Smart Retinal Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.67 Million |

| Market Size (2031) | USD 51.89 Million |

| Growth Rate (2026 - 2031) | 13.40% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

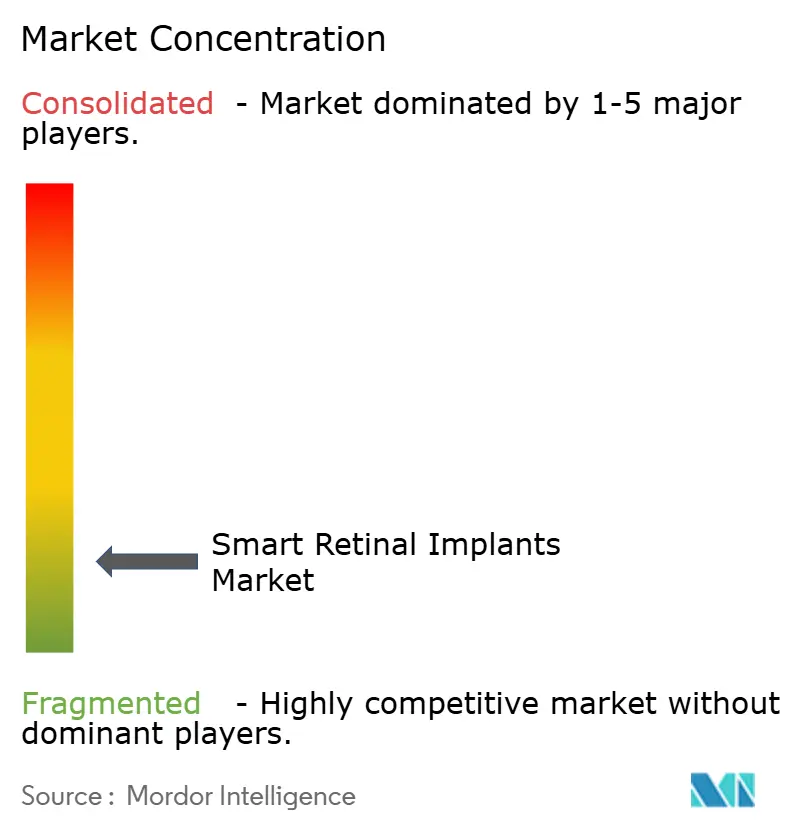

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Retinal Implants Market Analysis by Mordor Intelligence

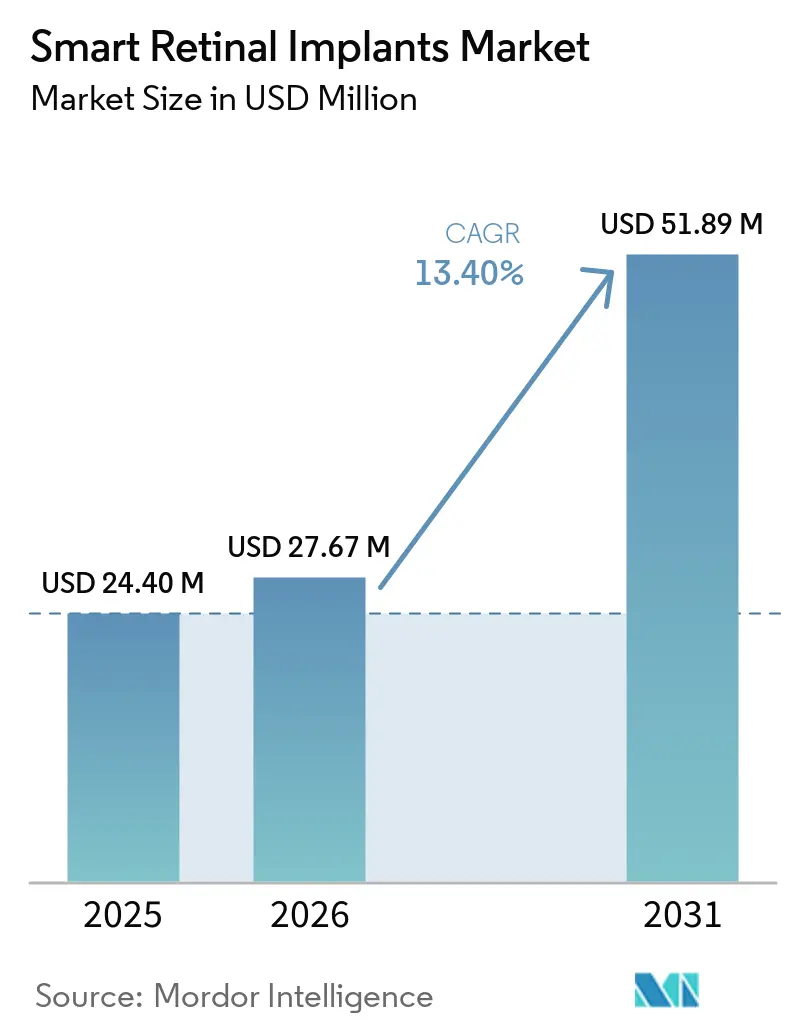

The Smart Retinal Implants Market size is expected to grow from USD 24.40 million in 2025 to USD 27.67 million in 2026 and is forecast to reach USD 51.89 million by 2031 at 13.40% CAGR over 2026-2031.

The smart retinal implants market is advancing due to stronger clinical validation, compact implant designs, and improved wireless power transfer. The October 2025 PRIMAvera publication strengthened the clinical foundation of the category and boosted confidence in regulatory progress for next-generation systems.[1]Science Corporation, “Science Submits CE Mark Application for PRIMA Retinal Implant,” Neurofounders, neurofounders.co Additionally, closer integration of implant hardware, external optics, and software is enhancing visual output post-implantation. Regulatory support in the United States and Europe is expediting development programs, though reimbursement uncertainties and concerns over long-term packaging reliability continue to limit the transition from trials to widespread commercial adoption. The market is also shaped by a limited number of specialized surgical centers, providing early leaders with advantages in clinical execution, physician training, and initial commercialization.

Key Report Takeaways

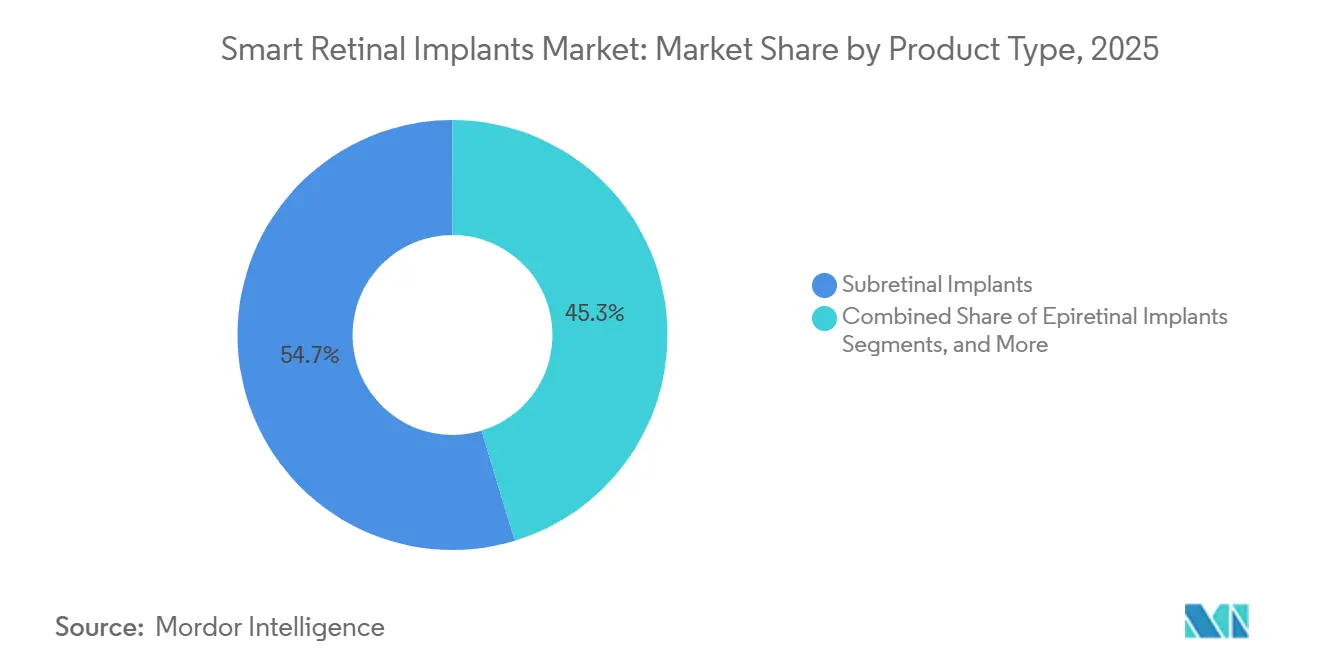

- By product type, subretinal implants accounted for 54.66% of the smart retinal implants market size in 2025, while cortical visual prostheses are forecast to grow at a 14.20% CAGR through 2031.

- By implant platform, wired systems held 61.53% of revenue in 2025, while wireless systems are projected to record the highest CAGR at 15.15% through 2031.

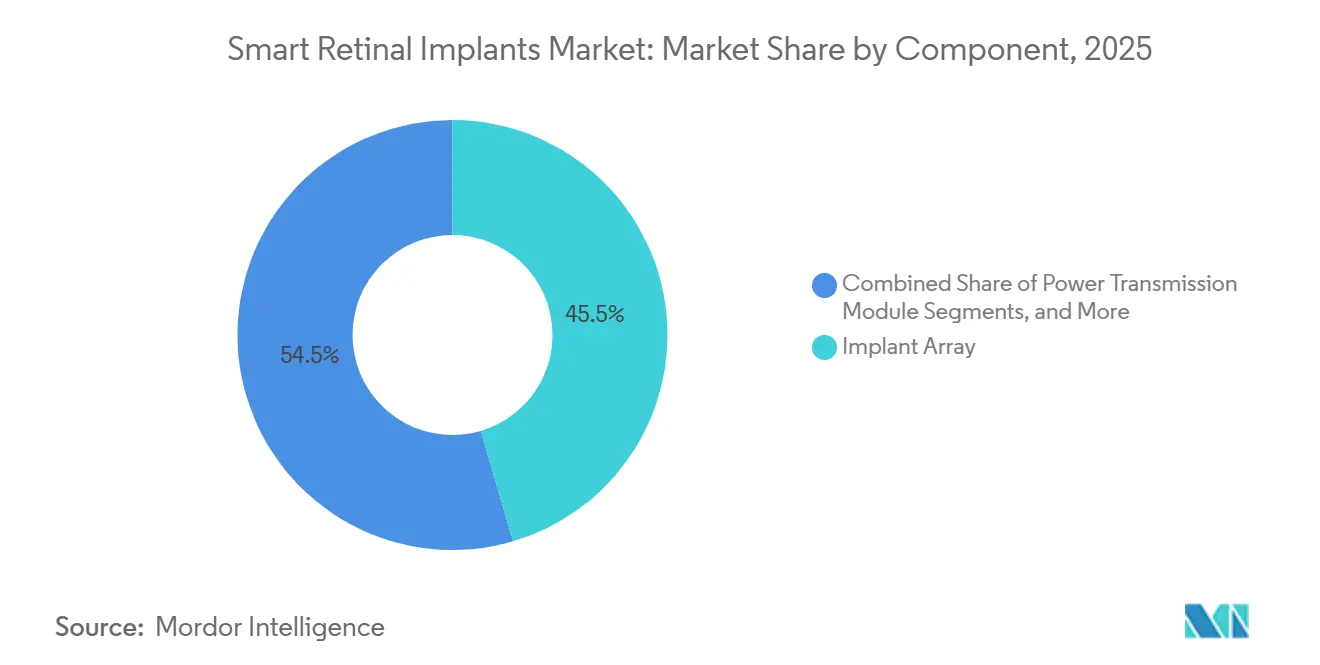

- By component, implant arrays represented 45.45% of revenue in 2025, while processing units are forecast to grow at a 14.45% CAGR through 2031.

- By disease indication, retinitis pigmentosa accounted for 65.45% of revenue in 2025, while geographic atrophy is projected to expand at a 13.90% CAGR through 2031.

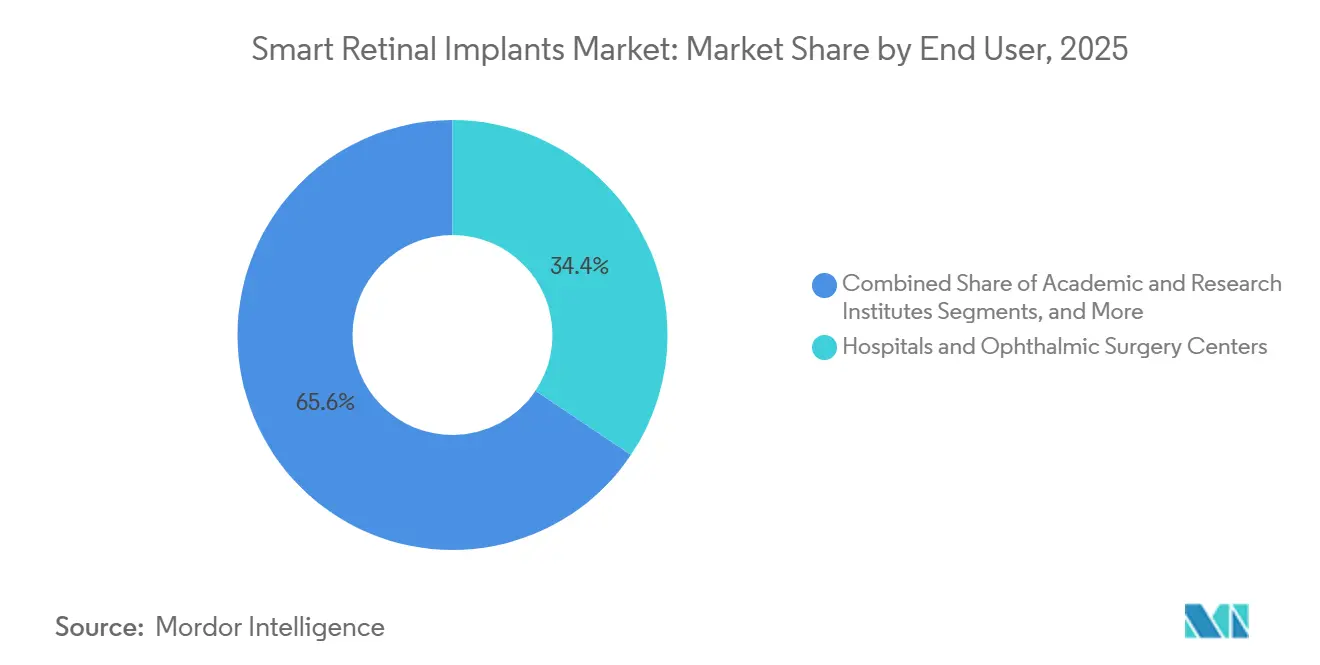

- By end user, hospitals and ophthalmic surgery centers held 34.44% of revenue in 2025, while academic and research institutes are projected to grow at a 15.33% CAGR through 2031.

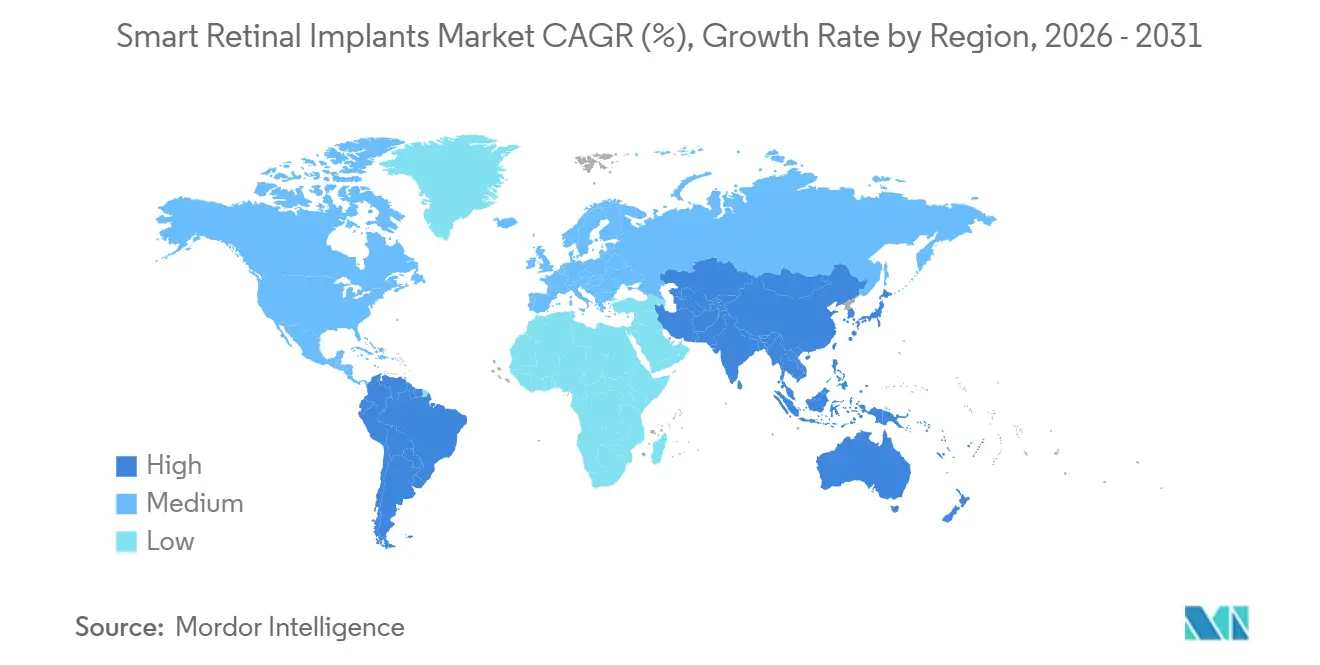

- By geography, North America held 40.65% of the smart retinal implants market share in 2025, while Asia-Pacific is projected to expand at a 15.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Retinal Implants Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising clinical validation for vision restoration | +3.2% | Global, with early traction in North America and Western Europe | Short term (≤ 2 years) |

| Expanding addressable population in geographic atrophy and retinitis pigmentosa | +2.8% | Global, especially North America, Europe, and Japan | Medium term (2-4 years) |

| Convergence of miniaturized electronics and wireless power transfer | +2.5% | Asia-Pacific core, with spillover into North America and Europe | Medium term (2-4 years) |

| Post-implant rehabilitation and digital vision training | +1.5% | North America and Europe | Long term (≥ 4 years) |

| Breakthrough device and accelerated regulatory pathways | +2.1% | United States and Europe | Short term (≤ 2 years) |

| Precision-targeted retinal stimulation and AI-assisted scene encoding | +1.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Clinical Validation for Vision Restoration

The PRIMAvera study has significantly strengthened the clinical foundation of the smart retinal implants market. Published in October 2025, the trial demonstrated that 80% of patients with geographic atrophy achieved meaningful visual acuity improvements after 12 months.[2]Nanoscope Therapeutics, “Nanoscope Therapeutics Initiates Rolling Submission of Biologics License Application to FDA for MCO-010,” Nanoscope Therapeutics, nanostherapeutics.com This shift enables evaluations based on real patient outcomes rather than engineering potential. Furthermore, these results have advanced discussions from feasibility to approval and market readiness in Europe, where Science Corporation submitted its CE Mark application in 2025. The market is also gaining validation across multiple technical paths, as Cortigent's 6-year Orion feasibility data from January 2026 showed less than 4% electrode loss and improved visual function in all 6 subjects. This diversification of clinical evidence has increased confidence among surgeons, regulators, and investors.

Expanding Addressable Population With Geographic Atrophy and Retinitis Pigmentosa

The smart retinal implants market benefits from a large patient base, particularly in geographic atrophy and retinitis pigmentosa, where durable vision restoration options remain limited. Geographic atrophy affects millions globally, while retinitis pigmentosa impacts an additional 1.5 to 2 million people, ensuring sustained demand even with a gradual commercial rollout. The PRIMA platform has expanded its focus through a new clinical study targeting patients with photoreceptor degeneration, including retinitis pigmentosa and Stargardt-related vision loss. Japan's STS Phase 3 program, launched in September 2025, highlights growing institutional support for retinal implant development in Asia, which is critical for future market expansion. While optogenetics is advancing in retinitis pigmentosa, the diverse clinical needs across disease stages and retinal structures ensure continued demand for implants.

Convergence of Miniaturized Electronics and Wireless Power Transfer

The transition to compact, cable-free systems is a key growth driver for the smart retinal implants market. Science Corporation's PRIMA platform uses pulsed near-infrared light to transmit power and stimulation data, eliminating transcutaneous cables and reducing physical burdens associated with older designs. Advances in pixel technology are also enhancing wireless systems, with amorphous silicon resistors reducing pixel pitch from 100 µm to 22 µm, enabling higher visual resolution without compromising wireless architecture. Additionally, LambdaVision secured USD 7 million in seed funding in November 2025 to advance its protein-based retinal implant platform and scale-up efforts, showcasing alternative manufacturing approaches.

Precision-Targeted Retinal Stimulation and AI-Assisted Scene Encoding

Software advancements in converting visual scenes into effective stimulation patterns are shaping the smart retinal implants market. Post-implant vision quality depends on both electrode count and the system's ability to map images to surviving retinal or cortical pathways. Science Corporation's integration of implant hardware with augmented reality glasses reflects a shift toward integrated hardware-software systems. Similarly, Japan's KAKENHI-backed 3D chiplet artificial retina program is developing a wide-field implant architecture with machine-learning-based scene processing. These innovations enable software-driven performance upgrades post-implant, improving patient outcomes without requiring additional surgeries.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited visual acuity gains versus surgical and device complexity | -1.6% | Global | Short term (≤ 2 years) |

| High procedure cost and unclear reimbursement pathways | -2.0% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Long-term biocompatibility, packaging, and hermeticity risks | -1.4% | Global | Long term (≥ 4 years) |

| Small eligible patient pool and dependence on specialized surgical centers | -1.2% | Global, with greater impact in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Visual Acuity Gains Versus Surgical and Device Complexity

The smart retinal implants market has achieved significant clinical advancements, but a gap remains between these improvements and their application in daily visual functions. The PRIMAvera study demonstrated progress in visual acuity; however, many patients still could not achieve independence in tasks like reading, face recognition, or navigation. The trial reported 26 serious adverse events among 38 participants, with 95% resolving within two months, highlighting challenges in broader adoption.[3]Japan Registry of Clinical Trials, “jRCT2052250192, Clinical Trial of Artificial Retina System Using STS Method for Advanced Outer-Layer Retinal Degeneration,” Japan Registry of Clinical Trials, nanbyo-chiken.nibn.go.jp Additionally, the implantation process requires specialized vitreoretinal or neurosurgical expertise, which is not widely available, slowing the transition from clinical trials to routine care.

High Procedure Cost and Unclear Reimbursement Pathways

The high cost of smart retinal implants remains a significant barrier, as expenses extend beyond the device to include operating room time, anesthesia, imaging, follow-up care, and visual rehabilitation. The Argus II set a high benchmark for procedure costs, and next-generation wireless systems are unlikely to be cost-effective due to complex fabrication and low production volumes. Reimbursement pathways remain unclear in Europe and Japan, creating a lag where clinical acceptance may outpace payment approvals. As a result, the market relies on a limited number of institutions capable of supporting trials, specialized care, and patient training while reimbursement challenges persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Subretinal Devices Lead While Cortical Prostheses Expand Their Role

In 2025, subretinal implants captured 54.66% of the smart retinal implants market, solidifying their top position. Their advantage lies in their placement beneath the retina, enabling direct stimulation of intact bipolar cells and offering superior visual fidelity compared to many surface-mounted designs. The PRIMA system stands out in this segment, with its October 2025 publication bolstering subretinal technology's clinical credibility. As a result, the market views subretinal systems as the most promising avenue for treating patients with geographic atrophy and related degenerations.

While epiretinal systems played a pivotal role in the field's early clinical history, they no longer steer the course of new developments. Suprachoroidal implants are gaining traction as a less risky surgical alternative, with a second-generation 44-channel device boasting 97% electrode functionality after 2.7 years, as reported in a 2025 feasibility study. Meanwhile, cortical visual prostheses are on a rapid ascent, projected to grow at a 14.20% CAGR through 2031. Their broader appeal stems from their ability to cater to patients unsuitable for retinal implants, including those with optic nerve damage or advanced retinal diseases.

By Implant Platform: Wireless Designs Gain Momentum While Wired Systems Hold the Legacy Base

In 2025, wired systems commanded 61.53% of the revenue, a testament to the enduring influence of earlier implant programs and design choices. However, this dominance is more historical than strategic. Most recent advancements in the smart retinal implants market have pivoted towards wireless and hybrid systems. While wired architectures offer familiar engineering pathways and stable transmission, their reliance on cables and external hardware complicates surgery, patient comfort, and MRI compatibility over time. Consequently, while the wired base remains relevant in the near term, it isn't setting the pace for future designs.

Wireless systems are on a trajectory to grow at a 15.15% CAGR through 2031, marking them as the fastest-growing platform in the smart retinal implants arena. The PRIMA system exemplifies this trend, utilizing near-infrared light for power and data transmission, thereby eliminating the need for a transcutaneous cable. This innovation significantly enhances both patient experience and surgical ease. Furthermore, a 2026 technical study highlighted the potential of photovoltaic arrays to downsize pixels without compromising wireless functionality, bolstering the platform's long-term prospects.

By Component: Implant Arrays Anchor Current Revenue While Processing Units Scale Faster

In 2025, implant arrays accounted for 45.45% of the revenue, solidifying their status as the leading component in the smart retinal implants market. Their prominence stems from the technical precision required in electrode fabrication, stringent biocompatibility controls, and the need for consistent manufacturing. External glasses and camera systems also play a crucial role, managing image capture, projection, and user interface tasks vital for the device's overall functionality. While power modules and surgical accessories contribute smaller shares, they are essential for follow-up care, replacements, and procedural use, bolstering the industry's commercial framework.

Processing units are set to grow at a 14.45% CAGR through 2031, marking them as the fastest-scaling component in the smart retinal implants market. Their rising significance is attributed to advancements that reduce latency, enable personalized stimulation, and facilitate software updates post-implantation. The KAKENHI-funded chiplet retina project in Japan underscores this trend, integrating machine-learning capabilities directly into the processing layer, rather than relegating software to a secondary role. This approach is commercially pivotal, as the industry stands to gain more from performance enhancements via software refinements alongside new hardware generations.

By Material: Established Metals and Polymers Hold the Base While Nanomaterials Move Up the Priority List

In the smart retinal implants market, biocompatible metals like platinum and titanium remain foundational. Their longstanding presence in implantable devices has made them familiar to regulators, engineers, and clinicians, especially concerning long-term biocompatibility. Polymers such as polyimide and parylene-C are crucial for their flexibility, which aligns better with retinal tissue and minimizes interface stress over time. Ceramics play a vital role in packaging, ensuring long-term enclosure integrity, a key factor for durable device performance.

Nanomaterials are emerging as a pivotal growth area in the materials design landscape for the smart retinal implants market. Their advantage lies in superior charge handling per unit area, enabling smaller electrode geometries and enhanced resolution without necessitating higher current loads. This positions them favorably in the industry's push for denser arrays and improved visual outputs. While the transition to widespread nanomaterial adoption won't be instantaneous, the strategic emphasis on materials is evident as developers strive to harmonize flexibility, conductivity, sealing reliability, and MRI compatibility within a single product architecture.

By Disease Indication: Retinitis Pigmentosa Keeps the Core Base While Geographic Atrophy Widens the Opportunity

In 2025, retinitis pigmentosa constituted 65.45% of the revenue, solidifying its position as the primary disease indication in the smart retinal implants market. This dominance is rooted in the historical development of retinal prostheses, including the inaugural FDA-approved device, which centered around this patient demographic. Such a foundation has endowed retinitis pigmentosa with a wealth of surgical experience, clinical documentation, and tailored program design. Consequently, the market's knowledge base and expertise have predominantly revolved around this condition, rather than age-related macular degeneration.

Geographic atrophy is on the rise, projected to expand at a 13.90% CAGR through 2031, making it the fastest-growing segment in the smart retinal implants market. The impetus behind this growth is the credible evidence from PRIMA, demonstrating that a subretinal device can enhance central vision for a patient demographic previously devoid of such an implant-based restoration avenue. Additionally, Science Corporation's recent study on photoreceptor degeneration patients signals a broader clinical strategy, moving beyond a singular indication focus.

By End User: Hospitals Hold the Current Base While Research Institutes Drive Near-Term Activity

In 2025, hospitals and ophthalmic surgery centers accounted for 34.44% of the revenue, establishing them as the predominant end-user group in the smart retinal implants market. This dominance is attributed to their access to operating rooms, advanced imaging, and post-procedure monitoring, all essential for successful implantation. Hospitals involved in trials are poised to remain key commercial reference centers, given their trained personnel, patient selection expertise, and familiarity with follow-up protocols. In essence, the market's reliance on a select few centers underscores the importance of integrating surgery, rehabilitation, and clinical study infrastructure.

Academic and research institutes are on a growth trajectory, projected to expand at a 15.33% CAGR through 2031, outpacing other end users in the smart retinal implants market. This surge is largely due to the current stage of the sector, where many device-patient interactions still transpire within clinical trials rather than through widespread reimbursement channels. Japan exemplifies this trend, with Osaka University's STS Phase 3 study and Tohoku University's chiplet project highlighting academic centers as both trial operators and development collaborators.

Geography Analysis

In 2025, North America dominated the smart retinal implants market, holding a 40.65% share. The United States led this growth due to its strong specialist capacity and supportive regulatory pathways, which advanced both retinal and cortical device programs. Science Corporation progressed its PRIMA program through U.S. regulatory channels in 2025, while Cortigent presented 6-year study data for its Orion program under Breakthrough Device status in January 2026. The region's concentrated network of implanting hospitals, device developers, and ophthalmic research centers further supports clinical enrollment and commercial readiness.

Europe remains the second-largest hub in the smart retinal implants market. The region played a key role in the PRIMAvera program, with an October 2025 publication strengthening the evidence package for European regulators and advancing the CE Mark review. Germany, France, and the UK stand out for their combination of specialist retinal surgery and academic trial participation. Europe is also a critical launch region, as successful approval could establish a structured commercial pathway, despite slower reimbursement timelines.

Asia-Pacific is projected to grow at a 15.44% CAGR through 2031, making it the fastest-growing region in the smart retinal implants market. Japan drives this growth with its aging population and advancements in suprachoroidal systems and wide-field chiplet implants. Osaka University initiated its STS Phase 3 trial in September 2025, while Tohoku University is advancing a government-backed 3D laminated artificial retina targeting a 160-degree visual field. The region also benefits from Australia's suprachoroidal prosthesis program, expanding its innovation base. South America and the Middle East and Africa currently contribute less revenue but are expected to grow as retinal disease prevalence rises and ophthalmic infrastructure improves.

Competitive Landscape

Clinical programs, rather than widespread commercial sales, predominantly shape the fragmented smart retinal implants market. No single company dominates the commercial landscape, with most players focused on validating safety, efficacy, durability, or manufacturability before achieving significant revenue scaling. Science Corporation edges closer to market leadership, having advanced its PRIMA device through a pivotal European study, submitted a CE Mark application in 2025, and unveiled a new study broadening the device's indications. This combination of clinical validation and regulatory progress positions Science Corporation as a frontrunner in the smart retinal implants market.

Cortigent adopts a distinct strategy, centering its growth on cortical access rather than solely on retinal placement. An update from January 2026 highlighted enhanced visual function in all six subjects of the Orion study and a mere 4% electrode loss over six years, reinforcing the durability of this approach. LambdaVision differentiates itself with a protein-based artificial retina and a manufacturing process tied to microgravity. The company secured USD 7 million in seed funding in November 2025 and received a NASA Phase 2 InSPA award in September 2025, reflecting strong investor and institutional support despite its early development stage.

Competition is intensifying as companies position themselves within the broader eye care and neurostimulation ecosystem. Smaller developers leverage pivotal studies, Breakthrough Device status, and specialized center partnerships to build value, while larger ophthalmic firms focus on integrating implants with existing surgical platforms and service networks. A significant gap remains in adaptive post-implant software, rehabilitation support, and surgeon-enabling tools, which are critical for long-term success. Companies that align implant performance with surgeon workflows and patient training are likely to gain a competitive edge over those focusing solely on hardware.

Smart Retinal Implants Industry Leaders

Pixium Vision SA

Retina Implant AG

Nano Retina Ltd.

Bionic Vision Technologies Pty Ltd

iBionics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: i-Lumen Scientific received FDA IDE approval to begin U.S. enrollment for the 120-participant i-SIGHT2 pivotal study on intermediate-to-advanced dry AMD, introducing a parallel device program targeting the same patient pool.

- February 2026: SparingVision completed dosing in the Phase 1/2 PRODYGY study of SPVN06 for retinitis pigmentosa, enrolling 33 patients, and received positive FDA feedback for a Phase 2 geographic atrophy expansion.

- January 2026: Cortigent presented 6-year Orion feasibility data at NANS 2026, showing improved visual function in all 6 subjects with electrode loss below 4%, and announced plans to discuss a larger pivotal trial with the FDA.

- November 2025: LambdaVision raised USD 7 million in seed funding to extend operations into 2027 and support preclinical work and scaling of its protein-based artificial retina platform for retinitis pigmentosa and AMD.

- October 2025: PRIMAvera results showed 80% of 38 geographic atrophy patients achieved significant visual acuity improvement at 12 months, while Science Corporation submitted its CE Mark application.

Global Smart Retinal Implants Market Report Scope

As per the scope of the report, smart retinal implants, also known as "bionic eyes," are advanced bioelectronic devices surgically implanted to restore sight to individuals blinded by degenerative retinal diseases (like retinitis pigmentosa or macular degeneration). They replace damaged photoreceptors by converting visual input into electrical signals that stimulate the surviving retinal cells.

The smart retinal implants market is segmented by product type, implant platform, component, material, disease indication, end-user, and geography. By product type, the market includes epiretinal implants, subretinal implants, suprachoroidal implants, and cortical visual prostheses. By implant platform, the market is segmented into wired systems, wireless systems, and hybrid systems. By component, the market is categorized into implant array, external glasses and camera system, processing unit, power transmission module, and surgical accessories and tools. By material, the market includes biocompatible metals (platinum, titanium), polymers (polyimide, silicone), ceramics, nanomaterials (graphene, carbon nanotubes), and hybrid materials. By disease indication, the market is segmented into retinitis pigmentosa, geographic atrophy due to age-related macular degeneration, and other degenerative retinal disorders. By end-user, the market is categorized into hospitals and ophthalmic surgery centers, specialty eye clinics, and academic and research institutes. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Epiretinal Implants |

| Subretinal Implants |

| Suprachoroidal Implants |

| Cortical Visual Prostheses |

| Wired Systems |

| Wireless Systems |

| Hybrid Systems |

| Implant Array |

| External Glasses and Camera System |

| Processing Unit |

| Power Transmission Module |

| Surgical Accessories and Tools |

| Biocompatible Metals (Platinum, Titanium) |

| Polymers (Polyimide, Silicone) |

| Ceramics |

| Nanomaterials (Graphene, Carbon Nanotubes) |

| Hybrid Materials |

| Retinitis Pigmentosa |

| Geographic Atrophy Due to Age-Related Macular Degeneration |

| Other Degenerative Retinal Disorders |

| Hospitals and Ophthalmic Surgery Centers |

| Specialty Eye Clinics |

| Academic and Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Epiretinal Implants | |

| Subretinal Implants | ||

| Suprachoroidal Implants | ||

| Cortical Visual Prostheses | ||

| By Implant Platform | Wired Systems | |

| Wireless Systems | ||

| Hybrid Systems | ||

| By Component | Implant Array | |

| External Glasses and Camera System | ||

| Processing Unit | ||

| Power Transmission Module | ||

| Surgical Accessories and Tools | ||

| By Material | Biocompatible Metals (Platinum, Titanium) | |

| Polymers (Polyimide, Silicone) | ||

| Ceramics | ||

| Nanomaterials (Graphene, Carbon Nanotubes) | ||

| Hybrid Materials | ||

| By Disease Indication | Retinitis Pigmentosa | |

| Geographic Atrophy Due to Age-Related Macular Degeneration | ||

| Other Degenerative Retinal Disorders | ||

| By End User | Hospitals and Ophthalmic Surgery Centers | |

| Specialty Eye Clinics | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of smart retinal implants?

The smart retinal implants market size stands at USD 27.67 million in 2026 and is forecast to reach USD 51.89 million by 2031 at a 13.40% CAGR.

Which product type leads current revenue?

Subretinal implants lead with 54.66% of revenue in 2025 because they are the most clinically advanced route and have the strongest recent human data.

Which platform is growing the fastest?

Wireless systems are forecast to grow at a 15.15% CAGR through 2031 as developers move away from cable-based designs and improve pixel density in wireless architectures.

Why is geographic atrophy becoming more important for developers?

Geographic atrophy is projected to grow at a 13.90% CAGR because PRIMA showed meaningful central vision improvement in this population, which widened the addressable path beyond retinitis pigmentosa.

Which region is expanding the fastest?

Asia-Pacific is the fastest-growing region with a 15.44% CAGR through 2031, led by Japan's active trial and research programs.

Who currently has the strongest near-term commercial position?

Science Corporation appears closest to near-term leadership because it combined strong PRIMAvera data with a CE Mark application and a broader follow-on study path.

Page last updated on: