Smoked Fish Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

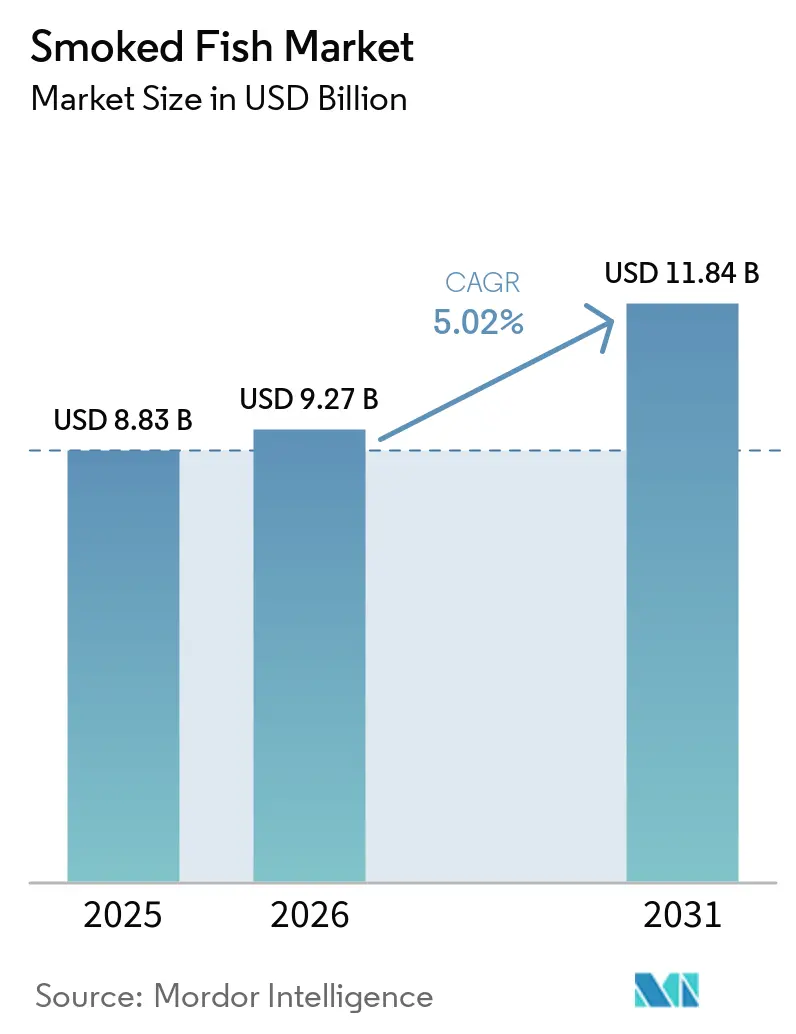

| Market Size (2026) | USD 9.27 Billion |

| Market Size (2031) | USD 11.84 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

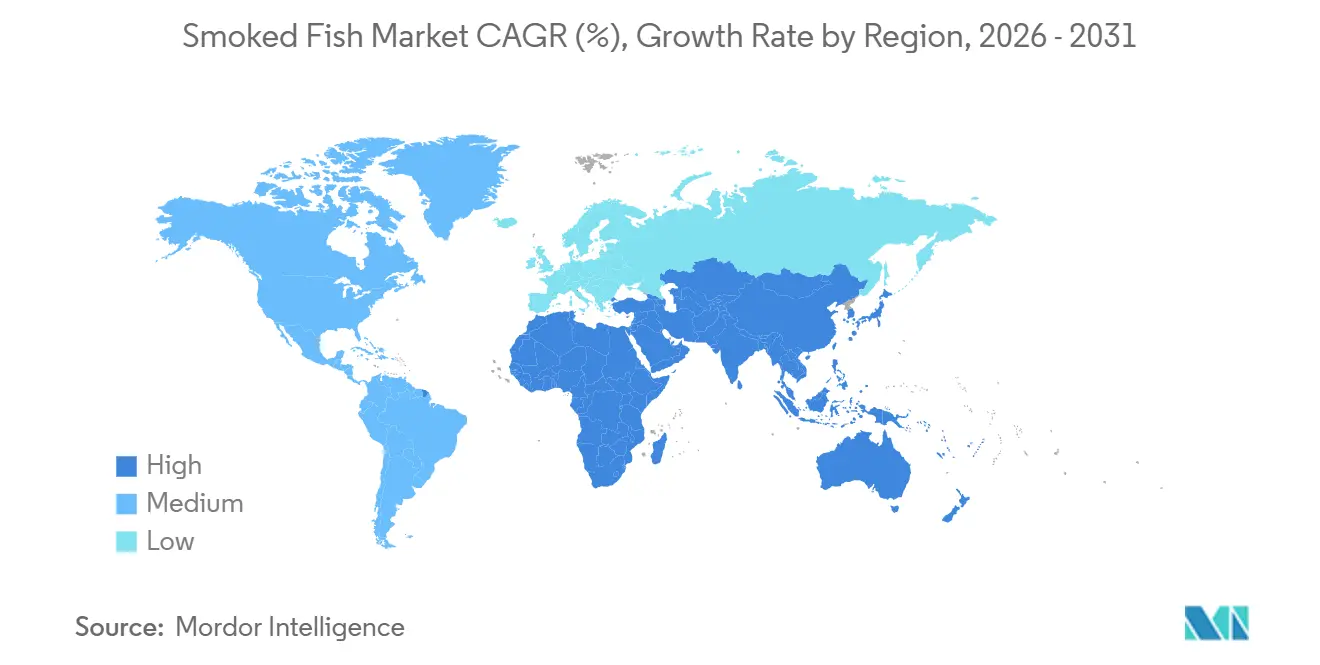

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Smoked Fish Market Analysis by Mordor Intelligence

Despite facing cost challenges and evolving consumer preferences, the Smoked Fish Market is poised for steady growth. Projected to rise from USD 8.83 billion in 2025 to USD 9.27 billion in 2026, the market is forecasted to hit USD 11.84 billion by 2031, marking a CAGR of 5.02% from 2026 to 2031. This growth is buoyed by a global shift towards health-conscious consumption and advancements in cold-chain logistics. While premium product positioning ensures price stability, cold-smoked fish products lead in revenue generation, especially in Europe, where they hold cultural significance. On the other hand, hot-smoked fish products are witnessing a surge, thanks to a rebound in the foodservice sector and an expanded menu post-pandemic. The Asia-Pacific stands out as a pivotal growth hub, fueled by rising urbanization and a broader protein consumption palette. Furthermore, the market's fragmented nature offers consolidation avenues for major corporations eyeing acquisitions, while niche producers cater to specific segments.

Key Report Takeaways

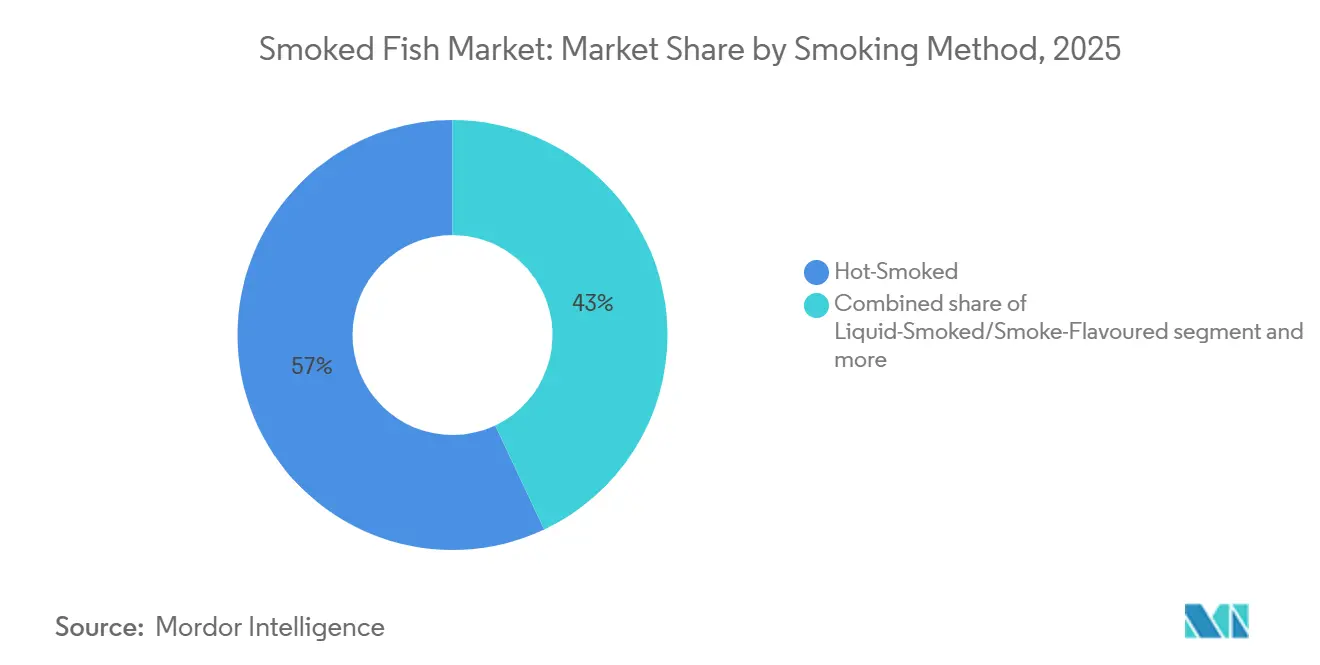

- By smoking method, hot-smoked products led with 57.01% of the smoked fish market share in 2025, while liquid-smoked and smoke-flavored variants are advancing at a 6.01% CAGR through 2031.

- By species, salmon commanded 43.81% share of the smoked fish market size in 2025, and trout is projected to expand at a 6.52% CAGR between 2026 and 2031.

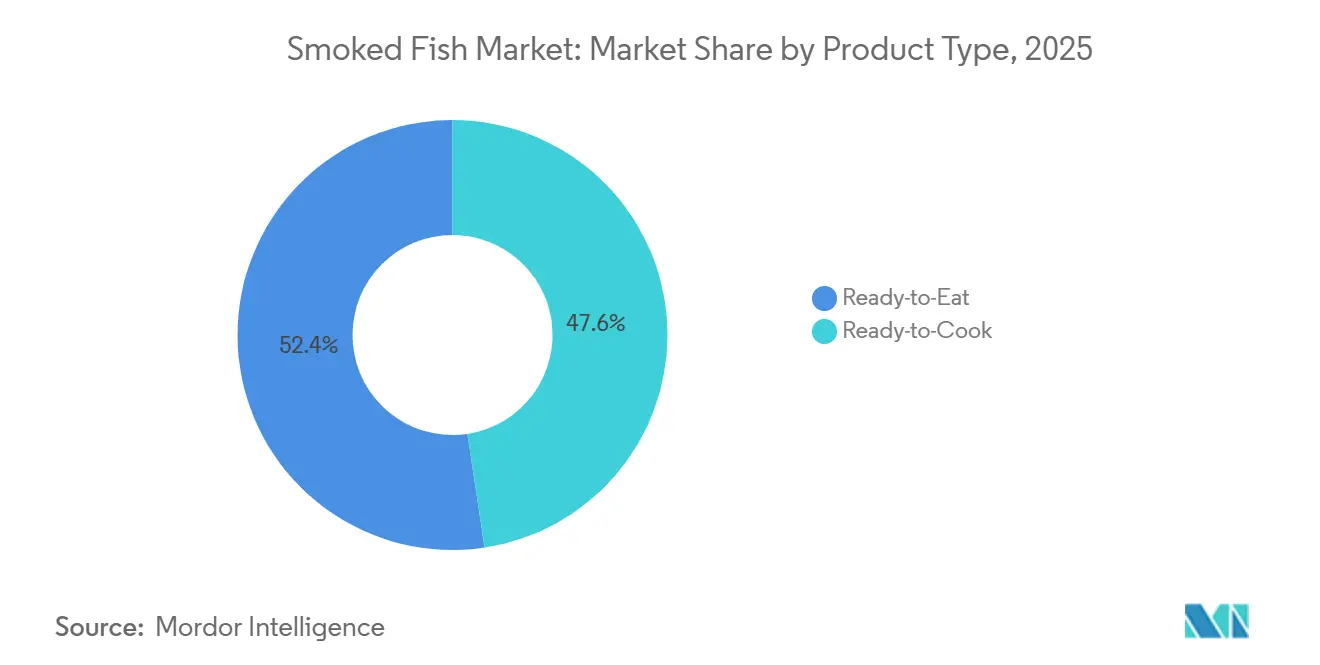

- By product type, ready-to-eat formats held 52.38% revenue share in 2025, whereas ready-to-cook offerings are forecast to post a 7.21% CAGR to 2031.

- By distribution channel, off-trade retail captured 65.92% share in 2025, and on-trade foodservice is rebounding at a 6.98% CAGR through 2031 as casual dining recovers.

- By geography, Europe accounted for 40.03% of the 2025 value, while Asia-Pacific is set to record the fastest regional CAGR at 7.45% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smoked Fish Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for ready-to-eat and ready-to-cook seafood aligns with busy lifestyles | +1.2% | Global, with early gains in North America, Western Europe, and urban Asia-Pacific (Singapore, Japan, South Korea) | Short term (≤ 2 years) |

| Growth in pescatarian and flexitarian diets boosts seafood as a meat alternative | +1.5% | North America, Europe, and Australia; emerging in urban China and India | Medium term (2-4 years) |

| E-commerce and online retail growth enables wider reach and direct-to-consumer sales | +0.8% | Global, with APAC core (China, Japan, Singapore) and spill-over to Middle East and South America | Short term (≤ 2 years) |

| Sustainable sourcing, certifications like MSC/ASC, and traceability build consumer trust | +1.0% | Europe, North America, and premium segments in Asia-Pacific | Medium term (2-4 years) |

| Seafood's high protein, omega-3s, and vitamins support heart health and weight management | +0.9% | Global, with strongest uptake in North America and Europe | Long term (≥ 4 years) |

| Increasing popularity of gourmet and artisanal foods | +0.6% | North America, Western Europe, and affluent urban centers in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for ready-to-eat and ready-to-cook seafood aligns with busy lifestyles.

As urbanization accelerates and dual-income households face tighter meal-preparation windows, consumers increasingly prefer proteins requiring minimal effort. Ready-to-cook smoked fish, such as Echo Falls' Smoked Norwegian Atlantic Salmon Party Slices, lightly smoked and ready in 10-15 minutes, gained significant retail shelf space in 2025. These products, launched in January 2026, cater to the growing demand for convenient options suited for weeknight dinners and impromptu gatherings. In Japan, the Ministry of Agriculture, Forestry, and Fisheries reported that 70% of the seafood supply consists of processed products, highlighting a strong consumer preference for convenience over raw preparation. Additionally, per-capita seafood consumption stabilized at 22.0 kilograms in 2022 after years of decline, suggesting that value-added formats like smoked fish are helping to reverse this trend. In China, e-commerce platforms such as Freshippo, Meituan Grocery, and Douyin have transformed seafood distribution by enabling same-day delivery of chilled smoked salmon to inland cities, bypassing traditional wet markets and reducing spoilage risks. This shift is particularly evident in tier-2 and tier-3 cities, where significant improvements in cold-chain infrastructure between 2024 and 2026 have expanded access to premium smoked products for previously underserved consumers[1]Source: Agriculture and Agri-Food Canada. "Sector Trend Analysis – Fish and seafood trends in China", agriculture.canada.ca.

Growth in pescatarian and flexitarian diets boosts seafood as a meat alternative

As plant-based and flexitarian diets continue to grow in popularity, many consumers are shifting towards animal proteins with a lower environmental impact, such as fish and seafood, instead of traditional beef or pork. In Germany, research conducted in May 2025 revealed that 38% of adults planned to increase their plant-based consumption, while 34% intended to reduce their intake of animal meat and dairy. Notably, fish and seafood experienced only an 8% net decline compared to the 19% drop for red meat, highlighting their sustained appeal among reducetarians[2]Source: Good Food Institute Europe. "Germany – Understanding plant-based category dynamics, motivations and consumers." gfieurope.org. Smoked fish, in particular, benefits from this trend as the smoking process enhances umami flavors and extends shelf life without relying on additives commonly found in processed red meats, aligning with the clean-label preferences of modern consumers. Additionally, the Norwegian Seafood Council reported that over 30% of global seafood consumers began eating more seafood at home during inflationary periods to save costs, with many opting for premium options like smoked salmon meal kits and subscription boxes that offer restaurant-quality experiences at lower prices. Younger consumers aged 25-34 are leading this shift, showing the strongest intent to increase both plant-based and seafood consumption, creating a significant opportunity for smoked fish brands that emphasize sustainability and high-protein nutrition.

E-commerce and online retail growth enables wider reach and direct-to-consumer sales

Smoked fish, with its higher unit value and extended vacuum-packed shelf life, is particularly well-suited for e-commerce. Direct-to-consumer models, such as Wulf's Fish in the United States and Fish Delish in Canada, which launched in September 2025, offering artisan smoked salmon with kosher certification, enable producers to retain retail margins while fostering brand loyalty through subscription boxes and customizable selection options[3]Source: Norwegian Seafood Council, "Evolving retail channels in a disrupted global seafood market", en.seafood.no. In China, livestreaming commerce on platforms like Douyin and Xiaohongshu has demonstrated significant potential, as a single Norwegian Seafood Council campaign garnered over 15 million views, showcasing the ability to convert browsing into purchases instantly while bypassing traditional distribution layers. South Korea's advanced cold-chain logistics and strong consumer trust in online reviews have driven the success of frozen and chilled seafood e-commerce, providing a model for other Asia-Pacific markets experiencing rising urbanization and smartphone penetration. The shift towards omnichannel retail, which integrates physical fishmongers, wholesale, and online sales under one brand, has proven effective in reducing customer acquisition costs and mitigating demand volatility, further strengthening the market's adaptability and growth potential.

Sustainable sourcing, certifications like MSC/ASC, and traceability build consumer trust

Certifications from the Marine Stewardship Council (MSC) and the Aquaculture Stewardship Council (ASC) have become essential for premium retail placement in Europe and North America. In February 2026, the MSC Improvement Program received recognition from ASC's Feed Standard, simplifying traceability protocols and reducing audit redundancies for vertically integrated producers. Alaska's salmon fisheries achieved MSC recertification in November 2024, reinforcing their status as a reliable supplier of sustainable wild-catch salmon, particularly for smoked salmon processors focusing on provenance. Similarly, in August 2024, Secret Smokehouse in the United Kingdom obtained B Corp certification, showcasing how smaller artisanal players are leveraging third-party validations to compete with larger brands on environmental and social governance metrics. In China, where food-safety scandals have undermined consumer trust in domestic supply chains, blockchain-based traceability systems are emerging as a solution. Importers of Norwegian and Chilean smoked salmon now use QR codes to provide farm-level data, catch dates, and processing timestamps, addressing the trust deficit. The European Union's reliance on third-country seafood, which accounts for 69% of its supply and includes 80% of salmon sourced from Norway, highlights the importance of import-compliance frameworks to ensure auditable sustainability claims. Although certification costs and complexities remain obstacles for small-scale smokehouses, the premium pricing they unlock justifies the investment. For instance, in December 2025, smoked Atlantic salmon fillets were priced at EUR 36.00-38.00 per kilogram, significantly higher than the EUR 21.00 per kilogram for trout, making certification a strategic move for producers targeting high-end retail and foodservice markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and food safety challenges | -0.7% | Global, with heightened enforcement in EU, North America, and Japan | Short term (≤ 2 years) |

| Short shelf life leads to spoilage risks and higher waste during storage | -0.9% | Global, with acute impact in emerging markets (Middle East, South America, Southeast Asia) | Short term (≤ 2 years) |

| Environmental impact of traditional smoking | -0.4% | Europe and North America, with regulatory pressure from environmental agencies | Medium term (2-4 years) |

| Competition from fresh, frozen, or alternative seafood products | -0.5% | Global, with strongest substitution in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory and food safety challenges

New food safety regulations and compliance requirements are posing operational challenges for the smoked fish market. Changes within the FDA have led to a reduction in specialized expertise, potentially causing delays in seafood trade and import approvals, thereby disrupting supply chain operations. Due to heightened risks of Listeria monocytogenes contamination in cold-smoked fish products compared to their hot-smoked counterparts, the UK's Food Standards Agency is mandating stricter HACCP protocols. In a parallel move, the USDA's actions against meat smoking operations, including recalls due to creosote and black particle contamination, have cast a shadow of regulatory uncertainty over fish smoking processes. Additionally, the market is witnessing a surge in demand for certifications such as BRCGS, MSC, and ISO 22000, creating higher barriers to entry in the premium segment. As a result, these stringent regulatory standards tend to benefit larger companies equipped with dedicated compliance departments and robust food safety systems. In contrast, smaller processors find it challenging to navigate these requirements, potentially paving the way for market consolidation.

Short shelf life leads to spoilage risks and higher waste during storage

Vacuum-packed smoked salmon remains fresh for 55-62 days at 4°C, whereas air-packed variants spoil within 24-27 days, with any cold-chain breach accelerating microbial growth and lipid oxidation, which degrade flavor and texture. Modified atmosphere packaging using 100% carbon dioxide can extend the shelf life of cod fillets to 40-53 days; however, high CO2 levels cause increased drip loss and color changes, making it less suitable for smoked fish, where visual appeal and moisture retention are critical. Emerging markets in the Middle East and South America face significant spoilage challenges due to inadequate cold-chain infrastructure. For example, Saudi Arabia aims to increase per-capita seafood consumption from 11.7 kilograms in 2020 to 20 kilograms by 2030, but achieving this target requires expanding cold-chain systems beyond coastal hubs like Jeddah and Dammam, as inland regions still lack refrigerated last-mile delivery. In January 2026, Chile exported 96,503 tons of salmon, marking a 13.5% year-on-year increase in volume, yet only 0.6% of these exports were smoked formats, highlighting the difficulty of maintaining quality during long-distance shipments to Asia and the United States. Retailers often absorb spoilage costs through markdowns and write-offs, which compress profit margins, discourage deeper inventory levels, and limit product availability and consumer choice.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Smoking Method: Liquid Smoke Gains as Clean-Label Demand Rises

In 2025, hot-smoked products captured a dominant 57.01% share of the market, leading both retail and foodservice sectors. This method not only fully cooks the fish but also extends its shelf life and imparts a robust flavor, reminiscent of traditional smokehouse techniques. The widespread adoption of hot smoking can be traced back to decades of investments in brick kilns and automated smoking chambers. However, this process isn't without its drawbacks: it produces polycyclic aromatic hydrocarbons and demands 8-12 hours of fuel combustion, raising both environmental and health concerns. On the other hand, cold-smoked variants, often chosen for premium salmon and trout, maintain the fish's delicate texture and translucent look. Yet, they require meticulous temperature management (staying below 30°C) and extended curing durations, which can limit production rates and inflate labor expenses.

Forecasted to grow at a 6.01% CAGR through 2031, liquid-smoked and smoke-flavored products are leading the pack among smoking methods. This surge is largely attributed to processors embracing innovations like Sensient's SmokeLess Smoke, introduced in March 2024. This solution slashes flavoring time by 40-60% and cuts down ingredient additives by 85%, all while preserving the essence of natural smoke. Meanwhile, products like Ruitenberg's FumX range and proFagus's Pure Smoke, both derived from regenerated beech-wood liquid smokes, adhere to the European Union's clean-label standards and successfully eliminate carcinogenic compounds. This move aligns with retailer demands for safer product formulations. While liquid smoke commands a 20-25% premium over artificial flavors, high-volume producers, especially those catering to health-conscious consumers, find value in this trade-off. The savings from bypassing kiln maintenance, fuel expenses, and emissions permits make it a lucrative choice. In 2025, hickory-flavored liquid smoke dominated the global liquid smoke arena, holding a 35% share, a testament to North American palate preferences. In contrast, European processors leaned towards beech and oak flavor profiles.

By Species: Trout Gains Ground as RAS Technology Scales

In 2025, salmon dominated the species market with a 43.81% share, supported by Norway's 815,300-ton Atlantic salmon harvest, which marked a 16.0% year-on-year increase, and Chile's total salmon production of 1.5 million tons, including Coho and Atlantic varieties. Smoked salmon maintained its premium positioning, with vacuum-packed fillets priced at EUR 36.00-38.00 per kilogram in December 2025, enabling vertically integrated producers like Mowi and SalMar to achieve high margins through their control over farming, processing, and distribution. Salmon's popularity is driven by its omega-3 content, strong brand recognition, and adaptability in ready-to-eat formats, ensuring consistent demand across retail, foodservice, and e-commerce channels. Meanwhile, mackerel and herring remain staples in European diets, with the Netherlands consuming 76 million herring annually, and smoked kippers being a traditional breakfast choice. However, wild-catch volatility and quota restrictions continue to limit supply growth for these species.

Trout, on the other hand, is projected to grow at a 6.52% CAGR through 2031, making it the fastest-growing species. This growth is attributed to the adoption of recirculating aquaculture systems (RAS), which enable year-round production while mitigating risks like sea-lice and algae blooms that affect marine salmon farms. Blue Aqua's RAS trout facility in Singapore, operational by the end of 2025 with an annual capacity of 1,025 tons, is Southeast Asia's first and targets premium smoked-trout demand in Japan and Singapore, where freshness and traceability are highly valued. In Europe, Finnforel introduced RAS-farmed trout with smoked fillets in 2025, emphasizing a low-carbon footprint and antibiotic-free production, which appeal to environmentally conscious consumers. Smoked trout fillets, priced at EUR 21.00 per kilogram in December 2025, offer a 44% discount compared to salmon, making them an attractive option for price-sensitive consumers and foodservice operators seeking cost-effective menu items. Additionally, trout's milder flavor and smaller fillet size are well-suited for single-serve packaging and snack formats, aligning with the growing demand for convenience-focused products.

By Product Type: Ready-to-Cook Expands as Meal-Kit Culture Spreads

In 2025, ready-to-eat formats captured a 52.38% market share, featuring vacuum-sealed slices, deli packs, and charcuterie-board assortments that require no further preparation. Dominating both supermarket seafood counters and online subscription boxes, these products cater to time-starved consumers, eliminating cooking risks and prioritizing convenience. Launched in March 2026, Ducktrap's Hot Honey Smoked Salmon showcases flavor innovation in the ready-to-eat segment, blending sweet and spicy notes to entice younger demographics and stand out on crowded retail shelves. Loch Duart's premium smoked salmon, introduced in May 2025, capitalized on Scotland's esteemed provenance, targeting gift markets and special occasions to command premium pricing.

Forecasted to grow at a 7.21% CAGR through 2031, ready-to-cook smoked fish emerges as the fastest-growing product type, driven by the rising meal-kit culture and the allure of semi-prepared proteins among dual-income households. Lightly smoked salmon portions from Select Fish, needing just 10-15 minutes of oven or pan finishing, retain moisture and offer home cooks the flexibility to customize seasoning and sauces. Launched in January 2026, Echo Falls' Smoked Norwegian Atlantic Salmon Party Slices cater to weeknight dinners and spontaneous entertaining, positioning themselves between fully prepared and raw seafood. These ready-to-cook formats not only mitigate spoilage risks for retailers, due to consumers purchasing closer to consumption, but also extend shelf life beyond that of raw fish, all while maintaining a "fresh" perception.

By Distribution Channel: On-Trade Rebounds as Casual Dining Recovers

Off-trade channels, supermarkets, hypermarkets, specialty stores, and online retail- commanded 65.92% of distribution in 2025, reflecting consumers' preference for at-home consumption and the cost savings versus restaurant dining. Supermarkets and hypermarkets remain the primary point of purchase for smoked fish, offering broad assortments, promotional pricing, and the ability to inspect packaging and expiration dates before buying. Specialty stores, fishmongers, and gourmet shops capture affluent consumers seeking artisanal products and personalized service, while online retail enables direct-to-consumer brands to bypass traditional retail markups and build subscription revenue streams. China's e-commerce platforms, Douyin, Freshippo, and Meituan Grocery, enable same-day delivery of chilled smoked salmon to inland cities, expanding addressable markets beyond coastal provinces.

On-trade foodservice is projected to grow at 6.98% CAGR through 2031, the fastest distribution channel, as casual dining and travel-leisure segments recover from pandemic-era closures. UK foodservice seafood sales reached GBP 6.47 billion in 2025, up 28.8% year-on-year, with smoked salmon featuring prominently in brunch menus, bagel sandwiches, and charcuterie boards that command high margins. Casual dining establishments grew seafood servings by 28%, and travel-leisure venues, airports, hotels, and cruise ships posted positive growth, reflecting pent-up demand for experiential dining. U.S. restaurant sales registered positive growth in 2026, with seafood categories benefiting from health-conscious diners seeking lean proteins. Smoked fish's premium positioning and ease of plating, no cooking required, make it attractive for quick-service and fast-casual operators who need to minimize kitchen labor while maintaining menu variety.

Geography Analysis

In 2025, Europe held 40.03% of the market share, driven by Norway's 815,300-ton Atlantic salmon harvest, a 16.0% year-on-year increase, and the Netherlands' Urk hub, which processes smoked herring and mackerel for European retail chains. Major markets like the UK, Germany, France, and Spain have made smoked salmon a staple, while EU regulations requiring MSC and ASC certifications ensure quality despite a 69% reliance on third-country imports, with 80% of salmon sourced from Norway. Poland and the Netherlands re-export bulk smoked fish from Norway and Iceland to key markets. In North America, Alaska's MSC-certified wild salmon fisheries (recertified in 2024) and Canada's lobster and shrimp exports support the market, though smoked fish remains a smaller segment compared to Europe.

Asia-Pacific, projected to grow at a 7.45% CAGR through 2031, benefits from rising incomes, urbanization, and e-commerce in China, Japan, and Singapore. In 2023, China imported USD 23.2 billion in seafood, with Norway supplying 50.8% of its USD 1.06 billion fresh salmon imports. Platforms like Douyin and Xiaohongshu streamline smoked product sales, while Japan's stabilized seafood consumption at 22.0 kilograms per capita in 2022 and Singapore's upcoming Blue Aqua RAS trout farm (1,025 tons annual capacity by 2025) highlight demand for premium, traceable products. South America and the Middle East, though smaller markets, show potential with Chile's 1.5 million tons of salmon production in 2025 and Saudi Arabia's plan to raise per-capita seafood consumption from 11.7 kilograms in 2020 to 20 kilograms by 2030, supported by expanding cold-chain infrastructure.

North America represents an established smoked fish market with developed distribution infrastructure, regulatory compliance requirements, and consumer health considerations. In 2024, salmon led U.S. fish consumption, with Alaska supplying 99% of the nation's production, supported by sustainability certification programs. Market participants include integrated corporations and specialized producers, utilizing cold-chain logistics and digital marketing operations. Market developments reflect regulatory requirements and consumer demand for product transparency. E-commerce distribution channels enable market access for premium smoked fish products to specific consumer segments.

Competitive Landscape

The smoked fish market remains highly fragmented, which creates room for both consolidation and specialized niche players. Larger companies are strengthening their positions through vertical integration, supply-chain control, and acquisitions, while smaller artisanal brands continue to compete by offering premium, locally rooted products.

Technology and compliance are becoming increasingly important competitive levers. Companies are investing in smart cold-chain tracking, advanced smoking and preservation methods, and sustainable processing to improve quality, reduce environmental impact, and meet stricter regulatory expectations.

At the same time, market participants are using direct-to-consumer channels, sustainability certifications, and culinary partnerships to build trust and brand visibility. Overall, success in this fragmented market depends on operational efficiency, product differentiation, and the ability to respond quickly to changing consumer and regulatory demands.

Smoked Fish Industry Leaders

-

Mowi ASA

-

Acme Smoked Fish Corp.

-

SalMar ASA

-

Labeyrie Fine Foods

-

Ocean Beauty Seafoods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Young's has expanded its restaurant-inspired Gastro range with the launch of Young's Gastro Luxury Fish Pie. Young’s Gastro Luxury Fish Pie is a premium single-serve frozen meal made with Atlantic salmon, pollock, smoked pollock, and king prawns in a mature cheddar and white wine sauce, topped with mashed potato and a cheddar-and-chive breadcrumb, according to the brand.

- March 2026: Patagonia Provisions expanded its tinned fish lineup with the launch of Smoked Jack Mackerel, a wild-caught product from Chile that is smoked over bay wood and packed with organic extra virgin olive oil and sea salt. According to the brand, the new item is fully cooked, shelf-stable, and positioned for use in pastas, salads, sandwiches, or camping meals

- February 2026: Waitrose launched a new range of smoked fish from April to offer customers tasty alternatives - including Hot Smoked Herring, Hot Smoked Peppered Herring and first to supermarket innovation, Hot Smoked Sweetcure Seabass.

- February 2025: Salmon Evolution, a land-based hybrid flow-through salmon producer, introduced the first smoked salmon from a land-based facility to the Norwegian retail market. The product became available at NorgesGruppen's Meny stores and select Spar locations. Through a strategic partnership with Lofotprodukt AS, the salmon produced at the Indre Harøy facility was processed and distributed under the premium Lofoten brand. This marked a significant development in land-based aquaculture production for the Norwegian consumer market.

Global Smoked Fish Market Report Scope

Smoked Fish is a fish product that has been preserved and flavored by exposing it to smoke, typically from burning wood such as oak, hickory, or beech.

The Smoked Fish Market Report is Segmented by Smoking Method into Hot-Smoked, Cold-Smoked, Liquid-Smoked/Smoke-Flavoured. By Species, the market is segmented into Salmon, Mackerel, Trout, Herring, and Others. By Product Type, the market is segmented into Ready-to-Eat and Ready-to-Cook. By Distribution Channel, the market is segmented into On-Trade and Off-Trade. By Geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Hot-Smoked |

| Cold-Smoked |

| Liquid-Smoked/Smoke-Flavoured |

| Salmon |

| Mackerel |

| Trout |

| Herring |

| Others (Sablefish, Eel, Haddock, etc.) |

| Ready-to-Eat |

| Ready-to-Cook |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Smoking Method | Hot-Smoked | |

| Cold-Smoked | ||

| Liquid-Smoked/Smoke-Flavoured | ||

| By Species | Salmon | |

| Mackerel | ||

| Trout | ||

| Herring | ||

| Others (Sablefish, Eel, Haddock, etc.) | ||

| By Product Type | Ready-to-Eat | |

| Ready-to-Cook | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global smoked fish sales be by 2031?

They are projected to reach USD 11.84 billion, up from USD 9.27 billion in 2026.

Which smoking technique shows the highest forecast growth?

Liquid-smoked and smoke-flavored products are set to advance at a 6.01% CAGR through 2031, outpacing hot- and cold-smoked formats.

Which region is expected to post the fastest sales gains by 2031?

Asia-Pacific is forecast to expand at a 7.45% CAGR, helped by improved cold-chain logistics and strong e-commerce adoption in China, Japan, and Singapore.

Which species is on track for the quickest growth?

Trout is projected to grow at a 6.52% CAGR as recirculating aquaculture systems deliver year-round, low-carbon supply.

Page last updated on: