Application Programming Interface Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

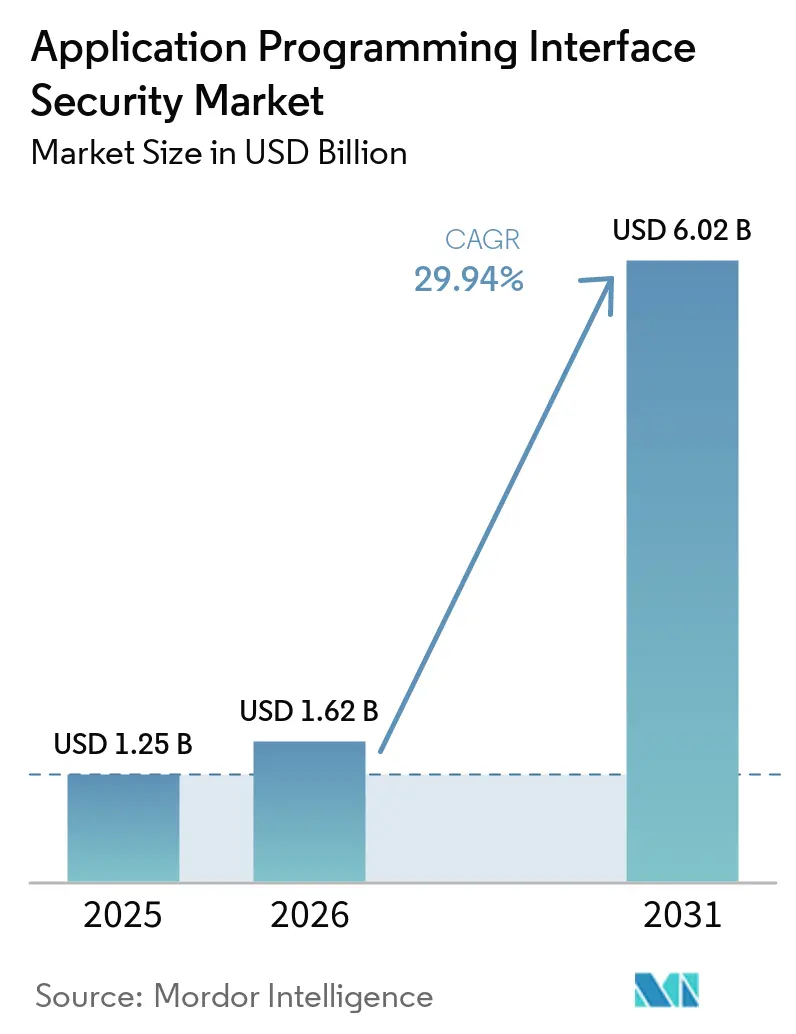

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2026 - 2031) | 29.94% CAGR |

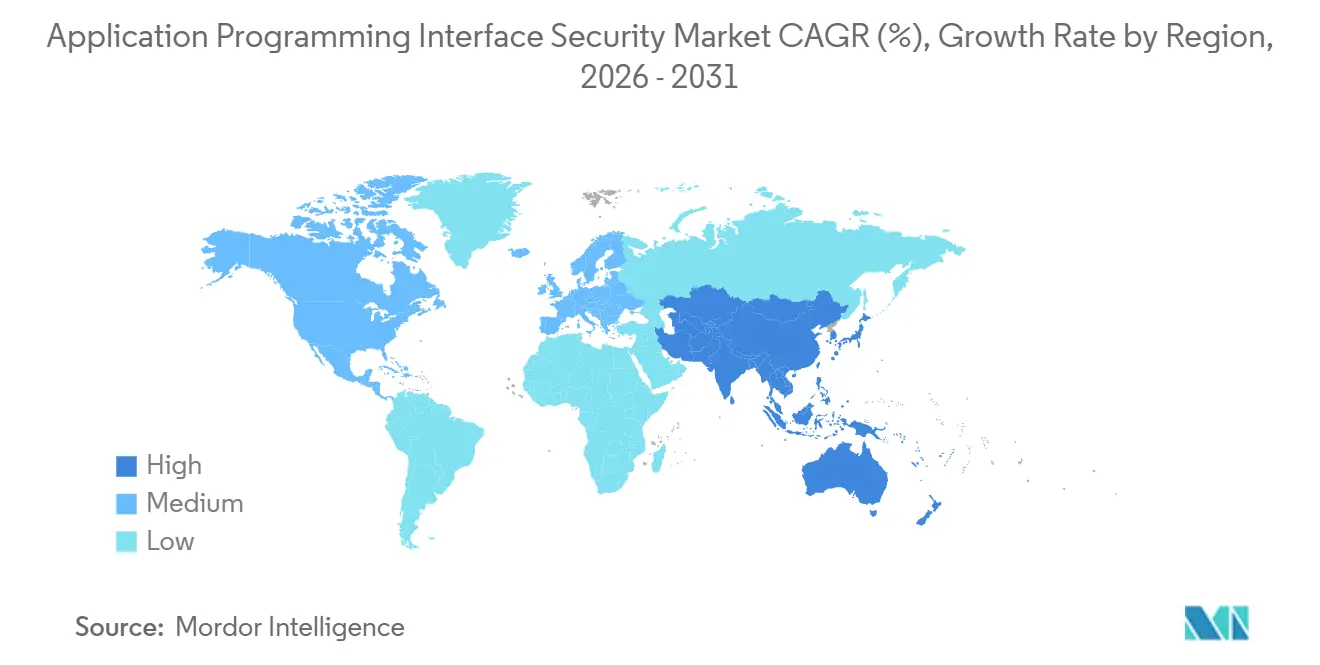

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application Programming Interface Security Market Analysis by Mordor Intelligence

The application programming interface security market size is expected to grow from USD 1.25 billion in 2025 to USD 1.62 billion in 2026 and is forecast to reach USD 6.02 billion by 2031 at a CAGR of 29.94% over 2026-2031. This expansion reflects a clear shift in enterprise security priorities, as APIs now sit closer to revenue flows, customer interactions, and regulated data than the old network edge did. Cloud-native application design and the broader adoption of LLM-enabled software agents are increasing the number of exposed interfaces, making continuous API discovery and runtime monitoring more important than periodic review. Compliance pressure is also accelerating spending, especially after PCI DSS 4.0.1 enforcement in 2025 and the 2026 HIPAA technical safeguard changes that raised the standard for API-related protection in sensitive environments. North America held the largest regional share in 2025 because regulation, vendor depth, and enterprise budgets were concentrated there, while Asia-Pacific is set to expand fastest as incident exposure and executive attention continue to rise. The application programming interface (API) security market remains fragmented, so specialists and broader platform vendors are both using product expansion, workflow integration, and AI-led analytics to compete for the next wave of spending.

Key Report Takeaways

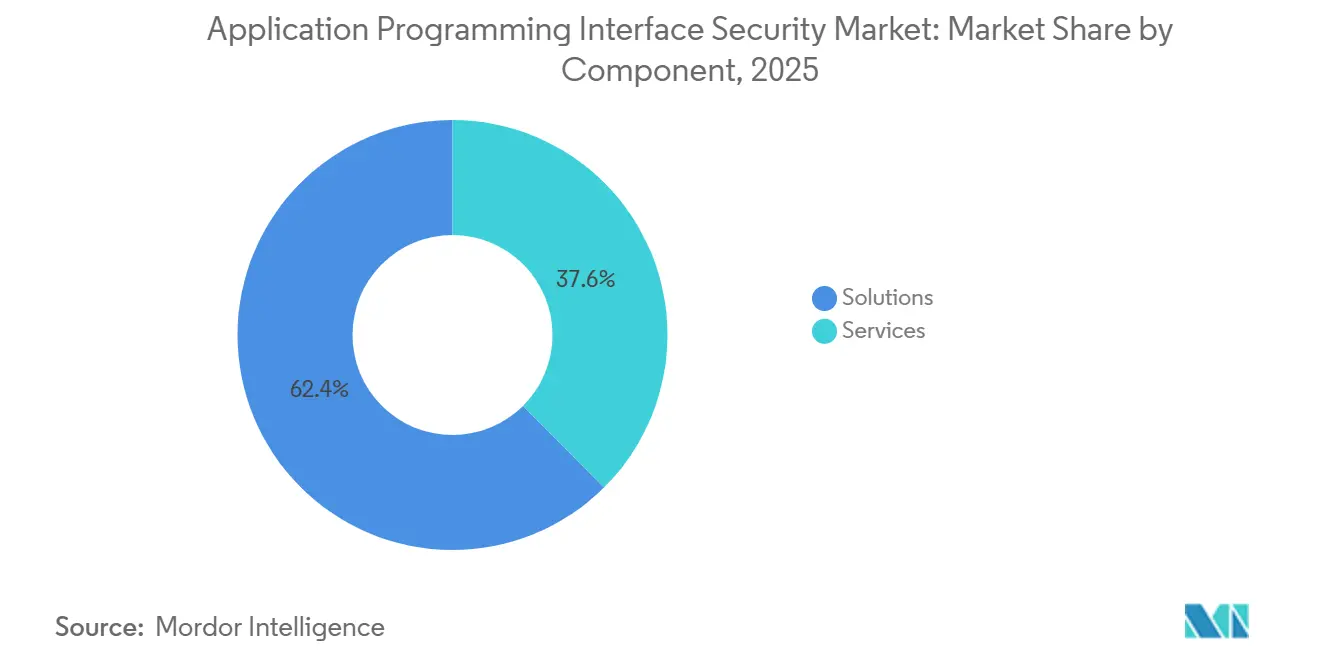

- By component, solutions held 62.44% share of the application programming interface security market in 2025, while services are projected to expand at a 29.98% CAGR through 2031.

- By deployment mode, cloud accounted for 58.31% share of the application programming interface (API) security market in 2025, while hybrid is forecast to grow at a 30.41% CAGR through 2031.

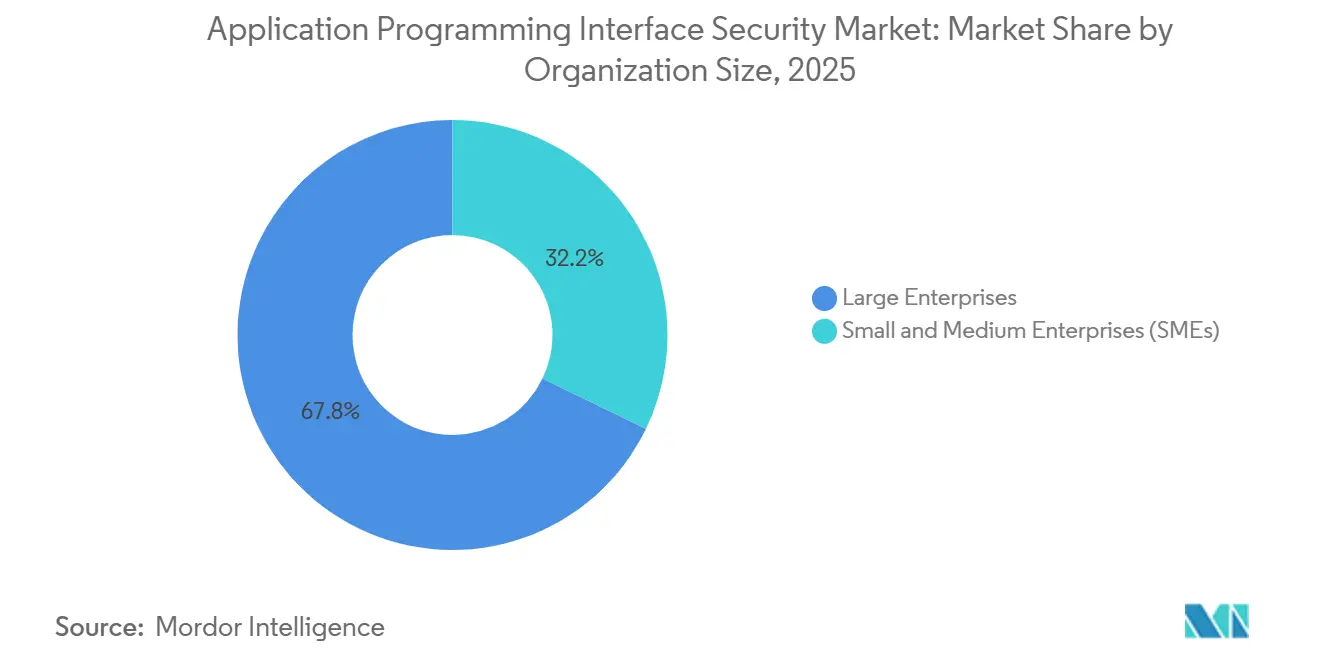

- By organization size, large enterprises held 67.82% share of the API security market in 2025, while small and medium enterprises (SMEs) are expected to record the fastest growth at a 30.23% CAGR through 2031.

- By end-user industry, BFSI held 24.13% share of the application programming interface security market in 2025, while healthcare and life sciences is projected to advance at a 30.34% CAGR through 2031.

- By geography, North America held 38.74% share of the application programming interface security market in 2025, while Asia-Pacific is expected to expand at a 30.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Application Programming Interface Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising API Attack Frequency And Breach Costs | +5.8% | Global | Short term (≤ 2 years) |

| Rapid API Proliferation Across Cloud-Native Architectures | +5.2% | Global, North America and APAC concentration | Medium term (2-4 years) |

| Expanding Compliance And Data Governance Obligations | +4.3% | North America and EU primary, expanding to APAC | Long term (≥ 4 years) |

| Growth Of Partner, Fintech, And Ecosystem APIs | +3.2% | North America, EU, and APAC fintech hubs | Medium term (2-4 years) |

| AI Agents And LLM Workflows Making APIs The AI Control Plane | +3.0% | Global | Short term (≤ 2 years) |

| Shadow, Zombie, And Unmanaged APIs Forcing Discovery-Led Security Spend | +2.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising API Attack Frequency And Breach Costs

The application programming interface security market is moving higher because API attacks are now frequent enough to create direct budgetary urgency for security leaders. Akamai reported that 87% of surveyed global organizations experienced an API-related security incident in 2025. The same release said average daily API attacks per organization rose to 258 in 2025 from 121 in 2024, which marked a 113% year-over-year increase. Akamai also noted that Layer 7 DDoS attacks, which commonly target API endpoints and application resources, climbed 104% over the prior 2 years. This pattern matters because security teams are no longer dealing with isolated misuse, but with automated campaigns that test application logic, rate limits, and access controls at machine speed. As a result, the API security market is increasingly tied to loss prevention, uptime protection, and regulatory exposure instead of discretionary tool spending.

Rapid API Proliferation Across Cloud-Native Architectures

The application programming interface security (API) market is also being driven by the speed at which cloud-native architectures create new interfaces that require governance. Salt Security said nearly 47% of respondents reported API growth of 51%-100% over the prior year, indicating that endpoint inventories are expanding rapidly. In microservices environments, each new service can introduce separate endpoints, identities, and east-west traffic paths that legacy monitoring tools were not designed to interpret in depth. Auto-scaling containers make the problem harder because APIs can appear, move, and retire faster than static documentation or manual reviews can keep pace. That operating model increases the number of shadow and unmanaged APIs, even within firms with mature engineering practices, because the infrastructure itself changes continuously. This is why discovery, posture management, and behavior-based monitoring have become core control layers in the API security market rather than optional add-ons.

Expanding Compliance And Data Governance Obligations

The application programming interface security market is also benefiting from a sharper compliance environment, because several major frameworks now treat API protection as a direct control requirement. PCI DSS 4.0.1, which was fully enforced from March 2025, explicitly requires API security testing under Requirement 6.2.4 for payment environments.[1]PCI Security Standards Council, “PCI DSS v4.0.1,” PCI Security Standards Council, pcisecuritystandards.org The same standard also sets stronger authentication expectations for access to cardholder data environments, reducing the room for weak API-linked access paths. In healthcare, the U.S. Department of Health and Human Services updated the HIPAA Security Rule technical safeguards in February 2026, raising the bar for protecting electronic protected health information that moves through connected systems. In Europe, DORA brought continuous ICT risk management and stronger oversight of third-party technology relationships into the operating model for regulated financial entities, which directly supports API inventory and monitoring programs. These overlapping obligations are pushing buyers toward consolidated platforms that can combine discovery, schema validation, runtime monitoring, logging, and audit support inside a single API security market offering.

Growth Of Partner, Fintech, And Ecosystem APIs

The application programming interface security (API) market is expanding further because partner APIs and ecosystem integrations now sit inside many customer-facing and revenue-generating workflows. Every third-party integration adds another trust boundary, and each boundary brings its own tokens, identities, permissions, and data-handling rules that must be enforced consistently. 42Crunch reported that implementation mistakes around authentication and authorization remained the dominant source of API exposure across industries and organization sizes. Cloudflare's March 2026 scanner launch also focused on active detection of Broken Object Level Authorization, underscoring that object-level access control remains a practical weakness in live deployments. Monetary Authority of Singapore guidance reinforces that regulated firms remain accountable for technology risk, even when services depend on external digital connections, thereby raising the standard for partner oversight. As a result, buyers in the API security market are placing greater value on tools that continuously validate partner access without slowing commercial traffic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity Across Hybrid And Multi-Cloud Estates | -4.2% | Global | Medium term (2-4 years) |

| Shortage Of Specialized API Security Talent | -3.1% | Global | Short term (≤ 2 years) |

| False Confidence In Legacy WAF And Authentication-Centric Controls | -2.5% | Global | Short term (≤ 2 years) |

| Evolving MCP And Agentic AI Security Standards And Ownership Gaps | -1.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across Hybrid And Multi-Cloud Estates

The application programming interface security market still faces friction because many enterprises need to enforce controls across cloud, on-premises, and private infrastructure simultaneously. Those environments often rely on different gateways, identity methods, inspection points, and logging formats, which makes uniform policy enforcement difficult. Fragmentation also weakens runtime context because security teams may see only a slice of API behavior when traffic and ownership are split across multiple tools. Harness positioned Traceable Cloud WAAP around unified discovery, runtime protection, bot mitigation, and DDoS defense, which shows that customers are still trying to replace several disconnected controls with a workable common layer.[2]Harness, “Introducing Traceable Cloud WAAP: Built for the Way Applications Work Today,” Harness, harness.io Akamai's code-to-runtime mapping follows the same logic by linking live API findings to code ownership and reducing the coordination gap between developers and security teams. Until these connections become easier to deploy, integration efforts will continue to limit the pace of adoption across the API security market.

Shortage Of Specialized API Security Talent

The application programming interface security market is also restrained by a shortage of teams that can configure, tune, and operate these platforms consistently. Salt Security found that only 23.5% of security leaders considered their current tools very effective at preventing API-based attacks. That result points to an operating gap as much as a product gap, because continuous discovery and response depend on ownership, process, and skilled tuning. When internal teams cannot keep pace, unmanaged endpoints accumulate between reviews and incident handling becomes more reactive than preventive. This pushes more budget into onboarding, consulting, and managed support instead of direct platform scale-up, especially among smaller organizations. The near-term effect is that talent scarcity continues to slow broader self-service adoption in the API security market, even while demand remains strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Lead While Services Expand With Deployment Needs

Solutions held 62.44% of the application programming interface security market share in 2025, maintaining its leading position within the component mix. That lead reflects the need for continuous discovery, runtime protection, posture management, and governance across large API estates. The API security market favors solutions that can identify unknown endpoints, monitor live traffic, and surface unusual behavior before misuse escalates into a breach. Behavioral analytics has become more important in 2026 because service-to-service traffic and AI-assisted workflows are harder to judge with static rules alone. Buyers are also placing more weight on workflow features that connect findings to code ownership and remediation, which supports the shift toward broader platform functionality.

Services are projected to grow at a 29.98% CAGR through 2031, underscoring the significant implementation work still surrounding platform adoption. Customers often need support to connect API security tools to gateways, CI/CD workflows, identity controls, and security operations processes across mixed environments. In the API security industry, this service pull is strongest where compliance programs and hybrid estates raise the cost of poor integration. Training and consulting are also becoming increasingly relevant, as many teams still need help with discovery tuning, alert triage, and ownership mapping. Even so, the API security market continues to place the bulk of commercial value in scalable software platforms, while services shape deployment quality and long-term account retention.

By Deployment Mode: Cloud Holds The Lead While Hybrid Gains Ground

Cloud deployment accounted for 58.31% of the application programming interface (API) security market in 2025, making SaaS delivery the largest deployment mode. This position reflects faster rollout, easier updates, and simpler policy distribution in environments where new APIs can appear within hours of a release. The API security market also benefits from cloud delivery because vendors can improve detection models centrally and extend coverage without waiting for local upgrade cycles. At the same time, on-premises deployments remain relevant in regulated settings where local inspection and tighter control over sensitive traffic still matter. That split keeps delivery strategy flexible, because vendors cannot assume that one operating model fits every enterprise.

Hybrid deployment is forecast to grow at a 30.41% CAGR through 2031, which makes it the fastest-growing option in the mix. The API security market size for hybrid environments is expanding because large organizations rarely operate fully in the cloud or fully on premises for long periods. Buyers increasingly want combined control across WAF, DDoS mitigation, bot management, and API security rather than maintaining separate tools for each layer. Harness used that combined approach in Traceable Cloud WAAP, while Cloudflare extended API Shield with active vulnerability scanning to narrow the gap between passive observation and direct exploit testing. Vendors that can support both runtime visibility and developer workflows are likely to capture a larger share of the API security market as customer estates remain mixed through the forecast period.

By Organization Size: Large Enterprises Anchor Spend While SMEs Accelerate

Large enterprises held a 67.82% share of the application programming interface security market in 2025, making them the main spending base for the API security market. Their lead reflects the concentration of endpoint sprawl, regulatory exposure, and operational complexity in organizations running large digital businesses across several regions. These buyers usually need design-time checks, runtime anomaly detection, inventory control, and post-incident visibility in the same operating model. They are also more able to fund managed services and multi-year rollouts that reduce the strain of integration and internal coordination. For that reason, a large share of the current API security market revenue still comes from enterprises with broad estates and strict governance demands.

Small and Medium Enterprises (SMEs) are projected to expand at a 30.23% CAGR through 2031, making them the fastest-growing segment by organization size. Smaller firms now depend on cloud applications, digital payments, and partner integrations in ways that expose them to the same API abuse patterns seen in larger accounts. Many of these firms still lack deep internal security coverage, which makes lightweight SaaS-led discovery and runtime protection more attractive. Vendors are responding with simpler pricing, packaged policies, and lower-touch onboarding, reducing the operational burden for lean teams. The API security industry is well-positioned to benefit from this cohort, as mid-market penetration remains much lower than in the large-enterprise market.

By End-user Industry: BFSI Leads While Healthcare And Life Sciences Advance Fastest

BFSI held 24.13% share of the application programming interface security market in 2025, giving it the largest end-user position in the API security market. Digital banking, payment processing, fraud management, and third-party integrations make financial APIs both commercially critical and highly exposed. PCI DSS 4.0.1 keeps pressure on payment environments to test APIs and tighten access controls, while DORA raises resilience expectations for regulated financial entities and their technology relationships. Authorization weaknesses remain especially important in this segment because attackers often exploit object-level access errors to access customer or transaction data. This combination keeps BFSI central to both compliance-led and breach-led demand across the API security market.

Healthcare and life sciences are projected to grow at a 30.34% CAGR through 2031, making it the fastest-growing vertical in the mix. The February 2026 HIPAA technical safeguard changes heightened the urgency of protecting data that flows through connected healthcare systems and API-linked workflows.[3]Cloudflare, “Active Defense: Introducing a Stateful Vulnerability Scanner for APIs,” Cloudflare, cloudflare.com That change reduces room for delayed investment and pushes providers, payers, and digital health platforms toward stronger runtime and posture controls. Retail, IT and telecom, government, manufacturing, and media and entertainment also contribute significant demand as mobile apps, digital services, and connected operations deepen their reliance on APIs. Even so, healthcare stands out because regulatory pressure and digital integration are rising simultaneously in this part of the API security market.

Geography Analysis

North America held 38.74% of the application programming interface security market share in 2025, maintaining the region's lead. The United States drove most of that position because large enterprises there combine deep cloud adoption with strong compliance pressure from payment and healthcare rules. The region also benefits from a dense vendor base that includes both specialists and platform providers, enabling customers to access mature products and integration partners. Reported incident frequency has kept executive attention high, which supports steady budgets for API discovery, monitoring, and response. This combination of demand maturity, vendor presence, and regulatory pressure gives North America a durable lead in the API security market.

Europe remained a strategically important secondary region for the API security market in 2026. DORA raised the standard for continuous ICT risk management and third-party oversight across regulated financial entities, which directly supports demand for API inventory, monitoring, and control evidence.[4]U.S. Department of Health and Human Services Office for Civil Rights, “HIPAA Security Rule: 2026 Updates to Technical Safeguards,” U.S. Department of Health and Human Services, hhs.gov Regional buyers also place strong weight on auditability and documented operational control, which favors platforms that can connect detection outcomes to governance processes. That keeps European spending focused on consolidated platforms that can manage partner APIs and compliance requirements within a single operating model.

Asia-Pacific is projected to grow at a 30.15% CAGR through 2031, making it the fastest-growing region in the API security market. Akamai found that 93% of surveyed organizations in India and 90% in Singapore reported at least 1 API security incident in the prior year, underscoring how quickly API use has outpaced control maturity. The same research said API security incidents cost Japanese enterprises JPY 246 million (USD 1.71 million) per incident on average, while Chinese respondents were the only group to rank API threat protection as their top cybersecurity priority. This mix of rapid digital growth, high exposure, and stronger executive focus makes Asia-Pacific the most dynamic regional growth engine for the API security market.

Competitive Landscape

The application programming interface security market remained fragmented, with no single vendor controlling the full stack of discovery, runtime protection, posture management, and emerging AI-governance needs. That structure keeps competition active between specialists and broader platform providers. Salt Security, Cequence Security, and 42Crunch compete through depth in behavior-led detection, exposure management, and developer-facing security testing. Akamai and Cloudflare use their larger edge and application security footprints to bundle API controls into broader protection layers. This balance keeps customers from following a single product pattern across the API security market.

Product strategy in 2026 is centered on closing the gap between code ownership, runtime traffic, and exploit testing. Akamai introduced its API Security Posture Center with code-to-runtime mapping in May 2026, linking live APIs to repositories, files, and recent committers to enable remediation to move faster. Cloudflare launched a stateful vulnerability scanner for API Shield in March 2026, adding active BOLA testing to its existing edge-native protection model.[5]European Banking Authority, “Digital Operational Resilience Act (DORA) - Regulatory Technical Standards,” European Banking Authority, eba.europa.eu Harness also positioned Traceable Cloud WAAP as a unified layer for API discovery, runtime threat detection, bot mitigation, and DDoS defense, demonstrating how vendors are moving away from point tools toward integrated platforms.

The next major opening sits around agentic AI and machine-to-machine visibility, where standards and ownership models are still developing. Salt Security said 48.9% of organizations remain completely blind to traffic between AI agents and enterprise systems, leaving a significant monitoring gap in current security operations. Cequence responded in February 2026 with a dedicated security layer for governing agentic AI workflows and enterprise API interactions, while OWASP's GenAI Security Project is formalizing guidance for agentic applications. Vendors that can turn this emerging control area into usable policy, discovery, and runtime enforcement are likely to shape the next phase of the API security market.

Application Programming Interface Security Industry Leaders

Salt Security Inc.

Akamai Technologies Inc.

Cequence Security Inc.

42Crunch Ltd.

Cloudflare Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Akamai introduced its API Security Posture Center and code-to-runtime mapping capability, linking APIs detected in live traffic to the specific code repositories, files, and last committers responsible for their deployment. The update significantly reduces mean time to remediation by eliminating manual ownership tracing and giving developers actionable vulnerability context without requiring security team intermediation.

- March 2026: Cloudflare launched the open beta of its Web and API Vulnerability Scanner for API Shield customers, a stateful Dynamic Application Security Testing (DAST) platform that actively detects Broken Object Level Authorization (BOLA) vulnerabilities by building API call graphs to simulate attacker and owner contexts. The launch marks Cloudflare's entry into the active API vulnerability scanning space, extending its API Shield platform from passive traffic monitoring to proactive exploit simulation.

- April 2025: Following their February 2025 merger announcement, Harness and Traceable launched Traceable Cloud WAAP, the first combined product from the merged entity, integrating API discovery, runtime threat detection, bot mitigation, and DDoS defense into a unified cloud-native platform designed for engineering and security teams operating modern microservices architectures.

- April 2025: Cequence Security unveiled a new security layer to govern and protect agentic AI systems, providing organizations with controls to manage AI gateway traffic, monitor agentic workflows interacting with enterprise APIs, and enforce PCI DSS compliance requirements within AI-driven application environments.

Global Application Programming Interface Security Market Report Scope

The Application Programming Interface Security Market Report is segmented by Component (Solutions, and Services (Implementation and Integration, Training and Consulting, and Support and Maintenance)), Deployment Mode (On-Premises, Cloud, and Hybrid), Organization Size (Small and Medium Enterprises (SMEs), and Large Enterprises), End-user Industry (BFSI, Retail and eCommerce, Healthcare and Life Sciences, IT and Telecom, Government and Public Sector, Manufacturing, Media and Entertainment, and Other End-user Industries), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | |

| Services | Implementation and Integration |

| Training and Consulting | |

| Support and Maintenance |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Retail and eCommerce |

| Healthcare and Life Sciences |

| IT and Telecom |

| Government and Public Sector |

| Manufacturing |

| Media and Entertainment |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Solutions | |

| Services | Implementation and Integration | |

| Training and Consulting | ||

| Support and Maintenance | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-user Industry | BFSI | |

| Retail and eCommerce | ||

| Healthcare and Life Sciences | ||

| IT and Telecom | ||

| Government and Public Sector | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the application programming interface security market size in 2026 and what is the 2031 forecast?

The application programming interface security market stands at USD 1.62 billion in 2026 and is forecast to reach USD 6.02 billion by 2031, growing at a 29.94% CAGR over 2026-2031.

Why is spending on application programming interface protection rising so quickly?

Spending is rising because application programming interfaces have become a primary attack surface, with 87% of surveyed organizations reporting an API-related security incident in 2025 and daily attacks increasing sharply.

Which deployment model leads adoption today?

Cloud leads with 58.31% of revenue in 2025, supported by faster rollout and update cycles, while hybrid is growing fastest at a 30.41% CAGR through 2031.

Which customer group is driving current demand the most?

Large enterprises lead current spending with 67.82% of revenue in 2025 because they manage larger API estates, stronger compliance exposure, and more complex digital operations.

Why is healthcare growing faster than other end-user groups?

Healthcare and life sciences is projected to grow at a 30.34% CAGR through 2031, largely because the 2026 HIPAA technical safeguard changes raised the urgency around protecting connected data flows.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific has the strongest growth outlook with a 30.15% CAGR through 2031, supported by high incident exposure in markets such as India and Singapore and rising executive focus across the region.

Page last updated on: