Sodium Benzoate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

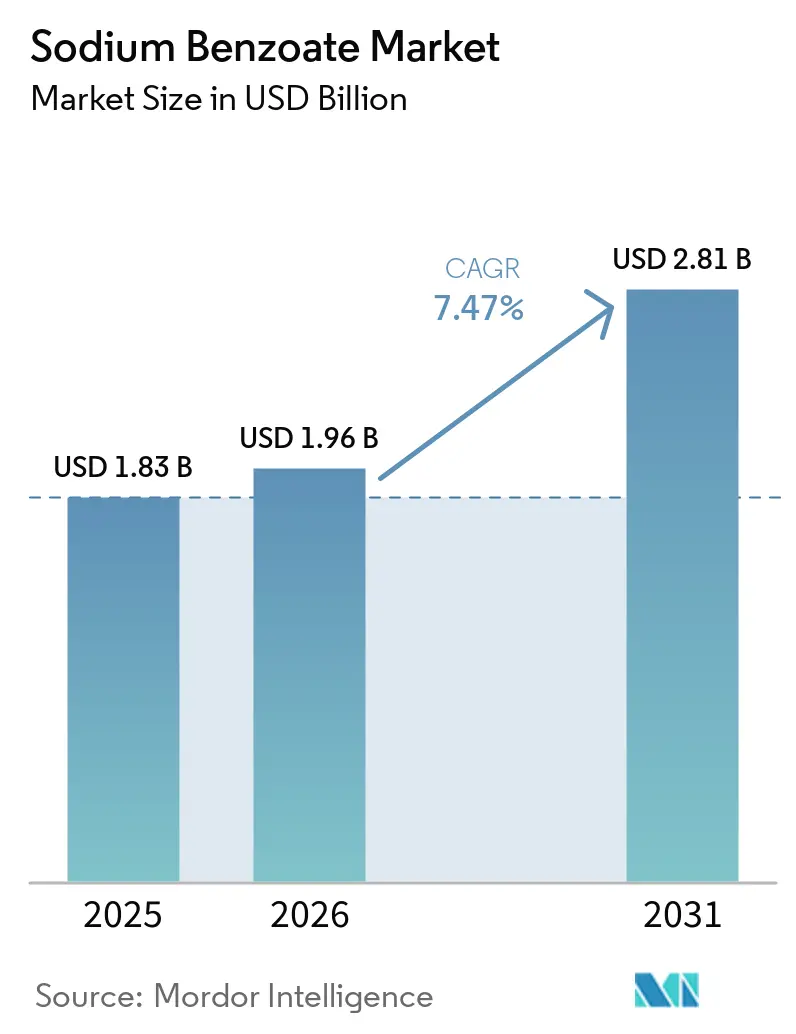

| Market Size (2026) | USD 1.96 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 7.47% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sodium Benzoate Market Analysis by Mordor Intelligence

The Sodium Benzoate Market size was valued at USD 1.83 billion in 2025 and is estimated to grow from USD 1.96 billion in 2026 to reach USD 2.81 billion by 2031, at a CAGR of 7.47% during the forecast period (2026-2031). Robust demand from processed-food manufacturers in Asia-Pacific and Africa, expanding use as an antimicrobial excipient in oral liquid drugs, and incremental industrial consumption in electroplating and cooling-water systems will keep volumes expanding despite clean-label reformulation and tighter preservative regulations in the European Union and California. Food and beverage producers continue to anchor global volumes because sodium benzoate delivers reliable microbial control below pH 4.5 at a cost roughly 20-30% lower than potassium sorbate. Personal care formulators are accelerating adoption as the shift toward water-rich cosmetic bases requires pH-dependent protection that alternatives such as parabens or phenoxyethanol cannot always guarantee. Meanwhile, large integrated suppliers, including LANXESS, Eastman Chemical, and Avantor, are pivoting toward lower-carbon manufacturing footprints and capacity expansions to sustain supply resilience.

Key Report Takeaways

- By application, food and beverages led with 45.18% of the sodium benzoate market share in 2025, while personal care and cosmetics are projected to grow at an 8.34% CAGR through 2031.

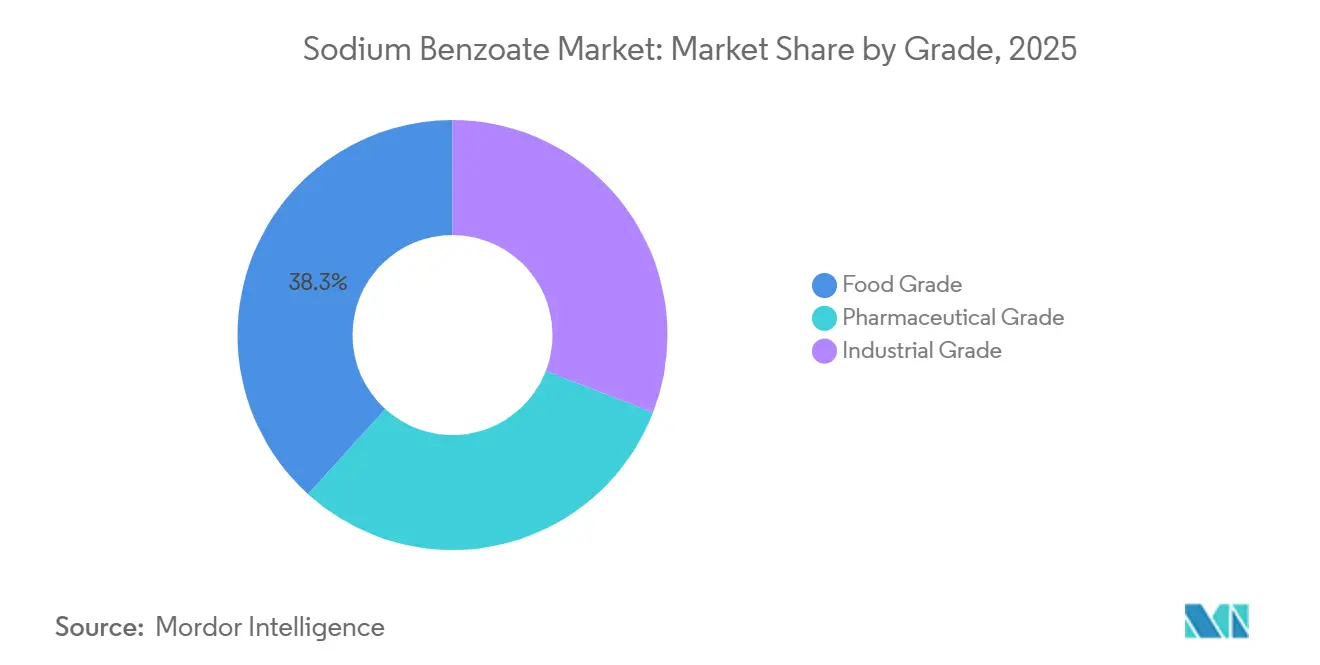

- By grade, food grade accounted for 38.28% of the sodium benzoate market size in 2025; pharmaceutical grade is on track for the fastest 8.23% CAGR to 2031.

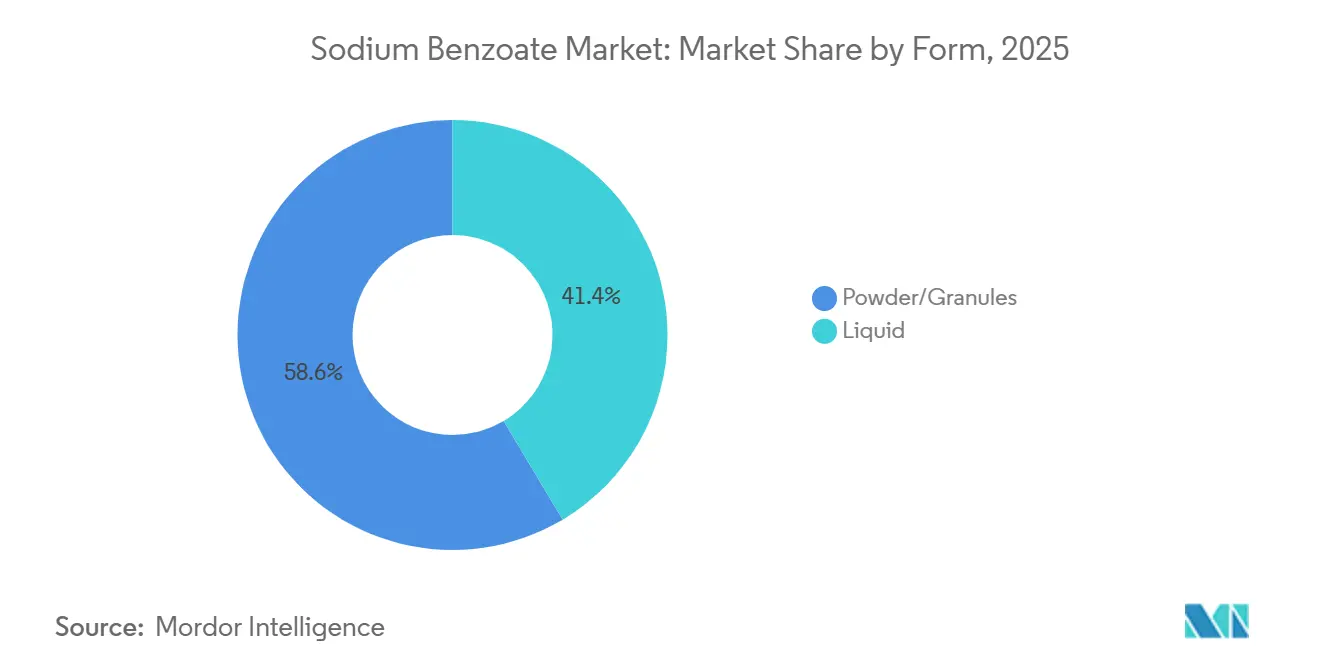

- By form, powder and granules captured 58.56% share of the sodium benzoate market size in 2025, yet the liquid form will advance at an 8.45% CAGR through 2031.

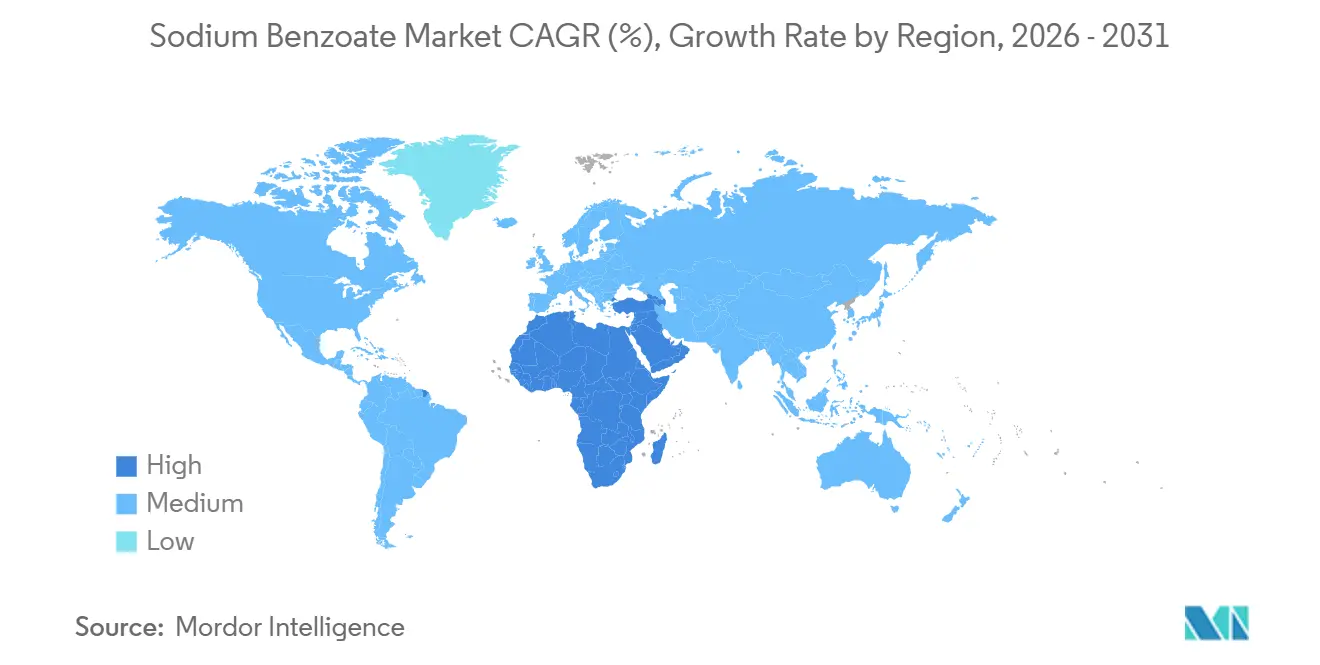

- By geography, Europe held 34.50% of the sodium benzoate market share in 2025, whereas the Middle East and Africa are forecast to post the quickest 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sodium Benzoate Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food and beverage preservative demand surge | +2.1% | Global, focus on APAC and Africa | Medium term (2-4 years) |

| Shift toward processed foods in APAC and Africa | +1.8% | APAC core, spill-over to MEA | Long term (≥4 years) |

| Pharma demand for antimicrobial excipients | +1.3% | Global, led by North America and Europe | Medium term (2-4 years) |

| Adoption in animal-nutrition acidifiers | +0.6% | Europe, North America, expanding to APAC | Long term (≥4 years) |

| Electroplating and cooling-water treatment use | +0.5% | APAC manufacturing hubs, North America industrial belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Food and Beverage Preservative Demand Surge

Roughly 52% of global food-application volume flows into carbonated drinks, juices, and acidic condiments, where sodium benzoate is used up to 0.1% for reliable inhibition below pH 4.5. The U.S. FDA continues to list the preservative as GRAS, reinforcing confidence in emerging markets that benchmark American regulations. Cost-sensitive bottlers in India, Nigeria, and Indonesia prefer sodium benzoate because it remains 20-30% cheaper than potassium sorbate on a molar basis. A 2025 survey of beverages in Sulaymaniyah, Iraq, found mean concentrations of 84.10 mg/L, well inside Codex limits, confirming safety margins under real-world conditions[1]Jassim Mohammed et al., “Benzoate Levels in Beverages Marketed in Iraq,” Journal of Food Protection, iafponline.org. These economics and compliance buffers offset clean-label erosion in premium Western brands.

Shift Toward Processed Foods in APAC and Africa

India’s packaged-food sector is projected to rise from INR 10,180 billion (USD 122 billion) in fiscal 2024 to INR 17,120 billion (USD 206 billion) by fiscal 2029 at an 11% CAGR, with ready-to-eat meals expanding 16% annually. Urbanization and growing e-commerce penetration motivate shelf-stable recipes that can travel ambient supply chains, sustaining the sodium benzoate market even as premium labels test natural alternatives. Comparable patterns in Nigeria, Kenya, and Egypt underpin the 8.21% regional CAGR forecast for the Middle East and Africa through 2031.

Pharma Demand for Antimicrobial Excipients

Over 85% of liquid drug formulations rely on preservatives, and sodium benzoate remains the default organic acid listed in IP, BP, and USP monographs. Pediatric syrups favor the excipient for its neutral taste, helping adherence without masking agents. A 2020 stability study demonstrated complete microbial inhibition in flavored oral solutions at 0.1% through 96 days, validating efficacy. Growth is tempered by parenteral segments moving to preservative-free formats, yet rising generic production in India and Brazil offsets the shift.

Adoption in Animal-Nutrition Acidifiers

European and U.S. regulators allow sodium benzoate or benzoic acid in pig and poultry feed up to 2,400mg/kg to improve feed conversion and pathogen control. The global push toward antibiotic-free livestock fosters incremental uptake, especially in China’s vast swine sector recovering from African swine fever. Solubility advantages over benzoic acid simplify incorporation into liquid supplements, although ruminant efficacy remains limited.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising clean-label reformulation pressures | -1.2% | North America and Europe, urban APAC | Short term (≤2 years) |

| Safety concerns on benzene formation | -0.8% | Global, acute in California and EU | Medium term (2-4 years) |

| EU and California tightening benzoate limits | -0.5% | Europe and California | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Clean-Label Reformulation Pressures

Consumers in the United States and Western Europe increasingly pay 7-20% premiums for beverages and sauces promoted as free from synthetic additives, redirecting preservative share toward rosemary extract, nisin, or cultured dextrose. European rules require proof that no alternative process can ensure safety, raising hurdles for sodium benzoate in premium SKUs. Laboratory work in 2025 showed that partially replacing sodium benzoate with honey and clove oil retained antimicrobial performance in cough syrups, hinting at hybrid systems that reduce synthetic load; however, scale-up and real-time shelf-life validation remain pending.

Safety Concerns on Benzene Formation with Vitamin C

Sodium benzoate may react with ascorbic acid under heat or UV light to form benzene, a carcinogen. The issue resurfaced after the 2005 soft-drink recalls and now drives California Proposition 65 warning-label policies[2]Office of Environmental Health Hazard Assessment, “Proposition 65 Chemical List,” oehha.ca.gov. To avoid label stigma, many vitamin-fortified beverage brands switched to potassium sorbate or installed in-line benzene monitoring, trimming sodium benzoate volumes in the fastest-growing functional-drink niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Food and Beverages Maintain Scale, Cosmetics Accelerate

Food and beverages commanded 45.18% of the sodium benzoate market size in 2025, owing to carbonated soft drinks, fruit juices, pickles, and salad dressings that collectively consume more than half of the food-grade tonnage. Personal care and cosmetics, however, will log the fastest 8.34% CAGR through 2031 as shampoos, lotions, and micellar waters adopt the preservative to secure micro-stability at pH 4-5. Consumer backlash against parabens and reduced phenoxyethanol efficacy below pH 5 positions sodium benzoate as a technically robust alternative.

The sodium benzoate market continues to depend on processed foods for baseline demand, yet the cosmetics uptrend diversifies volume risk. In pharmaceuticals, pediatric syrups and topical creams underpin an 18-20% share, while industrial uses in corrosion-inhibition remain a small but stable niche. Consequently, long-term growth rests on dual momentum: sustained beverage consumption in emerging economies and cosmetic formulators’ search for preservative systems compatible with low-pH, surfactant-rich bases.

By Grade: Food Grade Dominates, Pharmaceutical Grade Expands

Food grade secured 38.28% of the global market share in 2025, leveraging broad regulatory acceptance and low per-kilogram cost. Pharmaceutical grade, though smaller, is expected to increase at an 8.23% CAGR through 2031 as multi-dose pediatric syrups and topical generics multiply in India, Brazil, and Nigeria. Higher purity (over 99%) and stringent impurity limits (less than 0.5%) justify a 15-25% price premium that vertically integrated suppliers absorb through benzoic-acid back-integration, reinforcing their margin resilience.

While the sodium benzoate market size continues to lean on food applications, pharmaceutical-grade demand secures a healthy pipeline as global healthcare access widens. Industrial grade follows regional manufacturing trends but faces substitution pressure from phosphonate-based chemistries in high-temperature cooling systems.

By Form: Powder Retains Volume Leadership, Liquid Leads Growth

Powder and granules captured 58.56% of the sodium benzoate market size in 2025 because they handle well in dry spice mixes, beverage bases, and automated dosing. Liquid sodium benzoate, often supplied as a 30-40% solution, is forecast to climb at an 8.45% CAGR through 2031 as beverage, pharmaceutical, and cosmetic plants seek dust-free, instantly soluble ingredients that cut batch times.

Bulk powder remains cost-optimal for commodity foods, but liquid form’s process-efficiency benefits resonate with high-throughput bottlers and GMP-audited drug makers. The sodium benzoate market will likely see more suppliers introducing turnkey liquid blends containing potassium sorbate or EDTA to help customers comply with benzene-mitigation protocols.

Geography Analysis

Europe held 34.50% of global share in 2025, supported by high soft-drink intake and a sizeable pharmaceutical base. Germany’s food-processing and France’s beverage industries remain anchor buyers, yet retailers’ preference for “E-number-free” labels is prompting gradual reformulation, particularly in children’s products.

The Middle East and Africa will be the fastest-growing region at 8.21% CAGR during 2026-2031. Limited cold-chain infrastructure and packaged-food security programs boost reliance on ambient-stable preservatives. Regulatory regimes across Gulf Cooperation Council states mirror Codex limits, giving formulators confidence to maintain sodium benzoate usage without immediate costlier substitutions.

Asia-Pacific demand is propelled by India’s double-digit packaged-food expansion and China’s vast beverage output. While clean-label cues resonate in tier-1 Chinese cities, mass-market segments in ASEAN and South Asia still prioritize cost-effective shelf-life. The current demand in North America reflects a mature baseline and California’s Proposition 65 influence; most reformulations substitute or reduce sodium benzoate in vitamin-fortified drinks rather than mainstream carbonated brands. South America rounds out global share with steady commodity-focused demand.

Competitive Landscape

The sodium benzoate market is consolidated. Vertical integration into benzoic acid secures cost leverage and impurity control, critical for pharmacopeial-grade supply. LANXESS converted its Botlek, Netherlands, plant to low-emission electricity in September 2025, aligning with EU Green Deal targets and appealing to sustainability-focused tenders. Eastman expanded U.S. benzoic-acid capacity in October 2024 and raised prices in April 2024, signaling supply tightness and margin protection in high-purity segments.

Chinese mid-tier players compete on price and flexible minimum-order quantities, servicing Asian and African buyers that value short lead times. Strategic whitespace centers on premixed liquid preservative blends, hybrid clean-label systems, and technical support for benzene-risk mitigation. Quality consistency, regulatory documentation, and supply resilience remain stronger differentiators than headline pricing, especially in pharmaceutical and premium cosmetic channels.

Sodium Benzoate Industry Leaders

LANXESS

Eastman Chemical Company

WUHAN YOUJI

Tengzhou Tenglong Food science and technology development co.,ltd

Foodchem International Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: LANXESS switched its Botlek site to low-emission electricity for sodium benzoate manufacturing, cutting the product’s carbon footprint and strengthening its position in EU sustainability-driven tenders.

- October 2024: Eastman Chemical invested more than USD 50 million in new U.S. benzoic-acid capacity to serve rising pharmaceutical-grade demand and reduce North American reliance on Asian imports.

Global Sodium Benzoate Market Report Scope

Sodium benzoate is a water-soluble chemical compound commonly utilized as a preservative to inhibit the growth of mold, bacteria, and yeast in acidic foods, beverages, and cosmetic products.

The sodium benzoate market is segmented by application, grade, form, and geography. By application, the market is segmented into food and beverages, pharmaceuticals, personal care and cosmetics, and industrial (corrosion inhibitors, adhesives). By grade, the market is segmented into food grade, pharmaceutical grade, and industrial grade. By form, the market is segmented into powder/granules and liquid. The report also covers the market size and forecasts for the sodium benzoate market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Food and Beverages |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial (corrosion inhibitors, adhesives) |

| Food Grade |

| Pharmaceutical Grade |

| Industrial Grade |

| Powder/Granules |

| Liquid |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Food and Beverages | |

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial (corrosion inhibitors, adhesives) | ||

| By Grade | Food Grade | |

| Pharmaceutical Grade | ||

| Industrial Grade | ||

| By Form | Powder/Granules | |

| Liquid | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the sodium benzoate market by 2031?

The Sodium Benzoate Market size was valued at USD 1.83 billion in 2025 and is estimated to grow from USD 1.96 billion in 2026 to reach USD 2.81 billion by 2031, at a CAGR of 7.47% during the forecast period (2026-2031).

Which segment is expected to grow fastest through 2031?

Personal care and cosmetics will post the quickest 8.34% CAGR during 2026-203 as water-based formulations seek pH-dependent antimicrobial protection.

Why are beverage makers in emerging economies favoring sodium benzoate?

The preservative costs 20-30% less than potassium sorbate on an equivalent basis and dissolves readily in acidic drinks, making it attractive for high-volume bottling lines.

How is regulation influencing demand in Europe?

Ongoing EFSA re-evaluations and consumer preference for “E-number-free” labels are prompting gradual reformulation.

Which region will experience the highest growth rate?

The Middle East and Africa will lead with an 8.21% CAGR through 2031, supported by urbanization and limited cold-chain infrastructure that favors ambient-stable products.

Page last updated on: