Science Based Targets Initiative (SBTi) Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 5.11 Billion |

| Growth Rate (2026 - 2031) | 21.50% CAGR |

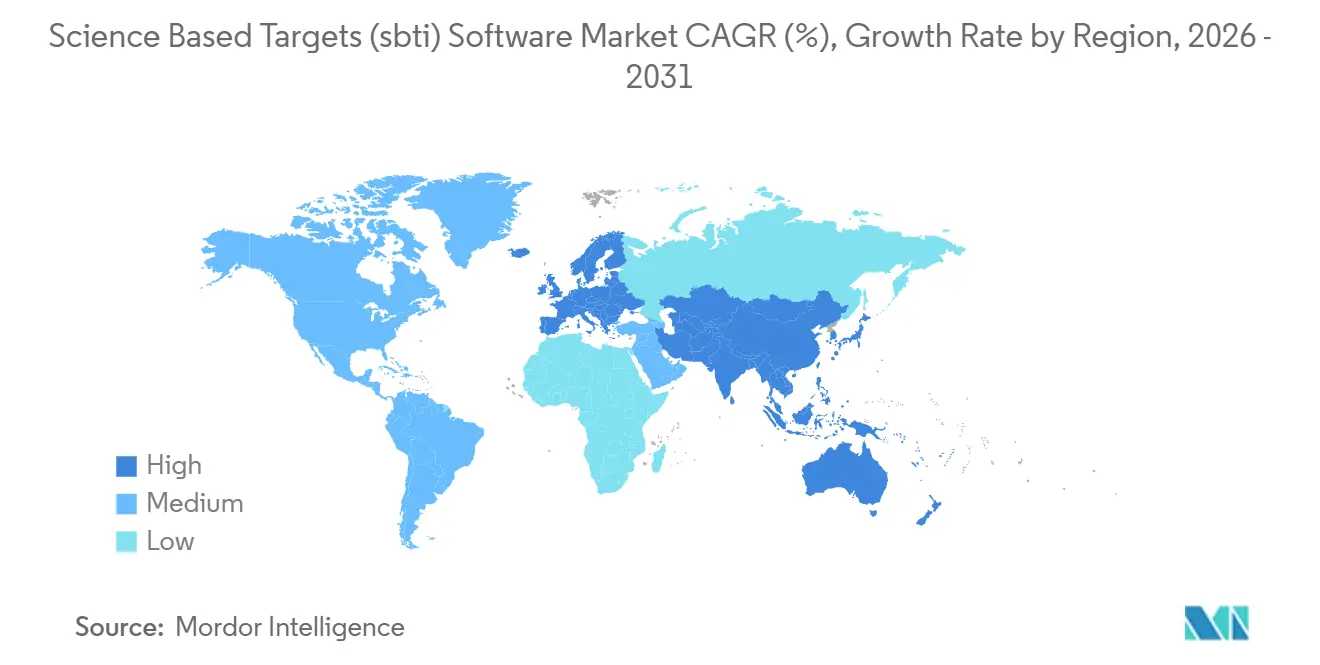

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

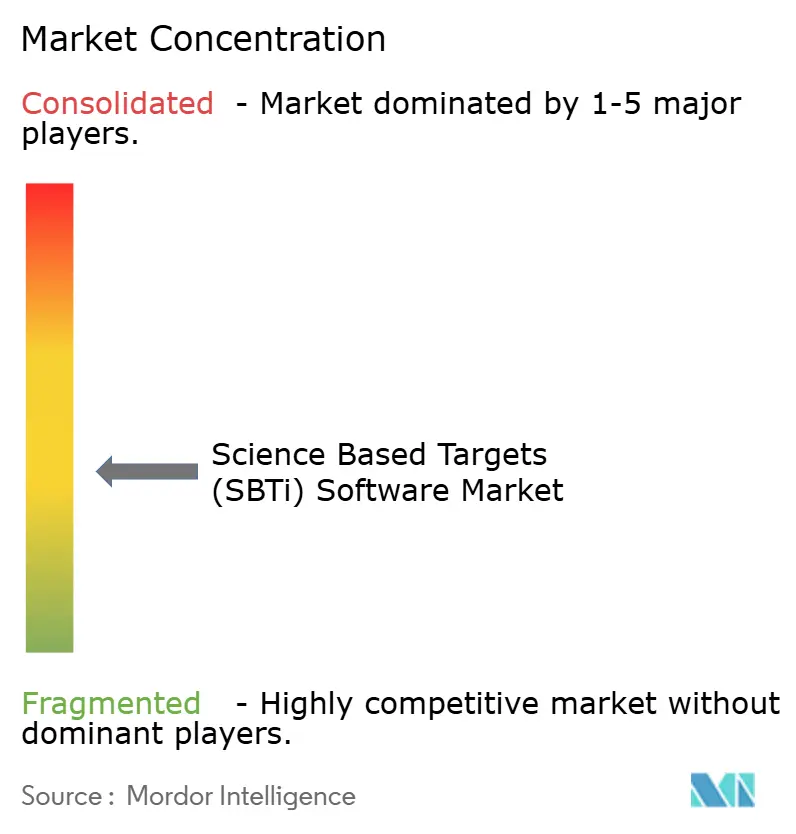

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Science Based Targets Initiative (SBTi) Software Market Analysis by Mordor Intelligence

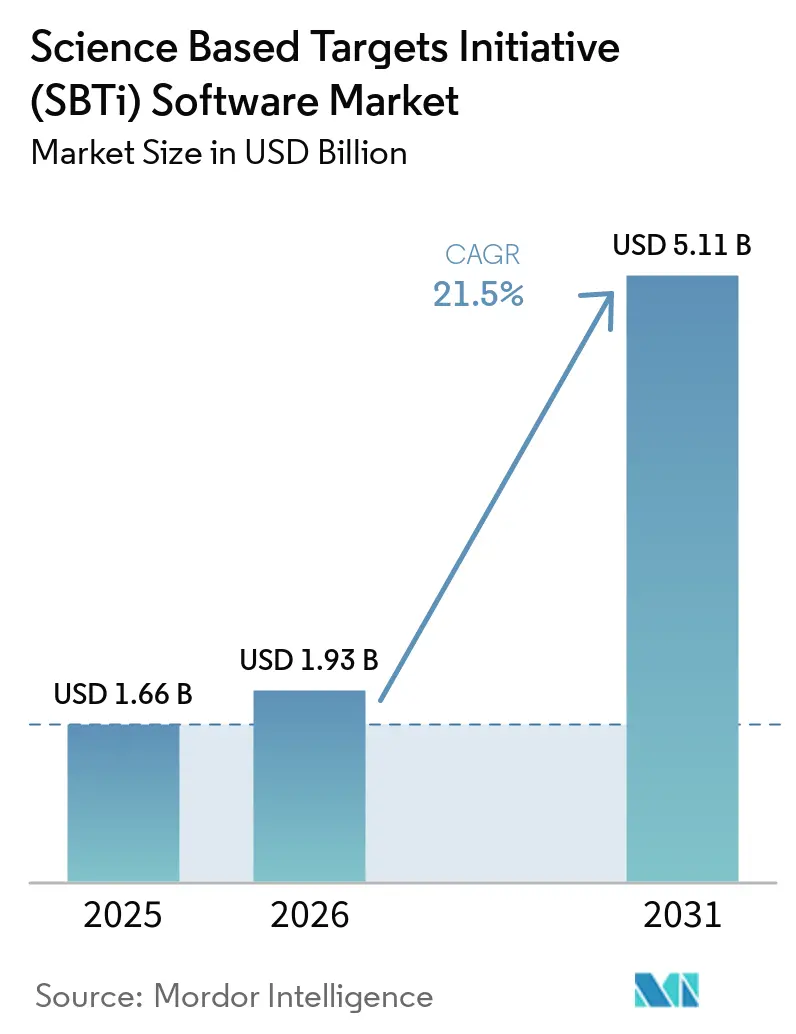

The Science Based Targets Initiative (SBTi) Software Market size was valued at USD 1.66 billion in 2025 and estimated to grow from USD 1.93 billion in 2026 to reach USD 5.11 billion by 2031, at a CAGR of 21.50% during the forecast period 2026-2031. The Science Based Targets Initiative (SBTi) Software Market is being supported by a clear shift in corporate climate programs from optional signaling to recurring compliance work, especially as large companies continue to face formal emissions disclosure and transition planning requirements. The validated company base has expanded to the point that annual emissions reporting, ongoing data management, and five-year target reviews now drive durable software demand that is not dependent solely on new target announcements. Europe remained the largest regional revenue center because reporting obligations and high SBTi penetration among listed companies kept enterprise buying active, while Asia-Pacific is set to rise faster as supply-chain requests from global buyers spread software adoption across export economies. The Science Based Targets Initiative (SBTi) Software Market is also being shaped by enterprises' preference for platforms that integrate with finance, ERP, and supplier systems, which favors vendors with deeper implementation capabilities and stronger audit readiness. At the same time, methodology revisions and fragmented Scope 3 data continue to limit precision, which keeps advisory services, platform upgrades, and supplier engagement tools central to long-term demand.

Key Report Takeaways

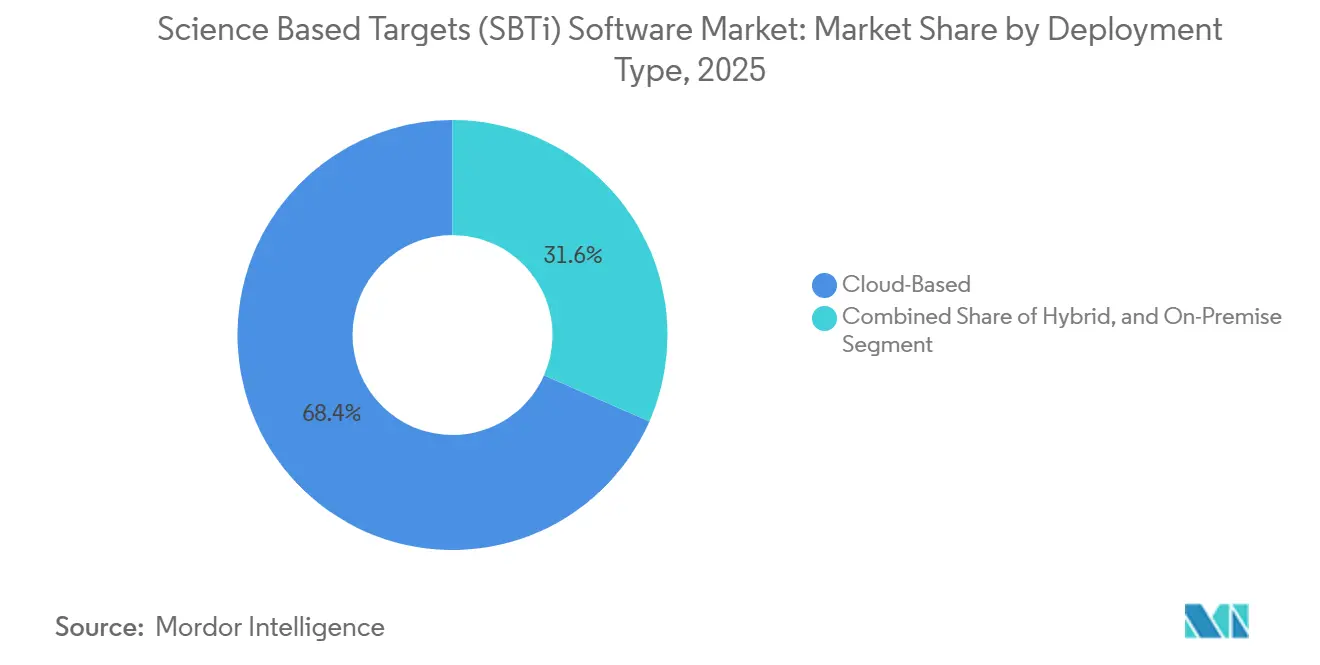

- By deployment type, cloud-based deployment led the Science Based Targets Initiative (SBTi) Software Market in 2025 with a 68.42% share, while hybrid deployment is projected to expand at a CAGR of 22.63% during 2026-2031.

- By component, software platforms accounted for 70.18% of the SBTi software market in 2025, while services are expected to register the fastest CAGR of 23.74% through 2031.

- By enterprise size, large enterprises held 65.91% of the Science-Based Targets Management Software Market in 2025, while small and medium enterprises are projected to grow at a CAGR of 24.56% during 2026-2031.

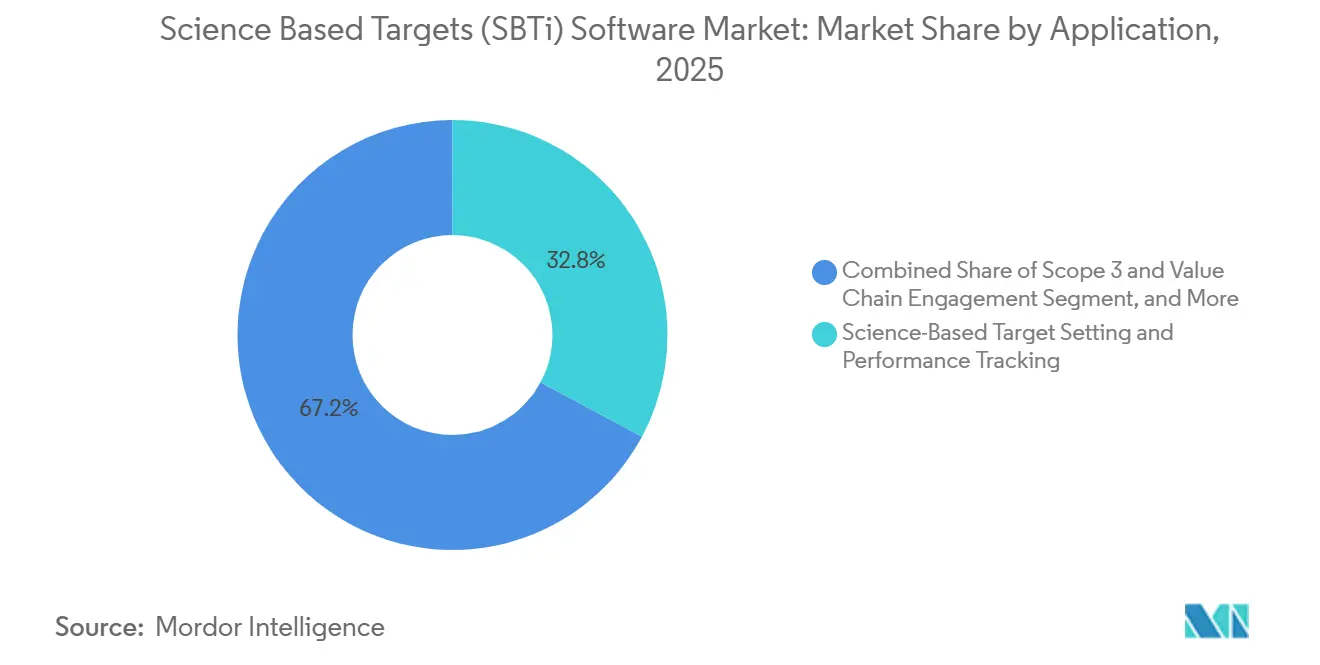

- By application, science-based target setting and performance tracking were the largest application types in 2025, with a 32.84% share, while Scope 3 and value chain engagement are expected to post the fastest CAGR of 25.12% through 2031.

- By end-user industry, industrial manufacturing led in 2025 with a 27.63% share, while energy and utilities are projected to advance at a CAGR of 22.87% over 2026-2031.

- By geography, Europe led the SBTi software market in 2025 with a 35.74% share, while Asia-Pacific is projected to record the highest CAGR of 26.41% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Science Based Targets Initiative (SBTi) Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Regulatory Disclosure and Assurance Requirements | +5.0% | Global, concentrated in Europe and North America | Short term (≤ 2 years) |

| Rising Corporate Science Based Target Commitments | +4.5% | Global, led by Europe and Asia-Pacific | Medium term (2-4 years) |

| Scope 3 Data Automation Across Complex Value Chains | +4.0% | Global, high impact in Asia-Pacific, Europe, and North America | Medium term (2-4 years) |

| ERP, Finance, and Sustainability Workflow Convergence | +2.5% | Global, strongest in North America, Europe, and Japan | Medium term (2-4 years) |

| AI Assisted Decarbonization Planning and Target Tracking | +3.0% | Global, early adoption concentrated in North America and Europe | Long term (≥ 4 years) |

| Supplier Engagement for Measurable Scope 3 Reduction | +2.0% | Global, high impact in Asia-Pacific and South America supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Regulatory Disclosure and Assurance Requirements

The Science Based Targets Initiative (SBTi) Software Market is seeing stronger demand because climate disclosure has become a live reporting task for large companies rather than a future planning exercise. The European Commission states that CSRD requires reporting under ESRS, and the first wave of companies applied the new rules for the 2024 financial year, with reporting beginning in 2025.[1]European Commission, “Corporate Sustainability Reporting,” European Commission, finance.ec.europa.eu Even after the scope was narrowed to the largest companies, climate reporting duties remained central enough to keep emissions accounting, target tracking, and assurance-ready data management in active procurement cycles. This matters for the Science Based Targets Initiative (SBTi) Software Market because large, in-scope enterprises tend to have the most complex organizational boundaries, the deepest supply chains, and the largest reporting burden. As a result, software buying is increasingly linked to mandatory disclosure calendars, internal controls, and external review requirements rather than to one-time sustainability campaigns.

Rising Corporate Science Based Target Commitments

The Science Based Targets Initiative (SBTi) Software Market is also benefiting from the sheer scale of companies already operating within the SBTi system. SBTi reported that 9,764 companies had validated science-based targets by the end of 2025, and the total number of validated companies crossed 10,000 in January 2026.[2]Science Based Targets Initiative, “SBTi 2026-2030 Strategy Summary,” Science Based Targets Initiative, files.sciencebasedtargets.org Its 2026 to 2030 strategy also noted that around 3,100 companies set targets in 2025 and that a similar number is expected in 2026, pointing to continued onboarding demand and a broader renewal pipeline. SBTi further signaled that ambition will be upheld through annual progress reporting and third-party assurance of five-year reviews, which adds recurring workflow needs after initial validation. That recurring review cycle gives the Science Based Targets Initiative (SBTi) Software Market a larger installed base of buyers who must update data models, monitor performance, and prepare for renewed assessment rather than simply set a target once.

Scope 3 Data Automation Across Complex Value Chains

The Science Based Targets Initiative (SBTi) Software Market is moving closer to core operational systems because Scope 3 reporting is difficult to manage with isolated spreadsheets and manual supplier outreach. Microsoft added Scope 3 automation to Dynamics 365 Business Central so users can calculate and surface carbon-equivalent data within standard ERP processes, demonstrating how emissions collection is being pushed into routine transaction flows.[3]Microsoft, “Provide Carbon Equivalent Data for Sales Based on Scope 3 Automation,” Microsoft Learn, learn.microsoft.com IBM also introduced standardized emissions calculations into Excel workflows as a first step toward scalable emissions accounting, recognizing that many companies still begin with fragmented datasets before migrating to more robust platforms. These changes matter because the Science Based Targets Initiative (SBTi) Software Market grows faster when procurement teams can improve data capture within the systems they already use. Vendors that support direct ERP links, repeatable calculation logic, and controlled workflows are therefore better positioned than standalone tools that depend heavily on manual uploads.

AI Assisted Decarbonization Planning and Target Tracking

The Science Based Targets Initiative (SBTi) Software Market is beginning to add another layer of value from AI, especially for sustainability teams that need faster data cleanup, anomaly review, and draft reporting support. Watershed announced AI agents in April 2026, reflecting a move toward software that automates repetitive sustainability tasks while keeping analysts focused on decision-making and follow-up actions. SAP also expanded AI-supported sustainability functions around data unification, emissions factors, and reporting workflows, embedding them more closely into enterprise operating systems. Persefoni’s 2025 year-in-review highlighted OCR-based document extraction, anomaly detection, and smart emission-factor matching, indicating that practical AI adoption is already reaching emissions accounting workflows. Over time, the Science Based Targets Initiative (SBTi) Software Market should reward vendors that can combine this automation with clear data lineage, since regulated users still need traceable inputs and defensible outputs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Emissions Data Across Multi-Tier Supply Chains | -3.5% | Global, most acute in Asia-Pacific and South America multi-tier manufacturing sectors | Medium term (2-4 years) |

| High Implementation and Change Management Cost | -2.5% | Global, disproportionately affecting SMEs and enterprises in emerging markets | Short term (≤ 2 years) |

| Methodology Risk in Science Based Target Validation | -2.0% | Global, with heightened impact in Europe and North America | Medium term (2-4 years) |

| Supplier Data Privacy and Commercial Sensitivity Constraints | -1.5% | Global, heightened in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Emissions Data Across Multi-Tier Supply Chains

The main friction point in the Science Based Targets Initiative (SBTi) Software Market remains the uneven quality of supplier emissions data across complex value chains. Even in advanced markets, standards are still being refined for lifecycle emissions treatment, as shown by NTT’s March 2026 development of CO₂ calculation rules covering the full software lifecycle and aligned with Japan’s carbon footprint guidelines.[4]NTT, “Development of CO₂ Emissions Calculation Rules Covering the Entire Software Lifecycle and Promoting the Creation of Low-Carbon Software Businesses,” NTT, group.ntt That kind of rules work highlights how difficult it is to achieve consistent, auditable reporting when suppliers operate across different countries, methods, and reporting capabilities. The Science Based Targets Initiative (SBTi) Software Market can still grow under these conditions, but buyers often delay full platform expansion when upstream data remains incomplete or inconsistent. This is especially true in sectors with long supplier chains, high purchased goods emissions, and limited reporting maturity beyond tier one partners.

High Implementation and Change Management Cost

The Science Based Targets Initiative (SBTi) Software Market also faces resistance due to the time, cost, and coordination required to implement enterprise-grade systems. Workiva’s public reporting consistently emphasizes integrated financial and sustainability data, stronger governance, and automated data collection, indicating that deployment usually extends well beyond the sustainability team alone. That means procurement, finance, IT, operations, and internal controls teams often need to align before a platform can become part of routine reporting. IBM’s Excel-based emissions tool directly addresses this pain point by providing organizations a lighter entry point before they move to a broader accounting stack. Even so, the Science Based Targets Initiative (SBTi) Software Market still sees slower adoption among budget-sensitive organizations and in emerging markets, where software spending must compete with other compliance priorities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Leadership Holds While Hybrid Demand Deepens

Cloud-based deployment accounted for 68.42% of the Science Based Targets Initiative (SBTi) Software Market in 2025, reflecting a clear preference for SaaS delivery in distributed reporting environments. The largest buyers favor cloud models because emissions factors, disclosure workflows, and regulatory mappings can be updated more consistently without local software maintenance. The Science Based Targets Initiative (SBTi) Software Market has therefore leaned toward platforms that support remote collaboration across sustainability, finance, procurement, and audit teams. Cloud systems also align with how many companies now centralize group-level disclosures while collecting operational data across multiple countries and business units.

That said, the cloud does not eliminate the need for local control in every case. Some industrial, infrastructure, and security-sensitive users still keep sensitive production or supplier data in local environments and move only reporting, analytics, or disclosure outputs into shared environments. Hybrid deployment is projected to grow at a 22.63% CAGR through 2031, showing that many enterprises want a balance between flexibility and tighter control. IBM’s work on emissions calculations within familiar workflow tools and Microsoft’s ERP-linked Scope 3 automation both support this blended model by making carbon accounting usable across mixed technology stacks. For the Science Based Targets Initiative (SBTi) Software Market, that means hybrid design is becoming an important competitive feature rather than a temporary transition step.

By Component: Services Gain Weight as Reporting Complexity Rises

Software platforms accounted for 70.18% of the component segment in 2025, confirming that core calculation engines, workflow tools, and reporting dashboards remain the center of customer spending. This part of the Science Based Targets Initiative (SBTi) Software Market remains essential because companies need a single system of record for emissions baselines, target pathways, and annual disclosure outputs. The strongest platforms are increasingly judged on their use of controlled data models, traceability, and the ability to support multiple reporting frameworks without duplicating work. SAP’s move to make Sustainability Control Tower available within SAP Business Data Cloud shows how vendors are strengthening the software layer by connecting emissions data directly with enterprise operations.

Services are projected to expand at a CAGR of 23.74% through 2031, indicating that buyers still need help turning software into a functioning reporting process. The Science Based Targets Initiative (SBTi) Software Market does not stop at license sales because target setting, data mapping, internal governance, and assurance preparation often require implementation support. Workiva’s public position on integrated reporting, combined with its broad reach across large enterprises, highlights how service-heavy delivery can support more complex customer needs. In practice, many buyers now look for vendors and partners that can combine platform deployment with methodology support and change management. This shift is raising the commercial importance of implementation partners, advisory networks, and post-deployment service capacity across the Science Based Targets Initiative (SBTi) Software Market.

By Enterprise Size: SME Growth Expands the Customer Base Beyond the Largest Buyers

Large enterprises held 65.91% of the Science Based Targets Initiative (SBTi) Software Market share in 2025, supported by their greater reporting exposure and stronger ability to fund multi-year technology programs. The Science Based Targets Initiative (SBTi) Software Market naturally drew early demand from this group because large companies face more complex entity structures, more supplier relationships, and more scrutiny from investors, customers, and regulators. They also have more internal functions involved in sustainability reporting, which increases the value of standardized platforms. Workiva’s reach across 85% of the Fortune 1000 and 6,600+ customers shows how deeply large-company reporting relationships already shape software adoption patterns.

Small and medium enterprises are projected to grow at a CAGR of 24.56% through 2031, making them the fastest-growing segment in the Science-Based Targets Initiative (SBTi) Software Market. This shift is closely tied to supply chain pressure because larger buyers are asking many SMEs to provide emissions data even when they are not directly regulated. SBTi’s 2026 to 2030 strategy explicitly points toward broader network growth, stronger partnerships, and expanded coverage in high-emitting regions and sectors, which support wider SME participation over time. Persefoni reported that Persefoni Pro surpassed 8,000 users across more than 100 countries by the end of 2025, demonstrating how lower-cost, entry-tier offerings can widen the funnel for smaller organizations. As that funnel grows, the Science Based Targets Initiative (SBTi) Software industry is becoming less dependent on a narrow pool of very large buyers.

By Application: Scope 3 Engagement Becomes the Most Important Expansion Layer

Science-based target setting and performance tracking accounted for the largest share at 32.84% in 2025, reflecting the continuing need to establish baselines, monitor progress, and prepare for recurring reviews. The Science Based Targets Initiative (SBTi) Software Market still relies on this application as the first anchor sale because it gives companies a starting point for target governance and annual disclosure. SBTi’s 2026 to 2030 strategy reinforced that annual progress reporting and five-year reviews will remain part of the operating model, keeping target tracking relevant long after initial validation. For many customers, this application remains the practical entry gate before they invest in more advanced planning and supplier engagement functions.

Scope 3 and value chain engagement is projected to grow at a 25.12% CAGR through 2031, making it the fastest application in the Science Based Targets Initiative (SBTi) Software Market. The pressure is clear because supplier emissions remain the hardest part of enterprise carbon management and often determine whether reported progress is credible at scale. Microsoft’s integration of Scope 3 automation into business processes and NTT’s lifecycle CO₂ rules in Japan both point to a future in which more value chain data is collected in structured, repeatable ways. This is why the Science Based Targets Initiative (SBTi) Software industry is moving beyond reporting alone toward supplier networks, workflow automation, and scenario-linked emissions management. As vendors connect these application areas into a single data model, contract value and customer stickiness are likely to improve.

By End-User Industry: Manufacturing Leads While Utilities Move Faster

Industrial manufacturing retained the largest end-user share at 27.63% in 2025, reflecting the sector’s heavy emissions profile and extensive supplier networks. SBTi reported that Industrials accounted for 30% of all globally validated targets by the end of 2025, which helps explain why the Science Based Targets Initiative (SBTi) Software Market remains concentrated around this customer group. Manufacturers often need a single platform that can handle direct facility emissions, purchased goods data, and group-level disclosures simultaneously. That combination makes the segment a natural anchor for enterprise software spending, especially in global companies with multi-country operations and high supplier counts.

Energy and utilities are projected to expand at a 22.87% CAGR through 2031, making it the fastest-growing end-user segment in the Science Based Targets Initiative (SBTi) Software Market. SBTi’s Trend Tracker showed that validated companies in Japan’s energy and utilities segment rose by 48% in 2025, supporting the case for faster adoption in regulated energy systems. The same report also showed strong growth in information technology and health care, suggesting that software demand is expanding into sectors with different reporting patterns and product footprints. Even so, industrial manufacturing should remain the revenue center because its reporting scope is broader and its implementation challenges are more complex. This balance between a large installed manufacturing base and a faster-growing utilities segment will shape sales priorities across the Science Based Targets Initiative (SBTi) Software Market.

Geography Analysis

Europe accounted for 35.74% of the SScience Based Targets Initiative (SBTi) Software Market share in 2025, maintaining its position as the largest regional market. The region’s leadership comes from a combination of formal reporting obligations and high penetration of validated targets among major listed companies. SBTi reported that 70% of CAC 40 companies and 68% of DAX 40 companies had validated targets by the end of 2025, supporting a large installed base for software renewals and upgrades. The European Commission’s reporting framework also keeps implementation activity active because the first wave of CSRD companies has already entered the reporting cycle, and ESRS remains the operating standard for required disclosures.

Asia Pacific is projected to deliver the fastest regional growth in the Science Based Targets Initiative (SBTi) Software Market, at a 26.41% CAGR through 2031. The region is moving quickly because supplier demands from global buyers are reaching more companies than direct regulation alone would capture. SBTi reported that Japan led all territories with 2,091 validated target companies by the end of 2025, while China grew 92% year over year to 598 validated companies. The same report showed growth in India, South Korea, and several Southeast Asian markets, indicating that demand is broadening across the region rather than relying on a single national market. NTT’s 2026 work on software lifecycle CO₂ rules in Japan also shows how local standards development is increasing the need for structured data and more capable reporting platforms.

North America accounted for 11% of the global validated target companies by the end of 2025, with the United States contributing 943 companies, up 33% from the previous year. SBTi’s 2026 to 2030 strategy noted that only a negligible number of U.S. companies left the framework after the U.S. withdrawal from the Paris Agreement, suggesting that customer and investor expectations still support enterprise spending on climate reporting tools. South America is still smaller in revenue terms, but Brazil and neighboring markets are expanding as export-linked sectors face rising disclosure and supply chain pressures. The Middle East and Africa remain early-stage markets, yet company-led infrastructure development is emerging, including SINAI’s 2025 Saudi partnership to deploy an AI-enabled enterprise decarbonization platform, which signals a gradual broadening of addressable demand beyond the current core regions.

Competitive Landscape

The Science Based Targets Initiative (SBTi) Software Market remains moderately fragmented because no single vendor group controls demand across carbon accounting depth, ERP integration, assurance readiness, and supplier network reach. Pure play platforms such as Persefoni, Watershed, and Normative compete on workflow depth and carbon management specialization, while IBM, SAP, Microsoft, Workiva, and Diginex bring broader enterprise relationships into the category. The Science Based Targets Initiative (SBTi) Software Market is therefore split between companies that start from climate functionality and companies that start from enterprise systems or reporting infrastructure. This structure keeps the field competitive because buyers often compare specialized capability against the cost and convenience of extending an existing software stack.

Consolidation has become more visible as vendors try to add customers, methods, and adjacent capabilities more quickly. Diginex completed the acquisition of Plan A in 2026 and positioned the business within a broader sustainability and compliance platform, demonstrating how general ESG infrastructure providers are moving deeper into carbon management. Persefoni also acquired Diligent’s carbon accounting customer base in 2025, using the move to widen its reach inside governance and compliance environments. IBM’s emissions calculations launch, and Watershed’s AI agents represent another kind of strategic move, where vendors strengthen usability and workflow automation rather than relying solely on acquisition-led scale. These steps suggest that the Science Based Targets Initiative (SBTi) Software Market rewards both platform breadth and operational depth, depending on the buyer's needs.

Competitive advantage is increasingly tied to system integration, traceable data, and the ability to adapt when standards evolve. SAP’s sustainability data strategy and Microsoft’s ERP-linked emissions workflows show that enterprise vendors are working to make carbon accounting part of the standard business data environment rather than a separate reporting layer. Workiva’s reporting position and customer reach also matter because assurance and disclosure controls are becoming harder to separate from core corporate reporting processes. At the same time, standards work such as NTT’s software lifecycle CO₂ rules points to room for sector-specific differentiation that general-purpose platforms still need to build out. For that reason, the Science Based Targets Initiative (SBTi) Software Market still has room for both large suites and focused specialists, even as recent acquisitions narrow the field.

Science Based Targets Initiative (SBTi) Software Industry Leaders

Persefoni AI, Inc.

Watershed Technology, Inc.

Normative AB

Plan A GmbH

Greenly SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: IFS launched IFS Zero, an agentic Emissions Operating System for asset-intensive industries, providing a unified Scope 1, Scope 2, and Scope 3 calculation and disclosure platform. The product launched alongside IFS Cloud 26R1, which became generally available on May 28, 2026, marking IFS's entry into the dedicated enterprise emissions management segment.

- April 2026: Watershed launched a suite of AI Agents during San Francisco Climate Week, automating utility bill processing, emissions analysis, and ESG report drafting. Early users reported up to 12 weeks of annual time savings and a 93% reduction in duration on select data-cleaning tasks, with average time-to-actionable data improving approximately 80%.

- April 2026: IBM launched the Envizi Emissions API on April 30, 2026, providing programmatic access to over 140,000 globally recognized emissions datasets for Scope 1, Scope 2, and Scope 3 calculations. The API enabled enterprises and software providers to embed GHG calculation engines directly into existing operational workflows, reducing reliance on manual spreadsheet-based processes.

- January 2026: Diginex (NASDAQ: DGNX) completed its acquisition of Plan A GmbH for EUR 55 million (USD 64 million), paid primarily in Diginex shares. Visa and Deutsche Bank became Diginex shareholders through the transaction, and Plan A CEO Lubomila Jordanova retained her position, reflecting continuity in Plan A's sustainability platform strategy.

Global Science Based Targets Initiative (SBTi) Software Market Report Scope

The Science Based Targets Initiative (SBTi) Software Market refers to digital platforms and services that enable organizations to align their climate strategies with the Science Based Targets initiative (SBTi) framework. These solutions provide functionalities such as emissions baseline management, science-based target setting, performance tracking, Scope 3 and value chain engagement, and decarbonization roadmapping with transition scenario modeling.

The Science Based Targets Initiative (SBTi) Software Market report is segmented by Deployment Type (Cloud-Based, On-Premise, and Hybrid), Component (Software Platforms and Services), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Emissions Baseline Management and Reporting, Science-Based Target Setting and Performance Tracking, Scope 3 and Value Chain Engagement, Decarbonization Roadmapping and Transition Scenario Modeling), End-user Industry (Industrial Manufacturing, Energy and Utilities, Oil and Gas, Retail and Consumer Goods, Food and Beverage, IT and Telecom, Construction and Infrastructure, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform | Carbon-aware schedulers |

| Workload orchestration engines | |

| Cloud optimization platforms | |

| Carbon-intensity analytics | |

| Multi-cloud optimization systems | |

| AI-based workload placement tools | |

| Sustainability automation engines | |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Carbon-Aware Workload Scheduling |

| Resource Utilization Optimization |

| Multi-Cloud Workload Placement |

| AI Infrastructure Optimization |

| Sustainable DevOps and Testing |

| Energy-Efficient Data Processing |

| Industrial Manufacturing |

| Energy and Utilities |

| BFSI |

| Retail and Consumer Goods |

| IT and Telecom |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Transportation and Logistics |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Platform | Carbon-aware schedulers |

| Workload orchestration engines | ||

| Cloud optimization platforms | ||

| Carbon-intensity analytics | ||

| Multi-cloud optimization systems | ||

| AI-based workload placement tools | ||

| Sustainability automation engines | ||

| Services | ||

| By Deployment | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Carbon-Aware Workload Scheduling | |

| Resource Utilization Optimization | ||

| Multi-Cloud Workload Placement | ||

| AI Infrastructure Optimization | ||

| Sustainable DevOps and Testing | ||

| Energy-Efficient Data Processing | ||

| By End-user Industry | Industrial Manufacturing | |

| Energy and Utilities | ||

| BFSI | ||

| Retail and Consumer Goods | ||

| IT and Telecom | ||

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Transportation and Logistics | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the Science Based Targets Initiative (SBTi) Software Market?

The Science Based Targets Initiative (SBTi) Software Market was valued at USD 1.66 billion in 2025, is estimated at USD 1.93 billion in 2026, and is projected to reach USD 5.11 billion by 2031 at a 21.50% CAGR.

Which region leads spending today, and which one is growing fastest?

Europe held the largest share at 35.74% in 2025 because of reporting obligations and high target penetration, while Asia-Pacific is projected to grow fastest at a 26.41% CAGR through 2031.

Which deployment model has the strongest position?

Cloud-based deployment led with a 68.42% share in 2025, reflecting enterprise demand for easier updates, multi-user collaboration, and more scalable compliance workflows.

Why is Scope 3 engagement becoming such an important software use case?

Scope 3 and value chain engagement is projected to grow at a 25.12% CAGR through 2031 because buyers need more structured supplier data, better workflow control, and stronger audit support across complex value chains.

Which customer group is widening the buyer base the fastest?

Small and medium enterprises are projected to grow at a 24.56% CAGR through 2031 as supply-chain mandates from larger buyers push emissions reporting further down the supplier base.

Which end-user sectors matter most for vendors?

Industrial manufacturing remained the largest end-user segment with a 27.63% share in 2025, while energy and utilities is expected to expand fastest at a 22.87% CAGR through 2031.

Page last updated on: