Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Inventory Management Software Market is Segmented by by Deployment (On-Premise and Cloud), End-User Enterprise Size (Large Enterprises and Small and Medium Enterprises (SME)), Application (Order Management, Inventory Control and Tracking, and More), End-Use Industry (Manufacturing, Retail and E-Commerce, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

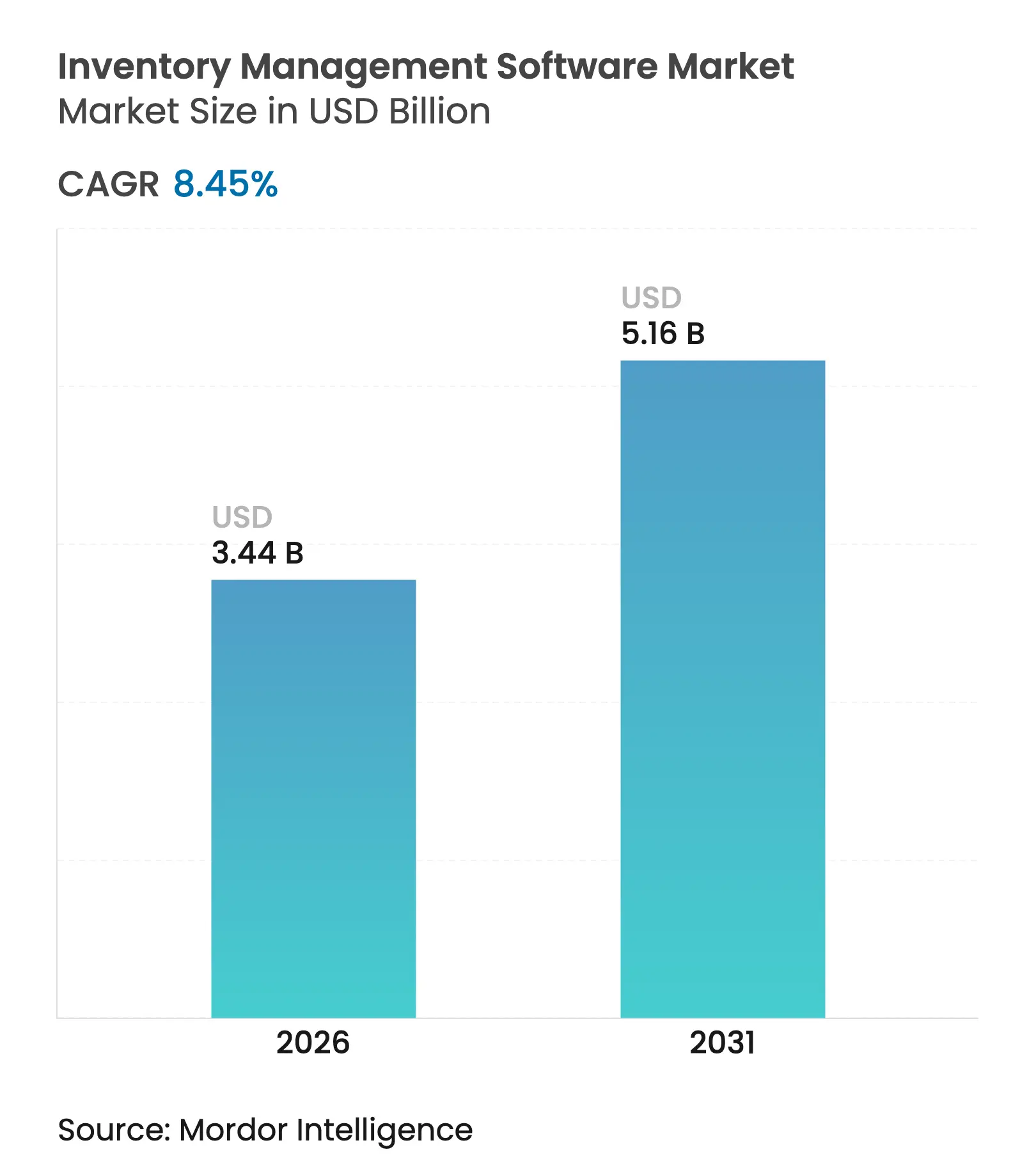

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 5.16 Billion |

| Growth Rate (2026 - 2031) | 8.45 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

inventory management software market size in 2026 is estimated at USD 3.44 billion, growing from 2025 value of USD 3.17 billion with 2031 projections showing USD 5.16 billion, growing at 8.45% CAGR over 2026-2031. Strong demand for real-time stock visibility, AI-enhanced demand forecasting, and cloud-native deployment are reshaping competitive dynamics, turning inventory control into a board-level priority. Regulatory pressures in pharmaceuticals and food safety, together with rising omnichannel fulfillment expectations, accelerate adoption across both mature and emerging economies. Vendors are embedding IoT, RFID, and machine-learning models directly into platforms, allowing enterprises to move from reactive to predictive inventory practices. Mid-market firms are closing functionality gaps with large enterprises by choosing subscription-based suites that integrate easily with e-commerce, finance, and logistics applications.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Real-time

tracking demand in e-commerce and retail

Real-time

tracking demand in e-commerce and retail

| +2.1% | North America, Europe (global spillover) | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

North

America, Europe (global spillover)

|

Impact Timeline

:

Short

term (≤ 2 years)

|

Cloud

migration momentum among SMEs

Cloud

migration momentum among SMEs

| +1.8% | Global with Asia-Pacific acceleration | Medium term (2-4 years) | |||

AI-driven

demand-forecast integration

AI-driven

demand-forecast integration

| +1.5% | North America, EU leadership | Medium term (2-4 years) | |||

Omnichannel

and micro-fulfillment expansion

Omnichannel

and micro-fulfillment expansion

| +1.3% | Urban centers worldwide | Short term (≤ 2 years) | |||

Serialized

tracking compliance in pharma and food

Serialized

tracking compliance in pharma and food

| +1.0% | North America, EU, widening to Asia-Pacific | Long term (≥ 4 years) | |||

Plug-and-play

APIs for vertical SaaS

Plug-and-play

APIs for vertical SaaS

| +0.9% | Tech-forward markets | Short term (≤ 2 years) | |||

Real-time

tracking demand in e-commerce and retail

Real-time

tracking demand in e-commerce and retail

| +2.1% | North America, Europe (global spillover) | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Growing demand for real-time inventory tracking and automation in e-commerce/retail

Retailers now target 99% stock-accuracy thresholds because any channel mismatch erodes customer loyalty and revenue. RFID tags, smart shelves, and IoT gateways push millisecond-level stock updates to order-management engines, eliminating manual cycle counts and avoiding out-of-stocks. PackageX reports that omnichannel merchants deploying end-to-end RFID capture raised accuracy by 15 percentage points during 2025, with fulfillment latency dropping below two hours for same-day delivery promises.[1]PackageX, “Inventory Accuracy and RFID Adoption 2025,” packagex.com Academy Sports + Outdoors strengthened this case by recording a 20% increase in inventory accuracy after rolling out handheld RFID scanners across core product lines. The resulting data clarity fuels AI modules that trigger dynamic reorder points, smart substitutions, and markdown optimization, keeping working capital lean while safeguarding service levels. Early adopters thus gain a defensible advantage, which in turn drives faster license renewals and expansion deals for software vendors in the inventory management software market.

Rapid cloud migration among SMEs for cost flexibility

Subscription pricing, automatic upgrades, and elastic compute make cloud suites particularly attractive for cash-constrained SMEs. These firms cut capital budgets, reallocate staff from maintenance work, and tap pre-built integrations to marketplaces and carriers. O2b Technologies observes that SME inquiries for SaaS inventory solutions grew 34% year-on-year in 2024, driven by surging cross-border e-commerce. Oracle echoed this trend, disclosing 21% growth in quarterly cloud ERP revenue to USD 5.6 billion, with many wins tied to mid-market brands upgrading from spreadsheets.[2]Oracle Corporation, “Fiscal 2025 Annual Report,” oracle.com Cloud adoption also shortens implementation cycles from months to weeks, letting smaller firms react to demand peaks without costly over-provisioning. As SMEs scale internationally, multi-subsidiary ledgers and multi-currency inventory layers can be switched on instantly, removing prior growth bottlenecks. This momentum propels the inventory management software market toward double-digit expansion through 2030.

Integration of AI-driven demand-forecast engines into inventory suites

Machine-learning algorithms parse point-of-sale feeds, weather trends, promotions, and social chatter, raising forecast accuracy by up to 50% relative to moving-average models. Microsoft embedded Copilot inside Dynamics 365 Supply Chain Management so planners can ask plain-language questions such as “What is the next-week forecast for SKU-123 in Dallas?” and receive contextual demand curves in seconds.[3]Microsoft, “Copilot in Dynamics 365 Supply Chain Management,” microsoft.com Improved foresight means leaner safety stocks, reduced obsolescence, and fewer expedited shipments. AI agents now also recommend supplier reallocations when lead-time variance spikes, further trimming working-capital exposure. Vendors that bundle native AI gain pricing power and higher customer retention because switching away would sacrifice hard-won accuracy gains. The technology therefore exerts a structural push on the inventory management software market toward predictive, self-tuning workflows.

Expansion of omnichannel fulfillment and micro-fulfillment centres

Urban delivery promises under one hour are rewriting network design. Retailers deploy compact, automated micro-fulfillment centres that slot behind stores or in suburban hubs, stocking high-velocity items within reach of dense populations. Swisslog estimates that automated micro-sites can cut last-mile costs by 30% while slashing delivery miles. Inventory software must orchestrate thousands of SKUs across dozens of nodes, recalculating ATP (available-to-promise) every few minutes. Rule-based allocation engines push orders to the closest location, while robotic storage systems feed pick stations without human hand-offs. As adoption spreads, real-time connection between store shelves, dark stores, and carriers becomes mandatory, spurring upgrades from batch-driven legacy systems. Consequently, omnichannel dynamics continue to lift software licence growth, particularly within grocery, apparel, and specialty retail segments of the inventory management software market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High

switching costs from legacy ERP systems

High

switching costs from legacy ERP systems

| −1.2% | Global enterprises | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

−1.2%

|

Geographic Relevance

:

Global

enterprises

|

Impact Timeline

:

Long

term (≥ 4 years)

|

Cyber-security

and data-sovereignty concerns

Cyber-security

and data-sovereignty concerns

| −0.8% | EU and regulated sectors worldwide | Medium term (2-4 years) | |||

Interoperability

gaps across multi-channel commerce platforms

Interoperability

gaps across multi-channel commerce platforms

| −0.6% | Global omnichannel retailers | Short term (≤ 2 years) | |||

Shortage

of domain-skilled implementation partners

Shortage

of domain-skilled implementation partners

| −0.4% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High switching costs from legacy ERP systems

Enterprises running highly customized ERP stacks confront multi-million-dollar migration budgets covering data cleansing, custom code rewrites, and workforce training. SAP notes that some global manufacturers allocate up to 3% of annual IT spend solely to keep older versions patched, yet still hesitate to re-platform because any outage could stall production. A North American apparel firm ultimately cut processing time by 75% after a phased Microsoft modernization, but only following two years of dual-running and intense change-management investments. Such hurdles slow decision cycles and defer cloud deals, dragging on the overall growth trajectory of the inventory management software market.

Cyber-security and data-sovereignty concerns with cloud deployments

European regulators enforce strict residency rules under GDPR, prompting firms to favour regional providers such as Evroc and Ionos over US hyperscalers. BBC News reports that several public-sector agencies migrated workloads locally in 2024 to satisfy data-parliament audits. Healthcare networks weigh HIPAA compliance alongside ransomware risk, sometimes choosing hybrid models that keep patient identifiers on-premises while leaving less-sensitive catalog data in public clouds. These compliance intricacies add architectural complexity and sometimes tip cost-benefit analyses back in favour of incremental upgrades, tempering near-term addressable demand.

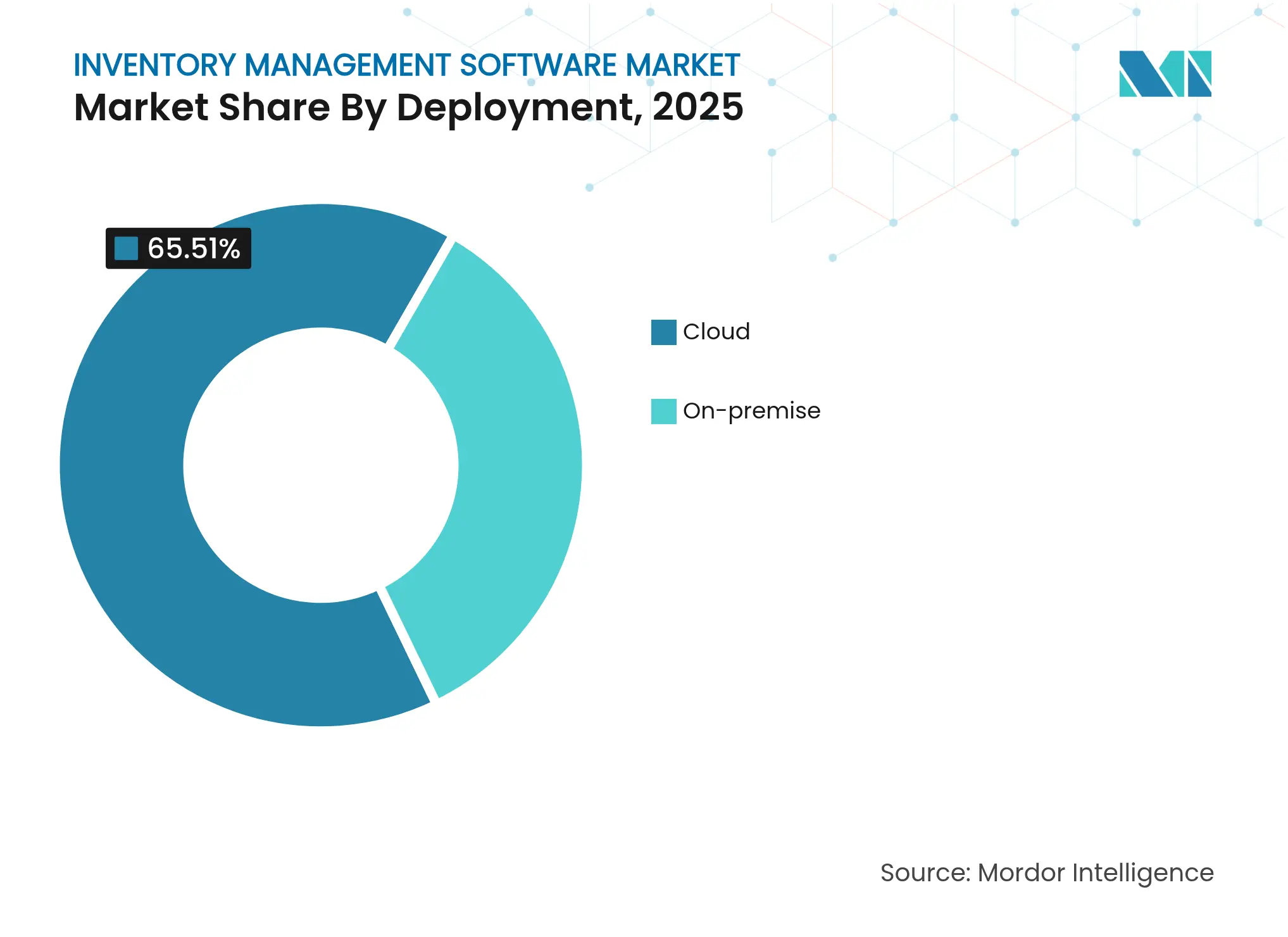

By Deployment: Cloud dominance accelerates digital transformation

Cloud solutions generated 65.51% of 2025 revenue, illustrating clear buyer confidence in subscription models. This slice of the inventory management software market is growing the fastest, with a 13.85% CAGR as enterprises prioritize scalability, zero-downtime upgrades, and embedded analytics. Oracle’s infrastructure services alone added USD 44 billion in 2025, evidencing the capital flowing into hyperscale backbones. On-premises installations persist where data-residency rules are strict, yet many of these environments are retrofitting with cloud gateways for AI inference and external partner connectivity. The inventory management software market size for hybrid deployments is expected to see upper-single-digit growth because regulated operators value a phased path that balances compliance with innovation. Movement toward cloud also signals a governance reset: finance, warehousing, and commerce functions converge on unified data models, erasing silos that historically frustrated planners. Multi-tenant architectures allow vendors to push weekly code drops containing AI micro-services, RFID drivers, and compliance updates without downtime. Cost predictability further lures CFOs because fees track usage, not peak hardware forecasts. This adoption curve underpins sustained momentum in the inventory management software market over the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

By Enterprise Size: SMEs drive growth through accessibility

Large enterprises retained 56.12% share in 2025 because they operate vast SKU catalogs and complex global networks. Yet SMEs are expanding at 13.12% CAGR, the highest pace within the inventory management software market, as user-friendly SaaS packages replace spreadsheets. NetSuite’s modular plans illustrate this democratization; mid-market brands can activate finance, inventory, and fulfilment modules sequentially, aligning spend with growth milestones SMEs often lack dedicated IT teams, making vendor-managed security patches and automatic backups decisive. API marketplaces let merchants connect point-of-sale, last-mile carriers, and pay-wall solutions in days rather than months. As cross-border sales increase, SMEs rely on real-time landed-cost engines inside inventory platforms to avoid margin erosion. Continuous SME onboarding therefore remains a material revenue engine inside the wider inventory management software market.

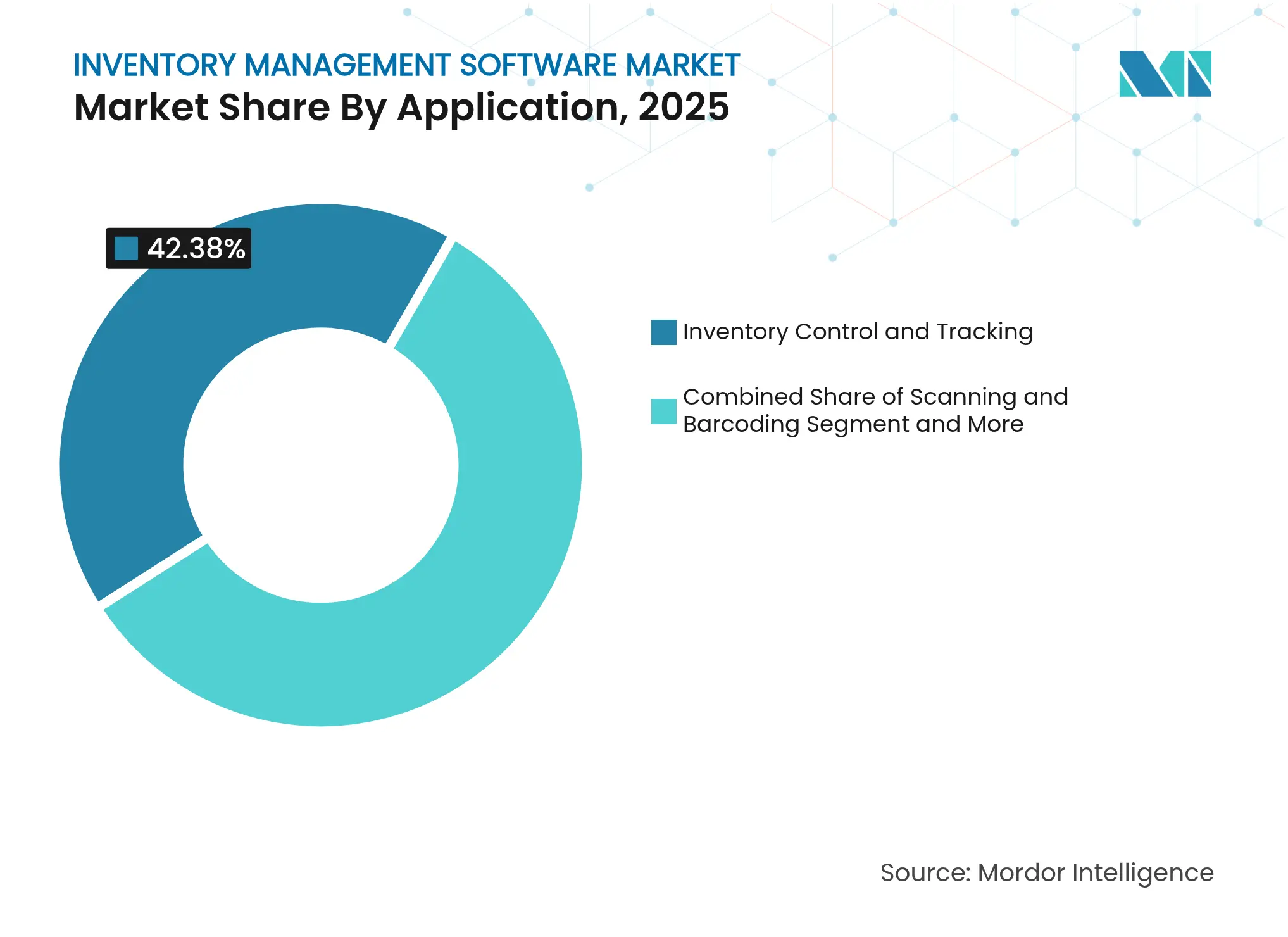

By Application: Scanning and barcoding technologies lead innovation

Inventory control and tracking remained the largest application segment, securing 42.38% revenue share in 2025. This core function anchors every deployment and often acts as the initial beachhead before customers layer on analytics and omni-fulfilment modules. Meanwhile, scanning and barcoding posted a 14.58% CAGR outlook, the quickest among application tiers, thanks to cost-effective RFID inlays, smartphone-based scanners, and smart label printers. These tools collapse manual entry time and drive the shift toward touchless receiving docks, particularly within apparel, electronics, and grocery verticals. The inventory management software market share for advanced vision-based scanning is set to widen as 2D imagers and AI-driven defect detection become affordable. Order-management engines leverage the resultant clean data to promise accurate delivery dates and reduce split shipments. Vendors that wrap scanning, inventory, and warehouse execution inside a single UI gain competitive stickiness, lowering integration hurdles for customers. Thus, application innovation loops back to reinforce top-line growth across the inventory management software market.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Healthcare compliance drives accelerated adoption

Retail and e-commerce continued to dominate with 30.36% of 2025 revenue, reflecting intense SKU variability and short product lifecycles. Yet healthcare will see the steepest climb at 14.19% CAGR, propelled by the Drug Supply Chain Security Act and looming FSMA 204 traceability deadlines. The inventory management software market size tied to healthcare is forecast to exceed USD 707.3 million by 2031, underpinned by requirements for unit-level serialization, temperature monitoring, and recall readiness. Pharma distributors now embed blockchain-backed pedigree verification inside inventory flows to meet audit protocols. Food and beverage processors also accelerate spending as regulators push granular ingredient tracing. Manufacturing firms integrate production planning and inventory on one ledger to eliminate blind spots that can halt lines. Logistics providers, in turn, invest in real-time inventory visibility layers to support same-day freight reallocation when disruptions strike. Together, these industry vectors amplify software bookings and diversify revenue streams in the inventory management software market.

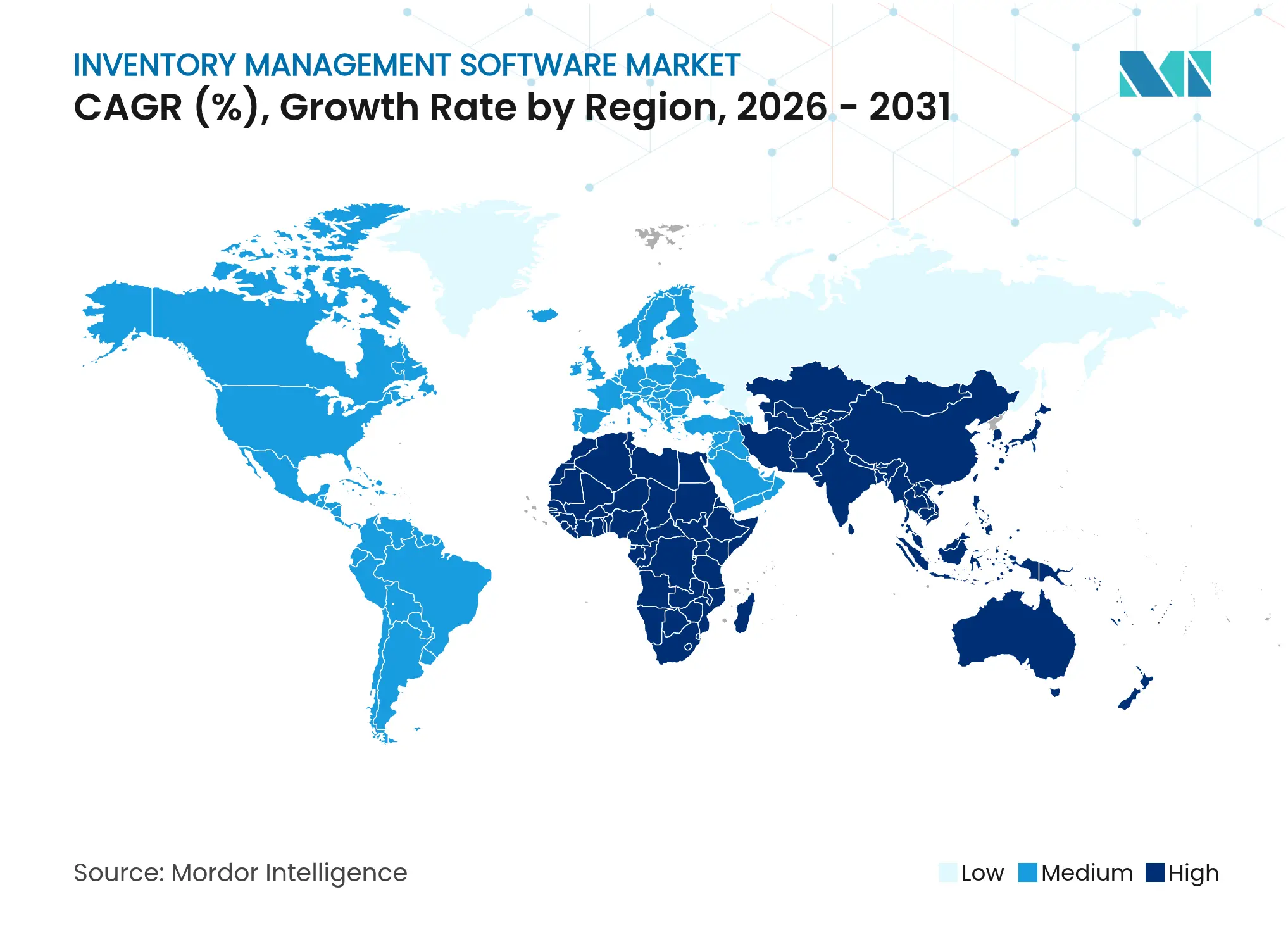

North America delivered 38.51% of 2025 global revenue, supported by robust digital infrastructure and well-established regulatory mandates such as the Drug Supply Chain Security Act that require serialized drug tracing from plant to patient hhs.gov. Cloud penetration is already above 70% among tier-one retailers, so incremental growth pivots on AI upgrades, edge-IoT rollouts, and multimodal fulfilment orchestration. Vendors differentiate through government-grade security certifications and deep integrations with bonded warehouse systems that handle cross-border returns.Asia-Pacific is the growth engine, charting a 15.74% CAGR as warehouse operators commit to next-generation automation. Zebra Technologies’ 2023 study found that more than 90% of the Asia-Pacific respondents plan to raise robotics spending before 2027, compared with 70% in North America. China scales micro-fulfilment nodes in mega-cities, while India’s D2C brands deploy pay-as-you-go SaaS suites to manage rising order volumes. Skills shortages remain, but government incentives for smart factories and logistics corridors are improving partner ecosystems, propelling regional uptake of inventory management software market solutions.Europe maintains steady mid-single-digit expansion, anchored by data-sovereignty statutes that influence vendor selection. BBC News highlights public-sector pilots migrating to European-owned clouds to preserve legal control over citizen data, a trend spilling into private industry. Brexit-induced customs complexity further raises the need for multi-jurisdictional inventory visibility, nudging exporters toward platforms that automate tariff codes and documentary compliance. Latin America and Africa start from smaller bases yet show promise as retailers leapfrog directly to cloud, circumventing on-premises legacies. However, limited bandwidth, fragmented last-mile carrier networks, and fewer certified partners temper near-term rollout speed.

Market Concentration

The inventory management software market is moderately fragmented but trending toward consolidation as deep-pocketed platform vendors pursue tuck-in deals. IBM’s announced purchase of Accelalpha and Applications Software Technology LLC expands its Oracle consulting bench, enabling larger transformation contracts in public-sector and logistics domains. Veralto’s USD 350 million buyout of TraceGains strengthens traceability and compliance depth in food and beverage, areas where mid-tier ERPs often struggle. Oracle’s USD 57.4 billion fiscal-2025 revenue, with cloud services up 12%, equips the firm to embed AI copilots and low-code extension tools directly into its inventory workflows, tempting existing ERP customers to stay on-platform.

Specialist vendors compete by blending vertical expertise with rapid feature shipping. Manhattan Associates secured the 2024 SupplyTech Breakthrough Award for its yard-management module that synchronizes dock appointments with inventory availability, shaving average trailer dwell time by 19%. Fishbowl, Cin7, and DEAR Systems target high-growth brands needing multi-channel inventory orchestration without enterprise-grade overhead. Integration-platform-as-a-service providers such as Celigo and Boomi also gain relevance because they bridge disparate commerce, finance, and warehouse systems, speeding data flow between ecosystems.

Generative AI is fast becoming a battleground. Early pilots show that conversational planning assistants cut forecast cycle time by 30% while raising planner adoption rates. Vendors embedding explainable AI, strong data-provenance controls, and industry-specific ontologies will likely capture disproportionate share. Meanwhile, customers insist on open standards to avoid lock-in, pressuring suppliers to expose RESTful APIs and event streams. The interplay of innovation velocity and acquisition appetite will define competitive hierarchies over the next five years within the inventory management software market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Mordor Intelligence defines the inventory-management-software market as all packaged or cloud-delivered solutions whose primary purpose is to monitor, reconcile, and optimize stock levels across one or more physical or virtual locations, while integrating with ordering, fulfillment, and accounting modules. Revenue is tracked in USD and reflects license, subscription, and platform fees attributable to inventory functions only.

Scope excludes point-of-sale suites that contain basic stock ledgers, stand-alone barcode hardware sales, and bespoke in-house tools developed by retailers or manufacturers.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

We reinforce secondary findings through interviews with supply-chain directors, e-commerce operations heads, software channel partners, and implementation consultants across North America, Europe, Asia-Pacific, and Latin America. These conversations confirm average deal sizes, uptake among small firms, and the pace at which legacy on-premise users migrate to cloud systems, allowing us to tighten critical assumptions before modeling.

Desk Research

Our analysts begin with publicly available cornerstones, such as US Census Annual Retail Trade, Eurostat structural business statistics, UN Comtrade shipment codes for scanners and tags, and policy papers from bodies like the GS1 standards group and the Food and Drug Administration on serialized tracking. Company 10-Ks, cloud vendor investor decks, and trade-association factbooks (e.g., National Retail Federation, Material Handling Institute) then clarify penetration benchmarks, pricing shifts, and upgrade cycles. Where line-item revenue splits are missing, we lean on paid datasets, D&B Hoovers for vendor financials and Dow Jones Factiva for contract wins, to size vendor exposure by geography and deployment. The sources listed illustrate our desk work and are not exhaustive.

Market-Sizing & Forecasting

The baseline value is first derived through a top-down reconciliation of global packaged-software spend with inventory-specific shares reported by public vendors, complemented by trade data on handheld scanning devices which are then mapped to bundled software attach rates. Supplier roll-ups of sampled average selling price times active client counts act as a directional bottom-up check. Key variables feeding the model include cloud migration rate among SMEs, e-commerce order volume growth, average annual subscription price, regulatory mandates for serialized tracking in pharma and food, and warehouse automation spending. A multivariate regression projects each driver forward, while scenario analysis bounds upside from AI-driven demand forecasting modules. Gaps in country-level bottom-up data are bridged by applying validated penetration curves anchored to GDP-per-capita cohorts.

Data Validation & Update Cycle

Model outputs pass through variance tests against independent metrics, such as scanner import peaks, vendor bookings, and SaaS revenue disclosures, before senior review. We refresh figures every twelve months and trigger interim updates when acquisitions, price resets, or new compliance deadlines materially shift market math. A final analyst pass occurs just prior to delivery so clients receive the freshest view.

Why Our Inventory Management Software Baseline Commands Credibility

Benchmark comparison

Published numbers often differ because firms pick divergent module mixes, deployment definitions, and refresh cadences.

Key gap drivers include whether services bundles sit inside the revenue pool, the aggressiveness of SME adoption curves, and currency conversion timing. Mordor's study reports subscription plus license fees tied strictly to inventory functionality in 2025, whereas other publishers may blend broader warehouse or point-of-sale modules or rely on earlier year snapshots.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 3.17 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 3.58 B (2024) | Regional Consultancy A | Counts bundled POS and asset-tracking suites, older baseline year | ||

USD 2.31 B (2024) | Industry Journal B | Excludes integration services and applies conservative SME uptake |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.