Sodium Cocoyl Isethionate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

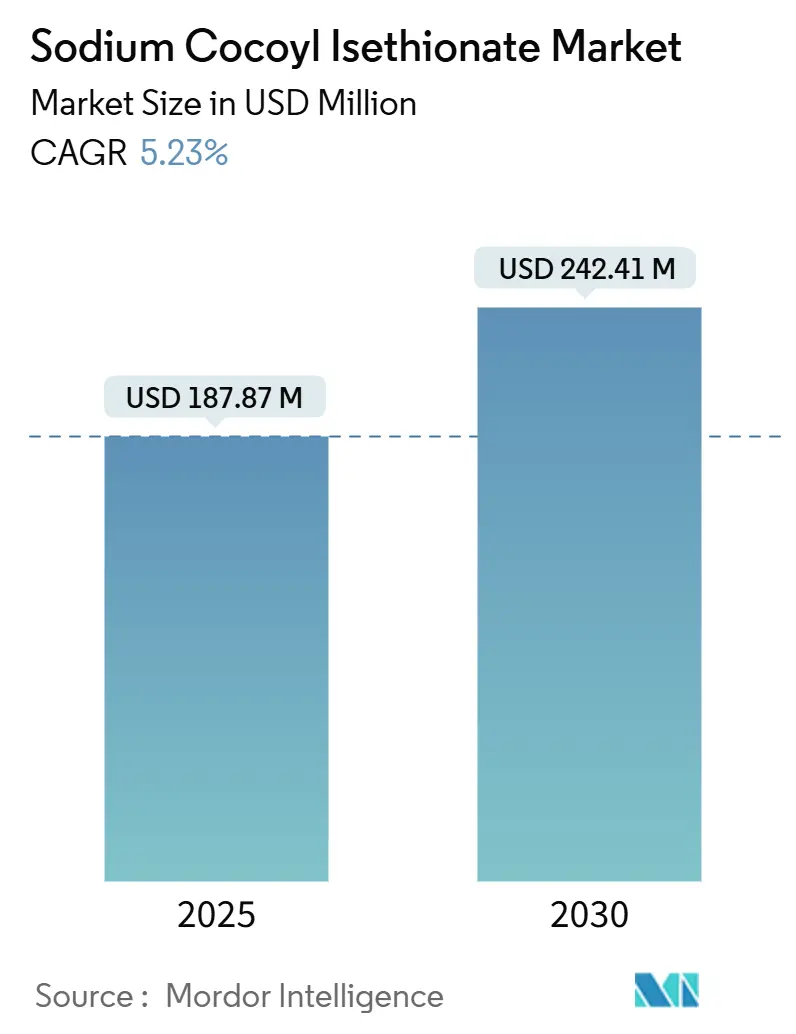

| Market Size (2025) | USD 187.87 Million |

| Market Size (2030) | USD 242.41 Million |

| Growth Rate (2025 - 2030) | 5.23% CAGR |

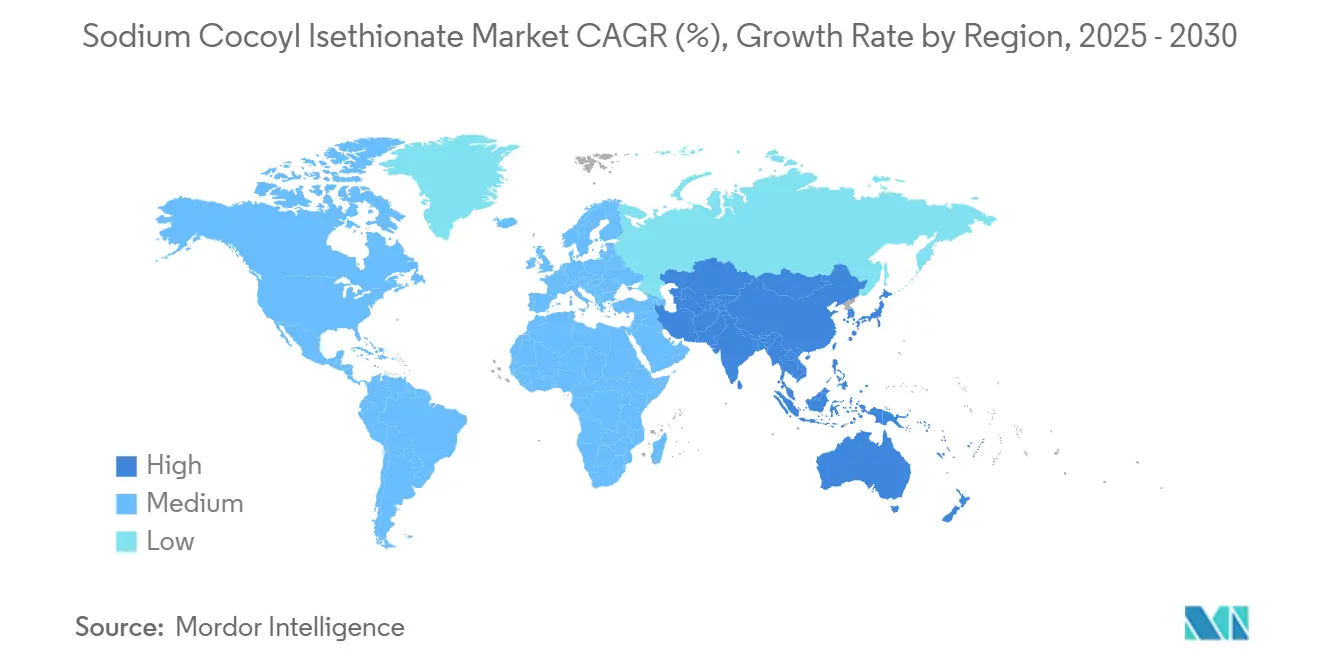

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sodium Cocoyl Isethionate Market Analysis by Mordor Intelligence

The Sodium Cocoyl Isethionate Market size is estimated at USD 187.87 Million in 2025, and is expected to reach USD 242.41 Million by 2030, at a CAGR of 5.23% during the forecast period (2025-2030). Solid consumer demand for mild, sulfate-free formulations, steady innovation in waterless beauty formats, and tightening regulations that favor biodegradable surfactants underpin this expansion. Powder grades continue to anchor volume growth as syndet and solid bars gain mainstream acceptance. Asia-Pacific remains the strategic growth engine because of its coconut supply advantages, expanding middle class, and the rapid localization of premium personal-care brands. Competitive intensity is rising as large chemical multinationals and specialty surfactant makers race to secure certified feedstocks, optimize 1,4-dioxane-free processes, and integrate downstream to private-label and contract manufacturing channels. Cost volatility in coconut and palm supply chains, plus the persistent price gap with commodity sulfates, will keep margin management in sharp focus.

Key Report Takeaways

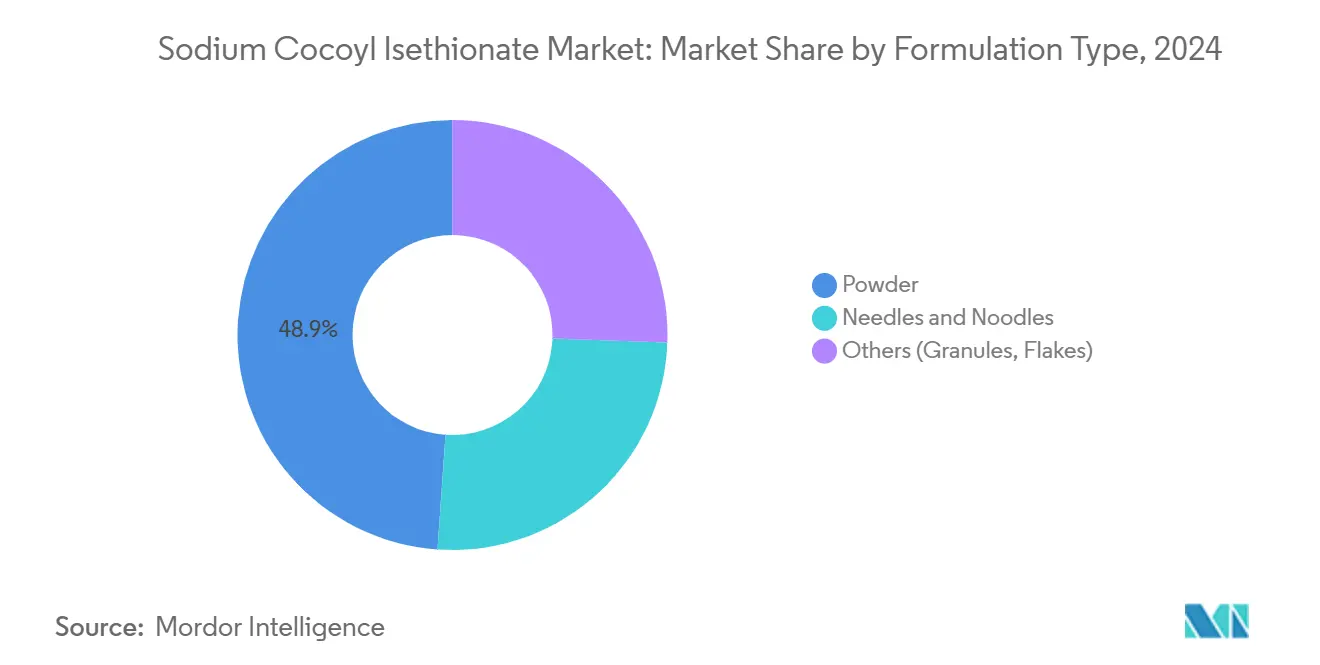

- By formulation type, powder variants led with 48.89% revenue share in 2024, while needles and noodles are projected to advance at a 5.41% CAGR through 2030.

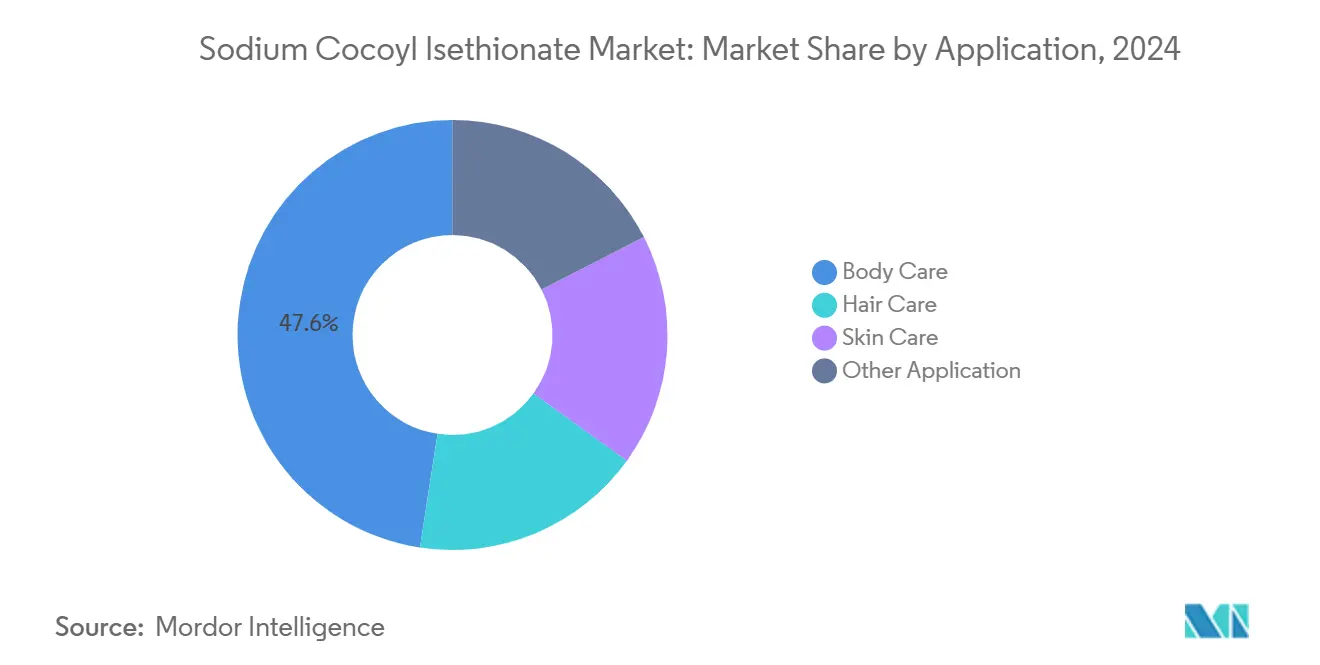

- By application, Body care accounted for 47.58% of the Sodium Cocoyl Isethionate market share in 2024, whereas hair care products are expanding at a 5.76% CAGR to 2030.

- By geography, Asia-Pacific dominated with 37.78% share in 2024 and is growing at a 5.85% CAGR to 2030.

Global Sodium Cocoyl Isethionate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Mild and Sulfate-free Surfactants | +1.2% | Global, stronger in North America and Europe | Medium term (2-4 years) |

| Rising Adoption in Solid Shampoo, Facial and Baby Cleansers | +0.9% | Global, led by Asia-Pacific and North America | Long term (≥ 4 years) |

| Preference for Naturally-derived, Eco-friendly Ingredients | +0.8% | Primarily North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Regulatory Push for Biodegradable, Low-toxicity Surfactants | +0.7% | Europe and North America, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of Water-less Beauty Formats Driving High-active Powders | +0.5% | Global, early uptake in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Mild and Sulfate-free Surfactants

Sodium Cocoyl Isethionate (SCI) has shifted from niche option to mainstream backbone in premium hair-care and skin-cleansing formulas as dermatological studies confirm its non-sensitizing profile up to 50% load in rinse-off applications. Color-protection claims in salon-grade shampoos rely on SCI’s ability to cleanse without stripping dye molecules, helping brands capture price premiums. Clariant’s “gentle giants” portfolio shows that performance foam and mildness coexist when isethionate chemistry replaces traditional sulfates[1]Clariant AG, “Gentle Giants Portfolio Technical Brochure,” clariant.com. Social media conversations around scalp sensitivity and barrier health accelerate consumer migration, while retailers expand sulfate-free shelf space, reinforcing the demand loop.

Rising Adoption in Solid Shampoo, Facial and Baby Cleansers

Waterless beauty has entered the mass channel, propelling syndet bars that meet airline and zero-waste criteria. SCI’s high binding efficiency gives bars structural strength and quick lather, enabling lines such as Stephenson’s Syndopal range to claim a melt-free user experience even in humid climates. Infant care gains momentum because SCI’s irritation score is lower than conventional sulfates, aligning with pediatric dermatology guidelines. Formulation research shows that SCI combined with microcrystalline cellulose delivers gentle exfoliation and stable textures in anhydrous formats. The segment crossover into facial cleansing sticks and foaming tablets broadens channel exposure beyond niche eco-stores.

Preference for Naturally Derived, Eco-friendly Ingredients

Consumers scrutinize ingredient origin, and SCI’s coconut-oil pedigree provides a tangible plant narrative. BASF has already certified roughly 150 surfactants, including SCI, under the Roundtable on Sustainable Palm Oil (RSPO) Mass Balance scheme to assure deforestation-free sourcing. The biodegradability profile shortens aquatic persistence, satisfying brand promises under new eco-labels. Although biosurfactant start-ups attract venture capital, they validate, rather than threaten, the trajectory toward nature-aligned chemistries. Enhanced skin compatibility further reinforces the clean-beauty positioning that drives premium pricing.

Regulatory Push for Biodegradable, Low-toxicity Surfactants

The EU Chemicals Strategy for Sustainability elevates biodegradation and toxicity screens, positioning SCI favorably versus ethoxylated alternatives. Digital ingredient disclosure under the updated Detergents Regulation strengthens downstream demand for transparent supply chains. New York State’s 1 ppm cap on 1,4-dioxane acts as a blueprint for wider U.S. adoption, indirectly shifting volume toward SCI because its process route avoids ethoxylation. ISO 16128 natural-origin thresholds let brands promote SCI-based products under regulated “natural” claims, helping justify price premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Cost Relative to SLS/SLES | -1.8% | Global, price-sensitive segments | Short term (≤ 2 years) |

| Feed-stock Volatility (coconut and palm supply chain) | -1.1% | Global, highest in Asia-Pacific | Medium term (2-4 years) |

| Stricter 1,4-dioxane Impurity Limits Raising Compliance Costs | -0.6% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Cost Relative to SLS/SLES

SCI trades three to five times the CIF price of commodity sulfates because of multi-step esterification, hydrogenation, and spray-drying stages lacking comparable scale economies. Margin constraints deter mass-market lines, especially in regions with tight disposable income. Brands that switch emphasize total-cost-of-use benefits such as reduced dermal complaints and fewer returns, but mainstream consumers still perceive only shelf price. As global capacity scales and continuous processes replace batch steps, cost gaps should narrow, though parity with sulfates is unlikely within the forecast window.

Feed-stock Volatility (Coconut and Palm Supply Chain)

Coconut oil prices swung between USD 1,900 and USD 2,050 per metric ton in 2025 as weather anomalies disrupted harvests in the Philippines and Indonesia[2]International Coconut Community, “Quarterly Coconut Oil Outlook 2025,” internationalcoconutcommunity.org. This volatility pinches SCI producers because fatty acid costs account for as much as 60% of manufacturing expense. Integrated players hedge with futures contracts and diversified sourcing, yet smaller firms face margin compression. Climate-resilient crop programs and synthetic biology routes to lauric alcohols, such as BASF’s fermentation partnership, aim to dilute reliance on natural harvest cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation Type: Powder Leads Sodium Cocoyl Isethionate Market, Flakes Sees Rapid Growth

In 2024, powder grades dominated the Sodium Cocoyl Isethionate market, capturing 48.89% of its total value. These grades have solidified their role as the primary surfactant backbone, not just for traditional solid bars and syndets, but also for an emerging trend: waterless cleansing formats. Their appeal lies in their low moisture content, extended shelf stability, and compatibility with high-active ingredients, aligning perfectly with the industry's pivot towards concentrated and plastic-free products. Innovations like micronized and dust-controlled variants are streamlining operations, reducing dispersion times, and cutting down batch cycles in facilities with high throughput.

Needles and noodles, growing at a 5.41% CAGR, are gaining traction due to their structured shapes, which enable predictable feeding, reduced dusting, and smoother flow in automated lines. Their uniform geometry ensures consistent wetting and rapid dissolution, appealing to contract manufacturers focused on dosing precision and operator safety. New formats with optimized aspect ratios and surface textures are driving adoption in hybrid surfactant bases and high-solid cleansing systems.The Others category, including flakesand granules, addresses specialized manufacturing needs like flowability, melt control, and particle uniformity. Flakes are valued for controlled melting in mid-temperature processes, while granules reduce airborne particulates and enhance hopper performance. Suppliers are differentiating through tailored particle engineering to improve wetting kinetics and batch consistency.

By Application: Body-care Leads Sodium Cocoyl Isethionate Market, Hair-care Sees Rapid Growth

In 2024, body-care claimed a dominant 47.58% share of the Sodium Cocoyl Isethionate market. The surge in body washes, shower gels, and syndet bars fueled this trend. As consumers pivoted to pH-balanced, moisturizing alternatives over traditional soap, the adoption of waterless, cardboard-packaged bar formats surged. Sodium Cocoyl Isethionate (SCI), known for its creamy lather and "soap-free" profile, seamlessly aligned with these sustainability-driven product claims.

Hair-care, on the other hand, emerged as the sector's fastest-growing segment. The demand was buoyed by sulfate-free shampoos, conditioners, and hybrid styling products. Brands turned to SCI for its dense foam and ability to minimize cuticle swelling. This not only bolstered claims of color protection and curl maintenance but also emphasized gentle scalp cleansing. The growth trajectory was further amplified by premium and salon categories, which leaned towards milder surfactant systems.

Skin-care saw consistent demand, particularly in facial cleansers, washes, and cream-based formulations. Backed by dermatologists, the emphasis on "gentle cleansing" routines and the rising trend of double-cleansing kept SCI in the limelight. Its soft-foam texture and compatibility with acidic pH systems made it a staple in sensitive-skin product lines.

Meanwhile, other applications such as spanning intimate-care, men's grooming, and pet-wash products witnessed gradual expansion. Formulators harnessed SCI's mildness across diverse pH environments. This strategic diversification not only stabilized overall market demand but also bolstered scale efficiencies for integrated producers.

Geography Analysis

Asia-Pacific generated 37.78% of global revenue in 2024 and is on track for a 5.85% CAGR to 2030, fueled by proximity to coconut feedstock, expanding middle-class incomes, and brand localization strategies that translate mildness claims into local languages. China and India dominate consumption, while Indonesia and the Philippines anchor raw-material processing and export refined SCI to global finished-goods hubs.

North America follows with a robust premium segment that rewards sulfate-free labels, bolstered by state regulations limiting 1,4-dioxane and microplastics. Distribution infrastructure supports fast replenishment, allowing direct-to-consumer innovators to iterate formulas rapidly. Europe mirrors North America in regulatory trajectory, and the Chemicals Strategy for Sustainability amplifies demand for biodegradable surfactants such as SCI. Tight feedstock logistics incentivizes European blenders to source lauric acids from certified plantations, reinforcing supply-chain transparency.

South America shows emergent potential as local firms tap regional biodiversity narratives to bundle SCI with native actives. Middle East and Africa remain nascent but benefit from rising disposable income and the spread of modern retail. Trade liberalization across the African Continental Free Trade Area could streamline intra-regional movement of raw materials, supporting broader penetration of the Sodium Cocoyl Isethionate market.

Competitive Landscape

The Sodium Cocoyl Isethionate market is moderately consolidated. BASF, Clariant, and Stepan leverage backward integration into fatty alcohols and global technical service centers, advancing RSPO-certified supply networks. Galaxy Surfactants and SEPPIC focus on tailor-made grades and collaborative formulation platforms to secure high-margin niches. The Sodium Cocoyl Isethionate market rewards providers that combine green chemistry credentials with application support. Companies deploy virtual labs and AI-assisted formulation tools to shorten development cycles for indie brands. Pricing power, therefore, hinges on volume capacity and the ability to co-create differentiated end-products.

Sodium Cocoyl Isethionate Industry Leaders

BASF

SEPPIC

Dow

Clariant

Galaxy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BASF has unveiled three new natural-based products, bolstering its commitment to sustainable personal care solutions. One of these, Dehyton PK45 GA/RA is a betaine sourced from Rainforest Alliance Certified coconut oil. Given its derivation from fatty acids in coconut oil, this strategic move could bolster the Sodium Cocoyl Isethionate market.

- March 2025: Galaxy Surfactants Limited partnered strategically with a global client to develop a new performance surfactants plant overseas. This move focuses on enhancing Galaxy’s global footprint in Sodium Cocoyl Isethionate (SCI) and specialty ingredient production.

Global Sodium Cocoyl Isethionate Market Report Scope

| Powder |

| Needles and Noodles |

| Others (Granules, Flakes) |

| Hair Care |

| Skin Care |

| Body Care |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Turkey | |

| Rest of Middle-East and Africa |

| By Formulation Type | Powder | |

| Needles and Noodles | ||

| Others (Granules, Flakes) | ||

| By Application | Hair Care | |

| Skin Care | ||

| Body Care | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Turkey | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Sodium Cocoyl Isethionate market?

The market is valued at USD 187.87 Million in 2025 and is projected to reach USD 242.41 Million by 2030 at a 5.23% CAGR.

Which region leads in demand for Sodium Cocoyl Isethionate?

Asia-Pacific holds the top position, accounting for 37.78% of 2024 global revenue and posting the fastest 5.85% CAGR.

Which application captures the largest share of Sodium Cocoyl Isethionate consumption?

Body care constitute 47.58% of 2024 revenue, driven by strong use in body washes, shower gels, and syndet bars.

How do regulations influence Sodium Cocoyl Isethionate adoption?

EU biodegradability mandates and U.S. 1,4-dioxane limits favor SCI, which inherently avoids ethoxylation and meets stricter safety thresholds.

Page last updated on: