Capryloyl Glycine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

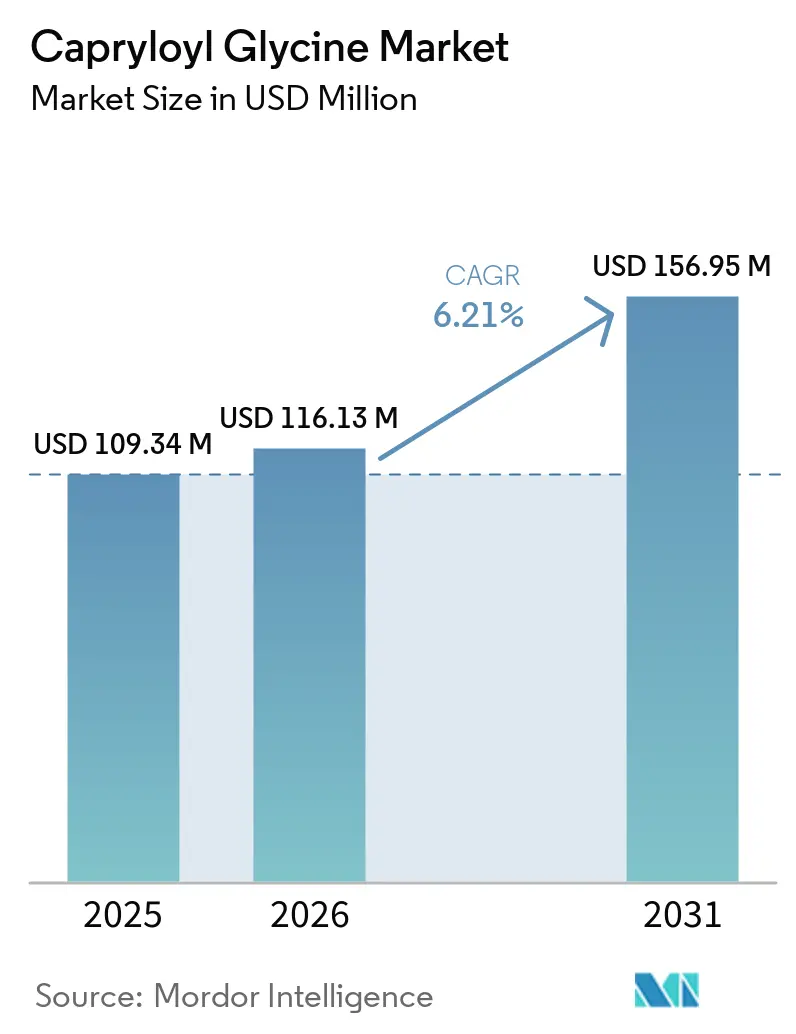

| Market Size (2026) | USD 116.13 Million |

| Market Size (2031) | USD 156.95 Million |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Capryloyl Glycine Market Analysis by Mordor Intelligence

The Capryloyl Glycine Market size is projected to expand from USD 109.34 million in 2025 and USD 116.13 million in 2026 to USD 156.95 million by 2031, registering a CAGR of 6.21% between 2026 to 2031. A global pivot toward sulfate-free, preservative-lite cleansing is underpinning demand as formulators replace legacy lauryl sulfates with amino-acid surfactants that deliver mildness, foam density, and sebum control in a single molecule. Growth is reinforced by the impending European Union ban on intentionally added microplastics, which is accelerating the shift toward biodegradable surfactants that satisfy both cleansing and preservation requirements. Asia-Pacific retains a structural cost advantage through high-volume production in China and Japan, while K-beauty and J-beauty exports normalize the use of low-pH, amino-acid-based cleansers worldwide. Parallel momentum in men’s grooming, waterless solid formats, and pharmaceutical-grade dermatology lines widens commercial runway, with suppliers competing on purity profiles, sustainability certifications, and green-chemistry processing.

Key Report Takeaways

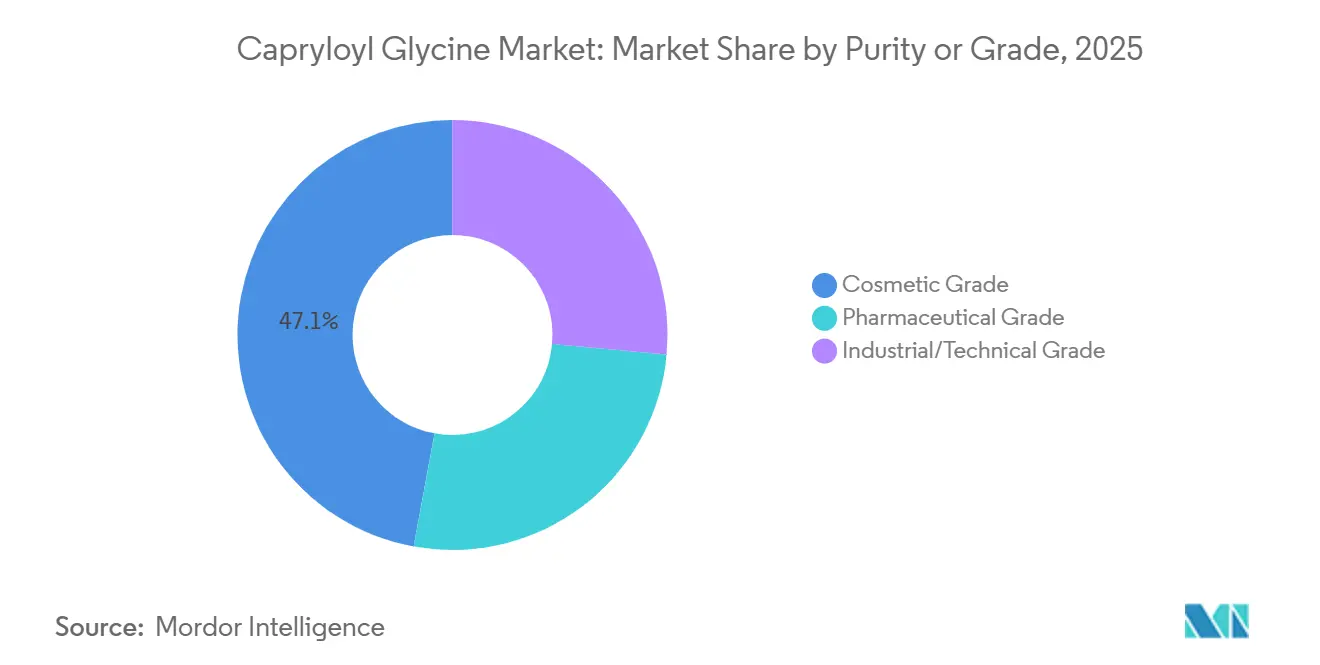

- By purity/grade, cosmetic grade held 47.12% of the capryloyl glycine market share in 2025, while pharmaceutical grade is projected to expand at a 6.55% CAGR through 2031.

- By form, powder led with 54.33% revenue share in 2025; liquid/solution formulations are forecast to grow at 6.56% CAGR to 2031.

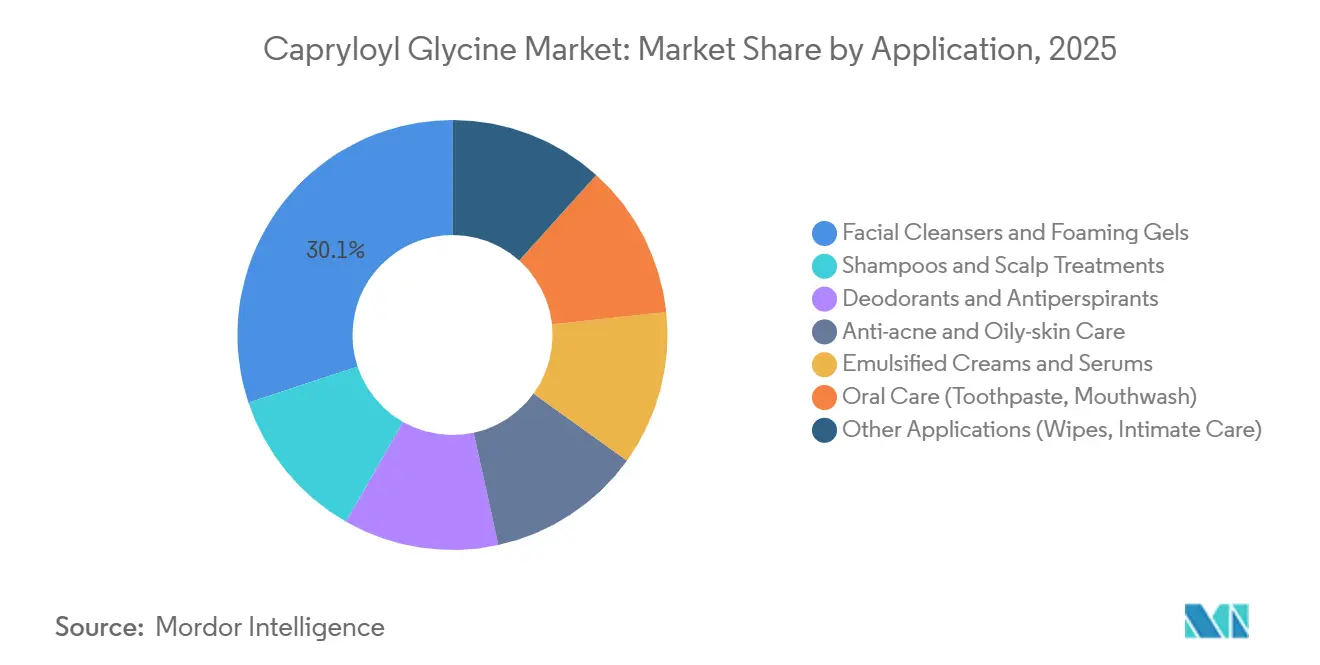

- By application, facial cleansers accounted for 30.11% of the capryloyl glycine market size in 2025, whereas anti-acne and oily-skin care are expected to advance at a 6.89% CAGR over the outlook period (2026-2031).

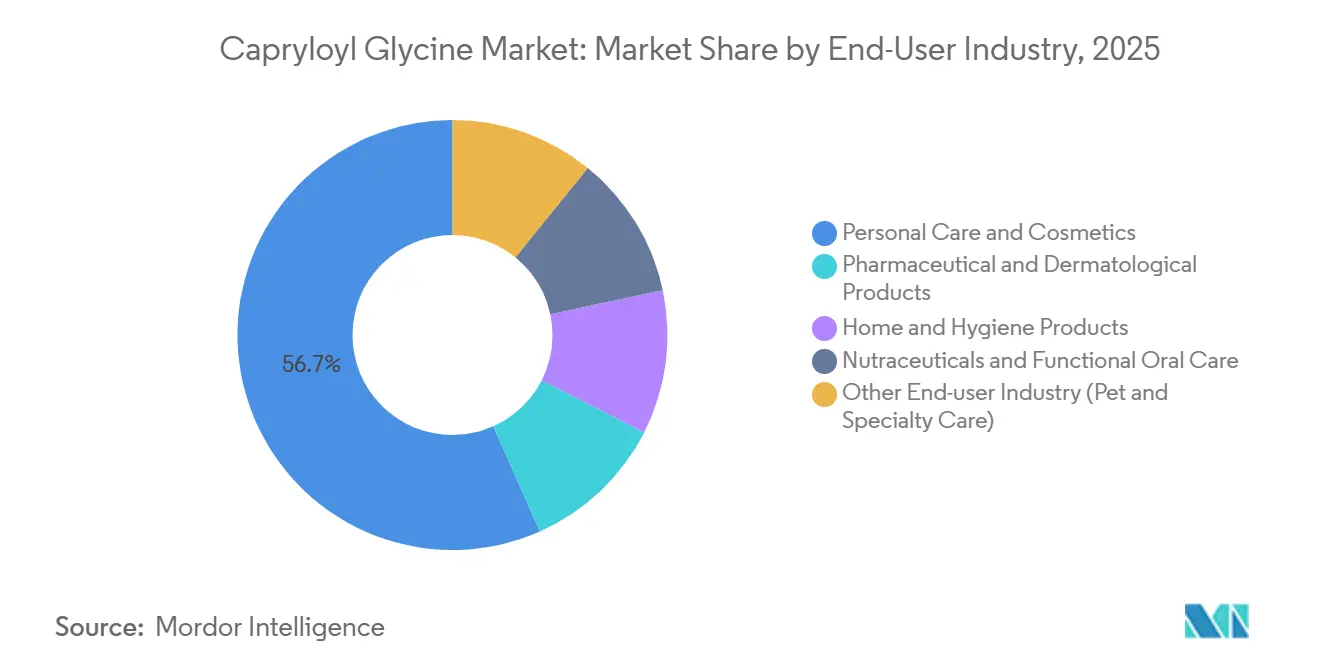

- By end-user industry, personal care and cosmetics captured 56.67% market share in 2025, while pharmaceutical and dermatological products are expected to post the fastest 7.03% CAGR through 2031.

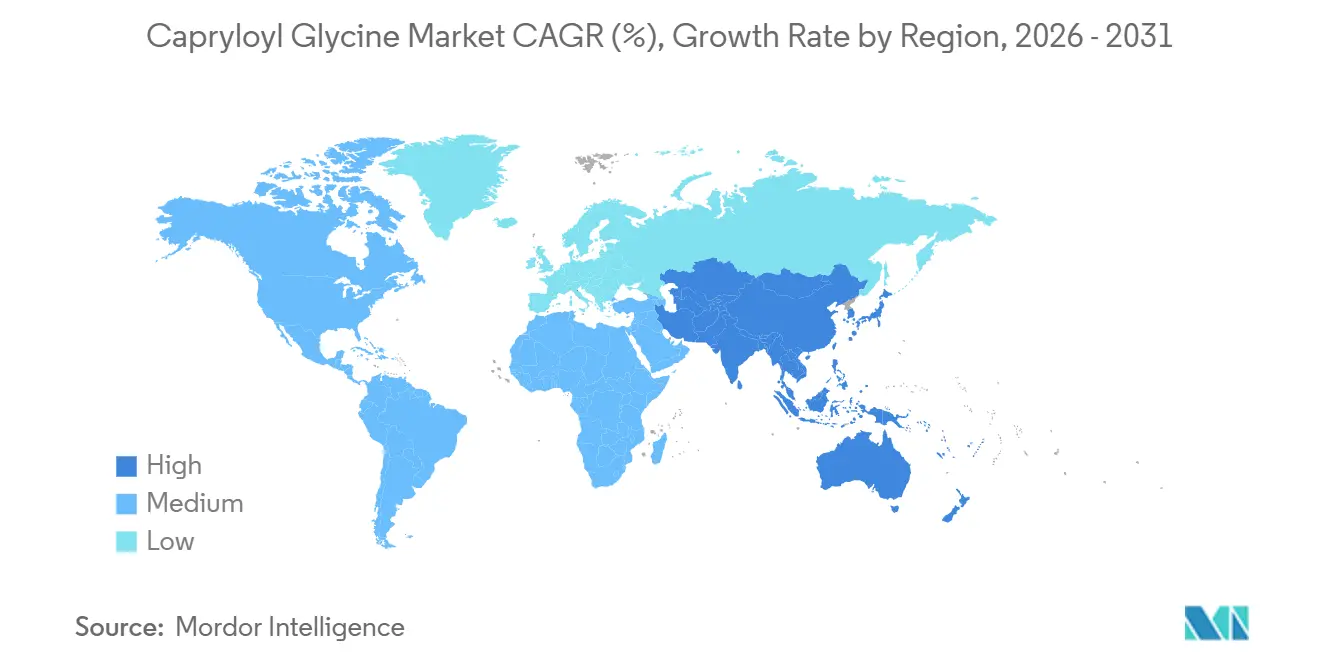

- By geography, Asia-Pacific contributed 43.31% of the 2025 global revenue and is expected to grow at a 6.98% CAGR for the forecast period (2026-2031), the highest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Capryloyl Glycine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward preservative-free and sulfate-free formulations | +1.2% | Global, early adoption in North America & EU | Medium term (2-4 years) |

| Rising use of cosmetic-grade amino-acid derivatives | +1.4% | APAC core (Japan, South Korea, China) with spill-over to North America | Short term (≤2 years) |

| Expansion of men’s grooming and sensitive-skin lines | +0.9% | North America, Europe, urban APAC markets | Medium term (2-4 years) |

| Impending EU microplastics ban boosting biodegradable surfactants | +1.5% | Europe, spill-over to Canada and select APAC markets | Short term (≤2 years) |

| Rise of water-less solid-format cosmetics | +0.8% | Global, concentrated in North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Preservative-Free and Sulfate-Free Formulations

Formulators are eliminating both sulfates and standalone preservatives, creating demand for multifunctional molecules that deliver cleansing, antimicrobial cover, and sebum regulation simultaneously. Capryloyl glycine supplies an anionic head group for foam plus a lipophilic tail that disrupts microbial membranes, allowing brands to reduce parabens and phenoxyethanol without sacrificing shelf stability. A 2025 comparative study showed lauroyl-glycine analogs matched sodium dodecyl sulfate in interfacial adsorption yet caused 35% less protein denaturation, validating the switch to amino-acid surfactants in shampoos and facial cleansers[1]Li Y. et al., “Lauroyl Glycine Surfactants Exhibit Low Protein Denaturation,” frontiersin.org. Clean-beauty retailers in North America and Europe blacklist sulfates, fast-tracking commercial uptake, while price-sensitive markets lag because consumers do not yet penalize sulfate usage.

Rising Use of Cosmetic-Grade Amino-Acid Derivatives

Asia-Pacific normalizes amino-acid surfactants thanks to decades of low-pH formulation expertise in Japan and South Korea. Ajinomoto’s Amisoft and Amilite lines validated large-scale commercial performance, and capryloyl glycine is tracing the same curve as brands seek shorter-chain acyl groups for enhanced sebum control. Sino Lion’s existing 30,000 tons capacity, with plans to exceed 100,000 tons, signals long-run confidence in cosmetic-grade demand[2]Sino Lion, “Capacity Expansion Announcement,” sinolion.com. Zwitterionic behavior at physiological pH enables capryloyl glycine to form mixed micelles with betaines, lowering overall surfactant load and viscosity adjustments, a property prized in multi-step K-beauty and J-beauty regimens.

Expansion of Men’s Grooming and Sensitive-Skin Lines

Men’s grooming SKUs incorporate capryloyl glycine into cleansers, shave gels, and scalp formulations to balance higher male sebum output without stripping lipids. Dove Men+Care’s 2024 sensitive-skin cleanser lists the ingredient to reinforce mildness claims, evidencing mainstream crossover. Dermatologists recommend amino-acid surfactants to maintain the acid mantle and reduce post-shave irritation, aligning with urban male consumers’ preference for efficacy and minimal routines. Sensitive-skin offerings that replace cocamidopropyl betaine further broaden appeal in rosacea or eczema lines.

Impending EU Microplastics Ban Boosting Biodegradable Surfactants

The 2027 EU restriction on intentionally added microplastics bans acrylates, copolymers, and polyethylene exfoliants, obligating brands to reformulate rinse-off products. Amino-acid surfactants biodegrade greater than 90 % in 28 days under OECD-301B, meeting new standards while offering viscosity and film-forming support when blended with salts and polyols. SEPPIC and Ajinomoto are securing COSMOS and NATRUE certifications in anticipation of spill-over rules in Canada and high-end APAC markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited awareness among mass-market brands | -0.6% | India, Southeast Asia, Latin America, MEA | Medium term (2-4 years) |

| Feed-stock sustainability risk (palm/coconut) | -0.4% | Global, acute exposure in APAC and Europe | Short term (≤2 years) |

| Performance drop in hard-water applications | -0.3% | Hard-water regions of North India, Northern China, MENA | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Limited Awareness Among Mass-Market Personal-Care Brands

Emerging-market formulators default to sodium lauryl sulfate because of lower raw-material costs and familiarity, underestimating total formulation savings from reduced preservatives and co-surfactants. Capryloyl glycine costs three to five times more per active kilogram, and marketing teams in price-sensitive regions struggle to translate the value proposition into shelf pricing. Supplier-led workshops and cost-in-use calculators are gradually bridging the gap, yet widespread conversion remains constrained until consumer willingness to pay rises.

Feed-Stock Sustainability Risk (Palm/Coconut Dependency)

Caprylic acid derives mainly from palm kernel and coconut oil. Weather-driven supply tightness in Southeast Asia pushed coconut oil to USD 1,400/ton in Q3 2025, creating volatility. Brands committed to Roundtable on Sustainable Palm Oil certification absorb premiums that shrink margin on amino-acid surfactants, while only 19% of global palm output meets RSPO Mass Balance or higher criteria. Pilot-scale fermentation of medium-chain fatty acids offers a long-term hedge but remains cost-prohibitive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Purity/Grade: Pharmaceutical Uptake Outpaces Cosmetic Maturity

Cosmetic-grade capryloyl glycine captured 47.12% of 2025 revenue via facial cleansers and sulfate-free shampoos that conform to ECOCERT parameters. The Capryloyl Glycine market size for pharmaceutical-grade material is projected to advance at 6.55% CAGR through 2031 as dermatology brands demand USP-level heavy-metal and endotoxin limits. SEPPIC’s LIPACIDE C8G commands a 20-30% premium, enabling formulators to claim hospital-grade purity.

Pharmaceutical-grade versatility extends into prescription acne gels and post-procedure washes, where lower bioburden thresholds are obligatory. Industrial-grade uses in eco-labeled household cleaners remain niche yet steadily expand as brands seek readily biodegradable alternatives. The Capryloyl Glycine market benefits from this two-track dynamic, with cosmetic volumes financing the process controls needed for higher-margin medical lines.

By Form: Liquid Solutions Gain on Handling Efficiency

Powder held 54.33% of the 2025 market share, dominating waterless bars and powder-to-foam cleansers. Contract manufacturers pursuing lean GMP (Good Manufacturing Practices) operations, however, are pivoting toward 25-30% liquid concentrates that cut mixing times by 15-20 minutes per batch and eliminate dust-extraction infrastructure, supporting a 6.56% CAGR to 2031.

Liquid concentrates ease inline dosing yet introduce preservative and shelf-life trade-offs, typically requiring 0.5-1% phenoxyethanol and offering 12-18 months stability versus up to three years for powder. The Capryloyl Glycine market share for liquid solutions is therefore highest in turnkey facilities producing fast-moving SKUs where throughput trumps storage life.

By Application: Anti-Acne Leads Growth on Clinical Validation

Facial cleansers and foaming gels retained 30.11% of 2025 revenue owing to stable foam at pH 5.5-6.5. Anti-acne and oily-skin care is forecast to grow at 6.89% CAGR through 2031, pushing the Capryloyl Glycine market size within that niche to new highs as trials show superior Cutibacterium acnes inhibition without barrier damage.

Shampoos and scalp lotions represent a mature lane, while deodorants and oral-care products demonstrate emergent upside because capryloyl glycine controls Corynebacterium and periodontal pathogens. Tailored blends that pair the anionic glycinate with zinc salts or peptides let formulators position leave-on serums as microbiome-friendly, expanding the Capryloyl Glycine market into functional skincare segments previously dominated by salicylic acid or benzoyl peroxide.

By End-user Industry: Dermatology Captures High-Margin Growth

Personal care and cosmetics accounted for 56.67% of 2025 revenue, anchoring the Capryloyl Glycine market in mass facial cleansers and sulfate-free shampoos. Pharmaceutical and dermatological products are advancing at 7.03% CAGR during the forecast period (2026-2031), leveraging GMP-grade inputs and randomized-controlled trial data to justify 30-50% shelf premiums.

Oral-care manufacturers explore amino-acid-based actives to replace controversial triclosan, while household cleaning brands tap capryloyl glycine’s biodegradability to win EU Ecolabel approval. Pet-care and wound-care lines provide another frontier, sustaining diversification within the Capryloyl Glycine industry.

Geography Analysis

Asia-Pacific commanded 43.31% of 2025 revenue and is projected to expand at 6.98% through 2031. Japan pioneered low-pH cleansers, creating consumer standards now spreading across China, South Korea, and ASEAN urban markets. Sino Lion’s planned 100,000 tons capacity expansion underpins regional supply security, while Ajinomoto’s Amisoft line anchors quality benchmarks. Campaigns pairing sulfate-free claims with K-beauty routines accelerate uptake among Gen Z consumers.

North America held a substantial share of the 2025 market turnover as U.S. clean-beauty retailers mandated sulfate exclusions and dermatologists endorsed amino-acid surfactants for post-procedure care. Safic-Alcan’s 2026 acquisition of Deveraux Specialties strengthens West Coast distribution, enhancing technical support for indie brands. TRI-K’s solvent-free TRICare CG resonates with formulators seeking microbiome-friendly seals.

Europe’s 2025 revenue was driven by Germany, France, and the United Kingdom. The 2027 microplastics ban forces reformulation, propelling biodegradable surfactant adoption. COSMOS and NATRUE certifications act as gatekeepers, with Nordic countries exhibiting the highest per-capita consumption. Southern and Eastern Europe grow from a smaller base as multinationals harmonize formulations to avoid region-specific SKUs. Latin America, Middle East, and Africa collectively hold the least share, constrained by cost sensitivity and hard-water performance issues but offering niche upside in premium men’s grooming and halal-compliant lines.

Competitive Landscape

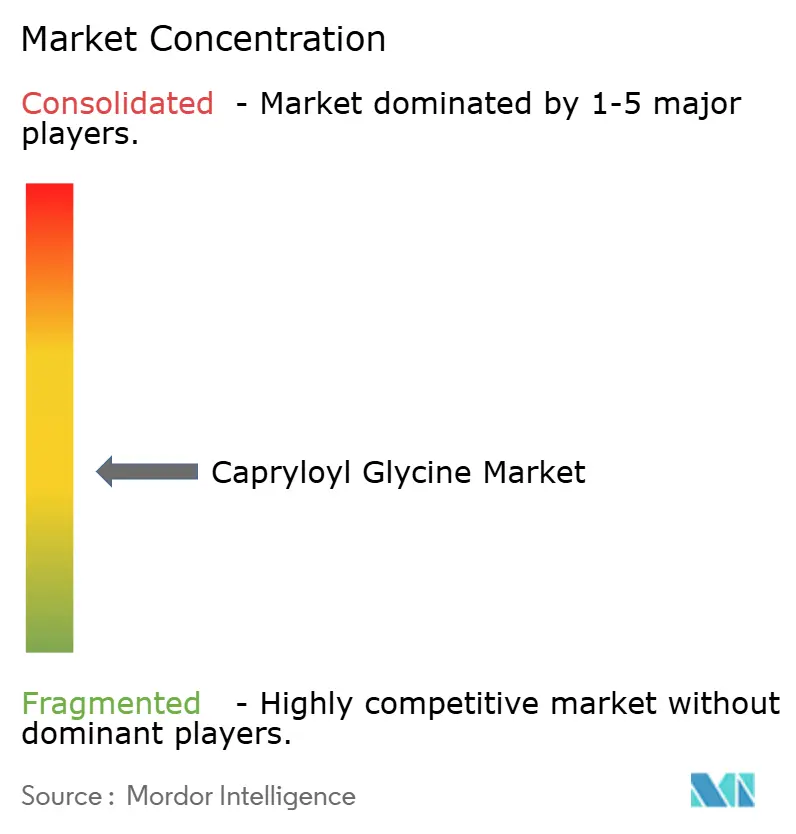

The Capryloyl Glycine market is moderately fragmented. White-space growth lies in pharmaceutical-grade supply, waterless solid formats, and fermentation-derived caprylic acid that mitigates palm-related sustainability concerns. Suppliers capable of delivering turnkey blends optimized for hard-water performance and regulatory compliance are positioned to outpace commodity competitors within the Capryloyl Glycine industry.

Capryloyl Glycine Industry Leaders

AE Chemie, Inc.

Air Liquide

EURO-KEMICAL SRL

Minafin Group

ZLEYGROUP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Safic-Alcan, a distributor of specialty chemicals, acquired Deveraux Specialties, LLC. Deveraux, based in the United States, specializes in distributing ingredients like Capryloyl Glycine, catering primarily to the cosmetic and personal care sectors.

- April 2024: TRI-K Industries Inc. has announced the launch of TRICare CG (Capryloyl Glycine), a multifunctional ingredient derived from amino acids. Utilizing a patented green chemistry process, TRICare CG offers superior purity, is solvent-free, achieves 100% atom conversion, and incorporates a biodegradable catalyst.

Global Capryloyl Glycine Market Report Scope

Capryloyl glycine is a lipo-amino acid, formed by combining the amino acid glycine with caprylic acid, used in cosmetics as a multifunctional skin-conditioning agent, surfactant, and preservative booster.

The Capryloyl Glycine market is segmented by purity/grade, form, application, end-user industry, and geography. By purity/grade, the market is segmented into cosmetic grade, pharmaceutical grade, and industrial/technical grade. By form, the market is segmented into powder and liquid/solution. By application, the market is segmented into facial cleansers and foaming gels, shampoos and scalp treatments, deodorants and antiperspirants, anti-acne and oily-skin care, emulsified creams and serums, oral care (toothpaste and mouthwash), and other applications (wipes and intimate care). By end-user industry, the market is segmented into personal care and cosmetics, pharmaceutical and dermatological products, home and hygiene products, nutraceuticals and functional oral care, and other end-user industries (pet and specialty care). The report also covers the market size and forecasts for capryloyl glycine in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Cosmetic Grade |

| Pharmaceutical Grade |

| Industrial/Technical Grade |

| Powder |

| Liquid/Solution |

| Facial Cleansers and Foaming Gels |

| Shampoos and Scalp Treatments |

| Deodorants and Antiperspirants |

| Anti-acne and Oily-skin Care |

| Emulsified Creams and Serums |

| Oral Care (Toothpaste, Mouthwash) |

| Other Applications (Wipes, Intimate Care) |

| Personal Care and Cosmetics |

| Pharmaceutical and Dermatological Products |

| Home and Hygiene Products |

| Nutraceuticals and Functional Oral Care |

| Other End-user Industries (Pet and Specialty Care) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Purity/Grade | Cosmetic Grade | |

| Pharmaceutical Grade | ||

| Industrial/Technical Grade | ||

| By Form | Powder | |

| Liquid/Solution | ||

| By Application | Facial Cleansers and Foaming Gels | |

| Shampoos and Scalp Treatments | ||

| Deodorants and Antiperspirants | ||

| Anti-acne and Oily-skin Care | ||

| Emulsified Creams and Serums | ||

| Oral Care (Toothpaste, Mouthwash) | ||

| Other Applications (Wipes, Intimate Care) | ||

| By End-user Industry | Personal Care and Cosmetics | |

| Pharmaceutical and Dermatological Products | ||

| Home and Hygiene Products | ||

| Nutraceuticals and Functional Oral Care | ||

| Other End-user Industries (Pet and Specialty Care) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Capryloyl Glycine market by 2031?

The Capryloyl Glycine Market size is projected to expand from USD 109.34 million in 2025 and USD 116.13 million in 2026 to USD 156.95 million by 2031, registering a CAGR of 6.21% between 2026 to 2031.

How fast is the Capryloyl Glycine market expected to grow?

Capryloyl Glycine market is set to record a 6.21% CAGR during 2026-2031.

Which region currently leads global demand?

Asia-Pacific commands the largest share at 43.31% of 2025 revenue.

Why are pharmaceutical-grade volumes rising?

Dermatology brands require USP-quality inputs for prescription acne and rosacea lines.

Page last updated on: