Video Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

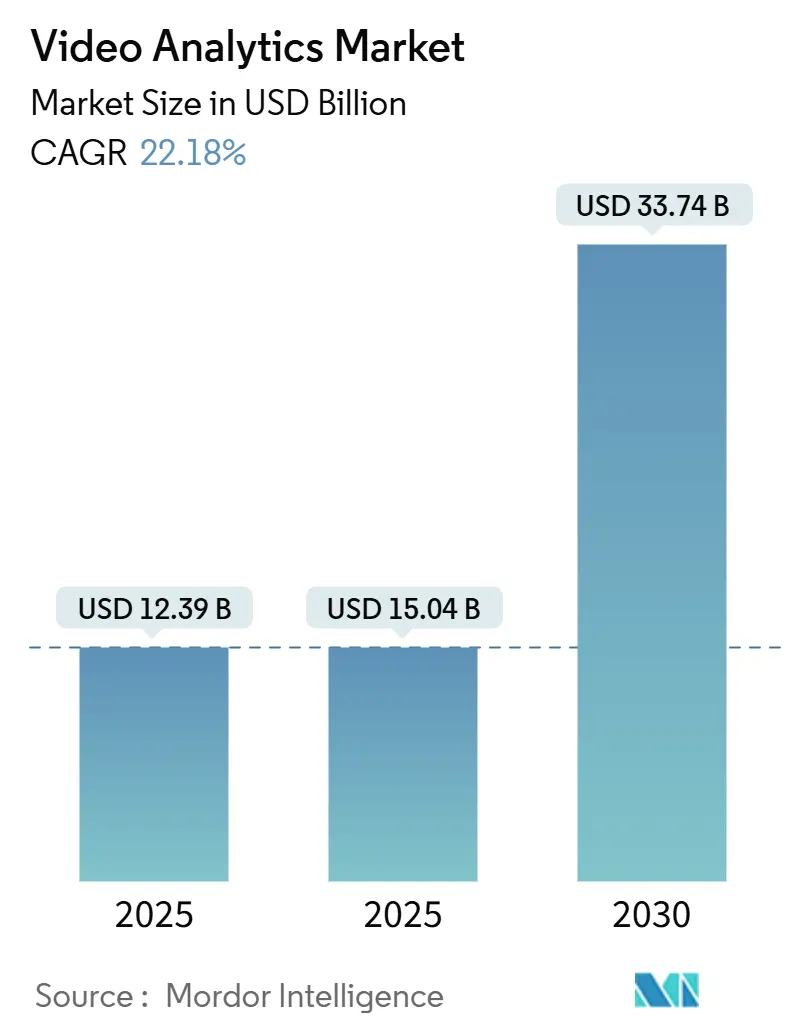

| Market Size (2026) | USD 15.04 Billion |

| Market Size (2030) | USD 33.74 Billion |

| Growth Rate (2025 - 2030) | 22.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Analytics Market Analysis by Mordor Intelligence

The Video Analytics Market size is projected to be USD 12.39 billion in 2025, USD 15.04 billion in 2026, and reach USD 33.74 billion by 2030, growing at a CAGR of 22.18% from 2026 to 2030. Strong demand comes from AI-enabled edge computing, rapid 5G rollouts, and the falling cost of high-resolution cameras. Regulatory mandates for body-worn cameras in the United States, smart-city investments in Asia Pacific, and strict data-protection rules in Europe collectively shape adoption patterns. Supply-chain stress around GPUs and tighter semiconductor pricing put short-term pressure on margins, yet advances in low-power accelerators are easing cost barriers. Strategic alliances between cloud hyperscalers and AI-native vendors shorten time-to-market for vertical solutions, while open API ecosystems accelerate third-party innovation across retail, healthcare, and transportation.

Key Report Takeaways

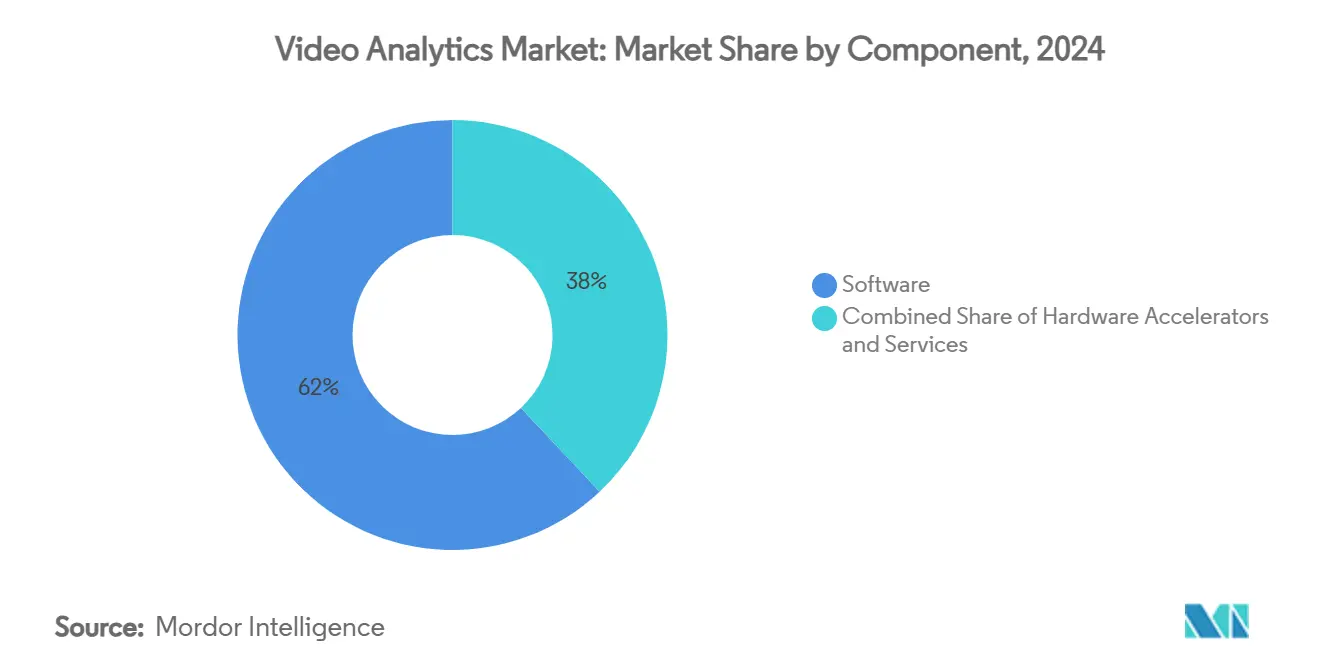

- By component, software solutions led with 62% of video analytics market share in 2024; cloud-based SaaS is forecast to grow at 25.4% CAGR to 2030.

- By application, intrusion and perimeter protection accounted for 28% of the video analytics market size in 2024, while facial recognition is advancing at a 24.1% CAGR through 2030.

- By deployment mode, on-premise/server installations held 67% share of the video analytics market in 2024; edge deployments post the highest projected CAGR at 26.3% over 2025-2030.

- By end-user vertical, government and public safety maintained 31% share in 2024; healthcare and life sciences is expanding at 23.7% CAGR to 2030.

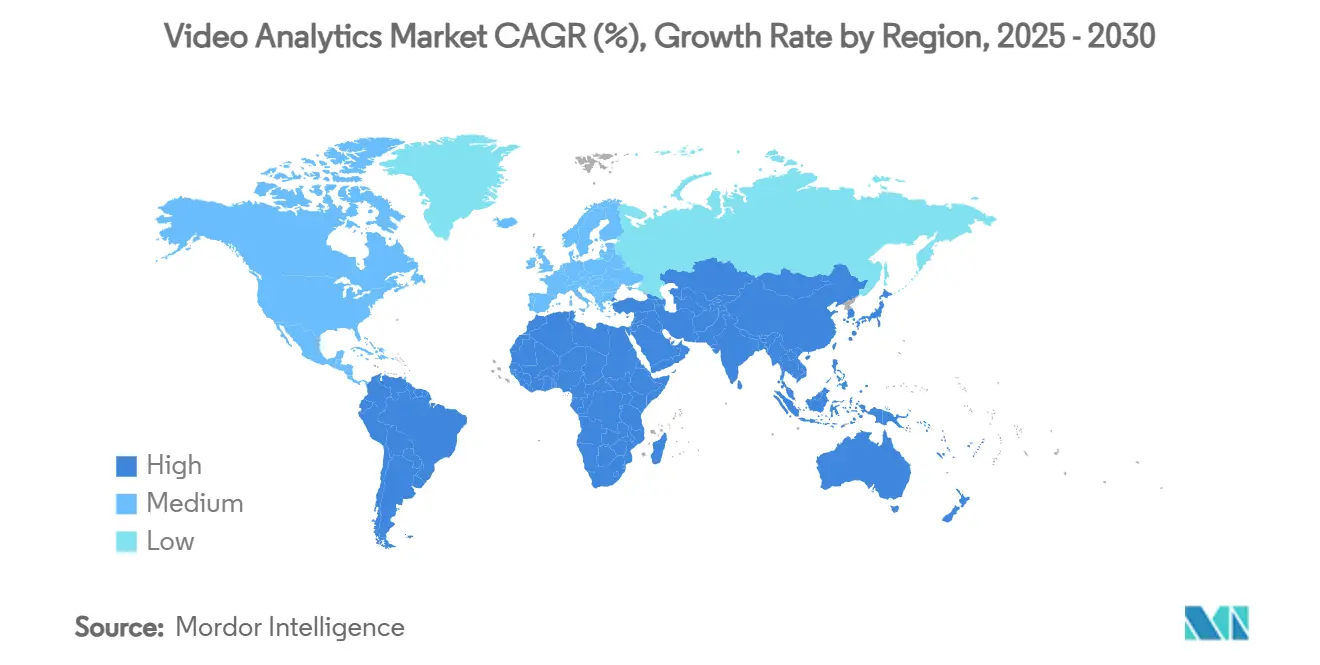

- By geography, North America led with 38% revenue share in 2024, whereas Asia Pacific is set to record a 22% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Video Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Migration from CCTV Monitoring to AI-Based Analytics in GCC | +4.2% | GCC countries, spillover to MEA | Medium term (2-4 years) |

| Smart-City Initiatives | +3.8% | Global, concentrated in APAC and GCC | Long term (≥ 4 years) |

| Integration of Video Analytics with Retail POS in North America | +3.1% | North America, expanding to Europe | Short term (≤ 2 years) |

| Mandates for Body-Worn-Camera Analytics in U.S. Law-Enforcement | +2.9% | United States, influence on global standards | Medium term (2-4 years) |

| Edge-Based Analytics for Autonomous Vehicle Fleets | +2.7% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| GDPR-Compliant Privacy Masking Boosting European Healthcare Adoption | +2.4% | Europe, regulatory influence globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Migration from CCTV Monitoring to AI-Based Analytics in GCC

The Gulf Cooperation Council is shifting from passive CCTV toward intelligent analytics that detect anomalies, predict incidents, and optimise resource allocation. Saudi Arabia’s Vision 2030 and the UAE’s smart-city programmes channel public funding into AI retrofits for existing camera estates, while Dubai’s largest mall demonstrated real-time anomaly detection after upgrading with Icetana technology.[1]Macnica Press Office, “Dubai's Main Shopping Mall Transforms Its Video Surveillance Security System with Icetana,” Macnica, macnica.com High societal trust in technology and diversification away from oil revenue underpin sustained investment. Edge-ready appliances reduce bandwidth costs, and pan-GCC interoperability standards are emerging to ensure data-sharing across city platforms. These factors collectively add 4.2 percentage points to the forecast CAGR.

Smart-City Initiatives

Municipalities worldwide embed video analytics in traffic control, public-safety hubs, and environmental monitoring infrastructure. Orange County deployed AI analytics across 52 intersections, improving road-safety metrics and aligning with Caltrans’ Vision Zero goal.[2]Derq Communications, “Next-Gen AI Smart City Solutions from Econolite and Derq to Assist Caltrans with Road Safety Initiatives in Orange County,” Derq, derq.com Seoul’s Smart Traffic Management platform applies live weather feeds to prevent congestion, while Copenhagen leverages cycling-traffic video for urban planning. 5G links enable millisecond-level response times, widening the scope from static surveillance to dynamic crowd management. Long-term smart-city funding pipelines give this driver a 3.8 percentage-point lift on CAGR.

Integration of Video Analytics with Retail POS in North America

Escalating shrinkage forecast at USD 132 billion in 2024 pushes retailers to fuse transaction data with video streams. DTiQ’s partnership with GNC scales loss-prevention analytics across hundreds of stores, producing rapid ROI through automated exception reporting.[3]DTiQ Newsroom, “DTiQ and GNC Partner Up to Scale In-Store Loss Prevention Visibility Across the Country,” DTiQ, dtiq.com Beehive’s platform overlays real-time heat maps to refine store layouts and staffing. Integration reduces investigation time, strengthens evidence chains, and supports queue-management analytics, adding 3.1 percentage points to market growth.

Mandates for Body-Worn-Camera Analytics in U.S. Law Enforcement

Body-worn cameras are now standard across 82% of U.S. agencies, but reviewing footage manually is impractical. The Paterson Police Department adopted Truleo’s AI engine to flag escalation risks automatically. Similar pilots at the NYPD focus on transparency and training insights. Privacy laws in Texas, Florida, and Oregon require PII redaction before public release.[4]Police1 Staff, “What New Data Privacy Laws in Texas, Florida and Oregon Mean for Law Enforcement,” Police1, police1.com Compliance pressure and efficiency gains raise the sector’s CAGR by 2.9 percentage points.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High GPU Power Consumption in Remote Oil and Gas Sites | -2.8% | Global, concentrated in remote locations | Medium term (2-4 years) |

| Fragmented Camera Firmware in Latin-American Retail | -2.1% | Latin America, emerging markets | Short term (≤ 2 years) |

| Litigation Risks from BIPA on U.S. Facial Analytics | -1.9% | United States, influence on global practices | Long term (≥ 4 years) |

| Lack of Local-Language Datasets in Middle-East Airports | -1.6% | Middle East, multilingual environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High GPU Power Consumption in Remote Oil and Gas Sites

Off-grid facilities rely on diesel generators, making multi-GPU clusters costly and impractical. Supply constraints on high-end GPUs further intensify the hurdle. Axelera’s Metis PCIe accelerator showcased 5× lower energy draw and 4× lower cost than conventional GPU setups while sustaining analytic performance. Yet thermal management, maintenance logistics, and limited technical personnel at remote sites slow adoption, subtracting 2.8 percentage points from the forecast CAGR.

Fragmented Camera Firmware in Latin-American Retail

Retail chains in Latin America often run mixed-vendor camera fleets with proprietary firmware that lacks unified APIs. Integration projects incur extra middleware and hardware-replacement costs. Smaller retailers without in-house IT teams face long deployment lead times and training overheads. Cloud-hosted analytics could bypass firmware lock-in but depend on stable connectivity that remains inconsistent across parts of the region. The resulting complexity reduces growth potential by 2.1 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Cloud Migration

Software solutions commanded 62% of the video analytics market in 2024 as customers prioritised AI models over hardware upgrades. Subscription-priced SaaS is forecast to grow at 25.4% CAGR as enterprises trade CapEx for OpEx and tap elastic cloud capacity. Hybrid frameworks keep sensitive streams on-premise while sending metadata to the cloud, balancing sovereignty and scalability. Hardware accelerators gain traction for edge inference, especially in logistics yards and quick-service restaurants where latency budgets are strict. The University of Virginia’s SMAST network underscores the jump in accuracy now achievable through transformer-based models.

Services expand in parallel. Managed offerings appeal to organisations lacking 24/7 analytics expertise, while professional services remain vital for multi-site roll-outs, API integrations, and compliance validation. As SaaS penetration deepens, managed-service providers bundle health monitoring, model updates, and cyber-hygiene checks into per-camera pricing. Together, these trends affirm software’s primacy and reinforce the long-term weighting of software revenue in the video analytics market size.

By Application: Facial Recognition Surges Despite Privacy Concerns

Intrusion and perimeter protection retained 28% video analytics market share in 2024, anchored by critical-infrastructure and campus security mandates. Facial recognition and demographics analytics is expected to compound at 24.1% CAGR through 2030 despite patchwork regulation. Airports deploy passive watch-list screening, while retailers use face-based demographics for marketing segmentation, provided that consent rules are met. Traffic analytics also gain lift from smart-city projects, and ANPR systems alone are projected to reach USD 4.8 billion by 2027.

Behaviour recognition has matured beyond simple loitering detection; modern algorithms now isolate violent gestures in real time, aiding rapid security intervention. Retail heat-mapping closes the loop between shopper movement and merchandising. The breadth of use cases keeps application diversification high and positions analytics suites to address multiple needs within one licence.

By End-User Vertical: Healthcare Emerges as Growth Leader

Government and public safety retained 31% share in 2024, supported by city-wide camera networks and evolving policing mandates. Healthcare is projected to expand at 23.7% CAGR, fuelled by continuous-patient-monitoring demands and GDPR-compliant privacy masking solutions. LookDeep Health’s system processes more than 300 high-risk patient streams while protecting identities.

Retail invests to cut shrinkage and refine customer insights, whereas BFSI uses computer vision for ATM security and branch analytics. Transportation operators deploy analytics for predictive maintenance and safety compliance. Industrial use cases span safety-gear detection, defect inspection, and workflow optimisation, reflecting cross-vertical diffusion of best practices.

By Deployment Mode: Edge Computing Accelerates Real-Time Processing

On-premise and central-server setups held 67% of the video analytics market in 2024, mainly in government and finance where data sovereignty is non-negotiable. Edge deployments, however, are projected to climb 26.3% CAGR as compact AI boxes and ASIC accelerators bring millisecond inference to checkpoints, drive-through lanes, and factory lines. VideoMind’s chain-of-low-rank adaptation framework shows how lightweight models can run continuous analysis on resource-constrained nodes.

Cloud deployment still appeals for archival search, on-demand analytics, and elastic training workloads, especially where broadband is robust. The emerging norm is a hybrid mesh that pushes time-critical inference to the edge while centralising deep-learning retraining and dashboard visualisation. This mix controls bandwidth fees, preserves privacy, and satisfies low-latency SLAs.

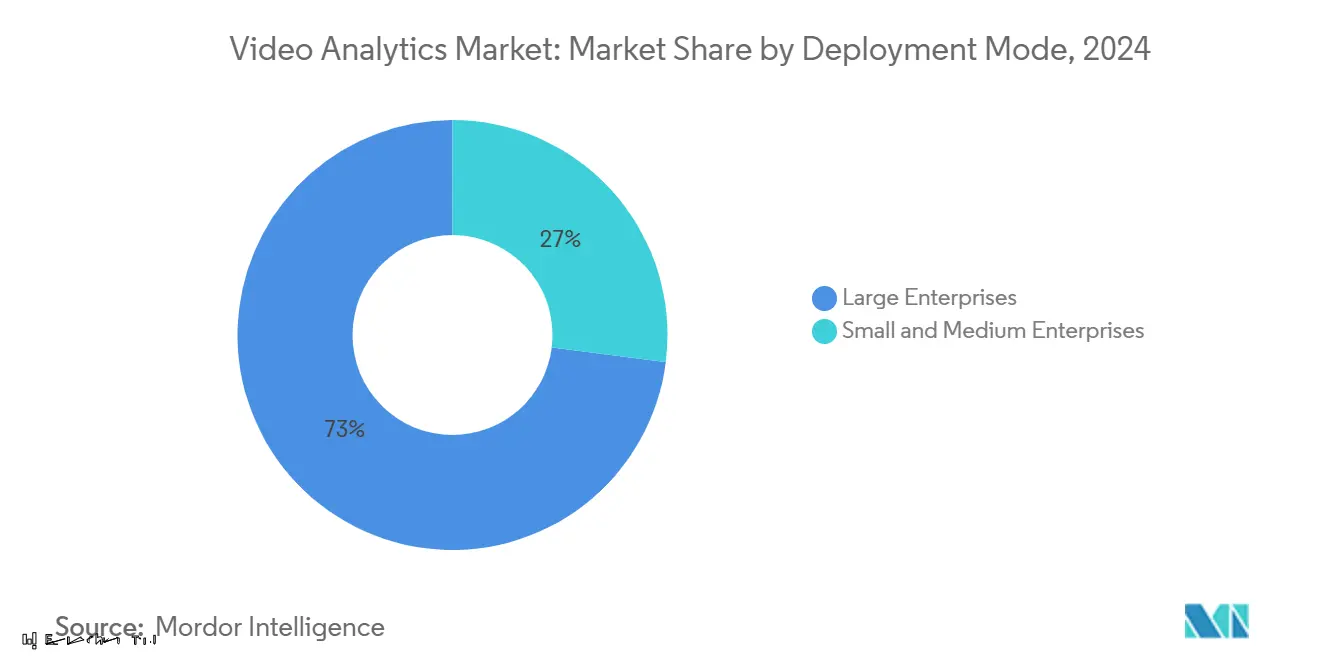

By Organization Size: Large Enterprises Drive Adoption

Large enterprises controlled 73% share of the video analytics market in 2024 and are forecast to grow 23.5% CAGR as multi-site rollouts require scale, redundancy, and advanced cyber safeguards. Telstra Retail’s edge-based foot-traffic solution achieved 95% counting accuracy while masking identities at the device layer. Such deployments demand high-availability clusters, multi-factor authentication, and SOC integrations.

Small and medium enterprises lag due to capital limits and integration skill gaps, yet SaaS bundles and camera-agnostic gateways lower entry barriers. Managed-service providers target SMEs with pay-as-you-grow packages that bundle hardware leasing, cloud analytics, and compliance reporting into one monthly invoice. Over the forecast horizon, SME uptake will lift overall camera penetration but large enterprises will continue to dictate platform feature roadmaps.

Geography Analysis

North America led the video analytics market with 38% revenue share in 2024, anchored by federal and state grants for body-worn-camera programmes and aggressive retail loss-prevention initiatives. Post-pandemic stimulus accelerated city surveillance upgrades, while 5G rollouts underpin low-latency edge deployments. Canada’s ban on selected vendors prompted public-sector buyers to diversify supply chains, opening space for domestic and European providers.

Asia Pacific is projected to post 22% CAGR through 2030, benefitting from megacity construction, factory automation, and national AI policies. China’s vast surveillance estate fosters home-grown algorithm training, though export restrictions affect foreign component sourcing. Japan and South Korea emphasise industrial quality control, whereas Southeast Asian governments focus on transport modernisation. Australia’s high labour costs encourage analytics-driven self-service models across retail and hospitality.

Europe balances innovation with stringent privacy rules. The EU AI Act classifies face recognition as high-risk, compelling vendors to embed bias testing and audit trails. Healthcare adoption accelerates through GDPR-compliant masking, while smart-city pilots in Scandinavia integrate environmental-sensor fusion. National security concerns spur made-in-Europe hardware initiatives, supporting regional chip sovereignty and reinforcing supply-chain resilience.

Competitive Landscape

The video analytics market exhibits moderate fragmentation. Incumbent camera makers such as Hikvision and Axis Communications retain brand loyalty and channel depth, but AI-native start-ups accelerate innovation cycles with specialised models and low-power silicon. Comcast Smart Solutions extended reach by teaming with Eagle Eye Networks and C2RO, showing how telcos leverage network assets to bundle analytics.

Cloud hyperscalers pursue ecosystem influence rather than hardware revenue. Coactive AI’s strategic collaboration with AWS embeds generative AI workflows for visual data, broadening addressable use cases beyond security. Axelera AI’s purpose-built accelerators cut total cost of ownership, intensifying price competition against GPU-centric stacks. IntelliVision’s acquisition by Nipun Vision preserves its product line while injecting fresh capital for autonomous-mobility algorithms.

Algorithmic differentiation remains pivotal. The University of Virginia’s SMAST transformer increased action-recognition accuracy, setting a new bar for human-centric analytics. Vendors bundle continual-learning pipelines to adapt models across geographies and camera types, turning AI performance into a moving target that refreshes upgrade cycles. As private-equity interest rises, M&A activity is likely to consolidate mid-tier suppliers and accelerate platform convergence.

Video Analytics Industry Leaders

Axis Communications AB

Cisco Systems , Inc.

International Business Machines Corporation

Aventura Technologies Inc.

Avigilon Corporation (Motorola Solutions)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Hudl acquired Balltime, an AI-powered volleyball analysis platform, expanding its sports analytics portfolio and demonstrating growing integration of video analytics in athletic performance evaluation.

- January 2025: Amagi announced a strategic partnership with Tellyo to integrate advanced video toolset for sports and news broadcasters, combining Amagi's cloud-based broadcast infrastructure with Tellyo's video production capabilities to streamline workflows for over 700 content brands across 40+ countries.

- January 2025: Coactive AI signed a Strategic Collaboration Agreement with AWS to deliver enhanced image and video analytics solutions, leveraging generative AI to streamline organization and analysis of unstructured visual data for customers in Media & Entertainment, Retail, Technology, and Real Estate sectors.

- November 2024: IntelliVision, a global provider of AI and Video Analytics, was acquired by Nipun Vision Corporation from Nice North America, enabling the company to operate as a standalone entity while focusing on security, surveillance, and advanced driver-assistance systems for fleets.

Global Video Analytics Market Report Scope

Video analytics is software that is used for monitoring video streams in near real-time. While monitoring the videos, the software identifies attributes, events, or patterns of specific behavior via video analysis of monitored environments. The software can generate automatic alerts and facilitate forensic analysis of historical data to identify trends, patterns, and incidents. The software enables users to analyze, organize, and share any insight gained from the data to make smarter, better decisions.

The video analytics market is segmented by type (software (on-premise and cloud) and services), by end user (BFSI, healthcare, retail & logistics, critical infrastructure, hospitality and transportation, defense and security, and other end-user verticals), and by geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Software | On-Premise |

| Cloud-Based (SaaS) | |

| Hardware Accelerators | |

| Services | Managed Services |

| Professional Services |

| Intrusion and Perimeter Protection |

| Crowd and People Counting |

| Facial Recognition and Demographics |

| Traffic and Vehicle Analytics (ANPR, Incident Detection) |

| Behaviour Recognition (Loitering, Violence) |

| Retail Heat-Mapping and Conversion |

| Edge |

| On-Premise / Server |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Government and Public Safety |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Transportation and Logistics |

| Critical Infrastructure and Energy |

| Hospitality and Entertainment |

| Manufacturing and Industrial |

| Others (Education, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (DK, SE, NO, FI) | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC (SA, UAE, Qatar, etc.) |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | On-Premise | |

| Cloud-Based (SaaS) | |||

| Hardware Accelerators | |||

| Services | Managed Services | ||

| Professional Services | |||

| By Application | Intrusion and Perimeter Protection | ||

| Crowd and People Counting | |||

| Facial Recognition and Demographics | |||

| Traffic and Vehicle Analytics (ANPR, Incident Detection) | |||

| Behaviour Recognition (Loitering, Violence) | |||

| Retail Heat-Mapping and Conversion | |||

| By Deployment Mode | Edge | ||

| On-Premise / Server | |||

| Cloud | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User Vertical | Government and Public Safety | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Transportation and Logistics | |||

| Critical Infrastructure and Energy | |||

| Hospitality and Entertainment | |||

| Manufacturing and Industrial | |||

| Others (Education, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics (DK, SE, NO, FI) | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC (SA, UAE, Qatar, etc.) | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the video analytics market?

The video analytics market stands at USD 12.39 billion in 2025 and is forecast to reach USD 33.74 billion by 2030, displaying a 22.18% CAGR.

Which component segment leads the market?

Software dominates, accounting for 62% market share in 2024, with cloud-based SaaS solutions growing fastest at 25.4% CAGR.

Which region will grow most rapidly?

Asia Pacific is projected to record the highest regional CAGR at 22% over 2025-2030 due to extensive smart-city and manufacturing automation investments.

How are edge deployments influencing adoption?

Edge implementations are expected to expand at 26.3% CAGR as organisations seek real-time inference, reduced bandwidth costs, and data-sovereignty compliance.

Why is healthcare a high-growth vertical?

Healthcare facilities adopt GDPR-compliant privacy masking and continuous patient-monitoring analytics, driving a 23.7% CAGR for the sector.

What are the main restraints on market growth?

High GPU power consumption in remote sites and fragmented camera firmware in Latin-American retail environments collectively reduce the overall CAGR by 4.9 percentage points.

Page last updated on: