Benzene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

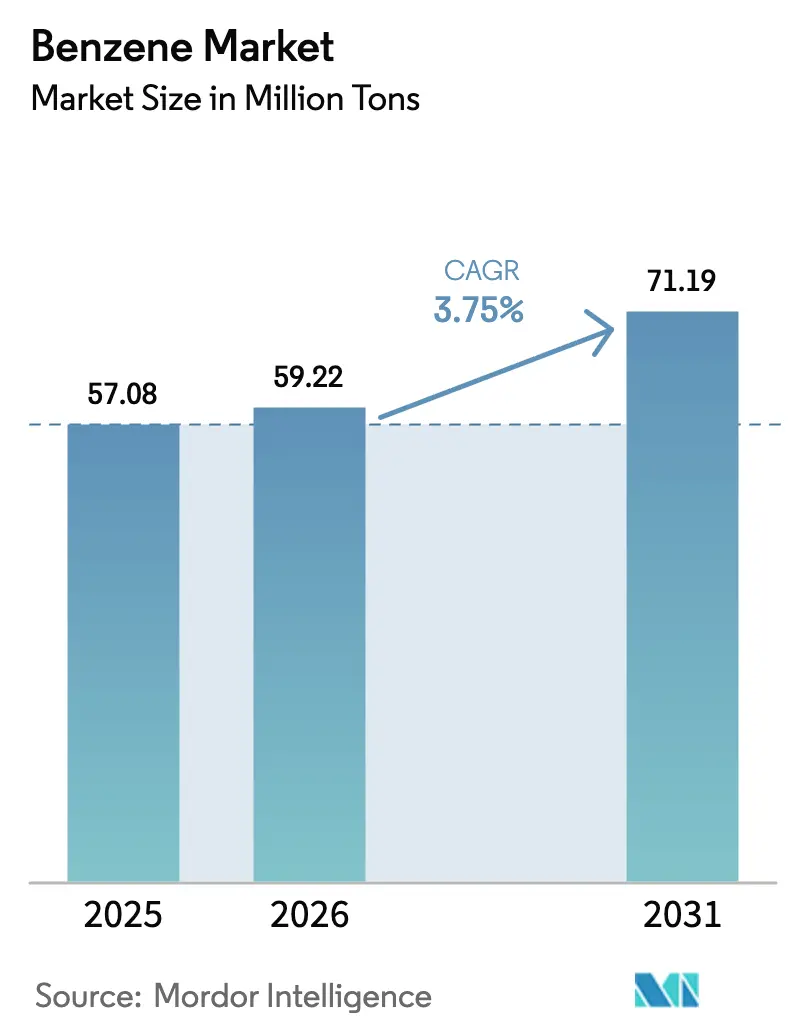

| Market Volume (2026) | 59.22 Million tons |

| Market Volume (2031) | 71.19 Million tons |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benzene Market Analysis by Mordor Intelligence

The Benzene Market size is expected to grow from 57.08 million tons in 2025 to 59.22 million tons in 2026 and is forecast to reach 71.19 million tons by 2031 at a 3.75% CAGR over 2026-2031. Current momentum comes from integrated refinery-petrochemical complexes in Asia that convert heavy crude directly into aromatics, from the accelerating pickup of pharmaceutical intermediates, and from resilient demand for styrene-based polymers in packaging and automotive applications. Margin performance in the benzene market is increasingly determined by downstream integration, process energy efficiency, and the ability to hedge crude-linked feedstock swings. Integrated producers that swing benzene allocation among ethylbenzene, cumene, and nitrobenzene enjoy cost and optionality advantages, while merchant producers face tighter spreads and higher compliance costs in North America and Europe. Capacity rationalization in high-cost regions and simultaneous greenfield projects in China, India, and the Gulf reinforce a re-balancing that anchors the benzene market to Asia-Pacific over the next five years.

Key Report Takeaways

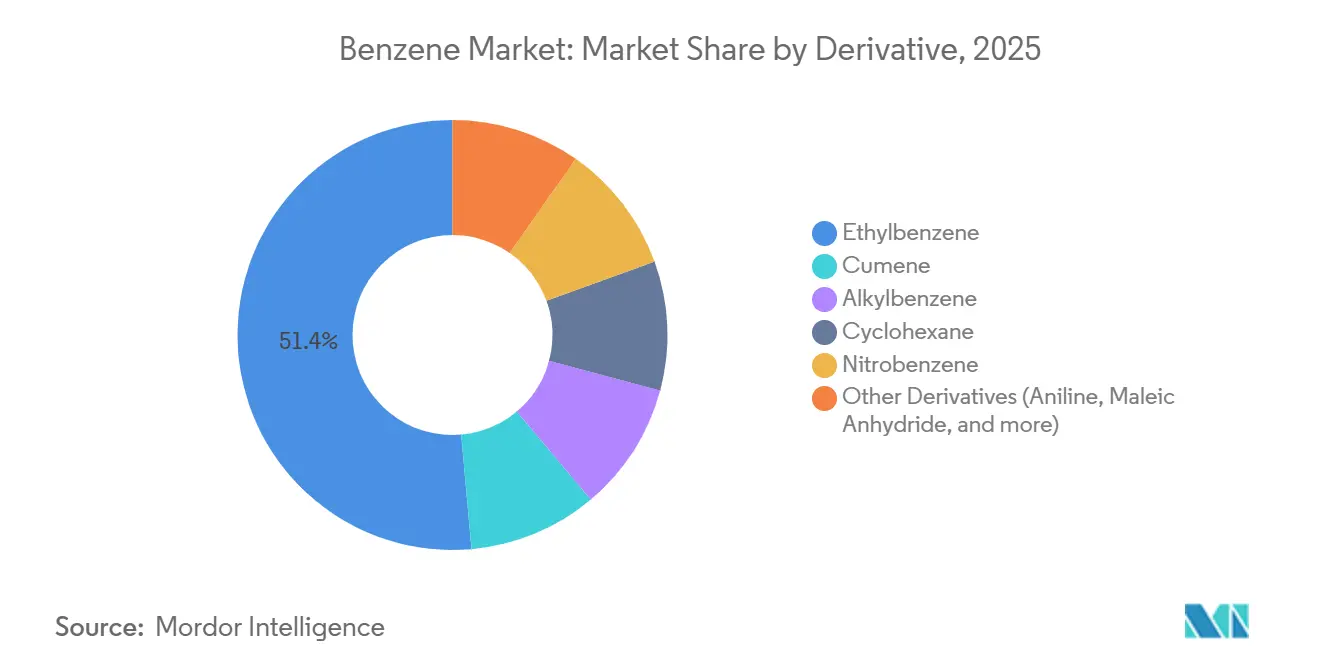

- By derivative, ethylbenzene accounted for 51.40% of 2025 volume, while nitrobenzene is forecast to expand at a 4.48% CAGR to 2031.

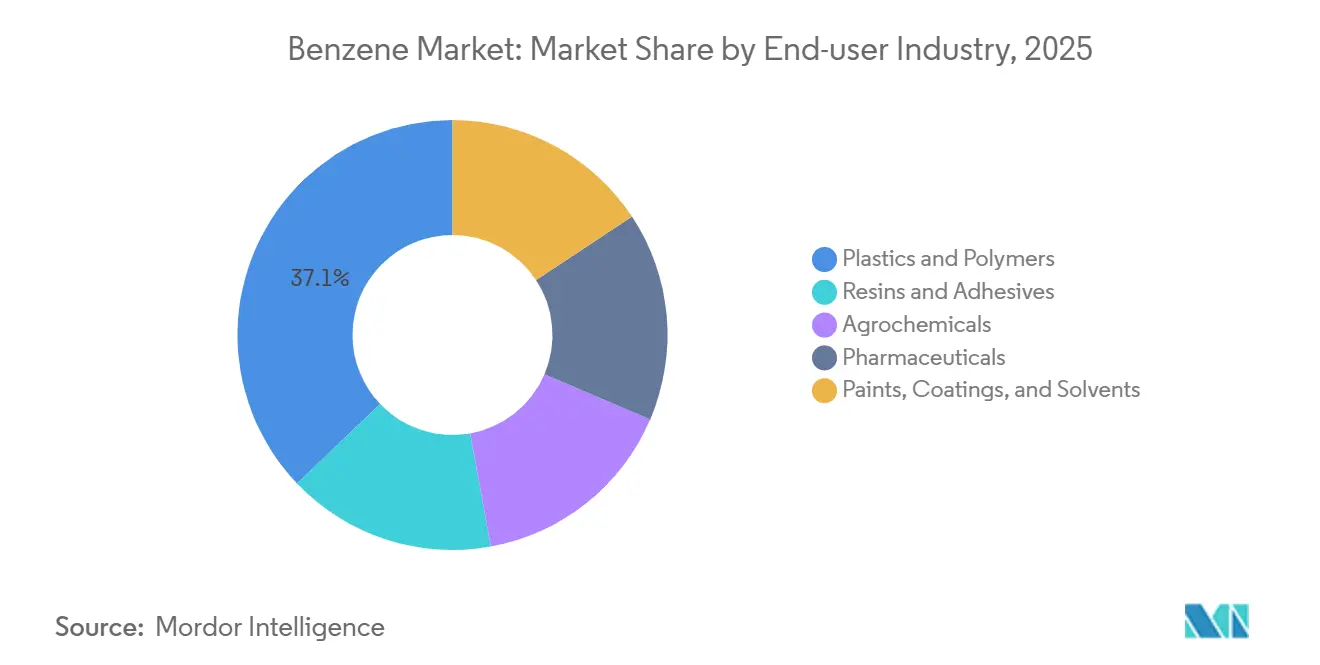

- By end-user industry, plastics and polymers led with 37.14% of 2025 demand, whereas pharmaceuticals posted the fastest growth at 4.91% CAGR through 2031.

- By geography, Asia-Pacific captured 55.80% of 2025 consumption and is set to grow at a 4.32% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Benzene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand growth for styrene-based polymers in packaging and automotive | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Downstream chemical capacity additions by integrated Asian producers | +1.0% | Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Recovery of construction activity lifting phenol and caprolactam chains | +0.8% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Rising uptake of alkylbenzene surfactants in emerging economies | +0.5% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Expanding pharmaceutical demand for aniline intermediates | +0.3% | India, China, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Styrene-Based Polymers in Packaging & Automotive

Styrene monomer consumed about 51% of global benzene supply in 2025, underpinning polystyrene markets for packaging and acrylonitrile-butadiene-styrene resins for automotive interiors. Asia-Pacific registers 4-5% annual growth in polystyrene consumption, supported by e-commerce logistics and cold-chain expansion, while North American and European demand grows below 2% amid single-use plastics restrictions. Automotive lightweighting pushes ABS and styrene-acrylonitrile resins into dashboards and exterior trim, sustaining benzene throughput even when packaging moderates. Integrated investments such as BASF’s 1 million tpa cracker-styrene complex in Zhanjiang, started in November 2025, exemplify strategic co-location that captures margin and mitigates price volatility. Inventory cycles in both packaging and automotive impose simultaneous supply-chain risks, making flexible production scheduling critical for benzene market participants.

Capacity Additions for Downstream Chemicals by Integrated Producers in Asia

Between 2023 and 2025, Asian complexes added about 12 million tpa of aromatics, anchored by Sinopec-Aramco’s USD 10 billion Fujian project and Reliance’s USD 9.75 billion crude-to-chemicals facility. Direct crude-to-aromatics technology trims benzene cash costs by USD 50-80 per ton versus European naphtha cracker routes, widening the competitiveness gap. The April 2025 framework for a 1.5 million tpa aromatics plant in Yanbu extends this model to the Gulf, positioning the region as a swing exporter to Europe and Africa. Spot prices in Asia fell from USD 900 per ton in January 2025 to USD 728 per ton in July 2025, reflecting the oversupply cycle. Non-integrated producers consequently curtailed run rates or exported at breakeven, underscoring the necessity of downstream linkages within the benzene market.

Recovery of Construction Sector Boosting Phenol & Caprolactam Chains

Phenol resins for plywood and caprolactam for nylon-6 electrical fittings gain momentum as residential and infrastructure spending rebounds in India and selective European markets. India’s phenol demand reached 650,000 tons in 2025 and is growing near 9% annually under the National Infrastructure Pipeline. Cumene capacity such as INEOS’s 750,000 tpa unit, ramped up in March 2025, is set to leverage phenol-acetone co-production, though it remains exposed to construction PMI swings. Nylon-6 growth in automotive air-intake manifolds and industrial textiles cushions demand variability, helping stabilize benzene allocations in the phenol and cyclohexane value chains.

Growing Adoption of Alkylbenzene-Based Surfactants in Emerging Markets

In 2023, the volume of linear alkylbenzene sulfonate increased, with projections indicating further growth by 2034, marking a steady CAGR. Asia-Pacific represents roughly half of LAB demand, driven by the transition from bar soaps to liquid detergents in India, Indonesia, and Vietnam. Cepsa, holding a near 20% share, serves Middle Eastern and Latin American exporters, demonstrating the globalized LAB network. Integrated olefin-aromatics plants in Saudi Arabia capitalize on captive benzene and alpha-olefin streams, enabling lower delivered costs than European or North American suppliers. Household cleaning products’ low-income elasticity ensures underlying stability, positioning surfactants as a dependable avenue for incremental benzene market demand[1]SABIC, “Corporate Fact Sheet 2026,” sabic.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent occupational exposure limits and litigation risk | -0.6% | North America, Europe, emerging China | Short term (≤ 2 years) |

| Crude-oil-linked feedstock price volatility | -0.4% | Global, sharper on non-integrated producers | Short term (≤ 2 years) |

| Competing C4 aromatics routes for derivatives | -0.2% | North America, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Occupational Exposure Limits & Litigation Risk

OSHA caps benzene exposure at 1 ppm time-weighted average, with similar thresholds under the European Union’s REACH framework, compelling continuous air monitoring, personal protective equipment, and medical surveillance[2]U.S. Occupational Safety and Health Administration, “Benzene Safety and Health Topics,” osha.gov. Compliance adds USD 5-10 per ton to production costs in mature regions. Litigation precedents, including refinery worker settlements, elevate liability premiums and accelerate plant closures such as INEOS’s scheduled Sarnia exit in June 2026. Regulators in China have begun tightening enforcement, narrowing historical cost advantages for some Asian sites. High compliance spending, combined with muted local derivative demand, underpins a wave of rationalization that redistributes benzene market capacity toward integrated low-cost hubs.

Volatility of Crude-Oil-Linked Feedstock Prices

Naphtha tracks Brent crude within a USD 50-100 per ton spread, translating price oscillations directly into benzene cash costs. Brent fluctuated between USD 70 and USD 90 per barrel during 2024-2025, squeezing benzene-naphtha spreads from USD 440 to USD 335 per ton. Non-integrated producers struggle to hedge such swings, while integrated refiners offset volatility through internal transfer pricing. Spot demand deferral during falling crude cycles intensifies price drops, forcing run-rate cuts or breakeven exports. Crude-to-chemicals platforms in India and China lower benzene cash costs by up to USD 80 per ton, reinforcing competitive divergence inside the benzene market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Derivative: Ethylbenzene Dominates Volume, Nitrobenzene Drives Growth

Ethylbenzene held 51.40% of global demand in 2025, anchoring the benzene market through styrene monomer for polystyrene, ABS, and styrene-butadiene rubber. While the overall benzene market sees slight expansion, growth in polystyrene is tempered by packaging legislation in developed economies. Cumene plays a pivotal role, feeding into phenol-acetone chains associated with construction panels and polycarbonate glazing. Nitrobenzene, while smaller today, records the highest 4.48% CAGR, supported by the polyurethane insulation push and automotive lightweighting. Alkylbenzene contributes to steady surfactant demand, and cyclohexane underpins nylon-6. Specialty outlets such as maleic anhydride and chlorobenzenes collectively remain limited. Integrated complexes, able to swing output among these derivatives, capture diversification benefits unavailable to single-derivative plants, especially during styrene down-cycles.

The benzene market share leadership gives ethylbenzene pricing influence, yet margin resilience increasingly gravitates toward nitrobenzene and pharmaceutical aniline, where ISO-certified supply chains secure premiums. Commodity ethylbenzene plants in Europe face tightening spreads, while Asian nitrobenzene units linked to local MDI facilities post stable earnings. Cross-derivative optionality, such as reallocating benzene from ethylbenzene to nitrobenzene when styrene spreads compress, emerges as a tactical lever for integrated producers. Merchant suppliers without downstream capture must rely on export arbitrage, exposing them to freight, currency, and spot volatility.

By End-User Industry: Plastics Lead, Pharmaceuticals Accelerate

Plastics and polymers consumed 37.14% of benzene in 2025, driven by polystyrene packaging and ABS components. As e-commerce and light-vehicle production counterbalance regulatory challenges, the segment experiences growth. Resins and adhesives align closely with industrial GDP and infrastructure investments. Agrochemicals are seeing growth driven by heightened crop-protection efforts in Latin America and Southeast Asia. Paints, coatings, and solvents are closely tied to automotive refinishing and renovations in the building sector.

Pharmaceuticals outpace all other industries with a 4.91% CAGR to 2031. India and China lead the way in generics production, utilizing benzene-derived aniline for both paracetamol and sulfonamide antibiotics. Producers who uphold traceability systems enjoy higher specialty margins in the benzene sector. Meanwhile, textiles, electronics, and personal care industries contribute the remaining share, adding diversity to the portfolio. As a result, benzene market players linked to pharmaceutical supply chains find themselves buffered against the cyclical fluctuations of commodity plastics.

Geography Analysis

Asia-Pacific retained 55.80% of global volume in 2025 and is set to post a 4.32% CAGR through 2031. China alone runs more than 18 million tpa of capacity, augmented by Sinopec’s multi-site expansions and the Fujian complex under construction for a 2027 start-up. India’s Reliance crude-to-chemicals hub adds 3.5 million tpa BTX capability, elevating the country to net-export status by 2028. Japan and South Korea emphasize yield optimization and specialty derivatives, exporting surplus benzene to Taiwan. Thailand and Malaysia fill regional logistics gaps through PTT Global Chemical’s 2.42 million tpa and ChemOne’s 656 thousand tpa projects, respectively. Lower cash costs, flexible feed slates, and captive derivatives collectively anchor Asia-Pacific leadership in the benzene market.

In North America, US Gulf Coast refineries and ethylene crackers form the backbone, yet the pivot toward ethane feed reduces benzene co-product output, forcing styrene makers to import. OSHA’s 1 ppm exposure limit and litigation premiums raise fixed costs, prompting plant rationalization exemplified by INEOS’s Sarnia closure plan. Canada and Mexico contribute modest capacity, relying on imports during maintenance or unplanned outages.

In Europe, energy pricing, REACH compliance, and aging assets compress margins. BASF’s Verbund network maintains competitiveness through integration, while independent units review divestment or shutdown options. Import reliance deepens as Middle Eastern and Asian exporters target Antwerp-Rotterdam-Amsterdam terminals. Projects such as SABIC’s electrically heated furnace in the Netherlands aim to cut emissions and enhance operational flexibility.

South America’s benzene market is dominated by Braskem’s main chemicals system in Brazil. Operational disruptions in 2025 trimmed exports and weighed on regional prices. The Transforma Sul and Transforma Rio programs will raise gas feedstock share, likely lowering future benzene co-production and tightening supply. Argentina and other producers contribute minor volumes, so incremental demand may be met by imports.

In the Middle East and Africa, Aramco-Sinopec’s Yanbu project and the Amiral complex at Jubail expand integrated aromatics in the Gulf. Export optionality through Red Sea and Gulf terminals positions the region as a swing supplier to Europe and Africa. South African demand remains import-oriented. Logistics risks, such as Red Sea transit disruptions, persist, encouraging buyers to diversify contract portfolios within the benzene market.

Competitive Landscape

The benzene market is fragmented. Integration with styrene, phenol, or cyclohexane units sustains their margin profile, while merchant players face spread compression. SABIC’s 40% capacity uplift at Nexlene and BASF’s Zhanjiang complex underscore commitment to value-chain capture. Furthermore, bio-based benzene remains at the pilot scale. Platforms such as Bio-TCat and BioForming demonstrate technical feasibility but remain 2-3× higher in cost. Commercial roll-out depends on carbon-credit monetization and regulatory incentives. Until then, petro-derived benzene will dominate, albeit with rising pressure to decarbonize aromatics value chains through renewable electricity and circular feedstocks.

Benzene Industry Leaders

LG Chem

BASF

China Petrochemical Corporation

Shell

ExxonMobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Tamilnadu Petroproducts Limited achieved a significant regulatory milestone for its expansion project, obtaining the green light from the Tamil Nadu Pollution Control Board for its enlarged Linear Alkyl Benzene (LAB) facility. This consent permits the company to operate and release emissions, adhering to set environmental benchmarks.

- September 2025: Farabi Petrochemicals Co. inaugurated its fourth integrated linear alkyl benzene (LAB) plant in Yanbu Industrial City, with total investments of SAR 3.6 billion (USD 950 million). The new facility represents a significant addition to its production capacity, boosting annual output by 120,000 metric tons of LAB.

Global Benzene Market Report Scope

Benzene is an organic compound with the molecular formula C6H6. It is a clear, colorless, volatile liquid at room temperature and is considered a hazardous and carcinogenic chemical. Benzene is produced from five primary sources, including catalytic reforming of naphtha (reforming), conversion of toluene and/or xylenes to benzene (hydrodealkylation), recovery from ethylene plant pyrolysis gasoline (steam cracking), conversion of toluene to benzene (toluene disproportionation), and conversion of toluene and C9/C10 aromatics to benzene and xylenes (trans alkylation). The benzene market is segmented by derivative and geography. By derivative, the market is segmented into ethylbenzene, cumene, alkylbenzene, cyclohexane, nitrobenzene, and other derivatives (aniline, maleic anhydride, etc.). The report also covers the market size and forecast for the market in 17 countries across major regions. For each segment, the market sizing and forecast have been done based on volume (tons).

| Ethylbenzene |

| Cumene |

| Alkylbenzene |

| Cyclohexane |

| Nitrobenzene |

| Other Derivatives (Aniline, Maleic Anhydride, and more) |

| Plastics and Polymers |

| Resins & Adhesives |

| Agrochemicals |

| Pharmaceuticals |

| Paints, Coatings, and Solvents |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Derivative | Ethylbenzene | |

| Cumene | ||

| Alkylbenzene | ||

| Cyclohexane | ||

| Nitrobenzene | ||

| Other Derivatives (Aniline, Maleic Anhydride, and more) | ||

| By End-user Industry | Plastics and Polymers | |

| Resins & Adhesives | ||

| Agrochemicals | ||

| Pharmaceuticals | ||

| Paints, Coatings, and Solvents | ||

| Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected global demand for benzene in 2031?

Global consumption is expected to reach 71.19 million tons by 2031 from 59.22 million tons in 2026, reflecting a 3.75% CAGR.

Which derivative will contribute most to incremental growth through 2031?

Nitrobenzene leads growth at a 4.48% CAGR, buoyed by rising polyurethane and pharmaceutical demand.

Why is Asia-Pacific dominant in the benzene market?

Integrated crude-to-chemicals complexes, lower cash costs, and large downstream styrene and phenol chains together anchor 55.80% of 2025 volume with a 4.32% CAGR outlook.

How do regulatory limits affect North American benzene producers?

OSHA’s 1 ppm exposure limit increases operating costs by USD 5-10 per ton, prompting plant closures and capacity reviews.

Which end-user industries are expanding fastest?

Pharmaceutical intermediates post the highest 4.91% CAGR, followed by agrochemicals and nylon applications that each grow above the overall market rate.

Page last updated on: