Organic Fish Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

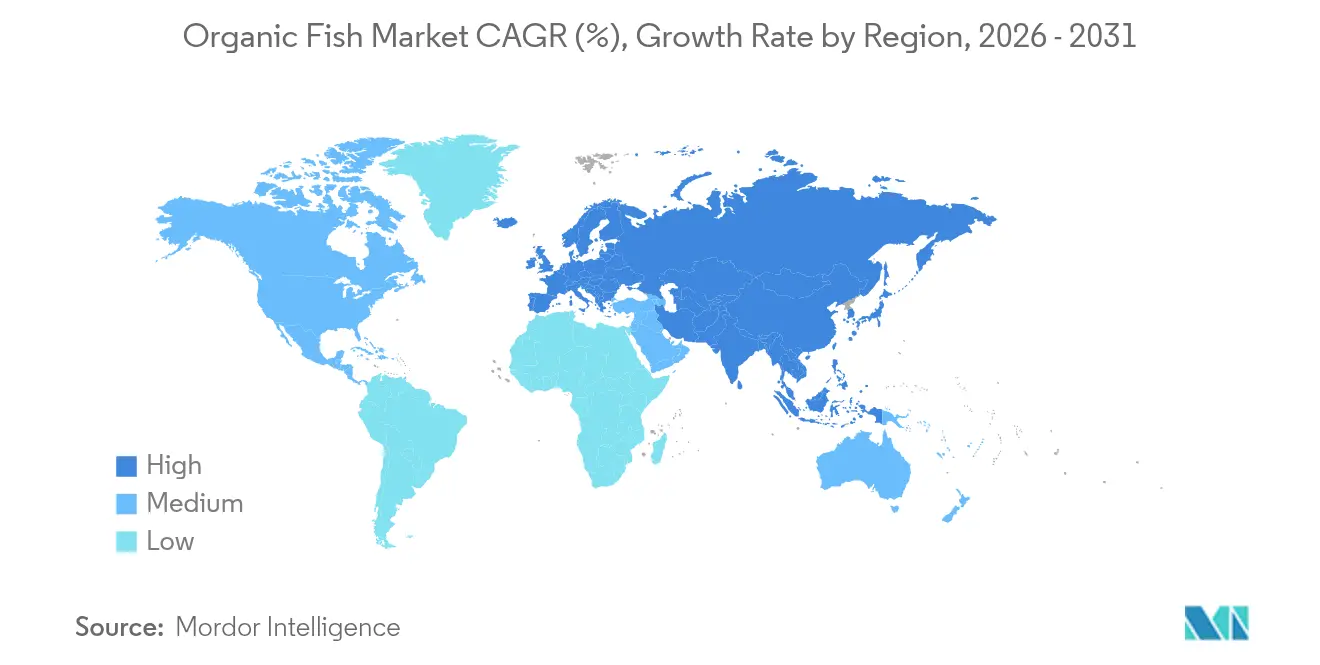

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Fish Market Analysis by Mordor Intelligence

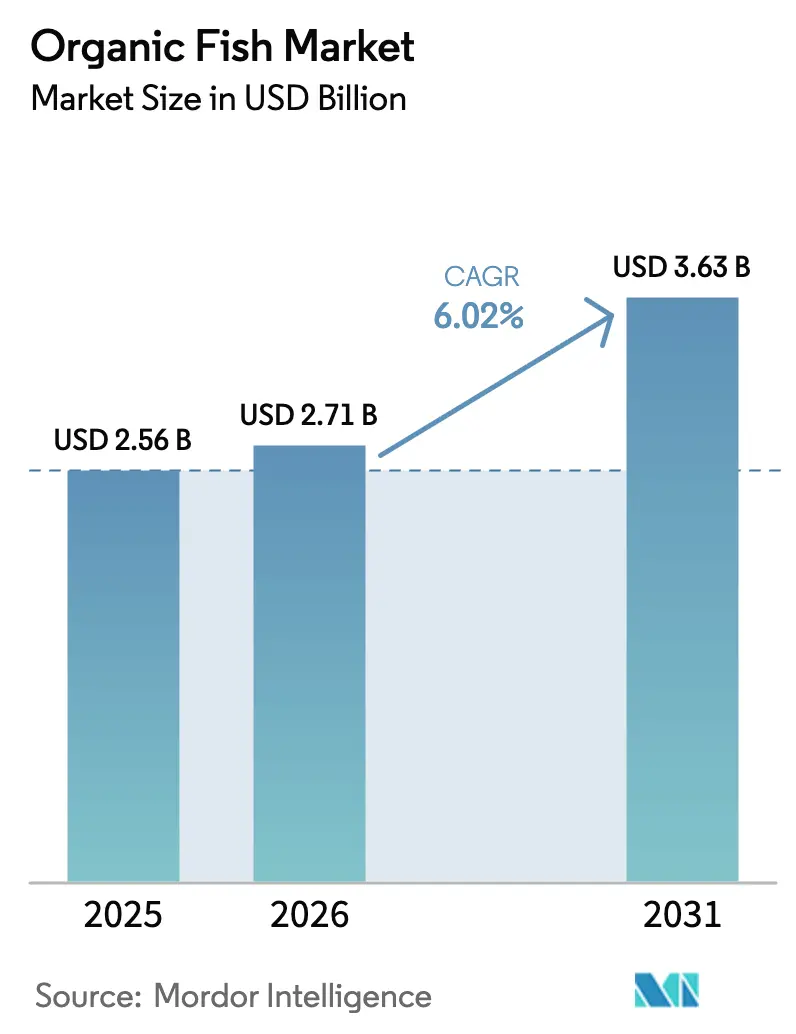

The organic fish market size is expected to grow from USD 2.56 billion in 2025 to USD 2.71 billion in 2026 and is forecast to reach USD 3.63 billion by 2031 at 6.02% CAGR over 2026-2031. Rising consumer consciousness about chemical residues in conventional aquaculture, broader alignment with sustainable diets, and the enforcement of tighter organic aquaculture regulations collectively underpin this growth. Demand momentum is amplified by educated millennial and Gen Z cohorts who routinely prioritize traceability, animal welfare, and climate metrics when purchasing seafood. Momentum is especially clear in regions that combine high disposable incomes with well-developed cold-chain networks, allowing retailers to stock a widening range of certified fresh, chilled, and processed products. Meanwhile, land-based recirculating aquaculture systems (RAS) and novel packaging platforms such as water-resistant DryPack are cutting distribution losses and broadening shelf life, reducing one of the main historical barriers to scale.

Key Report Takeaways

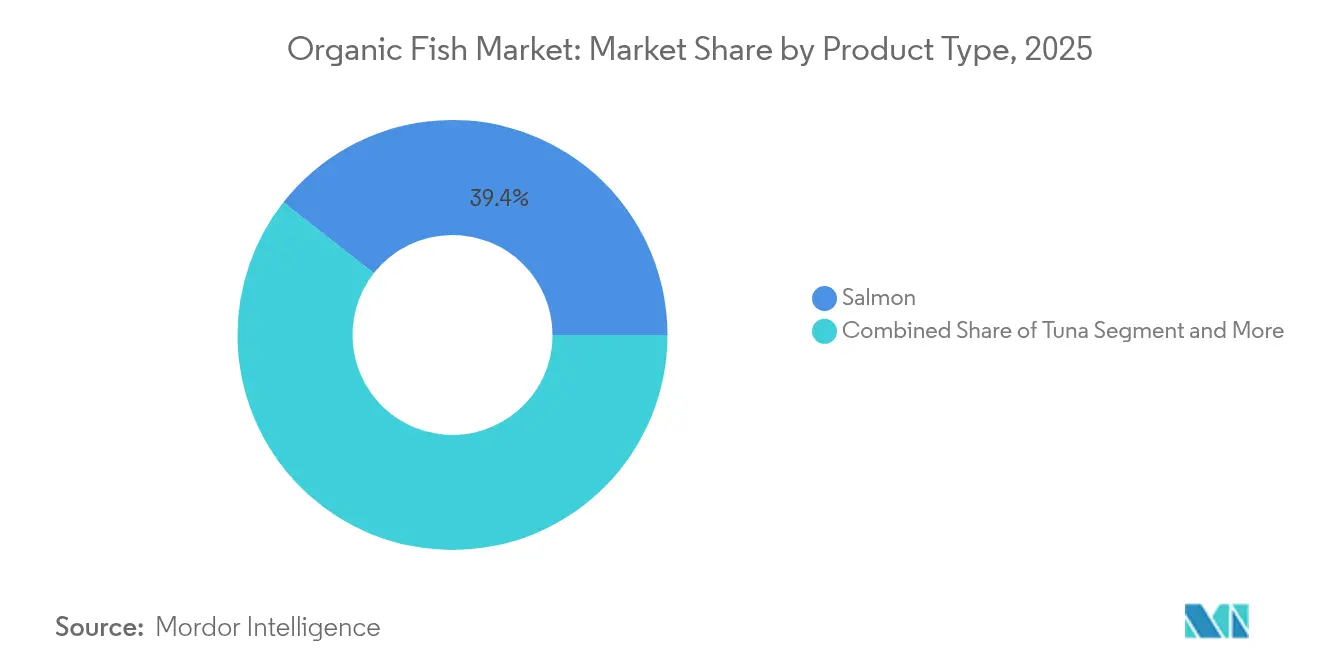

- By product type, salmon led with 39.42% of organic fish market share in 2025, while trout is forecast to grow fastest at an 8.30% CAGR through 2031.

- By form, fresh and chilled products captured 46.10% of revenue in 2025; processed variants are poised for a 7.19% CAGR to 2031.

- By price range, premium lines dominated with 59.48% of value in 2025, whereas value offerings are on track for a 7.08% CAGR.

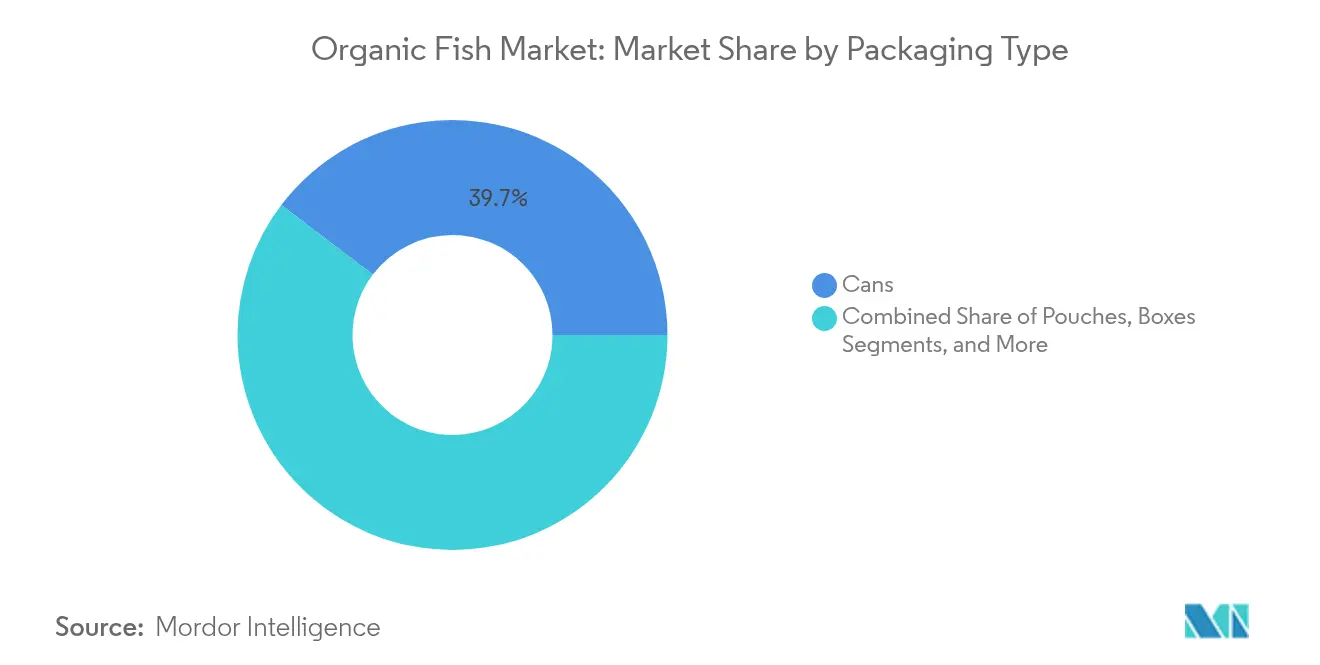

- By packaging, traditional cans retained 39.67% share in 2025; pouches represent the quickest-expanding format at an 8.39% CAGR.

- By distribution channel, the off-trade segment accounted for 68.22% of the organic fish market size in 2025, as the on-trade channel advances at a 7.10% CAGR.

- By geography, Europe held 36.12% of global revenue in 2025, while Asia-Pacific is expected to accelerate at a 7.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organic Fish Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Preference for Chemical-Free and Sustainably Farmed Fish | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Strict Government Regulations on Chemical Use | +0.9% | Europe and North America core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of Organic Certification Programs | +0.7% | Global, with emphasis on developing markets | Medium term (2-4 years) |

| Rising Disposable Income in Developed and Emerging Markets | +0.8% | Asia-Pacific core, spill-over to South America | Short term (≤ 2 years) |

| Increasing Availability Through Modern Retail and Online Channels | +0.6% | Global, with early gains in urban centers | Short term (≤ 2 years) |

| Growing Demand for Traceability and Transparency | +0.5% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Chemical-Free and Sustainably Farmed Fish Fuels Market Growth

The market is experiencing significant growth, primarily driven by increasing consumer demand for chemical-free and sustainably farmed fish. Consumers are becoming more conscious of the environmental and health impacts associated with conventional aquaculture practices. This shift in preference is fueled by growing awareness of the benefits of organic fish, which include the absence of synthetic chemicals, antibiotics, and genetically modified organisms (GMOs) in production. The rising trend of health-conscious eating and the increasing popularity of organic food products are also contributing to the expansion of the organic fish market. As consumers prioritize quality and sustainability, the demand for organic fish is expected to grow steadily during the forecast period. In addition to regulatory support, advancements in aquaculture technology are playing a crucial role in meeting the growing demand for organic fish. Innovations in water quality management, feed optimization, and disease prevention are enabling producers to maintain high standards of organic certification while improving yield efficiency. These technological developments are reducing production costs, making organic fish more accessible to a broader consumer base.

Strict Government Regulations on Chemical Use Encourage Organic Fish Farming Practices

Regulatory frameworks are tightening globally. The EU has established the world's strictest aquaculture standards through Organic Regulation 2018/848, requiring maximum stocking densities, organic feeds, and banning artificial hormones for induced spawning.[1]Source: European Commission, "Organic production and products", www.agriculture.ec.europa.eu The U.S. has launched a USD 300 million Organic Transition Initiative to support farmers transitioning to organic practices. Starting March 2024, the U.S. enforced stricter measures by requiring NOP Import Certificates for all organic shipments [2]Source: U.S. Department of Agriculture, "Organic Situation Report, 2025 Edition", www.ers.usda.gov. These regulatory changes increase compliance costs but also create market barriers that protect certified producers from low-quality competition. In the UK, the Soil Association completed an 18-month review of welfare and environmental practices in Scottish salmon farms. They warned that they might withdraw from the sector within a year if meaningful progress does not occur. China's organic aquaculture sector, which produces 85,000 tonnes annually, faces fragmentation due to inconsistent certification standards across provinces. This highlights the need for unified regulatory measures. As regulations converge globally, producers who meet the highest standards can seize opportunities, while those unable to adapt may face exclusion.

Expansion of Organic Certification Programs Improves Consumer Trust and Market Credibility

The expansion of organic certification programs is a significant driver in the market. These programs ensure that organic fish products meet stringent standards, including sustainable farming practices, chemical-free production, and ethical sourcing. By adhering to these certifications, producers can enhance transparency and build consumer trust. This trust is crucial as consumers increasingly prioritize health-conscious and environmentally friendly choices. Furthermore, the credibility provided by recognized certification bodies strengthens the market position of organic fish products, enabling producers to differentiate themselves in a competitive landscape. The growing awareness and demand for certified organic products are expected to further propel the organic fish market during the forecast period. Organic certification programs also play a pivotal role in addressing consumer concerns regarding food safety and quality. These certifications assure that the fish are raised in controlled environments, free from harmful chemicals, antibiotics, and synthetic additives. This assurance is particularly important as consumers become more informed about the potential health risks associated with conventionally farmed fish. Additionally, the certifications promote sustainable aquaculture practices, which align with the increasing consumer preference for environmentally responsible products. The emphasis on sustainability not only attracts eco-conscious consumers but also supports long-term resource conservation, further driving the market.

Rising Disposable Income in Developed and Emerging Markets Supports Premium Organic Fish Sales

As disposable incomes rise in emerging markets, particularly in the Asia-Pacific region, consumers are increasingly driving the expansion of the market for premium organic fish products. This growth is significantly broadening the consumer base, extending beyond the traditionally developed markets. Consumers in these regions are actively seeking healthier and environmentally friendly dietary options, showing a growing preference for sustainable and organic food products. Their willingness to invest in high-quality, premium offerings is further fueling this demand. In response to this trend, India's Department of Fisheries is implementing the Pradhan Mantri Matsya Sampada Yojana with ambitious goals to double fishers' income and boost fish production to 22 million metric tonnes by 2024-25 [3]Source: Government of India, Ministry of Fisheries, Animal Husbandry and Dairying, "Department of Fisheries", www.dof.gov.in. The initiative emphasizes sustainable aquaculture practices, encouraging the adoption of organic production methods to ensure long-term environmental sustainability and economic growth. By prioritizing these measures, the program actively addresses economic and ecological challenges, fostering a balanced and sustainable development of the fisheries market while enhancing the livelihoods of fishers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Costs Limit Affordability and Restrict Market Penetration | -1.4% | Global, most acute in developing markets | Medium term (2-4 years) |

| Longer Growth Cycles Affect Timely Market Supply | -0.8% | Global, particularly affecting seasonal demand | Short term (≤ 2 years) |

| Competition From Conventional Fish Products with Lower Prices | -1.1% | Global, strongest in price-sensitive markets | Long term (≥ 4 years) |

| Supply Chain Inefficiencies and Limited Cold Storage Infrastructure | -0.6% | Developing markets, rural distribution networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Costs of Organic Fish Limit Affordability and Restrict Market Penetration

Organic aquaculture production costs significantly exceed conventional methods due to expensive organic feed requirements, extended certification processes, and stringent monitoring protocols that limit economies of scale. Transitioning from conventional to organic aquaculture is complex and costly, with organic yields typically lower than conventional systems, potentially limiting contribution to global food security despite environmental advantages. Feed represents the largest production cost component in European fish farming, with organic feed requirements adding substantial expense premiums that smaller producers struggle to absorb. Certification costs create additional barriers, particularly for small-scale producers who may require group certification arrangements to achieve economic viability, with high certification expenses limiting market entry for emerging producers. The cost structure challenges are most pronounced in developing markets where consumer price sensitivity restricts premium product adoption. However, Norwegian case studies demonstrate that effective biological risk management in organic systems can offset some cost disadvantages through reduced mortality rates and improved feed conversion efficiency. Industry consolidation may emerge as a response to cost pressures, potentially favoring larger integrated producers over smaller independent operations.

Competition From Conventional Fish Products with Lower Prices Challenges Market Growth

Conventional aquaculture products consistently challenge the expansion of the organic fish market. This is especially true as conventional producers, benefiting from economies of scale, outpace their organic counterparts constrained by volume limitations. While consumers show a willingness to pay a premium for organic fish, their purchasing behavior often skews towards conventional products when price differences surpass perceived value thresholds. This dynamic introduces volatility for organic producers, making it difficult to maintain consistent growth. The Scottish salmon industry feels this pressure acutely. The potential removal of distinctions between organic and conventional salmon in geographical indications threatens to commoditize the market. Such a shift could disadvantage smaller organic producers who depend on premium positioning to differentiate their products and sustain profitability. Companies in this sector are intensifying efforts to enhance taste, texture, and affordability, positioning themselves as challengers to both conventional and organic fish products. These advancements in plant-based alternatives could further fragment the market and increase competition. Given this competitive landscape, organic producers must articulate their value propositions more clearly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Salmon Remains Dominant While Trout Accelerates Innovation

In 2025, salmon commands a dominant 39.42% market share, bolstered by the robust production infrastructure of Norway and Scotland. Meanwhile, trout is making waves as the fastest-growing segment, boasting an 8.30% CAGR through 2031. This surge is largely attributed to land-based recirculating aquaculture systems, which are adept at addressing pressing environmental concerns. Hima Seafood, at the forefront, operates the world's largest land-based trout farm in Norway. By harnessing advanced RAS technology, they not only cultivate trout but also produce organic fertilizer as a byproduct, showcasing scalable and sustainable production methods. Tuna, while carving out a premium niche in organic aquaculture, faces hurdles. Meanwhile, other species like sea bass, sea bream, and shellfish are diversifying the market, with China stepping up as a leader in producing a range of organic species, moving beyond the traditional salmon-centric focus.

Established supply chains and consumer familiarity tilt the competitive scales in favor of salmon. However, trout is reaping the rewards of technological advancements that not only mitigate environmental impacts but also slash production costs. Norwegian producers of organic salmon are proving that strategic differentiation can outpace the profitability of standard commodity production. One such company stands out, consistently reaping superior returns on sales, thanks to astute biological risk management. As conventional salmon farming grapples with regulatory scrutiny especially concerning sea lice management and environmental repercussions—organic producers find a golden opportunity. By showcasing their enhanced sustainability credentials, they can carve out a more significant market share.

By Form: Fresh Dominates While Processing Innovations Drive Growth

Fresh and chilled products command 46.10% market share in 2025, reflecting consumer preferences for minimally processed organic seafood, while processed products including smoked and ready-to-eat variants expand at 7.19% CAGR through 2031, driven by convenience demands and shelf-life extension technologies. High-pressure processing, modified atmosphere packaging, and smart packaging technologies enable organic fish processors to extend shelf life by up to 50% while maintaining organic integrity, addressing key distribution challenges. Frozen organic fish products serve as market entry vehicles for emerging producers, offering lower distribution costs and extended market reach compared to fresh products that require sophisticated cold chain infrastructure.

Processing innovation focuses on maintaining organic standards while improving convenience and shelf stability, with edible coatings derived from biopolymers emerging as sustainable preservation methods that enhance nutritional value. The form segmentation reflects broader consumer trends toward premium fresh products in developed markets and processed convenience options in emerging markets where cold chain infrastructure remains limited. Regulatory frameworks increasingly scrutinize processing aids and additives used in organic fish products, creating opportunities for companies that can develop clean-label processing technologies. Value-added processing represents a key differentiation strategy for organic producers seeking to capture higher margins while addressing diverse consumer preferences across geographic markets.

By Price Range: Premium Still Rules While Value Lines Extend Reach

In 2025, premium products account for 59.48% of the global fish market value. This dominance highlights the cost dynamics associated with organic aquaculture and the growing consumer preference for products with verified sustainability credentials. The premium segment's stronghold reflects the willingness of consumers to pay a higher price for quality and environmentally responsible practices, which are increasingly becoming key differentiators in the market. As sustainability continues to gain traction, the premium segment is expected to maintain its significant share in the market over the coming years. Additionally, the premium segment benefits from advancements in aquaculture technologies and certifications that ensure traceability and compliance with environmental standards, further solidifying its position in the market.

Meanwhile, value segments are experiencing faster growth, expanding at a 7.08% CAGR through 2031. This growth indicates ongoing efforts to democratize the market, making fish products more accessible to a broader consumer base. The rising demand for affordable options is driving innovation and efficiency in production processes, enabling companies to cater to cost-conscious consumers without compromising on quality. This trend suggests a shift in market dynamics, where both premium and value segments coexist to meet diverse consumer needs. Furthermore, the growth of the value segment is supported by increasing investments in supply chain optimization and the adoption of cost-effective farming practices, which help reduce production costs and enhance market penetration. As a result, the global fish market is evolving to balance premium offerings with affordable alternatives, ensuring sustained growth across all segments.

By Packaging: Sustainability Drives Pouch Innovation Leadership

In 2025, traditional cans hold a 39.67% market share in the global fish market. This dominance is attributed to their well-established supply chains and the ability to provide extended shelf life, which is crucial for preserving fish products. Traditional cans have long been a preferred choice for manufacturers and consumers alike, offering durability and reliability in maintaining product quality over time. Their widespread availability and compatibility with existing distribution networks further reinforce their strong position in the market. Additionally, the affordability of traditional cans compared to other packaging formats makes them a cost-effective solution for both producers and consumers, particularly in regions with high demand for canned fish products.

On the other hand, pouches are emerging as the fastest-growing packaging format in the global fish market, with a projected CAGR of 8.39% through 2031. This growth is driven by increasing sustainability initiatives and the rising demand for convenient packaging solutions among consumers. Pouches are lightweight, require less material, and are easier to transport, making them an environmentally friendly alternative to traditional packaging. Additionally, their resealable features and ease of use cater to modern consumer preferences, positioning them as a key driver of innovation in the fish packaging segment. The growing focus on reducing plastic waste and adopting eco-friendly materials further accelerates the adoption of pouches, as they align with global sustainability goals.

By Distribution Channel: Off-Trade Dominance Faces On-Trade Growth Challenge

In 2025, off-trade channels, which include supermarkets, hypermarkets, convenience stores, specialty stores, and online retail, dominate with a 68.22% market share. Meanwhile, on-trade segments, primarily restaurants and foodservice, are witnessing a robust growth at a 7.10% CAGR through 2031. This surge is largely attributed to the rising demand for traceable organic seafood in restaurants. Among off-trade channels, online retail stands out as the fastest-growing subsegment. It not only facilitates direct-to-consumer sales, allowing for higher profit margins, but also caters to the organic consumer's demand for detailed product information and traceability. Supermarkets and hypermarkets continue to lead the market, bolstered by their established cold chain infrastructure and ingrained consumer shopping habits. However, specialty stores are carving out a niche, offering premium positioning for high-value organic fish products.

The evolution of distribution channels underscores a shift in consumer behavior and a trend in the restaurant industry leaning towards sustainability and transparency in sourcing. Maine's seafood sector pinpoints enhanced access to markets and distribution networks as pivotal for growth. This is especially true in the Northeast and South Atlantic regions, where the appetite for organic seafood is on the rise. Restaurants are driving the on-trade growth, aiming to set themselves apart through sustainable sourcing. Organic fish products not only enhance their menu but also justify a premium pricing strategy. These channel dynamics highlight the enduring significance of traditional retail, while also spotlighting the burgeoning opportunities in foodservice and direct-to-consumer sales, both of which promise greater value for organic producers.

Geography Analysis

In 2025, Europe commands a dominant 36.12% share of the organic fish market, leveraging its robust certification infrastructure and a discerning consumer base that values sustainability. Norway and Ireland spearhead production in Europe. Norwegian companies highlight the lucrative nature of organic salmon farming, attributing their success to effective biological risk management. Conversely, Scottish producers face pressure from the Soil Association, which has issued a warning of withdrawal unless notable welfare improvements are implemented within a year. Germany, the UK, and France emerge as key consumption centers, while Nordic nations, with their favorable aquaculture conditions, dominate production. In a testament to the region's trade tensions, European processors unite to challenge Norway's export restrictions on production-grade salmon, a move poised to reshape regional supply chains.

Asia-Pacific is set to emerge as the fastest-growing region, forecasting a 7.90% CAGR through 2031. This growth is fueled by rising disposable incomes, heightened awareness of organic food benefits, and a surge in aquaculture activities. Leading this momentum are countries like China, India, and Vietnam, bolstered by government initiatives championing sustainable aquaculture. The region's burgeoning middle class, willing to invest in organic and sustainably sourced fish, further propels this growth. Yet, challenges loom with inadequate certification frameworks and a nascent cold chain infrastructure, potentially curbing the market's expansive potential.

North America and the Middle East & Africa are also pivotal players in the global organic fish arena. North America, with its pronounced focus on sustainability and health, sees the U.S. and Canada as its primary markets. The region's edge is amplified by advanced aquaculture technologies and a robust certification system. Meanwhile, the Middle East & Africa, buoyed by urbanization and a surging appetite for organic products, sees the UAE and South Africa emerging as key players. These nations benefit from escalating investments in aquaculture and enhancements in supply chain infrastructure, though they grapple with challenges like high production costs and a lack of consumer awareness.

Competitive Landscape

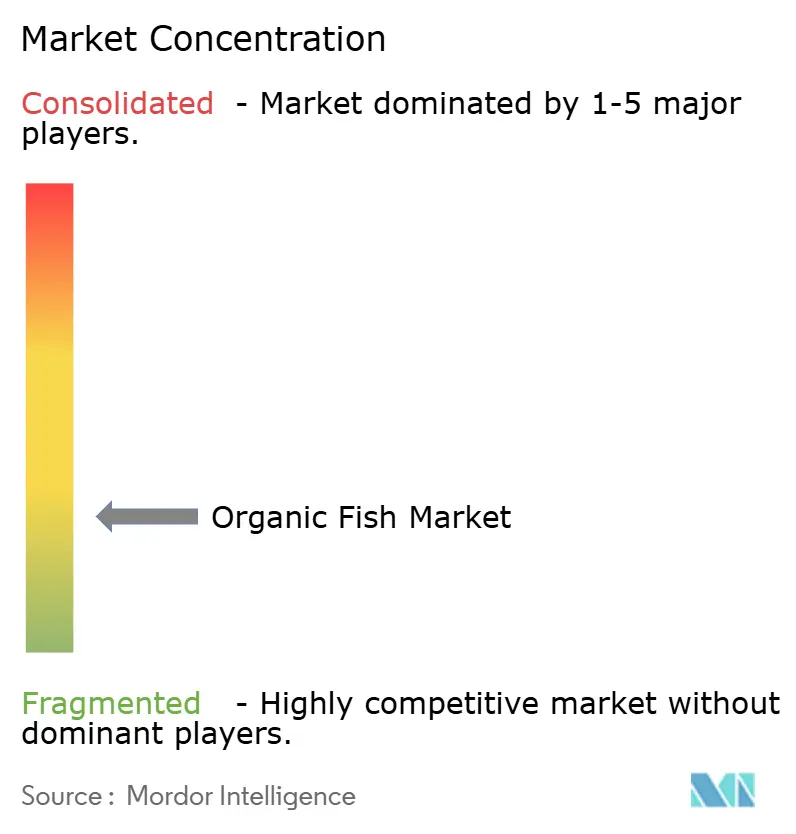

The organic fish market is characterized by fragmented competition, reflected in a low concentration score of 3 out of 10. This fragmented nature creates significant opportunities for both well-established aquaculture companies and emerging technology-driven disruptors to gain market share through innovative differentiation strategies. Major players such as Mowi ASA, Loch Duart Ltd., Leroy Seafood Group ASA, and SalMar ASA dominate the market by leveraging their extensive expertise in salmon farming and their well-integrated value chains. These companies benefit from economies of scale and robust operational frameworks, enabling them to maintain a competitive edge. On the other hand, smaller, specialized producers like Cooke Scotland and Glenarm Organic Salmon focus on carving out a niche by emphasizing premium organic positioning.

A key strategic trend in the market is the emphasis on vertical integration. Companies are increasingly controlling every stage of the value chain, from feed production and farming operations to processing and distribution. This approach ensures compliance with organic standards across the supply chain, enhances traceability, and reduces dependency on external suppliers. Vertical integration also allows companies to maintain consistent product quality and optimize cost structures, further strengthening their market position. Technological advancements play a pivotal role in shaping the competitive landscape. Companies are adopting innovative solutions such as recirculating aquaculture systems (RAS), which enable efficient water usage and minimize environmental impact.

Furthermore, the market dynamics are influenced by evolving consumer preferences, regulatory frameworks, and environmental challenges. The rising awareness of health benefits associated with organic fish consumption and the growing demand for sustainably sourced seafood are driving market growth. Companies that can effectively align their strategies with these trends are well-positioned to capture a larger share of the market. The competitive landscape is expected to remain dynamic, with both established players and new entrants striving to innovate and differentiate themselves in this rapidly evolving market.

Organic Fish Industry Leaders

-

Mowi ASA

-

Loch Duart Ltd.

-

Leroy Seafood Group ASA

-

SalMar ASA

-

Glenarm Organic Salmon Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Hima Seafood has started building its RAS trout facility in Rjukan, Norway. The company asserts that this facility will be the ‘world’s largest land-based Recycling Aquaculture System trout facility’, with a weekly output of 150 tonnes of head-on-gutted (“HOG”) trout, totaling approximately 8,000 tonnes annually.

- August 2023: Goldman Sachs has acquired a controlling 72 percent stake in aquaculture services firm Frøy, completing the transaction valued at approximately NOK 6.6 billion (USD 630 million). This acquisition highlights Goldman Sachs' strategic interest in the aquaculture sector, reflecting its commitment to expanding its portfolio in this growing industry.

- March 2023: Natural Grocers, the largest family-operated organic and natural grocery retailer in the U.S., has unveiled five new canned seafood varieties under its premium house brand, Natural Grocers Brand Products. The new offerings feature Albacore and Skipjack Tuna, Wild Pink Salmon, and two types of Wild Sardines.

Global Organic Fish Market Report Scope

Organic fish is produced by organic aquaculture methods. It is grown without chemicals, such as human-made pesticides, antibiotics, fertilizers, and genetically modified organisms (GMOs).

The organic fish market is segmented by type, form, distribution channel, and geography. Based on the type, the market is segmented into salmon, tuna, and others. Based on the form, the market is segmented into fresh/chilled, frozen/canned, and processed. Based on the distribution channel, the market is segmented into on-trade and off-trade. Off-trade is further segmented into convenience/grocery stores and online retail stores. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East&Africa).

The report offers market size and forecasts in value (USD million) for the above segments.

| Salmon |

| Tuna |

| Trout |

| Other Species |

| Fresh/Chilled |

| Frozen |

| Processed (Smoked, Ready-to-Eat) |

| Premium |

| Value |

| Cans |

| Pouches |

| Boxes |

| Others |

| Off-Trade | Supermarkets & Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| On-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Salmon | |

| Tuna | ||

| Trout | ||

| Other Species | ||

| By Form | Fresh/Chilled | |

| Frozen | ||

| Processed (Smoked, Ready-to-Eat) | ||

| By Price Range | Premium | |

| Value | ||

| By Packaging | Cans | |

| Pouches | ||

| Boxes | ||

| Others | ||

| By Distribution Channel | Off-Trade | Supermarkets & Hypermarkets |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the organic fish market?

The organic fish market size reached USD 2.71 billion in 2026, and forecasts point to USD 3.63 billion by 2031 due to a 6.02% CAGR.

Which region leads global demand for organic fish?

Europe holds the top position with 36.12% of 2025 revenue, benefiting from mature certification systems and consumers who readily pay premiums for traceable seafood.

What species dominates organic fish sales?

Salmon accounted for 39.42% organic fish market share in 2025, supported by established Nordic farming infrastructure.

Why are pouches the fastest-growing packaging format?

Pouches deliver 81% freight-space savings and full recyclability, pushing their adoption pace to an 8.39% CAGR through 2031.

Page last updated on: