Surveillance Camera Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

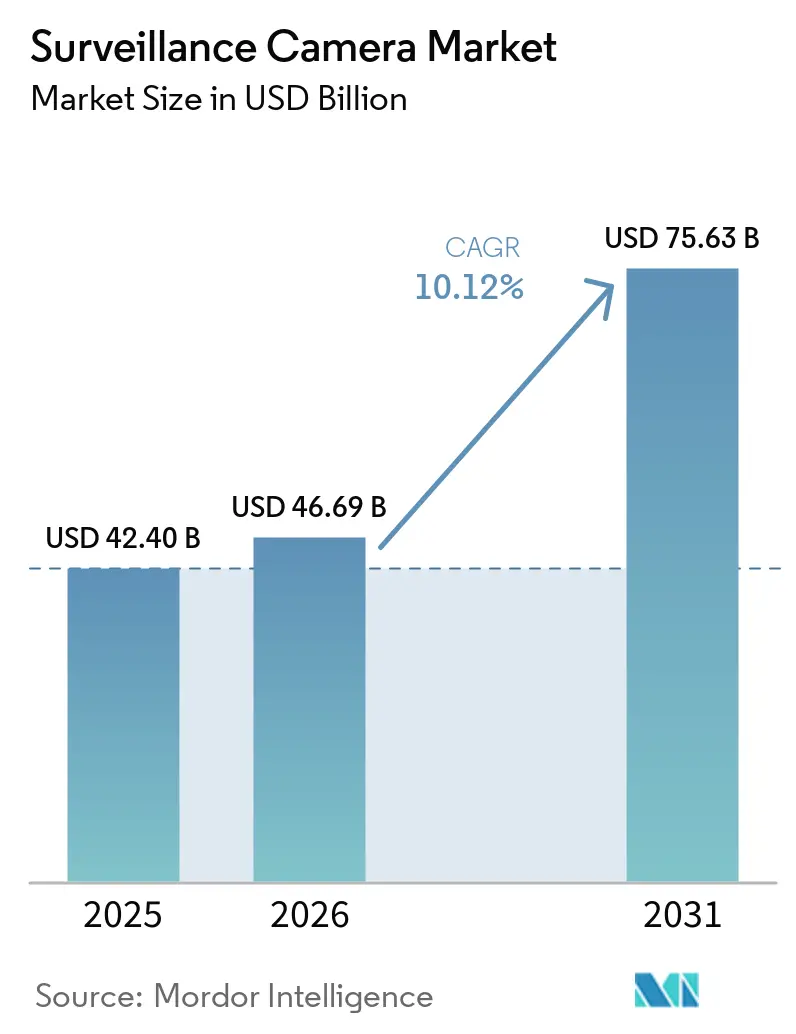

| Market Size (2026) | USD 46.69 Billion |

| Market Size (2031) | USD 75.63 Billion |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

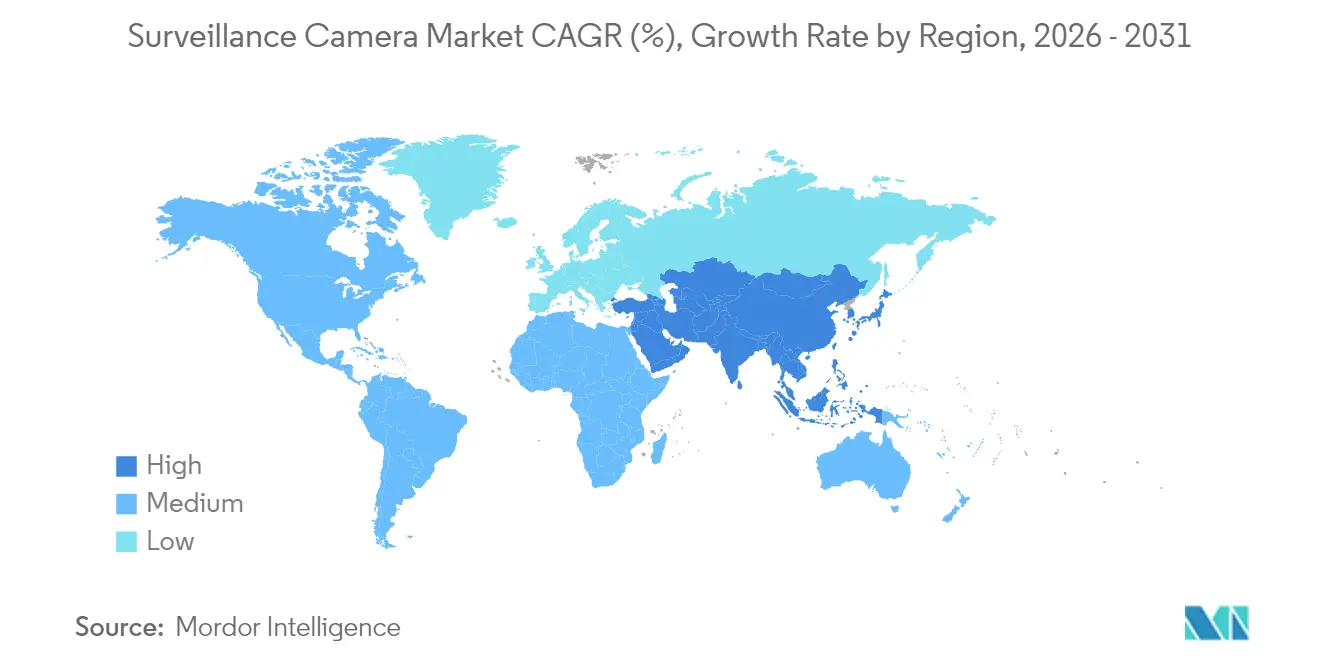

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

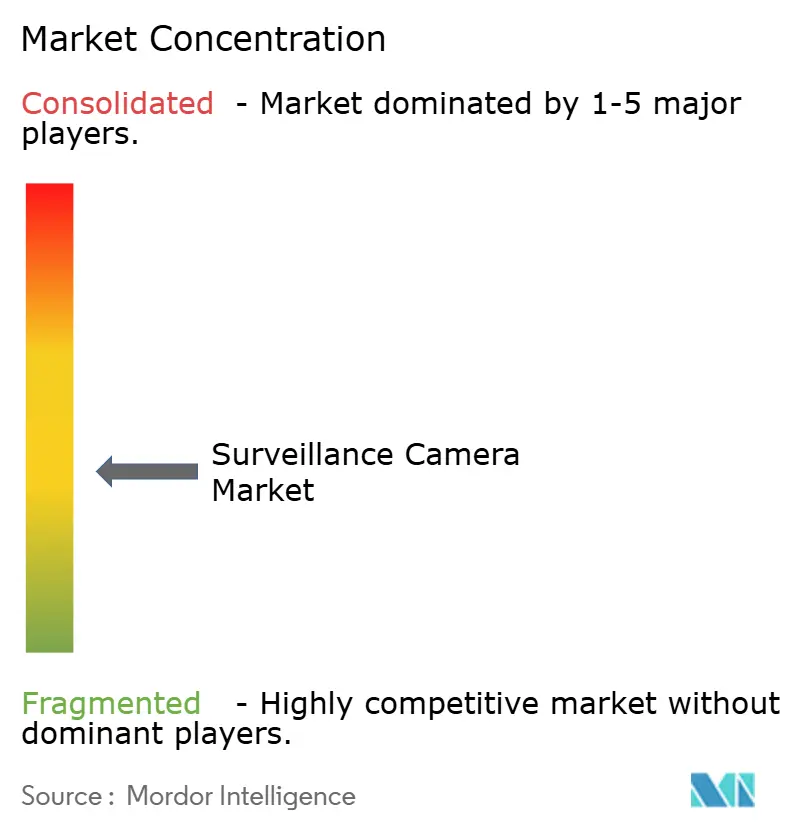

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surveillance Camera Market Analysis by Mordor Intelligence

surveillance camera market size in 2026 is estimated at USD 46.69 billion, growing from 2025 value of USD 42.40 billion with 2031 projections showing USD 75.63 billion, growing at 10.12% CAGR over 2026-2031. Growth is powered by AI-enabled edge analytics that convert video feeds into real-time operational intelligence and by expanding 5G coverage that removes bandwidth constraints for Ultra-HD streaming. Demand is shifting from hardware sales to integrated platforms that bundle cameras, cloud storage, and analytics, reshaping vendor business models. Asian safe-city programs, retail loss-prevention upgrades in North America, and privacy-conscious deployments in Europe are creating distinct regional demand patterns. Competitive strategy is diverging: cost-optimized Chinese manufacturers dominate volume sales, while Western suppliers focus on cybersecurity and specialized analytics to win high-value projects.

Key Report Takeaways

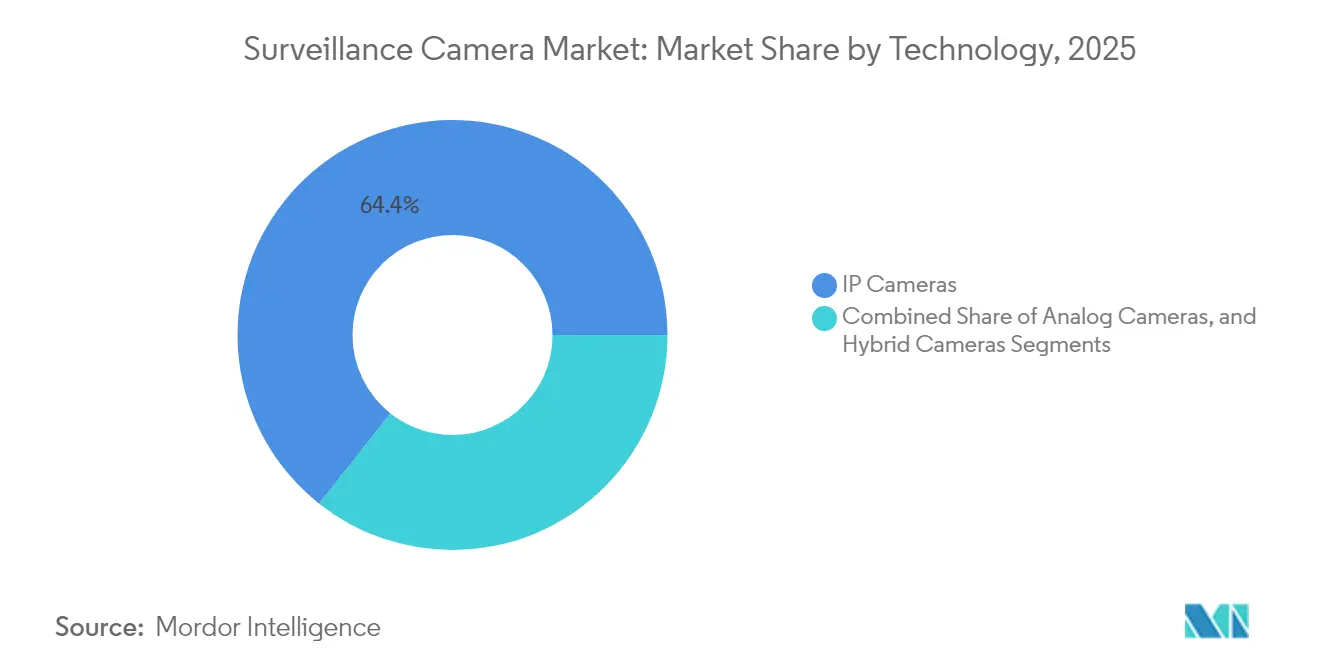

- By technology, IP cameras held 64.35% of the surveillance camera market revenue in 2025; hybrid models register the fastest expansion at a 11.84% CAGR through 2031.

- By form factor, dome cameras led with 31.45% of 2025 revenue, while PTZ units grow the quickest at a 12.88% CAGR to 2031.

- By resolution, full-HD systems accounted for 31.60% of 2025 revenue; Ultra-HD/4K platforms are set to rise at a 15.02% CAGR through 2031.

- By connectivity, wired solutions contributed 69.20% of 2025 revenue; cellular connections record a 13.06% CAGR between 2026-2031.

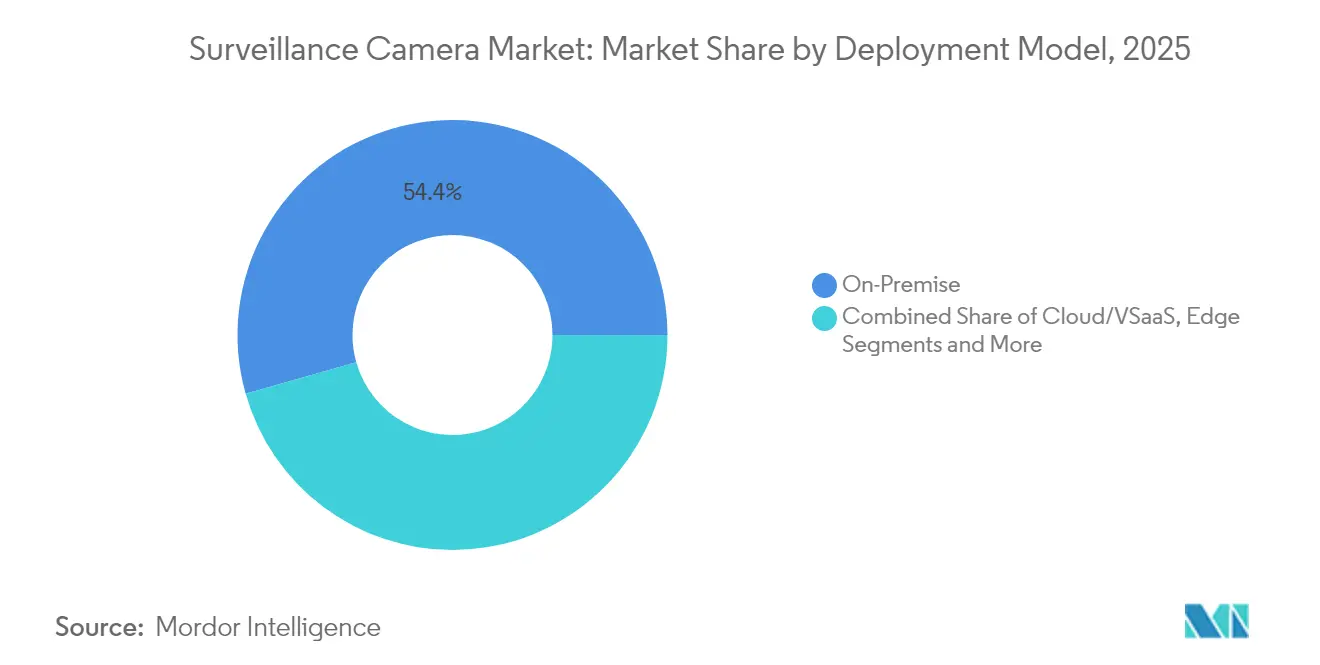

- By deployment model, on-premise architectures held 54.40% of the surveillance camera market revenue in 2025; cloud/VSaaS is expanding at a 14.18% CAGR to 2031

- By end-user, commercial/retail secured 22.55% share of the surveillance camera market revenue in 2025; the residential segment is pacing ahead at a 12.98% CAGR through 2031.

- Hikvision and Dahua together captured 39.20% surveillance camera market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surveillance Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enabling 5G-Edge Networks Unlocking Real-Time UHD Surveillance in Smart Factories | +2.1% | North America, Europe, East Asia | Medium term (2-4 years) |

| Mandates for AI-based Crowd Analytics in Mega Asian Transport Hubs | +1.8% | Asia, Middle East | Short term (≤ 2 years) |

| Shift to Cloud-Native VSaaS Among North-American Multi-site Retailers | +1.7% | North America, Europe | Medium term (2-4 years) |

| Rapid Roll-out of Safe-City Programs in Middle-East Oil Economies | +1.5% | Middle East, North Africa | Medium term (2-4 years) |

| Insurance Incentives for Connected-Home Cameras in Europe's High-Risk Urban Zones | +1.3% | Europe, North America | Short term (≤ 2 years) |

| Heightened Compliance Requirements for Critical Infrastructure under US TSA Directives | +1.1% | North America, with spillover to allied nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G-edge networks unlock UHD surveillance

Industrial sites adopting 5G achieve sub-10 ms latency, allowing 4K cameras to stream uninterrupted while embedded AI flags anomalies such as equipment defects or safety breaches. Manufacturers report 37% fewer safety incidents and a 42% uptick in quality-control efficiency as edge inference replaces manual inspection.[1]Intel, “AI Outcomes in the Security Market and Beyond,” cdrdv2-public.intel.com

AI crowd analytics in mega Asian hubs

Transit authorities in Singapore and South Korea deploy analytics that distinguish routine movement from security threats, cutting false alarms by 76% and boosting detection accuracy to 94%. Passenger-flow insights improve staffing decisions, raising peak-hour throughput by 23%.

Safe-city programs accelerate in GCC capitals

Saudi Arabia lifted smart-city surveillance outlays by 34% in 2024, integrating multi-agency command centers that coordinate traffic, emergency response, and public services. Vendors supplying desert-rated hardware and AI modules gain an early-mover edge.

Cloud-native VSaaS adoption in North-American retail

Multi-site chains report 43% lower five-year total cost of ownership versus on-premise DVRs after migrating to cloud video platforms. Central dashboards merge loss-prevention feeds with merchandising analytics, transforming video data into revenue-driving insights.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating GPU Shortages Inflating AI-Camera BOM Costs | -1.2% | Global, with higher impact in North America and Europe | Short term (≤ 2 years) |

| Data-Localization Laws Hindering Cross-Border Video Storage in GCC & ASEAN | -0.9% | Middle East, Southeast Asia | Medium term (2-4 years) |

| Privacy-Centric OS Updates Curbing On-Device Face-Recognition in EU | -0.8% | Europe, with potential spillover to other privacy-conscious regions | Medium term (2-4 years) |

| Power Constraints in Off-Grid Mining Sites Limiting UHD Adoption | -0.6% | Africa, South America, Remote Asia-Pacific regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GPU shortages raise AI-camera costs

Edge-AI cameras face component cost spikes of 18-25% as delivery windows for vision accelerators stretch to 26 weeks. Smaller vendors without preferential allocation risk delays that can shift channel share to larger rivals.

Data localization complicates cloud roll-outs

ASEAN and GCC rules mandating in-country video storage inflate compliance spending by up to 60% for multinationals and force vendors to design hybrid architectures that keep biometric data on-premise while pushing less-sensitive footage to the cloud.[2]Shota Watanabe et al., “Current Status of ASEAN Data Governance,” eria.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: IP leadership accelerates analog sunset

IP cameras commanded a 64.35% revenue share in 2025, and their installed base is expanding on the back of PoE simplicity and software-defined functionality. Hybrid models, which bridge coaxial infrastructure to IP analytics, are advancing at a 11.84% CAGR as cost-sensitive users phase out legacy analog gear. Value is migrating from the lens to the algorithm; consequently, software-centric entrants capture margin by embedding AI into video management systems that formerly relied on human monitoring.

Market incumbents now bundle API-rich platforms that integrate intrusion sensors, access control, and business dashboards. This service-oriented pivot positions vendors to monetize recurring analytics subscriptions rather than one-time camera sales, a trend reshaping revenue recognition across the surveillance camera market.

By Form Factor: PTZ versatility drives premium growth

Dome units retained 31.45% of 2025 sales thanks to vandal resistance and aesthetic appeal in retail aisles and office lobbies. PTZ models, with a 12.88% CAGR, allow operators to track suspects across wide areas, making a single device the functional equivalent of multiple fixed cameras and supporting higher average selling prices. Bullet designs remain favored for perimeter defense where directional deterrence is paramount, while turret and multi-sensor innovations answer niche requirements for 360° coverage without fisheye distortion.

Manufacturers are embedding auto-tracking algorithms that reposition PTZ lenses in real time, ensuring that the surveillance camera market size for PTZ solutions captures incremental share from static devices in logistics hubs and transport terminals. At the same time, thermographic options are being specified for smoke-filled or zero-light environments to safeguard critical energy assets.

By Resolution: 4K adoption redefines detail capture

Full-HD systems held 31.60% of 2025 revenue, balancing fidelity with manageable storage. Ultra-HD/4K units, scaling at a 15.02% CAGR, satisfy stringent forensic requirements for license-plate recognition and facial identification. Compression advancements and falling sensor costs lower bandwidth demands, enabling 4K roll-outs even on existing network backbones. HD (720p-1080p) remains prevalent in budget applications, though its market trajectory is gradually tapering as AI models demand higher pixel density to maintain precision.

Vendors now tout AI super-resolution that reconstructs details lost in compression, effectively stretching the usability of mid-tier sensors. By pairing high-resolution capture with edge analytics, suppliers convert video streams into metadata, reducing storage overhead and reinforcing demand for premium cameras within the surveillance camera market.

By Connectivity: Cellular expansion untethers surveillance

Wired links—chiefly Ethernet with PoE—delivered 69.20% of 2025 revenue through their reliability and ability to power devices without local outlets. Cellular connections, lifting at a 13.06% CAGR, unlock deployment in temporary sites, remote pipelines, and disaster zones. 5G’s gigabit throughput makes real-time UHD streaming feasible, democratizing advanced analytics in mobile contexts such as law-enforcement command vans.

Hybrid architectures that blend wired, Wi-Fi, and LTE back-up ensure resilience against single-path failures, a priority for critical infrastructure operators. Edge storage that records locally when coverage drops further strengthens business cases for wireless deployments, expanding the surveillance camera market to locations previously deemed unreachable.

By Deployment Model: Cloud migration reshapes infrastructure

On-premise deployments controlled 54.40% of 2025 revenue, supported by compliance obligations in finance and critical infrastructure. Cloud/VSaaS, growing 14.18% annually, erodes hardware dependency by shifting video recording and analytics to managed data centers. Enterprises cite reduced maintenance, elastic scaling, and global policy enforcement as decisive benefits.

The surveillance camera market size for hybrid deployments is climbing as firms safeguard sensitive footage locally while leveraging cloud AI for occupancy analytics and anomaly detection. Camera-embedded SSDs and micro-data centers at the edge orchestrate bandwidth-aware uploads, trimming connectivity costs and accelerating AI inference latency.

By End-User Industry: Residential segment disrupts commercial dominance

Commercial and retail facilities generated 22.55% of 2025 revenue through shrinkage mitigation and shopper analytics. The residential smart-home category grows 12.98% annually as insurers in Europe offer premium discounts to homeowners who install connected cameras. Mid-tier devices with DIY installation and mobile access resonate with new buyers and expand the addressable surveillance camera market.

Governments and defense remain heavy spenders on high-spec systems, particularly for perimeter protection and border control. Healthcare, transportation, and manufacturing verticals deploy AI modules that analyze workflows for safety breaches and throughput optimization, embedding cameras into broader Industry 4.0 frameworks.

Geography Analysis

Asia accounted for 40.60% of global revenue in 2025 and continues to expand at an 10.78% CAGR as China’s public-safety investments and India’s smart-city tenders accelerate procurement cycles. Singapore’s metro upgraded to AI crowd analytics that trimmed false alerts by 76% while boosting threat recognition accuracy to 94%. Regional manufacturers capitalize on domestic scale to iterate rapidly, closing technology gaps with Western competitors.

North America holds the second-largest share, underpinned by retail VSaaS adoption and federal initiatives protecting critical infrastructure. Forty-four percent of users now operate at least one cloud-connected site, a figure that grows as multi-location chains consolidate security operations. Privacy mandates in Canada spur demand for anonymization tools, influencing product roadmaps oriented toward compliance-ready analytics.

Europe’s market is shaped by GDPR and the emerging AI Act, pushing suppliers to integrate privacy-preserving functions such as on-device redaction. The United Kingdom modernizes an extensive legacy network with edge AI, while Germany emphasizes industrial integration where cameras feed quality-control systems. Nordic municipalities deploy cameras not only for safety but also to manage congestion and environmental metrics, expanding application breadth.

Mordor Intelligence provides coverage of the surveillance camera market across other key regional markets, including Latin America, Europe, and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Mexico, United Kingdom, China, United States, France, Canada, and India incorporating local coverage and market participation, as required.

Competitive Landscape

Global supply is bifurcated: Hikvision and Dahua collectively hold 40% share, leveraging vertically integrated factories and component scale to dominate volume orders. Axis Communications, Bosch, and Hanwha pursue value-added niches, bundling cybersecurity hardening and edge analytics to capture premium projects. The barbell structure leaves a long tail of specialists focused on thermal imaging, body-worn solutions, or AI software overlays.

Geopolitical scrutiny of Chinese vendors in Western markets spurs diversification toward regional suppliers and cloud-first challengers. Bosch’s commercial alliance to market Sony surveillance outside Japan exemplifies asset-light expansion that avoids integration hurdles and accelerates time-to-market. Cloud natives such as Eagle Eye Networks monetize subscription analytics atop commodity hardware, signaling a shift in bargaining power from hardware producers to platform orchestrators.

M&A and strategic partnerships are intensifying as traditional camera makers seek AI expertise, while IT incumbents enter physical security arenas. Cybersecurity certifications like ETSI EN 303 645 become competitive differentiators, as end users elevate threat models to encompass camera firmware and supply-chain provenance. Amid this strategic jockeying, vendors that orchestrate an ecosystem of cameras, analytics, and cloud orchestration are best positioned to unlock lifetime customer value in the surveillance camera market.

Surveillance Camera Industry Leaders

Hangzhou Hikvision Digital Technology Co., Ltd.

Zhejiang Dahua Technology Co., Ltd.

Bosch Security Systems GmbH

Honeywell International Inc.

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hikvision launched HikCentral Lite, an AI-enabled VMS for SMBs, positioning the firm to tap underserved small-business demand.

- April 2025: Axis Communications published “The State of AI in Video Surveillance,” reinforcing thought-leadership credentials and guiding enterprise AI roadmaps.

- March 2025: Hikvision secured ETSI EN 303 645 and EN 18031 certifications, elevating its cyber-posture and mitigating procurement barriers in sensitive projects.

- February 2025: Dahua partnered with EdgeVision to embed generative AI threat modeling, enhancing anomaly detection and targeting higher-margin analytics-centric contracts.

Global Surveillance Camera Market Report Scope

Video surveillance cameras, comprising monitor/display units and recorders, come in analog or digital formats. They find placement in both indoor and outdoor spaces of buildings, operating around the clock. They can be set to record either in response to motion or at scheduled intervals. Businesses primarily employ these cameras for forensics, post-incident analysis, remote monitoring, and situational awareness. The market is defined by the revenue accrued from the sales of different types of products and services to various end users across the regions, including North America, Europe, Asia-Pacific, and the rest of the world.

The surveillance camera market is segmented by type (analog cameras, IP-based cameras), end-user industry (retail, airports, education, banking, healthcare, transportation, and logistics), and geography (North America, Europe, Asia Pacific, Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Analog Cameras |

| IP Cameras |

| Hybrid Cameras |

| Dome Cameras |

| Bullet Cameras |

| PTZ Cameras |

| Box Cameras |

| Turret Cameras |

| Fisheye Cameras |

| Thermal Cameras |

| Non-HD (≤720p) |

| HD (720p-1080p) |

| Full HD (1080p-2K) |

| Ultra HD / 4K (≥4K) |

| Wired |

| Power-over-Ethernet (PoE) |

| Wireless (Wi-Fi/Zigbee) |

| Cellular (4G/5G NB-IoT) |

| On-Premise |

| Cloud / VSaaS |

| Edge / On-Device Storage |

| Hybrid |

| Banking and Financial Institutions (BFSI) |

| Transportation and Infrastructure |

| Government and Defense |

| Healthcare Facilities |

| Industrial and Manufacturing |

| Retail and Hospitality |

| Enterprise and Commercial Offices |

| Residential / Smart Home |

| Logistics and Warehousing |

| Educational Campuses |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe | |

| APAC | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Australia | |

| New Zealand | |

| ASEAN-5 | |

| Rest of APAC | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Technology | Analog Cameras | |

| IP Cameras | ||

| Hybrid Cameras | ||

| By Form Factor | Dome Cameras | |

| Bullet Cameras | ||

| PTZ Cameras | ||

| Box Cameras | ||

| Turret Cameras | ||

| Fisheye Cameras | ||

| Thermal Cameras | ||

| By Resolution | Non-HD (≤720p) | |

| HD (720p-1080p) | ||

| Full HD (1080p-2K) | ||

| Ultra HD / 4K (≥4K) | ||

| By Connectivity | Wired | |

| Power-over-Ethernet (PoE) | ||

| Wireless (Wi-Fi/Zigbee) | ||

| Cellular (4G/5G NB-IoT) | ||

| By Deployment Model | On-Premise | |

| Cloud / VSaaS | ||

| Edge / On-Device Storage | ||

| Hybrid | ||

| By End-User Industry | Banking and Financial Institutions (BFSI) | |

| Transportation and Infrastructure | ||

| Government and Defense | ||

| Healthcare Facilities | ||

| Industrial and Manufacturing | ||

| Retail and Hospitality | ||

| Enterprise and Commercial Offices | ||

| Residential / Smart Home | ||

| Logistics and Warehousing | ||

| Educational Campuses | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| APAC | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Australia | ||

| New Zealand | ||

| ASEAN-5 | ||

| Rest of APAC | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the surveillance camera market and how fast is it growing?

The market stands at USD 46.69 billion in 2026 and is projected to expand to USD 75.63 billion by 2031, reflecting a 10.12% CAGR.

Which technology segment will add the most value over the next five years?

IP cameras remain the largest revenue generator, while hybrid IP-analog models post the fastest growth as enterprises replace legacy infrastructure in phases.

How quickly is cloud-based Video Surveillance as a Service (VSaaS) scaling?

Cloud/VSaaS deployments are advancing at a 14.18% CAGR over 2026-2031, driven by lower ownership costs and centralized management for multi-site operations.

What role does 5G play in future surveillance deployments?

5G enables real-time 4K streaming with sub-10 ms latency, allowing industrial and mobile applications to run edge analytics without local servers.

Which geographic region offers the strongest demand outlook?

Asia commands 40.60% of global revenue and continues to outpace other regions with an 10.78% CAGR, propelled by safe-city initiatives and smart-infrastructure spending.

How concentrated is supplier power in this market?

The top five vendors hold roughly 70% of global sales, indicating moderate concentration that still leaves room for agile specialists in advanced analytics and cloud platforms.

Page last updated on: