Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

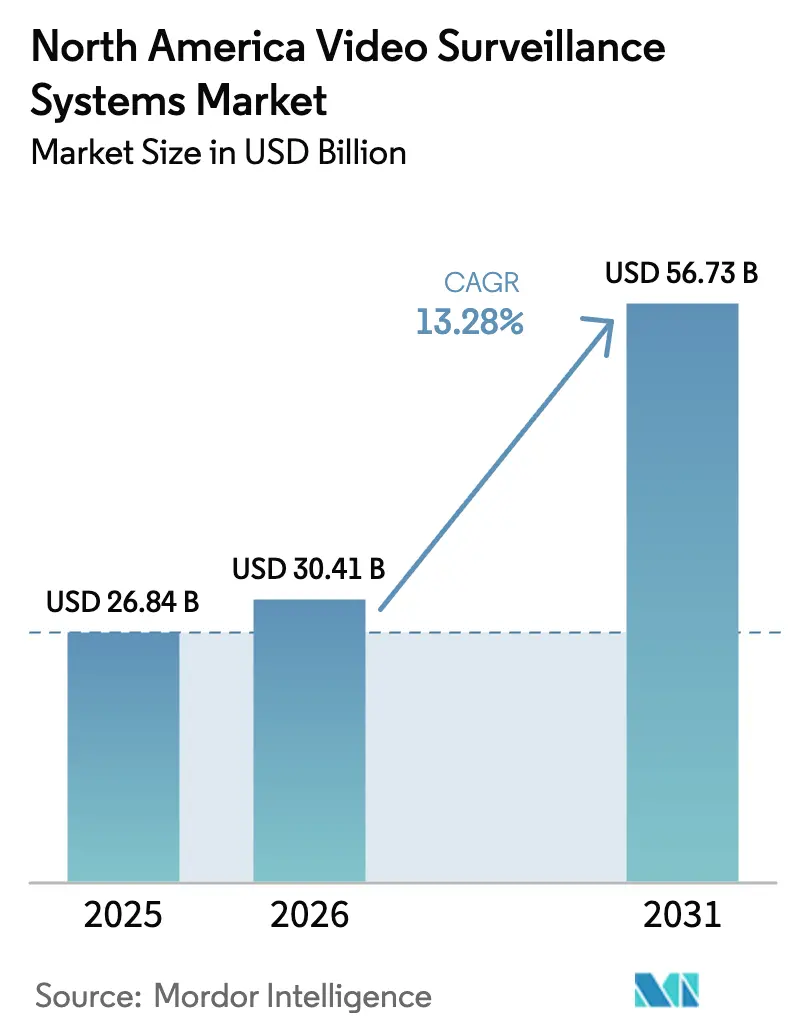

| Base Year Market Size (2025) | USD 26.84 Billion |

| Market Size (2026) | USD 30.41 Billion |

| Market Size (2031) | USD 56.73 Billion |

| Growth Rate (2026 - 2031) | 13.28% CAGR |

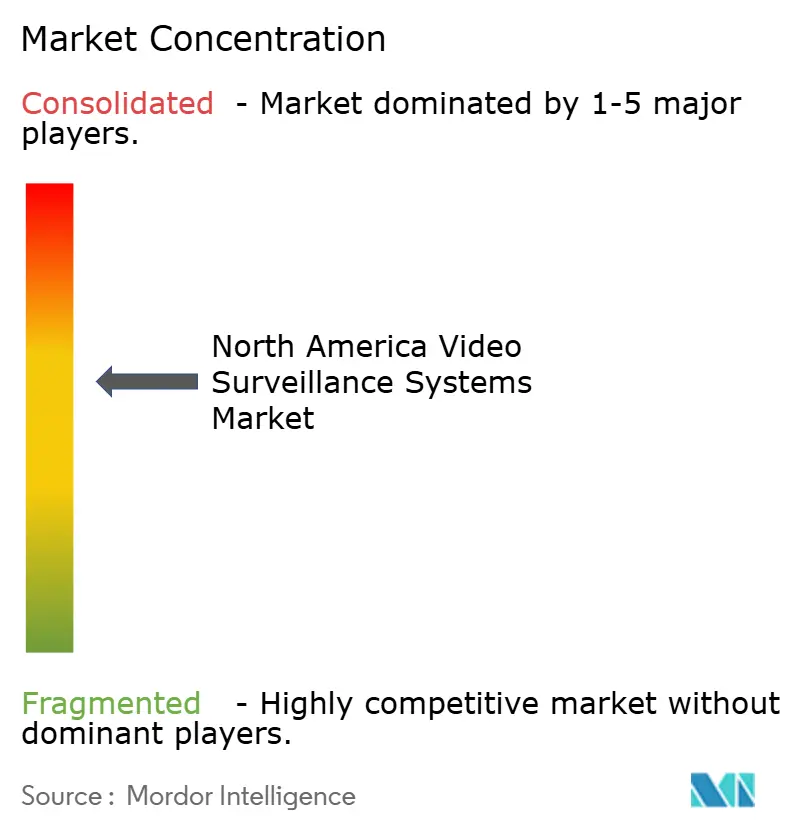

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Video Surveillance Systems Market Analysis by Mordor Intelligence

North America video surveillance systems market size in 2026 is estimated at USD 30.41 billion, growing from 2025 value of USD 26.84 billion with 2031 projections showing USD 56.73 billion, growing at 13.28% CAGR over 2026-2031. Rising demand for AI-enabled analytics, wider availability of edge computing chips, and the migration toward cloud-delivered Video Surveillance as a Service are reshaping customer expectations. Organizations now treat cameras as data-generating sensors that feed real-time business intelligence platforms, trimming bandwidth needs and lowering total cost of ownership. Rapid 5G roll-outs are unlocking previously unreachable outdoor and mobile use cases, while multi-sensor and 4K cameras are becoming standard in critical infrastructure and smart city deployments. Deepening consolidation among hardware incumbents and the arrival of cloud-native specialists are intensifying competition and accelerating the pace of software-centric innovation.

Key Report Takeaways

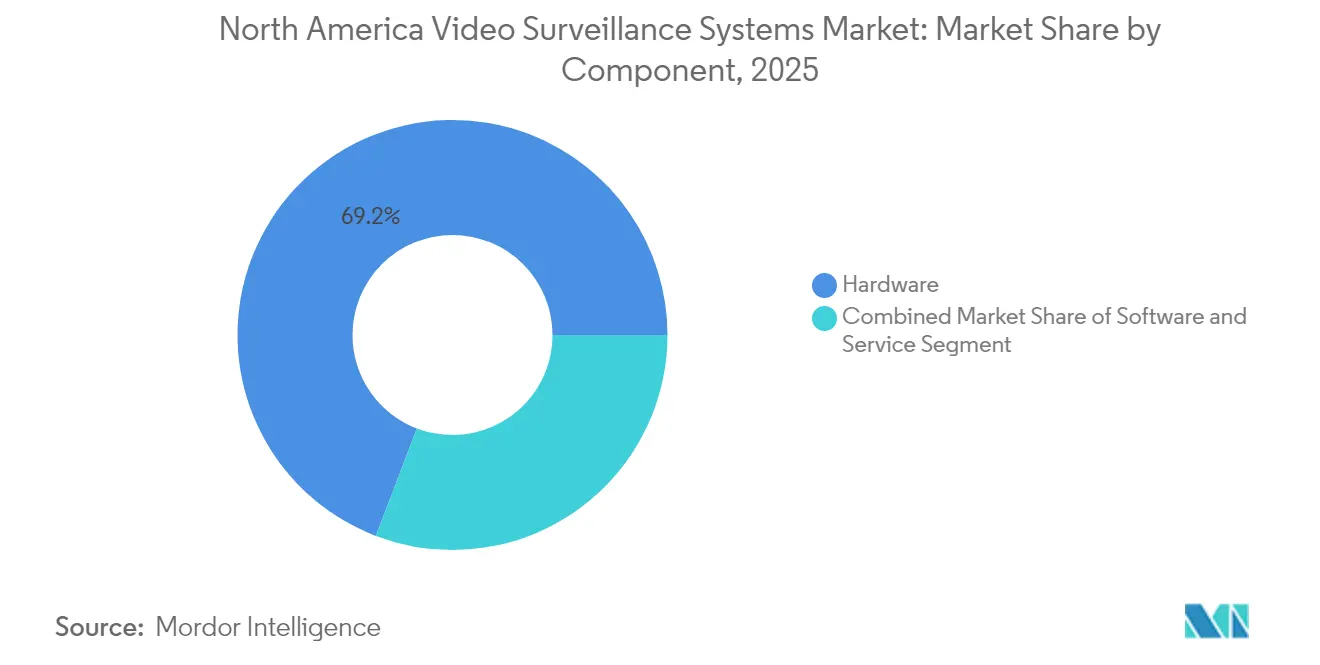

- By component, hardware retained a 69.20% share of the North America video surveillance systems market in 2025; Video Surveillance as a Service is forecast to grow at a 15.5% CAGR through 2031.

- By deployment mode, on-premises solutions held 84.10% of the North America video surveillance systems market share in 2025, whereas cloud deployments are projected to register a 15.9% CAGR between 2026 and 2031.

- By connectivity, wired installations accounted for 74.20% of the North America video surveillance systems market size in 2025; wireless connectivity is the fastest-growing segment at a 15.2% CAGR over the same period.

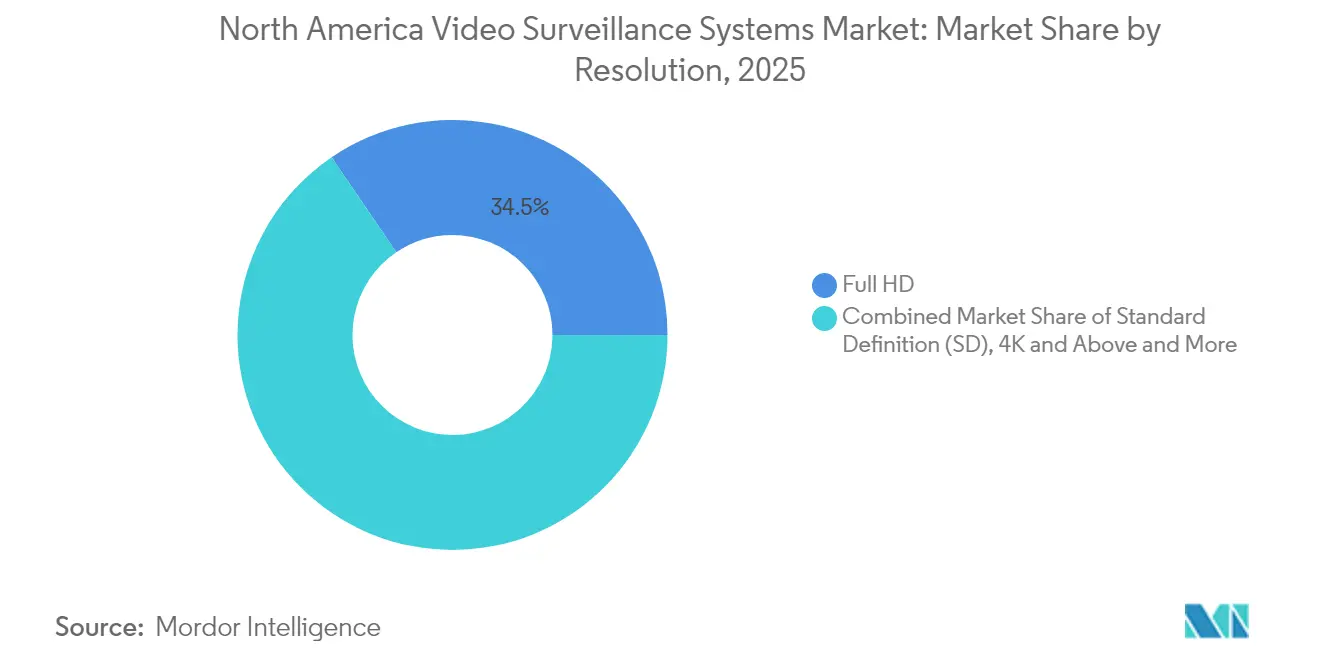

- By resolution, Full HD systems controlled 34.50% of the North America video surveillance systems market in 2025, while 4K & Above cameras are set to expand at a 15.5% CAGR to 2031.

- By end-user industry, the commercial sector commanded 39.30% of the North America video surveillance systems market size in 2025; infrastructure applications are forecast to post a 15.6% CAGR through 2031.

- By geography, the United States dominated with a 89.40% share of the North America video surveillance systems market in 2025, whereas Mexico is the fastest-growing national market at a 13.7% CAGR to 2031.

- The top five suppliers together controlled roughly 21-32% of the North America video surveillance systems market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Video Surveillance Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advances in edge-AI chips reducing TCO | +3.2% | United States, Canada | Medium term (2-4 years) |

| Mandated body-worn & in-vehicle cameras for U.S. law-enforcement agencies | +2.1% | United States | Short term (≤ 2 years) |

| Integration of video surveillance with POS & inventory systems in big-box retail chains | +2.5% | North America | Medium term (2-4 years) |

| Accelerated uptake of cloud-native VSaaS among SME multi-site franchises | +2.8% | United States, Canada, Mexico | Medium term (2-4 years) |

| Surge in federal & state funding for school security modernization | +1.9% | United States | Short term (≤ 2 years) |

| Growing adoption of thermal & multi-sensor cameras at North-American critical infrastructure | +1.7% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advances in Edge-AI Chips Reducing Total Cost of Ownership (TCO) in U.S. Installations

Specialized AI processors embedded inside cameras shift analytics from central servers to the edge, cutting bandwidth needs by up to 70% and lowering storage requirements. [1]ADLINK Technology Inc., "ADLINK Boosts Edge AI Solutions with NVIDIA at COMPUTEX 2024", adlinktech.com Platforms powered by NVIDIA Jetson Orin demonstrate how real-time object detection, smart parking, and perimeter monitoring can run locally, eliminating costly back-end appliances. The architectural change is meaningful for retailers, campuses, and multisite enterprises where centralized analytics previously required heavy capital spending. As component prices fall and chipsets attain higher thermal efficiency, adoption is expected to climb across small and mid-sized projects, driving incremental demand for subscription-based software updates.

Mandated Body-Worn & In-Vehicle Cameras for U.S. Law-Enforcement Agencies

Statutory requirements at federal, state, and municipal levels are turning mobile video capture into a non-discretionary line item for public-safety budgets. Body-worn and vehicle-mounted devices now integrate with central evidence management systems that automate chain-of-custody tracking and facilitate rapid disclosure under freedom-of-information rules. Departments experimenting with cellular backhaul have shown crime-deterrent benefits and reduced citizen complaints. These mandates ripple through adjacent segments such as secure cloud storage, digital-evidence software, and data-protection services, enlarging the overall revenue pool.

Integration of Video Surveillance with POS & Inventory Systems in Big-Box Retail Chains

Large retailers overlay transaction data onto live video streams to detect fraud, reduce shrinkage, and improve merchandise placement. Video analytics correlate scan times, basket size, and customer dwell time, yielding insights that sharpen staffing models and marketing campaigns. Deployments indicate up to 40% improvement in loss-prevention efficacy when visual verification is linked directly to point-of-sale exceptions.[2]Lumana, "Best AI Video Analytics Solution for 2025: Top Platforms Compared.", lumana.aiThe convergence is redefining store security as part of a broader operational-intelligence stack, encouraging vendors to bundle video software with analytics dashboards that speak the language of retail operations rather than physical security alone.

Accelerated Uptake of Cloud-Native VSaaS among SME Multi-Site Franchises

Subscription-based video surveillance enables smaller chains to centralize monitoring without on-prem servers. Case studies report three-year savings of nearly USD 60,000 per location, chiefly through lower hardware outlays and reduced IT labor.[3]Micron, "Securing Your Business While Lowering TCO with VSaaS.", securityworldmarket.comHybrid architectures—local recording paired with cloud management—help customers navigate bandwidth constraints while still enjoying automatic firmware updates and AI enhancements. These economics make VSaaS an attractive alternative at the natural replacement cycle of analog DVRs, fueling double-digit growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-level “surveillance-sanctuary” legislation limiting facial recognition use | -1.2% | United States (select states) | Medium term (2-4 years) |

| Escalating cyber-insurance premiums for cloud-connected cameras | -0.8% | North America | Short term (≤ 2 years) |

| Supply-chain re-shoring raising hardware costs | -1.1% | North America | Medium term (2-4 years) |

| Video data-retention rules driving up storage OPEX for municipalities | -0.9% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

State-Level “Surveillance-Sanctuary” Legislation Limiting Facial Recognition Use

Patchwork bans on biometric analytics across multiple jurisdictions create compliance complexity and legal exposure. Enterprises operating nationwide must deploy redaction tools that blur faces or automatically toggle algorithms by location, increasing software and process overhead. Uncertainty about federal standards prolongs procurement cycles for projects that rely on advanced analytics, restraining revenue growth in the interim.

Escalating Cyber-Insurance Premiums for Cloud-Connected Cameras

Higher premiums and stricter underwriting requirements are prompting buyers to reassess the risk-reward calculus of cloud connectivity. Insurers now insist on end-to-end encryption, zero-trust architectures, and third-party penetration testing, adding cost layers that may delay smaller deployments. While stringent controls ultimately improve ecosystem security, they also raise the entry threshold for resource-constrained users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces VSaaS Challenge

The North America video surveillance systems market size for hardware stood at USD 18.57 billion in 2025 and captured 69.20% of total revenue, reflecting ongoing large-scale camera roll-outs across retail chains, campuses, and utilities. IP cameras, network video recorders, and multi-sensor devices drive the bulk of spending thanks to higher resolution and analytics readiness. Suppliers differentiate through low-light performance, cybersecurity hardening, and open-API design that simplifies integration with access-control and building-management platforms. Despite near-term resilience, the hardware share is expected to erode gradually as customers favor asset-light procurement models.

During 2026-2031, Video Surveillance as a Service is projected to post a 15.5% CAGR, outstripping all other component categories. Cloud subscriptions decouple software capabilities from replacement cycles, letting users activate new AI modules without buying fresh cameras. This shift diverts budget away from capital equipment toward recurring operating expenditure, challenging hardware-centric vendors to reinvent go-to-market strategies and bundle managed services.

By Deployment Mode: Cloud Adoption Accelerates Beyond Security Applications

On-premises installations represented 84.10% of the North America video surveillance systems market share in 2025, anchored by industries that prize deterministic performance and data sovereignty. Large retailers and airports historically favored local servers to avoid latency and bandwidth constraints. Yet the cost and complexity of scaling such infrastructures are prompting a reassessment, especially as cloud-native platforms demonstrate rapid feature release cycles.

Cloud deployments are forecast to grow 15.9% annually through 2031, propelled by centralized policy management, elastic storage, and integration with enterprise analytics workloads. The hybrid model—edge recording combined with cloud orchestration—offers a pragmatic migration path, delivering uptime assurance while exposing APIs that feed corporate dashboards with real-time insights on occupancy, queue length, or asset utilization.

By Connectivity: Wireless Expansion Enables New Deployment Scenarios

Wired Ethernet and PoE architectures held a dominant 74.20% revenue share in 2025, favored for reliability, consistent throughput, and predictable power delivery. Multi-gigabit switching and improved compression allow existing cabling to support 4K streams without forklift upgrades, extending the lifespan of baseline infrastructure. Structured cabling standards continue to evolve, encouraging facility owners to invest in Cat6A or fiber backbones that future-proof campus networks.

Wireless connectivity is seeing the fastest growth, with the North America video surveillance systems market expected to add 15.2% CAGR in this segment. Introduction of Reduced Capability (RedCap) 5G modules strikes a cost-performance balance ideal for battery-powered cameras, construction sites, and remote substations. Complementary technologies such as Wi-Fi 6/7 and 60 GHz mesh links further diversify deployment options, enabling agile, event-driven coverage that can be relocated as needs change.

By Resolution: 4K Adoption Drives Analytics Capabilities

Full HD (1080p) systems remained the volume leader with 34.50% of 2025 revenue, offering sufficient clarity for conventional surveillance tasks while keeping storage overhead manageable. Continuous improvements in H.265/H.266 compression let operators record longer retention periods without expanding server capacity, sustaining Full HD’s appeal in cost-conscious deployments.

The 4K & Above cohort is forecast to grow at 15.5% CAGR thanks to smart city programs, stadium upgrades, and critical-infrastructure mandates that demand high pixel density for forensic inquiries. Edge AI mitigates bandwidth penalties by transmitting metadata instead of raw video, allowing higher resolution without overwhelming networks. As lens, sensor, and SoC prices fall, 4K is expected to become the default spec for new projects, while 8K trials in rail and border security hint at the next frontier.

By End-User Industry: Infrastructure Growth Outpaces Commercial Dominance

Commercial facilities accounted for 39.30% of 2025 spending, driven by retail, banking, and hospitality chains that integrate surveillance with point-of-sale and customer-experience systems. Healthcare providers are increasing orders for privacy-compliant solutions that segment patient areas and automate access auditing. Vendors serving these verticals must navigate specialized compliance regimes, tailoring analytics to operational key performance indicators beyond security.

Infrastructure projects—transport hubs, smart corridors, and energy plants—are projected to expand at a 15.6% CAGR, the fastest among all verticals. Governments fund networked camera grids to enhance perimeter defense, traffic optimization, and environmental monitoring. Contracting cycles are lengthy, but deal values are large and include multi-year maintenance revenue, rewarding suppliers that master complex tender requirements and open-platform interoperability.

Geography Analysis

The United States anchors the North America video surveillance systems market with a 89.40% revenue share and is set to climb from USD 24.00 billion in 2025 to USD 50.72 billion by 2031. Federal infrastructure bills, state-level school-safety grants, and private-sector demand for AI-enabled loss-prevention sustain a robust pipeline of projects. Approximately 26.1 million CCTV cameras are expected to ship nationally in 2030, reflecting both greenfield installations and analog-to-IP retrofits. Buyers increasingly specify NDAA-compliant hardware and zero-trust architectures, reshaping supplier shortlists and accelerating domestic manufacturing initiatives.

Mexico, while smaller in absolute terms, delivers the fastest pace of expansion at a 13.7% CAGR through 2031. Smart city blueprints in Mexico City, Guadalajara, and Monterrey showcase large-scale deployments that integrate license-plate recognition, facial authentication, and crowd analytics. The North America video surveillance systems market size for Mexico is benefiting from nearshoring trends that entice global manufacturers to build facilities requiring stringent security perimeters. Government incentives for public-private partnerships further broaden the addressable base, especially in transport and energy corridors linking to the United States.

Canada presents a steady yet privacy-sensitive environment. Provinces enforce stringent personal-data regulations under PIPEDA, obliging operators to adopt redaction, data-minimization, and transparent governance controls. Municipalities from Vancouver to Toronto are overlaying camera networks with multi-modal sensors—acoustic, environmental, and traffic—to produce integrated situational-awareness dashboards. Extreme weather conditions and vast remote areas spur demand for ruggedized, low-maintenance equipment, creating niches for specialized vendors.

Competitive Landscape

The North America video surveillance systems market demonstrates moderate concentration, with the leading five suppliers collectively controlling an estimated 21-32% revenue in 2024. Incumbents such as Motorola Solutions leverage acquisitions to bolster end-to-end portfolios, integrating cameras, video management, and analytics into single-vendor stacks that appeal to public-sector buyers seeking procurement simplicity. Cloud-native challengers position subscription models that convert capital budgets into predictable operating expenses, narrowing the gap with entrenched hardware brands.

Strategic themes revolve around ecosystem breadth, AI differentiation, and compliance readiness. Bosch’s divestiture of its Building Technologies security unit to Triton Partners underscores a sharpening focus on core competencies, while Axis and i-PRO double down on edge-based analytics to raise the value of each device in the field. Chinese manufacturers continue to participate actively, but NDAA restrictions encourage U.S. federal agencies and many state entities to vet supply chains more rigorously, indirectly benefiting domestic and European brands.

Partnerships with cloud hyperscalers, access-control specialists, and 5G carriers are proliferating. Vendors bundle API access, software development kits, and low-code toolkits so customers can integrate video feeds into broader digital-transformation programs. Go-to-market teams now include vertical-industry consultants who speak the language of retail operations, refinery safety, or sports-venue guest experience, reflecting the transition of surveillance from pure security to multi-disciplinary data utility.

North America Video Surveillance Systems Industry Leaders

-

Honeywell International Inc.

-

Genetec Inc.

-

Avigilon (Motorola Solutions)

-

Axis Communications AB

-

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: i-PRO Americas secured a framework agreement with E&I Cooperative Services to supply advanced security solutions to over 6,000 educational institutions, broadening its reach in the education vertical and easing procurement hurdles.

- March 2025: Genetec extended Security Center SaaS to include intrusion management, unifying video, access, and alarm data in a single cloud instance and accelerating migration paths for on-prem customers.

- February 2025: Axis Communications deployed an integrated surveillance and analytics suite at MetLife Stadium, enhancing perimeter protection and crowd-flow monitoring ahead of major sports events.

- January 2025: San Luis Obispo Police Department implemented Verkada cellular gateways to connect remote cameras, cutting vehicle-break-in incidents in parking areas previously lacking wired infrastructure.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America video surveillance systems market as all networked cameras, storage devices, monitors, and related management software sold for security, safety, and remote monitoring across the United States, Canada, and Mexico.

(Scope exclusion: stand-alone video analytics software that is not bundled with a recording or camera solution is outside this market.)

Segmentation Overview

-

By Component

-

Hardware

-

Cameras

- Analog

- IP

- Hybrid

- Storage

- Monitors

- Accessories

-

Cameras

-

Software

- Video Analytics

- Video Management Software

-

Services

-

VSaaS

- Hosted

- Managed

- Installation and Integration

- Maintenance and Support

-

VSaaS

-

Hardware

-

By Deployment Mode

- On-Premises

- Cloud

-

By Connectivity

- Wired

- Wireless

-

By Resolution

- Standard Definition (SD)

- High Definition (HD)

- Full HD

- 4K and Above

-

By End-User Industry

-

Commercial

- Retail

- BFSI

- Hospitality and Entertainment

- Healthcare

-

Infrastructure

- Transportation (Airports, Rail, Ports)

- Smart Cities

- Energy and Utilities

-

Industrial

- Manufacturing

- Oil and Gas

- Mining

-

Institutional

- Education

- Religious Buildings

- Residential

- Government and Law Enforcement

-

Commercial

-

By Country

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed North American security integrators, public safety chiefs, retail loss prevention managers, and cloud VSaaS platform architects. These dialogues validated replacement cycles, cloud uptake rates, and typical per-site camera counts, and they reconciled government grant disbursements with actual installation timelines.

Desk Research

We began with public datasets that quantify the installed base of cameras, building permits, and crime statistics, such as the FBI UCR, Statistics Canada, and Mexico's INEGI; these series let us gauge demand triggers by sector. Trade associations like the Security Industry Association, the US Smart Cities Council, and the Canadian Security Association provide shipment trends and average selling prices. Company 10-K filings, FCC procurement notices, and municipal tender portals reveal recent contract values, while customs records parsed via Volza clarify import flows for cameras and NVRs.

A second sweep draws on premium sources that Mordor analysts license, including D&B Hoovers for vendor financial splits and Dow Jones Factiva for deal alerts, plus Marklines for automotive camera adoption inside factories. This mix shows how pricing, cloud migration, and NDAA-compliant hardware rules vary by end user. The sources listed illustrate our desk work and are not exhaustive; dozens of additional documents underpin every data point we retain.

Market-Sizing & Forecasting

Top-down modeling starts with national construction spending and active commercial floor space to build an addressable pool, which is then multiplied by camera penetration ratios derived from our interviews. Parallel supplier roll-ups of leading hardware vendors serve as a bottom-up check. Key variables include average camera density per 1,000 sq ft, migration rate from analog to IP, cloud storage attach rate, NDAA-driven replacement share, and city-level smart pole deployments. A multivariate regression with ARIMA refinements projects each driver, producing a market value and a growth rate for the forecast period. Gaps where bottom-up totals lag the top-down baseline are closed through weighted adjustments using verified shipment data.

Data Validation & Update Cycle

Before publication, two senior analysts review variance flags, cross-check currency conversions, and benchmark outputs against new contracts or regulatory shifts. The model refreshes annually, and interim updates occur whenever a material event, such as a federal funding tranche or major supply chain disruption, changes demand outlooks.

Why Our North America Video Surveillance Systems Baseline Earns Trust

Published numbers often diverge because firms frame geography, product mix, and cloud services differently, and some rely on dated assumptions. By anchoring scope to full systems across all three NAFTA nations and by treating VSaaS revenue as integral, Mordor offers a wider, more current lens.

Key gap drivers include competitors quoting only the United States, omitting cloud subscriptions, using 2023 pricing, or relying on vendor press releases without shipment audits. Our annual refresh and dual-path modeling mitigate these blind spots.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.84 B (2025) | Mordor Intelligence | - |

| USD 18.84 B (2024) | Regional Consultancy A | Covers US only and excludes VSaaS revenue, older base year |

| USD 12.34 B (2024) | Trade Journal B | Hardware-focused US estimate, relies on vendor declarations, no cloud adjustment |

These contrasts show that while other publishers highlight slices of the opportunity, Mordor's disciplined scope selection, live primary validation, and yearly recalibration furnish decision-makers with the most dependable baseline for planning.

Key Questions Answered in the Report

What is the projected value of the North America video surveillance systems market by 2031?

The market is forecast to reach USD 56.73 billion by 2031, growing at a 13.28% CAGR.

Which component category is expanding fastest?

Video Surveillance as a Service is the fastest-growing component, set to post a 15.5% CAGR between 2026 and 2031.

How much of the market do cloud deployments currently represent?

Cloud deployments accounted for 15.90% of revenue in 2025 and are projected to rise swiftly at a 15.9% CAGR.

Which country is the fastest-growing national market in North America?

Mexico is expanding at a 13.7% CAGR, propelled by smart city initiatives and infrastructure investment.

Why are edge-AI cameras gaining traction?

Embedded processors cut bandwidth by up to 70% and eliminate costly servers, lowering total cost of ownership and enabling real-time analytics.

What impact do new privacy regulations have on the market?

State-level restrictions on facial recognition and stricter federal data-protection rules raise compliance costs and slow analytics adoption in certain jurisdictions.

Page last updated on: