Methyl Ester Ethoxylate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

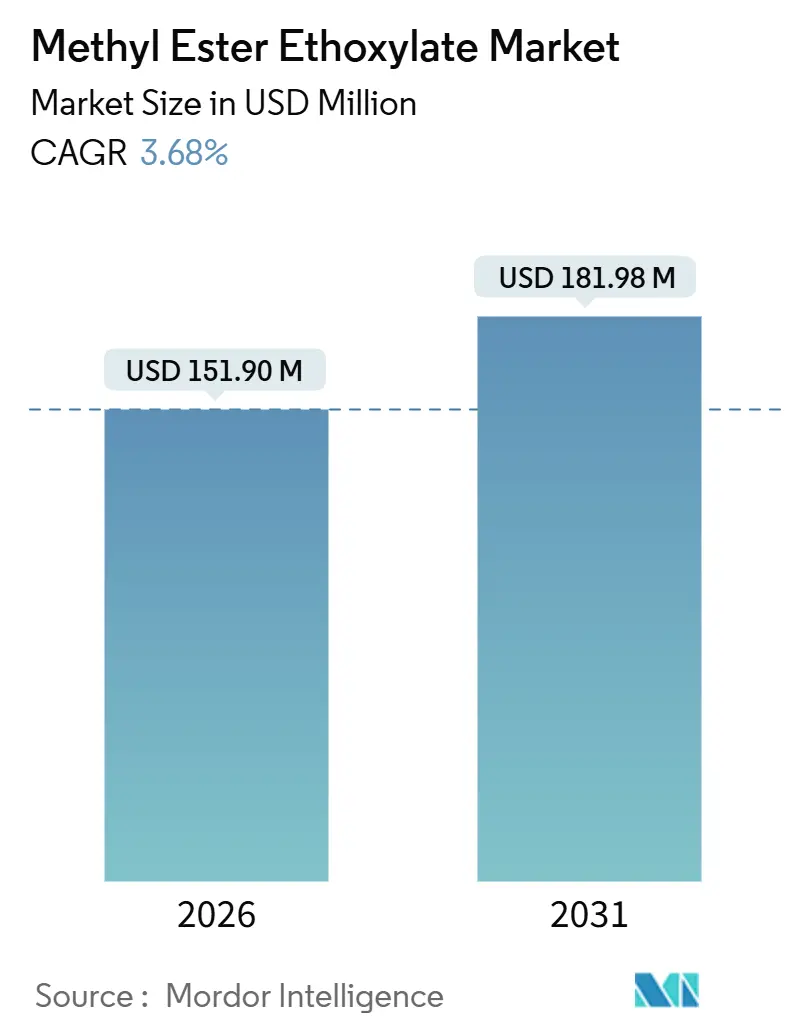

| Market Size (2026) | USD 151.90 Million |

| Market Size (2031) | USD 181.98 Million |

| Growth Rate (2026 - 2031) | 3.68% CAGR |

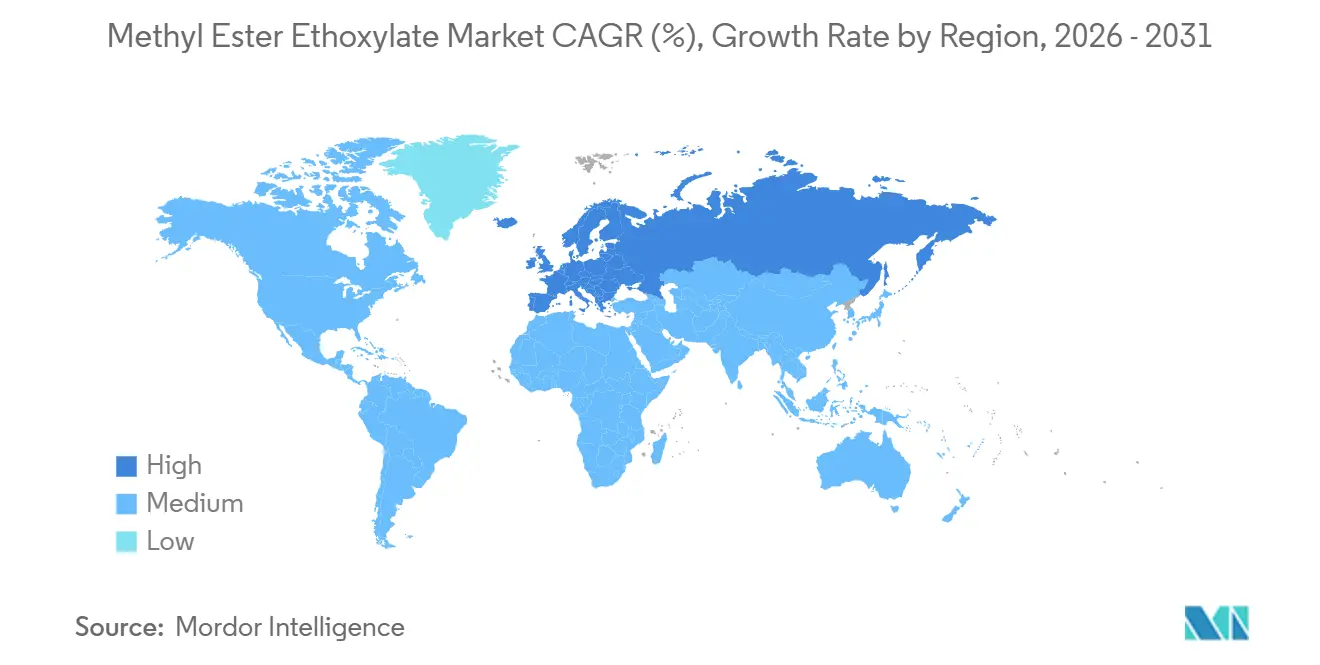

| Fastest Growing Market | Europe |

| Largest Market | Europe |

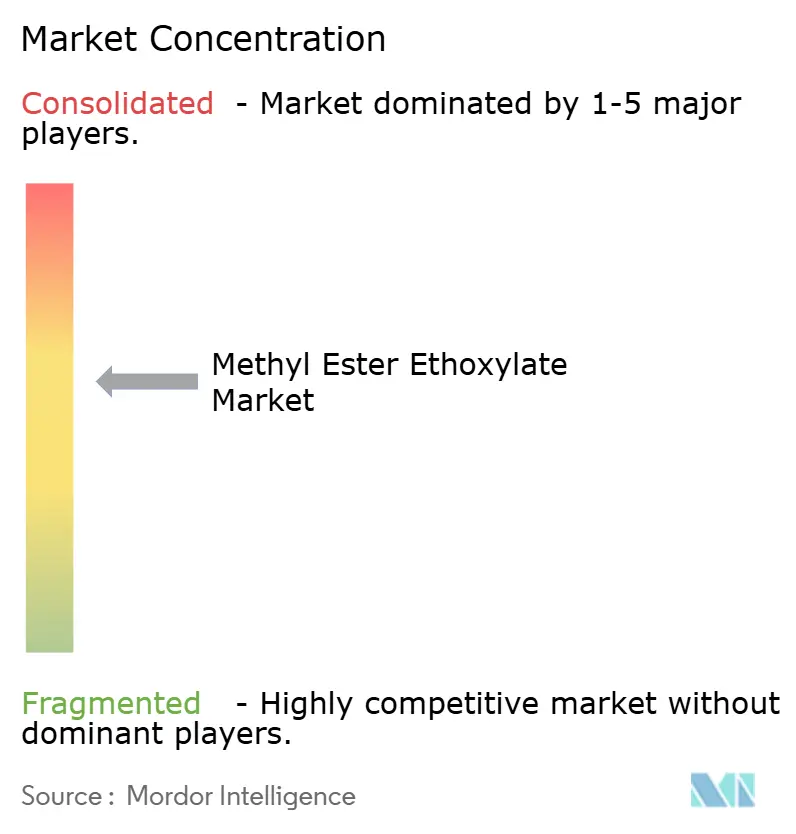

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Methyl Ester Ethoxylate Market Analysis by Mordor Intelligence

The Methyl Ester Ethoxylate Market size is estimated at USD 151.90 million in 2026, and is expected to reach USD 181.98 million by 2031, at a CAGR of 3.68% during the forecast period (2026-2031). This trajectory captures the sector’s shift away from commoditized tonnage toward higher-margin grades that satisfy stricter biodegradability rules and address mounting Scope 3 emissions targets set by global brand owners. Growth remains closely tied to detergent and industrial-cleaning consumption in Asia-Pacific, where institutional buyers favor low-foam, rapid-rinse formats that cut water and energy use. Europe is emerging as the fastest-growing geography, buoyed by proposed detergent-regulation amendments that encourage formulators to swap linear alkylbenzene sulfonates for readily biodegradable nonionics. Meanwhile, enzymatic ethoxylation is beginning to reshape production economics by trimming energy demand and carbon footprints, thereby differentiating suppliers competing with a wave of bio-based alternatives. Oleochemical feedstock volatility and certification costs remain the primary near-term headwinds, but strategic moves into coconut- and rapeseed-derived fatty acids coupled with backward integration are moderating margin pressure.

Key Report Takeaways

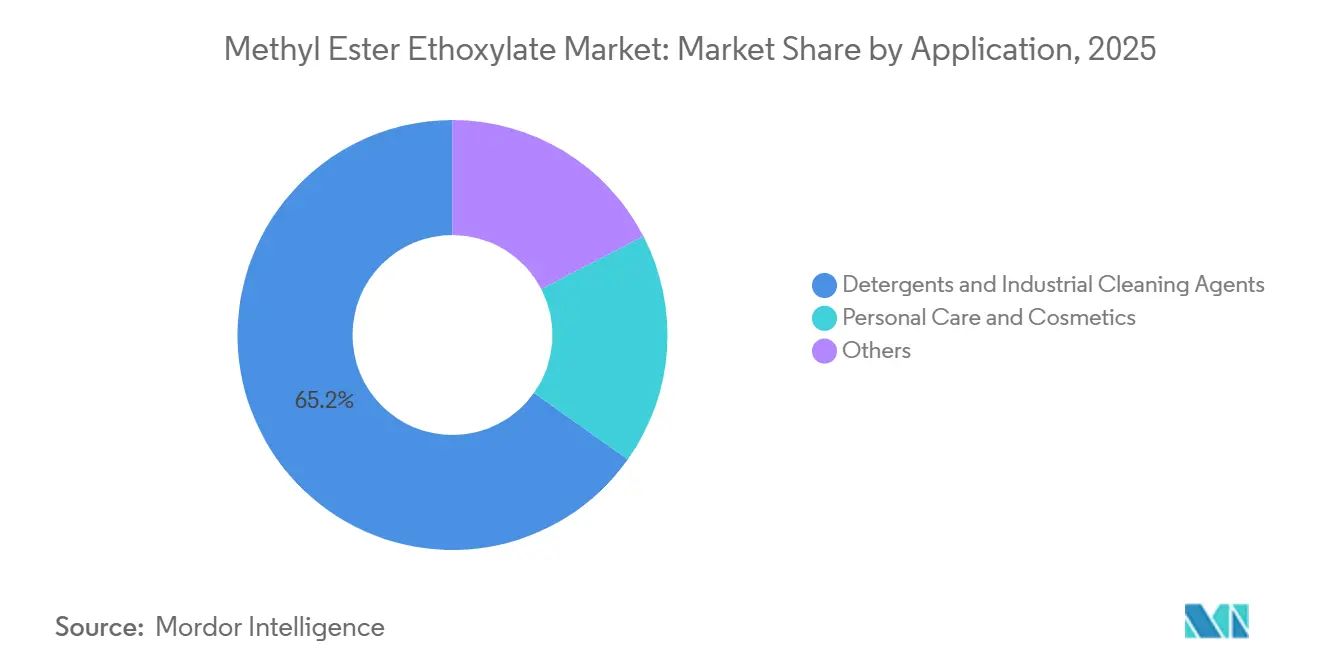

- By application, detergents and industrial cleaning agents led with 65.18% of the methyl ester ethoxylate market share in 2025, and will record the highest projected 3.98% CAGR through 2031.

- By geography, Europe held 37.53% of the methyl ester ethoxylate market share in 2025 and is forecast to expand at a 4.39% CAGR through 2031, the fastest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Methyl Ester Ethoxylate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from personal care and cosmetics | +0.6% | North America, Europe | Medium term (2-4 years) |

| Growth of low-foam, single-wash detergent formats | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Regulatory push for biodegradable surfactants | +1.1% | Europe, North America, emerging in China | Long term (≥ 4 years) |

| Expansion of industrial and institutional cleaning in Asia-Pacific | +0.8% | China, India, ASEAN, secondary Middle East | Medium term (2-4 years) |

| Enzymatic ethoxylation lowering carbon footprint | +0.5% | Global, early adoption in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Personal Care and Cosmetics

Methyl ester ethoxylates provide foam stability without the irritation often associated with anionic surfactants. This quality makes them a preferred choice for sulfate-free shampoos, body washes, and leave-on treatments, especially among clean-beauty consumers. The medium-term influence of this trend can be attributed to formulators striving to balance cost, sensory attributes, and eco-label compliance. While methyl ester ethoxylates are cost-competitive in mass-market hair-care and body-wash products, they find themselves in competition with amino-acid surfactants and alkyl polyglucoside (APG) blends in ultra-luxury skincare lines.

Growth of Low-Foam, Single-Wash Detergent Formats

Across Southeast Asia, institutional laundries and conveyor dishwashers are increasingly adopting single-wash, low-foam systems, leading to reduced water consumption and shorter cycle times. Kao reported a surge in sales of institutional detergents in the region, attributing the boost to their new formulation[1]Kao Corporation, “Annual Report 2024,” kao.com. This formulation, enhanced with methyl ester ethoxylates, enzymes, and chelants, ensures effective one-pass soil removal. In water-scarce nations like India, the introduction of appliance-efficiency labels is indirectly incentivizing the use of low-foam surfactant packages, hastening their adoption. This rapid embrace of low-foam systems is now making waves in the Middle East's hospitality sector, where soaring water tariffs are pushing hotel operators to overhaul their laundry practices.

Regulatory Push for Biodegradable Surfactants

Under the OECD 301 standard, the European Commission's 2024 proposal mandates that ultimate surfactants must biodegrade within 28 days. This move effectively sidelines certain poorly degradable linear alkylbenzene sulfonates from specific consumer and institutional products. While methyl ester ethoxylates meet the new standards, heightened ceilings for aquatic toxicity and stricter thresholds for anaerobic digestion are narrowing the formulation options. In the U.S., the EPA's 2025 Safer Choice update is placing a similar emphasis on biodegradability[2]U.S. Environmental Protection Agency, “Safer Choice Criteria,” epa.gov. Likewise, China's 2025 draft standards are aligning with this trend. In response, producers are not only expanding their analytical laboratories but also reformulating their blends, all in a bid to secure the coveted ISO 14024 eco-labels. This underscores the long-term global significance of these regulatory drivers.

Expansion of Industrial and Institutional Cleaning in Asia-Pacific

In China, India, and ASEAN states, urbanization, increased healthcare investments, and a resurgence in tourism are fueling a surge in demand for institutional cleaning. In 2024, India Glycols reported an increase in surfactant shipments to cleaning distributors, a move spurred by government hygiene mandates in public hospitals and schools. China's commercial cleaning services market experienced growth in 2025, driven by a trend of outsourcing to professional custodial firms that emphasize standardized low-residue products. Methyl ester ethoxylates, known for their compatibility with alkaline builders and chlorine sanitizers, are becoming essential in floor care, hard surfaces, and on-premise laundry solutions in these rapidly growing economies.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from more efficient alternative surfactants | −0.7% | Europe and North America, spreading globally | Medium term (2-4 years) |

| Oleochemical feedstock price volatility | −0.5% | Global, most severe in Asia-Pacific and South America | Short term (≤ 2 years) |

| Supply-chain certification (RSPO, traceability) costs | −0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from More Efficient Alternative Surfactants

In 2024, Evonik launched a rhamnolipid plant in Slovakia. The biosurfactant produced there biodegrades faster than traditional methyl ester ethoxylates in anaerobic conditions and achieves the same wetting effect at reduced dosage. Also in 2024, BASF boosted its APG capacity, promoting a glucose-based nonionic that surpasses methyl ester ethoxylates in both cold-water detergency and foam control. Producers like Elevance, specializing in sophorolipids, achieve lower surface tensions, allowing for a reduction in total surfactant load. Despite price advantages for methyl ester ethoxylates in volume-driven institutional markets, rising fermentation yields and decreasing capital costs are heightening competitive pressures in Europe and North America.

Oleochemical Feedstock Price Volatility

Producers face volatility as palm and coconut oils, which constitute a significant portion of the methyl ester feedstock, are influenced by weather events, biofuel mandates, and geopolitical disruptions. Palm oil prices surged, tightening margins for producers without plantation integration or hedge contracts. Coconut oil prices jumped due to drought-induced yield reductions in Southeast Asia. While some manufacturers experiment with rapeseed and sunflower methyl esters, the complexities arise from performance trade-offs and distinct price cycles. The financial strain is most pronounced in Asia-Pacific and Latin America, regions where oleochemical supply chains are prevalent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Detergents Dominate, Personal Care Commands Premium

The detergents and industrial-cleaning segment captured 65.18% of 2025 revenue, and its share of the methyl ester ethoxylate market size is projected to expand at a 3.98% CAGR through 2031. Growth rests on institutional laundries and conveyor dishwashers that prize low-foam, hard-water-tolerant surfactant systems capable of one-pass soil removal in high-throughput tunnels. Methyl ester ethoxylates pair well with alkaline builders, enzymes, and chlorine sanitizers, sustaining their role as drop-in workhorses for commercial dishwashing, hospitality laundering, and food-service floor cleaning across Asia-Pacific and the Middle East.

Demand in household laundry remains sizable yet moderating in mature markets as concentrated pods and unit-dose sachets favor higher-activity blends of APG and linear alkylbenzene sulfonates. Nevertheless, value-added formats such as ultra-low-dose powders for mechanized laundries are opening margin-rich niches where methyl ester ethoxylates’ foam control provides cycle-time advantages. Adoption of enzymatic pre-treatment concentrates further integrates the surfactant into broader cleaning packages that cut chemical load without sacrificing whiteness.

While personal care and cosmetics lag in volume, they consistently command premium margins, often pricing above their detergent-grade counterparts. The methyl ester ethoxylate market for this segment is projected to grow, buoyed by sulfate-free and mild-surfactant claims that appeal to consumers with sensitive skin. Nonionic backbones not only stabilize foam and maintain viscosity in clear shampoos and body washes, but they also mitigate irritation concerns commonly associated with anionic surfactants. Prestige beauty houses are securing COSMOS-certified supply chains, yet they grapple with competition from amino-acid surfactants and APG blends, which boast even milder dermatological profiles and a higher bio-based content.

Geography Analysis

Europe, accounting for 37.53% of 2025 revenue, leads the methyl ester ethoxylate market share and is forecast to grow at a 4.39% CAGR, the highest regional rate. Demand is anchored in Germany, the United Kingdom, and France, where Blue Angel and Nordic Swan eco-labels steer formulators toward readily biodegradable nonionics. Southern European hospitality booms are elevating low-residue cleaning requisites, notably in Spain and Italy. Eastern Europe remains underpenetrated, yet rising hygiene standards and the gradual rollout of EU-aligned regulations signal medium-term upside for suppliers prepared to navigate fragmented distributors.

By 2025, the Asia-Pacific region is set to account for a significant share of global revenue, boasting a projected growth. In 2025, China's commercial cleaning services saw robust growth, driven by retailers and hotels opting for outsourced custodial services, with a shift towards standardized, surface-friendly, low-foam cleansers. Meanwhile, India is testing energy-efficiency labels that prioritize water-saving laundry cycles, inadvertently promoting the use of methyl ester ethoxylate. Japan and South Korea are witnessing steady growth, focusing on cleaning products for personal care and electronics. The hospitality sector in ASEAN is rebounding from the pandemic, leading to increased demand for floor-care and hard-surface cleaners. Simultaneously, government hygiene mandates in educational and healthcare institutions are driving up demand.

North America is projected to account for a significant share of the 2025 revenue, with steady growth. The EPA’s Safer Choice initiative is steering formulators towards biodegradable surfactants. However, the growth potential is tempered by the maturity of the household detergent market. In Canada and Mexico, there's a swift adoption of eco-labeled cleaners in institutions, bolstered by cross-border supply chains that simplify compliance. South America, along with the Middle East and Africa, is expected to capture a notable portion of the 2025 turnover. Key players include Brazil and Argentina in South America, and Saudi Arabia and South Africa in the Middle East and Africa. While currency fluctuations, tariff changes, and underdeveloped regulations introduce volatility, the trends of urbanization and heightened hygiene standards suggest a long-term alignment with the demands of more developed markets.

Competitive Landscape

The global methyl ester ethoxylate market is moderately consolidated in nature. Strategic focus converges on backward integration into oleochemical feedstocks, geographic expansion across ASEAN and India, and co-development pacts with detergent majors to secure multi-year offtake. Mid-tier players are carving niches in personal-care and industrial adjacencies. Start-ups are exploring enzymatic ethoxylation scale-up and rapeseed-based feedstock diversification, aiming to combine carbon-footprint benefits with price stability. Patent filings on lipase-catalyzed ethoxylation and solvent-free routes have accelerated. Compliance with ISO 14024 eco-labels and RSPO certification is solidifying as a baseline requirement in Europe and North America, favoring players with capital to absorb audit and documentation costs. Competitive intensity is therefore migrating from purely price-based battles toward sustainability credentials, supply-chain transparency, and formulation-support services.

Methyl Ester Ethoxylate Industry Leaders

KLK OLEO

Lion Specialty Chemicals Co. Ltd

INEOS

Huntsman Corporation

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Bhageria Industries Limited, a specialty chemicals maker, launched a new Plasticizers and Ethoxylates product line. This follows the Maharashtra Pollution Control Board's (MPCB) Consent to Operate granted on October 7, 2025.

- July 2024: Clariant signed a deal with OMV to supply renewable low-carbon ethylene, supporting bio-based ethylene oxide derivatives and low-carbon ethoxylates in Europe. This is expected to drive growth in the market.

Global Methyl Ester Ethoxylate Market Report Scope

Methyl ester ethoxylate is an ester that yields methanol on hydrolysis of methyl esters of carboxylic acids. Methyl ester ethoxylates are low-foaming, non-ionic surfactants compared to fatty alcohol ethoxylates.

The methyl ester ethoxylate market is segmented by application and geography. By application, the market is segmented into detergents and industrial cleaning agents, personal care and cosmetics, and others. By geography, it is segmented into Asia-Pacific, North America, Europe, South America, and the Middle-East and Africa. The report also covers the size and forecasts for the methyl ester ethoxylate market in 16 countries across major regions. The report offers market size and forecasts in terms of revenue in USD million for all the above segments. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Detergents and Industrial Cleaning Agents |

| Personal Care and Cosmetics |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Detergents and Industrial Cleaning Agents | |

| Personal Care and Cosmetics | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the methyl ester ethoxylate market?

The methyl ester ethoxylate market size stands at USD 151.90 million in 2026, growing with a CAGR of 3.68% reaching USD 181.98 million, supported by institutional cleaning demand and regulatory shifts toward biodegradable surfactants.

Which application contributes the biggest revenue share?

Detergents and industrial cleaning agents dominate with 65.18% of 2025 revenue, expanding at a 3.98% CAGR as low-foam, rapid-rinse formulations gain traction.

Why is Europe the fastest-growing region?

Europe’s 4.39% CAGR stems from draft detergent regulations that phase out poorly degradable surfactants and from stringent eco-label programs that favor methyl ester ethoxylates.

What is driving methyl ester ethoxylate use in personal care?

Sulfate-free, mild-surfactant claims in shampoos and body washes allow methyl ester ethoxylates to command price premiums among COSMOS-certified prestige brands.

Which emerging biosurfactants pose the biggest threat?

Rhamnolipids, alkyl polyglucosides, and sophorolipids are narrowing the cost-performance gap by offering faster biodegradation and lower use rates, particularly in Europe and North America.

Page last updated on: