Tinned Fish Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 15.19 Billion |

| Market Size (2031) | USD 19.56 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

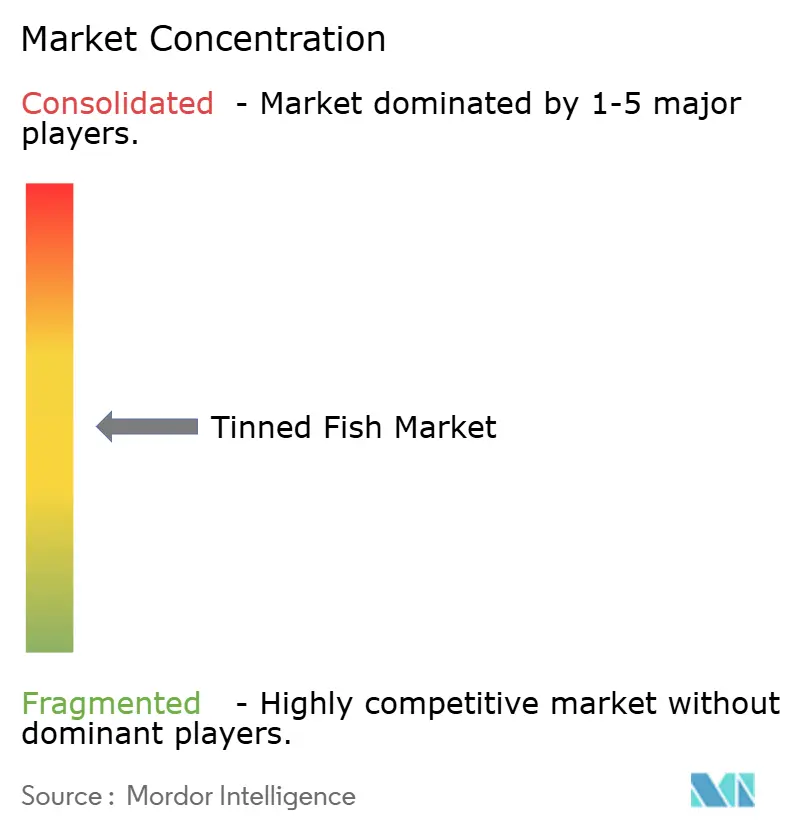

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tinned Fish Market Analysis by Mordor Intelligence

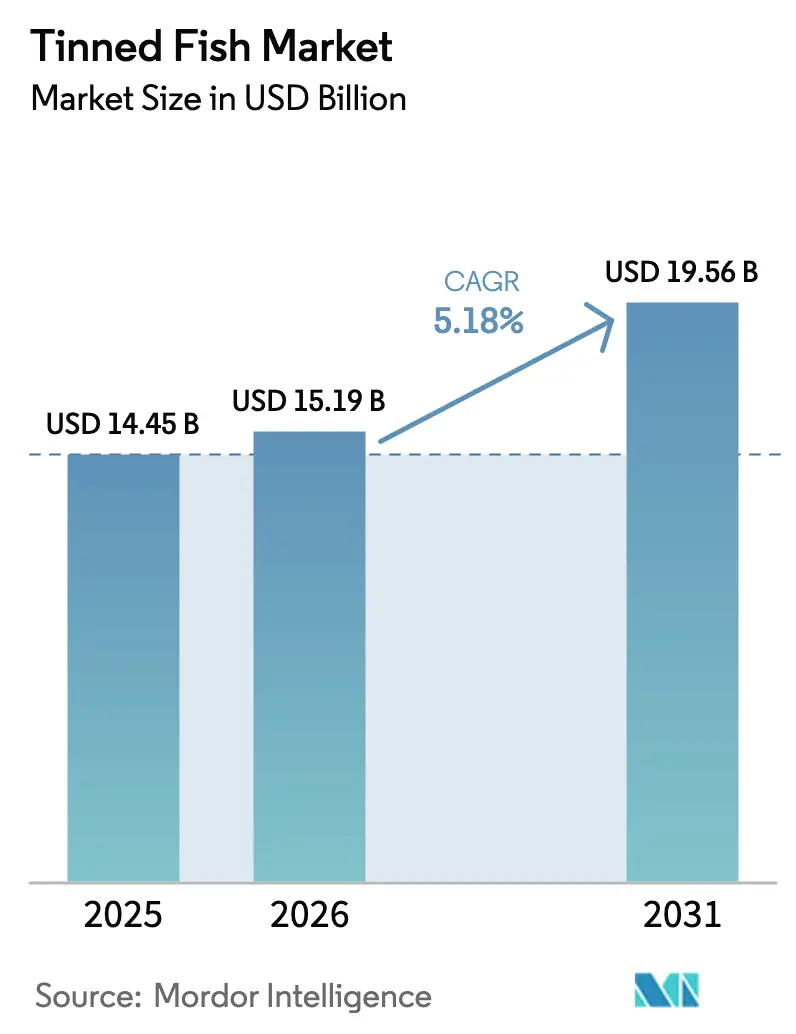

The global tinned fish market size is expected to grow from USD 14.45 billion in 2025 to USD 15.19 billion in 2026 and is forecast to reach USD 19.56 billion by 2031 at 5.18% CAGR over 2026-2031. The growing demand for seafood, coupled with its healthy attributes like the presence of superior quality proteins, essential fatty acids, and macro and micronutrients, is driving the global tinned fish market. Fish represents a rich source of nutrients necessary for good health. In addition, the expanding trend of consuming convenience foods due to busy lifestyles is influencing consumer inclination towards processed food, such as tinned fish. Further, the improved distribution infrastructure and fish processing methods are driving the growth of the tinned fish market across the globe. Therefore, new product introductions, expanding distribution channels, and improvements in canning techniques are anticipated to boost market expansion during the projection period.

Key Report Takeaways

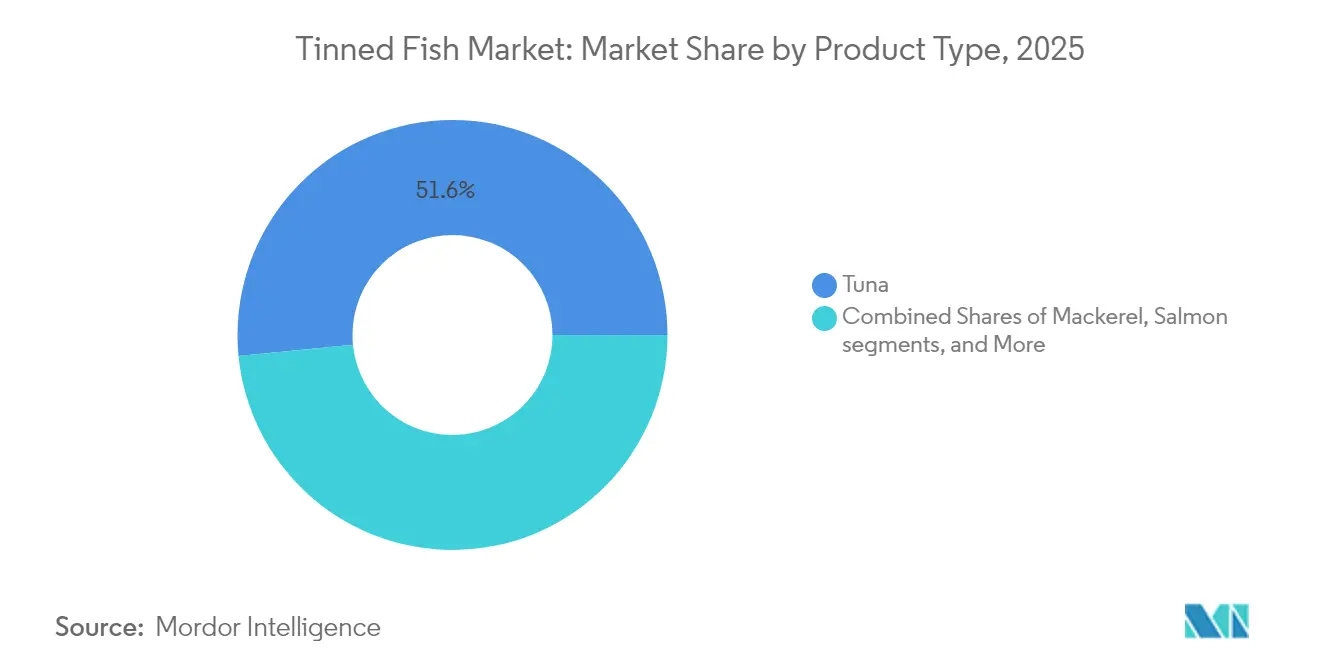

- By product type, tuna led with 51.55% of the tinned fish market share in 2025; mackerel is projected to expand at a 6.55% CAGR to 2031.

- By price, the mass segment accounted for 84.62% of the tinned fish market size in 2025; premium items are advancing at an 8.12% CAGR.

- By preservation medium, oil-based products captured 54.62% share of revenue in 2025, while brine-preserved lines are forecast to grow at 7.18% CAGR.

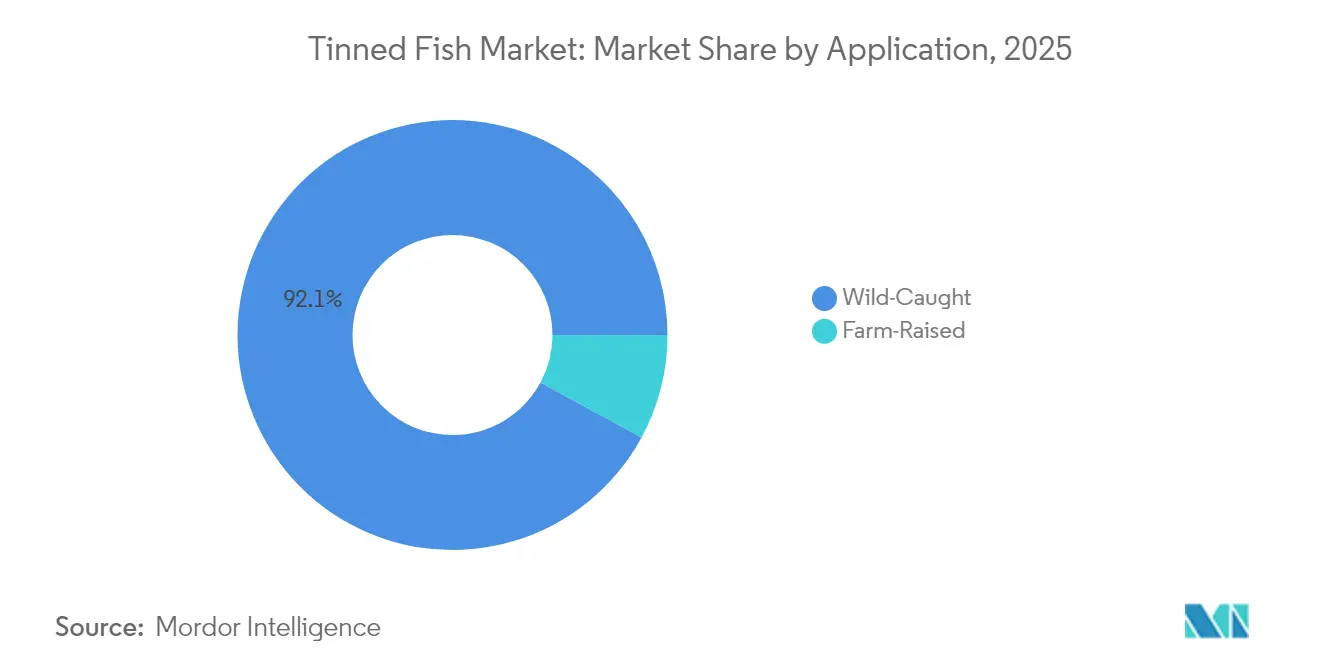

- By fish source, wild-caught offerings dominated with a 92.10% market share in 2025, whereas farm-raised products are poised for an 7.72% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets held 63.10% of the tinned fish market share in 2025; online retail is set to rise at 7.29% CAGR.

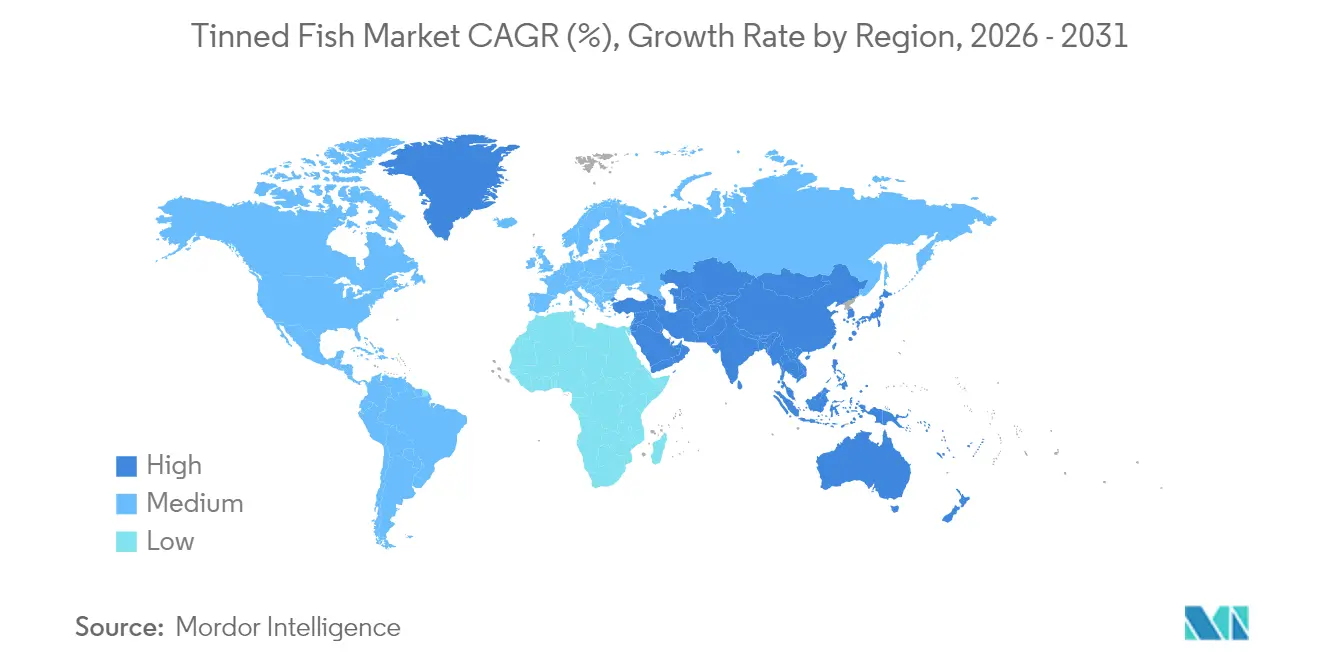

- By geography, Europe represented a 31.74% share of the global market in 2025; Asia-Pacific is projected to register a 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tinned Fish Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Convenient and Ready-To-Eat Protein Sources | +1.2% | Global, with strongest impact in North America and Europe | Short term (≤ 2 years) |

| Growing Awareness of Health Benefits Associated with Omega-3-Rich Fish | +0.9% | Global, particularly the Asia-Pacific emerging markets | Medium term (2-4 years) |

| Expansion of Organized Retail and E-Commerce | +0.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Longer Shelf Life Appeals to Consumers Seeking Food Security | +0.7% | Global, heightened in crisis-prone regions | Short term (≤ 2 years) |

| Rising Disposable Incomes in Emerging Markets | +0.6% | Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Sustainable Fishing and Eco-Labeling Initiatives | +0.5% | North America and EU, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient and Ready-To-Eat Protein Sources Boosts Tinned Fish Consumption

The growing adoption of tinned fish is driven by the need for convenient, protein-rich solutions among busy professionals, coupled with its rising appeal as a trendy food choice influenced by social media. Platforms have popularized concepts like "tinned fish parties" and "seacuterie" boards, elevating canned seafood from a basic pantry item to an aspirational product, particularly among younger demographics who value both practicality and visually appealing meals. Retailers such as Target have capitalized on this trend by prominently featuring tinned fish to meet the increasing demand for quick, nutritious meal options. This convenience factor gains further importance during periods of economic uncertainty, as consumers seek affordable protein sources without compromising on quality or nutritional value. The convergence of convenience, health consciousness, and affordability positions tinned fish as a sustainable growth driver, transcending traditional consumption patterns and economic cycles to establish itself as both a necessity and a lifestyle choice.

Growing Awareness of Health Benefits Associated with Omega-3-Rich Fish Supports Market Growth

Scientific validation of omega-3 fatty acids' cardiovascular and cognitive benefits is influencing consumer preferences, particularly toward fish consumption, with tinned options emerging as a practical and affordable source of concentrated nutrition. Studies highlight that regular fish intake reduces the risk of cardiovascular diseases, certain cancers, and cognitive decline, with tinned fish offering comparable levels of essential proteins, omega-3 fatty acids, and micronutrients to fresh alternatives. This trend is particularly pronounced among aging populations and health-conscious consumers, who increasingly recognize tinned fish as a convenient way to meet dietary guidelines recommending at least 8 ounces of seafood weekly. As healthcare costs rise and preventive nutrition becomes a priority, this awareness is driving sustained demand growth in the market. Additionally, the long shelf life and ease of storage associated with tinned fish make it an attractive option for consumers seeking both convenience and cost-effectiveness. The growing focus on sustainable fishing practices further enhances the appeal of tinned fish, aligning with the values of environmentally conscious buyers.

Expansion of Organized Retail and E-Commerce Enhances Product Availability and Visibility

The expansion of digital commerce and modern retail has significantly enhanced the availability of tinned fish products, extending their reach beyond traditional sales channels. E-commerce platforms enable specialty and artisanal brands to directly connect with consumers, fostering premium market segments with higher profit margins. Concurrently, the growth of organized retail in emerging markets ensures proper storage conditions and effective merchandising, which not only maintain product quality but also educate consumers on product varieties and usage. This evolution in retail creates a cycle where increased visibility drives trial purchases, leading to repeat buying as consumers explore diverse fish species and preparations. The integration of physical and digital retail has made premium tinned fish products, previously limited to specialty stores, more accessible to a wider audience. The market's growth is further propelled by innovative distribution strategies, rising consumer awareness, and the introduction of varied product offerings across multiple retail formats.

Longer Shelf Life of Tinned Fish Products Appeals to Consumers Seeking Food Security

Tinned fish, with its extended shelf life enabled by sterilization, has become a critical pantry item for consumers prioritizing food security during supply chain disruptions and economic uncertainties. Its ability to remain viable for years without refrigeration addresses storage challenges, particularly in regions with inadequate cold storage infrastructure, while supporting household food budgets. Consumer behavior during crises, such as natural disasters and supply chain disruptions, highlights the practical and psychological benefits of shelf-stable products. Additionally, modern packaging technologies, including sensor-based smart systems that monitor food quality, are reducing reliance on expiration dates and minimizing food waste. This innovation is particularly significant in emerging markets, where income fluctuations and limited infrastructure make shelf-stable protein sources essential for meal planning. These factors drive consistent demand during economic downturns and create opportunities for market expansion during periods of growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Concerns Over Mercury and Microplastic Contamination | -0.8% | Global, particularly Europe with stricter regulations | Medium term (2-4 years) |

| Volatility In Raw Material Prices Affects Production Costs | -0.6% | Global, most severe in import-dependent regions | Short term (≤ 2 years) |

| Growing Preference for Fresh or Frozen Fish Alternatives | -0.4% | North America and Europe, urban centers with cold chain access | Medium term (2-4 years) |

| High Sodium Content in Some Tinned Fish Products | -0.3% | Global, strongest in health-conscious developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Concerns Over Mercury and Microplastic Contamination in Fish May Deter Consumers

Regulatory scrutiny and consumer awareness of contaminants create headwinds for tinned fish consumption, particularly as European NGOs advocate for stricter mercury limits that could reshape product formulations. The methylmercury exposure risk particularly affects pregnant women and children, creating market segmentation challenges as health-conscious consumers seek low-mercury alternatives. However, technological innovation provides mitigation pathways, with Chalmers University developing packaging solutions that reduce mercury content by up to 35% using cysteine-infused water-based solutions that bind mercury without altering taste or appearance. Microplastic concerns add complexity, though FDA[1]US FDA, “Metals in Seafood: Microplastics and Mercury,” fda.gov guidance indicates current levels in seafood do not pose health risks, providing regulatory clarity that supports continued consumption. The contamination narrative creates opportunities for premium positioning around purity and sourcing transparency, enabling brands to differentiate through testing protocols and contamination reduction technologies.

Volatility In Raw Material Prices Affects Production Costs and Profit Margins

Raw material price fluctuations create margin pressure and supply chain disruptions that challenge profitability and market stability, particularly as climate change affects fish availability in traditional sourcing regions. The severe sardine shortage from Morocco, where production fell 60% in 2024 due to poor fish levels and climate impacts, demonstrates how environmental factors can rapidly disrupt supply chains and inflate costs for processors dependent on specific sourcing regions. Fish processing costs are particularly sensitive to raw material fluctuations, with over 70% of total costs attributed to raw materials in EU processing operations[2]European Commission, “Cost Structure in EU Fish Processing,” ec.europa.eu, making price management critical for maintaining competitive positioning. This volatility drives vertical integration strategies and long-term sourcing contracts, while also creating opportunities for alternative species development and aquaculture expansion to reduce dependence on wild-caught supplies subject to environmental variability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tuna Dominance Faces Species Diversification

Tuna holds a dominant 51.55% market share in 2025, supported by widespread consumer acceptance and established global supply chains. Meanwhile, mackerel shows significant growth potential with a projected 6.55% CAGR through 2031, indicating a shift in consumer preferences. This change stems from increased health awareness, sustainability considerations, and consumer response to rising tuna prices caused by supply limitations and regulatory measures. Salmon continues to maintain its market position through premium branding and omega-3 content, while sardines appeal to cost-conscious consumers and offer sustainability benefits, despite production challenges in key regions like Morocco. Anchovies remain prominent in Mediterranean and Asian markets, with expansion opportunities in Western regions as consumers embrace diverse culinary traditions.

Social media platforms accelerate species diversification by introducing consumers to new preparation methods and elevating lesser-known species. Mackerel's growth is particularly notable due to its high omega-3 content and lower mercury concentration compared to larger fish species. Processors are expanding their capabilities to include alternative species, reducing their reliance on fluctuating tuna markets. The "others" category, which includes species such as octopus and mussels, presents opportunities for premium product development and culinary innovation that may transform traditional market structures.

By Price: Mass Market Stability Enables Premium Growth

Mass market products hold an 84.62% market share in 2025, providing volume stability that supports infrastructure investment and economies of scale. The premium segment is growing at an 8.12% CAGR as consumers seek higher quality and sustainable products. This market division reflects broader food industry patterns where budget-conscious consumers maintain category loyalty through affordable options, while higher-income segments support margin growth through their willingness to pay more for quality, transparent sourcing, and artisanal products. The premium segment benefits from social media exposure, which has transformed tinned fish from a basic pantry item to a premium food choice through enhanced presentation and communication about sourcing and preparation.

The premium segment growth creates opportunities for brands to differentiate through innovative packaging, sustainability certifications, and limited-edition products that generate higher margins while strengthening brand value. The mass market provides stability during economic downturns, as consumers seek affordable protein options that maintain nutritional value and convenience. This parallel growth allows companies to maintain volume through mass market products while increasing margins through premium offerings. The price segmentation also shows geographic differences, with emerging markets driving mass consumption and developed markets focusing on premium products as higher disposable incomes support increased spending.

By Preservation Medium: Oil Preference Shifts Toward Health-Conscious Alternatives

Oil-based preservation maintains 54.62% market share in 2025, supported by traditional consumer preferences and established supply chain infrastructure. Brine-preserved products are growing at 7.18% CAGR, driven by consumers seeking lower-sodium options and simpler ingredient lists. This market evolution reflects increasing consumer focus on ingredient transparency and dietary requirements, particularly regarding sodium intake. The "others" segment, including sauce-based and smoked preparations, offers opportunities for product differentiation through unique flavors and premium offerings that address diverse consumer preferences.

Brine preservation's growth stems from its perception as a healthier alternative to oil-based products, particularly among health-conscious consumers and those monitoring cardiovascular health. Oil-based products continue to maintain strong market presence due to superior flavor retention and texture preservation capabilities. The market shows potential for innovative preservation approaches that combine health benefits with taste preferences, including low-sodium brines and alternative oil formulations. Manufacturers must consider how preservation methods affect product shelf life and storage requirements when developing new products.

By Fish Source: Wild-Caught Dominance Faces Aquaculture Innovation

Wild-caught fish holds a 92.10% market share in 2025, as consumers prefer its natural origins and traditional harvesting methods. Farm-raised fish production grows at an 7.72% CAGR, driven by aquaculture technology improvements and sustainability requirements. This market structure highlights the contrast between consumer preferences for wild-caught fish and industry requirements for reliable supply chains and environmental sustainability, especially as wild fish populations face overfishing pressures and climate change effects. Aquaculture's expansion is supported by technical advances that improve fish health, minimize environmental effects, and enhance product quality to match wild-caught fish in taste and nutrition.

Companies are adapting their sourcing strategies to address sustainability requirements while meeting consumer demands. Wild-caught products retain their premium market position through natural and traditional fishing method messaging, while aquaculture products increase market acceptance through transparent farming practices and environmental advantages. Marine Stewardship Council (MSC) certification for wild-caught fish and Aquaculture Stewardship Council (ASC) certification for farmed fish provide standards for consumers and industry practices. Companies increasingly adopt dual-sourcing approaches, developing capabilities in both wild-caught and aquaculture production to strengthen supply chain stability and serve various market segments.

By Distribution Channel: Off-Trade Evolution Drives Digital Transformation

Supermarkets and hypermarkets hold a 63.10% market share in 2025, offering consistent volume sales and widespread consumer access. Online retail stores are growing at a 7.29% CAGR as digital commerce changes seafood buying patterns and enables brands to sell directly to consumers. This shift in distribution channels reflects a broader retail transformation, where traditional off-trade faces competition from e-commerce platforms that provide convenience, product variety, and direct consumer engagement. Convenience stores serve impulse buyers and urban consumers, while specialty stores cater to niche markets seeking premium and artisanal products at higher price points.

Digital platforms create opportunities for product differentiation and consumer education through detailed product information, cooking instructions, and sustainability messaging that physical stores cannot easily provide. Online retail benefits smaller and artisanal brands that can bypass traditional retail distribution and reach consumers through e-commerce and subscription services. The diversification of sales channels reflects evolving shopping habits, as younger consumers increasingly buy food online while traditional buyers prefer examining products in stores. In response, brands are developing omnichannel strategies to reach different consumer segments across multiple purchasing platforms.

Geography Analysis

Europe holds a 31.74% market share in 2025, supported by established consumption patterns and robust supply chain infrastructure. However, market saturation and regulatory requirements necessitate a focus on innovation and premium offerings. Regional household spending on fishery products rose 6% to USD 71.35 billion in 2023, despite a 5% decline in total consumption, indicating consumer preference for quality and sustainable products (EUMOFA). European regulations on mercury content, with proposed reductions from 1 ppm to 0.3 ppm by NGOs, present operational challenges while offering competitive advantages for companies with superior contamination controls.

Asia-Pacific market growth rate at a 7.52% CAGR benefits from young, urban populations seeking convenient protein sources that complement modern lifestyles and health preferences. China maintains its position as the global seafood production leader, producing 71 million metric tons in 2023, influencing global market dynamics (United States Department of Agriculture). European markets navigate strict regulatory requirements for mercury content and sustainability, which increase operational costs but enable differentiation through safety and environmental compliance. Market expansion in emerging regions reflects infrastructure limitations, where inadequate cold chain facilities favor tinned fish over fresh options, establishing sustained demand patterns.

North America demonstrates characteristics of both European maturity and Asia-Pacific growth, offering opportunities for volume growth and premium positioning across consumer segments. The U.S. tinned fish market expands through increased demand for healthy, sustainable seafood, while domestic production faces capacity constraints in cannery infrastructure, creating opportunities for local production expansion and import growth. The region's emphasis on sustainability supports MSC and ASC-certified products, with over 1,750 MSC-certified products available in the U.S. and Canada, demonstrating established infrastructure for sustainable seafood distribution and consumer acceptance.

Competitive Landscape

Thai Union Group PLC, Bolton Group (Rio Mare), Century Pacific Food Inc., and Wild Planet Foods Inc. lead the moderately concentrated tinned fish market. Established firms capitalize on economies of scale, while new entrants gain traction by introducing innovative products and targeting specific market segments.

Companies actively differentiate themselves by advancing technologies in packaging, traceability systems, and contamination reduction. These initiatives address consumer concerns and ensure compliance with regulatory standards. For example, Chalmers University's mercury-reduction packaging technology provides a competitive advantage for early adopters. Additionally, smart packaging systems that monitor food quality in real time enhance premium product positioning and minimize waste.

Growth opportunities lie in direct-to-consumer sales, sustainability-certified products, and the development of alternative fish species. Traditional tuna-focused strategies face challenges from supply constraints and regulatory pressures. New entrants leverage e-commerce platforms and social media to establish premium brands without relying on extensive retail infrastructure. This shift drives established companies to adapt their distribution strategies and refine their market positioning.

Tinned Fish Industry Leaders

Thai Union Group PLC

Bolton Group (Rio Mare)

Century Pacific Food Inc.

Wild Planet Foods Inc.

Bumble Bee Seafoods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Newlat Food, an Italian food company, has acquired Princes for GBP 700 million (USD 892 million). The acquisition adds Princes' canned fish products and Napolina sauce brands to Newlat's portfolio, positioning the Milan-based company to reach a billion-dollar valuation.

- December 2024: Simak, an Oman-based company, launched its new line of commercial canned tuna products. The company's facility produces more than 100 million cans annually. The new products are now available in supermarkets and other retail channels in Oman.

- August 2024: Wild Planet introduced a limited edition Wild Tuna Snack Pack through a collaboration with Simple Mills and Chosen Foods. The product features sustainably caught Skipjack Wild Tinned Tuna with diced dill pickle, lemon juice, and sea salt.

- January 2024: King Oscar launched a new line of skinless and boneless Atlantic salmon in extra virgin olive oil. The product line significantly expanded the company's seafood offerings in the market, enhancing its presence in the premium seafood segment and providing consumers with additional high-quality options.

Global Tinned Fish Market Report Scope

Tinned fish is processed fish, sealed in an airtight can, and preserved in salt and water, or oil. The global tinned fish market is segmented by type, distribution channel, and geography. By type, the market is segmented into mackerel, salmon, sardines, tuna, and others. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, and Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Tuna |

| Salmon |

| Sardines |

| Mackerel |

| Anchovies |

| Others |

| Mass |

| Premium |

| In Oil |

| In Brine |

| Others (sauce, smoked) |

| Wild-caught |

| Farm-raised (Aquaculture) |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Tuna | |

| Salmon | ||

| Sardines | ||

| Mackerel | ||

| Anchovies | ||

| Others | ||

| By Price | Mass | |

| Premium | ||

| By Preservation Medium | In Oil | |

| In Brine | ||

| Others (sauce, smoked) | ||

| By Fish Source | Wild-caught | |

| Farm-raised (Aquaculture) | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the tinned fish market?

The tinned fish market size is USD 15.19 billion in 2026 and is projected to rise to USD 19.56 billion by 2031.

Which species commands the largest share?

Tuna leads with 51.55% of 2025 global revenue, although mackerel is the fastest-growing species segment.

Why is Asia-Pacific the fastest-growing region?

Rising disposable incomes, rapid urbanization, and strong e-commerce uptake push Asia-Pacific to a 7.52% CAGR through 2031.

What role does e-commerce play in category growth?

Online channels grow at 7.29% CAGR by offering direct-to-consumer access, detailed product storytelling, and subscription models that foster loyalty.

Page last updated on: