Smart Home Video Surveillance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

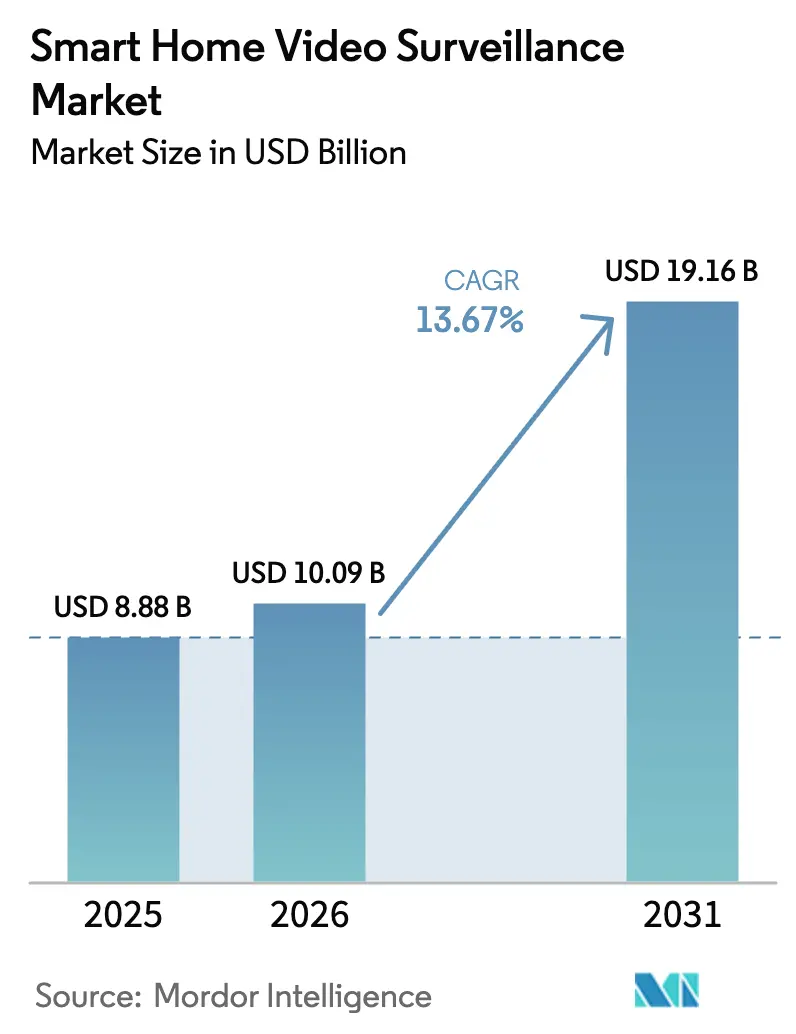

| Market Size (2026) | USD 10.09 Billion |

| Market Size (2031) | USD 19.16 Billion |

| Growth Rate (2026 - 2031) | 13.67% CAGR |

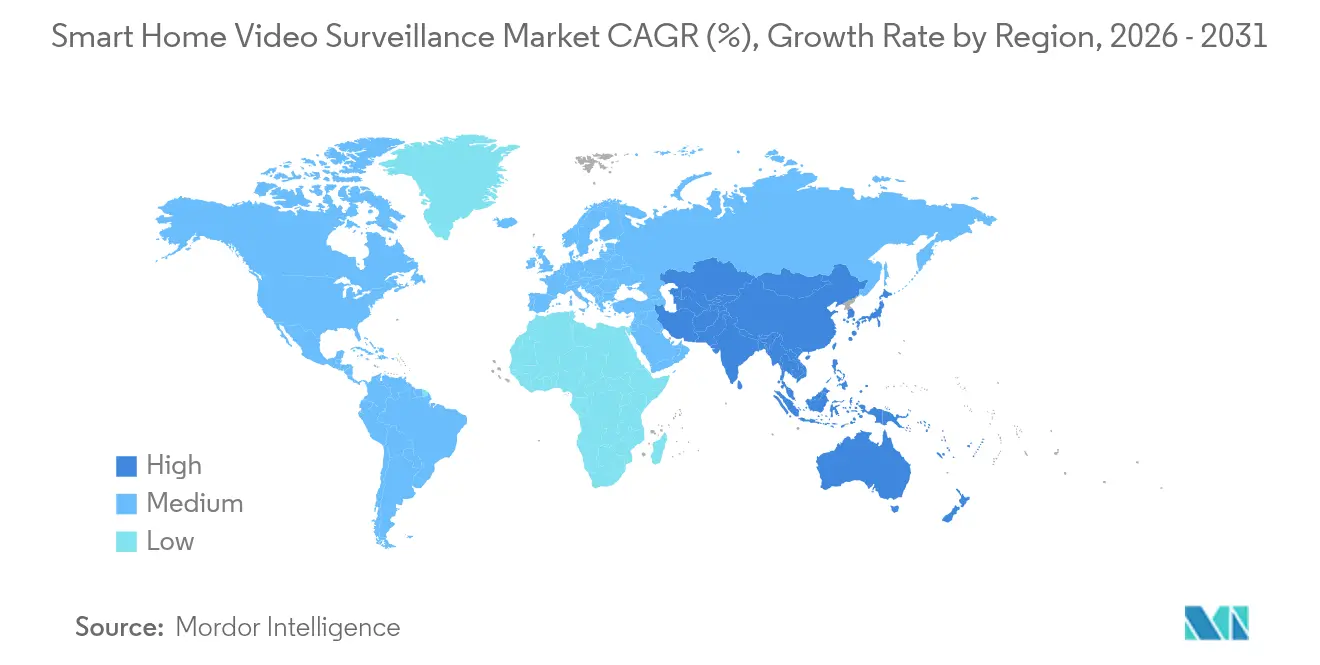

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

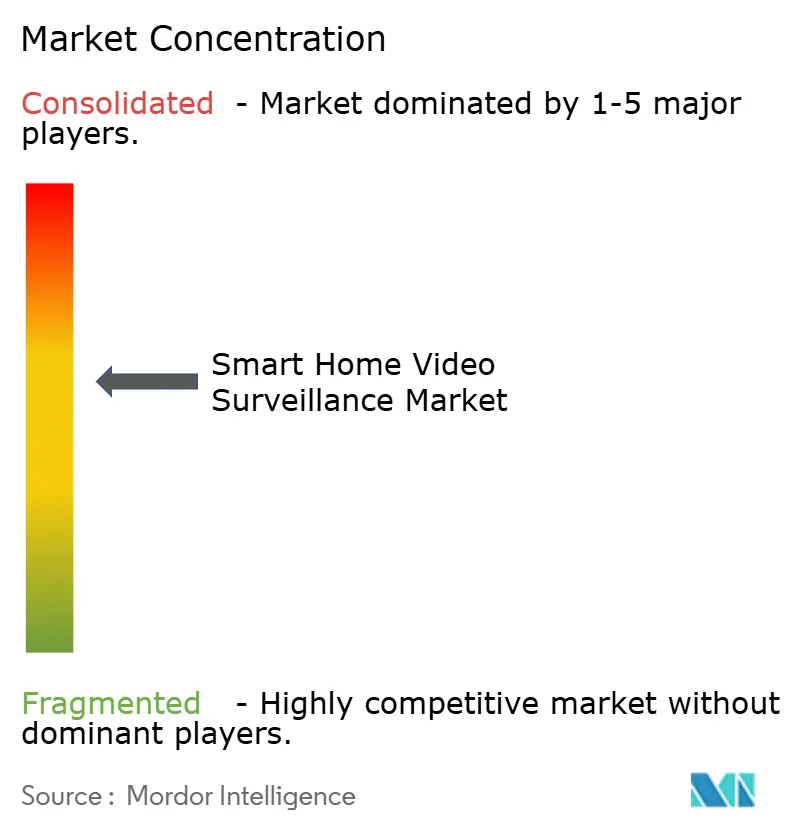

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Home Video Surveillance Market Analysis by Mordor Intelligence

The smart home video surveillance market size is expected to grow from USD 8.88 billion in 2025 to USD 10.09 billion in 2026 and is forecast to reach USD 19.16 billion by 2031 at 13.67% CAGR over 2026-2031. Momentum is building as Wi-Fi 6 household penetration supports stable 4K streaming, European insurers reward AI-enabled cameras with lower premiums, and global interoperability standards such as Matter and Thread reduce system-integration friction. Hardware remains the revenue backbone, but service subscriptions are scaling faster as edge AI transforms once-passive cameras into gateways for cloud analytics and proactive alerts. Competitive intensity is rising; platform leaders leverage cross-selling to bundle storage, monitoring and broadband while regional disruptors challenge on price and feature velocity.

Key Report Takeaways

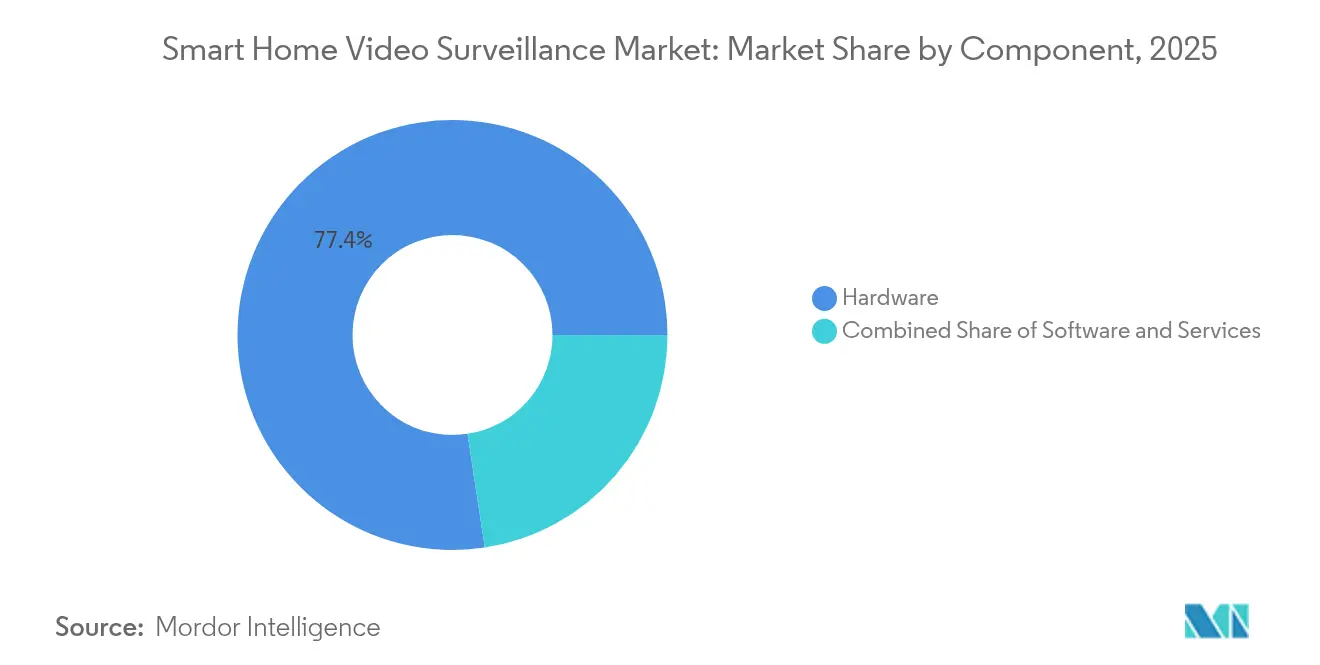

- By component, hardware led with 77.40% revenue share in 2025, whereas services are expanding at a 14.05% CAGR through 2031, highlighting a pivot toward recurring revenue.

- By device type, smart cameras captured 54.30% of the smart home video surveillance market share in 2025; video doorbells are forecast to grow at a 14.88% CAGR through 2031.

- By installation location, outdoor systems accounted for 59.20% share of the smart home video surveillance market size in 2025 and are advancing at a 15.22% CAGR through 2031.

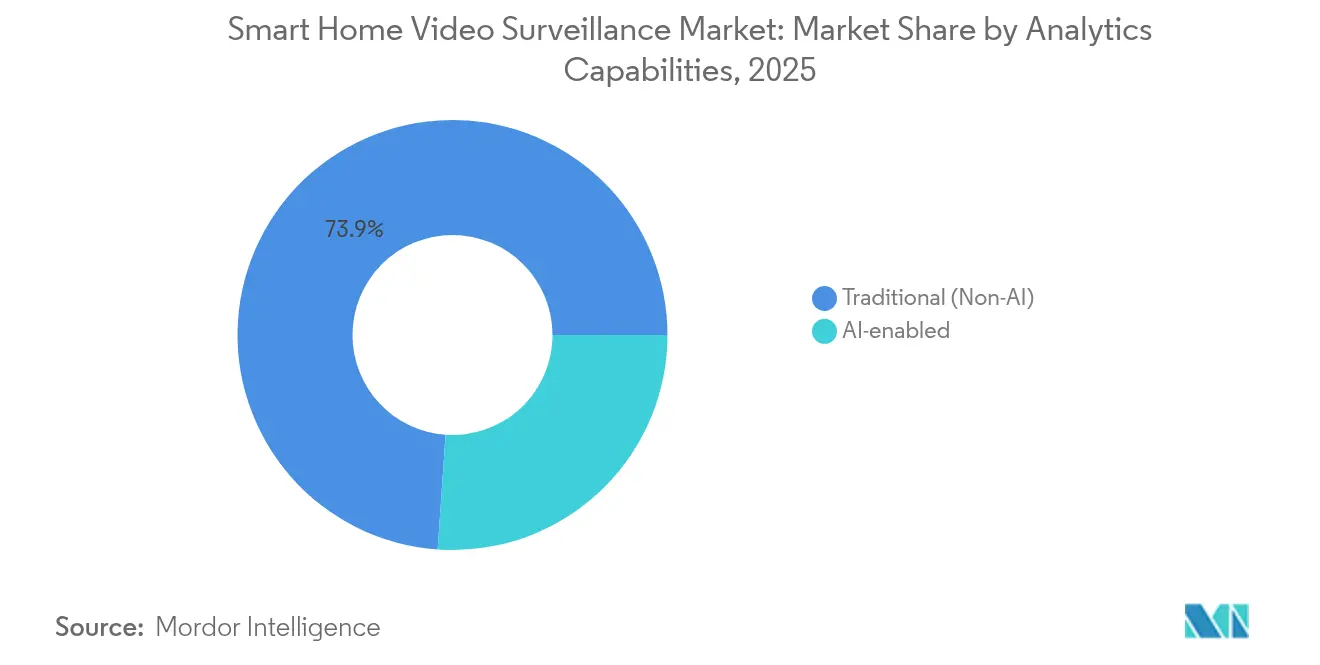

- By analytics capability, non-AI legacy products retained 73.90% share in 2025, while AI-enabled solutions are projected to expand at a 15.92% CAGR to 2031.

- By sales channel, online retail held 67.10% revenue share in 2025; offline specialty and mass-market stores trail, but online is accelerating at a 15.11% CAGR.

- By geography, North America commanded 36.60% share in 2025, whereas Asia Pacific posts the fastest regional CAGR at 14.55% through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Home Video Surveillance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Wi-Fi 6 Routers Enabling Low-Latency 4K Video Streams | +2.8% | North America and EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Insurance Premium Discounts for AI-based Surveillance Cameras | +2.1% | Europe core, expanding to North America | Short term (≤ 2 years) |

| Rising Adoption of Direct-to-Consumer Video Doorbells in Urban Asia | +1.9% | Asia-Pacific urban centers, secondary cities | Medium term (2-4 years) |

| Integration of Smart Home Surveillance with Matter and Thread Standards | +1.5% | Global, with early adoption in North America | Long term (≥ 4 years) |

| Legislative Mandates for Remote Monitoring in Elder-Care Residences | +1.3% | Japan and South Korea, potential EU adoption | Long term (≥ 4 years) |

| Bundling of Cloud Video Storage with Broadband Subscriptions | +1.1% | US and UK, expanding to developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Wi-Fi 6 Routers Enabling Low-Latency 4K Streams

Growing household adoption of Wi-Fi 6 improves bandwidth headroom and latency, allowing multiple 4K cameras to stream concurrently without congestion. Service providers exploit the upgrade cycle to bundle subscription video monitoring, creating incremental ARPU while reducing customer churn. Edge-based AI inference now runs directly on cameras, trimming cloud egress costs and enabling instant threat classification. Broadband operators in markets such as the United Kingdom use unlimited data offers to position surveillance as a value-add for premium tiers. The cumulative effect is to transform traditional CCTV into an always-connected, analytics-rich home service.

Insurance Premium Discounts for AI-Based Cameras

European insurers quantify loss-reduction benefits from real-time detection and have started offering device subsidies and policy discounts. Generali Switzerland showcases smart cameras in retail outlets, pairing hardware deals with tailored home-insurance policies that embed professional installation support.[1]Generali, “Reward for secure homes,” generali.ch Similar bundles from Sky Protect in the United Kingdom include doorbells and indoor cameras, reinforcing perceived value and accelerating penetration. The actuarial validation of AI cameras is set to migrate to the United States, where carriers search for competitive differentiation. Early adoption advantages should expand insurer–OEM partnerships and shift go-to-market economics toward risk-sharing models.

Rising Adoption of Direct-to-Consumer Video Doorbells in Urban Asia

Asia Pacific accounts for 61% of global B2C e-commerce parcels, intensifying doorstep security needs and boosting doorbell demand. Doorbells bypass professional installers, suiting dense apartment markets where quick self-installation is crucial. Samsung’s Family Care service weaves doorbells into broader elder-care monitoring, increasing lifetime value by adding caregiver analytics. Manufacturers add features such as multilingual prompts and integration with local couriers, differentiating against Western-centric products. Direct-to-consumer models compress distribution margins and accelerate upgrade cycles as new AI capabilities reach consumers faster.

Integration with Matter and Thread

Matter’s upcoming camera specification and Thread 1.4 mesh networking promise to end ecosystem silos by enabling devices from multiple brands to authenticate and communicate reliably. Thread ensures that security cameras do not need proprietary hubs, simplifying installation and broadening accessory choices.[2]Thread Group, “Thread 1.4 Paves The Path For Smart Devices To Work Together,” threadgroup.org Manufacturers preparing for Matter 1.5 leverage WebRTC to preserve low-latency streams within a secure, interoperable layer. Early compliance offers a first-mover advantage among platform players such as Apple, Google and Amazon, each seeking to anchor users within their wider smart-home ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Residency Regulations in EU Limiting Cross-Border Cloud Video Storage | -1.8% | EU core, potential global expansion | Medium term (2-4 years) |

| High Bandwidth Costs in Africa Restricting Adoption of High-Resolution Cameras | -1.2% | Sub-Saharan Africa, rural emerging markets | Long term (≥ 4 years) |

| Cyber-Attack Incidents Targeting Consumer IoT Devices Undermining Trust in APAC Markets | -1.0% | APAC core, with spillover concerns globally | Short term (≤ 2 years) |

| Neighbourhood Privacy Litigation in Canada and Germany Slowing Outdoor Camera Installations | -0.8% | Canada & Germany, potential spread to other developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Residency Regulations in the EU

GDPR mandates strict controls on video analytics, compelling vendors to process data locally or establish regional data centers. Providers such as Avigilon respond with granular user-permission layers, anonymization tools and enforced retention periods. While compliance raises development overhead, it confers trust advantages that can become competitive moats. [3]Europe Data Protection Board, “Guidelines 3/2019 on processing of personal data through video devices Version 2.0,” edpb.europa.eu The regulation is already shaping procurements in healthcare and elder-care facilities, where privacy remains paramount. Similar frameworks in other regions are likely, extending the need for adaptable architecture across multijurisdiction deployments.

High Bandwidth Costs in Africa

Limited fixed-line infrastructure elevates data pricing and constrains continuous 4K streaming across large territories. Consumers often downscale to 720p feeds to avoid data caps, muting hardware revenue potential for premium cameras. Vendors experiment with H.265 codecs and on-device storage to minimize consumption, yet adoption lags behind markets with affordable broadband. Opportunities persist for satellite connectivity and hybrid edge-cloud designs that ration bandwidth during off-peak hours, but near-term growth remains subdued compared with mature markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Subscription Transformation

Hardware still generates the majority of revenue because each household needs physical cameras, sensors and cabling before any software value can be realized. The services segment, however, is scaling at a 14.05% CAGR as consumers migrate from ownership to “security-as-a-service” models that bundle storage, AI analytics and professional response. In dollar terms, subscriptions represent the stickiest portion of the smart home video surveillance market size and already underpin USD 300 million in annual recurring revenue for Arlo. Leading brands encourage free-trial upgrades and tiered plans to lift average revenue per unit over the device life cycle.

Hardware margins are gradually tightening because of white-label entrants, reinforcing OEM dependence on cloud value propositions. This evolution parallels smartphone ecosystems where services eclipse hardware margins, and it forces manufacturers to maintain high up-time, intuitive dashboards and cross-platform experiences to limit churn. As the hardware base expands, lifetime value economics increasingly favor companies that own both firmware and subscription layers. Competitive focus therefore shifts toward retention metrics such as monthly active users and churn, not merely shipment volumes. The interplay between hardware economies of scale and software network effects defines the dominant strategy over the forecast horizon.

By Device Type: Video Doorbells Challenge Camera Dominance

Smart cameras continue to command a 54.30% share because they address universal monitoring needs inside and outside the home. Doorbells, projected to grow at 14.88% CAGR, now represent the face of the smart home video surveillance market owing to e-commerce parcel growth and remote access control. Amazon’s Ring sets benchmark expectations for two-way audio, motion zones, and natural-language video search, forcing competitors to match AI feature depth at consumer-friendly price points. The doorbell’s prominent placement on the front entrance accelerates brand visibility and cross-selling into complementary sensors.

Bundled kits that combine cameras, chimes and extenders shorten installation time and reduce friction in first-time buyer segments. In Asia Pacific, multilingual voice prompts and integration with ride-hailing and courier apps cater to local usage habits, widening differentiation beyond hardware specs. Meanwhile, NVR/DVR systems remain relevant for homeowners seeking centralized storage and longer retention, especially in markets with tight data privacy rules. Device diversity strengthens ecosystem stickiness by anchoring users inside a single control app, which in turn improves software upsell conversion. The market trajectory therefore favors brands that orchestrate a coherent device family rather than single-product plays.

By Installation Location: Outdoor Installations Lead Growth

Outdoor cameras account for 59.20% share and grow faster than indoor units because homeowners view perimeter vigilance as the first line of defense. Modern IP67-rated housings and onboard IR illumination remove historical barriers caused by weather and low-light limitations. Privacy concerns shift indoor adoption toward specific rooms such as entryways and nurseries, while legal precedents in Canada underscore the importance of respecting neighboring property lines. In practice, vendors embed masking zones and edge anonymization to remain compliant with emerging bylaws.

High-definition outdoor footage also feeds insurance claims, providing verifiable evidence that accelerates policy settlements and supports premium discounts. The convergence of crime-prevention incentives, insurer endorsements and maturing hardware reliability sustains the outdoor growth path. Indoor cameras still serve critical niches such as pet monitoring and elderly care, but future innovation will likely focus on privacy-first capabilities to overcome adoption hesitancy.

By Analytics Capability: AI Transformation Accelerates

Non-AI cameras held 73.90% share in 2025 because price-sensitive buyers gravitate toward basic motion-triggered models. AI-enabled units, recording a 15.92% CAGR, differentiate through person, package, and vehicle recognition that reduces false alarms and elevates customer satisfaction. Google’s Gemini integration allows subscribers to query hours of footage with plain-language prompts, turning raw data into actionable insights. Budget-oriented disruptors such as Wyze offer AI features for USD 19.99 monthly, pressuring incumbents to refine cost structures without diluting innovation.

Edge AI chips lower latency, diminish bandwidth usage and bolster privacy by processing detection locally. As battery-powered devices proliferate, efficient machine-learning models will determine battery life competitiveness, positioning silicon optimization as a key differentiation lever. The competitive battleground thus shifts from megapixel counts to algorithm quality, dataset breadth and responsible AI practices.

By Sales Channel: Online Retail Dominance Continues

Online platforms captured 67.10% of sales in 2025 as self-installation tutorials, customer reviews and flash promotions accelerate purchase decisions. Direct-to-consumer models eliminate traditional installer margins and allow brands to launch software updates instantly, preserving feature parity across geographies. Market leaders invest in interactive product configurators and live-chat support to replicate in-store consultations digitally.

Offline specialty stores retain value for consumers demanding professional setup or bundled smart-home advisory, yet rising do-it-yourself confidence restricts their growth. Hybrid go-to-market strategies emerge as incumbents offer click-and-collect, installer referral networks and extended warranties to bridge online and offline experiences. Dynamic pricing algorithms and influencer collaborations further intensify competition within the online channel. Over time, data-driven insights from e-commerce portals will refine product roadmaps and promotion calendars, solidifying online leadership.

Geography Analysis

North America continues to anchor the smart home video surveillance market with 36.60% revenue share because households prioritize connected security, benefit from high disposable incomes and enjoy near-ubiquitous broadband coverage. Internet service providers such as Comcast bundle cameras and cloud storage into broadband subscriptions, charging USD 10 per month and reducing friction for mass adoption. Regulatory clarity on data privacy allows rapid AI rollouts compared with Europe, and insurers begin to import discount models inspired by EU peers, nurturing demand. Canada follows a similar trajectory, while Mexico’s adoption accelerates through cross-border platform spillover and decreasing device prices.

Asia Pacific registers the fastest CAGR at 14.55% through 2031, powered by urbanization, dominant e-commerce logistics and government support for elder-care monitoring. South Korea and Japan legislate remote observation requirements in assisted-living facilities, driving institutional orders for AI cameras. China’s scale advantages compress manufacturing costs, making devices affordable for upper-middle-income households. India, with a rapidly urbanizing population, represents the next volume inflection point as broadband reach and mobile payment penetration rise. By 2030, Asia Pacific’s installed base is projected to eclipse North America, though per-unit monetization remains lower.

Competitive Landscape

The competitive field features a mix of diversified tech platforms, security specialists, and fast-moving disruptors. Amazon, Google and Arlo deploy ecosystem strategies: proprietary AI models, cloud storage tiers and smart-home integrations deepen user lock-in and raise switching costs. Amazon’s Ring pushes routine-learning algorithms that automate surveillance behaviors and integrates expanded safety devices like smart smoke alarms, broadening the platform footprint. Google’s release of Gemini AI across Nest devices underscores the shift toward natural-language interfaces that simplify user interaction. Arlo maintains momentum through partnerships with Samsung SmartThings and Origin AI, embedding verified human presence detection to decrease false positives and upsell premium subscriptions.

Price-challenger Wyze pressures incumbents by offering subscription AI services at USD 19.99 while maintaining aggressive hardware pricing, showcasing the potential for volume-based strategies in lower-income segments. Regional manufacturers leverage localization capabilities such as language support and courier integrations to capture share in Asia’s fast-growing urban markets. Meanwhile, patent filings concentrate on edge processing and privacy-preservation techniques that could redefine value propositions and licensing revenue.

Smart Home Video Surveillance Industry Leaders

Amazon (Ring)

Google (Nest)

Arlo Technologies Inc.

Hangzhou Hikvision Digital Technology Co. Ltd (Ezviz)

Wyze Labs Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Arlo Technologies expanded its partnership with Samsung SmartThings, adding two-way audio, event snapshots and computer-vision AI to enhance cross-platform functionality.

- June 2025: Amazon unveiled AI-generated security alerts that summarize Ring motion events in text form for premium subscribers in the United States and Canada.

- April 2025: Ring partnered with Kidde to launch smart smoke and carbon-monoxide alarms linked to the Ring app via Wi-Fi, extending the brand into broader home safety solutions.

- February 2025: Arlo Technologies allied with Origin AI to embed AI-verified human and vehicle detection, positioning itself for higher-tier monitoring revenue.

Global Smart Home Video Surveillance Market Report Scope

A smart home, as part of the Internet of Things (IoT), leverages internet-connected devices to remotely monitor and manage various systems, from lighting to heating. These systems not only share usage data but also automate actions based on homeowners' preferences. The smart home video surveillance market is defined by the revenue accrued from the sales of different types of video surveillance cameras in the residential sector over various end users across North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa. The scope includes only the hardware (camera) and service part of the market and excludes the software aspect.

The smart home video surveillance market is segmented by component (cameras, service) and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| Smart Cameras |

| Video Doorbells |

| NVR / DVR and Smart Hubs |

| Full-Kit Bundles |

| Indoor |

| Outdoor |

| AI-enabled |

| Traditional (Non-AI) |

| Online Retail |

| Offline (Specialty and Mass-Market Stores) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Device Type | Smart Cameras | ||

| Video Doorbells | |||

| NVR / DVR and Smart Hubs | |||

| Full-Kit Bundles | |||

| By Installation Location | Indoor | ||

| Outdoor | |||

| By Analytics Capability | AI-enabled | ||

| Traditional (Non-AI) | |||

| By Sales Channel | Online Retail | ||

| Offline (Specialty and Mass-Market Stores) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the market value of smart home video surveillance in 2026?

The market stands at USD 10.09 billion in 2026.

What compound annual growth rate will the market record between 2026 and 2031?

The market is projected to advance at a 13.67% CAGR, reaching USD 19.16 billion by 2031.

Which geographic region is expanding fastest?

Asia Pacific posts the highest regional growth at a 14.55% CAGR through 2031, driven by urban e-commerce demand and elder-care regulations.

Why is the services segment growing faster than hardware?

Cloud storage, AI analytics and professional monitoring subscriptions create recurring revenue, lifting the services segment at a 14.05% CAGR while hardware margins tighten.

Page last updated on: