Vision Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 75.14 Billion |

| Market Size (2031) | USD 109.38 Billion |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

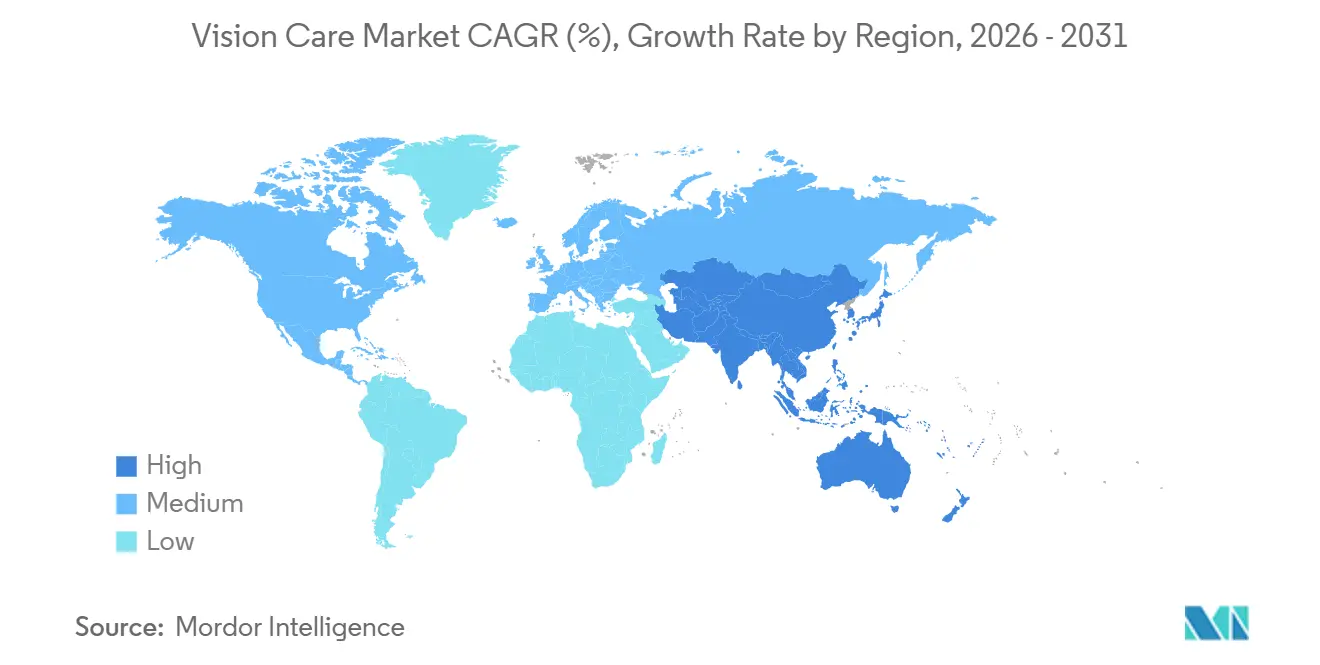

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

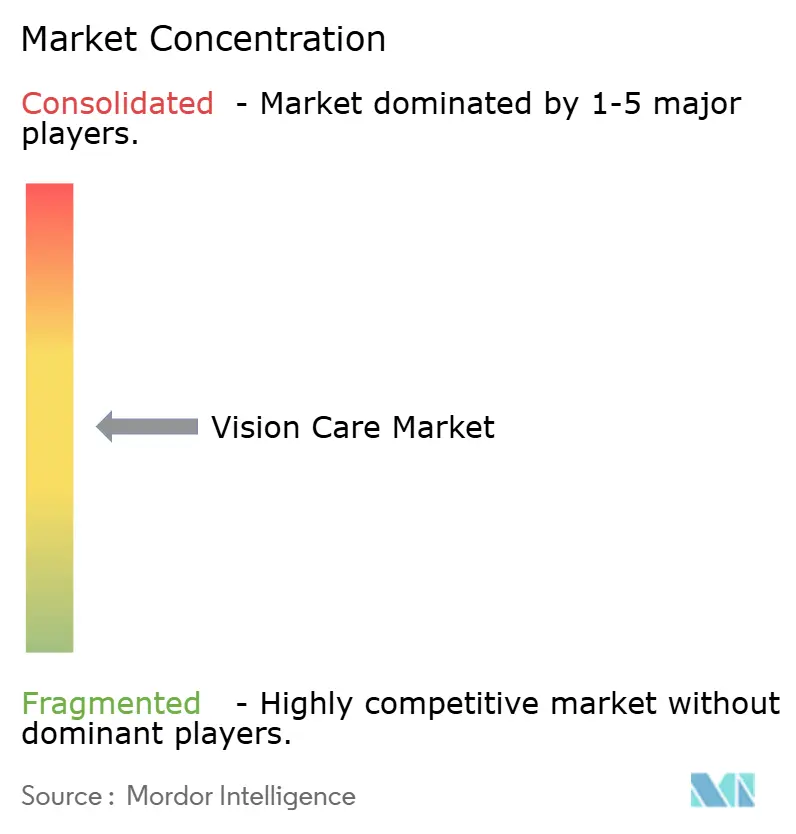

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vision Care Market Analysis by Mordor Intelligence

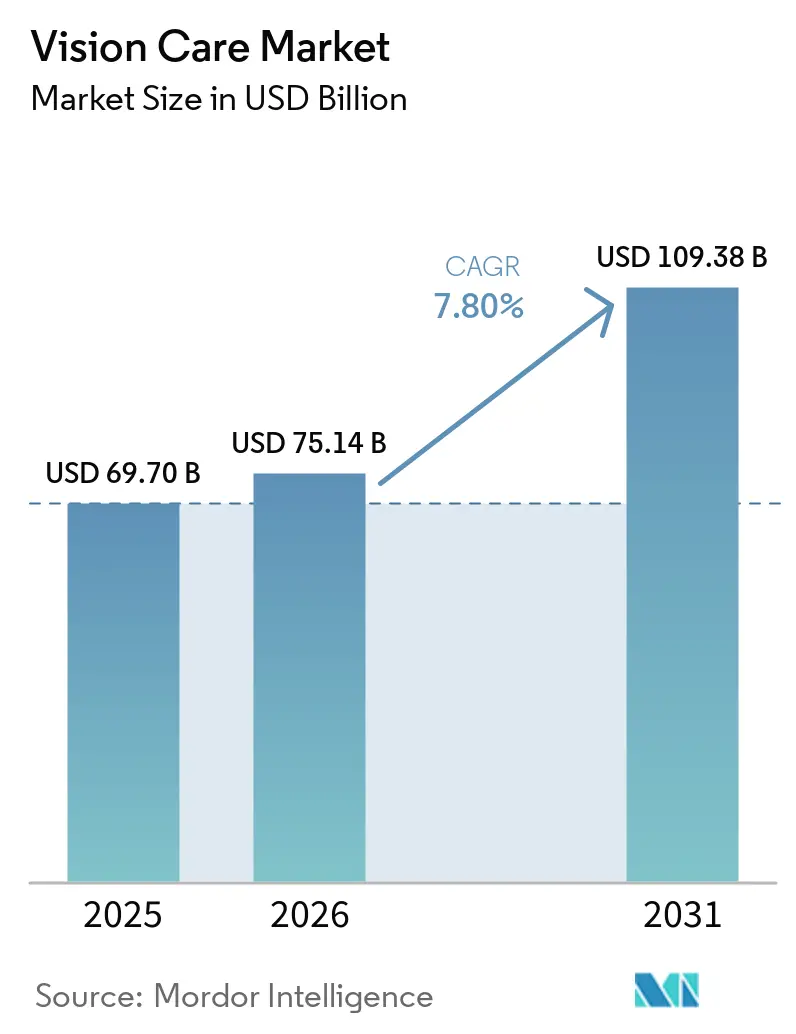

The Vision Care Market size was valued at USD 69.70 billion in 2025 and is estimated to grow from USD 75.14 billion in 2026 to reach USD 109.38 billion by 2031, at a CAGR of 7.80% during the forecast period (2026-2031).

The vision care market is evolving as providers and manufacturers adopt a medically integrated model, focusing on progression control, ocular disease management, and technology-driven diagnostics. This shift is driving higher revenue per patient, with premium myopia-control products, advanced intraocular lenses, and therapeutic eye care becoming key components of the treatment mix. Omnichannel retail is transforming the market, with digital platforms enhancing access for repeat purchases, while physical stores remain vital for first prescriptions and complex dispensing. North America leads the market, while Asia-Pacific is the fastest-growing region due to high myopia prevalence and expanded public screening programs.

Key Report Takeaways

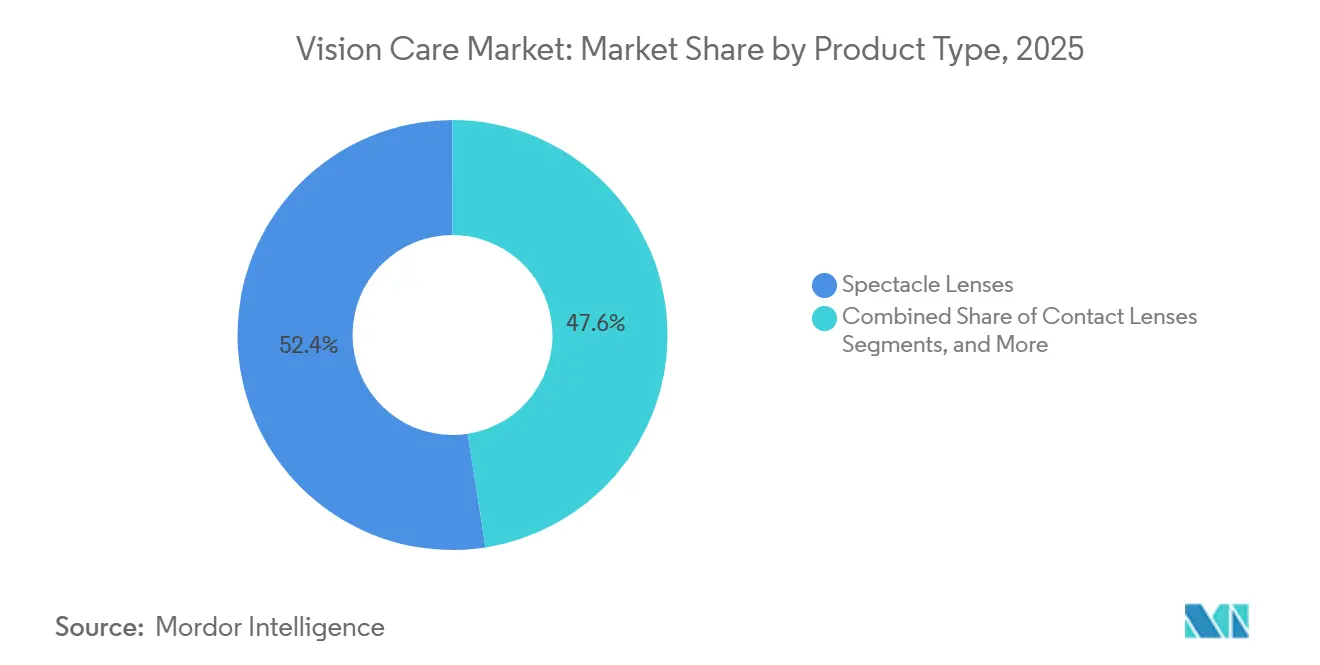

- By product type, spectacle lenses led with 52.45% share in 2025, while contact lenses are projected to expand at an 8.20% CAGR through 2031.

- By application, corrective vision care held 44.6% share in 2025, while therapeutic and disease management is projected to grow at a 9.10% CAGR through 2031.

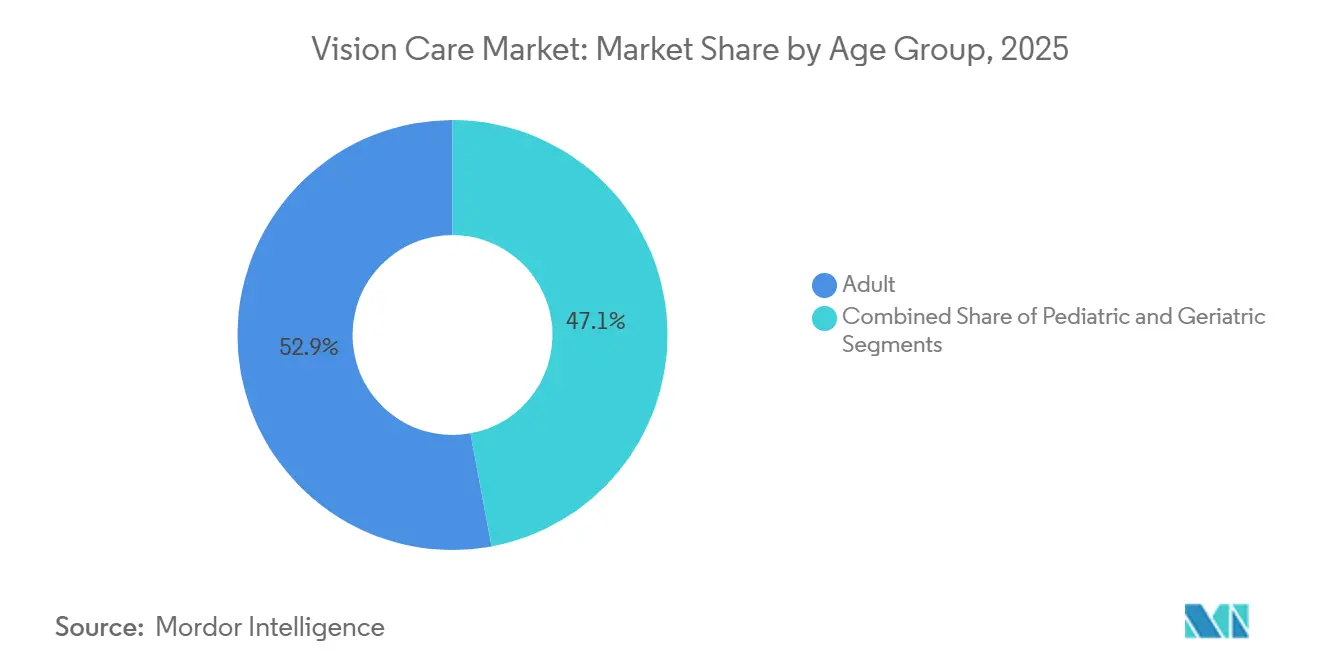

- By age group, adults accounted for 52.89% share in 2025, while the pediatric segment is projected to advance at a 7.98% CAGR through 2031.

- By distribution channel, optical retail stores and chains held 38.75% share in 2025, while e-commerce platforms are expected to grow at an 11.15% CAGR through 2031.

- By geography, North America held 44.67% of global revenue in 2025, while Asia-Pacific is projected to expand at a 10.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vision Care Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising refractive errors and myopia burden | +2.2% | Global, with highest intensity in APAC, including China, Japan, South Korea, and India | Long term (≥ 4 years) |

| Aging-driven demand for presbyopia and cataract care | +1.5% | Global, highest in Japan, Europe, and North America | Medium term (2-4 years) |

| Digital-eye-strain demand for premium lenses and coatings | +1.1% | North America, Europe, APAC core, with spillover to MEA | Short term (≤ 2 years) |

| Omnichannel optical retail and e-commerce expansion | +0.9% | North America and Europe, with rapid uptake in India and Southeast Asia | Medium term (2-4 years) |

| FDA-authorized pediatric myopia-control spectacles | +0.7% | North America, with spillover regulatory influence to EMEA and APAC | Short term (≤ 2 years) |

| Approved low-dose atropine broadens pediatric myopia management | +0.4% | Asia-Pacific and North America, with early gains in Australia and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Refractive Errors and Myopia Burden

The vision care market is experiencing growth due to the increasing prevalence of refractive errors, particularly myopia, among children and adolescents. A 2025 review highlighted that global myopia prevalence in this group reached 35.81% in 2023 and is projected to rise to 39.80% by 2050, affecting nearly 740 million individuals.[1]World Health Organization, “Eye Care, Vision Impairment and Blindness, Refractive Errors,” World Health Organization, who.int This trend is driving the market beyond single-vision correction toward products designed to slow myopia progression, enhancing value per patient. The FDA's approval of Essilor Stellest in 2025, the first spectacle lens in the U.S. to slow pediatric myopia progression, has expanded the addressable market. Additionally, China's focus on school-level myopia screenings continues to drive demand, particularly in East Asia, where prevalence rates are already high.

Aging-Driven Demand for Presbyopia and Cataract Care

The aging population is fueling demand for presbyopia correction, cataract surgeries, and improved postoperative vision, contributing to the vision care market's growth. Cataracts remain the leading cause of global blindness, with over 20 million surgeries performed annually, including 4.3 million in Europe and 3.8 million in the U.S.[2]Jinghong Liang et al., “Global Prevalence, Trend and Projection of Myopia in Children and Adolescents From 1990 to 2050, A Comprehensive Systematic Review and Meta-Analysis,” British Journal of Ophthalmology, bjo.bmj.com The market is seeing a shift toward premium intraocular lenses, which reduce spectacle dependence and generate out-of-pocket payments even in reimbursed systems. Alcon's launch of Clareon PanOptix Pro in 2025 and Bausch + Lomb's reported premium IOL growth of over 20% in Q4 2025 highlight the increasing preference for advanced visual outcomes. With global blindness and visual impairments projected to rise from 338.3 million in 2020 to 535 million by 2050, the aging trend will continue to support market expansion.[3]Stephen O'Brart, “The Global Burden of Cataract and Cataract Blindness,” Eye, doi.org

Digital-Eye-Strain Demand for Premium Lenses and Coatings

Rising screen time among working-age adults is driving demand for premium spectacle lenses, coatings, and contact lenses that offer comfort, dryness reduction, and extended wear. Employers, insurers, and consumers increasingly view digital strain as a recurring vision care need, supporting repeat purchases and product upgrades. Comfort-related features justify premium pricing, especially as daily screen exposure remains high. This trend is fostering a more profitable product mix in both spectacles and contact lenses, establishing digital strain as a sustained growth driver in the vision care market.

Omnichannel Optical Retail and E-Commerce Expansion

Channel dynamics are becoming a key growth driver in the vision care market, particularly for products with regular prescriptions and predictable reorder cycles. While e-commerce is reshaping revenue capture after initial prescriptions, physical stores remain essential for complex prescriptions and surgical needs. EssilorLuxottica's Direct-to-Consumer segment reported EUR 14.89 billion (USD 21.45 billion) in revenue for FY2025, with 10.3% growth, showcasing the shift toward integrated models. These models combine manufacturing, retail data, fulfillment, and clinical relationships, enhancing convenience and driving premium product adoption. The market is becoming more accessible for online repeat buyers while maintaining the importance of in-person care.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Premium-product affordability and reimbursement gaps | -1.4% | Global, most acute in South Asia, Sub-Saharan Africa, and Latin America | Long term (≥ 4 years) |

| Counterfeit products and online compliance friction | -0.7% | APAC, especially Southeast Asia, along with MEA and South America | Medium term (2-4 years) |

| Tariff-driven cost inflation in optical inputs | -0.6% | North America and APAC, with spillover to EMEA supply chains | Short term (≤ 2 years) |

| Quality-system recalls and single-source component risks | -0.5% | Global, most acute for companies with concentrated manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium-Product Affordability and Reimbursement Gaps

The vision care market faces a significant challenge as clinical needs far exceed the affordability of premium corrective or therapeutic services for many patients. The World Health Organization's SPECS 2030 framework aims to address this gap by increasing coverage for refractive error services by 2030. Annual productivity losses from uncorrected myopia are estimated at USD 244 billion globally, with many in low-income regions still lacking basic eyeglasses. This economic barrier impacts the adoption of fast-growing product segments like myopia-control lenses and premium surgical implants, which often rely on out-of-pocket spending. Without expanded reimbursements or affordable alternatives, affordability will continue to limit growth in high-potential regions.

Counterfeit Products and Online Compliance Friction

The vision care market also struggles with compliance issues in online channels, where unregulated products frequently reach consumers. Counterfeit or improperly dispensed contact lenses pose risks of corneal complications, undermining trust in the broader market. Legitimate manufacturers face increased costs for authentication, distributor monitoring, and prescription verification, which can reduce profit margins from digital sales. While e-commerce remains a key growth driver, it requires stricter operational controls to address these challenges effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spectacle Lenses Keep Scale While Contact Lenses Lead Growth

Spectacle lenses accounted for 52.45% of the vision care market in 2025, maintaining their position as the leading product type due to their widespread prescription and ease of adoption across patient groups. This reflects the foundational role of spectacles in addressing refractive errors in both developed and developing regions. Premium designs, advanced coatings, and myopia-control features are driving revenue growth, even as unit sales grow at a slower pace.

Contact lenses are the fastest-growing segment, with an 8.20% CAGR projected through 2031. Growth is driven by premium daily disposables, improved comfort, and their increasing role in myopia management, narrowing the value gap with premium spectacles. Intraocular lenses are also gaining traction due to rising cataract surgeries and a shift toward trifocal and extended-depth-of-focus designs, enhancing postoperative visual range.

By Application: Therapeutic Care Expands Beyond Traditional Correction

Corrective vision care held 44.6% of the market share in 2025, reflecting its role as the core revenue driver for optical dispensing and routine prescription updates. Most patient journeys in vision care begin with refraction and standard correction, ensuring the segment's continued relevance. However, providers are broadening the scope of visits to include recurring therapy, diagnostics, and follow-up care, moving beyond single corrective sales.

Therapeutic and disease management is the fastest-growing segment, with a 9.10% CAGR projected through 2031. Bausch + Lomb’s dry eye portfolio exceeded USD 1.1 billion in FY2025 revenue, with MIEBO contributing USD 316 million, highlighting the growing therapeutic market. Preventive and protective vision care is expanding as awareness of UV exposure, dry eye, and workplace strain increases. Cosmetic and lifestyle vision care remains a smaller niche, influenced more by fashion trends, safety compliance, and urban spending than disease prevalence.

By Age Group: Adult Demand Dominates While Pediatric Care Gains Speed

Adults accounted for 52.89% of the vision care market in 2025, driven by purchasing power, daily digital exposure, and growing interest in premium lenses. This group forms the core of the market, often seeking both routine corrections and performance-oriented upgrades like progressive or digital-use lenses. Adults also represent the primary customer base for optical retailers and employer-linked benefit programs, ensuring stable replacement cycles and funding innovation in pediatric progression control and advanced surgical solutions.

The pediatric segment is the fastest-growing age category, with a 7.98% CAGR forecast through 2031. Growth is linked to rising childhood myopia and the introduction of approved interventions that go beyond observation. Refraction disorders among children and adolescents increased from 21.49 million cases in 1990 to 24.45 million in 2023, with projections reaching 24.21 million by 2030. Geriatric demand is also strengthening, with refraction disorder cases among older adults more than doubling from 29.26 million in 1990 to a projected 79.71 million by 2030, supporting cataract care and premium IOL adoption.

By Distribution Channel: Physical Stores Hold Scale While Digital Sales Accelerate

Optical retail stores and chains held 38.75% of the vision care market in 2025, maintaining their position as the leading distribution channel. In-person care remains critical for prescription capture, fitting, and dispensing, especially for first-time buyers, multifocal users, and patients with complex needs. Store networks provide major brands with pricing control, clinical referral links, and insights into replacement cycles, ensuring continued investment in retail despite the growth of digital channels.

E-commerce platforms are the fastest-growing distribution channel, with an 11.15% CAGR projected through 2031. The digital channel is well-suited for repeat purchases like contact lenses and replacement eyewear, where prescription data allows for standardized fulfillment. Hospitals and ophthalmology clinics remain essential for surgical products, with EssilorLuxottica’s 2025 acquisition of Optegra adding over 70 eye hospitals across five European countries, integrating clinical and retail pathways. Pharmacies and drugstores are also gaining relevance, with Bausch + Lomb reporting 19% growth in its OTC dry eye portfolio over the year leading to late 2025.

Geography Analysis

In 2025, North America accounted for 44.67% of the global vision care market, driven by high per-capita spending, extensive private coverage, and strong innovation cycles. The U.S. leads regional demand due to a significant myopic population and rapid commercialization of new products. The FDA's approval of Essilor Stellest in September 2025 and the expanded age criteria for EVO ICL treatments in February 2026 have broadened access to premium care. While Canada and Mexico add depth, the U.S. remains the primary driver of pricing power. Cost inflation poses a challenge, with Alcon projecting a net tariff impact of USD 125 million to USD 175 million in its 2026 guidance.

Europe remains a mature vision care market, supported by aging populations, established clinical networks, and steady adoption of premium surgical products. Growth varies across the region due to differences in reimbursement policies and consumer spending between Western and Eastern Europe. Germany's optical market, for example, reported only 1% to 2% revenue growth in early 2026, constrained by cautious consumer spending. EssilorLuxottica's acquisition of Optegra highlights the growing integration of ophthalmology services with optical dispensing in the region.

Asia-Pacific is projected to achieve the fastest growth in the vision care market, with a 10.15% CAGR through 2031. The region benefits from high demand density, with myopia prevalence reaching 80% to 90% among school-leavers in parts of East Asia, supported by systematic public screening programs. East Asia leans toward high prevalence and premium product adoption, while China, Japan, India, and Southeast Asia offer growth potential due to uneven access. South America and the Middle East and Africa remain smaller contributors, with progress tied to urbanization and improved access rather than premium product penetration.

Competitive Landscape

EssilorLuxottica, Alcon, Bausch + Lomb, Johnson & Johnson Vision, CooperVision, and HOYA dominate the premium lenses, contact lenses, and eye care platforms in a moderately consolidated vision care market. While the top tier sees consolidation, the broader vision care market remains less concentrated than many medical device categories, largely due to the fragmented nature of downstream retail, specialty lens production, and various service layers. EssilorLuxottica significant control over manufacturing, retail distribution, brand ownership, and an expanding footprint in medical services. Leading players in the market excel by integrating product innovation, clinical access, and direct consumer engagement.

Mergers and acquisitions are a key strategic focus in the vision care market. In 2025, EssilorLuxottica acquired eight companies, including Optegra, Ikerian AG (specializing in AI for eye care), and PUcore’s ophthalmic lens material division. Alcon expanded its presence in adjacent ophthalmic care through acquisitions of LumiThera, Aurion Biotech, and Cylite. Bausch + Lomb increased its manufacturing capacity in Mexico in December 2025, emphasizing cost control and supply security.

Efforts to integrate routine optometry with chronic eye disease management are gaining momentum. This includes combining treatments for dry eyes, retinal screenings, glaucoma monitoring, and premium refractive corrections into a unified care pathway. Companies exceeding the growth rate of contact lenses and premium optics are likely to capitalize on this integrated care model for consistent revenue. EssilorLuxottica’s portfolio of over 15,000 designs and patents creates a strong competitive barrier against smaller players relying solely on innovation.

Vision Care Industry Leaders

Alcon Inc.

Bausch + Lomb Corporation

EssilorLuxottica

HOYA Corporation

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The FDA expanded the age indication for EVO/EVO+ Implantable Collamer Lenses (EVO ICL) in the U.S. to include patients aged 21 to 60, increasing the addressable market by approximately 8 million refractive candidates based on three years of clinical trial safety data.

- February 2026: STAAR Surgical surpassed 4 million cumulative global sales of ICL units, reflecting a growing shift from laser-based vision correction solutions.

- November 2025: EssilorLuxottica introduced Essilor Stellest 2.0 with enhanced efficacy in slowing axial elongation, currently available in Greater China with plans for global expansion in 2026, alongside Essilor Stellest Smartglasses for monitoring pediatric compliance through digital tracking of lens usage.

- October 2025: EssilorLuxottica completed the acquisition of Optegra, an ophthalmology platform operating over 70 eye hospitals across five European countries, performing more than 140,000 treatments annually, including cataract surgeries and elective vision corrections.

- October 2025: The FDA issued a Complete Response Letter to Sydnexis for its NDA submission of SYD-101 (atropine 0.01% ophthalmic solution) for pediatric myopia, citing insufficient evidence of efficacy in non-Asian populations and a declining treatment effect over 36 months, posing a challenge for the pharmacological myopia-control market.

Global Vision Care Market Report Scope

As per the scope of the report, vision care is a specialized branch of healthcare focused on assessing, treating, and preserving visual function and overall eye health. It encompasses preventative services, medical treatments, and corrective tools designed to improve visual acuity and diagnose sight-threatening diseases early.

The vision care market is segmented by product type, application, age group, and distribution channel. By product type, the market includes spectacle lenses, contact lenses, intraocular lenses, ocular health products, and vision correction systems and devices. By application, the market is segmented into corrective vision care, therapeutic and disease management, preventive and protective vision care, and cosmetic and lifestyle vision care. By age group, the market is categorized into pediatric, adult, and geriatric. By distribution channel, the market is segmented into optical retail stores and chains, hospitals and ophthalmology clinics, e-commerce platforms, and pharmacies and drugstores. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Spectacle Lenses |

| Contact Lenses |

| Intraocular Lenses |

| Ocular Health Products |

| Vision Correction Systems and Devices |

| Corrective Vision Care |

| Therapeutic and Disease Management |

| Preventive and Protective Vision Care |

| Cosmetic and Lifestyle Vision Care |

| Pediatric |

| Adult |

| Geriatric |

| Optical Retail Stores and Chains |

| Hospitals and Ophthalmology Clinics |

| E-Commerce Platforms |

| Pharmacies and Drugstores |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Spectacle Lenses | |

| Contact Lenses | ||

| Intraocular Lenses | ||

| Ocular Health Products | ||

| Vision Correction Systems and Devices | ||

| By Application | Corrective Vision Care | |

| Therapeutic and Disease Management | ||

| Preventive and Protective Vision Care | ||

| Cosmetic and Lifestyle Vision Care | ||

| By Age Group | Pediatric | |

| Adult | ||

| Geriatric | ||

| By Distribution Channel | Optical Retail Stores and Chains | |

| Hospitals and Ophthalmology Clinics | ||

| E-Commerce Platforms | ||

| Pharmacies and Drugstores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in vision care through 2031?

Growth is being supported by a large refractive error burden, aging-related demand, premium myopia management, therapeutic eye care expansion, and faster digital distribution. The market is valued at USD 75.14 billion in 2026 and is forecast to reach USD 109.38 billion by 2031 at a 7.80% CAGR.

Which product category is leading revenue today?

Spectacle lenses remain the largest product type, with 52.45% share in 2025, because they are still the most common entry point for refractive correction across age groups.

Which part of vision care is growing the fastest?

Among applications, therapeutic and disease management is growing the fastest at a 9.10% CAGR through 2031, while e-commerce platforms are the fastest-growing distribution channel at 11.15% CAGR.

Why is pediatric myopia becoming more important commercially?

Pediatric care is moving from simple correction to progression control. The FDA authorization of Essilor Stellest in 2025 created a new prescriber-led treatment pathway for children aged 6-12 in the United States.

Which region offers the strongest growth outlook?

Asia-Pacific has the fastest regional outlook, with a 10.15% CAGR through 2031, supported by very high myopia prevalence in East Asia and wider screening programs.

How concentrated is competition among leading companies?

Competition is moderately concentrated. Large groups such as EssilorLuxottica, Alcon, and Bausch + Lomb have strong positions in premium lenses and eye care platforms, but retail, specialty products, and service delivery remain more fragmented.

Page last updated on: