Frozen Meat And Fish Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 54.63 Billion |

| Market Size (2031) | USD 70.97 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

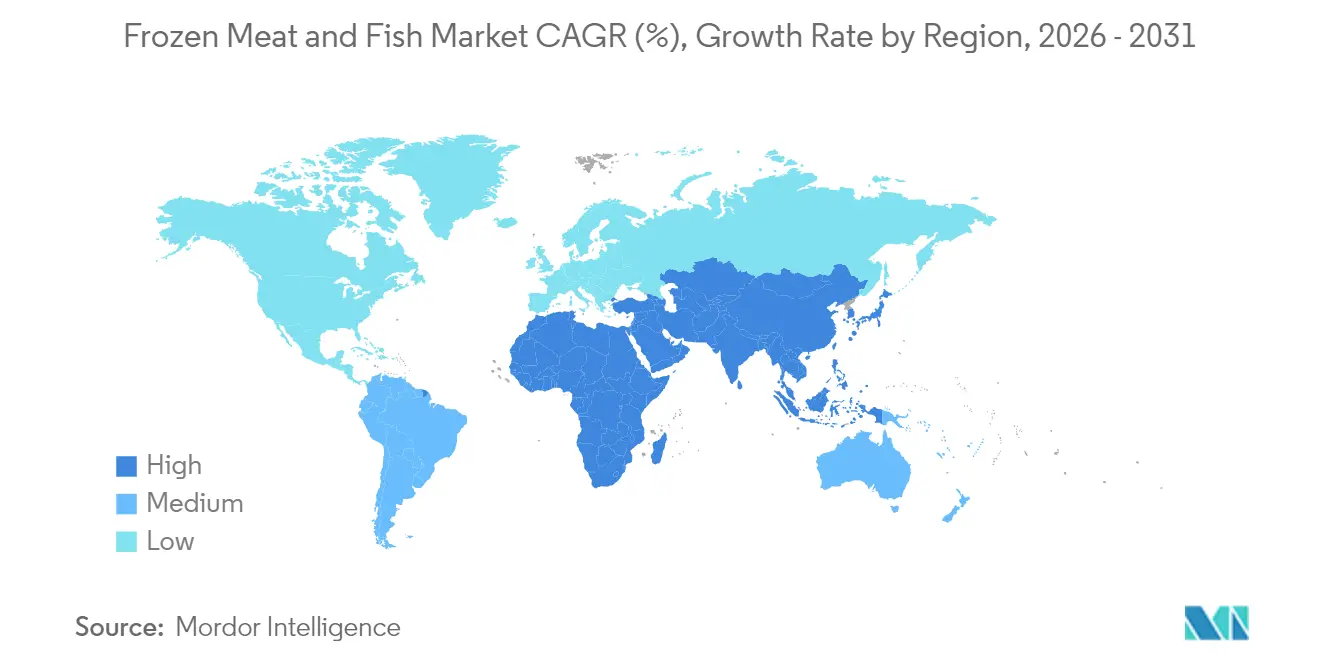

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Frozen Meat And Fish Market Analysis by Mordor Intelligence

The frozen meat and fish market size is expected to grow from USD 51.84 billion in 2025 to USD 54.63 billion in 2026 and is forecast to reach USD 70.97 billion by 2031 at 5.38% CAGR over 2026-2031. Shifts in consumer preferences and distribution strategies are reshaping the frozen meat and seafood market. While meat retains a dominant market share, seafood is rapidly gaining ground. Currently, wild-caught and caged sourcing leads the way, but there's a noticeable shift towards farm-raised and free-range products, driven by heightened consumer focus on sustainability and quality. Although foodservice is the primary distribution channel, retail is swiftly gaining momentum. A growing appetite for convenient, long-lasting, yet nutritious food options fuels this surge in retail. Technological advancements, especially in IQF and cryogenic freezing methods, have enhanced the quality, texture, and taste of frozen meat and seafood, bolstering consumer confidence. E-commerce's rise has revolutionized the landscape, enabling direct-to-consumer models and broadening access to premium frozen products across various regions. A discernible trend towards healthier, preservative-light options is steering manufacturers to craft products that marry convenience with nutrition. North America stands out as a major revenue contributor, while Asia-Pacific emerges as the region with the most rapid growth, hinting at a vibrant future and deepening consumer interest.

Key Report Takeaways

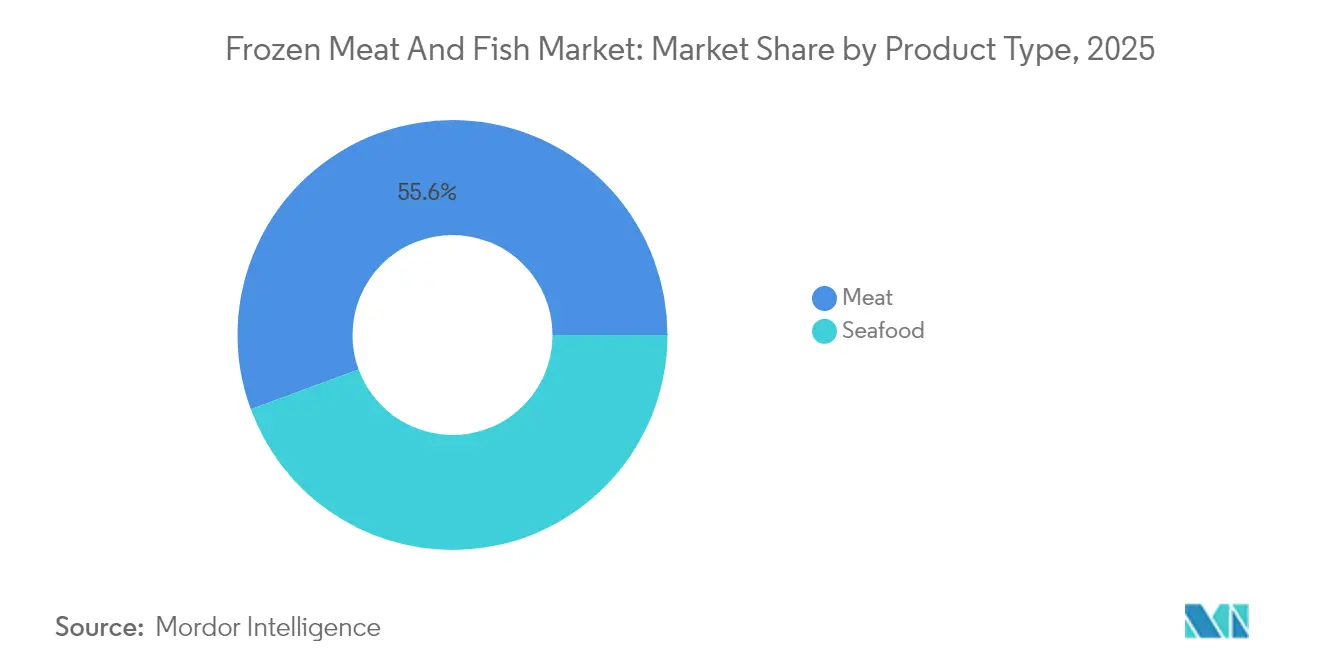

- By product type, meat held 55.62% of frozen meat and seafood market share in 2025, and seafood is forecast to climb at an 7.89% CAGR through 2031.

- By source, wild-caught/caged products accounted for 53.78% share of the frozen meat and seafood market size in 2025; the farm-raised/free-range segment is set to advance at an 8.29% CAGR between 2026-2031.

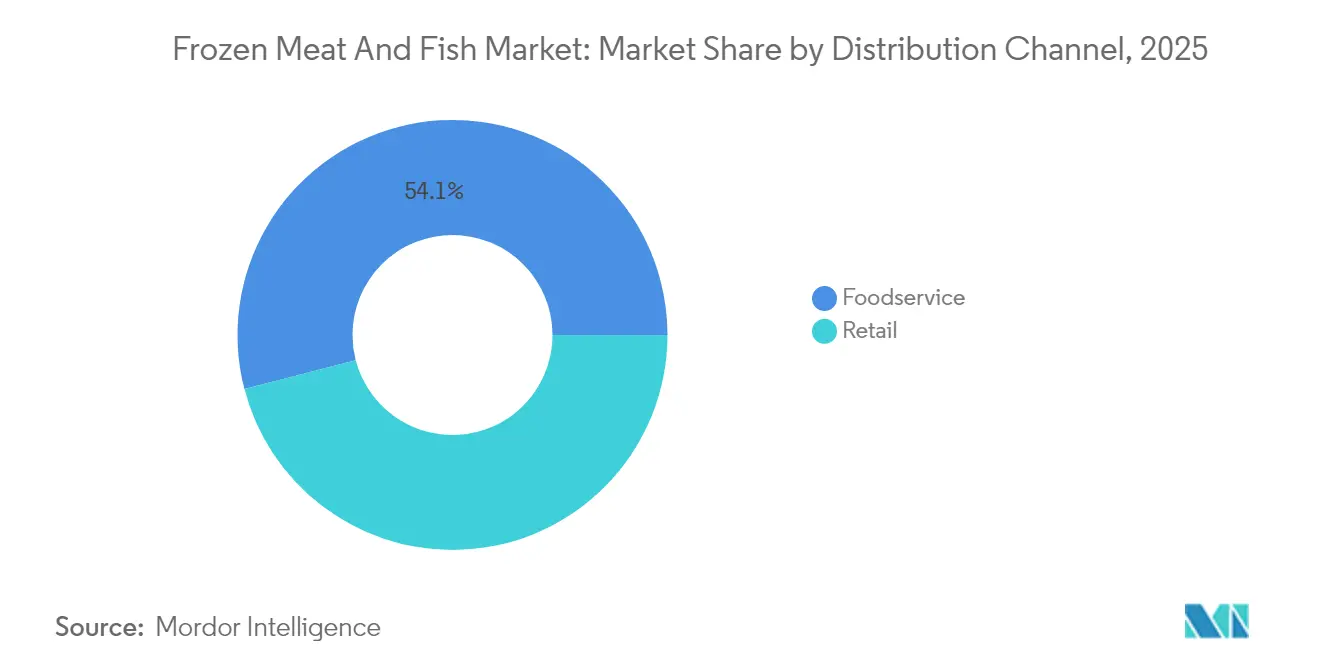

- By distribution channel, foodservice commanded 54.05% of the frozen meat and seafood market in 2025, while retail is slated to expand at a 9.01% CAGR by 2031.

- By geography, North America contributed 32.05% revenue in 2025; Asia-Pacific is projected to record the fastest 6.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Frozen Meat And Fish Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of IQF and cryogenic freezing for high-value meat and fish | +2.7% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Retailers' private-label penetration boosting frozen meat and fish | +3.2% | North America, Europe, with emerging influence in Asia-Pacific | Short term (≤ 2 years) |

| E-commerce-first D2C meat brands driving portion-controlled packs | +4.0% | Global, with highest adoption in urban centers | Medium term (2-4 years) |

| Extended shelf life of frozen products reduces food waste and supports bulk purchasing habits | +2.1% | Global, with higher impact in developed markets | Short term (≤ 2 years) |

| Growing awareness of protein-rich diets is boosting consumption of frozen meat and fish products | + 3.9% | Global, with strongest growth in Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of organized retail and e-commerce platforms is improving product accessibility | +2.3% | Asia-Pacific, Latin America, with spill over to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing adoption of IQF and cryogenic freezing for high-value meat and fish

Individual Quick Freezing (IQF) and cryogenic freezing technologies are transforming the market by improving product quality and shelf life. These freezing methods minimize ice crystal formation, preserving the cellular structure of seafood products and maintaining texture, flavor, and nutritional content after thawing. IQF tunnel freezers with rolling-wave technology enable processors to freeze individual seafood items while reducing operational costs. The technology maintains product separation during freezing, preventing clumping and ensuring consistent portion control for food service and retail applications. Companies such as BRF SA, Del Pacifico Seafoods and ABZ Frozen Foods utilize IQF technology in their frozen meat and fish products to maintain food quality and convenience. The improved product quality, extended shelf life, reduced energy consumption, and enhanced operational efficiency have increased the adoption of IQF and cryogenic freezing technologies in the frozen meat and fish industry. These freezing methods help manufacturers meet consumer demand for frozen products with fresh-like characteristics, supporting market growth.

Retailers' private-label penetration boosting frozen markets for meat and fish

Private label brands are experiencing substantial growth in the frozen meat and fish market as retailers expand their product portfolios. These brands focus on delivering high-quality products, sustainable sourcing practices, and competitive pricing to capture larger market shares. Consumer trust in retailer brands, combined with increasing price sensitivity, continues to support this expansion. For instance, in February 2024, ALDI, a German retailer, promoted its private-label seafood products and introduced pollock portions. ALDI sources all its exclusive fresh, frozen, and canned seafood from responsibly managed fisheries and farms that minimize environmental impact and maintain human rights standards. Private label brands are strengthening their market position through strategic partnerships and co-branding initiatives with established suppliers. The emphasis on transparency in sourcing, quality control measures, and competitive pricing strategies has enhanced consumer confidence in private label products. Additionally, retailers are investing in packaging innovations and product diversification to meet evolving consumer preferences. The integration of sustainability certifications and clear labeling practices has further positioned private label products as reliable alternatives to traditional branded offerings. These developments indicate sustained growth potential for private label frozen meat and fish products in the global market.

E-commerce-first D2C meat brands driving portion-controlled packs

E-commerce platforms are transforming the frozen meat and fish market by enabling direct-to-consumer (D2C) brands to reach customers through digital channels. These platforms facilitate seamless transactions between producers and consumers, offering premium seafood and meat products with portion-controlled packaging that addresses consumer preferences for convenience and waste reduction. The digital marketplace allows consumers to access detailed product information, compare prices, and make informed purchasing decisions from the comfort of their homes. Companies like Fresh N Frozen demonstrate this digital transformation by operating exclusively through their websites, eliminating traditional retail intermediaries. The rise of mobile applications and user-friendly interfaces has further simplified the ordering process, while efficient cold chain logistics ensure product quality during delivery. Additionally, e-commerce enables producers to gather valuable consumer data, helping them adjust their product offerings and packaging sizes to meet specific market demands.

Growing awareness of protein-rich diets is boosting consumption of frozen meat and fish products

The increasing consumer awareness about protein-rich diets is driving growth in the frozen meat and fish market. Health-conscious consumers seek high-protein food options for muscle development, weight management, and overall health benefits. Frozen meat and fish products provide a convenient solution with extended shelf life compared to fresh alternatives. The rise in fitness culture and specialized diets, such as keto and paleo, has increased demand for these protein-rich frozen products. Busy lifestyles and the need for quick meal preparation have made frozen meat and fish products particularly appealing, while portion-controlled options help consumers manage their protein intake effectively. Market players have responded by expanding their product portfolios and emphasizing protein content on packaging. According to the Food and Agriculture Organization (FAO), the global undernourishment rate was 9.1% in 2023, indicating the potential for frozen meat and fish to serve as an affordable protein source to improve dietary nutrition [1]Source: Source: Food and Agriculture Organization, “Share of Undernourished People Worldwide in 2023”, fao.org. These factors collectively demonstrate the significant role of frozen meat and fish products in meeting global protein requirements while addressing modern consumer preferences and nutritional needs..

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in ocean freight disrupting frozen fish supply | -1.8% | Global, with highest impact on Asia-Pacific exporters | Short term (≤ 2 years) |

| Cultural shift toward plant-based proteins among Gen-Z consumers | -1.2% | North America, Europe, Urban Asia | Long term (≥ 4 years) |

| Strict regulations regarding food safety, storage temperatures, and handling requirements increase compliance costs | -1.6% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Environmental concerns about packaging waste and energy consumption in cold storage facilities | -1.4% | Europe, North America, with growing influence in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in ocean freight disrupting frozen fish supply

Ocean freight volatility disrupts the frozen seafood industry's supply chains, affecting product availability and pricing. The National Retail Federation projects a 20% year-over-year decline in imports for May 2025, with annual volume expected to decrease by over 10[2] Source: National Retail Federation, "Import Cargo Levels to See First Year", nrf.com . China-US trade routes experienced a 25% reduction in daily ocean container bookings as of April 2025, primarily due to increased US tariffs on Chinese goods, which rose to 125%. These developments constrain the global frozen meat and fish market, impacting supply chain operations and market access. Ocean freight challenges extend beyond immediate supply disruptions, affecting cold storage capacity utilization and inventory management across major ports. The increasing freight rates, coupled with longer transit times, necessitate enhanced cold chain infrastructure investments by market participants. Additionally, port congestion and container shortages force companies to maintain higher inventory levels, increasing operational costs. The uncertainty in ocean freight schedules also influences procurement strategies, with importers diversifying their supplier base across multiple regions to mitigate risks. Furthermore, these logistics challenges prompt companies to explore alternative transportation methods and regional sourcing options, reshaping traditional supply chain networks in the frozen meat and fish market.

Cultural shift toward plant-based proteins among Gen-Z consumers

The growing preference for plant-based protein alternatives, particularly among Generation Z consumers, affects the frozen meat and seafood market. Companies like Beyond Meat, Impossible Foods, GoodDot, and Vegolution continue to expand their plant-based meat product lines to address this increasing demand. This consumer shift toward plant-based alternatives may limit the growth potential of the traditional frozen meat and seafood market over the long term. The rising environmental consciousness among consumers, coupled with health concerns related to meat consumption, drives the adoption of plant-based alternatives. Additionally, technological advancements in plant-based protein development have improved taste and texture, making these alternatives more appealing to consumers. The increasing availability of plant-based options in retail stores and restaurants further strengthens this trend, potentially impacting the market share of conventional frozen meat and seafood products. Moreover, government initiatives promoting sustainable food choices and the growing number of flexitarian consumers contribute to this market restraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Meat dominates while seafood outpaces on growth

The meat segment commands the largest market share at 55.62% in 2025. Poultry, specifically chicken and turkey, drives this dominance due to broad consumer acceptance and competitive pricing compared to alternative protein sources. The convenience of frozen meat products, combined with extended shelf life, appeals to busy households seeking quick meal solutions. Additionally, improvements in freezing technology have enhanced the texture and taste of frozen meat products, maintaining qualities similar to fresh alternatives. Companies such as Good Ranchers, Zanchick, and JBS SA have enhanced market growth through portion-controlled packaging and value-added frozen meat products.

The seafood segment demonstrates strong growth potential with a projected CAGR of 7.89% from 2026-2031. This growth stems from increased consumer awareness of health benefits and improved freezing technologies that maintain product quality. Tuna and salmon remain key products in the seafood segment, with salmon prices reaching record levels due to supply chain disruptions and farm production delays. The adoption of Individual Quick Freezing (IQF) technology improves frozen seafood quality, attracting consumers who traditionally purchased fresh products. Rising demand for omega-3 rich fish products and sustainable seafood options has expanded the frozen fish market.

By Source: Wild-caught leads while farm-raised gains momentum

The wild-caught/caged segment dominates the market with a 53.78% share in 2025, particularly in the seafood category, where wild-caught fish command premium prices due to consumer perception of superior taste and quality. This segment benefits from established distribution networks and traditional consumer preferences, especially in regions with a strong fishing heritage. The market position is further strengthened by the perception that wild-caught products offer better nutritional value. However, the segment faces increasing pressure from sustainability concerns as consumers become more aware of overfishing and environmental impacts. Companies like Sea To Table address these concerns by offering wild-caught flash-frozen fish sourced from sustainable fishing practices that support local communities. The implementation of stricter fishing regulations and increased focus on marine ecosystem preservation influence the segment's growth potential.

The farm-raised/free-range segment is expected to grow at a CAGR of 8.29% from 2026 to 2031. The farm-raised/free-range segment is on a steady upswing, driven by innovations in aquaculture, heightened sustainability efforts, and a growing acceptance among consumers. These controlled environments guarantee consistent quality and a year-round supply. Within the meat category, there's a rising trend for free-range and ethically raised livestock. This surge is especially pronounced among health-conscious consumers who prioritize animal welfare and are willing to pay a premium. Producers such as Verde Farms and Bell & Evans are aligning with this demand, emphasizing humane and antibiotic-free practices. Furthermore, the segment reaps the benefits of advanced feed solutions and a robust cold chain infrastructure, ensuring a stable supply and facilitating nationwide distribution. This reliability elevates farm-raised/free-range meat and seafood as a strong contender against their wild-sourced counterparts.

By Distribution Channel: Foodservice leads while online retail accelerates

The foodservice (HoReCa) segment accounts for 54.05% of the market share in 2025. This significant share stems from restaurants, hotels, and catering services requiring large volumes of frozen meat and seafood to maintain consistent quality and benefit from extended shelf life. The segment's dominance is further reinforced by the operational advantages frozen products offer to foodservice establishments, including reduced food waste and simplified inventory management. Commercial kitchens particularly value the convenience and cost-effectiveness of frozen meat and seafood products, as they help standardize portion control and maintain menu consistency throughout the year.

The retail segment is expected to grow at a CAGR of 9.01% during 2026-2031, driven by increased e-commerce adoption, improved cold chain logistics, and changing consumer shopping preferences. The expansion of temperature-controlled delivery services has increased consumer confidence in purchasing frozen meat and seafood products online. Supermarkets and hypermarkets maintain a significant presence in the retail segment, with growth supported by increased retail outlet distribution. For example, in November 2024, Prime Shrimp expanded into select Whole Foods Market stores across the United States, with availability in more than 200 stores across the Northeast, North Atlantic, Mid-Atlantic, South, and Southwest regions, strengthening retail sales channels.

Geography Analysis

North America holds the largest market share at 32.05% in 2025, supported by well-established cold chain infrastructure and robust retail and foodservice networks. The United States market features a mature retail landscape with increasing focus on ethical sourcing and food safety compliance. The region's strong distribution channels and advanced storage facilities ensure consistent product quality throughout the supply chain. Consumer preferences in North America increasingly favor premium frozen products with clear traceability and sustainability certifications. The market also benefits from technological advancements in freezing techniques that help maintain product quality.

Asia-Pacific is expected to grow at a CAGR of 6.88% from 2026-2031, driven by rising disposable incomes, urbanization, and evolving dietary preferences in China, Japan, and India. JD Super's partnerships with Argentina's Beef Promotion Institute (IPCVA) and Linking Fresh in May 2025 demonstrate strategic expansion in China's frozen meat market. The region's growing middle-class population has increased demand for convenient protein options, particularly in metropolitan areas. Improvements in cold storage infrastructure across developing Asian markets have enhanced product accessibility and distribution efficiency. Local retailers are expanding their frozen food sections to accommodate the increasing consumer demand for frozen meat and fish products.

Europe maintains a significant market share in the food industry, with consumer demand increasingly focused on sustainable and ethically sourced products. According to the National Library of Medicine, European consumers demonstrate a willingness to pay premium prices for meat products with health and ethical labels . Transparency is paramount for these consumers, leading them to prefer products boasting sustainability certifications. Companies such as Nomad Foods and Vion Food Group are rising to the occasion, adopting responsible sourcing and cutting-edge processing technologies to align with these consumer expectations. Meanwhile, the Middle East and Africa are witnessing uneven market growth. In the Gulf Cooperation Council (GCC) nations, urbanization and a burgeoning expatriate community have spiked the demand for frozen meat and seafood, especially in foodservice. Religious and cultural nuances also shape demand patterns here, evident in the strong preference for halal-certified frozen products.

Competitive Landscape

The frozen meat and seafood market exhibits a moderate fragmented market with global corporations and regional specialists competing across product segments and geographic regions. Key market players include Nomad Foods Limited, Marfrig Group, and Austevoll Seafood ASA. These companies maintain their competitive edge through product innovation, sustainability initiatives, and digital transformation efforts. The market structure allows for both large-scale operations and specialized regional players to coexist, creating a balanced competitive environment. Companies are increasingly investing in cold chain infrastructure and distribution networks to enhance their market reach and operational efficiency.

In October 2024, Bumble Bee Seafoods expanded its product portfolio with 11 new offerings in canned, pouched, and kit-based seafood categories. The new products include Wild-Caught Pink Salmon in Skinless and Boneless Pouch (MSC-Certified), Wild-Caught Sardines, and Prime Wild-Caught Tiny Shrimp. This product expansion reflects the industry's response to growing consumer demand for convenient, sustainable seafood options. The company's focus on MSC-certified products demonstrates the increasing importance of certification and traceability in the frozen seafood segment. Market players are continuously developing new product formats and packaging solutions to meet evolving consumer preferences.

Sustainability has become a key competitive advantage in the market, as demonstrated by High Liner Foods achieving 96% responsibly sourced seafood in 2023. The company has also set targets to reduce greenhouse gas emissions and food waste intensity by 50% by 2030. These sustainability commitments are becoming increasingly important for market competitiveness and consumer trust. Companies are implementing comprehensive environmental programs that encompass responsible sourcing, waste reduction, and emissions control. The industry's focus on sustainability extends beyond environmental concerns to include social responsibility and economic sustainability throughout the supply chain.

Frozen Meat And Fish Industry Leaders

-

Nomad Foods Limited

-

M&J Seafood Holdings Limited

-

Austevoll Seafood ASA

-

Marfrig Group

-

Cargill, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Deutsche See expanded its frozen product line with three new offerings. The company designed these products with portion-controlled packaging to address the needs of quality-conscious consumers and retailers looking for additional frozen food alternatives.

- March 2025: Birds Eye has unveiled "Captain's Discoveries," a fresh lineup of fish products. This new range features four innovative offerings alongside two established favorites. Highlights include the Tortilla Crumb Fish Fillets, infused with a zesty touch of lime and chili, drawing inspiration from Mexican cuisine, and the Focaccia Crumb Fish Fillets, echoing Mediterranean flavors with sun-dried tomatoes and thyme.

- October 2024: Butterball LLC introduced a Premium Whole Turkey product that allows consumers to cook the turkey directly from its frozen state. The product features a specially-formulated brine solution. This new Cook From Frozen Premium Whole Turkey enables direct cooking without prior thawing.

- March 2024: Moy Park introduced new frozen chicken products to Asda stores in response to increasing consumer demand for flavorful, diverse, and convenient frozen breaded chicken options across Great Britain and Northern Ireland.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global frozen meat and fish market as the factory-gate value of raw, unseasoned red and white meat cuts and fin fish that are quick-frozen to -18 °C or colder and later thawed by food service or retail buyers before consumption. We also follow integrated processors that ship directly to stores and restaurants under their own labels.

Scope exclusions include ready-to-eat frozen meals, batter-coated snacks, chilled or canned proteins, and plant-based analogs.

Segmentation Overview

-

By Product Type

-

Meat

- Chicken and Turkey

- Beef

- Pork

- Mutton

- Others

-

Seafood

- Tuna

- Salmon

- Other Species (Cod, Shrimp, etc.)

-

Meat

-

By Source

- Farm-raised/Free-range

- Wild-caught/Caged

-

By Distribution Channel

- Foodservice (HoReCa)

-

Retail

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Stores

- Other Retail Formats

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cold chain operators, export agents, menu developers, and modern retail buyers across North America, Europe, and Asia-Pacific. Their insights on IQF uptake, freezer utilization, and retail mark-ups corrected blind spots and validated early numbers.

Desk Research

We began with trusted public datasets such as FAO capture statistics, USDA cold-storage bulletins, Eurostat customs codes, and OECD meat outlooks, since these establish slaughter yields, catch volumes, and trade flows. Company 10-Ks, investor slides, and national meat association briefs added price brackets and channel splits, which we matched with customs unit values. Paid assets from D&B Hoovers and Dow Jones Factiva helped us verify processor revenues and capacity additions. This list is illustrative only; many other reputable outlets informed our evidence stack.

Market-Sizing & Forecasting

Every country's demand is first reconstructed through a top-down balance of slaughter yield plus marine catch minus frozen exports. We then stress-test totals with sampled processor shipments times average ex-works prices. Key variables like domestic beef kills, aquaculture output, freezer utilization, retail cabinet density, and average price variance feed a multivariate regression that extends the view through 2030. Scenario checks around freight costs and protein substitution temper the base case, while import parity factors bridge informal trade gaps.

Data Validation & Update Cycle

Outputs pass peer review, automated variance dashboards flag anomalies, and our team re-contacts experts before sign-off. The model refreshes each year, with interim updates triggered by material events.

Why Mordor's Frozen Meat And Fish Baseline Remains Deeply Dependable

Published values often diverge because firms mix processed meals, apply retail mark-ups, or use stale currency conversions. Our disciplined scope, yearly refresh, and primary tested variables anchor a reliable baseline that decision-makers can trace with confidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 51.84 B (2025) | Mordor Intelligence | - |

| USD 99.20 B (2025) | Global Consultancy A | Adds poultry and full retail mark-ups, scant primary work |

| USD 98.10 B (2023) | Industry Data Publisher B | Bundles all frozen food and double-counts re-exports |

These contrasts show how Mordor's balanced, transparent steps deliver figures grounded in clear inputs and repeatable logic.

Key Questions Answered in the Report

What is the current frozen meat and fish market size?

The frozen meat and fish market size stands at USD 54.63 billion in 2026 and is forecast to reach USD 70.97 billion by 2031.

Which product type commands the highest frozen meat and fish market share?

Meat, led by poultry SKUs, held 55.62% of frozen meat and fish market share in 2025.

Which channel is expanding fastest within the frozen meat and fish market?

Retail distribution channel is projected to grow at a 9.01% CAGR through 2031.

Why is seafood expected to outpace meat in growth?

Seafood enjoys an 7.89% CAGR outlook, aided by IQF technology that preserves texture and by rising health awareness around omega-3 benefits.

Page last updated on: