CCTV Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

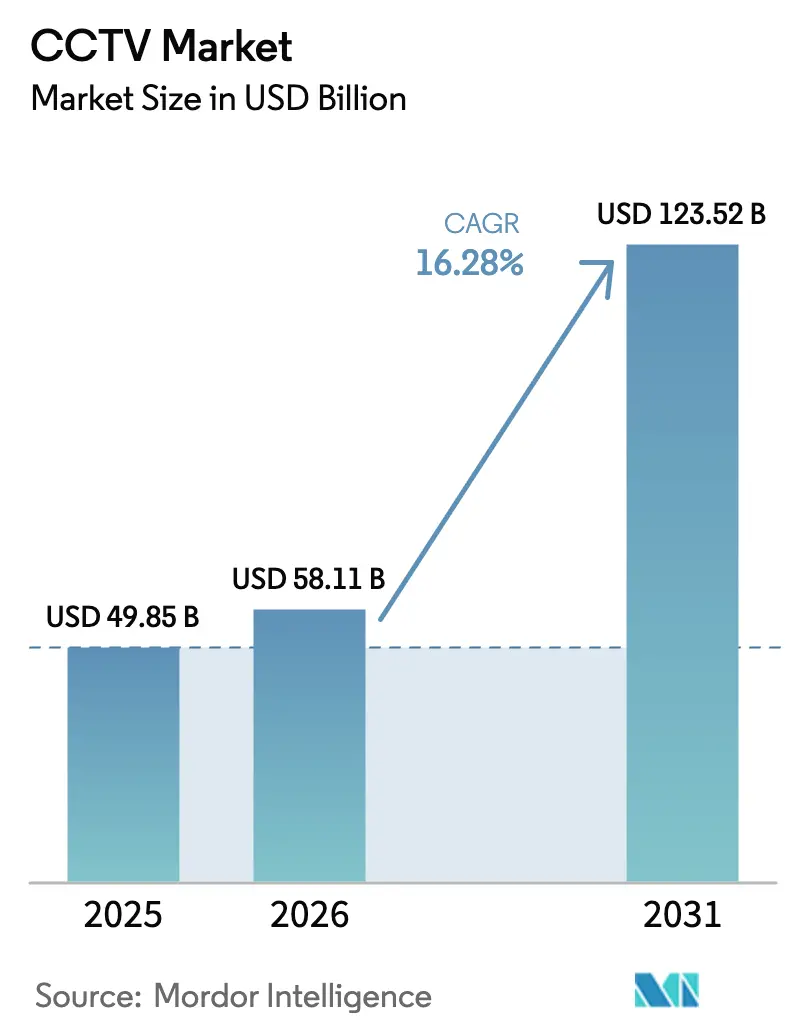

| Market Size (2026) | USD 58.11 Billion |

| Market Size (2031) | USD 123.52 Billion |

| Growth Rate (2026 - 2031) | 16.28% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CCTV Market Analysis by Mordor Intelligence

The CCTV market size is projected to expand from USD 49.85 billion in 2025 and USD 58.11 billion in 2026 to USD 123.52 billion by 2031, registering a CAGR of 16.28% between 2026 and 2031. The upswing reflects mandate-driven rollouts of AI video analytics in smart-city tenders, enterprise refresh cycles sparked by data-protection rules, and the shift toward cloud-managed surveillance subscriptions that reduce capital outlays. With wider 5G coverage, lower bandwidth tariffs, and chipsets that compress 4K streams at the edge, use cases are broadening beyond security, turning cameras into multi-purpose sensors for traffic flow, process quality, and occupancy analytics. Chinese manufacturers continue to price aggressively through vertical integration, while Western vendors differentiate on cybersecurity certifications. As a result, buyers weigh total cost of ownership against compliance exposure rather than megapixel counts alone.

Key Report Takeaways

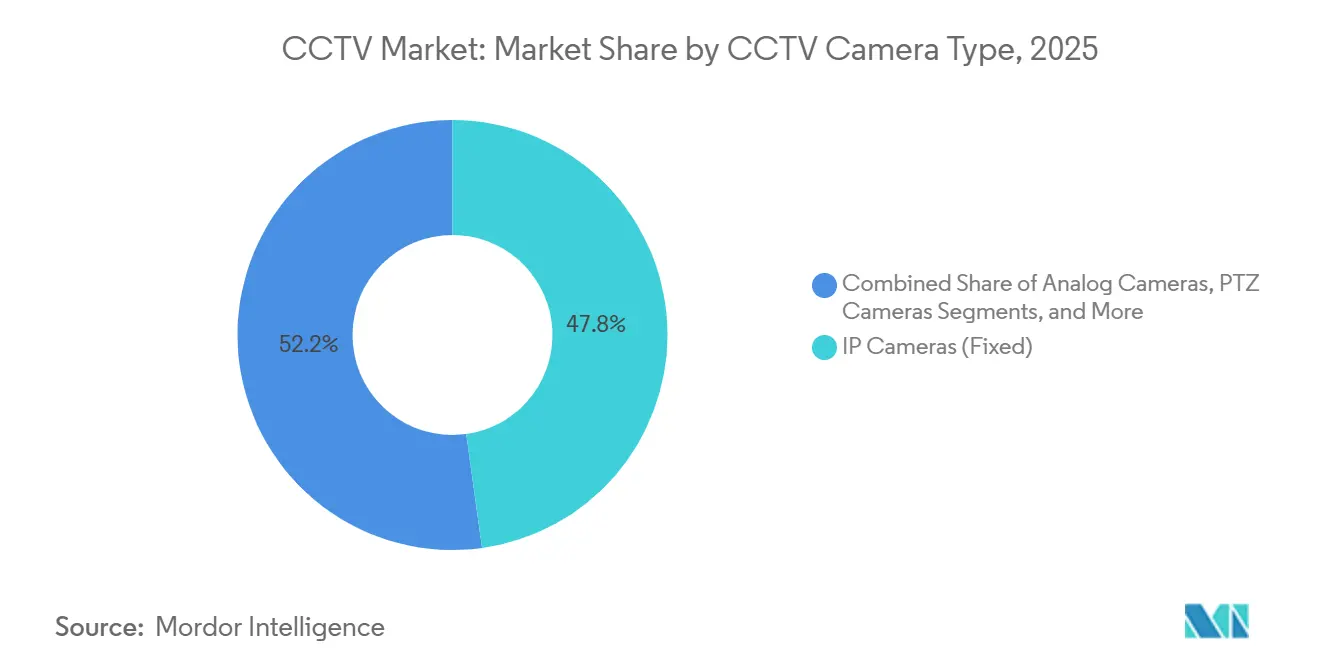

- By camera type, IP cameras commanded 47.80% of the CCTV market share in 2025, while 4K/Ultra-HD segment is projected to expand at an 17.3% CAGR through 2031.

- By resolution, HD formats held 38.30% revenue share in 2025, while the 4K and above segment is projected to expand at an 18.20% CAGR through 2031.

- By installation, fixed systems accounted for 72.80% of the CCTV market size in 2025; mobile and rapid-deploy platforms will lead growth at a 16.80% CAGR to 2031.

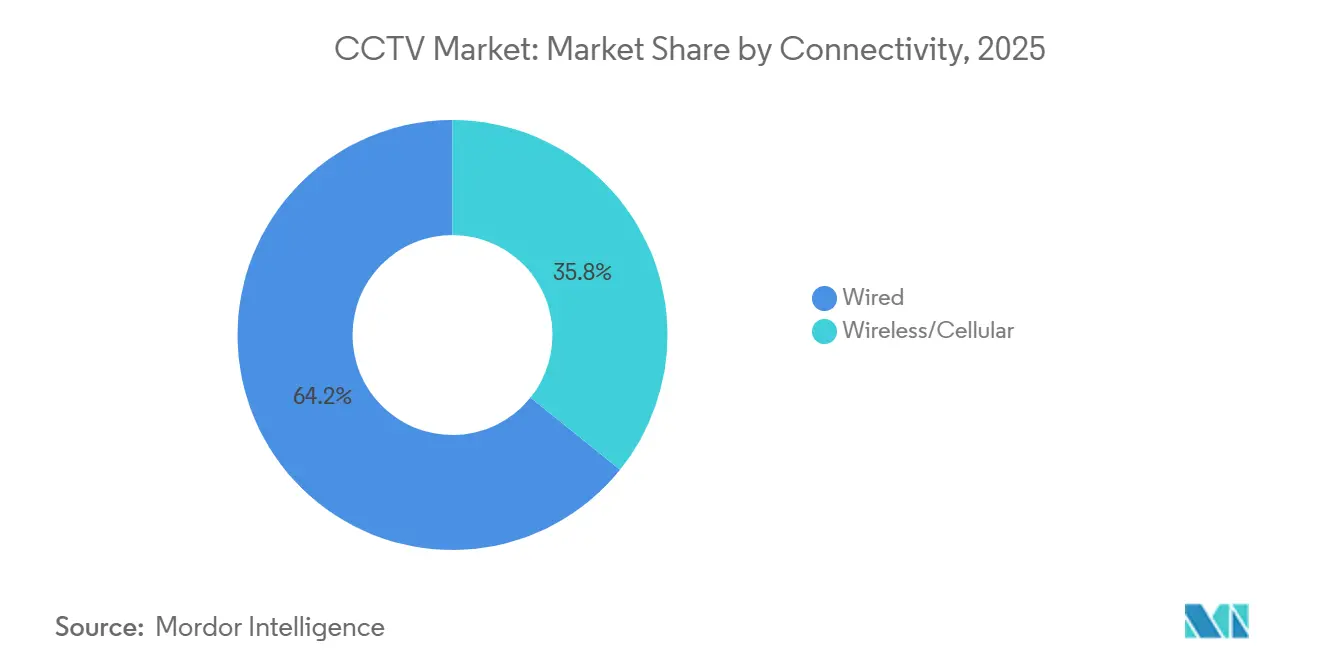

- By connectivity, wired solutions retained 64.23% share in 2025, yet wireless and cellular links are forecast to grow at a 16.40% CAGR over the same period.

- By end-user vertical, government and public safety led with 28.50% revenue share in 2025, while hospitality and healthcare are advancing at a 17.39% CAGR through 2031.

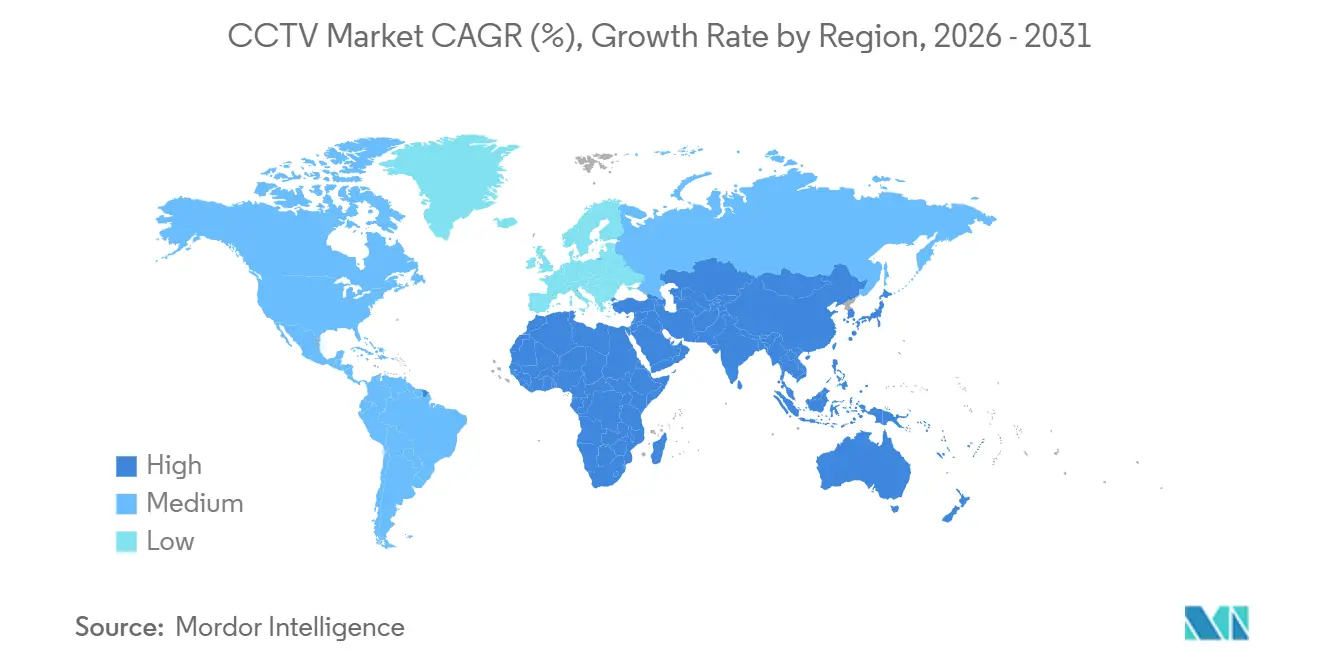

- By geography, Asia-Pacific led with 34.6% revenue share in 2025, while Africa are advancing at a 18.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CCTV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Enabled Video Analytics Propelling Smart-City Surveillance | +4.2% | Global with focus in Asia-Pacific and Middle East | Medium term (2-4 years) |

| GDPR-Driven Enterprise Upgrades | +2.8% | Europe and North America, spillover to Asia-Pacific multinationals | Short term (≤ 2 years) |

| Cloud-Managed CCTV Adoption by SMBs | +3.1% | North America and Europe, expanding to South America | Medium term (2-4 years) |

| Falling Bandwidth Costs Fueling HD and IP Uptake | +2.5% | Global, faster in emerging markets | Long term (≥ 4 years) |

| IoT-Edge Integration in Industrial Automation | +2.0% | North America, Europe, and Asian industrial hubs | Long term (≥ 4 years) |

| Government-Funded Safe-City Programs | +3.6% | Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Video Analytics Propelling Smart-City Surveillance

Municipal procurement teams now insist on cameras that run object detection, license plate recognition, and crowd-density estimation directly on the device to avoid pushing raw 4K streams to data centers. Singapore, Barcelona, and several tier-2 Chinese cities improved emergency-response speeds and trimmed operating budgets after moving to on-edge analytics. Bandwidth savings, data-sovereignty compliance, and emerging interoperability standards that let agencies swap AI models across brands all reinforce the trend.[1]Land Transport Authority, “AI-Enabled Traffic Management Systems 2025,” lta.gov.sg

GDPR-Driven Enterprise Upgrades

In Europe, stringent enforcement of regulations has significantly heightened the consequences for companies that fail to comply with retention practices. As a result, many firms have been compelled to transition from outdated DVRs to more advanced IP systems. These modern systems are now equipped with critical features such as encryption at rest, audit logs, and automated deletion workflows, ensuring better compliance and data security. At the same time, financial institutions and retailers have increasingly adopted privacy masking techniques. These techniques obscure faces in video footage until explicit operator authorization is obtained, thereby aligning with the data-minimization mandates outlined in Article 5 of the regulations. This shift reflects a broader trend toward prioritizing data privacy and regulatory adherence across industries.[2]Data Protection Commission Ireland, “GDPR Enforcement Actions 2024,” dataprotection.ie

Cloud-Managed CCTV Adoption by SMBs

Multi-site operators without dedicated IT staff find subscription bundles—integrating cameras, cloud storage, and mobile access—particularly appealing due to their convenience and comprehensive functionality. These operators benefit significantly from hybrid architectures that retain 30-120 days of footage on-device, ensuring critical data is readily accessible when needed. Additionally, these systems send thumbnails to dashboards for quick monitoring and revert to local storage during outages, maintaining operational continuity. This approach not only streamlines surveillance management but also alleviates concerns about bandwidth caps and cyber breaches, providing a reliable and secure solution for multi-site operations.

Falling Bandwidth Costs Fueling HD and IP Uptake

Between 2020 and 2025, average global bandwidth prices plummeted by two-thirds, significantly altering the digital landscape. This dramatic drop made full-HD and 4K streaming not only accessible but also affordable for ports, logistics yards, and municipal grids, enabling them to adopt advanced streaming technologies. With H.265 compression effectively cutting bit-rates in half, the efficiency of data transmission has improved considerably. Additionally, 5G fixed-wireless access has played a crucial role by delivering uplinks of 100-300 megabits in regions where fiber infrastructure remains scarce, further enhancing connectivity and streaming capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Facial-Recognition Privacy Litigations | -2.3% | Europe and North America, emerging in South America | Short term (≤ 2 years) |

| Semiconductor Supply Constraints Raising BOM Costs | -1.8% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Fragmented Cyber-Security Norms | -1.2% | Global with cross-border projects | Medium term (2-4 years) |

| Installer Skill Shortage Escalating Retrofit Costs | -0.9% | North America and Europe, spreading to urban Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Facial-Recognition Privacy Litigations

Class-action lawsuits and municipal bans have compelled end-users to either disable or restrict biometric modules, significantly impacting their adoption and usage. European directives now categorize real-time facial recognition in public spaces as high-risk processing, mandating comprehensive impact assessments and, in many cases, requiring individual consent to proceed. Vendors have responded by providing firmware switches that allow the deactivation of biometric features, ensuring compliance with regulatory requirements. Meanwhile, integrators are actively guiding clients towards alternative solutions, such as anonymized crowd analytics, which offer valuable insights while minimizing privacy concerns.[3]European Data Protection Board, “Guidelines on Facial Recognition Technology 2024,” edpb.europa.eu

Semiconductor Supply Constraints Raising BOM Costs

In 2025, the market experienced prolonged shortages of image-signal processors and AI accelerators, which led to a significant increase in bill-of-materials costs, rising by as much as 18%. This substantial cost escalation placed considerable pressure on profit margins and caused lead times to extend further. To mitigate these challenges, manufacturers took several measures, including reengineering boards to integrate alternative chips, increasing list prices to offset higher costs, and prioritizing high-volume contracts to maintain operational efficiency. However, these actions also resulted in delays for certain government tenders, highlighting the widespread impact of the shortages on various sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By CCTV Camera Type: IP Dominance Meets 4K Disruption

The segment with IP cameras led the CCTV market share at 47.80% in 2025, reflecting seamless IT integration and Power-over-Ethernet convenience. Analog cameras persist in cost-sensitive retrofits, while PTZ units occupy niches such as borders and stadiums. Thermal devices, though smaller in volume, gained industrial traction because operators value heat anomaly alerts. 4K and ultra-HD models, expanding at 17.30% CAGR, meet casino and airport forensic requirements and are set to reshape procurement priorities toward on-device compute rather than raw pixel counts.

Edge intelligence is altering total cost of ownership calculations. Axis debuted a neural-processing chip that runs ten AI models on-board, trimming server expenditure. Fixed IP units remain the enterprise workhorse, PTZ mechanisms face durability questions outdoors, and thermal sensors penetrate agriculture and logistics. As software-defined capabilities dominate specifications, price competition shifts from hardware toward long-term analytics licensing.

By Resolution: 4K Ascendancy Driven by Forensic Mandates

HD products accounted for 38.30% of 2025 revenue, balancing clarity with storage cost. Legacy standard-definition stock declines because suppliers phase out older sensors. Full-HD cameras satisfy most retail and office needs while keeping 30-day storage under USD 15 per camera. The premium 4K tier is growing at an 18.20% CAGR as casinos, airports, and financial regulators demand face or plate identification from longer distances. Variable-bitrate encoding and cloud-archival tiers help offset the added storage burden.

Regulatory pressure drives the shift as auditors insist on retrievable high-resolution footage within narrow service-level windows. Airports use 4K feeds to power biometric exit checks, retailers extract queue metrics, and hospitals monitor social distancing in waiting rooms. Storage inflation remains the main obstacle, prompting vendors to ship cameras that dynamically lower bit-rates in static scenes without compromising evidence-grade quality during motion bursts.

By Installation Type: Fixed Systems Anchor Share, Mobile Units Surge

Fixed installations captured 72.80% of the CCTV market size in 2025, benefiting from predictable coverage zones and scaled procurement of brackets, housings, and cabling. They fit 7-10 year depreciation cycles typical in government and enterprise budgets. Mobile and rapid-deploy platforms, projected to grow at a 16.80% CAGR, serve events, construction sites, and disaster zones where quick setup outranks per-camera costs. Solar panels, LTE modems, and rugged enclosures enable 30-90 day autonomous runs, expanding addressable markets for temporary surveillance.

Construction contractors use trailer-mounted units to reduce copper theft, while law-enforcement agencies rely on them for crowd management during demonstrations. Falling data-plan prices and 5G uplinks make cellular backhaul economical for short-term coverage. Hybrid estates emerge, combining fixed wired backbones with mobile over-cellular nodes that fill blind spots or provide failover during maintenance windows.

By Connectivity: Wired Reliability Versus Wireless Agility

Wired deployments held 64.23% revenue share in 2025, supported by PoE’s one-cable simplicity, centralized UPS backup, and deterministic bandwidth critical for 4K streams. Wireless and cellular links, advancing at a 16.40% CAGR, remove trenching costs for parking lots, heritage buildings, and leased retail spaces. 5G network slicing now guarantees sub-50 millisecond latency and 99.99% availability, making cellular viable for mission-critical feeds. Carriers bundle static IPs, VPN tunnels, and priority queues into camera-specific plans, easing security concerns.

Decision factors tilt on project tenure and recurring expense profiles. Wired solutions demand higher initial labor yet minimal monthly fees, while wireless flips the ledger. Increasingly, integrators propose hybrid topologies where prime cameras use PoE and auxiliary units rely on LTE or 5G, delivering resilience and coverage flexibility without over-building fixed infrastructure.

By End-User Vertical: Government Leadership, Healthcare Acceleration

Government and public safety remained the largest buyer group with 28.50% of 2025 spending, fueled by smart-city traffic systems, body-worn camera integration, and mass-transit surveillance. Transportation hubs, industrial plants, and banking facilities rely on cameras for both security and operational monitoring, linking footage to quality-control software and compliance mandates. Retailers deploy analytics that quantify footfall and detect organized theft rings.

Hospitality and healthcare lead growth at 17.39% CAGR to 2031. Hotels kept thermal screening at entrances after the pandemic, while hospitals stream surgical procedures for telemedicine and accreditation evidence. Behavioral-health centers add privacy masking to protect patient identities, and universities install entry cameras to respond to active-shooter threats. These sectors treat cameras as multipurpose sensors that enhance safety, optimize staffing, and underpin liability management.

Geography Analysis

In 2025, the Asia-Pacific region commanded a leading position with a 34.60% market share. China's initiatives, namely the Skynet and Sharp Eyes projects, deployed AI cameras in its secondary cities. Concurrently, India's Smart Cities Mission allocated a substantial USD 5.8 billion for command centers, with 20% of this budget directed towards surveillance. Japan harnessed fall-detection analytics for eldercare, while South Korea championed factory safety through subsidies for 5G-connected cameras.

North America, driven by robust demand from enterprises and municipalities for cloud-managed platforms, accounted for approximately 28% of the revenue. Europe, with a share of about 24%, saw its growth closely linked to GDPR compliance and transportation modernization efforts, notably funded by the Connecting Europe Facility. Meanwhile, the Middle East, with its ambitious mega-projects like NEOM, is seamlessly integrating cameras into building-management systems. Africa is witnessing the most rapid growth, boasting an impressive 18.10% CAGR projected through 2031. Countries like Nigeria, Kenya, and Ethiopia are capitalizing on infrastructure loans to roll out safe-city initiatives, effectively linking CCTV networks with emergency communications. South America is also making strides, with metro operators in São Paulo noting a decline in crime rates following the widespread adoption of cameras.

Globally, the increasing adoption of AI-powered surveillance systems is driven by advancements in technology and the growing need for public safety. Governments and private entities are investing heavily in smart infrastructure to enhance security, optimize urban management, and improve emergency response systems. This trend is expected to continue shaping the market dynamics during the forecast period.

Mordor Intelligence provides coverage of the cctv market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

In 2025, the top five suppliers collectively accounted for an estimated 48% of the revenue, indicating a moderately concentrated market. Chinese frontrunners, Hikvision and Dahua, leverage vertical integration to offer competitive pricing, while Axis, Hanwha, and Bosch cater to regulated sectors by adhering to IEC 62443 and FIPS cryptographic standards. Meanwhile, cloud-native entrants like Verkada and Rhombus are winning over SMBs by offering subscription bundles that eliminate the burden of capital expenses. Patent trends reveal contrasting focuses: Chinese companies are honing in on compressed AI models tailored for low-power edge chips, whereas their Western counterparts prioritize privacy-centric analytics, notably homomorphic encryption.

Strategic maneuvers further illuminate the evolving landscape. Axis unveiled a neural-processing chip, slashing the five-year ownership cost by 25%. Bosch clinched a project certified by IEC-62443 for critical infrastructure in 2025, emphasizing security as a key differentiator in tenders. Hikvision poured in USD 500 million to triple its thermal camera production, eyeing industrial and border applications. On another front, Motorola's acquisition of Ava Security seamlessly integrated cloud VMS into a broader public-safety suite, while Hanwha's collaboration with Azure IoT Edge empowers customers to deploy customized AI models, sidestepping vendor lock-in.

Looking ahead, the market is expected to witness intensified competition as suppliers focus on innovation and strategic partnerships. The adoption of AI-driven solutions, coupled with advancements in edge computing, is likely to redefine product offerings. Additionally, regulatory compliance and cybersecurity standards will remain critical factors influencing procurement decisions, particularly in sectors such as critical infrastructure and public safety.

CCTV Industry Leaders

Hangzhou Hikvision Digital Technology Co Ltd

Bosch Security Systems

Zhejiang Dahua Technology Co., Ltd.

Axis Communications AB

Hanwha Vision

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Axis Communications introduced its ARTPEC-9 chip with embedded neural processing, cutting external server needs and reducing five-year ownership cost by 25%.

- December 2025: Hikvision committed USD 500 million to expand thermal-camera production in Chongqing, aiming to triple capacity by Q3 2026.

- November 2025: Hanwha Vision teamed with Microsoft Azure to let enterprises push custom AI models to cameras and visualize events in Power BI.

- October 2025: Bosch Security Systems won a USD 132 million order to supply 15,000 IEC 62443-certified cameras to European critical-infrastructure operators.

Global CCTV Market Report Scope

CCTV (Closed-Circuit Television) is a video surveillance system that transmits signals through a closed network of cameras, monitors, and recording devices rather than broadcasting them publicly.

The study tracks the revenue accrued through the sale of CCTVs by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The CCTV Market Report is Segmented by Camera Type (Analog, IP, PTZ, Thermal, and 4K/Ultra-HD), Resolution (SD, HD, Full-HD, and 4K and Above), Installation (Fixed, and Mobile), Connectivity (Wired, and Wireless), End-User (Government, Transportation, Industrial, BFSI, Retail, Hospitality, Healthcare, and Education), and Geography. Market Forecasts are in Value (USD).

| Analog Cameras |

| IP Cameras (Fixed) |

| PTZ Cameras |

| Thermal and Infra-Red Cameras |

| 4K/Ultra-HD Cameras |

| SD |

| HD |

| Full-HD |

| 4K and Above |

| Fixed |

| Mobile and Rapid-Deploy |

| Wired |

| Wireless/Cellular |

| Government and Public Safety |

| Transportation |

| Industrial and Manufacturing |

| BFSI |

| Retail and Malls |

| Hospitality and Healthcare |

| Educational Institutions |

| Rest of End-User Vertical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By CCTV Camera Type | Analog Cameras | ||

| IP Cameras (Fixed) | |||

| PTZ Cameras | |||

| Thermal and Infra-Red Cameras | |||

| 4K/Ultra-HD Cameras | |||

| By Resolution | SD | ||

| HD | |||

| Full-HD | |||

| 4K and Above | |||

| By Installation Type | Fixed | ||

| Mobile and Rapid-Deploy | |||

| By Connectivity | Wired | ||

| Wireless/Cellular | |||

| By End-User Vertical | Government and Public Safety | ||

| Transportation | |||

| Industrial and Manufacturing | |||

| BFSI | |||

| Retail and Malls | |||

| Hospitality and Healthcare | |||

| Educational Institutions | |||

| Rest of End-User Vertical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the CCTV market expected to grow through 2031?

The CCTV market is forecast to advance at a 16.28% CAGR between 2026 and 2031, reaching USD 123.52 billion by the end of the period.

Which camera type currently dominates global sales?

IP cameras lead, holding 47.80% of global revenue in 2025 thanks to seamless IT integration and Power-over-Ethernet deployment.

Why are 4K cameras gaining momentum across deployments?

Regulators and operators need forensic-grade footage that allows face or license-plate recognition at long range, a requirement driving 4K units to an 18.20% CAGR through 2031.

What is the principal restraint on facial-recognition cameras?

Legal actions and policy bans in Europe and North America classify real-time facial recognition as high-risk processing, leading many buyers to disable biometric modules.

Page last updated on: