Secure Code Review Platforms Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

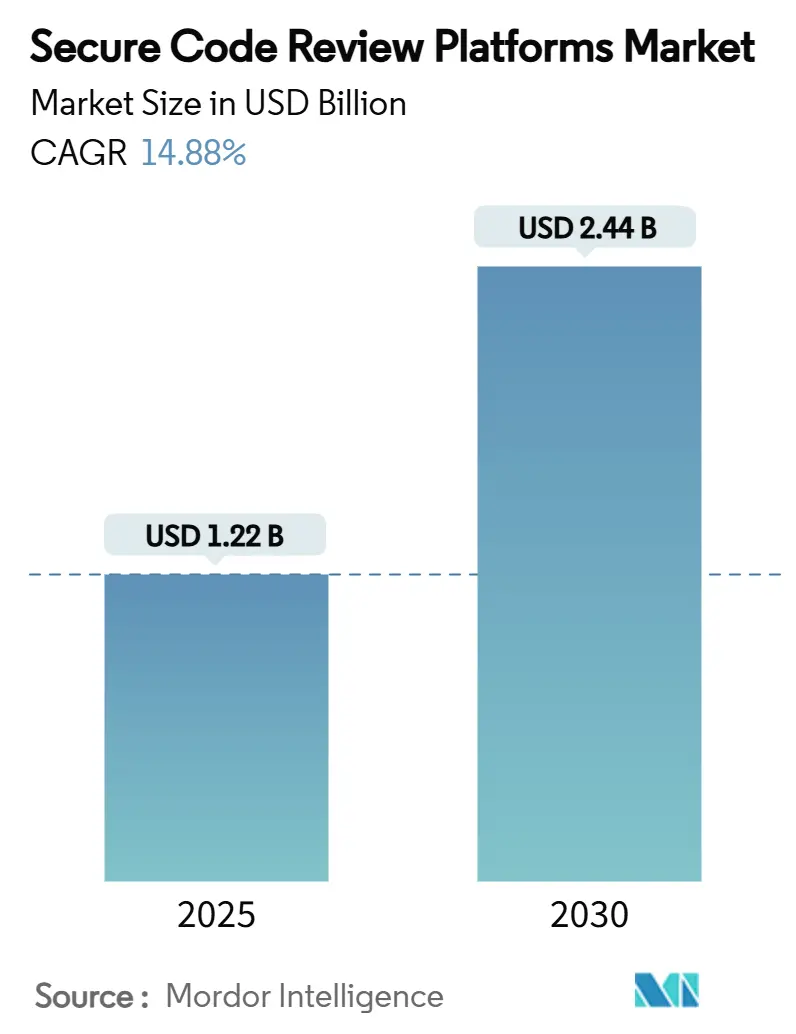

| Market Size (2025) | USD 1.22 Billion |

| Market Size (2030) | USD 2.44 Billion |

| Growth Rate (2025 - 2030) | 14.88% CAGR |

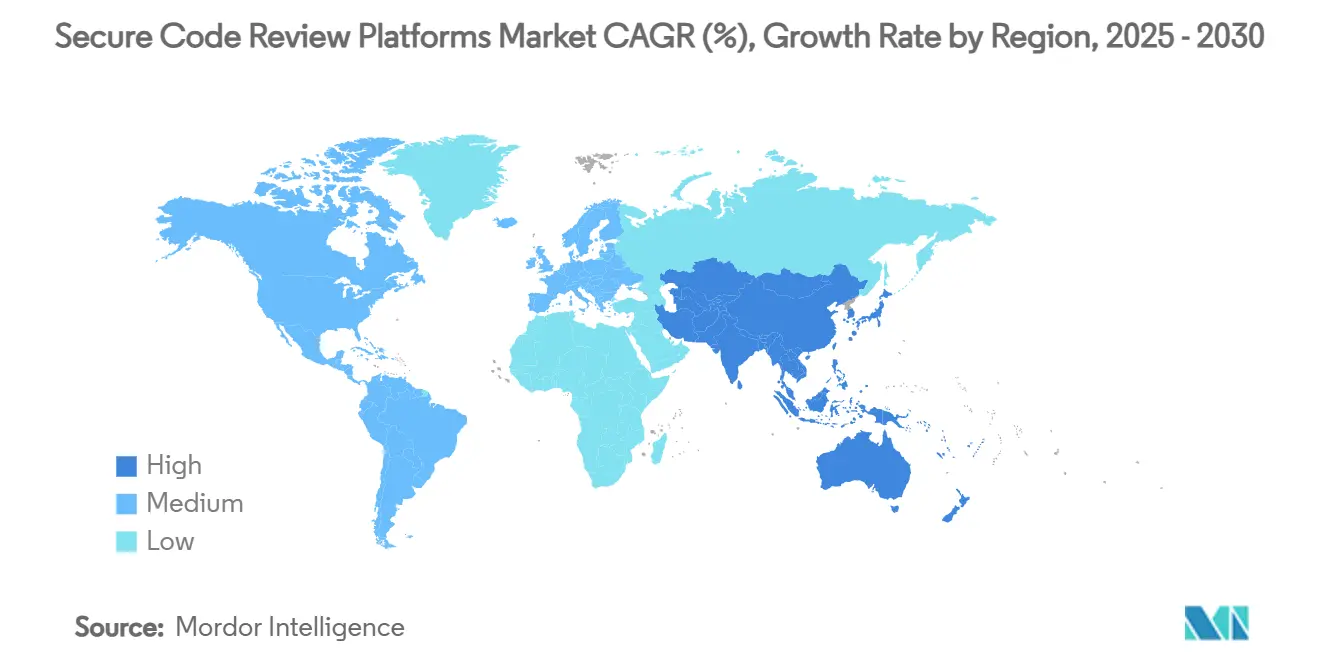

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secure Code Review Platforms Market Analysis by Mordor Intelligence

The secure code review platforms market size stands at USD 1.22 billion in 2025 and is forecast to reach USD 2.44 billion by 2030, reflecting a 14.88% CAGR. This expansion mirrors the widening digital transformation agenda, mounting regulatory pressure, and the accelerated use of AI-assisted development that requires continuous security validation. Executive Order 14028 in the United States and the EU’s NIS2 directive have moved secure coding from an internal best practice to a procurement prerequisite, shifting budget priorities toward platforms that generate software bills of materials, supply chain attestations, and automated compliance artifacts. The upsurge of AI-generated code deepens security blind spots and intensifies demand for tools that can evaluate machine-produced logic in real time. Consolidation continues—Synopsys divested its Software Integrity Group for up to USD 2.1 billion, while private-equity owners reportedly seek a USD 2.5 billion valuation for Checkmarx—showing investors’ confidence in scale-driven platform growth. Meanwhile, persistent quality issues in legacy static analysis create opportunities for AI-augmented detection and auto-remediation, positioning intelligent review engines as the next growth catalyst.

Key Report Takeaways

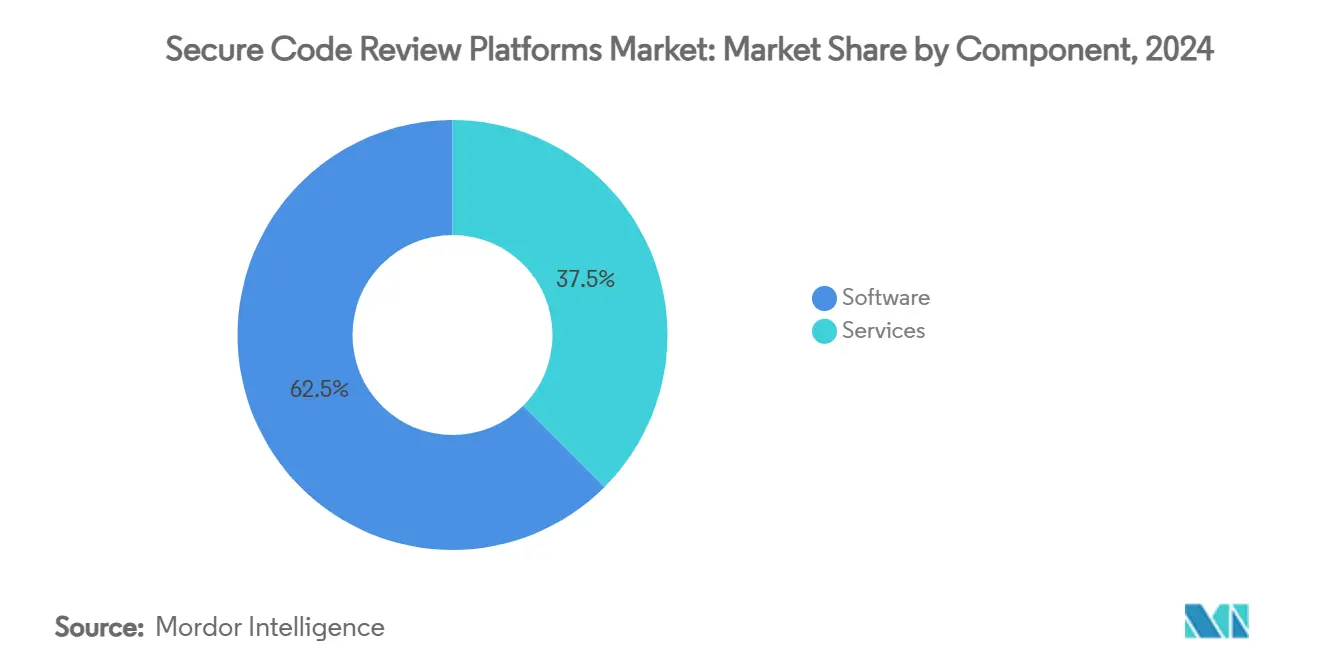

- By component, software led with 62.5% revenue share of the secure code review platforms market in 2024, while services are projected to advance at a 16.4% CAGR through 2030.

- By deployment, cloud-based solutions held 56.7% of 2024 revenue in the secure code review platforms market, whereas hybrid models are set to expand at a 16.2% CAGR over the forecast period.

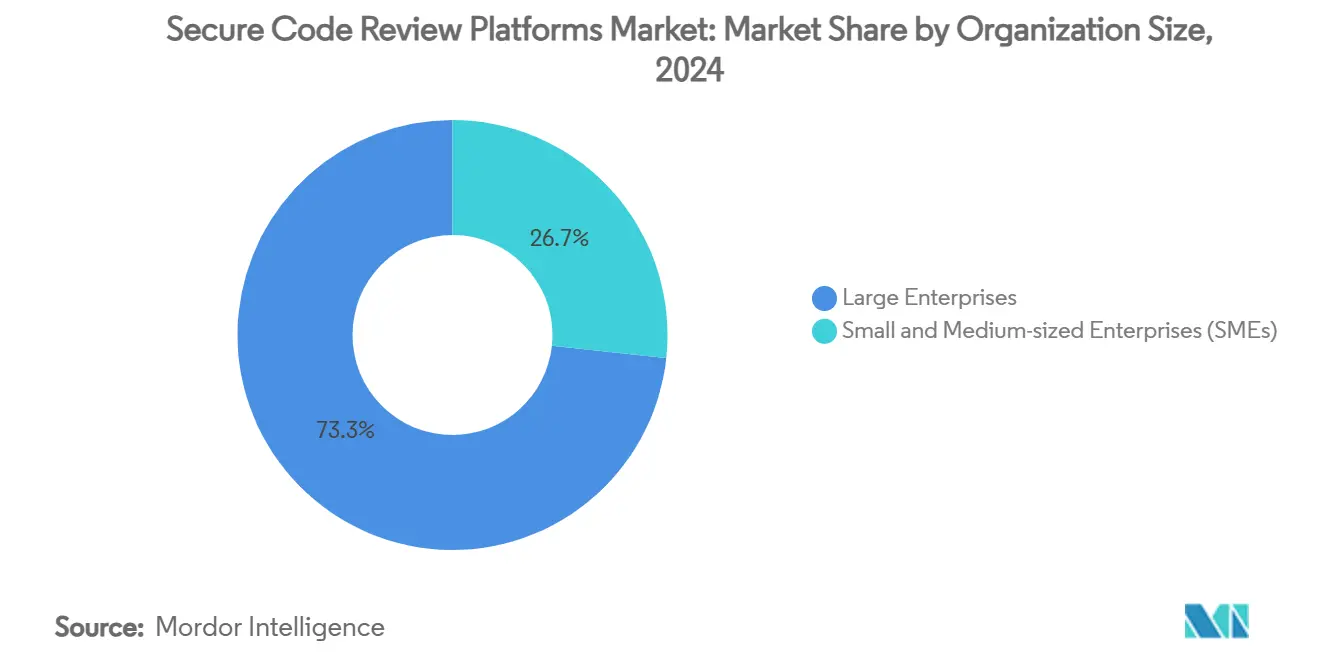

- By organization size, large enterprises accounted for 73.3% of spending in 2024, but SMEs are forecast to grow at a 16.5% CAGR to 2030 in the secure code review platforms market.

- By testing type, static application security testing commanded 42.7% of the secure code review platforms market revenue in 2024, while AI-augmented automated review is expected to post a 16% CAGR during the same horizon.

- By industry vertical, IT and telecom captured 29.5% of 2024 revenue, yet BFSI is poised to record a 15.9% CAGR through 2030 in the secure code review platforms market.

- By geography, North America dominated with a 38.2% share of the secure code review platforms market in 2024, whereas Asia-Pacific is anticipated to achieve a 16.1% CAGR across the forecast window.

Global Secure Code Review Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DevSecOps adoption across SDLC | +2.1% | North America, Europe | Medium term (2-4 years) |

| Regulatory mandates for secure software supply chain | +2.8% | North America, EU, expanding to APAC | Long term (≥ 4 years) |

| Open-source component explosion driving SCA | +1.9% | Global, enterprise focus | Short term (≤ 2 years) |

| GenAI-powered auto-remediation capabilities | +2.3% | North America, Europe | Medium term (2-4 years) |

| Cyber-insurance premiums tied to code security metrics | +1.7% | North America, Europe | Long term (≥ 4 years) |

| Commercialization of SBOM services | +1.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

DevSecOps Adoption Across SDLC

Growing recognition that post-deployment fixes slow delivery has prompted security controls to shift left into automated pipelines. Firms embedding continuous testing, policy-as-code, and real-time feedback reports reduced release delays and higher developer productivity. Adoption rises fastest in microservices and containerized environments where decentralized teams depend on automated guardrails to keep pace. [1]Pynt, “18 DevSecOps Tools to Know in 2025,” pynt.io Tool vendors now emphasize friction-free integrations with popular CI/CD orchestrators, enabling security checks to run on every commit without manual triggers. Companies that rolled out comprehensive DevSecOps in 2024 continue to expand coverage to third-party dependencies and Infrastructure-as-Code, enlarging addressable spend for review platforms.

Regulatory Mandates for Secure Software Supply Chain

The US federal supply-chain rules and Europe’s NIS2, CRA, and DORA directives oblige vendors to furnish SBOMs, vulnerability disclosure processes, and tamper-evident development pipelines. Non-compliance risks contractual exclusion and fines reaching 2% of global turnover in the EU. Demand therefore skews toward platforms that automate component inventory, generate attestation packages, and maintain immutable audit trails. Critical infrastructure operators—power, transport, and healthcare—face earlier deadlines, accelerating near-term purchases and creating durable demand for update-ready SaaS and hybrid deployments.

Open-Source Component Explosion Driving SCA

Modern applications average 80% open-source code, requiring continuous visibility into nested dependencies. The Log4j incident underscored cascading vulnerability exposure, spurring enterprises to adopt software composition analysis that maps component hierarchies, licenses, and known flaws. [2]HC3, “Open-Source Software Risks in the Health Sector,” hhs.gov Contemporary SCA suites integrate predictive analytics to flag emerging risks and trigger automated pull-request upgrades, helping security teams prioritize remediation across sprawling codebases without exhaustive manual triage.

GenAI-Powered Auto-Remediation Capabilities

Platform vendors embed large language models fine-tuned on secure coding corpora to explain findings in plain language and offer ready-to-merge patches. Snyk’s AI-native static engine surpassed USD 100 million annual recurring revenue, validating appetite for automated fixes that cut triage overhead. Early adopters cite dramatic reductions in duplicate alerts and faster merge cycles. Yet AI-generated patches must themselves be verified, spawning complementary solutions that scan model-produced code for policy adherence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High false-positive rates and developer fatigue | -1.8% | Global | Short term (≤ 2 years) |

| Shortage of AppSec talent | -2.1% | North America, Europe | Long term (≥ 4 years) |

| Rule-set portability across language ecosystems | -1.2% | Global | Medium term (2-4 years) |

| Data-residency limits on cloud review adoption | -0.9% | Europe, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High False-Positive Rates and Developer Fatigue

A flood of generic alerts undermines trust in scanning outputs, with platform telemetry showing more than one-quarter of flagged issues ultimately dismissed as non-exploitable. Development teams overwhelmed by noisy findings delay remediation, extending vulnerability windows. Vendors now embed context-aware ranking, data-flow tracing, and AI-based duplicate suppression to surface only actionable defects. Interactive Application Security Testing (IAST) further reduces noise by validating findings at runtime, though adoption is still hampered by integration complexity and performance overhead.

Shortage of AppSec Talent

Demand for secure development expertise continues to exceed supply, inflating salaries and elongating hiring cycles. Enterprises lacking dedicated application security engineers struggle to configure policies, fine-tune rule sets, and triage findings. Vendors respond with managed service offerings and pre-packaged best-practice workflows that lower entry barriers, yet effective oversight remains essential, tempering near-term platform penetration, especially among budget-constrained organizations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum

Software licenses retained 62.5% of the secure code review platforms market share in 2024 as core scanning engines remain fundamental purchase drivers. However, services revenue is projected to rise at a 16.4% CAGR as organizations outsource implementation, rule authoring, and continuous monitoring. The secure code review platforms market size for managed services is expanding quickest within regulated verticals that must demonstrate ongoing assurance to auditors. Hospitals, for example, engage external specialists to operate centralized code risk programs that integrate platform telemetry with broader cyber-supply-chain dashboards. [3]National Institute of Standards and Technology, “Case Studies in Cyber Supply Chain Risk Management: Mayo Clinic,” nist.gov

Rising service demand also reflects the transition from tool-centric to outcome-centric buying. Providers now bundle incident response, ticket triage, and compliance reporting into recurring subscriptions, enabling clients to circumvent hiring bottlenecks and focus scarce internal talent on strategic initiatives.

By Deployment: Hybrid Bridges Control and Scalability

Cloud deployments delivered the largest revenue slice at 56.7% in 2024, favored for zero-maintenance updates and proximity to SaaS-centric development teams. Yet the hybrid model is forecast to expand at 16.2% CAGR as firms reconcile data-sovereignty mandates with DevSecOps velocity. The secure code review platforms market size attributable to hybrid architectures grows most rapidly in Europe, where NIS2 and GDPR push repositories containing classified code to remain on-premise.

Hybrid designs typically run scanning engines locally while offloading analytics, dashboards, and ticketing to multitenant clouds, offering granular control without sacrificing collaborative features. On-premise-only deployments persist in defense and critical infrastructure, but their relative share declines as containerized scanners simplify isolated processing inside otherwise cloud-native workflows.

By Organization Size: SMEs Accelerate Adoption

Large enterprises commanded a dominant 73.3% share of the secure code review platforms market size in 2024, owing to complex portfolios and mandatory compliance. However, SME spending is set to climb at a 16.5% CAGR as subscription-based SaaS models with tiered pricing lower entry costs.

SMEs gravitate toward AI-assisted triage that reduces manual expertise requirements and toward cloud-hosted dashboards that abstract infrastructure management. Born-in-cloud startups frequently embed secure code review from day one, treating automated scanning as a standard pipeline step rather than an optional layer, accelerating tool stickiness and lifetime value for vendors.

By Testing Type: AI-Augmented Review Gains Traction

Static Application Security Testing held a 42.7% share in 2024, thanks to broad language coverage and early-stage defect detection. Nonetheless, AI-augmented automated review now records the fastest 16% CAGR as buyers prioritize context-rich insights and quick fixes. The secure code review platforms market share for AI-augmented products is likely to widen further as vendors demonstrate lower false-positive ratios and faster mean-time-to-remediate than legacy SAST.

Meanwhile, demand for Software Composition Analysis rises in tandem with open-source usage, and Interactive Application Security Testing adoption grows in containerized architectures where runtime feedback complements static scanning. Suites combining all four modalities on a unified dashboard increasingly dominate shortlist evaluations.

By Industry Vertical: BFSI Surges Ahead

IT and Telecom retained the revenue lead at 29.5% in 2024 due to large in-house engineering teams and high release cadence. Banking, Financial Services, and Insurance exhibits the strongest 15.9% CAGR as regulators tighten oversight and insurers link cyber-premiums to secure coding metrics. The secure code review platforms market size allocated to BFSI is buoyed by large modernization budgets across core banking, digital wallets, and embedded finance.

Healthcare and Life Sciences show renewed interest as the FDA enforces pre-market and post-market cybersecurity documentation for connected devices. [4]Medcrypt, “Meeting FDA Cybersecurity Requirements with Medcrypt Guardian & RTI Connext,” medcrypt.com Government agencies also increase funding to secure critical software infrastructure that underpins essential public services.

Geography Analysis

North America held a 38.2% share in 2024 on the back of federal procurement rules that embed SBOM and continuous monitoring requirements into contract clauses. The region’s venture ecosystem accelerates innovation, with Snyk crossing USD 100 million ARR and GitHub rolling out AI-based secret scanning that cuts false positives by 94%. Consolidation, such as Synopsys carving out its Software Integrity unit, signals sustained investor appetite for platform plays that cover the entire DevSecOps workflow.

Asia-Pacific is projected to register a 16.1% CAGR, the fastest among all regions. A growing pool of software engineers, rising cloud adoption, and new cybersecurity directives in Japan, India, and Singapore drive procurement. Companies headquartered in Singapore, India, and Vietnam export secure-code services globally, leveraging cost advantages while adhering to international standards. Local start-ups such as AppSecure showcase regional expertise by offering penetration testing and source review packages across APAC.

Europe witnesses steady growth anchored by NIS2, CRA, and DORA, which collectively cover an estimated 350,000 entities. Hybrid deployment popularity rises as organizations balance data residency with feature velocity. Supply-chain breaches have intensified purchaser scrutiny of vendor security programs, boosting demand for platforms that can map dependency trees and generate real-time vulnerability disclosures.

Competitive Landscape

The market remains moderately fragmented yet shows rising consolidation. Top platforms integrate SAST, SCA, IAST, and AI-powered remediation behind unified dashboards, creating high switching costs. Sonar’s acquisition of Tidelift broadens coverage into open-source dependency governance, while GitHub’s partnership with JFrog unifies artifact management with code security.

Private-equity activity remains brisk. Synopsys’s Software Integrity Group spun out to Clearlake Capital and Francisco Partners for up to USD 2.1 billion, enabling focused investment to accelerate cloud transformation. Investors reportedly value Checkmarx near USD 2.5 billion, reflecting confidence in cloud-native application security growth.

AI differentiation rises as a key theme. Snyk, Sonar, and Contrast Security showcase proprietary models that shrink alert volumes and auto-generate safe patches, while smaller entrants innovate with language-specific rule engines or vertical-sector coverage. White-space opportunities persist in industrial control software, firmware analysis, and low-code platforms, suggesting scope for niche specialists or targeted acquisitions.

Secure Code Review Platforms Industry Leaders

Synopsys, Inc.

Checkmarx Ltd.

Veracode, Inc.

Snyk Ltd.

SonarSource SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sonar introduced AI Code Assurance and AI CodeFix for one-click remediation.

- May 2025: Snyk unveiled the AI Trust Platform for secure AI-era development.

- March 2025: GitHub enhanced Copilot with AI-driven secret scanning that cuts false positives by 94%.

- March 2025: AWS and GitLab launched an integrated AI offering combining GitLab Duo with Amazon Q to streamline DevSecOps.

- February 2025: Snyk acquired Reviewpad to secure pull requests as AI-generated code volume grows.

- December 2024: Sonar completed the acquisition of Tidelift to strengthen open-source governance.

Global Secure Code Review Platforms Market Report Scope

| Software | |

| Services | Professional Services |

| Managed Services |

| Cloud-based |

| On-premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Static Application Security Testing (SAST) |

| Interactive Application Security Testing (IAST) |

| Software Composition Analysis (SCA) |

| AI-Augmented Automated Review |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Government and Defense |

| Retail and E-commerce |

| Manufacturing |

| Energy and Utilities |

| Education |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment | Cloud-based | ||

| On-premise | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Testing Type | Static Application Security Testing (SAST) | ||

| Interactive Application Security Testing (IAST) | |||

| Software Composition Analysis (SCA) | |||

| AI-Augmented Automated Review | |||

| By Industry Vertical | BFSI | ||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Education | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the secure code review platforms market?

It is valued at USD 1.22 billion in 2025.

How fast will spending on secure code review tools grow?

The market is projected to post a 14.88% CAGR, doubling to USD 2.44 billion by 2030.

Which segment is expanding quickest?

AI-augmented automated review leads at a 16% CAGR thanks to lower false positives and auto-remediation features.

Why are hybrid deployments gaining pace?

They let firms keep sensitive code on-premise while leveraging cloud analytics, meeting data-sovereignty rules such as those under EU NIS2.

Which region is expected to grow the fastest?

Asia-Pacific, supported by a 16.1% CAGR and expanding software-development talent pools.

How concentrated is vendor competition?

The market scores 6/10 on concentration, with the five largest providers holding roughly two-thirds of revenue.

Page last updated on: