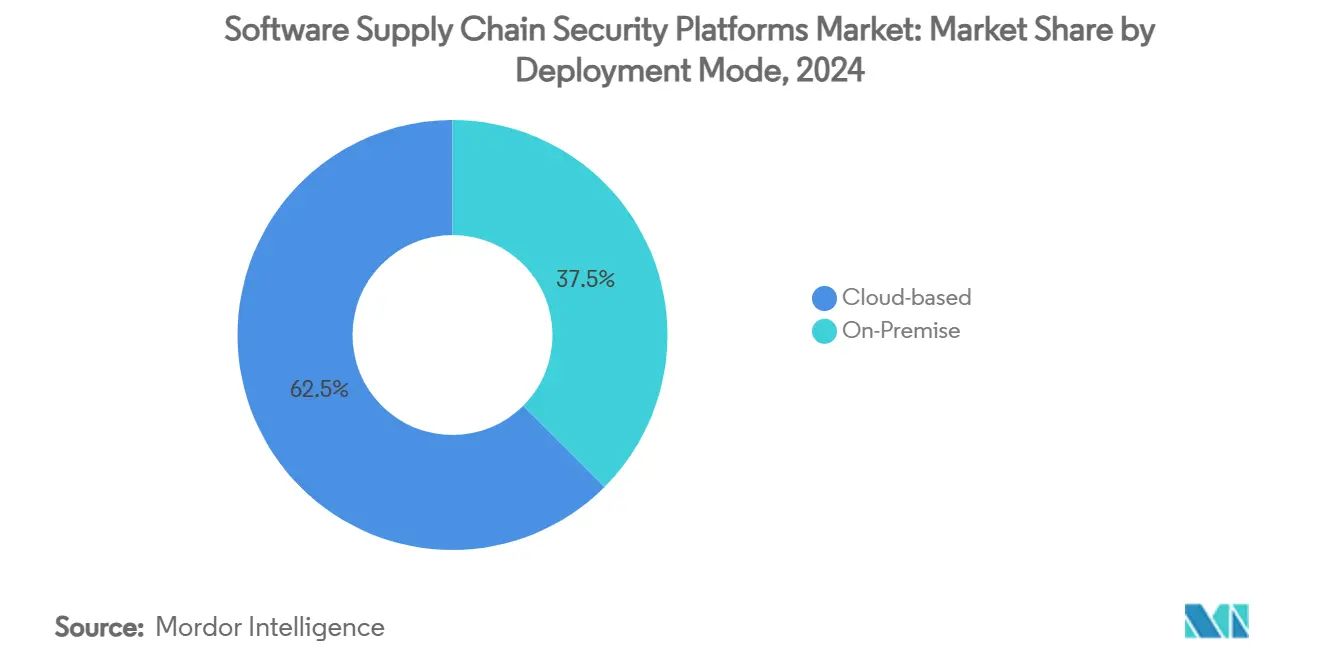

- By deployment mode, cloud-based solutions led with 62.5% revenue share of the Software Supply Chain Security Platforms market in 2024, and the same segment is projected to compound at 14.1% CAGR through 2030.

- By platform type, Software Composition Analysis captured 40.7% of the Software Supply Chain Security Platforms market share in 2024; continuous integrity and attestation tools are forecast to expand at a 13.9% CAGR through 2030.

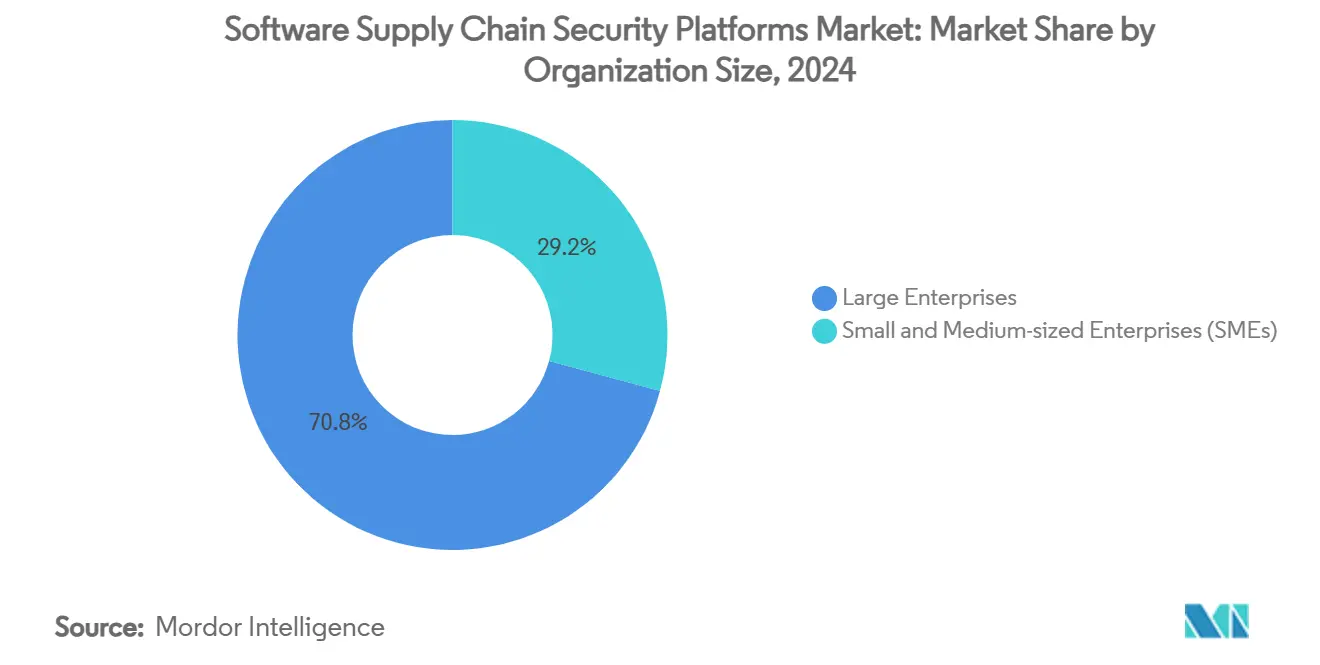

- By organization size, large enterprises commanded a 70.8% share of the Software Supply Chain Security Platforms market size in 2024, while SMEs recorded the highest projected CAGR at 14.5% through 2030.

- By end-user industry, IT and Telecom retained 29.3% revenue share of the Software Supply Chain Security Platforms market in 2024, whereas retail and e-commerce are advancing at 14.1% CAGR to 2030.

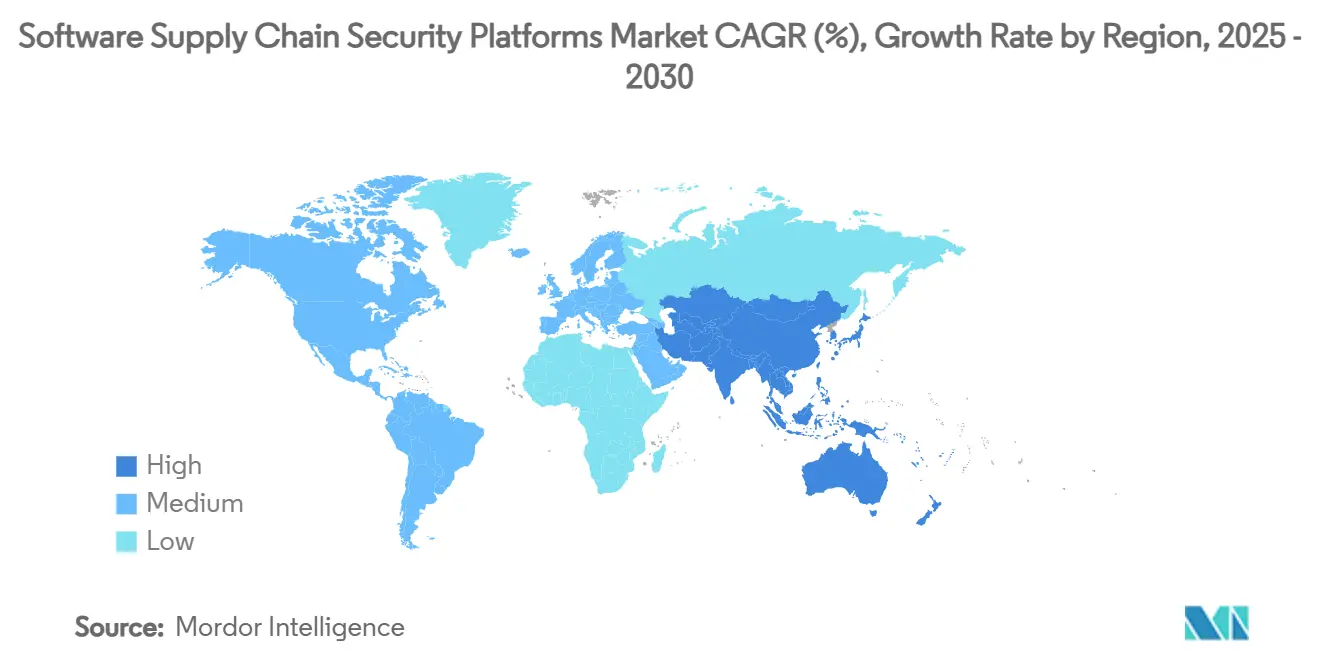

- By geography, North America held a 38.5% share of the Software Supply Chain Security Platforms market in 2024, although Asia-Pacific is set to climb fastest at 14.2% CAGR through 2030.

Global Software Supply Chain Security Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of open-source components | +2.5% | Global | Medium term (2-4 years) |

| Mandatory SBOM disclosure in U.S. federal procurements | +1.8% | North America, spillover to EU | Short term (≤ 2 years) |

| Surge in supply-chain attacks on CI/CD pipelines | +1.2% | Global (North America and Europe concentrated) | Short term (≤ 2 years) |

| Shift-left DevSecOps adoption across SMBs | +1.5% | Global, led by North America and APAC | Medium term (2-4 years) |

| VC-backed innovation in binary provenance | +0.9% | North America and Europe | Long term (≥ 4 years) |

| AI-assisted vulnerability triage | +0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Open-Source Components in Enterprise Applications

Open-source code now constitutes 75% of typical enterprise applications, reshaping risk postures and creating enduring pull for Software Composition Analysis solutions within the Software Supply Chain Security Platforms market. Vulnerabilities introduced by a single compromised library can cascade across thousands of downstream projects, as seen in healthcare, where the U.S. FDA demands SBOM submissions for all medical devices. [2]Erez Kaminski, “The FDA Drops a Cybersecurity Compliance SBOM in 2023,” Ketryx, ketryx.com Financial institutions echo this pressure; Germany-based NORD/LB cut key-management time from days to minutes after adopting HashiCorp Vault, reflecting how visibility into open-source dependencies improves compliance and operational performance. The trend intensifies as AI/ML frameworks enter mainstream development, prompting vendors such as JFrog to partner with Hugging Face to secure machine-learning model artifacts. The self-reinforcing cycle of higher open-source use driving richer platform demand promises sustained growth for the Software Supply Chain Security Platforms market.

Mandatory SBOM Disclosure in U.S. Federal Procurements

President Biden’s January 2025 Executive Order obliges every federal software supplier to submit a machine-readable SBOM, transforming SBOM generation from a best practice into a legal requirement. The rule immediately cascades across supply chains, because prime contractors now insist their vendors provide identical component transparency. Anchore’s role in the U.S. DoD “IRON Bank” illustrates the knock-on effect: container images without verifiable SBOMs cannot attain production approval. Spillover is evident in Europe, where the impending Cyber Resilience Act introduces parallel disclosure mandates, creating trans-Atlantic harmonization that multiplies addressable demand. The National Defense Authorization Act for FY 2025 further entrenches supply-chain security by inserting contractual obligations for defense contractors, cementing the Software Supply Chain Security Platforms market as a compliance imperative for thousands of suppliers.

Surge in Supply-Chain Attacks on CI/CD Pipelines

Attackers increasingly target build pipelines, exploiting implicit trust between automation scripts and artifact repositories. GitHub Actions-based incidents such as “tj-actions” and “reviewdog” compromises in 2024 underscored how malicious code injected during compilation propagates unchecked to production. A Fortune 500 U.S. bank reduced its DevOps compliance window from 30 days to mere hours by introducing event-driven governance that flags anomalous build steps, showcasing the business case for real-time pipeline security. Manufacturing organizations have recorded a 26% YoY rise in supply-chain breaches, averaging 4.16 incidents per company, reinforcing the urgency for integrated safeguards that monitor the entire development lifecycle. Retailers felt the financial sting when a major UK brand suffered a nine-figure loss following a pipeline-enabled intrusion, accelerating adoption across e-commerce platforms. The Software Supply Chain Security Platforms market, therefore, pivots from passive vulnerability scanning toward continuous integrity verification that protects build environments end-to-end.

Shift-Left DevSecOps Adoption Across the SMB Segment

Small and mid-sized organizations now embed security earlier in coding cycles to lower total remediation costs. Yet only 17% of these firms rate their cybersecurity skills as effective, widening the appetite for easy-to-deploy SaaS platforms. CISA’s supply-chain handbook highlights expertise gaps and supplier visibility as top risks that shift-left practices mitigate via automated testing and policy-as-code. Stacklok’s cloud-native Minder exemplifies mainstream adoption, delivering continuous policy enforcement for open-source projects without heavy configuration. Financial incentives such as U.S. tax credits and grants reduce budget constraints, while AI-driven tooling like Lineaje’s SBOM360 trims developer workload by up to 40% through automated triage. Collectively, these developments extend the Software Supply Chain Security Platforms market beyond large enterprises into high-growth SMB terrain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of universally accepted SBOM formats and standards | -0.8% | Global | Medium term (2-4 years) |

| Shortage of qualified AppSec and DevSecOps talent | -1.1% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Tool sprawl creating integration complexity | -0.7% | Global, concentrated in large enterprises | Medium term (2-4 years) |

| Perceived IP leakage risk with cloud-native scanners | -0.5% | Global, acute in regulated industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Universally Accepted SBOM Formats and Standards

Despite policy momentum, the SBOM exchange remains fragmented because no mandatory global format exists. NIST SP 800-161 offers comprehensive supply-chain guidance but does not enforce a single schema, leaving vendors to create proprietary outputs that hinder interoperability. Large manufacturers operating multi-tier networks must run several SBOM generators to satisfy diverse customer demands, inflating cost and complexity. IBM’s Trust Your Supplier blockchain shortened vendor onboarding from 60 days to 3 days, yet required bespoke connectors to reconcile incompatible SBOM data. The EU Cyber Resilience Act promises a harmonized template, but practical adoption is unlikely before 2027, perpetuating near-term friction. These inefficiencies temper the overall Software Supply Chain Security Platforms market growth until clearer standards emerge.

Shortage of Qualified AppSec and DevSecOps Talent

Global demand for professionals fluent in secure development practices far exceeds supply, especially in North America and Europe. Enterprises therefore rely heavily on automation, yet still need skilled personnel to interpret findings and prioritize remediation. A U.S. federal credit union implemented Skybox Network Assurance to streamline vulnerability management but retained specialists to assess strategic risk posture. Escalating salary premiums inflate project budgets and delay full-scale rollouts, particularly among resource-constrained firms. Universities are expanding curricula, yet the deep fusion of software engineering and security means training cycles remain multi-year, extending the talent bottleneck and restraining the Software Supply Chain Security Platforms market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Deployment Extends Dominance

Cloud-hosted solutions accounted for 62.5% of the Software Supply Chain Security Platforms market size in 2024 and are forecast to climb at a 14.1% CAGR, propelled by instant scalability and continuous product updates. [3]OpenText, “Large International Financial Services Organization,” opentext.com Financial institutions validate the value proposition: a European bank integrated Voltage SecureData on Microsoft Azure and met GDPR objectives in eight weeks while enabling secure analytics. Cloud elasticity also lowers entry barriers for SMEs, enabling subscription models without capital outlays.

On-premise deployments persist where data sovereignty or air-gap controls are mandatory, notably in defense and critical infrastructure. Yet maintenance overhead and patch-management burdens hamper their growth trajectory. Vendors increasingly offer hybrid architectures that synchronize on-premise scanners with cloud-based analytics, bridging regulatory constraints while sustaining the broader shift toward cloud-centric consumption in the Software Supply Chain Security Platforms market.

By Platform Type: SCA Leads but Integrity Solutions Accelerate

Software Composition Analysis platforms hold 40.7% of the Software Supply Chain Security Platforms market share, thanks to mature vulnerability and license management capabilities. Continuous integrity and attestation tools, however, post the fastest 13.9% CAGR as organizations seek proactive defenses that validate artifact provenance before deployment. Anchore’s evolution within DoD’s IRON Bank demonstrates how policy engines and custom compliance checks reduce false positives and automate SBOM generation.

Specialized niches expand in tandem: SBOM management suites streamline component inventories, dependency-manager add-ons secure package registries, and repository firewalls protect binary stores. AI-assisted analytics, embodied by Lineaje’s agentic remediation workflows, catalyze cross-segment convergence, indicating that multi-layered feature sets will define future competitive advantage within the Software Supply Chain Security Platforms market.

By Organization Size: SME Momentum Signals Democratization

Large enterprises represented 70.8% of 2024 revenues owing to complex software estates and stringent compliance pressures. Yet SME spending rises at 14.5% CAGR as intuitive cloud consoles and pay-as-you-grow billing erase historical barriers. Government handbooks and incentives fuel this democratization, while products like Stacklok Minder bundle default security policies that minimize configuration overhead.

As resource-limited teams lean on AI-driven triage to offset talent shortages, vendors courting SMEs embed workflow wizards and contextual tutorials, expanding total addressable demand. Consequently, the Software Supply Chain Security Platforms market now treats SMBs as growth engines, not fringe customers.

By End-User Industry: Retail and E-commerce Outpace IT and Telecom

IT and Telecom retained 29.3% of 2024 revenue on account of deep DevOps maturity and mission-critical uptime requirements. Nevertheless, retail and e-commerce exhibit the highest 14.1% CAGR as headline breaches expose direct revenue risks. Fine-grained SBOMs and pipeline hardening mitigate third-party plugin vulnerabilities common in omnichannel storefronts, driving accelerated investment.

BFSI, healthcare, government, manufacturing, and energy sectors continue steady adoption. Healthcare remains influenced by FDA SBOM requirements for medical devices, while defense contracts stipulate container hardening that spurs DoD-aligned platform enhancements. These sector-specific triggers diversify demand and stabilize growth for the Software Supply Chain Security Platforms market.

Geography Analysis

North America contributed 38.5% of Software Supply Chain Security Platforms market share in 2024, powered by sweeping U.S. federal directives that enforce machine-readable SBOM submissions and supply-chain attestations. The region’s mature vendor landscape, plus initiatives like DoD IRON Bank that embeds Anchore Enterprise, foster rapid private-sector replication. Canadian and Mexican firms increasingly align security postures with U.S. standards to preserve cross-border commercial flows, further cementing regional dominance.

Asia-Pacific emerges as the fastest-growing geography at 14.2% CAGR through 2030, underpinned by large-scale digital-government schemes, aggressive cloud adoption, and offshore development centers that must satisfy Western compliance mandates. India’s CERT-financed bug-bounty programs and Singapore’s Smart Nation blueprint galvanize local demand, while Japanese auto-makers embed SBOM verification in firmware pipelines. The region simultaneously supplies cost-effective innovation, injecting competitive dynamism into the Software Supply Chain Security Platforms market.

Europe maintains steady expansion on the back of the EU Cyber Resilience Act, plus established data-sovereignty norms. German, UK, and French banks unify key management via platforms such as HashiCorp Vault, securing cryptographic assets while meeting PSD2 and GDPR obligations. Eastern European software hubs adopt attestation tooling to fulfill export bids, underscoring the pan-regional ripple effect of unified legislation. Coordinated standards initiatives position Europe as a pivotal catalyst for global alignment in SBOM formats, a linchpin issue for the Software Supply Chain Security Platforms market.

Competitive Landscape

The Software Supply Chain Security Platforms market is moderately fragmented, with legacy cybersecurity vendors and venture-backed entrants racing to automate vulnerability triage and verify artifact provenance. Synopsys, Sonatype, and Snyk leverage broad product suites and enterprise sales footprints, while cloud-native specialists such as Chainguard, Endor Labs, and Lineaje target emerging zero-trust and attestation niches. Government backing amplifies challenger credibility; Chainguard received a USD 200,000 DHS award to advance SBOM tooling. [4]Chainguard, “Chainguard Joins DHS Cohort,” chainguard.dev

Consolidation proceeds via strategic investments—Wipro’s stake in Lineaje, following its USD 20 million Series A, exemplifies integrator interest in turnkey supply-chain offerings. Platform differentiation pivots on AI; Snyk’s AI Trust Platform surpassed USD 100 million ARR within months, showing buyer appetite for automated fix-prioritization. Cloud providers intensify rivalry: Red Hat’s Trusted Software Supply Chain bundles pipeline hardening and signature verification, pressuring independents to interoperate or risk displacement. As vendor ecosystems merge scanning, policy, and remediation, competitive advantage will hinge on unified workflows and compliance-grade reporting that address widening regulation, sustaining vibrant competition within the Software Supply Chain Security Platforms market.

Software Supply Chain Security Platforms Industry Leaders

Synopsys, Inc.

Sonatype, Inc.

Snyk Ltd.

GitLab Inc.

JFrog Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Snyk launched its AI Trust Platform, eclipsing USD 100 million ARR in months, underscoring demand for AI-driven remediation.

- March 2025: JFrog partnered with Hugging Face to secure machine-learning models in supply chains.

- March 2025: Sonatype expanded AI/ML vulnerability detection across its product family.

- February 2025: Chainguard secured a USD 200,000 DHS grant to advance SBOM composition tools.

- January 2025: U.S. Executive Order mandated machine-readable SBOMs for federal suppliers.

- December 2024: OPSWAT introduced MetaDefender Software Supply Chain for critical infrastructure.

Global Software Supply Chain Security Platforms Market Report Scope

| Cloud-based |

| On-Premise |

| Software Composition Analysis (SCA) Platforms |

| Software Bill of Materials (SBOM) Management Platforms |

| Dependency / Package Manager Security Platforms |

| Continuous Integrity and Attestation Platforms |

| CI/CD Pipeline Security Platforms |

| Binary / Artifact Repository Security Platforms |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Government and Defense |

| Retail and E-commerce |

| Manufacturing |

| Energy and Utilities |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-based | ||

| On-Premise | |||

| By Platform Type | Software Composition Analysis (SCA) Platforms | ||

| Software Bill of Materials (SBOM) Management Platforms | |||

| Dependency / Package Manager Security Platforms | |||

| Continuous Integrity and Attestation Platforms | |||

| CI/CD Pipeline Security Platforms | |||

| Binary / Artifact Repository Security Platforms | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-user Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Software Supply Chain Security Platforms market?

The market is valued at USD 5.53 billion in 2025.

How fast is the Software Supply Chain Security Platforms market expected to grow?

It is projected to expand at a 12.8% CAGR between 2025 and 2030.

Which deployment mode holds the largest share?

Cloud-based platforms captured 62.5% of revenue in 2024.

Which region is growing the fastest?

Asia-Pacific is forecast to register a 14.2% CAGR through 2030.

Why are SBOMs important in software supply-chain security?

SBOMs provide a machine-readable inventory of software components, enabling vulnerability tracking and regulatory compliance.

What is the biggest restraint facing this market?

A shortage of qualified AppSec and DevSecOps professionals restricts widespread platform deployment and optimization.

Page last updated on: