Video Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

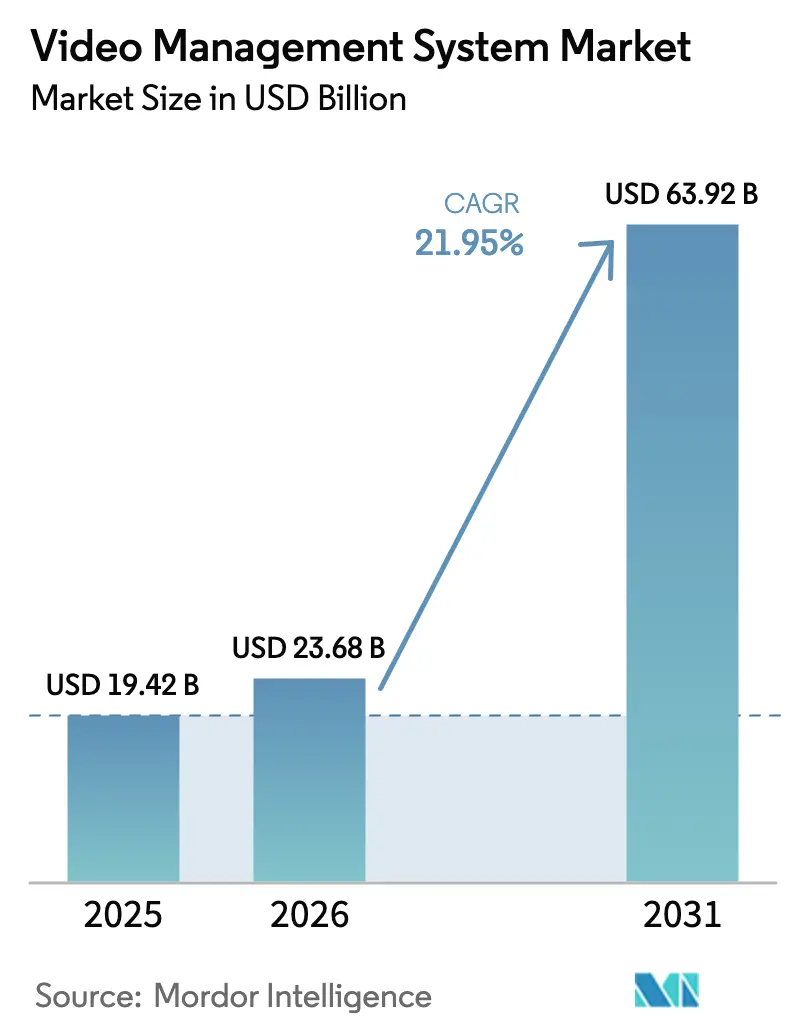

| Market Size (2026) | USD 23.68 Billion |

| Market Size (2031) | USD 63.92 Billion |

| Growth Rate (2026 - 2031) | 21.95% CAGR |

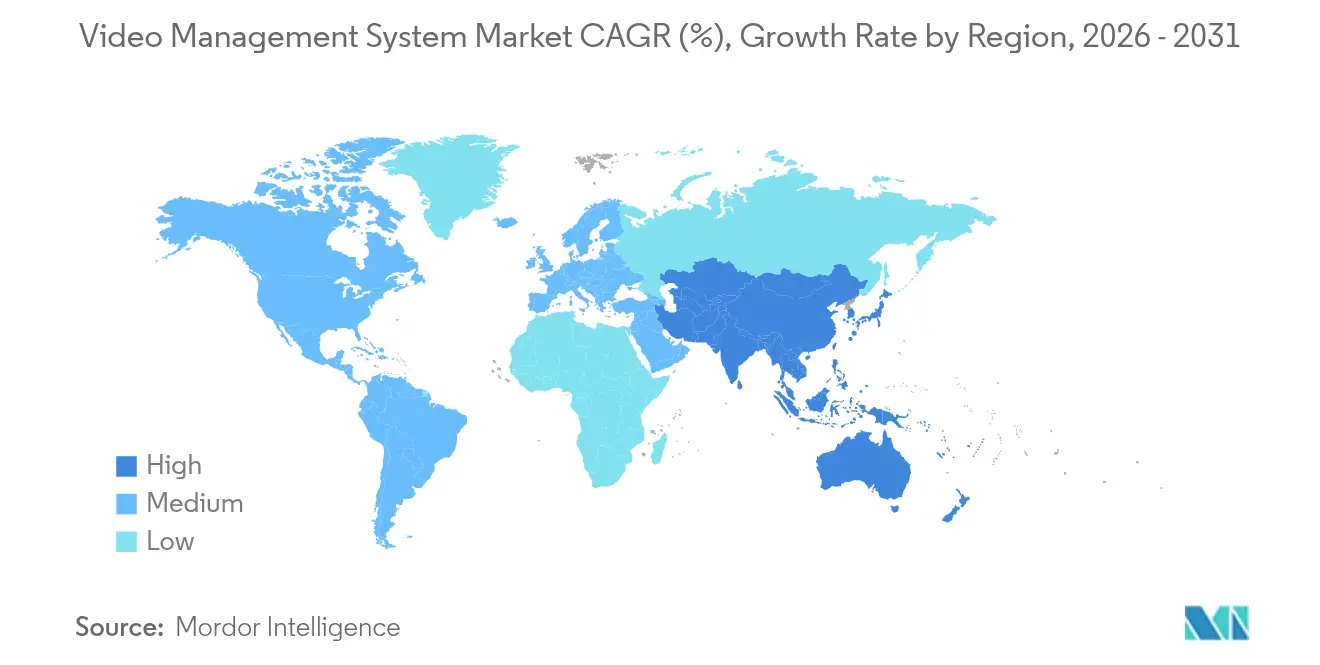

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

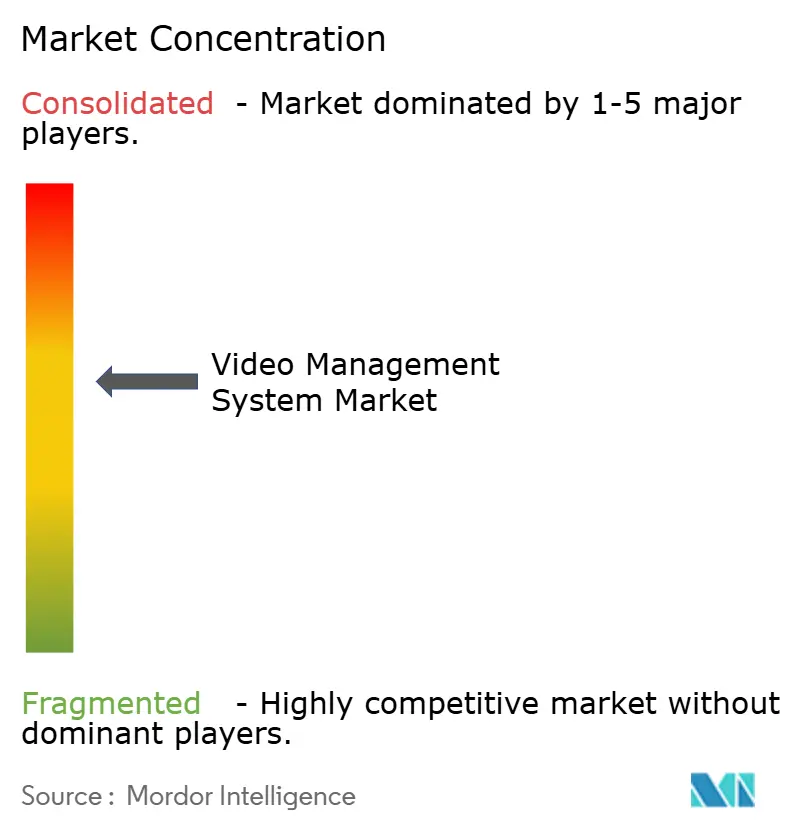

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Management System Market Analysis by Mordor Intelligence

video management system market size in 2026 is estimated at USD 23.68 billion, growing from 2025 value of USD 19.42 billion with 2031 projections showing USD 63.92 billion, growing at 21.95% CAGR over 2026-2031. This growth stems from three reinforcing forces: regulatory mandates that require higher-definition retention, ongoing analog-to-IP migration cycles, and digital transformation projects that reposition video from a passive record to an active data asset. Vendors that bundle open-platform software with cloud connectivity are capturing share as buyers seek vendor-agnostic architectures, while AI-ready cameras and rising 5G backhaul capacity remove historical bandwidth bottlenecks. The video management system market also benefits from falling per-camera prices, yet margin pressure is offset by demand for premium analytics licenses and managed services contracts.

Key risks continue to temper adoption. Municipal buyers face budget strain when 4K capture multiplies storage costs, European operators wrestle with privacy litigation exposure, and Middle-Eastern data-sovereignty rules complicate cross-border VSaaS strategies. Competitive dynamics remain moderately consolidated: established VMS publishers defend installed bases, hardware giants off-load non-core security units, and cloud-native entrants press subscription pricing. Long-term opportunity centers on hybrid deployment models that blend edge processing with centralized governance, positioning the video management system market for sustained double-digit expansion.

Key Report Takeaways

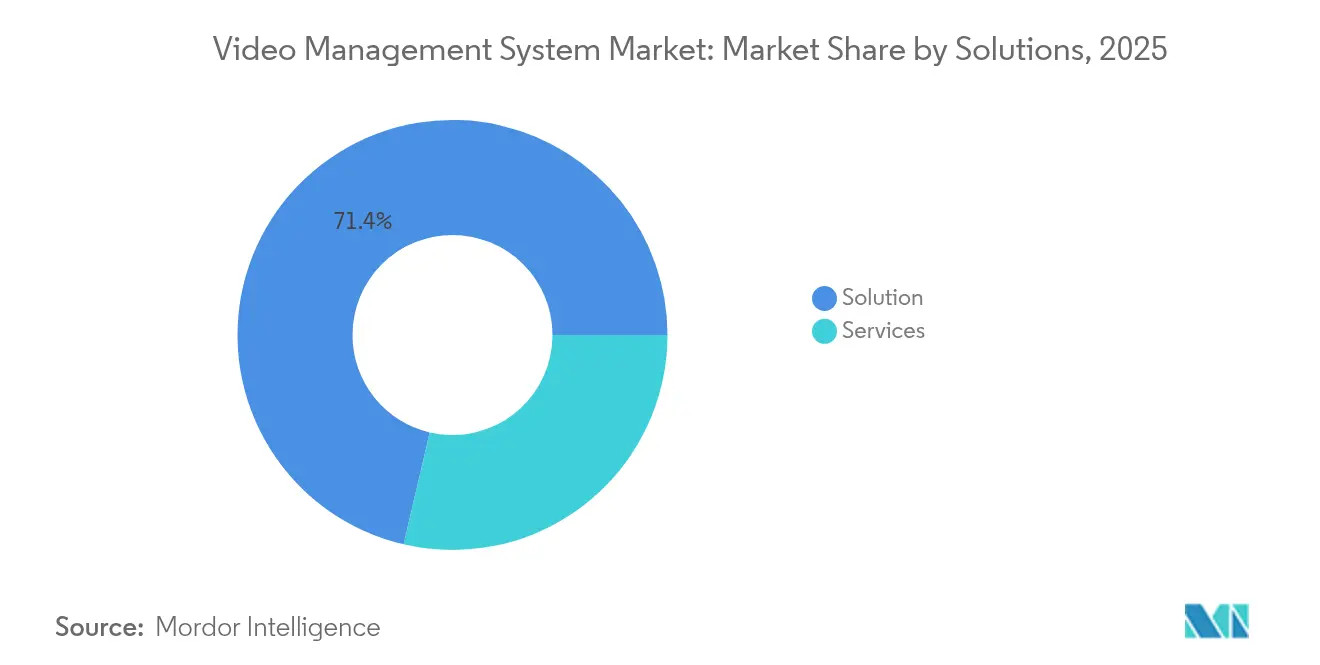

- By component, Solutions commanded 71.35% of the video management system market share in 2025; Services are forecast to grow at 23.6% CAGR through 2031.

- By technology, IP-based platforms held 67.20% share in 2025, whereas analog alternatives posted low-single-digit growth.

- By deployment model, On-premise installations retained 70.30% share in 2025; Cloud/VSaaS usage is expanding at 21.8% CAGR.

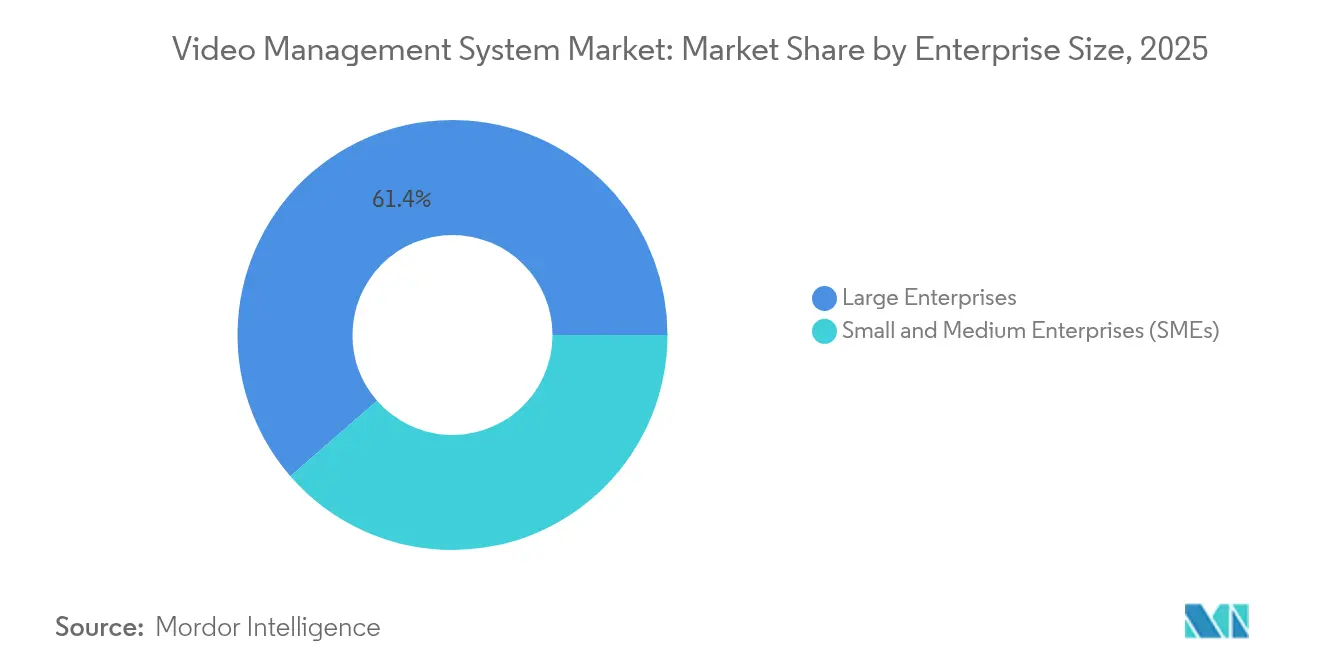

- By enterprise size, Large enterprises accounted for 61.40% of 2025 revenue; SMEs are accelerating at 23.1% CAGR.

- By end-user sector, Government & Public Safety captured 26.55% revenue in 2025; Retail applications are rising fastest at 22.35% CAGR.

- By geography, Asia Pacific led with 42.40% revenue share in 2025, while Middle East & Africa is projected to compound at 23.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Video Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Migration from analog DVRs to open-platform IP VMS across mid-size U.S. city surveillance | +4.2% | North America, spillover to Latin America | Medium term (2-4 years) |

| EU NIS2 and GDPR retention rules accelerating HD-storage upgrades | +3.8% | Europe, global compliance influence | Short term (≤ 2 years) |

| AI-powered real-time analytics adoption in APAC smart-transport hubs | +4.5% | Asia-Pacific core, expansion to MEA | Medium term (2-4 years) |

| Retail POS-integrated loss-prevention driving chain-wide roll-outs in North America | +3.1% | North America, expanding to Europe | Short term (≤ 2 years) |

| Cloud-managed VSaaS subscriptions among European SMEs | +3.9% | Europe, adoption in Asia-Pacific North America | Medium term (2-4 years) |

| NDAA-driven replacement of PRC OEM software in U.S. federal sites | +2.8% | United States, influence on allies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Migration from Analog DVRs to Open-Platform IP VMS across Mid-size U.S. City Surveillance

Municipal modernization has moved beyond routine refresh cycles as legacy DVRs near end-of-life and open-platform IP architectures show measurable operational synergy with traffic, emergency-response, and public-works platforms.[1]“NDAA-Compliant Security Technology: Cameras and Systems Explained,” Critical Technology Solutions, criticalts.com Cities between 50,000 and 250,000 residents unlock federal-grant funding by specifying NDAA-compliant equipment, thereby avoiding vendor lock-in and future-proofing integrations. Procurement teams now evaluate total-solution lifetime value rather than camera unit price, a shift that accelerates the video management system market.

EU NIS2 and GDPR Retention Rules Accelerating HD-Storage Upgrades

NIS2, in force since October 2024, obliges “Essential” and “Important” entities to preserve high-definition evidence with provable integrity, pushing enterprises toward encrypted, audit-ready storage that can scale for longer retention windows.[2]“Products – NIS2 Compliance for Industries White Paper,” Cisco, cisco.com Vendors offering automated lifecycle governance, role-based access, and immutability are gaining traction across multi-state operators, lifting premium-storage demand in the video management system market.

AI-Powered Real-Time Analytics Adoption in APAC Smart-Transport Hubs

Singapore’s Maritime & Port Authority is piloting AI-enabled collision prediction within its Next-Generation Vessel Traffic Management System, while Hong Kong railways employ camera-LiDAR analytics for obstacle detection.[3]“How Singapore's Maritime and Port Authority Is Crafting the Vessel Management System of the Future,” GovInsider, govinsider.asia These deployments showcase a pivot from reactive monitoring to predictive incident prevention, positioning APAC as a lighthouse for AI-centric transportation use cases in the video management system market.

Retail POS-Integrated Loss-Prevention Driving Chain-Wide Roll-Outs in North America

Retailers now correlate video streams with point-of-sale data to flag irregular transactions in real-time, trimming shrinkage and labor hours. High-frequency environments such as convenience and specialty chains see provable ROI, accelerating multi-store roll-outs and sustaining software-license demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TCO of 4K recording and storage outstripping municipal budgets | -2.8% | Global, acute in developing markets | Short term (≤ 2 years) |

| Scarcity of ONVIF-certified integrators in ASEAN | -1.9% | ASEAN core, spillover to Asia-Pacific | Medium term (2-4 years) |

| Data-sovereignty barriers to cross-border cloud VMS in Middle East | -1.7% | Middle East, global cloud influence | Long term (≥ 4 years) |

| Privacy-litigation risk curtailing AI analytics in the EU | -2.1% | Europe, global AI strategy influence | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

TCO of 4K Recording and Storage Outstripping Municipal Budgets

4K workflows triple data volumes, driving storage bids well beyond prior SDR systems. Wayne County, NY projected USD 120,000–192,000 in additional server spend, forcing program delays, while Baltimore County estimated USD 7.1 million five-year outlays including staffing. Absent grant offsets, municipalities downscale resolution or retention, tempering the broader video management system market.

Scarcity of ONVIF-Certified Integrators in ASEAN

Rising multi-vendor requirements expose a limited talent pool; few firms hold ONVIF credentials, lengthening deployment timelines and raising project costs. This skill gap slows adoption in Thailand, Vietnam and Indonesia despite strong demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Managed Services Expand Recurring Revenue

Solutions retained 71.35% revenue share in 2025, reinforcing hardware-plus-license sales as the primary entry point into the video management system market. However, services revenue is scaling at 23.6% CAGR as clients outsource integration, update management, and health monitoring. Large integrators now bundle multi-year support plans that, over a five-year horizon, eclipse upfront license outlays, an evolution that heightens stickiness and lifts lifetime value.

Subscription frameworks also resonate with CFOs seeking predictable opex. The shift has sparked partner-program redesigns, rewarding channel partners that deliver outcome-based SLAs rather than one-time installs. For vendors, higher services mix cushions margin compression in commoditized camera hardware.

By Technology: IP Platforms Cement Mainstream Status

IP-based deployments represented 67.20% of 2025 revenue and continue to grow at 22.55% CAGR, signaling that analog decline remains a multi-year story. Competitive RFPs routinely specify ONVIF profile support, PoE power, and multi-bitrate streaming, eliminating analog contenders outside budget-sensitive edge cases. The video management system market size for IP platforms is expanding in lock-step with fiber roll-outs and 5G fixed-wireless access, both of which remove last-mile constraints.

Beyond transport, IP architectures unlock software-defined upgrades. Features such as AI inference engines, cybersecurity patching, and zero-trust authentication can be delivered remotely, extending asset life and boosting ROI. Analog, by contrast, freezes functional capability at installation. Regulatory requirements for audit trails and secure encryption lean heavily toward digital formats, adding compliance impetus to IP adoption. As a result, the video management system market is witnessing secondary waves of analog-to-IP migration in education campuses and light-industrial estates that skipped the first cycle.

By Mode of Deployment: Hybrid Cloud Becomes the Default Path

On-premise systems still hold a 70.30% share, but cloud/VSaaS subscriptions are compounding at 21.8% CAGR with SMEs as early adopters. Enterprises now architect hybrid topologies: latency-sensitive video stays local, while metadata and analytics off-load to cloud nodes. This arrangement preserves bandwidth, satisfies data sovereignty statutes, and enables elastic computing for intensive AI tasks. The term “cloud first” has shifted to “cloud when it makes sense,” a pragmatic stance echoed in RFP language across banking, healthcare, and retail verticals.

Cost modeling further favors hybrid adoption. Storage tiering allows archival footage to reside in low-cost cloud buckets, trimming on-premise RAID investments. Vendors sweeten the proposition with consumption-based pricing, turning capital outlay into aligned operating expenses. As a result, the video management system market is transitioning from product-centric sales to platform subscriptions that bundle firmware, threat-intelligence feeds, and feature releases under one invoice.

By Architecture: Edge Computing Reduces Latency and Bandwidth

Centralized processing controlled 56.40% of 2025 spending, yet edge-enabled designs are forecast at 23.2% CAGR through 2031. AI-capable SoCs embedded in cameras now perform object detection and analytics locally, forwarding only metadata or alerts to command centers. This model slashes network load, a decisive factor for remote oil and gas facilities and highway traffic authorities. Vendors differentiate by offering federated-learning algorithms that train models across distributed nodes without raw-video transfer, satisfying privacy mandates while retaining global model accuracy.

Decentralization also improves resilience; if a WAN link fails, local nodes continue recording and decision-making. Cyber-architects appreciate the reduced attack surface when less data traverses the core. Consequently, procurement teams increasingly specify “edge-ready” capability even when they deploy traditional servers, future-proofing investments as AI cost curves decline. The video management system market thus evolves toward a continuum where processing happens wherever it is most efficient.

By Enterprise Size: SMEs Democratize Advanced Capabilities

Large enterprises generated 61.40% of 2025 revenue, reflecting multi-facility projects and stringent risk postures. Yet SME spend is climbing at 23.1% CAGR, powered by turnkey cloud offerings that remove integration headaches. Low-touch provisioning via QR code, AI-assisted camera positioning, and intuitive mobile apps appeal to resource-constrained operators who historically relied on basic NVRs. The video management system market thereby broadens from Fortune 500 corridors to independent retailers and mid-tier manufacturers.

Importantly, SME adoption shifts buying criteria from spec sheets to business outcomes. Store managers seek shrinkage reduction, while small logistics operators value real-time loading-dock visibility. Vendors respond with verticalized templates and analytics “recipes” that run out-of-box, shortening time-to-value. As SME churn among legacy DVR providers accelerates, incumbents must realign channel incentives and support structures to defend share.

By End-User Industry: Retail Takes the Growth Crown

Government & Public Safety preserved 26.55% share in 2025 thanks to large-scale municipal upgrades and federal compliance programs. However, retail use cases are scaling fastest at 22.35% CAGR, propelled by integration between video, POS, and inventory systems. Loss-prevention managers quantify ROI through measured shrinkage reduction, while marketing teams mine heat-maps and queue analytics to refine merchandising. The video management system market thus shifts from perimeter security to operational intelligence inside the store.

Other verticals maintain healthy pipelines. Airports integrate VMS with biometric access control to streamline passenger flow, banks fuse video with transaction logs for fraud detection, and hospitals leverage video for patient-safety monitoring and compliance. These varied requirements drive modular architecture demand, allowing customers to bolt on analytics without forklift upgrades.

Geography Analysis

Asia Pacific held 42.40% revenue share in 2025, underpinned by state-sponsored smart-city investments and fast 5G penetration. Chinese Tier-2 municipalities, Indian railway modernization, and Southeast Asian industrial parks all funnel capex into high-definition, AI-ready platforms. Singapore’s MPA deploys an AI-driven vessel-traffic system in 2025, exemplifying maritime adoption of VMS for predictive safety. Hong Kong’s railway hazard-detection project further illustrates APAC leadership in edge-analytics integration. The video management system market in the region also benefits from local manufacturing ecosystems that shorten supply chains and tailor products to regional compliance nuances.

Middle East & Africa is the fastest-growing region at 23.2% CAGR, buoyed by megacity initiatives in Riyadh, NEOM, and Lusail. Yet strict data-localization laws compel in-country cloud nodes or on-premise storage, influencing solution design and vendor selection. Market entrants capable of partnering with regional telecoms and hosting providers gain an execution edge. North America remains a technologically sophisticated buyer; NDAA replacement programs create steady demand, while retail chain consolidations drive POS-linked analytics purchases. Europe grows at a moderate clip as NIS2 and GDPR harmonize cyber and privacy expectations, spurring HD storage refreshes and cloud-managed VSaaS for SMEs. South America shows early-stage adoption as urbanization accelerates, though currency volatility and skills shortages temper scale. Across all regions, hybrid cloud and AI analytics form the unifying investment thesis driving the video management system market.

Mordor Intelligence provides coverage of the video management system market across other key regional markets, including Europe, Asia, and North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The 2024–2025 period marked active portfolio realignment. Bosch exited product manufacturing to focus on integration services, selling its USD 8 billion security unit to Triton Partners, signaling private-equity appetite for hardware assets. Milestone’s merger with Arcules fused on-premise VMS leadership with cloud VSaaS expertise, creating an end-to-end hybrid platform. Honeywell’s USD 4.95 billion purchase of Carrier’s Global Access Solutions expands its route-to-market and cross-sell potential, illustrating scale-driven synergy plays.

Strategy themes coalesce around three vectors. First, cloud migration: vendors integrate native VSaaS or acquire cloud specialists to hedge against slowing server-licensing growth. Second, AI differentiation: proprietary inference engines and open development kits aim to lock ecosystems. Third, cybersecurity assurance: NDAA compliance, secure-boot cameras, and CRA-aligned disclosure processes emerge as selling points. The video management system market thus rewards vendors that deliver holistic, secure, and analytically rich platforms.

Video Management System Industry Leaders

Milestone Systems

Genetec Inc

Bosch Security Systems GmbH

Honeywell International Inc

Dahua Technology Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Milestone Systems merged with Arcules to provide a unified on-premise-plus-cloud platform and accelerate addressable hybrid opportunities.

- January 2025: Honeywell closed the USD 4.95 billion acquisition of Carrier’s Global Access Solutions unit, broadening its security portfolio and cross-channel distribution.

- December 2024: Bosch finalized the sale of its Building Technologies security products business to Triton Partners, refocusing on solutions integration.

- October 2024: Genetec retained the 1 global VMS position per Omdia and Novaira Insights, consolidating leadership across regions.

Global Video Management System Market Report Scope

Video management systems are software-based platforms that facilitate the management and control of video surveillance cameras, recording devices, and other security-related components. These systems are commonly employed by businesses, governmental entities, and other entities that necessitate extensive surveillance and security oversight. It is a comprehensive system that enables organizations to monitor their facilities, resources, and personnel in real-time surveillance.

The video management system market is segmented by component (solution and services), technology (analog-based and IP-based), mode of deployment (on-premise and cloud), end-user industry (retail, airports, education, banking, healthcare, transportation and logistics, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solution |

| Services |

| Analog-based |

| IP-based |

| On-premise |

| Cloud / VSaaS |

| Centralized |

| Edge / Decentralized |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Government and Public Safety |

| Retail |

| Airports and Transportation |

| Banking and Finance |

| Healthcare |

| Education |

| Industrial and Logistics |

| Others (Stadia, Hospitality, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Solution | ||

| Services | |||

| By Technology | Analog-based | ||

| IP-based | |||

| By Mode of Deployment | On-premise | ||

| Cloud / VSaaS | |||

| By Architecture | Centralized | ||

| Edge / Decentralized | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-user Industry | Government and Public Safety | ||

| Retail | |||

| Airports and Transportation | |||

| Banking and Finance | |||

| Healthcare | |||

| Education | |||

| Industrial and Logistics | |||

| Others (Stadia, Hospitality, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the video management system market?

The video management system market size is USD 23.68 billion in 2026 and is projected to grow at 21.95% CAGR to USD 63.92 billion by 2031.

Which region generates the highest revenue?

Asia Pacific leads with 42.40% of global revenue, fueled by large-scale smart-city and transportation projects.

Why are services growing faster than products?

Rising system complexity and AI integration push end-users to outsource integration, updates, and monitoring, driving the services segment at 23.6% CAGR.

How fast is cloud adoption within VMS?

Cloud/VSaaS deployments are expanding at 21.8% CAGR as bandwidth improves and subscription models appeal to SMEs.

Page last updated on: