Sodium Sulfide Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

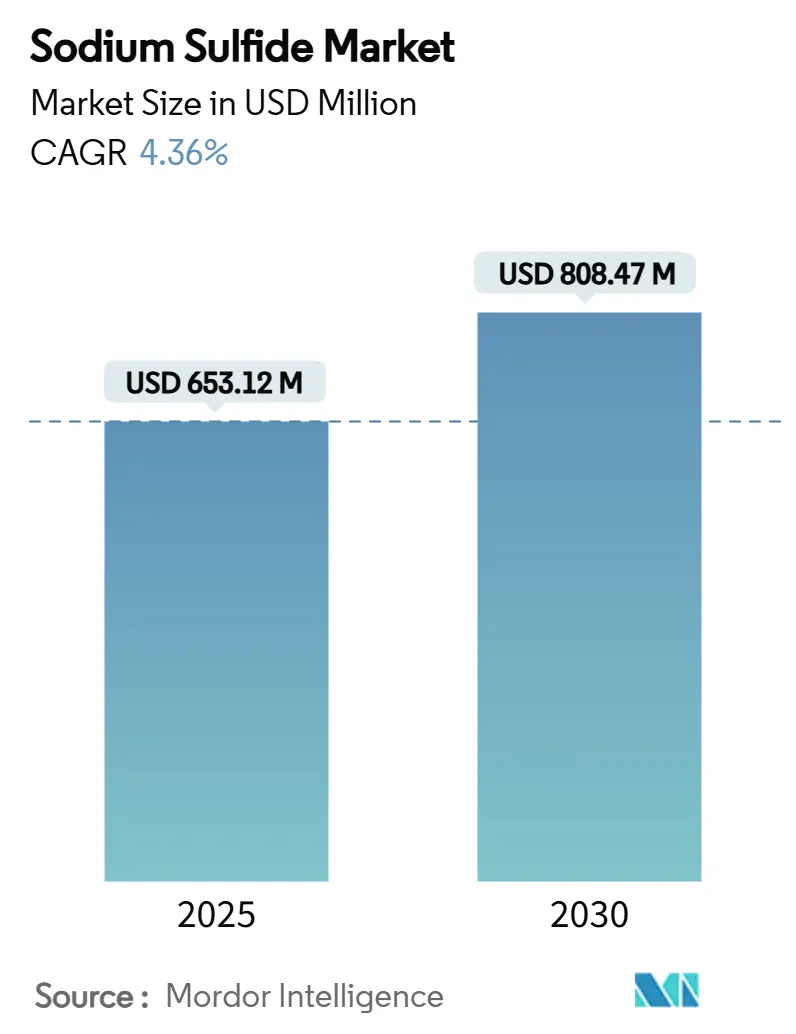

| Market Size (2025) | USD 653.12 Million |

| Market Size (2030) | USD 808.47 Million |

| Growth Rate (2025 - 2030) | 4.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sodium Sulfide Market Analysis by Mordor Intelligence

The Sodium Sulfide Market size is estimated at USD 653.12 million in 2025, and is expected to reach USD 808.47 million by 2030, at a CAGR of 4.36% during the forecast period (2025-2030). Enduring consumption in leather tanning, kraft pulp manufacturing and ore flotation underpins baseline growth, while nascent adoption in sodium-ion batteries and advanced water treatment solutions introduces new value pools. Asia-Pacific, anchored by China and India, continues to absorb the bulk of global output on the strength of cost-competitive manufacturing networks and the rapid build-out of municipal wastewater infrastructure. Technical-grade material dominates current trade flows, but battery-grade and low-fume prilled variants are expanding swiftly as customers tighten purity and safety specifications. Competitive intensity remains moderate: multinational specialists such as Solvay and Nouryon lean on process know-how and vertically integrated logistics, whereas regional firms in East and South Asia compete primarily on delivered cost and responsive service. Feedstock price swings and tightening workplace exposure limits inject uncertainty into margins, yet the compound’s irreplaceable chemistry in pulp delignification and hide depilation secures a resilient demand floor.

Key Report Takeaways

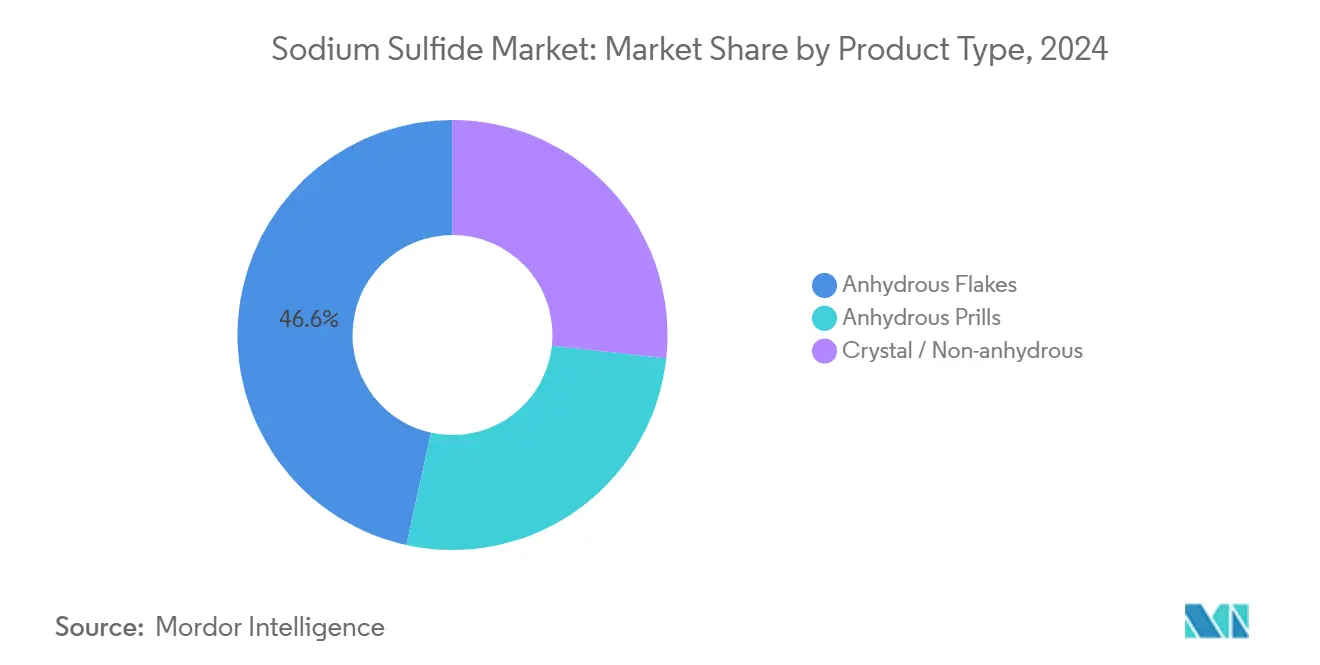

- By product type, anhydrous flakes led with 46.56% revenue share in 2024, while anhydrous prills are forecast to expand at a 5.03% CAGR through 2030.

- By form, solid sodium sulfide captured 62.13% share in 2024; liquid formulations hold the highest projected growth at 5.24% CAGR to 2030.

- By grade, technical grade accounted for 64.45% of volume in 2024, whereas battery grade is set to record a 5.66% CAGR over the same horizon.

- By application, leather tanning held 36.65% share in 2024; ore flotation and mining is anticipated to post the fastest 4.89% CAGR through 2030.

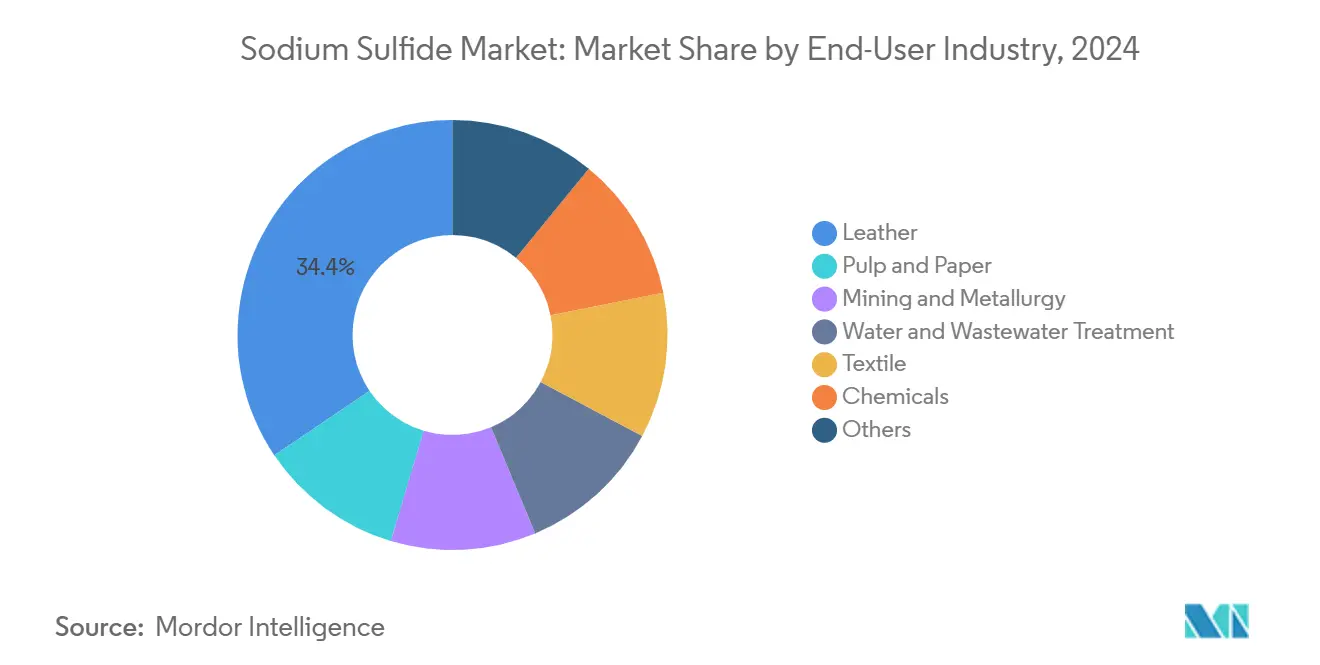

- By end-use industry, the leather sector commanded 34.45% of demand in 2024; mining and metallurgy is projected to grow at 4.77% CAGR to 2030.

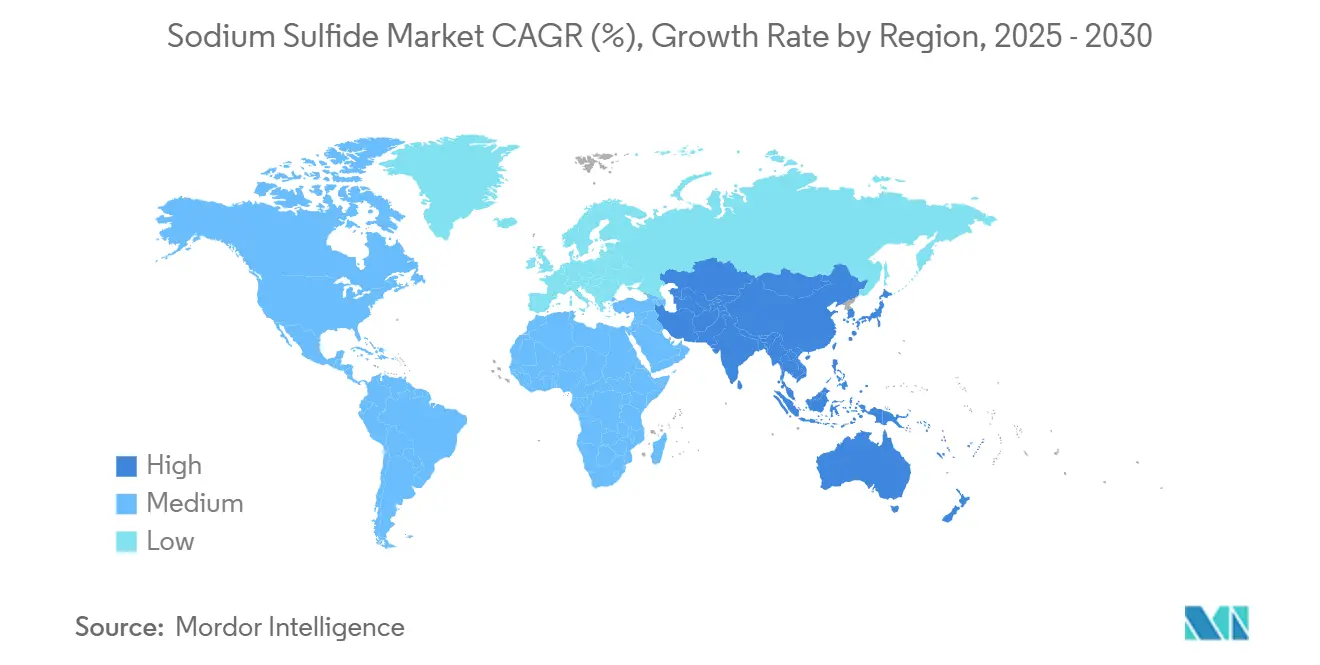

- By geography, Asia-Pacific controlled 64.56% of global revenue in 2024 and is expected to preserve the lead with a 5.23% CAGR through 2030.

Global Sodium Sulfide Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand from leather tanning and dye industries | +1.2% | APAC core, spill-over to South America | Medium term (2-4 years) |

| Rising consumption in pulp and paper manufacturing | +0.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Growing use in water treatment chemicals | +0.6% | Global, with early gains in APAC and MEA | Medium term (2-4 years) |

| Adoption in semiconductor copper CMP slurries | +0.5% | APAC core, North America secondary | Short term (≤ 2 years) |

| Low-fume prilled sodium sulfide market uptake | +0.3% | Global, with focus on developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand from Leather Tanning and Dye Industries

Premium automotive upholstery and high-end footwear production now require tighter hide quality tolerances that, in turn, call for more intensive chemical depilation cycles. Large tanneries in China, India and Vietnam have adopted closed-loop recovery systems that recapture sodium sulfide for recycling, yet the process still lifts overall consumption per hide processed due to higher starting dosages[1]European Chemicals Agency, “Classification and Labelling Inventory for Sodium Sulfide,” echa.europa.eu. Regional consolidation is concentrating throughput into fewer, better-capitalized plants; these facilities favour consistent bulk deliveries that stabilise baseline offtake volumes for producers. Near-shoring of tanning capacity into Southeast Asia and parts of Latin America offsets tapering growth in more mature centres such as Zhejiang and Uttar Pradesh. Concurrently, fashion houses shifting toward chrome-free finishing methods continue to rely on sodium sulfide during liming, preserving its centrality despite downstream process changes.

Rising Consumption in Pulp and Paper Manufacturing

Modern kraft mills installing high-efficiency chemical recovery loops demand technical-grade sodium sulfide with tighter impurity thresholds to maximise white liquor performance. Growing e-commerce activity has accelerated world demand for stronger packaging grades, prompting mills to target higher pulp yield through deeper delignification that elevates sodium sulfide dosage rates. North American brownfield upgrades and Scandinavian greenfield mills both specify low-iron material to reduce deposition on evaporators, creating value-added niches for quality-focused suppliers. In emerging economies, Indonesia and Brazil are each adding new bleached hardwood kraft capacity, translating into concentrated regional demand bursts. Research programmes in lignin extraction continue to evaluate customised sodium sulfide blends that improve lignin solubility while lowering total sulphur emissions.

Growing Use in Water Treatment Chemicals

Stricter discharge limits for cadmium, mercury and lead have turned sodium sulfide into an essential precipitant for industrial effluent streams[2]Health Canada, “Guidelines for Canadian Drinking Water Quality–Metals,” canada.ca. China’s new water reuse guidelines encourage on-site recirculation loops at textile and petrochemical complexes, raising recurring consumption of high-purity liquid formulations designed for continuous dosing systems. In the Middle East, large desalination-linked industrial parks use sodium sulfide as a hydrogen sulfide scavenger to protect downstream membranes. Produced-water management in unconventional oilfields is another emerging outlet, as operators trial sulphide-based heavy-metal removal stages that can be retrofitted into existing treatment trains. These regulatory-driven applications show limited price elasticity, supporting steady margins even when feedstock sulphur prices fluctuate.

Adoption in Semiconductor Copper CMP Slurries

Advanced node foundries have begun specifying sodium sulfide as a complexing agent in copper and barrier metal polishing slurries, where it modulates galvanic interactions and improves removal rate uniformity. Device miniaturisation to below 5 nm and the rise of 3D integrated structures increase slurry performance requirements, pushing formulators toward ultra-low contaminant grades with controlled sulphide activity. Several South Korean and Taiwanese fabs have signed joint-development agreements with regional chemical suppliers to secure just-in-time deliveries of semiconductor-grade sodium sulfide. Replacement of permanganate-based oxidisers with sulphide-containing blends aligns with industry sustainability roadmaps by lowering manganese discharges. Although chip demand can be cyclical, the long-term production expansion plans in East Asia underpin a positive volumetric outlook.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental and occupational regulations | -0.7% | Global, with emphasis on North America & Europe | Medium term (2-4 years) |

| Volatile sulfur feedstock prices | -0.4% | Global | Short term (≤ 2 years) |

| Shift to eco-friendly depilating agents in leather processing | -0.3% | Global, with early adoption in Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental and Occupational Regulations

European Union REACH classification lists sodium sulfide as toxic upon inhalation and corrosive to skin, compelling importers and downstream users to prepare extensive safety dossiers, certified exposure-scenario assessments and employee training records. The United States updated Hazard Communication Standard now mandates pictogram-based labeling on all transport containers, adding compliance labour and printing expenses. Ventilation retrofits and continuous hydrogen sulfide monitoring broaden the capital burden on pulp mills and tanneries in mature jurisdictions. While these measures favour established suppliers with advanced technical services, they also lengthen approval cycles for product modifications, slowing the rollout of next-generation formulations. Similar frameworks are progressing in South Korea and Brazil, signalling widening global reach of compliance-related cost inflation.

Volatile Sulfur Feedstock Prices

Sulfur supply hinges largely on refining and sour gas processing throughput; refinery maintenance outages and shifts toward low-sulphur fuels periodically tighten elemental sulphur availability, spiking prices and compressing producer margins. Smaller sodium sulfide manufacturers lacking long-term offtake contracts face most of the spot-market volatility, resulting in erratic quoting behaviour that destabilises customer procurement planning. Geopolitical risks around key suppliers in the Middle East and Central Asia further complicate sourcing strategies. Forward hedging instruments remain limited, prompting large integrated players to leverage multi-feedstock flexibility in thiosulfate or polysulfide intermediates to cushion swings. As global energy systems pivot toward decarbonised pathways, declining fossil-fuel refining volumes may structurally reduce recovered sulphur output, amplifying future supply-demand imbalances.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Established Flake Supremacy Meets Rising Prill Preference

Anhydrous flakes retained a 46.56% revenue share of the sodium sulfide market in 2024, underscoring their entrenched position across leather tanning and kraft digestion lines where legacy conveyance systems favour coarse granular feed. Prills, however, are registering the most vigorous advance at a 5.03% CAGR, a signal that occupational-safety considerations are now potent purchase drivers. During 2025, multiple Chinese suppliers expanded spray-granulation capacity, narrowing delivered-cost differentials against flakes and accelerating substitution among multinational tanners in Vietnam and Mexico. Technical teams at pulp mills in Scandinavia reported smoother dissolver operation and reduced tank clean-out frequency when shifting to prills, further supporting the format’s momentum.

Customer switching costs have begun to tilt supplier bargaining power. Producers able to guarantee tight prill size distributions and minimal residual free alkali secure premium contract renewals that lift blended selling prices. Conversely, flake-focused manufacturers risk share attrition unless they invest in deodorised formulations or flake-to-prill conversion. Niche crystal variants, though low in volume, retain relevance in specialty water treatment packages where controlled hydration underpins precise reagent dosing. The interplay between continuity of supply, worker-health mandates and process automation will shape relative product-type growth trajectories through 2030, positioning prills as the strategic growth vector within the sodium sulfide market.

By Form: Solid Dominance Encountering Liquids’ Convenience Wave

Solid sodium sulfide forms commanded 62.13% of shipment value in 2024, leveraging favourable freight economics that reward high active content per tonne shipped. Bags, IBCs and bulk container liners remain standard packaging in tanning clusters across Asia-Pacific, sustaining predictable solid-form baseline volumes. Nonetheless, liquid concentrates are expanding at a 5.24% CAGR, principally on the back of tighter process-control requirements in semiconductor slurry blending and continuous-flow heavy-metal precipitation units at petrochemical sites. End users value liquids for their immediate pump-and-dose convenience, avoiding in-house dissolving stations that carry splash risks and maintenance workloads.

Logistics costs for liquids are higher due to lower active loading and the need for ISO-tank or drum handling, yet this premium is frequently offset by labour savings and improved dosing accuracy. Suppliers with regional toll-blending hubs can capture liquids’ growth without sacrificing scale economies in base solid manufacture. For the upcoming planning cycle to 2030, a gradual dilution of solid-form share is probable, but the segment will stay the workhorse of the sodium sulfide market size given its enduring appeal to cost-sensitive customers in leather and pulp value chains.

By Grade: Technical Mainstay Confronts Battery-Driven Purity Escalation

Technical grade product, typically 60 %–70 % purity, held 64.45% of the sodium sulfide market share in 2024 and continues to anchor volumes for commodity-scale users whose primary purchase criterion remains delivered cost. Yet battery grade material, specified at greater than or equal to 99% purity and low moisture content, is on track for the strongest 5.66% CAGR. Sodium-ion battery developers exploit sodium sulfide as a presodiation reagent that replenishes irreversible sodium loss during the first charge-discharge cycle, boosting energy density. Research trials in China, Singapore and the European Union have validated performance benefits, stimulating the first wave of pilot-scale qualification contracts.

High-purity electronic grade serves slender but lucrative channels in photoresist stripping and semiconductor copper slurry reagents; typical lot sizes are smaller, but price realisation per tonne is several multiples of technical grade. To participate, producers must invest in closed-loop crystallisation, resin-bed polishing and sub-ppm impurity analytics—capex priorities that can tip competitive balance over the next five years. As electric mobility policy incentives broaden beyond lithium, the sodium sulfide market expects increasing enquiry volumes for battery grade, nudging overall purity averages higher across the supply base.

By Application: Leather Core Stable as Mining Accelerates

Leather tanning consumed 36.65% of global volume in 2024, reaffirming sodium sulfide’s irreplaceable role in efficient hide unhairing. Consumption concentration remains prominent in Zhejiang, Tamil Nadu and Ho Chi Minh clusters, yet capacity additions in Indonesia’s Central Java economic zone and Brazil’s Rio Grande do Sul are creating fresh offtake pockets. Ore flotation and mining, accounting for 4.89% projected CAGR, is benefiting from new copper, nickel and polymetallic projects targeting energy-transition metals in Peru and the Democratic Republic of Congo. Sodium sulfide acts as a selective depressant, improving valuable-to-gangue recovery ratios and offering an environmentally benign alternative to hydrosulfide salts with stronger odour profiles.

Pulp and paper operations maintain a steady pull—each tonne of kraft pulp requires roughly 19 kg of sodium sulfide in white liquor, and mill modernisations often tighten purity demands rather than reduce mass usage. Water treatment demand, while smaller, exhibits attractive growth tied to infrastructure spending in water-stressed regions such as Northern China and the Gulf Cooperation Council countries. Diversification toward semiconductor and battery applications should collectively lift the sodium sulfide market size even if leather’s unit growth moderates under sustainability pressures.

By End-Use Industry: Traditional Leather Hegemony Faces Metallurgical Upswing

The leather industry retained a 34.45% consumption share in 2024, a testament to deep-rooted process chemistry and consolidated production clusters that favour bulk chemical offtake contracts. Still, mining and metallurgy is the fastest climber at 4.77% CAGR, propelled by higher ore throughput ambitions at critical-mineral mines and the deployment of advanced flotation collectors and depressants. Kraft pulp mills follow as a stable anchor segment: while paperless communication curbs graphic-paper demand, corrugated packaging rise keeps pulp output resilient. Water utilities and industrial wastewater treatment operators collectively expand on regulatory imperatives to remove heavy metals, boosting recurring sodium sulfide purchase orders.

Chemical intermediate synthesis and semiconductor fabrication, though currently niche, command elevated price points per tonne and can materially lift profit mix for suppliers able to meet ultra-high purity specs. Across end-use sectors, three themes shape demand through 2030: compliance-driven quality upgrades, tighter worker-safety legislation and emergent electrochemical energy-storage technologies.

Geography Analysis

Asia-Pacific generated 64.56% of global revenue for the sodium sulfide market in 2024, fortified by vertically integrated leather, textile and chemical manufacturing ecosystems in coastal China and Western India. The region’s forecast 5.23% CAGR rests on brownfield debottlenecking in Guangxi tanning hubs, greenfield kraft pulp projects in Indonesia and expanding semiconductor capacity in Taiwan and mainland China. Regional governments continue to subsidise wastewater-treatment upgrades, which in turn increase sodium-based heavy-metal scavenger demand. Cross-border trade flows increasingly move via intra-Asia short-sea lanes, improving lead-time resilience against ocean-freight volatility.

North America holds a mature but lucrative share of the sodium sulfide market size. U.S. kraft pulp mills in the Pacific Northwest and South-East remain steady buyers, and the semiconductor corridors of Arizona and Texas are trialling battery-grade and electronic grade variants. Environmental Protection Agency wastewater rulings amplify demand in precious-metal recovery plants and electroplater rinse-water systems. Canada’s Health agencies also tightened cadmium discharge limits, bolstering municipal uptake of sodium sulfide precipitation programmes.

Europe commands a smaller proportion yet exerts outsized influence on product specification trends. EU REACH compliance and worker exposure directives accelerate the shift to low-fume prills and enforce stricter impurity ceilings, functions that ripple into global supplier quality systems. Leather factories in Italy’s Tuscany district and Germany’s Bavarian belt import high-purity flakes, while Nordic pulp mills demand consistent technical grade aligned to white-liquor optimisations. Elsewhere, South America’s copper-rich Andes and the burgeoning Middle East industrial corridors in Saudi Arabia and Oman illustrate emerging demand hotspots, though their combined share is still nascent compared to Asia-Pacific’s dominance.

Mordor Intelligence provides coverage of the sodium sulfide market across other key regional markets, including Middle East and Africa, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Global supply for the sodium sulfide market is moderately fragmented yet regionally concentrated, reflecting the practical need to locate capacity near sulphur feedstock and large industrial consumers. Solvay and Nouryon anchor the premium segment by leveraging proprietary purification technology, extensive logistics footprints and regulatory expertise that appeals to multinational hides processors and paper conglomerates. In 2025, Solvay commissioned an automated prill line at its Rosignano site that triples capacity for low-dust variants, while Nouryon expanded its Ningbo plant to produce battery-grade material under clean-room conditions. Mid-tier suppliers in China, led by Yabang Chemical and Shaanxi Fuhua, compete primarily on cost and short-cycle deliveries backed by proximity to leather and textile clusters.

Process innovation centres on emission abatement and product-form optimisation. Spray-granulation, closed-loop mother-liquor recycling and catalytic tail-gas oxidation systems are now standard in new capacity, driven by tougher permit thresholds in China’s latest Three-Year Blue-Sky Action Plan. Patent applications underscore ongoing mineral-processing formulation work, where nuanced sodium-sulfide blends enhance selectivity in polymetallic flotation cells. The ability to deliver consistent particle morphology in prills and sub-ppm arsenic levels in battery grade acts as a key differentiator for premium contracts.

Strategic alliances between chemical producers and battery developers have begun to crystallise. In 2024, a consortium involving a South Korean cathode maker and a Japanese trading house signed a multi-year offtake agreement with a Jiangsu-based high-purity sodium sulfide producer, signalling early vertical integration in the sodium-ion supply chain. Meanwhile, regional tanneries award multi-year contracts primarily on delivered cost and shipment punctuality, sustaining competitive opportunity for agile local players. On balance, bargaining power sits with large buyers in commoditised technical grade but shifts toward specialised suppliers in high-purity niches, shaping a nuanced competitive matrix.

Sodium Sulfide Industry Leaders

Arkema

Nouryon

Sankyo Chemical Co., Ltd.

Solvay

Tessenderlo Kerley

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: The European REACH regulation updates confirmed the classification requirements and usage restrictions for sodium sulfide. The updated framework necessitates detailed safety documentation for sodium sulfide applications, impacting market access and offering a competitive advantage to suppliers with robust compliance systems.

- May 2024: OSHA introduced revised Hazard Communication Standards, focusing on sodium sulfide labeling and safety data sheet requirements. These updated standards enhance safety documentation and strengthen worker protection measures. This regulatory change imposes compliance costs on suppliers and end-users, while potentially providing an advantage to larger companies with established regulatory expertise.

Global Sodium Sulfide Market Report Scope

| Anhydrous Flakes |

| Anhydrous Prills |

| Crystal / Non-anhydrous |

| Solid |

| Liquid |

| Technical / Industrial Grade |

| High-Purity Grade (Greater than or Equal to 99 %) |

| Battery Grade |

| Leather Tanning and Dye |

| Pulp and Paper |

| Water Treatment |

| Ore Flotation and Mining |

| Textile Processing |

| Chemical Intermediates |

| Others |

| Leather |

| Pulp and Paper |

| Mining and Metallurgy |

| Water and Wastewater Treatment |

| Textile |

| Chemicals |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Product Type | Anhydrous Flakes | |

| Anhydrous Prills | ||

| Crystal / Non-anhydrous | ||

| By Form | Solid | |

| Liquid | ||

| By Grade | Technical / Industrial Grade | |

| High-Purity Grade (Greater than or Equal to 99 %) | ||

| Battery Grade | ||

| By Application | Leather Tanning and Dye | |

| Pulp and Paper | ||

| Water Treatment | ||

| Ore Flotation and Mining | ||

| Textile Processing | ||

| Chemical Intermediates | ||

| Others | ||

| By End-Use Industry | Leather | |

| Pulp and Paper | ||

| Mining and Metallurgy | ||

| Water and Wastewater Treatment | ||

| Textile | ||

| Chemicals | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the sodium sulfide market growth outlook to 2030?

The sodium sulfide market is forecast to climb from USD 653.12 million in 2025 to USD 808.47 million by 2030, reflecting a 4.36% CAGR supported by resilient leather and pulp demand plus nascent battery uses.

Why are prilled products gaining popularity?

Low-fume prilled sodium sulfide lowers airborne dust exposure, easing compliance with stricter workplace-safety limits and offering smoother pneumatic handling that reduces plant downtime costs.

Which region will add the most new demand?

Asia-Pacific already holds 64.56% share and is projected to grow the fastest at 5.23% CAGR through 2030, driven by expanding tanning, pulp and semiconductor capacity in China, India and Southeast Asia.

How do environmental regulations affect sodium sulfide suppliers?

EU REACH and similar frameworks mandate rigorous labeling, emission control and worker-safety measures, raising compliance costs but also favouring established suppliers with advanced quality systems.

Page last updated on: