Butylated Hydroxytoluene Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

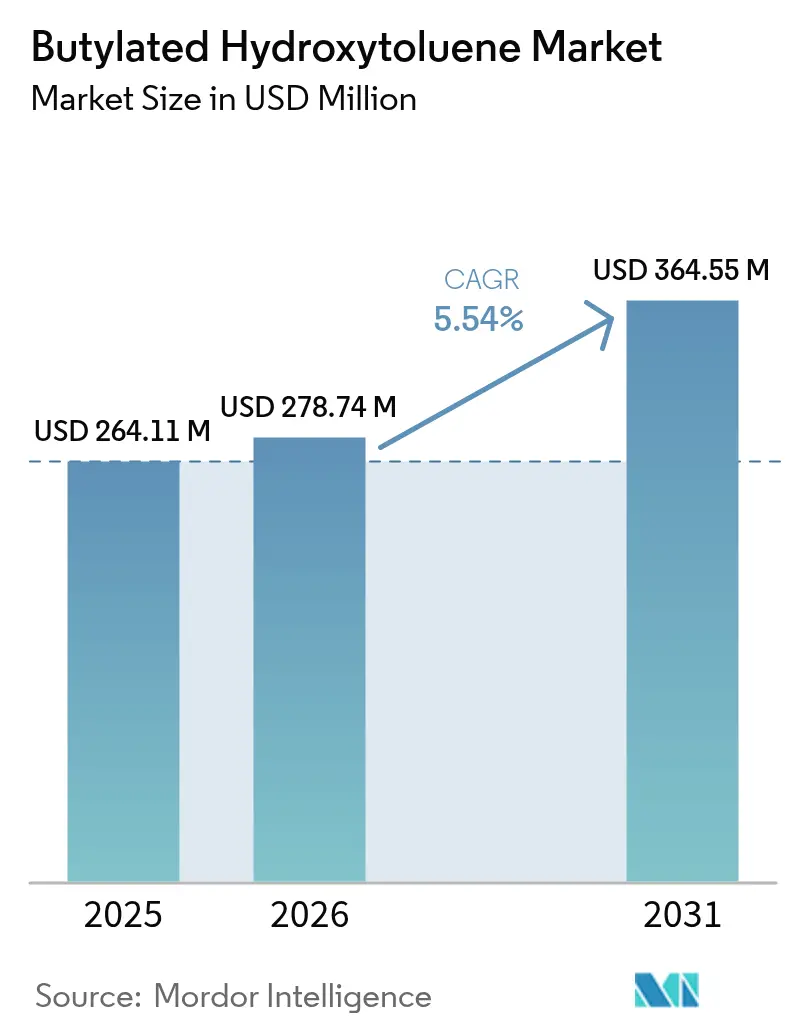

| Market Size (2026) | USD 278.74 Million |

| Market Size (2031) | USD 364.55 Million |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

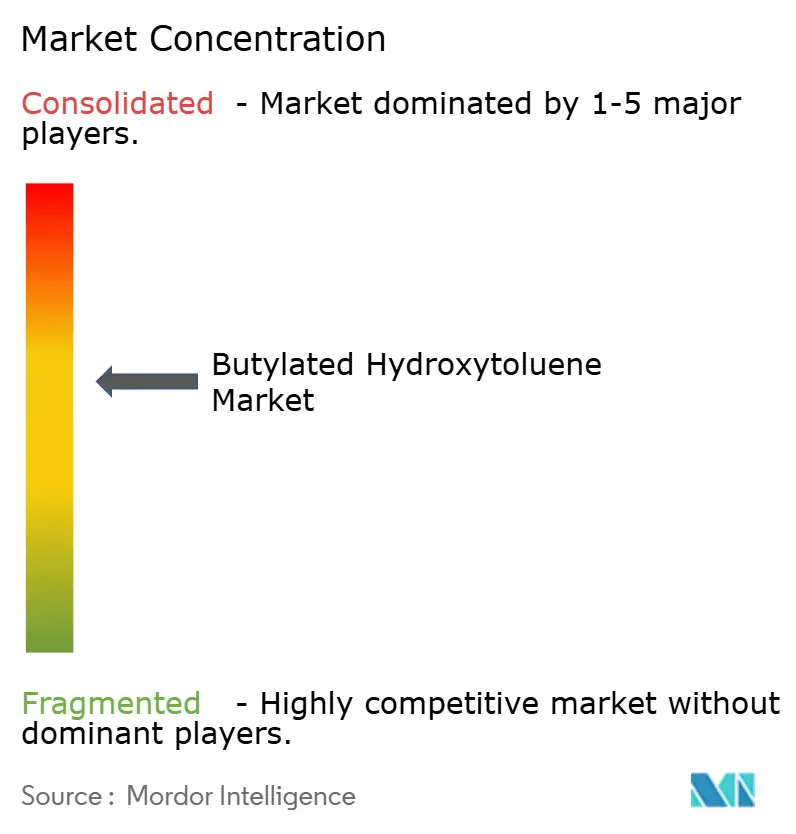

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Butylated Hydroxytoluene Market Analysis by Mordor Intelligence

Butylated Hydroxytoluene market size in 2026 is estimated at USD 278.74 million, growing from 2025 value of USD 264.11 million with 2031 projections showing USD 364.55 million, growing at 5.54% CAGR over 2026-2031. The upward trajectory reflects sustained demand for the synthetic phenolic antioxidant across polymer processing, food preservation, and personal-care formulations, even as regulators tighten oversight and brand owners trial natural replacements. Asia-Pacific’s manufacturing expansion, higher processed-food intake, and deep plastics conversion capacity collectively underpin regional consumption. Technical Grade volumes dominate due to the compound’s proven thermo-oxidative stability at elevated temperatures, while Food Grade purity supports value growth in emerging packaged-food hubs. Parallel investments in low-carbon production, such as BASF’s Zhanjiang complex that will run on 100% renewable electricity, signal confidence in long-term industrial consumption. Competitive behaviour pivots on feedstock integration, regulatory stewardship and application-specific technical service, ensuring that price remains only one of several purchasing criteria.

Key Report Takeaways

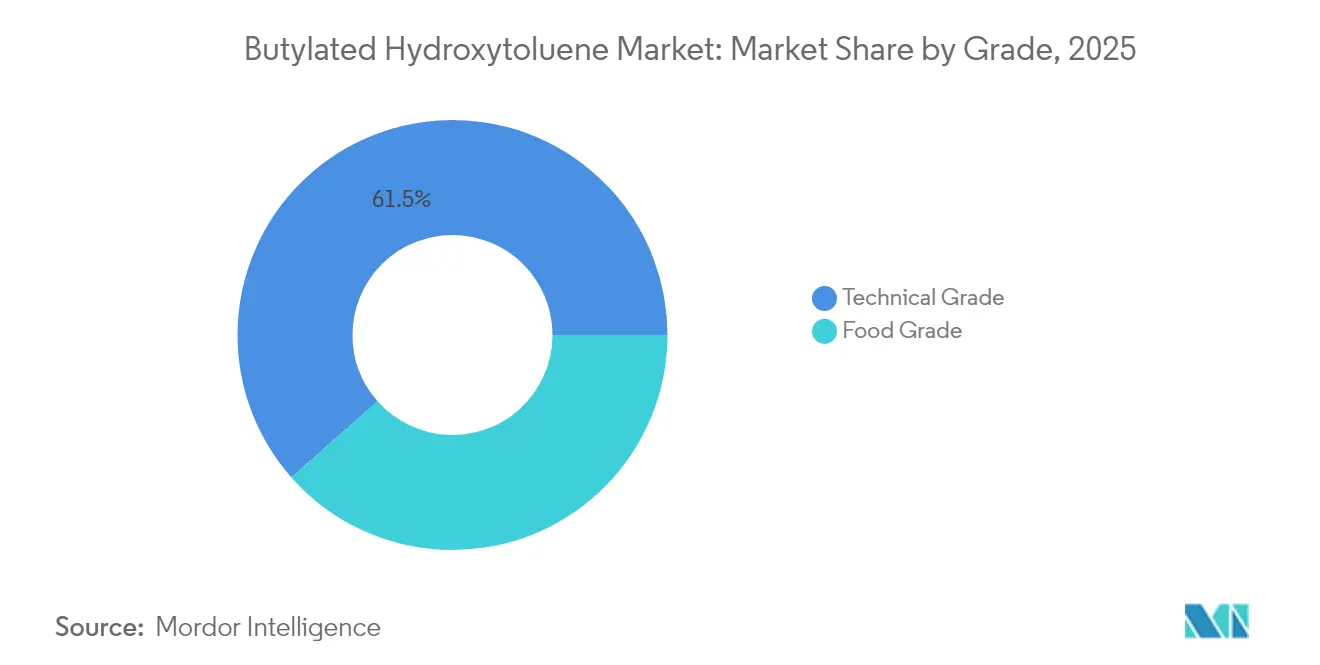

- By grade, Technical Grade commanded 61.52% of the Butylated Hydroxytoluene market share in 2025, while Food Grade is projected to register a 5.78% CAGR to 2031.

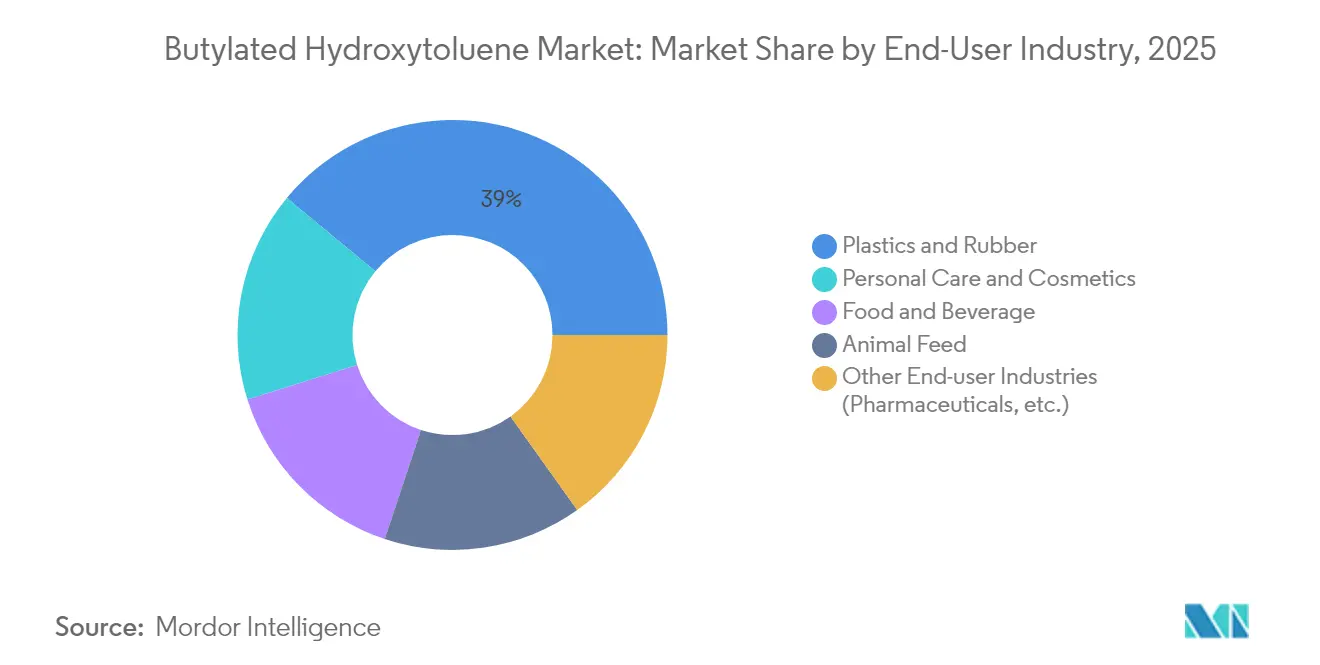

- By end-user industry, Plastics and Rubber accounted for 39.00% of the Butylated Hydroxytoluene market size in 2025; Personal Care and Cosmetics is forecast to expand at a 6.15% CAGR through 2031.

- By geography, Asia-Pacific led with 45.10% revenue share in 2025 and is expected to grow at a 6.05% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Butylated Hydroxytoluene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for antioxidants from polymer processing | +1.80% | Global, with APAC core concentration | Medium term (2-4 years) |

| Growing usage in food and beverage fat-rich products | +1.40% | Global, spill-over to emerging markets | Long term (≥ 4 years) |

| Expansion of personal-care and cosmetics preservatives | +1.20% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Surge in animal-feed micronutrient fortification | +0.90% | Global, with early gains in intensive farming regions | Medium term (2-4 years) |

| Adoption in smart flexible-electronics barrier coatings | +0.30% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Antioxidants in Polymer Processing

High-temperature polymer extrusion, injection moulding, and film blowing depend on antioxidants that intercept free radicals before chain scission damages mechanical strength. Butylated Hydroxytoluene fulfils this role because its sterically hindered structure donates hydrogen atoms rapidly without forming coloured by-products, preserving clarity in thin films used for electronics and food packaging. Demand intensifies in Asia-Pacific, where capacity additions for polyethylene, polypropylene, and engineering plastics remain onstream through 2028. Eastman’s Therminol heat-transfer fluids—designed for continuous operation near 330 °C—illustrate the narrow process-control windows in which BHT must remain active. The technical dependence reduces switching incentives, sustaining long contracts with established suppliers. Incremental gains in phosphite co-stabilisers further lift BHT volumes because formulators typically use it alongside secondary antioxidants to widen oxidative induction times.

Growing Usage in Fat-Rich Food Products

Global per-capita intake of packaged snacks, bakery mixes, and confectionery is rising in tandem with urbanisation, pushing manufacturers to curb lipid rancidity that shortens shelf life. Butylated Hydroxytoluene is authorised at 200 mg/kg in bakery wares and 400 mg/kg in chewing gum by the Codex General Standard for Food Additives, giving formulators a cost-efficient option for high-fat matrices[1]Food and Agriculture Organization, “GSFA Online Food Additive Details for BHT,” fao.org . Eastman’s Tenox portfolio supplies pre-blended BHT systems that combine the antioxidant with propyl gallate or EDTA, extending oxidative protection synergistically. While clean-label campaigns spur trials of tocopherol and rosemary extract, comparative studies show that those alternatives require higher loadings and struggle under elevated storage temperatures common in emerging markets. Consequently, BHT retains share within value-sensitive product lines, and its inclusion in multilayer packaging adhesives offers an indirect route for food safety assurance.

Expansion of Personal-Care Preservatives

Skin-care emulsions, lipsticks, and fragrance oils degrade when unsaturated lipids oxidise, leading to off-odours. Formulators add 0.02-0.1% BHT to stabilise these phases, and the US FDA lists the compound as GRAS for cosmetics. Although the UK has capped use at 0.8% in most personal-care items from 2025 onward, the ruling simultaneously clarifies safe concentration thresholds and spurs reformulation work rather than outright bans. Brands targeting antioxidant claims increasingly pair BHT with vitamin E or ascorbyl palmitate to broaden radical scavenging. The trend intersects with premiumisation in Asia, where consumers view oxidation-controlled products as higher quality, reinforcing volume gains despite headline regulatory headwinds.

Surge in Animal-Feed Micronutrient Fortification

Commercial livestock diets deliver fat-soluble vitamins A and E, both prone to oxidative breakdown during pelleting, storage, and transport. Adding BHT at parts-per-million levels stabilises premixes and injectable emulsions, safeguarding nutrient potency that supports immune function and weight-gain efficiency. The push toward antibiotic-free husbandry heightens reliance on optimised micronutrient delivery, expanding BHT uptake in feed mills across Latin America and Southeast Asia. The WHO’s temporary acceptable daily intake of 0-0.125 mg/kg body weight for BHT in animal feed provides a clear safety envelope, facilitating regulatory clearance in most jurisdictions[2]World Health Organization, “Butylated Hydroxytoluene JECFA Monograph,” inchem.org . As integrators scale vertically, antioxidant procurement is being centralised, favouring suppliers with consistent impurity profiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent toxicological and labeling regulations | -1.10% | Global, with EU and UK leading restrictions | Short term (≤ 2 years) |

| Consumer shift toward “clean-label” natural antioxidants | -0.80% | North America & EU, expanding globally | Medium term (2-4 years) |

| Low-phenol packaging directives in selected nations | -0.60% | EU, Japan, South Korea, with expanding scope to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Toxicological and Labelling Regulations

The EU Chemicals Strategy for Sustainability introduces a generic risk assessment that could mandate hazard-based restrictions across multiple product classes, placing BHT under renewed scrutiny. Parallel UK guidance limits cosmetics concentrations, forcing rapid reformulation among exporters. Compliance costs rise as manufacturers must compile toxicological dossiers, redesign labels, and validate alternative antioxidants in sensitive applications such as infant care. While BHT is categorised by IARC as Group 3 (not classifiable as to carcinogenicity), precautionary policies in Europe and parts of North America impose speed-to-market delays that temper near-term demand.

Consumer Shift Toward Clean-Label Antioxidants

Market research indicates shoppers increasingly equate shorter ingredient lists with premium quality, propelling brands toward natural extracts that carry familiar names like tocopherol. Comparative trials, however, show plant-derived antioxidants can alter product colour notes and have higher unit costs, limiting adoption in mass-market segments. Nonetheless, retail chains and quick-service restaurants in the United States now require suppliers to phase synthetic stabilisers out of certain private-label lines, diverting volume away from the Butylated Hydroxytoluene market in snack foods and baby care lotions. The momentum is expected to intensify once high-pressure processing and active-packaging advances reach price parity with additive-based preservation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Industrial Dominance with Emerging Food-Grade Upside

Technical Grade accounted for 61.52% of Butylated Hydroxytoluene market share in 2025 owing to its cost-advantaged production route and performance reliability under high-shear, high-temperature conditions. The segment is deeply entrenched in polymer compounding and lubricating-oil formulations where purity specifications are less stringent. In 2025, Asian resin converters scaled throughput by double digits, translating into proportional BHT uptake. Capital-intensive reactors and established supply chains grant incumbents pricing power, although periodic swings in petrochemical feedstock prices can influence margins.

Food Grade, despite its smaller size, is projected to achieve a CAGR of 5.78%, significantly contributing to the incremental growth of the Butylated Hydroxytoluene market during the forecast period. Growth stems from rising packaged-food penetration in India, Indonesia and Nigeria, where cold-chain gaps make antioxidant protection indispensable. Purity requirements demand lower tert-butyl contaminants, pushing processing costs higher yet enabling premium unit pricing. Clean-label pressures loom, but strict microbial-reduction standards and cost constraints in emerging economies continue to support synthetic options for the foreseeable future.

By End-user Industry: Polymer Pre-eminence Meets Cosmetic Acceleration

Plastics and Rubber captured 39.00% of the Butylated Hydroxytoluene market size in 2025, thanks to pervasive use across polyolefins, styrenics, and elastomers in automotive interiors and flexible films. The segment benefits from ongoing light-weighting trends that demand thinner yet more durable materials, amplifying antioxidant loading per tonne. Regional recycling mandates also require higher stabiliser doses because secondary resins undergo additional thermal history during reprocessing.

Personal Care and Cosmetics, while holding a smaller base, is projected to advance at 6.15% CAGR through 2031, outpacing all other sectors. The gain is led by premium Asia-Pacific skin-care launches emphasising product freshness and fragrance stability. Formulators leverage BHT’s compatibility with silicones and plant oils to extend shelf life without affecting texture. Regulatory nuances create complexity, yet large multinationals maintain dedicated toxicology teams, allowing continued controlled use. Food and Beverage remains a steady contributor as bakery and snack producers in Latin America and Southeast Asia scale automated lines, while Animal Feed and niche Pharmaceutical uses round out demand.

Geography Analysis

Asia-Pacific’s leading 45.10% revenue contribution in 2025, alongside a 6.05% CAGR outlook, highlights the region’s dual role as producer and consumer of synthetics. China alone houses more than 30% of global polyethylene capacity and sources antioxidants domestically, with food-contact studies recording BHT at 24 mg/kg in inner plastic layers. BASF’s USD 10.9 billion Zhanjiang investment, coming onstream in 2025, underpins sustained supply, and its renewable-electricity pledge addresses local decarbonisation targets. Japan and South Korea consume high-purity grades for electronics, while India’s packaged-foods sector enlarges the addressable base.

North America maintains entrenched demand due to early regulatory clarity: the FDA granted GRAS status to BHT in 1954, facilitating stable utilisation in cereals, snack coatings and polymeric additives. Leading suppliers operate integrated plants along the US Gulf Coast, benefiting from competitively priced natural gas liquids. Clean-label conversion is occurring, yet the shift is selective and slower for value-brand and industrial products that prioritise oxidative stability under harsh logistics.

Europe faces the most stringent regulatory climate. The European Food Safety Authority set the acceptable daily intake at 0.25 mg/kg body weight in 2012, yet new hazard-based approaches may truncate future permissible uses. The UK’s 2025 cosmetic limits visible in labelling updates have nudged some beauty brands toward mixed antioxidant systems, though complete phase-out remains unlikely given performance-cost trade-offs. Nonetheless, the uncertainty restrains investment in incremental capacity.

South America and the Middle East & Africa currently represent a small share of the total value but are expected to achieve above-average growth. Brazilian flexible-film producers increasingly add BHT for longer transit times in tropical climates, and Gulf Cooperation Council states expand polymer parks to diversify economies beyond oil. However, fragmented regulatory oversight and variable logistics infrastructure add risk premiums that smaller suppliers may avoid.

Competitive Landscape

The Butylated Hydroxytoluene market is moderately consolidated. BASF, Eastman Chemical, LANXESS, Oxiris, and Sasol leverage backward integration into key intermediates such as p-cresol, enabling cost leadership unavailable to standalone formulators. These incumbents maintain multi-regional production footprints that hedge currency risk and assure continuity during plant turnarounds.

Strategic investments target energy efficiency and Scope 3 emission reductions because downstream buyers, especially consumer-goods multinationals, embed sustainability metrics in supplier audits. BASF’s Zhanjiang complex embodies this shift by committing to 100% renewable electricity sourcing and process electrification. Eastman, meanwhile, markets Tenox antioxidants with technical service packages that optimise dosage via oxidant profiling, cultivating stickiness in food accounts.

Niche entrants focus on ultra-high-purity grades for pharmaceutical excipients and electronics coatings, where trace metals and odour thresholds are tightly controlled. Although volumes are small, margins offset scale disadvantages. Intellectual property barriers remain low for the base molecule, so differentiation hinges on quality assurance, logistics reliability and regulatory documentation. M&A appetite is muted, with recent activity limited to bolt-on acquisitions in regional distribution rather than upstream production assets.

Butylated Hydroxytoluene Industry Leaders

BASF SE

Eastman Chemical Company

Honshu Chemical Industry Co., Ltd.

LANXESS

Oxiris Chemicals S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Clean Fino-Chem Limited (CFCL), a wholly owned subsidiary of Clean Science and Technology Limited, has commenced commercial production of Butylated Hydroxy Toluene (BHT). The commercialization of BHT, a significant antioxidant, positions the company to play a crucial role in the antioxidant supply chain.

- September 2024: The United Kingdom has implemented stricter regulations on the use of Butylated Hydroxytoluene (BHT) in cosmetic products. This measure emphasizes the need for distributors, manufacturers, and importers to ensure compliance and uphold the safety standards of their products in the UK market.

Global Butylated Hydroxytoluene Market Report Scope

The addition reaction of p-cresol and either 2-methylpropene or isobutylene produces butylated hydroxytoluene (BHT). It is widely used as an antioxidant and a stabilizing agent in cosmetics and personal care products. It helps preserve the properties and functionality of materials exposed to air and vulnerable to oxidation, such as odor, color, and texture. The market is segmented based on type, end-user industry, and geography. By type, the market is segmented into food grade and technical grade. By end-user industry, the market is segmented into plastics and rubber, food and beverage, personal care and cosmetics, animal feed, and other end-user industries. The report offers market size and forecasts for 15 countries across major regions. For each segment, market sizing and forecasts are based on revenue (USD) for all the above segments.

| Food Grade |

| Technical Grade |

| Plastics and Rubber |

| Food and Beverage |

| Personal Care and Cosmetics |

| Animal Feed |

| Other End-user Industries (Pharmaceuticals, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Grade | Food Grade | |

| Technical Grade | ||

| By End-user Industry | Plastics and Rubber | |

| Food and Beverage | ||

| Personal Care and Cosmetics | ||

| Animal Feed | ||

| Other End-user Industries (Pharmaceuticals, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in the Butylated Hydroxytoluene market?

Increasing polymer production in Asia-Pacific, higher processed-food consumption and rising personal-care launches needing oxidative stability are key growth drivers supported by a 5.54% CAGR forecast.

Why does Technical Grade dominate Butylated Hydroxytoluene market share?

Technical Grade meets stringent thermal-stability requirements in polymer and lubricant processing, holding 61.52% share in 2025 because cost-effectiveness outweighs purity demands in industrial settings.

How will clean-label trends affect Butylated Hydroxytoluene demand?

Natural antioxidant adoption will limit growth in consumer foods and cosmetics, subtracting an estimated 0.8 percentage points from forecast CAGR, yet industrial applications are expected to maintain usage.

Which region offers the fastest growth for Butylated Hydroxytoluene suppliers?

Asia-Pacific is set to expand at a 6.05% CAGR through 2031, thanks to manufacturing capacity additions and rising packaged-food uptake, delivering the largest incremental volume opportunity.

What regulatory changes should companies monitor?

The EU’s Chemicals Strategy for Sustainability and UK concentration limits in cosmetics impose stricter hazard-based evaluations, necessitating proactive dossier updates and reformulation strategies.

Page last updated on: