United States Video Surveillance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

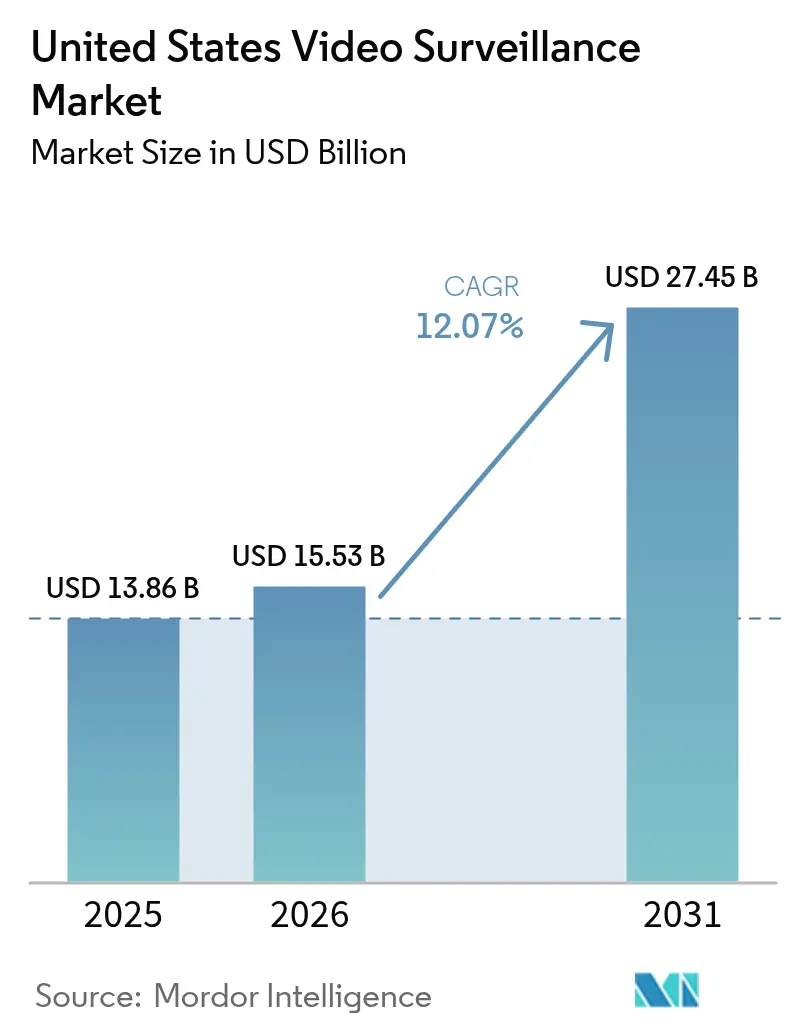

| Base Year Market Size (2025) | USD 13.86 Billion |

| Market Size (2026) | USD 15.53 Billion |

| Market Size (2031) | USD 27.45 Billion |

| Growth Rate (2026 - 2031) | 12.07% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Video Surveillance Market Analysis by Mordor Intelligence

The United States Video Surveillance Market size in 2026 is estimated at USD 15.53 billion, growing from 2025 value of USD 13.86 billion with 2031 projections showing USD 27.45 billion, growing at 12.07% CAGR over 2026-2031.

The United States video surveillance industry is undergoing a significant technological transformation, driven by the integration of advanced analytics and AI surveillance capabilities. The emergence of sophisticated surveillance technology solutions has expanded beyond traditional security applications into business intelligence and operational efficiency tools. According to the National Retail Federation, approximately 40% of retailers have reported increased fraud detection capabilities in multichannel sales environments, highlighting the growing importance of integrated video surveillance systems. The industry has witnessed notable innovations, such as Amazon's AWS Panorama technology, which enables customized deep learning and video analytic applications for security cameras regardless of manufacturer, demonstrating the market's evolution toward more sophisticated solutions.

The integration of video surveillance with Internet of Things (IoT) technology has revolutionized monitoring capabilities and data collection methods. Modern smart surveillance solutions now incorporate multiple IoT sensors that can detect environmental factors such as air quality, noise levels, and vibrations, providing comprehensive monitoring beyond visual data. This integration has particularly impacted the transportation sector, where March Networks secured a significant $4 million contract to implement advanced video monitoring solutions across an entire bus fleet in California, incorporating cloud-based monitoring and hybrid transit recording capabilities. The convergence of IoT and video surveillance has enabled more proactive security measures and enhanced operational insights.

The adoption of surveillance technology across various industry verticals has expanded significantly, with particular emphasis on retail, banking, and transportation sectors. In the banking sector, financial institutions are increasingly implementing advanced electronic surveillance systems to combat security threats, while retailers are leveraging video analytics for both security and customer behavior analysis. Edge360, a service-disabled veteran-owned small business, launched its Surveill VMS in July 2023, initially developed for government applications but expanded to serve the private sector, demonstrating the growing demand for sophisticated digital surveillance solutions across industries. The technology has evolved to support multiple applications, from security monitoring to business intelligence gathering.

Privacy and security considerations have become paramount in the video surveillance landscape, particularly as systems become more sophisticated and interconnected. The industry faces ongoing challenges in balancing enhanced security capabilities with privacy concerns, as evidenced by the increasing scrutiny of facial recognition technologies and data protection measures. According to an Insurance Zebra survey, while 46.9% of Americans don't have home security cameras installed, those who do are increasingly demanding systems with advanced privacy protection features and secure data transmission protocols. The industry has responded with innovations in encryption technologies and privacy-preserving analytics, ensuring that surveillance technology systems maintain security while protecting individual privacy rights.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Video Surveillance Market Trends and Insights

Rising Security Concerns and Crime Prevention Needs

The increasing focus on security and crime prevention has become a significant driver for the United States video surveillance market. According to FBI data from October 2022, while the national burglary rate showed improvement, dropping to 271.1 incidents per 100,000 people in 2021 from 308 incidents in the previous year, the ongoing security concerns continue to drive the adoption of security camera systems. The potential threat of criminal activities has prompted authorities to install advanced surveillance equipment across various locations, with cities like Chicago implementing extensive networks of tens of thousands of cameras and cities like New Orleans, New York, and Atlanta deploying plug-in surveillance networks that integrate private business and residential feeds into crime centers.

The Department of Homeland Security's initiative to provide billions of dollars in security grants to state agencies for installing video surveillance cameras demonstrates the government's commitment to enhancing public safety infrastructure. This is further evidenced by the implementation of sophisticated surveillance technologies by law enforcement agencies, which are increasingly integrating networked cameras, automated license plate readers, and predictive policing software with AI-enhanced video analytics. The development of real-time crime centers (RTCCs) as part of state-level government bodies has led to the identification of more than 80 RTCCs across 29 states, highlighting the growing emphasis on comprehensive surveillance infrastructure.

Technological Advancements in Video Analytics and AI Integration

The integration of artificial intelligence and advanced analytics capabilities has emerged as a crucial driver for the United States video surveillance market. The industry has witnessed significant advancements in video analytics applications, with systems now capable of performing multiple functions simultaneously, including real-time detections and alerts, video search, and business intelligence gathering without requiring additional hardware installation. These technological improvements have enabled more efficient monitoring and analysis of surveillance footage, with AI-powered systems capable of detecting and analyzing various scenarios, from security breaches to customer behavior patterns.

The evolution of facial recognition technology and smart analytics has particularly transformed the surveillance landscape. Cities like Chicago and Detroit have adopted facial surveillance systems, with Detroit's million-dollar system capable of scanning live video from cameras located at businesses, schools, health clinics, and apartment buildings. The integration of deep learning techniques has enhanced the capability of surveillance systems to provide actionable insights, with features such as high-speed person finder or tracker solutions finding applications in various sectors, from airport security to shopping mall surveillance. The development of real-time video processing with video analytics has enabled faster data aggregation and visualization into dashboards, driving business insights beyond traditional security applications.

Growing Smart Home Integration and Residential Security Demands

The emergence of smart homes has significantly elevated the role of video surveillance systems in the residential segment, driving market growth through increased consumer adoption. According to industry surveys, among the 26% of US broadband households planning to purchase smart video doorbells, a majority considered artificial intelligence and advanced analytics capabilities as crucial features in their selection process. This consumer preference has led to the development of more sophisticated residential surveillance systems that combine traditional security features with smart home integration capabilities, offering homeowners comprehensive monitoring and control solutions.

The residential surveillance market has evolved to offer systems equipped with advanced features such as motion detection, night vision, and integration with broader home automation systems. Manufacturers have responded to this demand by introducing innovative products, such as touchless video doorbells with internal video analytics that can detect visitors standing on doormats and trigger automated responses. The integration of these surveillance systems with mobile applications has enabled remote monitoring and control capabilities, allowing homeowners to manage their security systems remotely while receiving instant notifications of potential security events. This convergence of smart home technology with security features has created a more robust and user-friendly surveillance ecosystem for residential applications.

Segment Analysis

Video Management Systems and Storage Segment in United States Video Surveillance Market

Video Management Systems and Storage represent the largest segment in the United States video surveillance market, commanding approximately 47.35% market share in 2025. The segment's dominance is driven by the increasing need for sophisticated video management system solutions that can handle massive volumes of surveillance data from multiple sources. The rising adoption of cloud-based video management systems, particularly in enterprise and government sectors, has significantly contributed to this segment's market leadership. Organizations are increasingly investing in advanced storage solutions to comply with data retention regulations and leverage video data for business intelligence. The integration of artificial intelligence and deep learning capabilities within VMS platforms has further enhanced their value proposition, enabling automated video analysis and intelligent decision-making capabilities.

Video Analytics Segment in United States Video Surveillance Market

The Video Analytics segment is experiencing the most rapid growth in the United States video surveillance market, with an expected growth rate of approximately 14.72% during 2026-2031. This accelerated growth is primarily driven by the increasing integration of artificial intelligence and deep learning technologies in video surveillance systems. The segment is witnessing strong demand from various sectors, including retail, transportation, and smart cities, where advanced analytics capabilities are being deployed for applications ranging from facial recognition to crowd behavior analysis. The adoption of video analytics is further boosted by its ability to transform raw video footage into actionable intelligence, enabling proactive security measures and operational optimization. Recent developments in edge computing and AI-powered analytics have made these solutions more accessible and efficient, contributing to their widespread adoption across different industry verticals.

Remaining Segments in United States Video Surveillance Market by Type

The Cameras segment continues to be a fundamental component of the video surveillance market, encompassing a wide range of products from basic surveillance cameras to sophisticated PTZ and thermal imaging devices. This segment has evolved significantly with the integration of advanced features such as high-resolution imaging, night vision capabilities, and built-in analytics processing power. The continuous innovation in camera technology, including the development of AI-enabled cameras and multi-sensor devices, maintains its crucial role in the overall surveillance ecosystem. The segment's steady growth is supported by ongoing technological advancements and the increasing demand for high-quality video capture capabilities across various applications.

Segment Analysis: By End User

National Infrastructure and City Surveillance Segment in United States Video Surveillance Market

The National Infrastructure and City Surveillance segment dominates the United States video surveillance market, accounting for approximately 47% of the total market share in 2024. This segment's prominence is driven by increasing government initiatives regarding mandatory installations of video cameras and the rising adoption of advanced surveillance solutions across major cities. Cities like Washington have implemented sophisticated movement analytics programs that utilize data from video cameras to identify and track various entities moving through the city, including vehicles, buses, pedestrians, and bikes. The integration of artificial intelligence and deep learning technologies has enhanced the capabilities of city surveillance systems, enabling features like facial recognition, real-time video processing, and advanced analytics for law enforcement agencies. Additionally, the deployment of plug-in network surveillance networks in cities like Chicago, New Orleans, New York, and Atlanta, where private businesses and homes provide feeds integrated into crime centers, has significantly expanded the scope of city-wide surveillance infrastructure.

Transportation Segment in United States Video Surveillance Market

The Transportation segment in the United States video surveillance market is experiencing significant transformation, with an expected growth rate of approximately 12% during 2024-2029. This growth is primarily driven by the increasing integration of advanced video analytics solutions in public transportation systems, railways, and logistics operations. The sector is witnessing a shift towards AI-powered video monitoring systems that can automatically analyze railroad video data, supporting safety research and operational efficiency. The implementation of sophisticated surveillance solutions in transit authorities has led to the adoption of hybrid systems that support both analog and IP cameras, allowing transportation agencies to migrate to IP video cost-effectively. Furthermore, the integration of video analytics with Department of Transportation (DoT) requirements for vehicle safety checks and the rising demand for cargo security monitoring are contributing to the segment's rapid growth.

Remaining Segments in United States Video Surveillance Market End-User Segmentation

The Commercial segment maintains a strong presence in the market, driven by the growing adoption of surveillance equipment in banking, financial institutions, and office spaces. The Retail segment focuses on loss prevention and customer behavior analytics, while the Residential segment is experiencing growth due to increasing smart home adoption and security concerns. These segments are witnessing technological advancements through the integration of AI-based analytics, cloud storage solutions, and remote monitoring capabilities. The Other End Users segment, which includes educational institutions, healthcare facilities, and manufacturing sectors, continues to adopt video surveillance systems for various applications ranging from campus security to patient monitoring and industrial safety compliance.

Value Chain Analysis

The United States video surveillance value chain spans camera and edge-device OEMs, software layers (VMS, video analytics, and identity/biometric modules), storage and cloud infrastructure, and downstream deployment by distributors, systems integrators, and managed security/VSaaS providers serving commercial, government, transportation, and residential buyers. As deployments move from passive recording toward AI-assisted detection and workflow automation, the software and services layer has gained share, supported by platforms such as AWS Panorama and newer VMS and video-agent capabilities introduced in 2026 (for example, RADSight 2.0 and vision language model-driven security operations features).

Procurement eligibility and compliance checks have become a defining gating factor for the chain, particularly for public sector and regulated enterprise deployments, due to restrictions tied to NDAA Section 889 and evolving covered-entity screening. That dynamic is reinforcing demand for interoperable ecosystems (for example, ONVIF-compatible camera support) and for tighter integration between access control, video, and analytics, as highlighted by Honeywell and Rhombus collaborating on cloud-connected, AI-powered video security and access solutions in March 2026. In response, channel partners increasingly package compliant hardware, cybersecurity hardening, and cloud storage/VMS subscriptions into unified proposals, while end users are placing more emphasis on lifecycle services such as maintenance, software updates, and retention-ready storage management.

Competitive Landscape

Top Companies in United States Video Surveillance Market

The United States video surveillance market is characterized by continuous innovation and strategic developments from major players like Hikvision, Dahua, Axis Communications, Honeywell, and Cisco Systems. Companies are heavily investing in artificial intelligence (AI) and machine learning capabilities to enhance their surveillance solution offerings, while simultaneously developing cloud surveillance solutions to meet evolving customer demands. The industry demonstrates strong operational agility through rapid product development cycles and vertically integrated operations, enabling quick responses to market changes. Strategic partnerships with technology providers, particularly in cloud services and analytics, have become increasingly common as companies seek to strengthen their market positions. Geographic expansion strategies focus on establishing a local presence through technical support offices, while product portfolio diversification emphasizes end-to-end solutions incorporating hardware, software, and services.

Market Dominated by Global Technology Conglomerates

The United States video surveillance market exhibits a complex competitive structure with a mix of global technology conglomerates and specialized security solutions providers. Large multinational corporations leverage their extensive R&D capabilities and established distribution networks to maintain market leadership, while specialized players focus on niche segments with innovative solutions. The market demonstrates moderate consolidation, with major players continuously expanding their presence through strategic acquisitions of smaller, innovative companies, particularly those specializing in AI and analytics capabilities.

The industry has witnessed significant merger and acquisition activity, particularly focused on integrating complementary technologies and expanding market reach. Companies are increasingly pursuing vertical integration strategies, acquiring component manufacturers and software developers to strengthen their supply chains and enhance product offerings. The competitive landscape is further shaped by regulatory factors, particularly restrictions on Chinese manufacturers, which have created opportunities for US-based companies to expand their market share while fostering partnerships with domestic technology providers.

Innovation and Adaptability Drive Market Success

Success in the United States video surveillance market increasingly depends on companies' ability to develop comprehensive surveillance solution that integrate advanced technologies while maintaining strong cybersecurity measures. Incumbent players must focus on continuous innovation in AI-powered analytics, cloud integration, and edge computing capabilities while building strong partner ecosystems to maintain their market positions. The ability to provide scalable solutions that address specific vertical market needs, combined with strong after-sales support and professional services, has become crucial for maintaining a competitive advantage.

Market contenders can gain ground by focusing on specialized market segments, developing innovative solutions for emerging use cases, and building strong relationships with system integrators and channel partners. The increasing emphasis on privacy concerns and data protection regulations requires companies to demonstrate robust compliance capabilities and transparent data handling practices. Success also depends on the ability to adapt to changing end-user preferences, particularly the shift towards video surveillance as a service models and integrated security solutions that combine physical and cybersecurity capabilities.

United States Video Surveillance Industry Leaders

Dahua Technology Co. Ltd

Hikvision Digital Technology Co. Ltd

Hanwha Techwin

Schneider Electric SE

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Federal and critical infrastructure requirements are creating specific whitespace for vendors and integrators that can deliver compliant, fully maintained, and auditable surveillance deployments. In June 2026, the U.S. General Services Administration issued ADM 3490.1 on baseline minimum security standards in federally owned facilities, explicitly calling for video surveillance systems to be maintained and operable in alignment with Interagency Security Committee risk management practices, which supports opportunities in modernization, maintenance services, and refresh cycles across federally managed sites. At the same time, procurement and supply constraints tied to the FCC Covered List and related restrictions are pushing enterprises and government-adjacent buyers to requalify product stacks and strengthen vendor due diligence, expanding demand for NDAA-aligned alternatives and for migration projects that replace restricted devices.

Product momentum is moving toward cloud-native and AI-assisted operations, creating opportunities for platforms that reduce operator workload and improve investigation speed. For example, Brivo introduced Eeva (March 2026), an AI video agent integrated with Eagle Eye VMS for natural language-driven monitoring, and Honeywell worked with Rhombus (March 2026) to offer cloud-connected, AI-powered video security and access solutions for enterprise customers. In biometric and vision AI, Department of Homeland Security SAFETY Act DT&E designations, such as the July 2026 designation for Rank One Computing’s ROC Watch, can be a differentiator for deployments in higher-liability environments (public venues and critical infrastructure), where risk transfer and governance requirements often influence technology selection.

Recent Industry Developments

- July 2026: Rank One Computing (ROC) announced that ROC Watch received a U.S. Department of Homeland Security SAFETY Act Developmental Testing and Evaluation (DT&E) designation. The designation provides liability protections that can accelerate adoption in critical infrastructure and higher-risk venues, strengthening the case for vision AI platforms in regulated deployments.

- August 2025: Hanwha Vision secured a contract to modernize surveillance at the Music City Center in Nashville, Tennessee, deploying more than 700 cameras. Large venue wins of this scale reinforce the shift toward unified, enterprise-grade surveillance architectures and create follow-on opportunities in VMS, storage, and lifecycle services.

- April 2024: A federal appellate decision in the D.C. Circuit addressed challenges tied to U.S. supply-chain security rules affecting covered telecommunications and video surveillance equipment procurement. The ruling underscored the durability of federal restrictions, adding urgency for buyers and integrators to audit installed bases and standardize compliant sourcing for new projects.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated in the United States from video surveillance solutions used to capture, manage, store, and analyze video for security and monitoring across public and private sites.

Scope exclusions: We exclude consumer-only smart home gadgets that are not used as part of a broader surveillance setup, and we exclude unrelated physical security items like access control and intrusion alarms.

Segmentation Overview

- Type

- Cameras

- Video Management Systems and Storage

- Video Analytics

- End User

- Commercial

- Retail

- National Infrastructure and City Surveillance

- Transportation

- Residential

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on demand drivers and procurement patterns for surveillance equipment and related software. We rely on public sources such as U.S. Census construction and shipments data, Bureau of Labor Statistics cost trends, U.S. International Trade Commission trade statistics, NIST cybersecurity and technology guidance, and FCC-related equipment references where relevant for connected devices.

To keep the model realistic, we also reviewed company annual reports, investor presentations, official product documentation, and credible press coverage around public safety projects and enterprise security upgrades. A paid subscription that aggregates company financials and news was used selectively to standardize revenue splits and reduce the risk of double counting across subsidiaries. These desk sources are illustrative rather than exhaustive, and we also used other public references for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on checking what is actually being bought and deployed across the United States, then how budgets are split between cameras, video management, storage, and analytics. We spoke with a mix of manufacturers, channel partners, installers, and large end users covering commercial facilities, retail, transportation, city surveillance, and residential programs. Where end-use numbers looked inconsistent, we refined assumptions through follow-up re-checks.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 16% | |

| Mid tier: 55% | Functional/Unit leaders: 24% | |

| Smaller Players: 20% | Managers: 60% |

Market-Sizing & Forecasting

Our sizing begins with a top-down build that reconstructs the national demand pool using construction activity, facility expansion and retrofit cycles, and public safety and transportation project pipelines, and then translates those into surveillance spend. After that, we use selective bottom-up approximations, including sampled camera shipments and average selling price ranges, typical system sizes by site type, and channel checks on integrator project values. If the two views do not align, we adjust the total to reflect the stronger signal.

Key model inputs include the shift from analog to IP cameras, the installed base refresh rate, storage needs per camera (driven by resolution and retention policies), the adoption curve of video analytics and VMS upgrades, and labor and installation cost inflation that affects project timing. For forecasting, we apply scenario analysis supported by expert views on capital spending cycles, city surveillance funding, and enterprise security modernization, and we smooth scenario outputs to avoid unrealistic year-to-year jumps. Where bottom-up signals are missing for a niche end use, we apply conservative penetration ranges that are validated through interviews, then stress-test them against related spend indicators.

Data Validation & Update Cycle

Model outputs are checked against independent indicators such as import trends for camera-related equipment, construction and retrofit activity signals, and the pace of large project announcements in transportation and municipal surveillance. When a variance is detected, we re-check assumptions like camera counts per site, retention-driven storage sizing, or service attach rates. Experts are re-contacted if the change is material.

Before sign-off, the work goes through a multi-step review so calculation logic, unit economics, and year alignment stay consistent across the dataset. The report is refreshed annually, with interim updates when there are material events that can move demand or pricing. Right before delivery, a final pass incorporates the latest public releases so clients receive the most current view.

Mordor Intelligence's United States Video Surveillance Market Size Compared Against Other Published Estimates

Published market sizes for United States video surveillance do not always match because studies often use different component boundaries, base years, and ways to treat services and software that sit around the camera sale. Even when the growth rate looks similar, the starting point can change a lot based on what gets counted and how quickly pricing and mix-shift assumptions are refreshed.

Import trends for camera-related equipment, public project signals, and installer feedback on refresh cycles are the checks that keep the Mordor Intelligence USD 13.86 B (2025) estimate tied to cameras, video management and storage, and video analytics, rather than folding in adjacent physical security categories or broad security labor pools.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.86 B (2025) | |

| Global Consultancy A | USD 18.84 B (2024) | Uses a broader component stack (hardware, software, and services) and an earlier base year, which can lift totals when installation, maintenance, and managed services are fully counted and price escalation is embedded sooner. |

| Industry Publisher B | USD 12.34 B (2024) | Anchors sizing on a different base year and applies a component split that can understate near-term upgrades if refresh cycles and higher-resolution retention-driven storage needs are not fully reflected in the starting-year demand. |

The spread is largely explained by what each source includes around the core system and how the base year is built. When scope and assumptions are stated in plain terms and cross-checks are run against observable demand signals, the result is easier for us to replicate and update year after year.

Key Questions Answered in the Report

How big is the United States Video Surveillance Market?

The United States Video Surveillance Market size is expected to reach USD 15.53 billion in 2026 and grow at a CAGR of 12.07% to reach USD 27.45 billion by 2031.

What is the current United States Video Surveillance Market size?

In 2026, the United States Video Surveillance Market size is expected to reach USD 15.53 billion.

Who are the key players in United States Video Surveillance Market?

Dahua Technology Co. Ltd, Hikvision Digital Technology Co. Ltd, Hanwha Techwin, Schneider Electric SE and Robert Bosch GmbH are the major companies operating in the United States Video Surveillance Market.

What years does this United States Video Surveillance Market cover, and what was the market size in 2025?

In 2025, the United States Video Surveillance Market size was estimated at USD 15.53 billion. The report covers the United States Video Surveillance Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the US Video Surveillance Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: