Canned Tuna Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

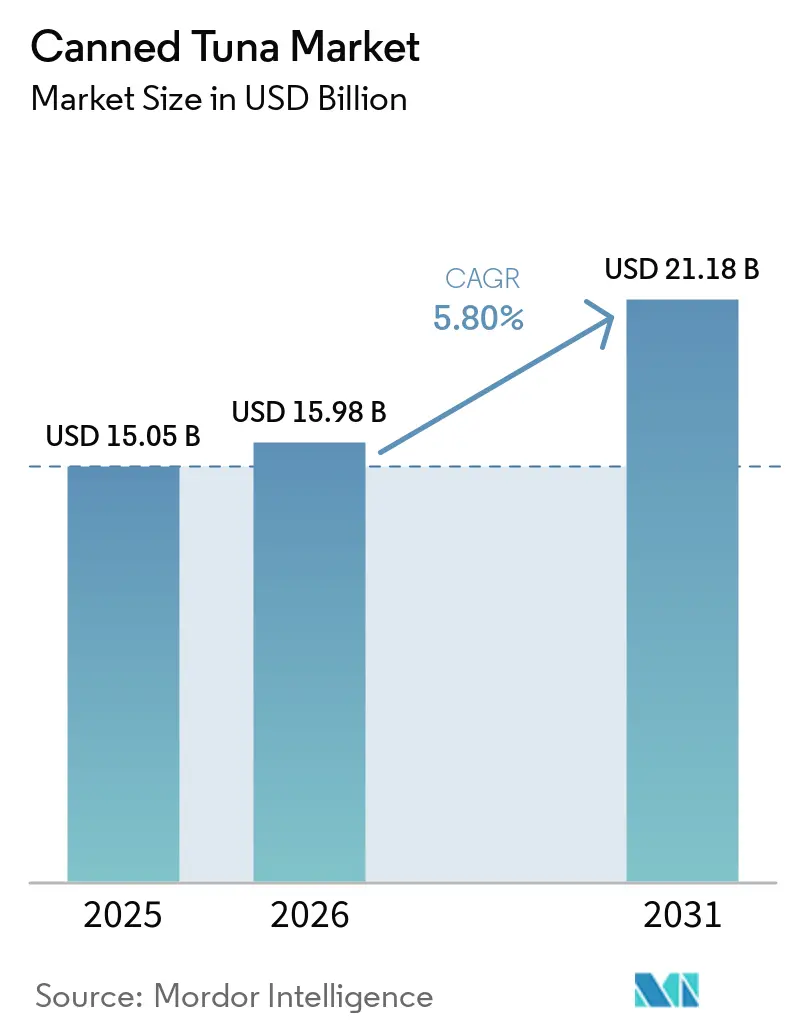

| Market Size (2026) | USD 15.98 Billion |

| Market Size (2031) | USD 21.18 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

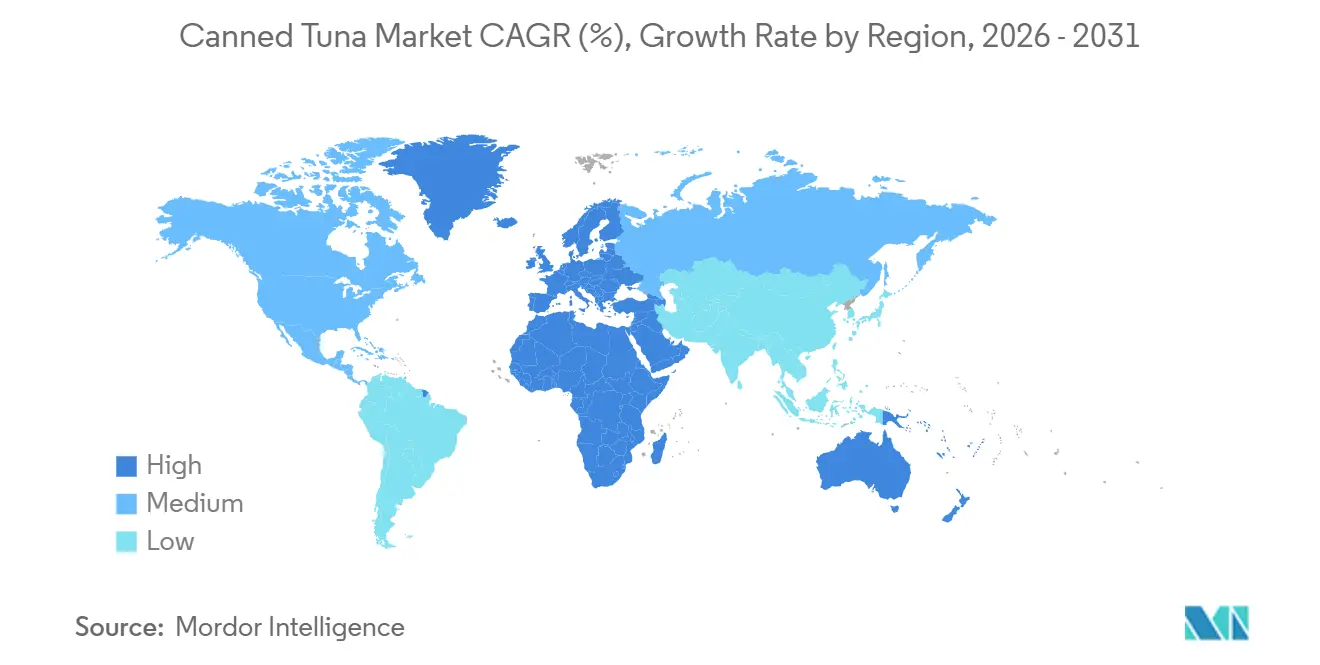

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

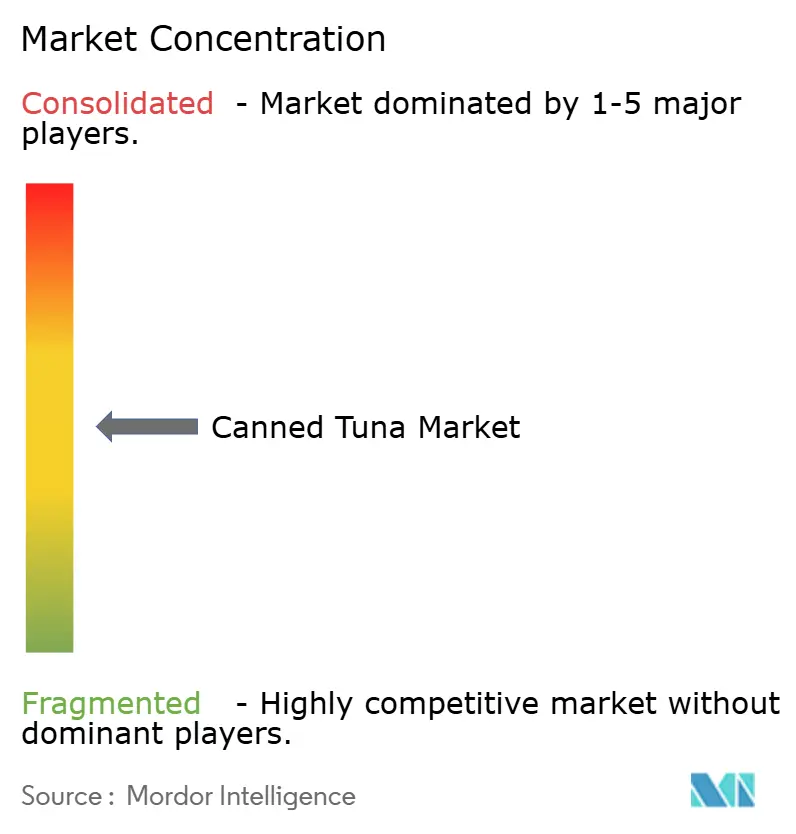

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canned Tuna Market Analysis by Mordor Intelligence

The canned tuna market size is projected to be USD 15.05 billion in 2025, USD 15.98 billion in 2026, and reach USD 21.18 billion by 2031, growing at a CAGR of 5.8% from 2026 to 2031. Demand continues to rise as price-sensitive shoppers seek shelf-stable protein, food-service buyers rebuild volume after the pandemic, and processors invest in flexible packaging that cuts steel and secondary-material use. Light tuna remains the volume anchor because skipjack’s low mercury content aligns with FDA “Best Choice” guidance, while white-tuna premiumization, MSC certification, and pole-and-line sourcing spur higher-margin growth in specialty retail. Europe dominates volumes, yet the Middle East and Africa now deliver the fastest gains, as Oman’s new 100-million-can plant exemplifies a pivot from reliance on imports to local value capture. E-commerce is amplifying repeat purchases through subscription bundles, and vertically integrated heavyweights keep margins stable despite skipjack price swings by locking in long-term contracts with certified fisheries.

Key Report Takeaways

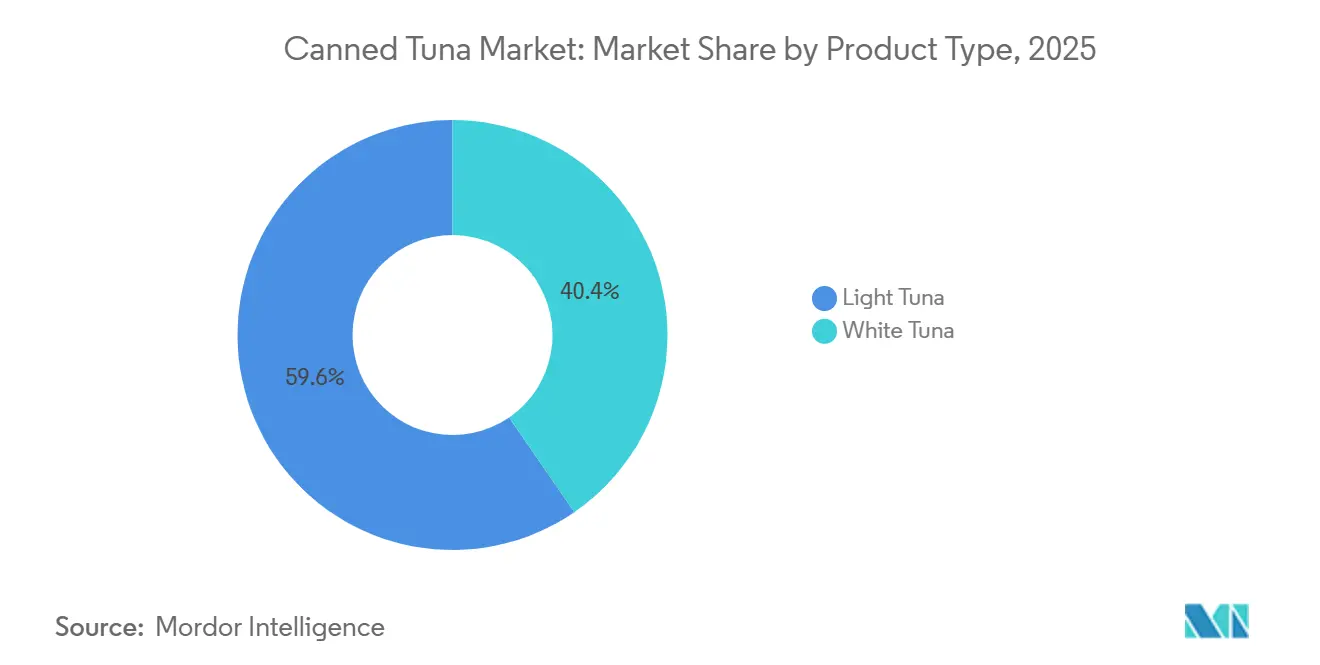

- By product type, Light tuna led with 59.59% of the canned tuna market share in 2025, while white tuna is forecasted to advance at a 6.48% CAGR through 2031.

- By flavor, Unflavored offerings held 85.69% of the 2025 base, while flavored varieties are expected to expand at a 6.97% CAGR through 2031.

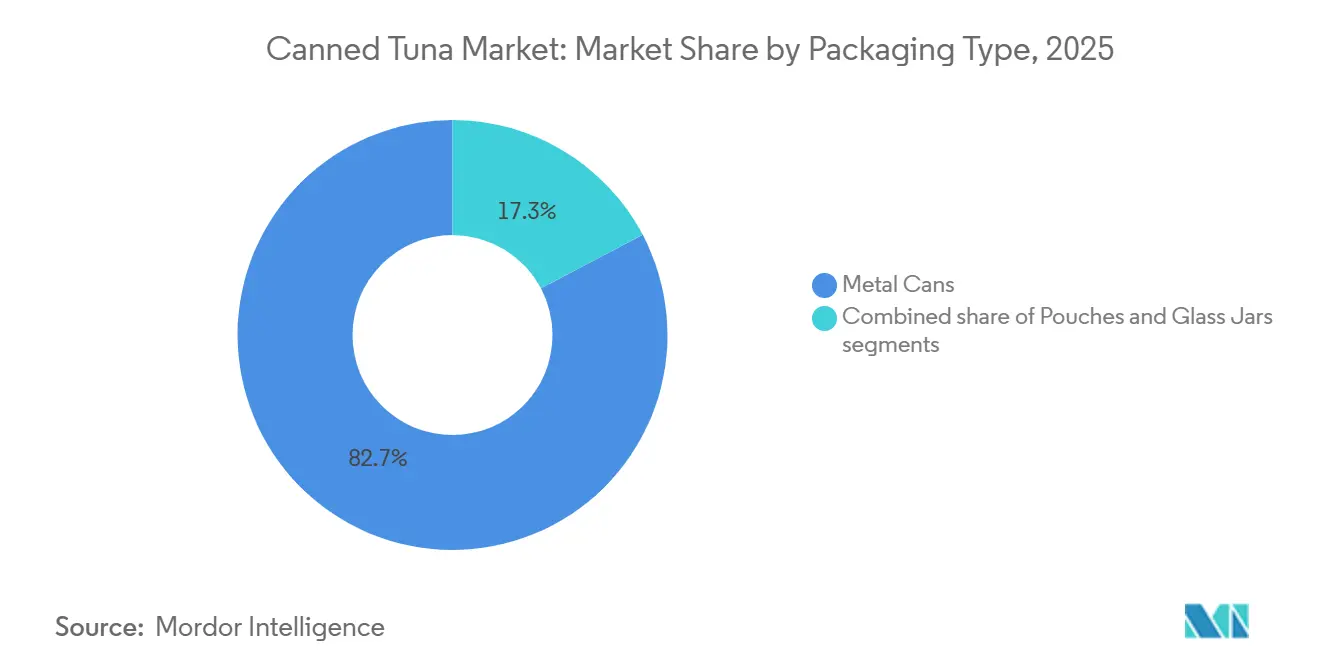

- By packaging, Metal cans accounted for 82.72% of 2025 revenue, whereas pouches are projected to post a 6.70% CAGR between 2026 and 2031.

- By distribution channel, Off-trade captured 60.72% in 2025, yet on-trade is anticipated to grow at a 7.20% CAGR through 2031 as food-service recovery accelerates.

- By geography, Europe commanded a 35.40% share in 2025, while the Middle East and Africa region is predicted to lead growth with a 6.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Canned Tuna Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience and ready-to-eat appeal | +1.2% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Product innovation and flavored varieties | +0.8% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Expansion of e-commerce and online retail | +0.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Technological advancements in processing and packaging | +0.5% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| High protein and nutritional value | +0.7% | Global, particularly health-conscious demographics | Long term (≥ 4 years) |

| Long shelf life and pantry staple status | +0.4% | Global, enhanced during supply chain disruptions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Convenience and ready-to-eat appeal

The convenience and ready-to-eat appeal of canned tuna is a major driver in the market, as consumers increasingly seek quick, nutritious meal solutions that fit busy lifestyles. Canned tuna requires no preparation, can be stored for long periods, and is easily incorporated into salads, sandwiches, and various dishes, making it a staple in both household and foodservice settings. Its portability and minimal need for refrigeration further enhance its attractiveness for on-the-go consumption, lunchboxes, and emergency food supplies. The rise in single-person households and urban living amplifies demand for ready-to-eat protein sources, while health-conscious consumers value canned tuna for its lean protein and omega-3 content. Additionally, manufacturers are innovating with flavored and pre-mixed options to cater to evolving tastes and convenience expectations. This trend is particularly evident in regions experiencing rapid urbanization and changing dietary habits. Overall, the convenience factor not only sustains steady demand but also encourages market players to diversify their product offerings and packaging formats.

Product innovation and flavored varieties

Flavored tuna varieties are transforming the market landscape by appealing to younger demographics and expanding consumption occasions beyond traditional uses. The segment's robust 7.12% CAGR growth highlights the effectiveness of differentiation strategies that not only command premium pricing but also address consumer fatigue with plain tuna products. Companies like Thai Union are driving innovation by integrating sustainability into their operations, with 85% of their tuna sourced from MSC-certified fisheries. This approach demonstrates that innovation extends beyond flavor profiles to include ethical and responsible sourcing practices, which are increasingly valued by consumers. Additionally, the FDA's proposed amendments to canned tuna standards in August 2023, allowing the broader use of flavorings and spices, provide a regulatory framework that supports continued innovation[1]Federal Register, "Fish and Shellfish; Canned Tuna Standard of Identity and Standard of Fill of Container", www.federalregister.gov. This flexibility empowers manufacturers to explore ethnic flavors and fusion concepts, catering to the evolving tastes of a diverse consumer base and further enhancing the segment's growth potential.

Expansion of e-commerce and online retail

Digital commerce channels are significantly altering canned tuna distribution patterns, a shift that accelerated during the pandemic as consumers increasingly adopted online grocery shopping. The rise of e-commerce has proven particularly beneficial for canned tuna due to its long shelf life and standardized packaging, which minimize shipping challenges compared to fresh seafood. Recognizing canned tuna's potential to drive online traffic, major grocery chains have introduced targeted seafood promotions. For instance, in 2025, Natural Grocers offered free canned tuna to loyalty members during their Resolution Reset Week, highlighting the strategic importance of such products in online retail strategies. Additionally, online platforms have created opportunities for premium and specialty tuna brands to engage directly with consumers, eliminating traditional retail markups and enhancing profit margins. This direct-to-consumer model also allows brands to build stronger customer relationships and cater to niche market demands more effectively.

Technological advancements in processing and packaging

Innovations in processing and packaging are revolutionizing the seafood industry by extending product shelf life and enhancing consumer convenience. Flexible pouches have emerged as a disruptive packaging format, replacing traditional metal cans to meet consumer demands for easier opening, improved portion control, and reduced storage space. This shift reflects a broader trend toward convenience and functionality in packaging. For instance, Bumble Bee's adoption of recyclable paperboard multipacks, producing 26 million units annually, highlights how packaging innovation can simultaneously address sustainability goals and improve operational efficiency. Additionally, active packaging technologies utilizing biodegradable materials, such as sago starch and chitosan, are being developed to extend tuna shelf life while minimizing environmental impact, aligning with the growing focus on eco-friendly solutions. Furthermore, Thai Union's significant investment of USD 172 million in 2023 to establish new facilities for protein hydrolysate and collagen peptides underscores the industry's move toward value-added products, showcasing how technological advancements are unlocking opportunities beyond traditional canned tuna offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability and overfishing concerns | -0.9% | Global, particularly Europe and North America | Long term (≥ 4 years) |

| Rise of plant-based canned-seafood alternatives | -0.3% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Supply chain and price volatility | -0.7% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Mercury-level concerns among pregnant and young consumers | -0.5% | Global, concentrated in health-conscious demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability and overfishing concerns

As consumer awareness of overfishing's impacts grows, the canned tuna industry grapples with the pressing challenge of environmental sustainability. The Western Central Pacific Ocean, responsible for about half of the global tuna catch, risks losing certification for its 33 MSC-certified tuna fisheries unless harvest control rules are established. In response to sustainability pressures, ICCAT introduced new measures for tropical tuna and management procedures for skipjack tuna in November 2024, yet challenges in implementation persist[2]Marine Stewardship Council, "Why Western Central Pacific Ocean Tuna Fisheries' Certification is Under Threat", www.msc.org. Companies like Pacifical are leading the charge, employing Ethereum-based verification through blockchain systems to trace over 200 million consumer units each year. This heightened consumer awareness has led to a willingness to pay premiums for sustainable products, creating lucrative opportunities for certified brands while intensifying pressure on those that remain non-compliant.

Rise of plant-based canned-seafood alternatives

Plant-based seafood alternatives are steadily gaining traction as a competitor to traditional canned tuna, fueled by increasing demand from environmentally conscious consumers and those with dietary restrictions. Thai Union's EUR 13 million investment in Algama, a company specializing in algae-based seafood products such as canned tuna analogs, underscores the industry's growing focus on the alternative protein market. Furthermore, the development of cell-based tuna directly addresses pressing environmental and animal welfare concerns while offering mercury-free options, which are particularly appealing to health-conscious consumers. Despite these advancements, the plant-based segment continues to face significant challenges in replicating the texture and taste of conventional seafood. However, sustained innovation and technological progress are expected to enhance product quality, enabling this segment to secure a larger share of the market. At the same time, the evolving regulatory landscape for alternative proteins introduces uncertainties, which could shape competitive dynamics and market growth in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Light Tuna Dominance vs White Tuna Premium Growth

In 2025, light tuna commands a dominant 59.59% market share, thanks to its cost-effectiveness and versatility. It's a staple, from basic meal prep to foodservice operations, where consistent and affordable protein sources are paramount. The segment's stability is bolstered by the healthy stock status of skipjack tuna, which constitutes 60% of the global tuna catch and enjoys effective management in key fishing regions. While yellowfin tuna adds diversity to light tuna products, it grapples with regional challenges in the Indian Ocean, unlike its more stable Pacific counterparts. The FDA's mercury monitoring programs ensure safety for light tuna products, which, due to the smaller size of skipjack compared to albacore species, typically boast lower mercury levels. This market dominance underscores a clear consumer preference: affordable protein options that seamlessly blend with various ingredients and seasonings.

White tuna is on a rapid ascent, boasting a 6.48% CAGR through 2031. This surge is attributed to savvy premium positioning strategies that play on consumer perceptions of its superior quality and taste over light tuna varieties. The price gap between white and light tuna presents processors with a lucrative margin expansion opportunity, especially in developed markets where consumers' disposable income leans towards higher-value purchases. Albacore tuna, the star of white tuna products, enjoys relatively stable stock conditions, ensuring a steady supply that bolsters its premium market stance. This growth trajectory signals a shift in consumer preferences, with health-conscious buyers ready to pay a premium for perceived quality. Furthermore, white tuna's premium status is amplified by its ties to traditional albacore fishing and artisanal processing methods, resonating with quality-centric consumers.

By Flavor: Traditional Unflavored Leadership vs Innovation-Driven Growth

In 2025, unflavored tuna commands a dominant 85.69% market share, underscoring its adaptability in cooking and the tendency of budget-conscious consumers to opt for basic products that can be tailored to personal tastes at home. This segment's robust position is attributed to its wide-ranging use, from classic tuna salads to modern grain bowls and global culinary adaptations. Unflavored products enjoy reduced production costs and streamlined supply chain management, allowing for competitive pricing that resonates with both budget-minded consumers and bulk buyers in the foodservice sector. The FDA's proposed updates to canned tuna standards aim to uphold product integrity while granting manufacturers leeway in basic formulations. Unflavored tuna's market supremacy is further bolstered by its status as a pantry essential, delivering dependable protein without flavor limitations that could restrict its culinary applications.

Flavored tuna varieties are on a growth trajectory, boasting a 6.97% CAGR. This surge is fueled by effective product differentiation strategies that broaden consumption occasions and draw in younger consumers in search of convenient and flavorful meal options. The uptick in this segment mirrors a wider industry shift towards convenience and diverse flavors. Manufacturers are channeling investments into research and development, crafting products that resonate with varied taste preferences and global culinary trends. There's a notable emphasis on ethnic and fusion flavors, with companies tapping into global taste movements to produce unique offerings that fetch premium prices compared to traditional unflavored varieties. Additionally, the flavored segment's rise is amplified by social media campaigns that highlight innovative uses for seasoned tuna, boosting visibility among younger audiences who prioritize convenience and flavor diversity.

By Packaging Type: Metal Can Tradition vs Pouch Innovation

In 2025, metal cans command a dominant 82.72% market share, a testament to decades of consumer trust and a well-honed supply chain. These cylindrical packages not only excel in product protection but also ensure shelf stability. Their longstanding reputation for preserving product quality over time is bolstered by a robust recycling infrastructure, addressing sustainability goals amidst concerns over metal production's environmental footprint. Furthermore, metal cans leverage economies of scale in both production and distribution, allowing for cost-effective packaging that supports competitive pricing across all market segments. Their inherent durability safeguards products during transit and storage, minimizing losses and upholding the quality standards synonymous with canned tuna. Additionally, metal cans boast enhanced barrier properties, shielding contents from light, oxygen, and moisture, thus preserving product integrity throughout distribution.

Pouches are on a rapid ascent, growing at a 6.70% CAGR, fueled by consumer desires for easier access, precise portion control, and compact storage. This shift in packaging mirrors a broader trend towards convenience, with pouches not only being portable for on-the-go consumption but also eliminating the need for can openers, which aren't always accessible. Bumble Bee's pivot to recyclable paperboard multipacks, churning out 26 million units yearly, underscores how packaging innovations can tackle sustainability while boosting operational efficiency. Pouches also shine in product differentiation, thanks to enhanced graphics and shelf presentation, bolstering premium positioning and brand visibility in competitive retail spaces. Moreover, advancements in active packaging, utilizing biodegradable materials like sago starch and chitosan, are being explored to prolong tuna's shelf life while minimizing environmental footprints.

By Distribution Channel: Off-Trade Dominance vs On-Trade Acceleration

In 2025, the off-trade channel secures a commanding 60.72% market share, underscoring canned tuna's entrenched position in retail grocery settings. Supermarkets and hypermarkets lead this channel, leveraging bulk purchasing and promotional strategies for competitive pricing. Notably, Spain's processing facilities act as pivotal distribution hubs, catering to the expansive European market. Online retail stores within the off-trade are witnessing a surge, propelled by rising e-commerce penetration. Major grocery chains are capitalizing on this trend, with Natural Grocers, for instance, enticing loyalty members with complimentary canned tuna during promotional events. The UAE's canned food market, expanding at an annual rate of 5-10%, sees major hypermarkets like Lulu and Carrefour playing a pivotal role in distribution. This underscores how concentrated retail efforts can bolster market growth in emerging regions. Furthermore, the off-trade channel thrives on canned tuna's status as a pantry staple, prompting consumers to buy in bulk and build their inventories.

The on-trade channel is witnessing a robust growth spurt, clocking in at an impressive 7.20% CAGR. This surge signals a notable shift in foodservice dynamics, with restaurants and institutional operators increasingly turning to canned tuna. This trend mirrors a broader foodservice movement, favoring convenience ingredients that ensure consistent quality, precise portion control, and bolster menu innovation and operational efficiency. A case in point is Bumble Bee's Quick Catch Tuna Bowls, which debuted as ready-to-eat meals boasting 12-15 grams of protein, suitable for hot or cold consumption. Their introduction spurred a remarkable 21.5% growth in the category. The channel's expansion is further fueled by canned tuna's adaptability, gracing everything from traditional sandwiches to modern grain bowls and salads, all of which resonate with health-conscious diners. Highlighting the trend, Chicken of the Sea is set to launch its 'No Drain Tuna' in July 2025, eyeing projected sales of a whopping USD 86.4 million, a testament to the industry's focus on foodservice convenience.

Geography Analysis

In 2025, Europe remains the leading market for canned tuna, holding a 35.40% market share. This dominance is primarily attributed to Spain's role as the region's processing powerhouse, accounting for 70% of Europe's canned tuna production. Spain's advanced processing capabilities and well-established distribution networks enable efficient access to broader European markets. Additionally, strong consumer acceptance in Southern Europe further reinforces the region's leadership. The market's growth is increasingly driven by the rising demand for premium products and a growing focus on sustainability in purchasing decisions. Germany, Italy, and France are key consumption markets, collectively importing canned tuna worth over USD 1.5 billion annually. Despite the trade disruptions caused by Brexit, the UK continues to exhibit strong consumption levels. The European market's emphasis on MSC certification provides a significant competitive advantage for sustainable brands, as environmentally conscious consumers are willing to pay a premium for certified products that align with their values.

The Middle East and Africa region is experiencing robust growth, with a projected CAGR of 6.58% through 2031. This growth is supported by rising disposable incomes, rapid urbanization, and an increasing shift toward Western dietary habits. The UAE leads the region in canned tuna consumption, significantly exceeding the global average. Saudi Arabia and Egypt are emerging as critical growth markets, driven by government-led initiatives focused on food security and aquaculture development. The region's young and expanding middle-class population further supports market expansion. However, economic instability and geopolitical tensions present periodic challenges. Import-dependent markets like the UAE benefit from low tariffs that facilitate inter-regional trade, although the region's limited local processing capacity remains a constraint on growth.

Asia-Pacific markets exhibit diverse growth trajectories, shaped by varying economic conditions and consumer preferences across the region. Japan's food processing industry faces significant challenges due to the weak yen, which has increased import costs. Despite a broader industry decline, the canned and bottled food segment remained stable at USD 1.24 billion in 2023, reflecting steady demand[3]United States Department of Agriculture, "Report Name: Food Processing Ingredients Annual", www.apps.fas.usda.gov. Vietnam has emerged as the second-largest tuna supplier to the US market, although the implementation of new regulations under Decree No. 37/2024/ND-CP, which mandate minimum catch sizes, has created export challenges. The region's growth outlook remains optimistic, supported by the expansion of middle-class populations and increasing protein consumption. However, supply chain disruptions and evolving regulatory frameworks continue to introduce volatility, impacting the overall market dynamics.

Competitive Landscape

The canned tuna market is moderately concentrated, with a few major players holding significant market shares alongside several regional and private-label brands. Leading companies benefit from strong supply chain networks, established brand loyalty, and economies of scale. Prominent companies in the market include Thai Union Group PCL, Dongwon Group, Century Pacific Group, Inc., Bolton Group, among others. However, smaller players continue to compete by offering niche products, sustainable sourcing, and competitive pricing. This structure maintains a balance between market control and healthy competition across regions.

Technology adoption has become a critical factor in gaining a competitive advantage. Leading players are implementing blockchain-based traceability systems and advanced packaging technologies to enhance product appeal and operational efficiency. For instance, Taiwan's tuna industry has adopted CCTV and blockchain technology on fishing vessels, addressing labor practice concerns while improving supply chain transparency. Such advancements highlight the growing importance of technology in ensuring ethical practices and operational improvements.

Opportunities for growth exist in premium product positioning and the development of alternative protein sources. Thai Union's EUR 13 million investment in algae-based seafood alternatives reflects the industry's acknowledgment of shifting consumer preferences and emerging trends. Regional dynamics also influence competitive intensity, with European markets emphasizing sustainability credentials, while price competition remains a dominant factor in developing markets. Additionally, emerging disruptors, such as plant-based alternative producers and direct-to-consumer brands leveraging e-commerce platforms, are reshaping the market by bypassing traditional retail channels and offering innovative solutions to meet evolving consumer demands.

Canned Tuna Industry Leaders

-

Thai Union Group PCL

-

Dongwon Group

-

Bolton Group

-

Bumble Bee Foods

-

Century Pacific Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: UK-headquartered canned food firm Princes Group announced to expand its tinned fish portfolio with two new premium tuna-flavored products. The two flavors include olive oil with lemon and olive oil with sweet chilli.

- February 2025: EROSKI has launched its first own-brand canned light tuna with Marine Stewardship Council (MSC) sustainable fishing certification on the Spanish market. According to the brand, this canned light tuna in olive oil, under the blue 'MSC' seal, is now available throughout its commercial network and in its online supermarket.

- January 2025: The Maldives Industrial Fisheries Company (MIFCO) has introduced a new 140-gram canned tuna product to the market, targeting small households and aiming to reduce food wastage. According to the company, the new product is 40 grams lighter than MIFCO's previous smallest offering of 180 grams, providing a more economical option for consumers.

Global Canned Tuna Market Report Scope

Canned tuna is a shelf-stable food product consisting of the processed flesh of specific tuna species that has been cooked, sealed in hermetically sealed containers (usually metal cans, glass jars, or vacuum-sealed pouches), and heat-sterilized to prevent spoilage. The canned tuna market is segmented by product type, flavor, packaging type, distribution channel, and geography. By product type, the market is segmented into White Tuna and Light Tuna. By flavor, the market is segmented into flavored and unflavored. By packaging Type, the market is segmented into metal cans, pouches, and glass jars. By distribution Channel, the market is segmented into on-trade and off-trade. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| White Tuna |

| Light Tuna |

| Flavored |

| Unflavored |

| Metal Cans |

| Pouches |

| Glass Jars |

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Specialty Stores | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | White Tuna | |

| Light Tuna | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Packaging Type | Metal Cans | |

| Pouches | ||

| Glass Jars | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Specialty Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the canned tuna market in 2026?

The canned tuna market size is USD 15.98 billion in 2026 with a projected 5.80% CAGR to 2031.

Which region leads canned tuna consumption?

Europe leads with 35.40% share, supported by Spain’s processing dominance and high consumer acceptance.

What is driving growth in the Middle East and Africa?

Rising disposable incomes, Western dietary adoption, and high seafood import reliance propel a 6.58% CAGR in the region.

Why are pouches gaining popularity over cans?

Pouches offer easier opening, lighter weight, and portion control, driving a 6.70% CAGR in this packaging segment.

Page last updated on: