SMB Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

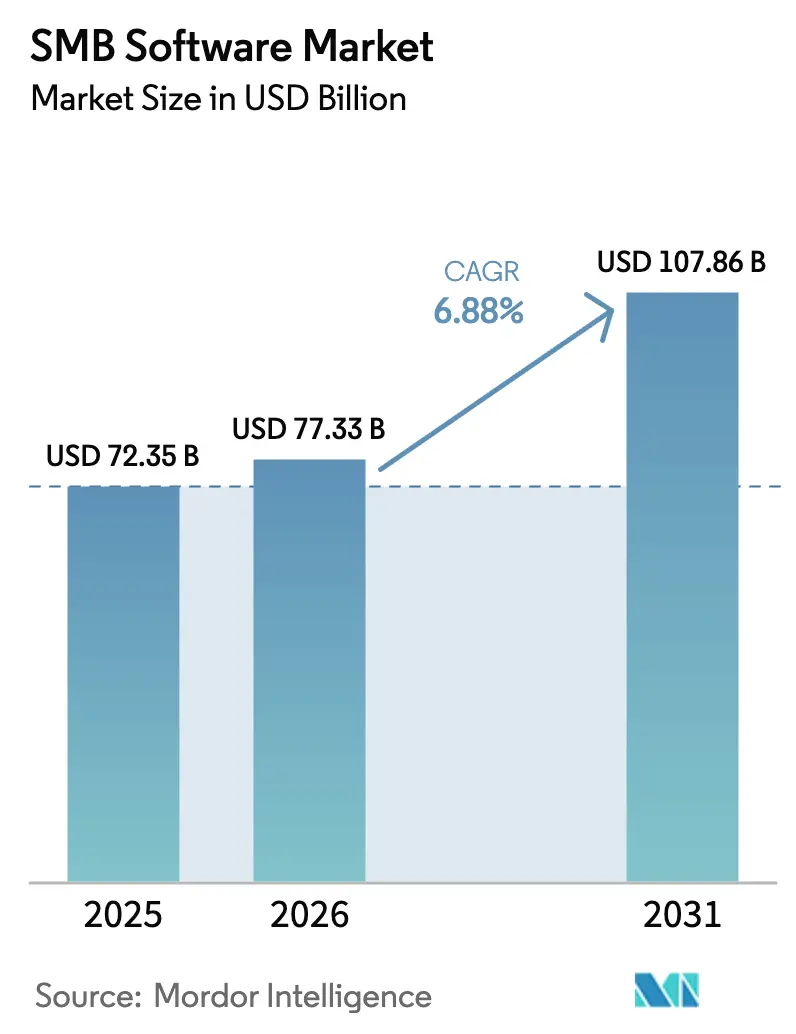

| Market Size (2026) | USD 77.33 Billion |

| Market Size (2031) | USD 107.86 Billion |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SMB Software Market Analysis by Mordor Intelligence

The SMB software market size was valued at USD 72.35 billion in 2025 and estimated to grow from USD 77.33 billion in 2026 to reach USD 107.86 billion by 2031, at a CAGR of 6.88% during the forecast period (2026-2031). Growth springs from a simple reality: digital tools have moved from optional to indispensable for small and mid-sized businesses that must keep pace with larger competitors. Cloud deployment dominates thanks to its pay-as-you-grow economics, while AI-ready platforms, tighter cybersecurity rules, and an acute shortage of in-house IT skills give vendors further tailwinds. Demand also benefits from macro-pressures such as inflation and supply-chain volatility because automation helps firms control rising costs. Competitive intensity is moderate: deep-pocketed incumbents eye the SMB software market for new revenue streams, yet nimble vertical specialists chip away at niche opportunities.

Key Report Takeaways

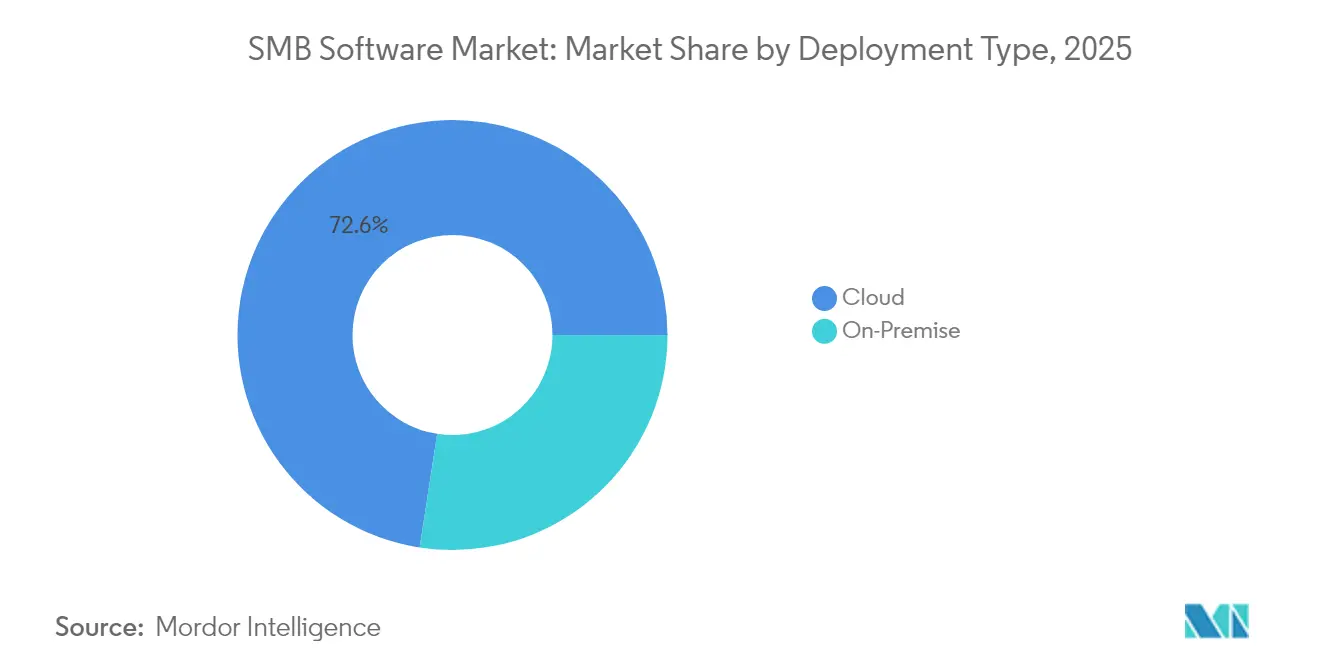

- By deployment type, cloud captured 72.56% of SMB software market share in 2025 and is expanding at 16.92% CAGR to 2031.

- By enterprise size, SMEs held 47.20% of the segment and are forecast to grow at 12.42% CAGR through 2031.

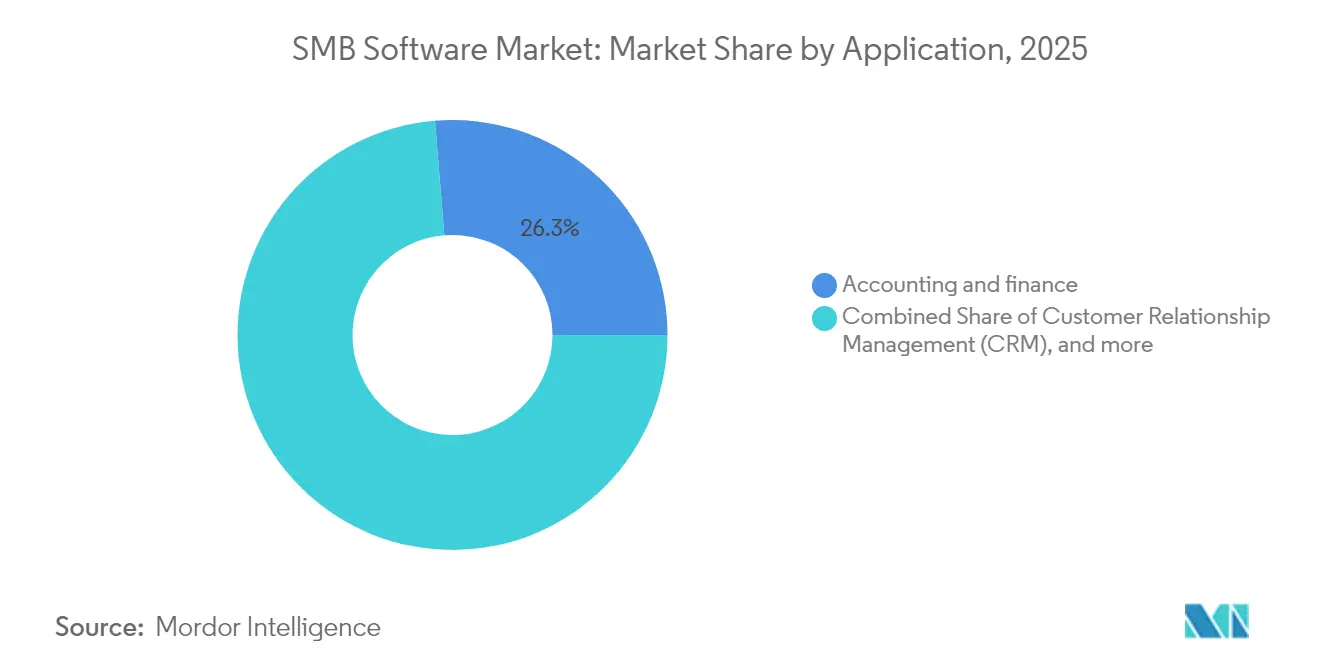

- By application, accounting and finance generated 26.30% revenue in 2025; security and compliance is set to climb by 15.98% CAGR.

- By end-user industry, retail and e-commerce led with 22.50% revenue in 2025; healthcare is projected to advance at 15.08% CAGR.

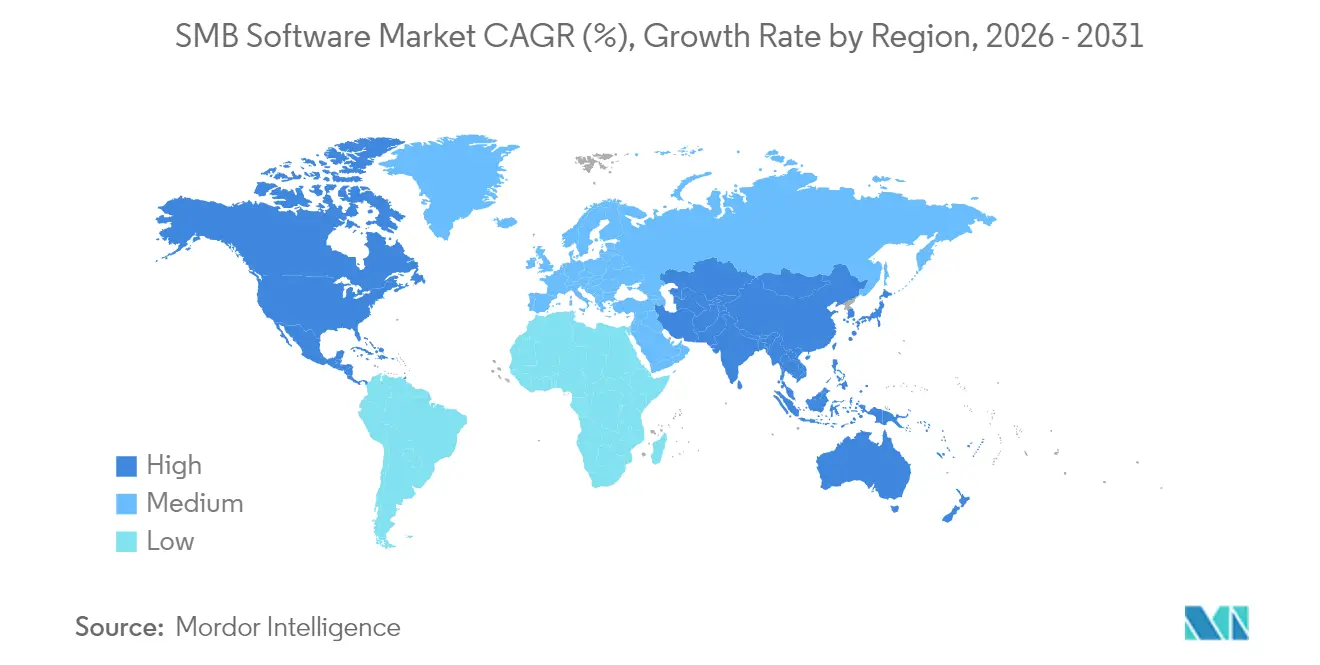

- By geography, North America contributed 39.60% revenue in 2025 while Asia-Pacific is charting the fastest 15.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global SMB Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream cloud adoption among SMBs | +2.1% | Global, with acceleration in APAC and Latin America | Medium term (2-4 years) |

| Surge in low-code/no-code development tools | +1.8% | North America & EU leading, expanding to APAC | Short term (≤ 2 years) |

| Proliferation of vertical SaaS bundles for SMBs | +1.5% | Global, strongest in developed markets | Medium term (2-4 years) |

| Rise of embedded fintech features in core apps | +1.2% | North America, EU, with emerging adoption in APAC | Long term (≥ 4 years) |

| Gen-AI copilots integrated in productivity suites | +0.9% | Global, enterprise-led with SMB following | Short term (≤ 2 years) |

| Telecom-led bundled IT services for micro-SMBs | +0.7% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream cloud adoption among SMBs

Close to 63% of SMB workloads now run in cloud environments, underlining how far the SMB software market has moved beyond on-premise infrastructure. The model removes up-front server spending and lets firms add or drop capacity as demand swings. Microsoft’s decision to widen Copilot access shows how cloud also opens the AI door to firms lacking data-science teams[1]Source: Microsoft, “Copilot expansion brings AI assistance to more businesses,” microsoft.com. Providers are further sweetening migration with fixed-fee bundles that package storage, backup, and support. North American and European SMBs remain in front, yet cost-sensitive Asian firms are catching up as local hyperscale data-centers cut latency and pricing.

Surge in low-code/no-code development tools

Developer shortages push SMBs toward platforms that let non-coders build apps with drag-and-drop blocks. Nearly one-half of surveyed firms have already deployed at least one low-code tool, while 56% plan heavier use within two years. Microsoft reports that Power Apps can lower app-build cost by 74% versus traditional coding[2]Source: Microsoft, “Power Apps Total Economic Impact study,” microsoft.com. The approach lets a retailer spin up an inventory dashboard in days or a clinic create appointment scheduling without writing a line of JavaScript. North American uptake is strongest, but European compliance and Asian mobile-first priorities spark similar demand.

Proliferation of vertical SaaS bundles for SMBs

Vendors now ship “operating systems” tailor-made for retail, hospitality, or construction instead of isolated modules. A restaurant package may fold in reservations, payroll, and payment processing, sparing owners the burden of knitting separate tools. Mastercard’s tie-up with Unipaas to embed payments inside vertical SaaS confirms the direction. Unified suites cut integration headaches, a pain point cited by 66% of small firms, and unlock cross-selling upside for providers.

Rise of embedded fintech features in core apps

Cash-flow visibility ranks top of mind for owners, so ERP and POS platforms now tuck in invoicing, lending, and BNPL workflows. Toast’s industry-specific stack bundles payments, payroll, and working-capital advances inside its restaurant cloud, boosting average revenue per user. The SMB software market stands to gain because financial stickiness reduces customer churn and fuels usage fees. Asia-Pacific leads early adoption as super-apps blur lines between banking and software, though U.S. vendors quickly follow suit.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Open-source and freemium alternatives | -1.4% | Global, strongest impact in cost-sensitive markets | Medium term (2-4 years) |

| Integration complexity across disparate apps | -1.1% | Global, particularly affecting multi-system environments | Short term (≤ 2 years) |

| SMB cybersecurity skills gap | -0.8% | Global, most acute in developing markets | Long term (≥ 4 years) |

| Inflation-driven IT budget compression | -0.6% | Global, varying by regional economic conditions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Open-source and freemium alternatives

Cost-conscious firms often eye open-source ERP or CRM to dodge licence fees. Odoo, for example, has gained traction among micro-retailers. Yet hidden implementation labour and the need for self-support erode headline savings. Commercial vendors respond by bundling 24/7 help-desks and one-click upgrades, easing total cost-of-ownership comparisons. As economic cycles tighten purse strings, the price debate re-enters boardrooms and weighs on premium subscription growth, especially in emerging markets where DIY culture is strong.

Integration complexity across disparate apps

SMBs now juggle an average of nine cloud tools, and data silos invite manual re-entry, errors, and compliance risk. An online seller may need CRM, e-commerce, accounting, marketing automation, and support software to talk to each other. Middleware connectors and iPaaS platforms have emerged, but configuration still demands skills that few small firms possess. Vendors that deliver native integrations or offer flat-fee implementation can win, while those needing custom code face longer sales cycles and higher churn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud infrastructure drives digital transformation

Cloud held 72.56% of the SMB software market in 2025 and is forecast to rise at 16.92% CAGR through 2031. The SMB software market size for cloud deployments is therefore set to widen far faster than on-premise sales, which linger among highly regulated health and finance users. Cloud’s lower entry cost, instant scalability, and embedded security controls resonate with owners who prefer subscriptions over hardware. Edge locations and regional data zones address sovereignty worries, while zero-trust frameworks ease audits.

The shift is further propelled by AI features that demand GPU power beyond most local servers. Microsoft Copilot Studio, priced at USD 200 per 25,000 messages, underscores how cloud democratises advanced tools Microsoft. Telcos such as T-Mobile bundle 5G, VoIP, and SaaS, letting micro-firms modernise in a single invoice T-Mobile. Hybrid models persist, yet the trajectory is firmly cloud-first, cementing the SMB software market leadership of hosted solutions.

By Enterprise Size: SMEs steer market expansion

SMEs accounted for 47.20% revenue in 2025 and will add 12.42% CAGR, outpacing large-enterprise peers. That share translates to the largest single slice of the SMB software market size and reflects a mindset shift: software is no longer discretionary. Agile decision hierarchies let these firms pilot and scale tools in weeks instead of quarters. Financing options such as monthly SaaS fees and revenue-based lending reduce adoption friction.

Large enterprises seek incremental gains through integration and analytics, so their purchases skew to complex suites with slower growth. Meanwhile SMEs snap up turnkey apps that can be live by Monday morning. Analyst surveys show 70% of new SME apps will rely on low-code by 2025, double the share in 2023. That appetite sustains the wider SMB software market through the decade.

By Function/Application: Security solutions head growth table

Accounting and finance retained 26.30% of SMB software market share in 2025 thanks to compulsory reporting and tax compliance. Yet security and compliance tools now post the swiftest 15.98% CAGR, a sign that rising breach costs push owners to act. Over 96% of firms admit lacking full cyber expertise, and the average ransomware hit locks systems for six days. Automated endpoint detection, MFA, and zero-trust suites top shopping lists.

Bookkeeping suites themselves evolve. Embedded expense scanning and real-time cash-flow dashboards shave processing time by 35% and cut costs by 75%. CRM, project collaboration, and HR software also maintain robust growth as hybrid work cements remote collaboration standards in the SMB software market.

By End-user Industry: Healthcare races ahead

Retail and e-commerce held 22.50% revenue in 2025, yet healthcare will grow the fastest at 15.08% CAGR. Telehealth adoption, electronic medical record mandates, and strict privacy rules force clinics to modernise. Average breach fines in healthcare exceed USD 9 million, so cloud security and compliance modules see brisk demand.

Retailers focus on unified commerce: POS terminals now merge inventory, loyalty programmes, and online catalogues in a single screen. Manufacturing adopts SaaS ERP to automate procurement and scheduling, achieving lead-time cuts as high as 84% in case studies. Each vertical’s push feeds the overall SMB software market run-rate.

Geography Analysis

Asia-Pacific’s SMB software market value has more than doubled in four years and now records the highest 15.35% CAGR outlook. The SMB software market size expansion stems from digital-maturity programmes in India, Indonesia, and Vietnam that subsidise cloud credits, cybersecurity audits, and ERP training. Telcos package broadband with software suites, cutting the need for channel partners. Local language interfaces and mobile-first design lower adoption barriers for micro-retailers that run operations entirely on smartphones. Meanwhile, regional data centres opened by hyperscalers have eased latency and compliance constraints.

North America remains the revenue leader with 39.60% share in 2025. High cloud penetration, a vibrant startup ecosystem, and aggressive AI rollouts keep spending robust. Yet the growth slope is flatter than in Asia-Pacific because the market is nearer to saturation. North American SMBs focus on optimisation: integrating disparate tools, adopting predictive analytics, and layering security across hybrid workforces. Public-private cyber-grants encourage zero-trust migrations, pushing security spending ahead of collaboration suites.

Europe delivers steady mid-single-digit growth as legal directives make digital invoices and data-privacy audits obligatory. Funding programmes such as the European Union Digital Innovation Hubs give small manufacturers vouchers to test ERP and AI before purchase. The region’s large base of micro-businesses—90% of European Union firms have fewer than ten employees—still relies on spreadsheets, so the addressable SMB software market remains considerable. However, energy inflation and economic uncertainty temper immediate spending plans, leading vendors to roll out flexible monthly billing and consumption-based pricing.

Competitive Landscape

The SMB software market shows moderate concentration. Microsoft, Intuit, Oracle, and SAP together hold a sizeable but not dominant slice, while a long tail of vertical or function-specific specialists expands share each year. Microsoft extends its advantage by embedding Copilot across Office, Dynamics, and Azure, courting owners who want AI without complexity. Intuit deepens small-business stickiness by linking QuickBooks data to credit underwriting, offering same-day capital advances. Oracle shrinks onboarding friction with guided setup wizards aimed at firms under 500 staff. SAP refines its Business One cloud with industry templates that shave implementation to weeks.

Challengers focus on simplicity and transparent pricing. Zoho bundles 55+ apps under one subscription, while Freshworks leans on an easy UI and rapid deployment to win support-desk deals. HubSpot offers free CRM modules that convert into paid plans as firms scale. Open-source providers such as Odoo find traction among budget-focused users but often cede ground when customers hit integration roadblocks.

Ecosystem partnerships intensify. T-Mobile teams with Dialpad to bundle 5G connectivity and AI voice for micro-retailers. Mastercard invests in embedded payments to sit inside vertical SaaS rather than remain a detached processor. Telcos in Europe and Middle East and Africa replicate the model, pairing fibre with HR or accounting portals. The result is a layered competitive field where infrastructure providers become software resellers and software firms offer financial services, reinforcing moderate but not high concentration in the SMB software market.

SMB Software Industry Leaders

Intuit Inc.

Microsoft Corp

Oracle Corp

SAP SE

Sage Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Microsoft unveiled streamlined Azure Solutions Partner paths designed for SMB system integrators, with an emphasis on AI services and cloud migrations.

- April 2025: Mastercard joined forces with Unipaas to embed payments inside vertical SaaS platforms, easing checkout and reconciliation for SMB clients.

- November 2024: NTT DATA Business Solutions accelerated its cloud adoption initiative for SMBs, promising faster go-lives and lower total cost

- March 2025: Redesign Health highlighted a USD 23 billion opportunity for AI-driven cybersecurity tools aimed at healthcare SMBs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysis defines the small-and-medium business (SMB) software market as all licensed or subscription-based application programs, including accounting, customer engagement, collaboration, payroll, security, and allied vertical SaaS, that are purpose-built for firms below 1,000 employees and sold on a stand-alone basis or bundled through cloud marketplaces.

Scope exclusion: infrastructure services, middleware, and hardware devices that support software execution are expressly left outside this market.

Segmentation Overview

- By Deployment Type

- Cloud

- On-Premise

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Function / Application

- Accounting and Finance

- Customer Relationship Management (CRM)

- Project and Collaboration

- HR and Payroll

- Security and Compliance

- Others (ERP, e-Commerce, etc.)

- By End-user Industry

- BFSI

- Healthcare

- Retail and e-Commerce

- Manufacturing

- IT and Telecom

- Professional Services

- Education

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- GCC

- Israel

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed product heads at regional SaaS providers, cloud resellers, and digital-first SMEs spanning North America, Europe, Asia-Pacific, and Latin America. These conversations clarified average contract values, module attach rates, and the pace at which paper-based workflows are moving to subscription tools, enabling us to refine model inputs gathered during desk work.

Desk Research

We began with foundational datasets from the US Small Business Administration, Eurostat's structural business statistics, the OECD SME finance scoreboard, and India's Ministry of Corporate Affairs, which map active firm counts and digital adoption ratios across regions. Trade association portals such as the Cloud Industry Forum and the National Retail Federation offered spend benchmarks, while peer-reviewed journals in the Journal of Small Business Management provided churn and payback insights. Our team also extracted recent revenue splits from listed SaaS vendors through SEC 10-Ks and investor decks, and sifted fast-moving news on partnerships via Dow Jones Factiva and company intelligence through D&B Hoovers. This list is illustrative; dozens of additional public and proprietary sources were referenced to validate figures and assumptions.

Market-Sizing & Forecasting

A top-down construct starts with the active SME base in each country, adjusts for cloud readiness, and multiplies the addressable firm pool by verified average software spend per employee. Results are sense-checked through selective bottom-up roll-ups of leading vendor revenues and sampled ASP × user counts. Key variables like new business registrations, VC funding into vertical SaaS, broadband penetration, average seat-based pricing, and churn-down upgrades inform annual snapshots. Multivariate regression, supported by expert consensus on GDP and hiring trends, projects demand to 2030. Gaps in bottom-up coverage are bridged with proximity ratios from adjacent segments before final reconciliation.

Data Validation & Update Cycle

We layer three-step variance checks, peer review, and exception re-runs before sign-off. Reports refresh every twelve months, with mid-cycle updates triggered when material events, such as large acquisitions, regulatory shifts, or abrupt price moves, shift our baseline, ensuring clients receive our freshest outlook.

Why Mordor's SMB Software Baseline Commands Reliability

Published estimates often diverge because firms pick different functional baskets, employee caps, currency years, and refresh cadences.

Key gap drivers include narrower scope that omits security and compliance suites or, at the other extreme, the inclusion of broader IT spending. Some publishers also annualize multi-year contracts without deflation, while a few rely on single-region samples and static exchange rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 72.35 B (2025) | Mordor Intelligence | - |

| USD 69.32 B (2024) | Global Consultancy A | Excludes security & compliance modules and vertical SaaS add-ons |

| USD 171.80 B (2024) | Industry Journal B | Bundles hardware support and IT services, inflates totals through undiscounted multi-year contracts |

Taken together, the comparison shows that Mordor Intelligence strikes a balanced midpoint, comprehensive in module coverage yet disciplined on spend categories, giving decision-makers a transparent, repeatable baseline they can confidently plug into strategic plans.

Key Questions Answered in the Report

What is the current value of the SMB software market?

The market is valued at USD 77.33 billion in 2026 and is projected to reach USD 107.86 billion by 2031.

Which deployment model is growing fastest?

Cloud-based solutions command 72.56% share and are advancing at a brisk 16.92% CAGR as firms favor subscription pricing and scalability.

Why is security software seeing sharp growth?

SMBs face rising cyberattacks and regulatory fines; security and compliance tools are therefore expanding at 15.98% CAGR, the fastest among functional segments.

Which region delivers the strongest growth?

Asia-Pacific posts the highest 15.35% CAGR, helped by government digital-adoption schemes and expanding cloud infrastructure.

Who are the major vendors?

Key players include Microsoft, Intuit, Oracle, SAP, along with SMB-focused specialists such as Zoho, Freshworks, and HubSpot.

How concentrated is the SMB software market?

The market is moderately concentrated, with no single vendor exceeding half of total revenue and a vibrant ecosystem of niche suppliers.

Page last updated on: