Market Overview

| Study Period | 2020 - 2031 |

|---|---|

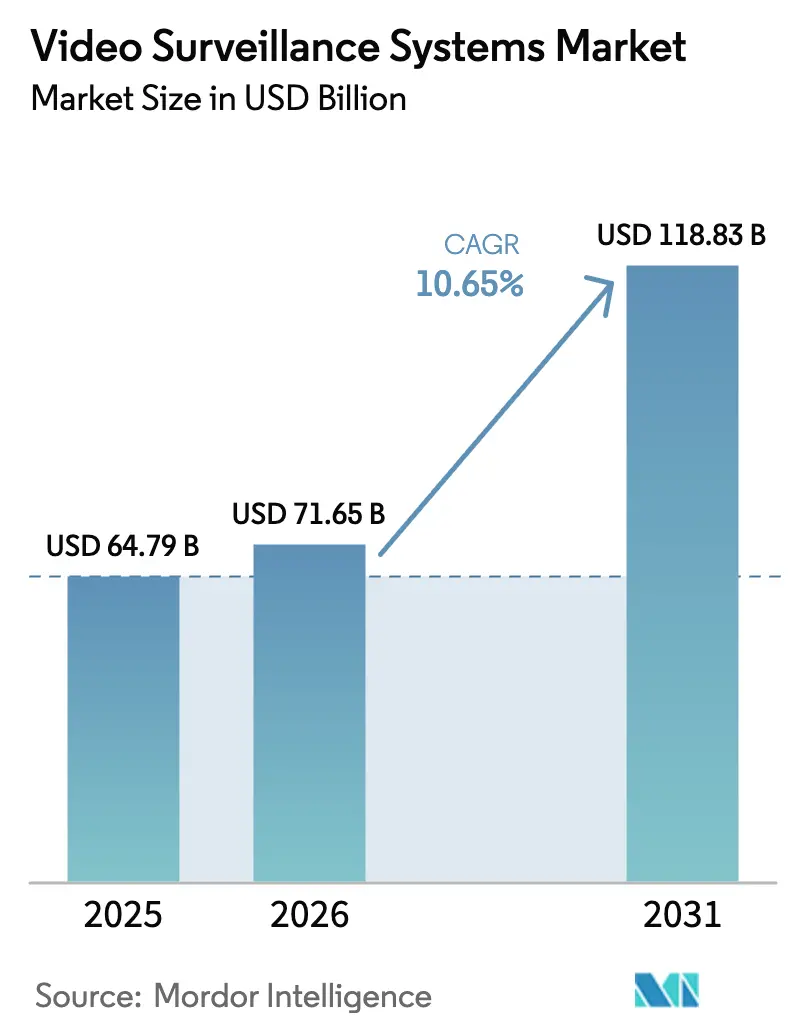

| Market Size (2026) | USD 71.65 Billion |

| Market Size (2031) | USD 118.83 Billion |

| Growth Rate (2026 - 2031) | 10.65% CAGR |

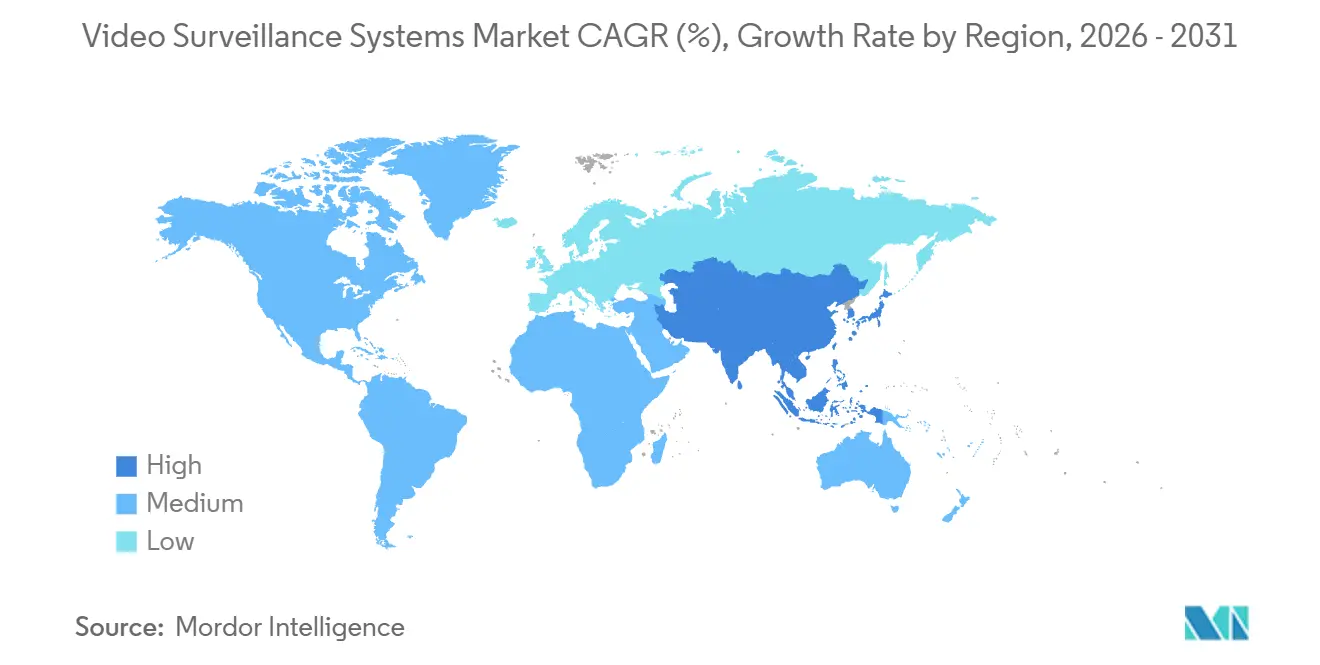

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

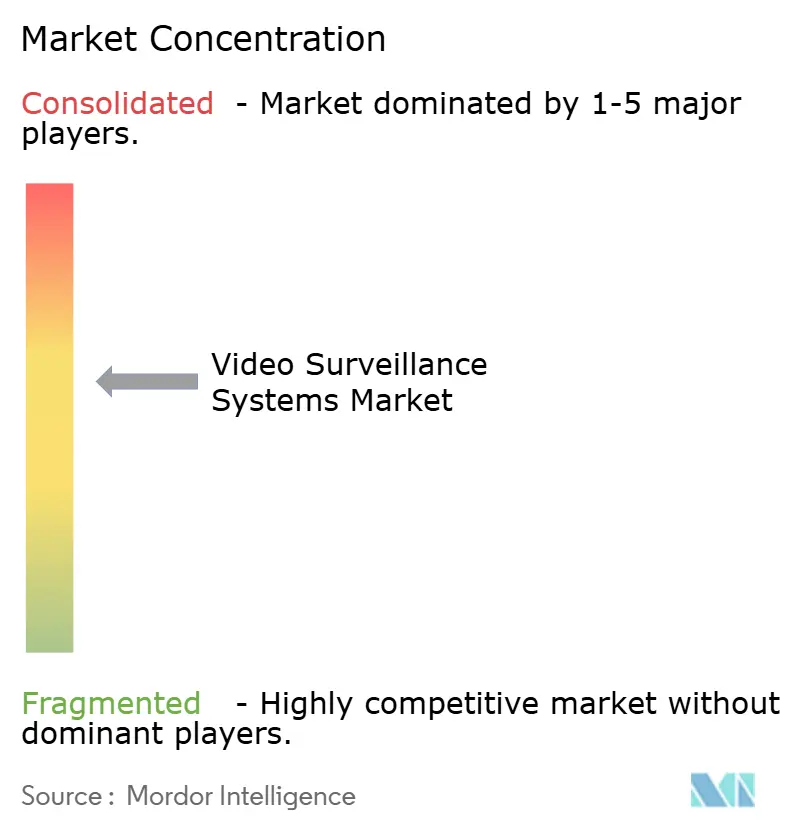

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Surveillance Systems Market Analysis by Mordor Intelligence

The Video Surveillance Systems Market size is projected to expand from USD 64.79 billion in 2025 and USD 71.65 billion in 2026 to USD 118.83 billion by 2031, registering a CAGR of 10.65% between 2026 to 2031. Mandatory migration from analog to IP, rapid 5G roll-outs, and camera-level artificial intelligence are shifting value from passive recording to real-time insight platforms. European municipalities are swapping legacy CCTV for encrypted IP networks that meet cybersecurity directives, while Asian transportation hubs rely on 5G backhaul to stream ultra-high-definition video with sub-20-millisecond latency. Edge analytics processors now cut cloud transmission costs by 40%-60% and reduce decision latency below 200 milliseconds, unlocking industrial automation and safe-city use cases. National safe-city grants across the Middle East and ESG-linked insurance discounts are accelerating refresh cycles, although chiplet shortages for AI system-on-chips and rising GDPR-compliance storage fees create uneven adoption patterns.

Key Report Takeaways

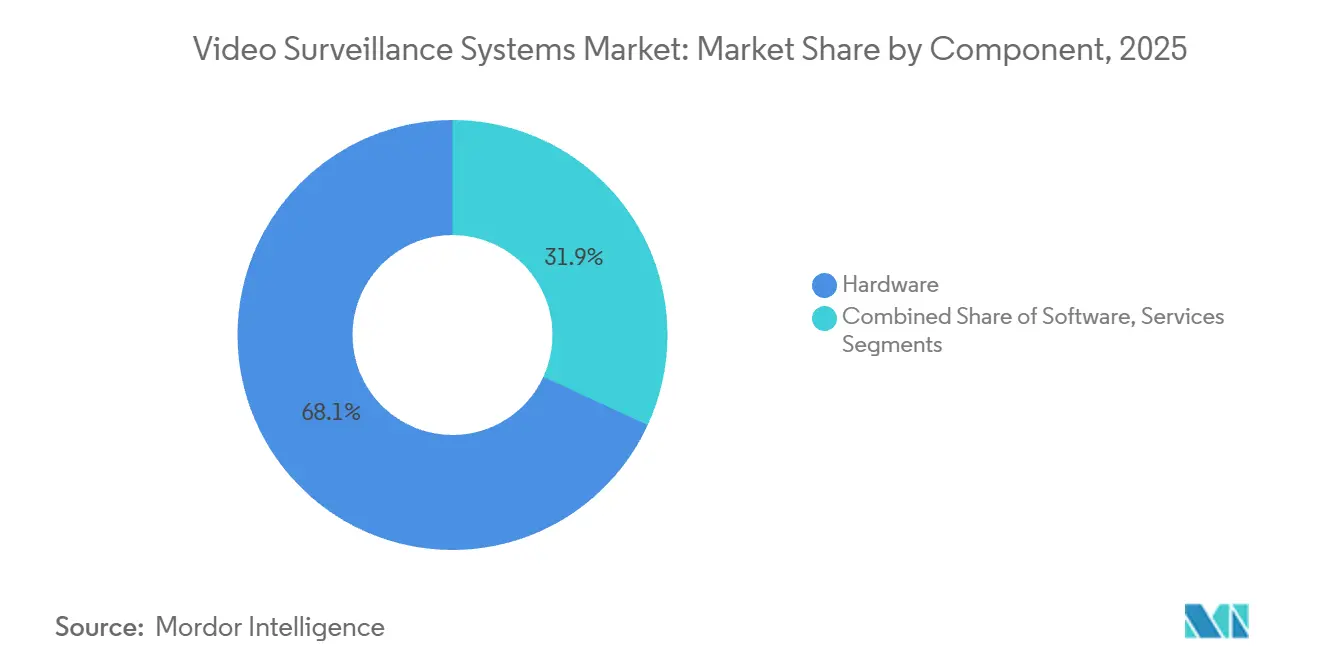

- By component, hardware led with a 68.13% share in 2025, whereas services are forecast to expand at an 11.14% CAGR through 2031.

- By system type, IP architectures commanded 74.26% of the 2025 base, while wireless 4G/5G is poised for a 12.78% CAGR.

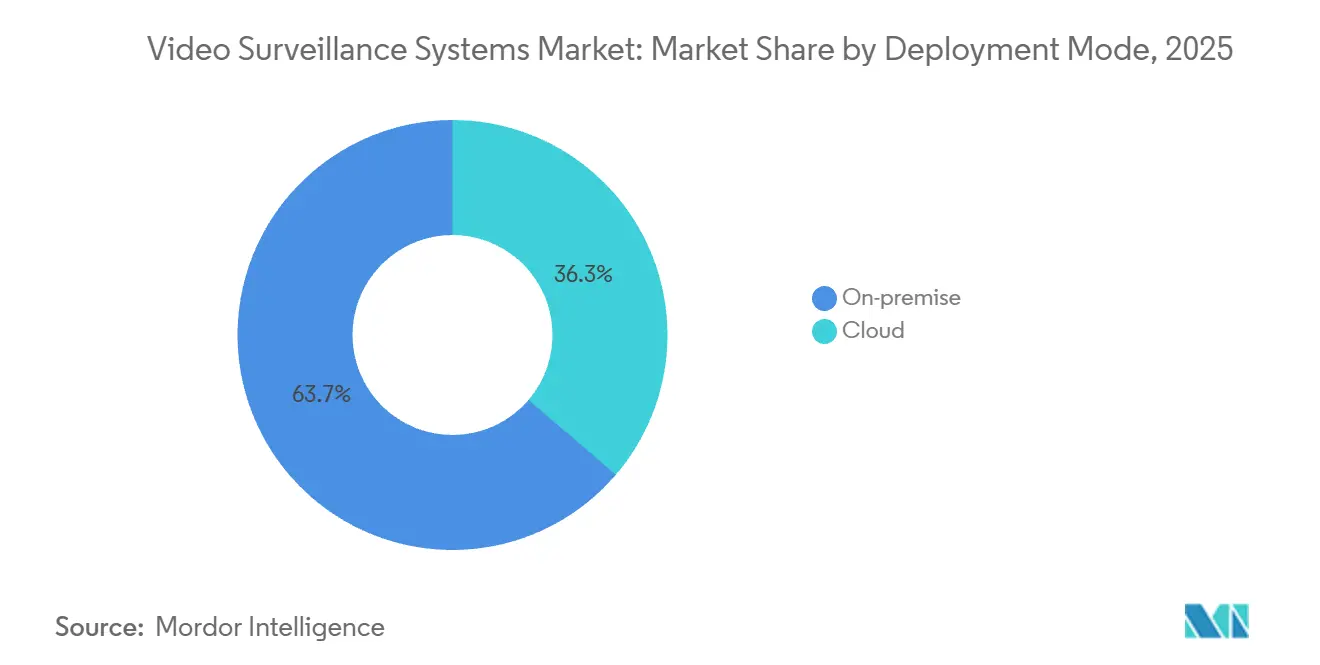

- By deployment mode, on-premise held 63.74% of 2025 installations; cloud models are set to grow at 12.51% as hybrid approaches satisfy data-sovereignty mandates.

- By connectivity, power-over-ethernet captured 51.31% of 2025 installations, yet cellular 5G new radio is forecast to expand at an 11.31% CAGR.

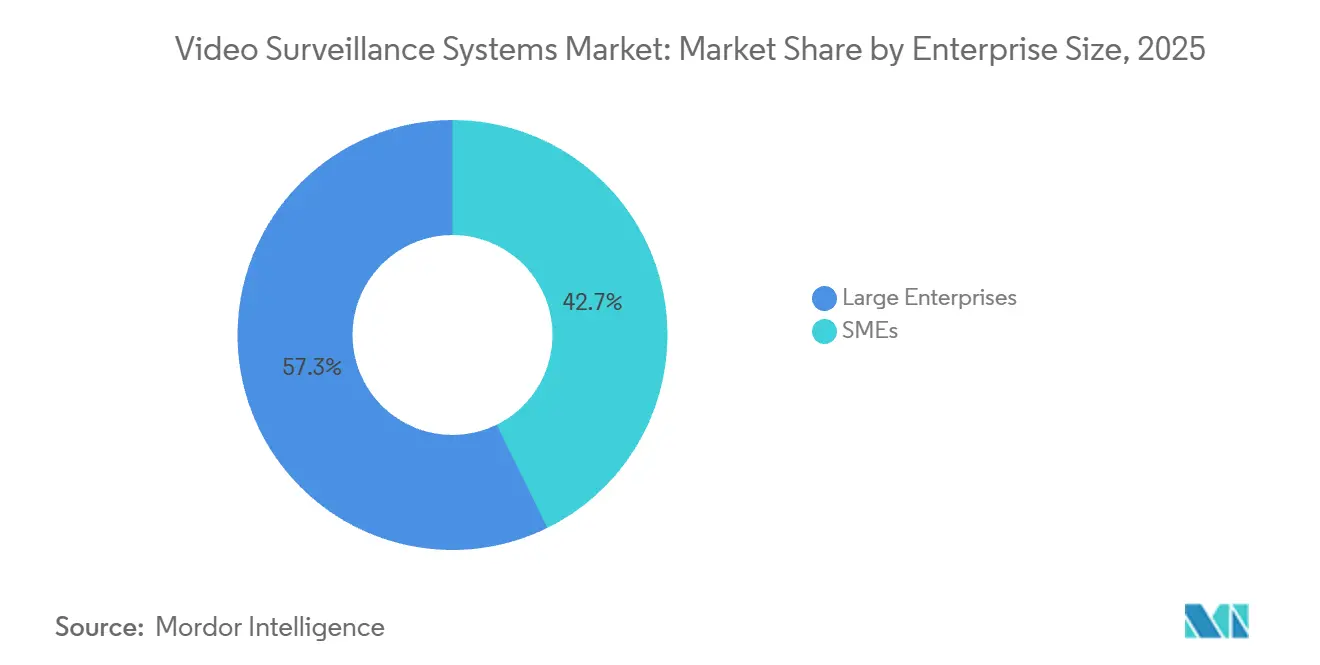

- By enterprise size, large organizations accounted for 57.28% of 2025 spending, but SMEs will advance at 12.76% on cloud video surveillance as a service uptake.

- By application, city surveillance controlled 32.53% of demand in 2025, while industrial manufacturing is the fastest-growing segment at 12.56% CAGR.

- By geography, Asia-Pacific generated 43.61% of 2025 revenue; the Middle East is the fastest-growing geography at 12.19% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Video Surveillance Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AI-Powered Edge Analytics Integration | +2.3% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Mandatory Migration from Analog to IP | +1.8% | Germany, France, Netherlands, Nordics | Short term (≤ 2 years) |

| Tier-3 and Tier-4 Data Center Surveillance | +1.2% | United States, Canada, selected Asia-Pacific hubs | Medium term (2-4 years) |

| 5G-Enabled Ultra-HD Streaming at Hubs | +1.9% | China, Japan, South Korea, Singapore | Short term (≤ 2 years) |

| National Safe-City Grants | +1.6% | Saudi Arabia, United Arab Emirates, Qatar | Medium term (2-4 years) |

| ESG-Linked Insurance Discounts | +1.0% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid AI-Powered Edge Analytics Integration

Edge cameras equipped with neural processing units now execute 30 trillion operations per second, enabling real-time object identification without backhauling raw video to data centers. Bandwidth use falls by as much as 70%, trimming cloud storage costs by USD 0.12 per camera per day and supporting autonomous decision loops under 200 milliseconds. Retailers deploy these units to curb inventory shrinkage, while manufacturers flag worker-safety violations at the point of capture. The architecture simultaneously lowers latency for airport perimeter security and facilitates solar-powered surveillance in remote energy sites, broadening addressable use cases.

Mandatory Migration from Analog to IP in European Smart Cities

European cybersecurity directives require municipalities to encrypt video streams, implement granular access controls, and automate retention policies.[1]Federal Office for Information Security, “Cybersecurity in Video Surveillance,” bsi.bund.de Cities such as Munich and Hamburg replaced 40,000 analog units with IP cameras certified to IEC 62443 before the December 2025 deadline, reducing maintenance outlays by 32%. Amsterdam integrated edge-analytics cameras into bicycle-traffic management, showing how public-safety budgets deliver mobility dividends. Updated guidance from the UK Information Commissioner obliges local authorities to complete data-protection impact assessments, anchoring compliance rigor in future tenders.

Tier-3 and Tier-4 Data Center Surveillance Build-Outs Across North America

Hyperscale and colocation operators spread into secondary U.S. markets for cost and power advantages, each new campus exceeding 50 MW capacity. Facilities require 180-day footage retention to satisfy SOC 2 Type II and ISO 27001 audits, lifting demand for 4K IP cameras and cabinet-level monitoring. Digital Realty’s Phoenix site commissioned 420 cameras in 2024, while Equinix’s Toronto campus added thermal units to track cooling-system health. Uptime Institute now mandates video verification of maintenance drills, embedding surveillance into resiliency frameworks.

5G-Enabled Ultra-HD Streaming Demand in Asian Transportation Hubs

Stand-alone 5G networks deliver uplink speeds above 100 Mbps and latency below 20 milliseconds, permitting 4K and 8K video feeds from mobile surveillance units. Beijing Daxing Airport streams 3,000 camera feeds for 100 million annual passengers, while Changi Airport leverages 5G slices to steer autonomous baggage tractors with 99.99% reliability. Hong Kong MTR replaced wired systems across 93 stations and cut installation time by 70%. Guaranteed 10-millisecond latency enables track-intrusion detection and crowd-management analytics for peak-hour safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-Driven Multi-Terabyte Retention Costs | -1.4% | Europe, expanding to GDPR-inspired markets | Short term (≤ 2 years) |

| U.S. NDAA and FCC Blacklist Restrictions | -1.8% | North America, Australia, Japan | Medium term (2-4 years) |

| Acute AI Chiplet Shortages | -1.2% | Global, most acute in Taiwan-fab dependent regions | Short term (≤ 2 years) |

| Rising Cyber-Insurability Thresholds | -0.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Multi-Terabyte Data Retention Costs

Retention periods extending to 180 days inflate monthly storage expenses to USD 15,000–25,000 for enterprises running 1,000 cameras.[2] UK Information Commissioner’s Office, “Guidance on Video Surveillance,” ico.org.uk Encrypted storage adds 20% compute overhead and complicates cross-border data transfers, while legal reviews and data-protection-officer fees consume up to 12% of surveillance budgets for German and French SMEs. Cloud providers must draft standard contractual clauses and perform transfer-impact assessments, lengthening sales cycles by 8 weeks and tilting smaller firms toward edge-only upgrades rather than full overhauls.

U.S. NDAA and FCC Black-List Sourcing Restrictions

Section 889 of the NDAA and the FCC Covered List prohibit federal agencies and contractors from buying Hikvision and Dahua products, removing 38% of global camera supply from eligible U.S. bids. Substitutes from Axis and Hanwha cost 20%-35% more, raising project capex and squeezing integrator margins. Australia and Japan adopted similar bans in 2025, forcing vendors to manage parallel product lines. U.S. military facilities must replace non-compliant cameras by 2027, a USD 1.2 billion program that strains approved-vendor capacity and inflates lead times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Hardware Commoditizes

Hardware commanded 68.13% of 2025 spending, but service revenue is forecast to expand at an 11.14% CAGR as cameras, storage, and recorders become interchangeable and enterprises outsource management. Video surveillance as a service bundles devices, cloud storage, and AI analytics into a single subscription, appealing to cost-sensitive SMEs. Verkada charges USD 300–500 per camera annually for its plug-and-play package. Meanwhile, Genetec’s hybrid model lets banks keep sensitive footage on-premises while running analytics in the cloud, satisfying sovereignty requirements without incurring capital expense spikes.

Second-generation edge-storage appliances cache footage locally and upload only event metadata, slicing egress costs by up to 75%. Component makers promote drives optimized for 24/7 write loads and AI indexing. As a result, services captured 31.87% of 2025 revenue and are projected to overtake hardware by 2030 if current adoption persists. Vendors are layering predictive maintenance, incident-response automation, and privacy masking into subscription tiers, expanding the addressable spend beyond physical security budgets.

By System Type: Wireless Architectures Challenge Wired Dominance

IP networks held a 74.26% share in 2025, anchored by Ethernet infrastructure in retail and municipal deployments. However, wireless 4G/5G systems are forecast for 12.78% CAGR as mobile operators bundle connectivity and cloud storage, slashing installation timelines by 70%. Verizon’s private 5G service supports 300 cameras per campus with 15-millisecond latency guarantees.[3]Verizon Private 5G Solutions, verizon.com AT&T’s edge-compute offload cuts round-trip delays by 40%, enabling real-time alerts for intrusions.

Analog deployments fell to 14% market share in 2025 but persist in legacy factories where coaxial cabling remains viable. Hybrid encoder boxes that bridge analog cameras to IP backbones account for 8% but will decline as analog devices reach end-of-life. As sensor costs drop and wireless uplink charges fall, fully untethered architectures are likely to erode wired incumbency across construction, disaster-recovery, and temporary-event use cases.

By Deployment Mode: Cloud Gains Despite Data-Sovereignty Concerns

On-premise solutions held 63.74% of 2025 deployments because financial and healthcare operators prefer local control. Yet cloud architectures are expected to expand at a 12.51% CAGR as hybrid models reconcile sovereignty needs with cost efficiency. Public-cloud usage represented 18% of the cloud segment, favored by retailers that prioritize scalability over data isolation. Private-cloud instances held 22%, providing dedicated hardware for regulated workloads.

Hybrid approaches dominated 2025 enterprise bids, allowing critical footage to remain onsite while archives migrate to object stores that cost USD 0.05 per gigabyte per month. This pattern aligns storage costs with retention policies, enabling automated tiering as footage ages. Vendors now offer single-pane dashboards that manage edge devices and cloud clusters, accelerating operational consolidation across geographically dispersed portfolios.

By Connectivity: Cellular 5G NR Disrupts Wired Incumbency

Power-over-Ethernet retained 51.31% of connections in 2025, leveraging IEEE 802.3bt’s 90-watt budget to drive pan-tilt-zoom units with integrated heaters. Nonetheless, cellular 5G NR connections are forecast for 11.31% CAGR as network slicing guarantees dedicated uplink throughput for security traffic. T-Mobile’s private network supports 200 cameras per logistics hub with 99.9% availability. Qualcomm’s QCS8250 chip merges 5G modem, AI accelerator, and ISP in one die, cutting power use 30% and enabling solar operation.

Wi-Fi 6/6E carved out 28% share in 2025, ideal for indoor sites with dense access-point coverage. Yet its 50-meter range ceiling limits outdoor reach, positioning cellular as the technology of choice for remote oil, gas, and border facilities. The GSMA IoT SAFE framework embeds SIM-based authentication and encryption, easing cyber insurance compliance.

By Enterprise Size: SMEs Embrace Cloud to Bypass Capital Constraints

Large enterprises captured 57.28% of 2025 revenue and maintain security operations centers with analysts monitoring multi-site feeds. However, SMEs are projected to grow at 12.76% CAGR as cloud platforms remove upfront hardware outlays. Rhombus Systems offers USD 20-30 per-camera monthly plans with 30-day retention, enabling firms with fewer than 100 employees to adopt enterprise-grade surveillance.

Cyber insurers now grant 10%-15% premium discounts to policyholders running encrypted, multi-factor-authenticated cloud video, nudging cash-constrained businesses toward subscription bundles. As plug-and-play cellular cameras require no wiring, SMEs in retail and hospitality deploy within hours, expanding addressable demand in previously unserved micro-business segments.

By Application: Industrial Manufacturing Leverages AI for Operational Gains

City surveillance secured 32.53% of 2025 demand, funded by crime-reduction grants and urban-mobility programs. Industrial manufacturing, though, is forecast to outpace all other segments at 12.56% CAGR as cameras feed robotic process automation and predictive maintenance engines. Siemens’ Industrial Edge integrates vision data with PLCs to adjust parameters in real time, cutting defects and downtime.

Factory deployments now track worker PPE compliance, detect product anomalies at 60 frames per second, and predict equipment failures hours in advance. The video surveillance systems market share for industrial sites reached 18% in 2025 and is expected to rise five points by 2031. Integrations with ERP and MES platforms further embed surveillance into operational intelligence, broadening spend beyond security budgets.

Geography Analysis

Asia-Pacific remains the revenue cornerstone, accounting for 43.61% of 2025 revenue, with China’s public-safety projects and India’s municipal tenders underpinning volume demand. National policies that favor domestic manufacturers and integrate cloud giants like Alibaba create vertically integrated ecosystems. Simultaneously, stringent cyber requirements in Japan and South Korea elevate the status of premium Western vendors for critical infrastructure deployments.

North America demonstrates high replacement velocity rather than first-time adoption. Federal agencies must strip banned Chinese equipment by 2027 and channel orders to Axis, Hanwha, and Motorola. Hyperscale data center surveillance drives follow-on demand as SOC 2 audits tighten. Canada’s safe-city grants catalyze provincial spending, while Mexican manufacturing hubs upgrade to cloud-managed cameras to meet export-plant compliance requirements.

Europe’s trajectory centers on compliance-driven modernization. Cities retrofit analog assets to IP with encryption and automated retention to meet GDPR mandates. Nordic nations are pioneering edge analytics for traffic management, using video to optimize pedestrian and cyclist flows. However, high retention costs and privacy litigation create friction that lengthens procurement cycles.

The Middle East, the fastest-growing geography at a 12.19% CAGR through 2031, executes mega-city builds with large unit counts. NEOM plans 500,000 cameras integrated into autonomous-vehicle grids, while Dubai Police attributes a 22% response-time drop to its AI-enabled network. Government mandates and sovereign-wealth financing ensure sustained capex despite macro volatility.

Latin America and Africa exhibit fragmented, project-based growth. Brazil deploys city-wide analytics for crime monitoring, whereas South Africa’s private-security sector adopts cloud video as a differentiator. Lagos State leverages trust-fund mechanisms to finance camera grids for traffic and crime, portending broader sub-Saharan uptake.

Competitive Landscape

Hikvision, Dahua, Axis Communications, Hanwha Vision, and Bosch together shipped 48% of 2025 units. Chinese vendors dominate low-price segments through vertically integrated supply chains but face procurement bans in North America, Australia, and Japan. Western players differentiate via open standards and ONVIF compliance, enabling multi-vendor analytics overlays.

Software and cloud layers remain fragmented, with more than 200 vendors. Genetec, Milestone, and Verkada rely on subscription revenue and maintain 65%–75% gross margins. Smaller disruptors bundle hardware, storage, and analytics into per-camera subscriptions, removing integrator complexity and capturing SME budgets.

Technology differentiation focuses on on-camera AI silicon. Axis’ ARTPEC-9 executes 40 TOPS and encodes 8K video, while Huawei’s Ascend 310B emphasizes performance-per-watt for solar deployments. Federated-learning patents enable distributed training without centralizing video, cutting bandwidth 90% and aligning with European data-minimization rules.

Video Surveillance Systems Industry Leaders

Hangzhou Hikvision Digital Technology Co. Ltd

Zhejiang Dahua Technology Co. Ltd

Axis Communications AB

Bosch Security & Safety Systems

Hanwha Vision (Samsung)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Panasonic Connect won the 2025 Security Industry Association New Product Showcase Award for its i-PRO Active Guard plug-in, enabling AI intrusion detection on legacy cameras.

- October 2025: Motorola Solutions acquired Ava Security for USD 445 million to deepen its cloud portfolio.

- September 2025: Hanwha Vision committed USD 320 million to expand Vietnamese camera capacity.

- July 2025: Axis Communications released the ARTPEC-9 chip with 40 TOPS on-camera AI.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global video surveillance systems market as all networked or analog cameras, on-premise or cloud storage, video management software, analytics engines, and related services that together capture, transmit, store, and interpret real-time or recorded video for security and business-intelligence tasks. The valuation therefore rolls up physical-hardware revenues with software licenses, subscription fees, and the recurring spend on Video Surveillance-as-a-Service, installation, and maintenance.

Scope Exclusions: Consumer baby monitors, dash cams, and stand-alone body-worn police cameras are not included.

Segmentation Overview

- By Component

- Hardware

- Cameras

- Analog

- IP

- Thermal / Multispectral

- Storage

- DVR/NVR

- SAN / Edge-Storage

- Cameras

- Software

- Video Management Software

- Video Analytics

- Services (VSaaS)

- Hosted

- Managed

- Hybrid

- Hardware

- By System Type

- Analog

- IP

- Hybrid

- Wireless 4G/5G

- By Deployment Mode

- On-premise

- Cloud

- Public

- Private

- By Connectivity

- Wired (PoE)

- Wireless (Wi-Fi 6/6E)

- Cellular (5G NR)

- By Enterprise Size

- Large Enterprises

- SMEs

- By Application

- City Surveillance and Safe-City

- Commercial

- Retail and Malls

- BFSI and Fin-Tech

- Critical Infrastructure

- Energy and Utilities

- Transportation (Airports, Rail, Ports)

- Industrial Manufacturing

- Residential and Smart-Home

- Defense and Homeland Security

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Singapore

- Australia

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed city-surveillance officers, retail loss-prevention heads, VSaaS integrators, and chipset suppliers across North America, Europe, Asia, and the Gulf. These conversations clarified live deployment densities, cloud-migration timelines, and discount structures, letting us refine the desk-derived assumptions.

Desk Research

Mordor analysts began by compiling baseline figures from open datasets such as UN Comtrade HS-8525 camera shipments, FCC equipment authorizations, U.S. Bureau of Labor Statistics price indices, China MIIT production releases, and newsletters from ONVIF and the Security Industry Association. We overlaid insights from corporate 10-Ks, SEC filings, smart-city tender portals, and patent families mined through Questel to pin down adoption curves and average selling prices.

A follow-up sweep captured policy catalysts, EU GDPR, India's DPDP Act, and U.S. NDAA bans, using Dow Jones Factiva, while D&B Hoovers supplied vendor revenue splits that anchored regional market shares. The sources named here are illustrative; many additional public records and proprietary feeds informed the desk exercise.

Market-Sizing & Forecasting

We constructed a top-down demand pool from installed-camera bases and new-construction footprints, validated through selective bottom-up checks such as sampled IP-camera ASP multiplied by estimated shipments of tier-one vendors. Key variables include smart-city urban population, 5G base-station rollouts, enterprise cloud-adoption ratios, and average storage hours per camera. Multivariate regression with GDP, construction spend, and data-center rack additions underpins the forecast, and scenario analysis adjusts for regulatory shocks. Gaps in emerging-market shipment data are bridged through tariff-code triangulation and expert ranges.

Data Validation & Update Cycle

Outputs pass variance checks against import data, vendor disclosures, and quarterly channel audits; anomalies trigger analyst re-runs. Reports refresh annually, with interim updates for material trade bans, major acquisitions, or security incidents, and a last-mile review ensures clients receive the freshest view.

Why Mordor's Video Surveillance Baseline Commands Reliability

Published estimates often diverge because publishers slice the market by dissimilar service mixes, apply varied ASP ladders, or freeze exchange rates at different snapshots.

Key gap drivers include exclusion of VSaaS revenues, hardware-only scopes, and reliance on historic panels that ignore 5G-enabled edge analytics. Mordor's 2025 update integrates the full hardware-software-service continuum and converts local revenues using trailing-twelve-month averages, making our totals more comparable and current.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 91.66 B (2025) | Mordor Intelligence | - |

| USD 83.49 B (2025) | Global Consultancy A | Omits VSaaS and analytics revenues; older 2024 base |

| USD 57.96 B (2025) | Industry Journal B | Hardware-only scope; single-source desk data; limited emerging-market inputs |

The comparison shows that when the full revenue stack and the latest policy filters are incorporated, Mordor delivers a balanced, transparent baseline that executives can trace back to clear variables and reproduce with modest effort.

Key Questions Answered in the Report

How large is the video surveillance systems market in 2026?

The video surveillance systems market size reached USD 71.65 billion in 2026 and is forecast to hit USD 118.83 billion by 2031.

Which component segment is growing fastest?

Services, particularly video surveillance as a service, are expected to grow at 11.14% CAGR as enterprises shift from capex to opex models.

Why are SMEs adopting cloud video platforms?

Subscription bundles eliminate upfront hardware costs, meet cyber-insurance requirements, and scale with business growth.

Which region will record the highest growth through 2031?

The Middle East is projected to lead with a 12.19% CAGR, propelled by Saudi Arabia’s Vision 2030 and UAE government mandates.

How do 5G networks impact surveillance deployments?

5G reduces latency below 20 milliseconds, enabling real-time 4K/8K streaming and rapid deployment where wired infrastructure is impractical.

What is the main regulatory restraint in North America?

U.S. NDAA and FCC sourcing restrictions ban certain Chinese equipment, raising costs and tightening vendor supply for federal projects.

Page last updated on: