Legal Bill Review Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

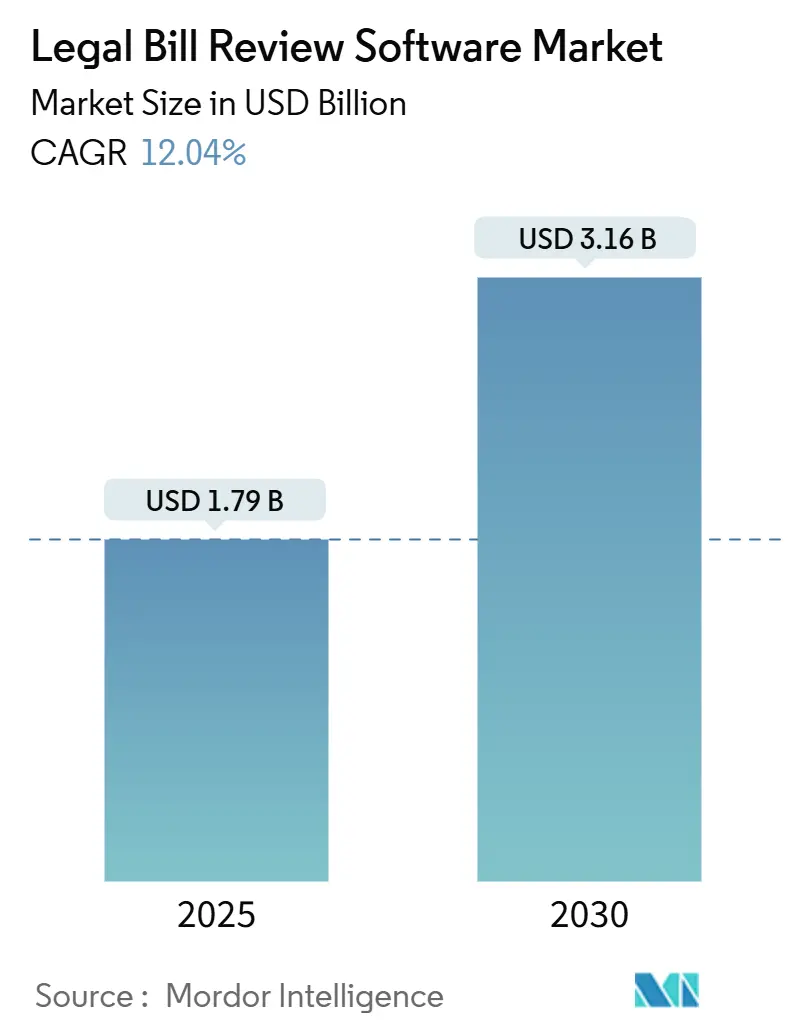

| Market Size (2025) | USD 1.79 Billion |

| Market Size (2030) | USD 3.16 Billion |

| Growth Rate (2025 - 2030) | 12.04% CAGR |

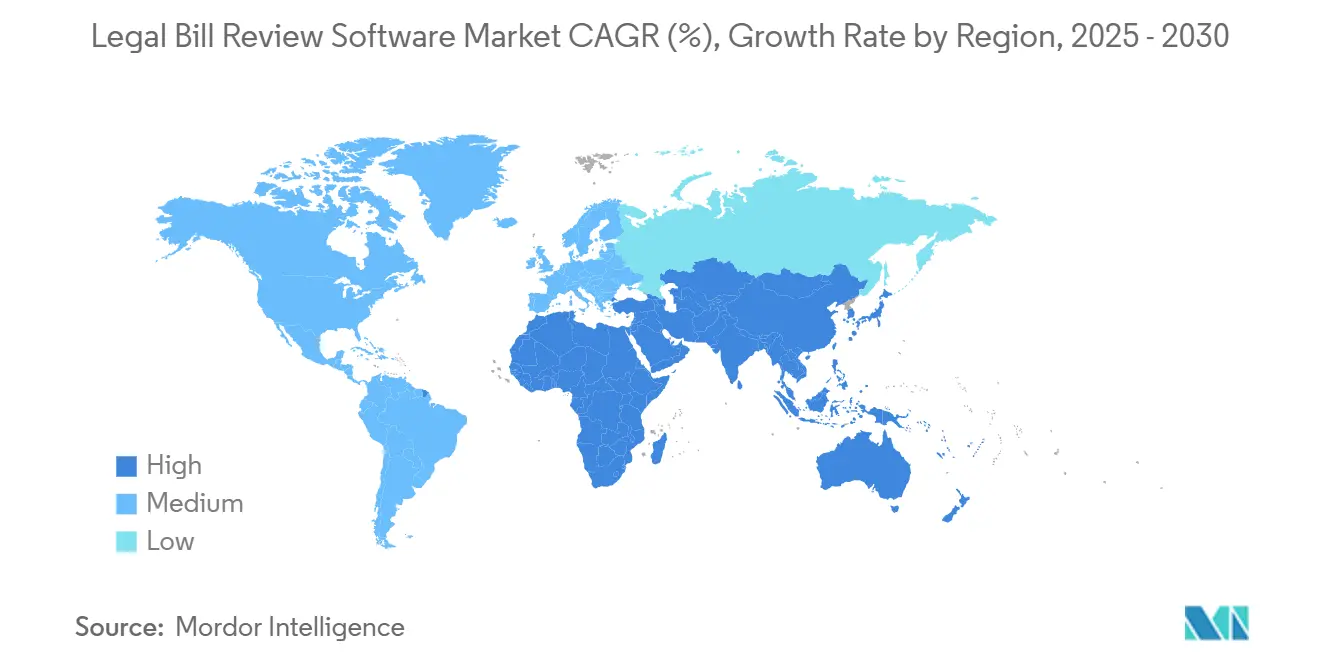

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Legal Bill Review Software Market Analysis by Mordor Intelligence

The legal bill review software market size is USD 1.79 billion in 2025 and is forecast to reach USD 3.16 billion by 2030, growing at a 12.04% CAGR, reflecting the sustained digitization of legal operations and the adoption of analytics-driven spend controls. Demand is accelerating because corporate legal departments seek real-time cost transparency, insurers confront social inflation, and law firms aim to defend margins in competitive procurement processes. Cloud-native architectures, artificial intelligence–powered anomaly detection, and seamless ERP integrations now form the baseline feature set, shifting buyer focus from simple invoice routing to predictive budgeting and performance benchmarking. Vendors that combine secure cloud delivery with configurable workflow engines are profiting from the convergence of e-billing, matter management, and analytics, while niche providers win share through verticalized content such as insurance claims taxonomies. Regional growth patterns favor the Asia Pacific, where emerging corporate legal functions are leapfrogging legacy on-premise systems and embracing subscription models that minimize upfront infrastructure spend.

Key Report Takeaways

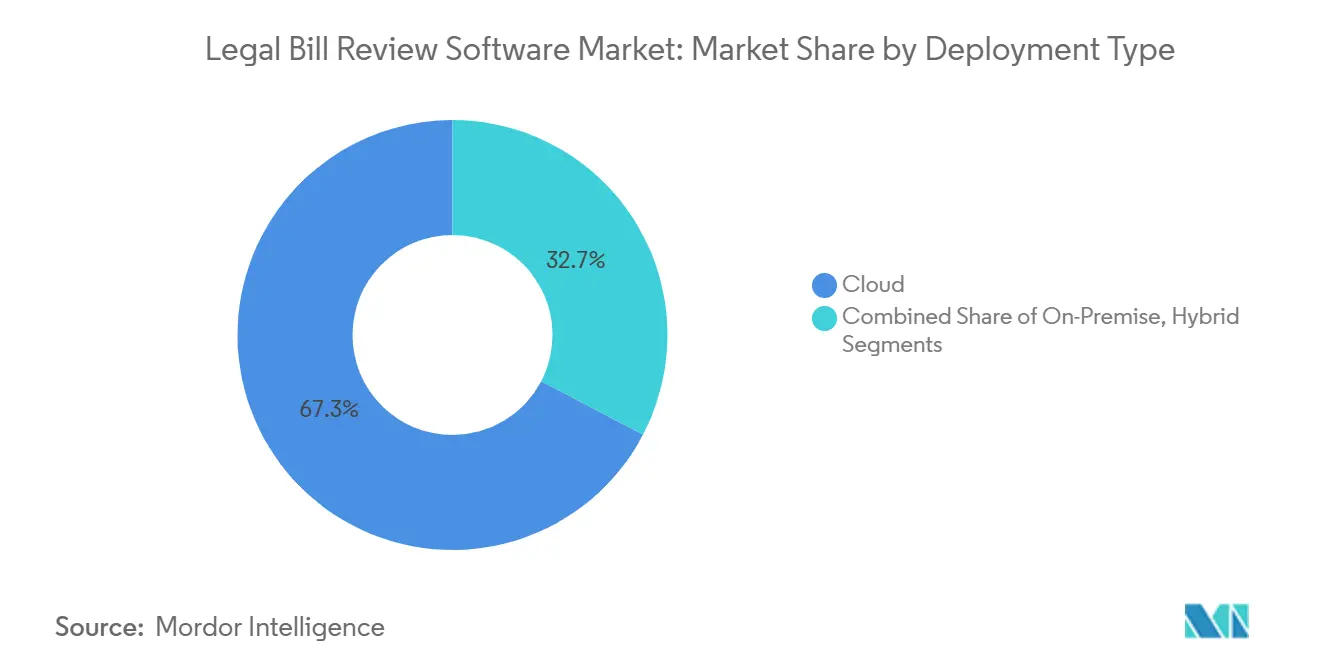

- By deployment type, cloud solutions captured 67.34% of the legal bill review software market share in 2024, while hybrid models were projected to have the highest CAGR at 13.81% through 2030.

- By organization size, large enterprises held a 58.46% share of the legal bill review software market size in 2024, and SMEs are expected to advance at a 12.43% CAGR to 2030.

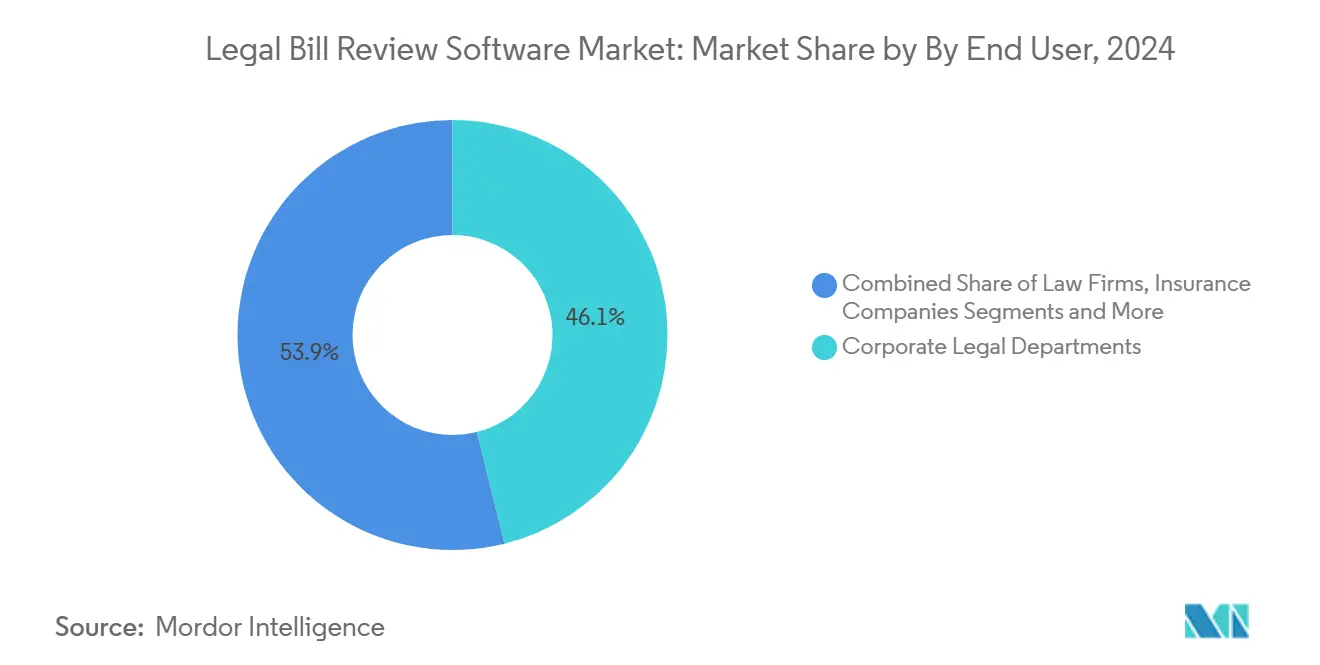

- By end user, corporate legal departments commanded 46.12% of the legal bill review software market share in 2024; meanwhile, insurance companies are projected to expand at a 14.02% CAGR through 2030.

- By application, invoice automation accounted for a 39.28% share of the legal bill review software market size in 2024, and analytics platforms are projected to grow at a 13.61% CAGR from 2024 to 2030.

- By geography, North America retained 41.64% revenue share in 2024, while Asia Pacific is poised for the fastest 12.92% CAGR between 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Legal Bill Review Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating adoption of cloud-native enterprise legal management platforms | +3.20% | Global, North America and Europe lead | Medium term (2-4 years) |

| Increasing pressure on corporate legal departments to control outside counsel spend | +2.80% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Shift toward value-based fee arrangements and AFAs | +2.10% | North America and Europe core, expanding to APAC | Medium term (2-4 years) |

| Integration of AI-powered invoice anomaly detection | +1.90% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Expansion of legal operations functions in mid-market enterprises | +1.40% | North America and Europe, APAC emerging | Medium term (2-4 years) |

| Rising regulatory scrutiny on legal spend transparency | +0.60% | Europe and North America, global spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Cloud-Native Enterprise Legal Management Platforms

Cloud-based legal technology now underpins remote collaboration, always-current software builds, and elastic compute that handles invoice volumes surging during litigation spikes. Three-quarters of global law firms are migrating their core billing processes to software-as-a-service (SaaS), citing lower infrastructure costs and easier integration with modern finance stacks. Top-tier firms prioritize cloud connectors that unify matter data, spend dashboards, and predictive alerts in a single interface, enabling partners to manage client budgets in real time. Rich API ecosystems facilitate plug-ins for contract review, compliance screening, and vendor portals, thereby enhancing the market appeal of legal bill review software among CIOs who prefer platforms over point tools. As machine learning models require large training datasets and ongoing version updates, cloud architectures deliver the scale and continuous improvement cycles necessary for accurate forecasting, thereby reducing the total cost of ownership compared to on-premise installations. The shift also accelerates global rollouts because new jurisdictions can be activated with tenant-level configurations, rather than requiring physical servers.

Increasing Pressure on Corporate Legal Departments to Control Outside Counsel Spend

Board-level scrutiny has intensified since 2024 as finance chiefs benchmark legal cost growth against company-wide cost-containment programs. Nearly nine in ten departments face mandates to keep law-firm invoices flat despite rising matter complexity, propelling adoption of automated validation engines that flag block billing, excessive partner hours, and unapproved disbursements. Early adopters documented double-digit savings in year one, predominantly through reversal of billing errors exposed by AI models cross-referencing rate cards and historical matter budgets. Real-time dashboards now surface variance alerts that legal operations teams can act on before invoices hit accounts payable, eliminating the lag that historically led to write-offs at quarter-end. Outside counsel guidelines have become more granular, embedding narrative conventions and task-based billing codes that software enforces automatically. The resulting transparency strengthens procurement negotiations and supports alternative fee pilots because accurate baselines exist for scoping fixed-price engagements.

Shift Toward Value-Based Fee Arrangements and AFAs

Growth in fixed, success-based, and blended-rate deals reached a tipping point in 2024, with 65% of Fortune 500 legal departments reporting more AFAs than hourly mandates for routine work. Sophisticated billing engines now allocate flat fees across phases, attach outcome metrics, and calculate performance bonuses when milestones are met. Law firms that integrate AFA tracking within standard time-entry tools report higher client satisfaction and stable margins, proving the model’s viability.[1]American Bar Association. "Legal Technology Survey 2024", americanbar.org Accurate data capture is critical; software must reconcile negotiated caps with actual resourcing, apportion shadow rates, and surface profitability analytics to partners. Corporate buyers leverage this insight to fine-tune scopes and shift matters to firms with superior value delivery scores, reinforcing competition on efficiency rather than hours. Regulatory agencies that oversee public companies increasingly request AFA disclosures, giving compliant departments a reputational edge.

Integration of AI-Powered Invoice Anomaly Detection

Natural language processing now parses narrative blocks to flag vague descriptors, detect duplicate tasks, and highlight noncompliant travel charges at scale. Machine learning baselines attorney behavior across thousands of matters, spotting deviations such as partner-level hours on clerical tasks. Vendors claim 60% reductions in human review time, converting paralegal resources into higher-value analytics roles. Predictive modules simulate matter costs based on historical patterns, alerting lawyers when budgets will burst before it happens. Insurers integrate these predictions with claims systems to allocate reserves earlier, improving combined ratios and capital planning. Continuous learning loops retrain models with every correction logged, so detection accuracy improves over time without manual rule maintenance. As AI explainability advances, audit teams and regulators gain confidence in algorithmic decisions, addressing earlier skepticism about black-box risk scoring.

Data Security Concerns Around Sharing Confidential Billing Data

High-profile ransomware attacks in 2024 exposed sensitive invoice repositories, galvanizing risk-averse firms to re-evaluate cloud migrations. Legal ethics rules obligate attorneys to validate vendor safeguards, so providers invest in zero-knowledge encryption, data localization, and SOC 2 Type II certifications to reassure buyers. European customers demand explicit GDPR compliance clauses that cover breach notification windows, audit trails, and data subject rights. Encryption-in-use technologies and private-cloud deployments mitigate apprehension among national-security and pharma clients. Insurers underwrite cyber policies contingent on verified security controls, making certification a competitive necessity. Although concerns slow decisions in the short term, independent penetration testing reports and transparent security roadmaps are reducing buyer friction, especially when budgets already earmark legacy hardware upgrades that can instead fund secure SaaS subscriptions.

Resistance to Change Among Traditional Law Firms

Partnership structures concentrate control among senior lawyers who perfected manual processes and fear that billing transparency will erode leverage with clients. Smaller practices often lack in-house IT talent, which magnifies concerns about configuration complexity. Implementation success stories emphasize phased roll-outs, clear KPI targets, and financial incentives that align partner compensation with adoption milestones. Vendors now pre-configure best-practice rule libraries to shorten go-live cycles to weeks, countering the narrative of lengthy disruptions. Younger associates are championing automation to eliminate late-night invoice reviews and redirect effort toward substantive legal analysis, slowly shifting the firm culture. Educational programs by bar associations and legal technology forums provide templates, checklists, and CLE credits, lowering the perceived learning curve. As marquee firms tout efficiency gains in client pitches, competitive pressure mounts on holdouts to modernize or risk being excluded from panels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Accelerates Integration

The cloud segment accounted for 67.34% of the legal bill review software market revenue in 2024, underscoring its position as the preferred deployment model for new projects. Within the legal bill review software market, cloud platforms are projected to post a 13.81% CAGR, widening their lead as organizations retire aging on-premise modules in favor of subscription pricing and elastic scaling. Early movers cite faster implementation cycles, automatic feature upgrades, and built-in disaster recovery as key advantages, particularly for law firms expanding their cross-border client teams. Hybrid approaches remain relevant where data sovereignty or air-gapped archives are mandatory; vendors respond with region-based tenancy and on-premise gateways that cache sensitive attachments locally while analytics engines operate in the cloud. Advanced API frameworks enable single sign-on, finance-system synchronization, and contract lifecycle triggers, creating an integrated legal spend command center.

Cloud penetration also advances AI maturity because algorithms train on aggregated, anonymized datasets drawn from multitenant traffic, producing robust anomaly libraries and benchmark fee curves. As predictive modules improve, purchasing committees weigh the cost of lagging behind peers who exploit superior forecasting accuracy. On-premise environments still attract government agencies handling classified matters, yet even those buyers increasingly embrace private-cloud blueprints inside sovereign data centers. Regional regulation shapes demand; European projects often start with hybrid proofs-of-concept to satisfy GDPR auditors before migrating more workloads. Over the forecast period, falling cloud unit costs and carbon-neutral data center commitments strengthen the environmental, social, and governance narrative for cloud adoption, reinforcing its trajectory toward market dominance.

By Organization Size: SMEs Drive Democratization

Large enterprises historically dictated feature roadmaps and negotiated enterprise license agreements, culminating in their 58.46% contribution to 2024 revenue. These corporations embed the legal bill review software market share within broader spend-management programs that integrate procurement, accounts payable, and vendor risk modules. However, the fastest expansion occurs among SMEs, where a 12.43% CAGR narrows the functionality gap as user-experience-oriented vendors launch tiered packages with guided onboarding. Subscription models calibrated to invoice volume eliminate steep upfront fees, allowing finance controllers at mid-market manufacturers, tech startups, and regional insurers to pilot enterprise-grade analytics without incurring capital outlay.

The democratization trend aligns with the rise of fractional general counsel services, where external lawyers manage legal operations for multiple SMEs and demand intuitive bill review dashboards accessible from mobile devices. Product-led growth tactics-such as self-service trials, transparent pricing pages, and in-app tutorials-accelerate viral adoption, while marketplaces featuring plug-and-play connectors remove integration obstacles that were once exclusive to large IT teams. As SME case studies showcase 15% cost reductions and faster accrual reporting, board members increasingly view bill review tools as essential controls rather than discretionary upgrades, ensuring sustained category penetration.

By End User: Insurance Sector Emerges as Growth Leader

Corporate legal departments remain the largest constituency with 46.12% market share, leveraging platforms to align legal spend with enterprise performance metrics and Sarbanes-Oxley audit requirements.[2]Wolters Kluwer, “CCH Axcess Legal Technology Platform,” wolterskluwer.com Yet insurers set the growth pace, clocking a 14.02% CAGR as claims inflation pressures force granular tracking of attorney costs by policy line, claimant demographics, and jurisdiction. Legal bill review software market size continues to expand within carriers that process tens of thousands of panel counsel invoices monthly, making automation indispensable for reserve accuracy and compliance with Department of Insurance guidelines.

Insurers prioritize rules engines tuned to industry-specific litigation codes and integrate outputs with core claims platforms to trigger predictive reserve adjustments. Corporate buyers in other verticals, such as healthcare and financial services, emulate these workflows to meet regulatory demands for transparency in fee recovery and patient settlement disputes. Law firms embrace embedded portals that expose matter budgets and guideline compliance statistics to clients, reinforcing collaborative cost controls that differentiate firms during panel reviews. Government agencies lag but show incremental adoption as public accountability initiatives gather momentum.

By Application: Analytics Reshape Spend Management

Invoice automation retained 39.28% revenue in 2024, illustrating that digital ingestion, LEDES validation, and task-code enforcement remain entry-level necessities. However, analytics and reporting applications outpace all others with a 13.61% CAGR, reflecting a strategic pivot toward value-oriented insights rather than clerical efficiency alone. The legal bill review software market size for predictive analytics is swelling because finance leaders demand scenario modeling that quantifies budget impact under different staffing assumptions or settlement pathways.

Modern suites bundle matter-level dashboards, cohort benchmarks, and trend visualizations that expose fee drivers and inform RFP scoring for panel counsel. Compliance management modules are escalating as jurisdictions legislate for transparency, requiring statutory data points to be embedded in invoice objects for automated audit export. Budget forecasting engines meld historical invoice data with machine learning to estimate burn rates and suggest fee arrangements likely to cap exposure. As AI-feedback loops iterate, accuracy climbs, encouraging risk-averse departments to shift more spend under proactive management rather than post-hoc audits.

Geography Analysis

North America contributed 41.64% of 2024 revenue, anchored by sophisticated legal operations, SEC reporting obligations, and a dense vendor ecosystem that lowers implementation risk. U.S. corporations embed bill review metrics into enterprise performance dashboards, while Canadian enterprises leverage bilingual interfaces to manage cross-border matters. Cloud readiness and aggressive procurement ensure technology refresh cycles every three to five years, sustaining replacement demand even as the installed base matures.

Europe remains pivotal as the GDPR and ESG frameworks intensify requirements for spend transparency and audit trails, prompting upgrades to systems that provide granular access controls and immutable logs.[3]European Commission, “GDPR Compliance Requirements,” ec.europa.eu Currency fluctuations post-Brexit heighten interest in multi-currency billing engines that calculate matter costs in GBP and EUR simultaneously, supporting consolidated reporting for multinational corporations. Vendor competition focuses on localized support and data residency assurances to navigate the continent’s heterogeneous data-sovereignty mandates.

The Asia Pacific registers the fastest 12.92% CAGR because emerging economies are fast-tracking digital legal infrastructures, and multinational companies are extending shared-services hubs into Singapore, Bangalore, and Manila. Early adopters in Japan and Australia promote region-wide standards that streamline cross-border invoice exchange, while Chinese and Indian conglomerates prioritize AI spend forecasting to curb rapidly rising litigation costs. Government digital-court programs create ancillary demand for billing data that feeds analytics on case durations and outcome probabilities, positioning bill review platforms as integral to judicial modernization.

Competitive Landscape

The market remains moderately fragmented. ProfitSolv’s USD 1 billion sale showcased the premium placed on scale and cross-sell potential. Strategic acquirers, such as Mitratech and Wolters Kluwer, pursue tuck-ins that provide workflow automation or facilitate mid-market entry, while private-equity-backed challengers fund AI research to leapfrog incumbents. Vendors differentiate via native ERP connectors, ISO 27001 certifications, and proprietary benchmark datasets that underpin pricing negotiations.

Partnerships with hyperscalers unlock advanced AI accelerators and regional data centers, addressing both performance and sovereignty concerns. Competitive pressure drives transparent roadmaps, with quarterly releases adding features like voice-activated invoice capture or ESG spend tagging.

Vertical specialization emerges as a hedge against commoditization; insurers seek litigation-code taxonomies, while public-sector buyers demand procurement-grade audit logs. Price competition remains contained because switching costs are material once complex approval workflows are embedded in adjacent systems.

Legal Bill Review Software Industry Leaders

-

Wolters Kluwer N.V.

-

Mitratech Holdings Inc.

-

Brightflag Inc.

-

Onit Inc.

-

LexisNexis Legal and Professional (RELX PLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Thomson Reuters expanded Legal Tracker with predictive budget forecasting and automated AFA optimization after investing USD 25 million in machine-learning infrastructure.

- January 2025: Wolters Kluwer acquired a mid-market legal operations vendor for USD 150 million to augment SME functionality.

- October 2024: Wolters Kluwer rolled out AI anomaly detection and spend analytics upgrades within CCH Axcess, a USD 15 million R&D initiative.

- September 2024: Mitratech purchased CounselGO, adding AFA management and compliance dashboards to its suite.

Global Legal Bill Review Software Market Report Scope

| Cloud |

| On-Premise |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Law Firms |

| Corporate Legal Departments |

| Government and Public Sector |

| Insurance Companies |

| Other End User |

| Invoice Processing Automation |

| Spend Management |

| Compliance Management |

| Budget Forecasting |

| Analytics and Reporting |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Type | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End User | Law Firms | |

| Corporate Legal Departments | ||

| Government and Public Sector | ||

| Insurance Companies | ||

| Other End User | ||

| By Application | Invoice Processing Automation | |

| Spend Management | ||

| Compliance Management | ||

| Budget Forecasting | ||

| Analytics and Reporting | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of legal bill review software in 2030?

Market value is forecast to reach USD 3.16 billion by 2030, growing at a 12.04% CAGR.

Which deployment model is expected to dominate future purchases?

Cloud platforms are projected to widen their lead, already holding 67.34% share in 2024 and expanding at 13.81% CAGR.

Why are insurance companies adopting legal bill review tools quickly?

Social inflation and claims-management scrutiny drive the sector’s 14.02% CAGR as carriers need granular cost analytics across jurisdictions.

How does AI improve legal bill review accuracy?

Machine-learning models identify duplicate charges and non-compliant entries, trimming manual review effort by up to 60% while boosting error detection.

What is the biggest restraint on market growth?

Data-security fears around cloud storage of confidential billing information remain the primary headwind, especially in Europe and North America.

Which region offers the fastest expansion opportunity?

Asia Pacific is set for a 12.92% CAGR as corporations digitize legal services and adopt alternative fee arrangements.

Page last updated on: