Home Security Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

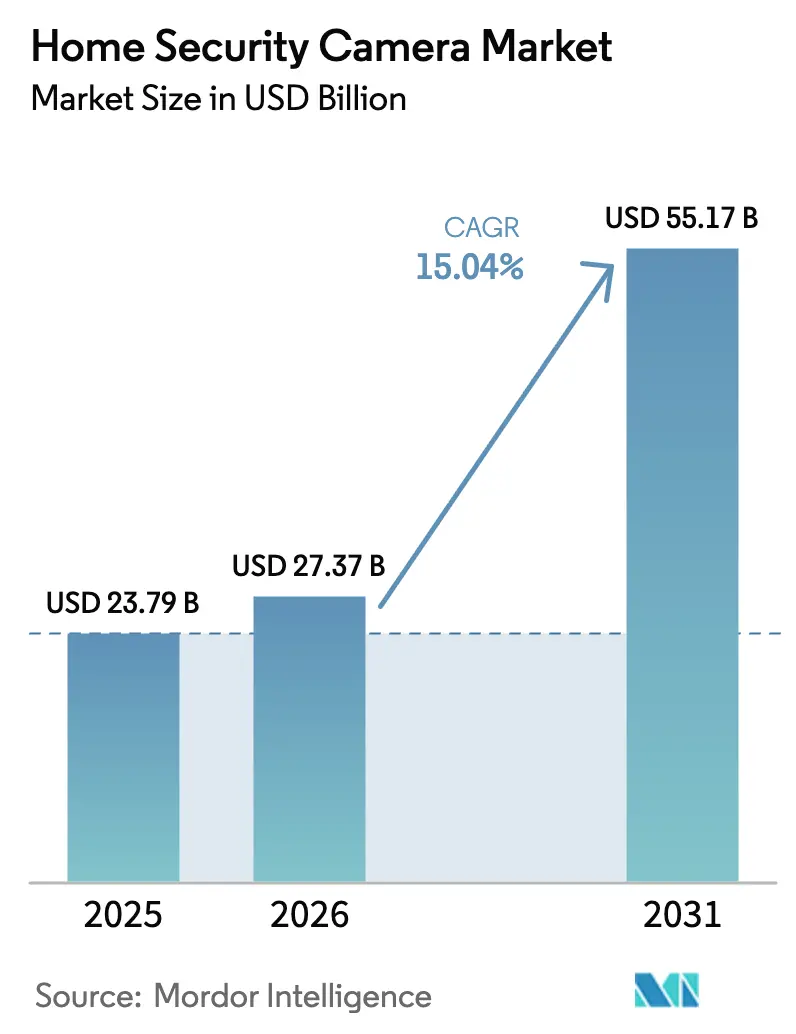

| Market Size (2026) | USD 27.37 Billion |

| Market Size (2031) | USD 55.17 Billion |

| Growth Rate (2026 - 2031) | 15.04% CAGR |

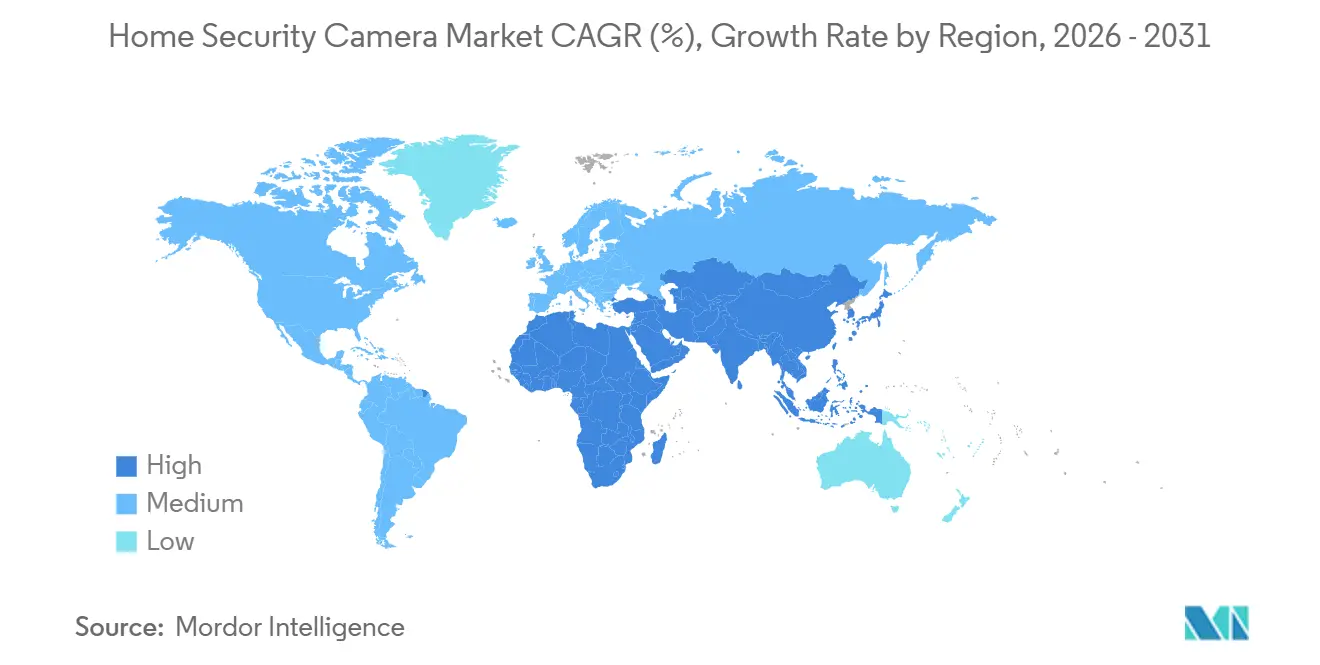

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Security Camera Market Analysis by Mordor Intelligence

The home security camera market size is expected to grow from USD 23.79 billion in 2025 to USD 27.37 billion in 2026 and is forecast to reach USD 55.17 billion by 2031 at 15.04% CAGR over 2026-2031. The growth reflects falling hardware costs, maturing cloud infrastructure, and rising consumer focus on preventive security amid urban crime patterns and insurance incentives. Artificial intelligence (AI) now augments traditional surveillance, enabling predictive analytics that broaden the value proposition of the home security camera market from passive monitoring to proactive risk mitigation. Wireless models dominate with 61% adoption, while battery and solar power solutions rise fastest as users seek flexible installation and energy independence. Data-privacy regulations in Europe and intensifying geopolitical scrutiny on Chinese brands temper the pace but also unlock opportunities for Western suppliers that differentiate on privacy compliance and supply-chain resilience. [1]European Data Protection Board, “Guidelines 3/2019 on Processing of Personal Data through Video Devices Version 2.0,” edpb.europa.eu

Key Report Takeaways

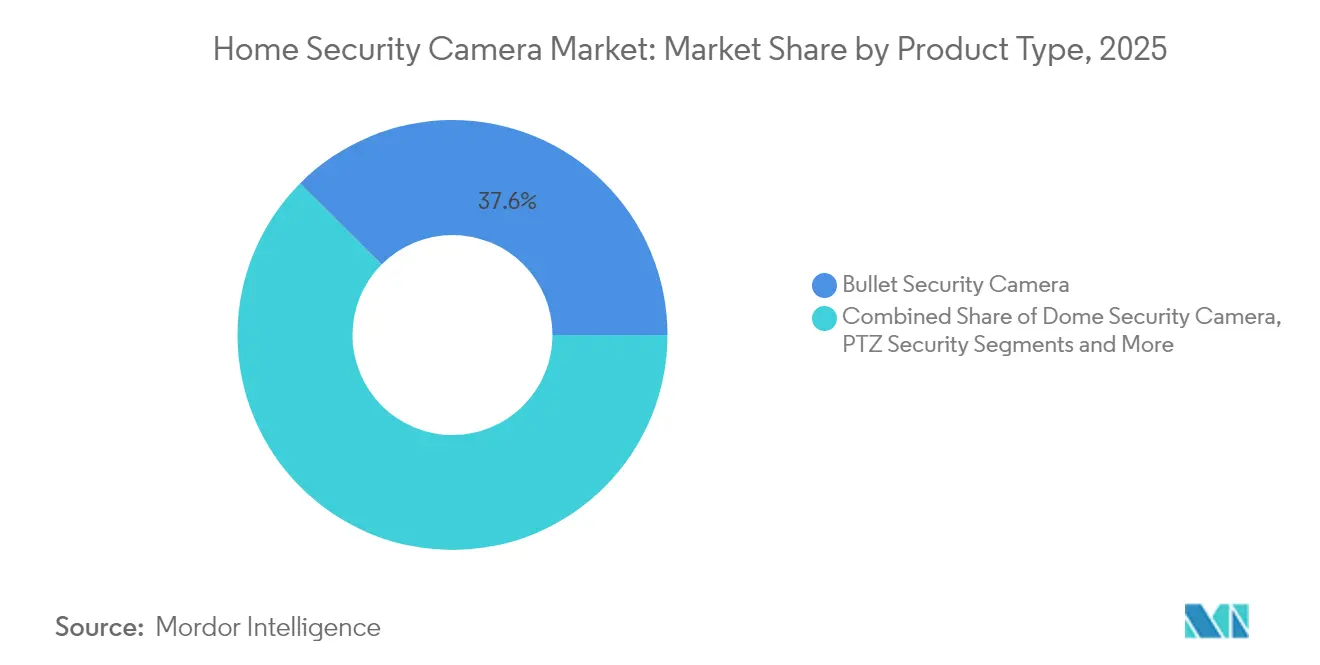

- By product type, bullet cameras held 37.55% of the home security camera market share in 2025, whereas doorbell cameras are projected to grow at 15.86% CAGR to 2031.

- By connectivity, wireless systems accounted for 60.45% of the home security camera market share in 2025, while the segment is set to expand at a 15.62% CAGR through 2031.

- By power source, AC-powered devices captured 71.20% share of the home security camera market size in 2025, yet battery and solar models are forecast to register a 15.28% CAGR to 2031.

- By resolution, HD models (≤1080p) represented 45.40% of the home security camera market size in 2025, whereas 4K cameras will advance at a 15.81% CAGR over the forecast horizon.

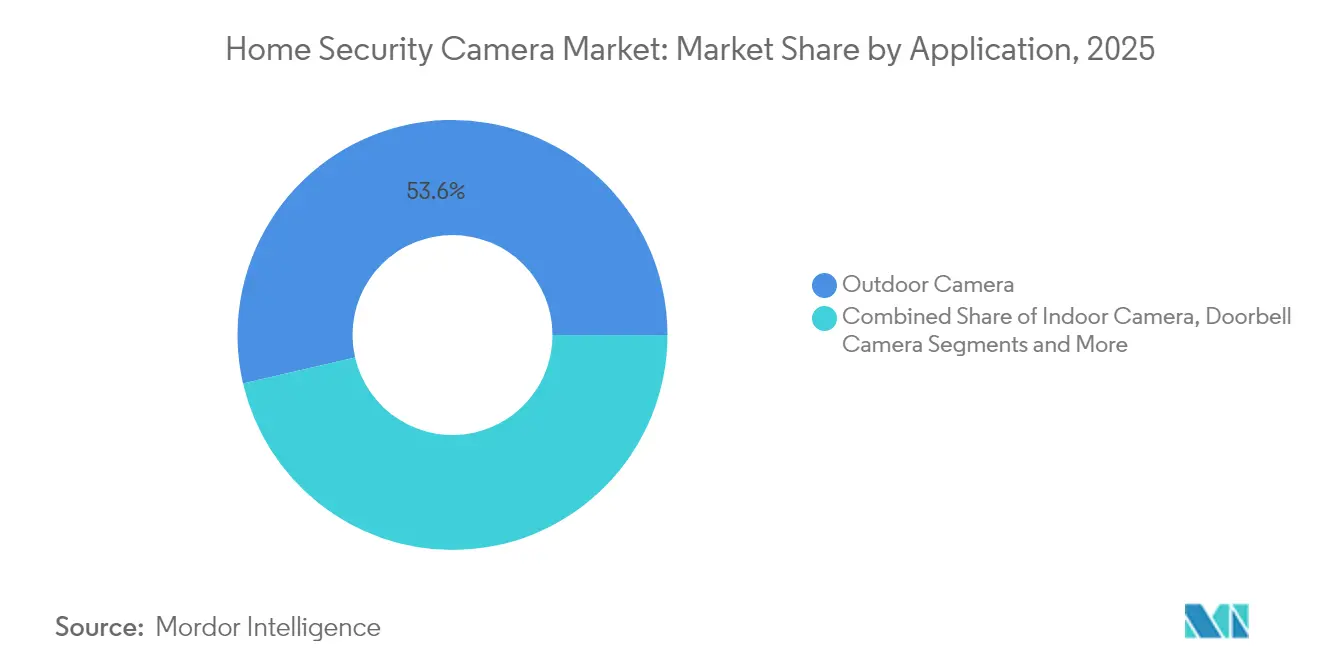

- By application, outdoor units commanded 53.62% share of the home security camera market size in 2025, and doorbell deployments are expected to grow at 15.84% CAGR to 2031.

- By geography, Asia Pacific is the fastest-growing geography with a 16.34% CAGR, whereas North America remains the largest contributor at 37.60% share of the home security camera market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Home Security Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration with Smart-Home Ecosystems and Voice Assistants in North America and Europe | +2.5% | North America and Europe | Medium term (2-4 years) |

| Declining ASP of HD and 4K IP Cameras due to Chinese OEM Overcapacity | +1.8% | Global | Short term (≤ 2 years) |

| Insurance Premium Discounts for Homes with Verified Video Monitoring | +0.9% | North America and Europe | Medium term (2-4 years) |

| Rapid FTTH Roll-outs Enabling 24/7 Cloud Uploads in ASEAN | +1.2% | ASEAN | Long term (≥ 4 years) |

| Urban Middle-Class Demand after Rise in Parcel Theft | +2.1% | Global, concentrated in urban areas | Short term (≤ 2 years) |

| Government Smart-City Safety Grants Subsidising Residential CCTV | +1.5% | North America, Europe, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration with Smart-Home Ecosystems and Voice Assistants

The convergence of security cameras, smart displays, and voice control creates a network effect that raises switching costs for consumers and cements platform loyalty. Apple’s planned AI Home Display underscores how major tech firms embed surveillance at the center of broader automation suites. [2]Jack Purcher, “Apple to launch an AI Home Display in 2025 with a built-in camera for Home Security,” Patently Apple, patentlyapple.comAmazon’s Ring pushes the envelope with AI-generated motion summaries that transform raw video into actionable insights, reinforcing the strategic value of proprietary cloud analytics. As ecosystems mature, hardware margins compress while recurring service revenues expand, redefining competitive dynamics in the home security camera market.

Declining ASP of HD and 4K IP Cameras from Chinese OEM Overcapacity

Overcapacity among Chinese original-equipment manufacturers triggers a price deflation cycle that democratizes 4K resolution, yet forces Western suppliers to pivot toward differentiated software and privacy features. Hikvision’s 2024 price list shows mainstream 4K models trending below prior HD price points, eroding the entry barrier for high-resolution adoption. Simultaneously, the US replacement program for restricted vendors channels USD 247 million into domestic alternatives, accelerating a bifurcated market where price-sensitive households gravitate to Chinese brands, while security-critical users favor Western vendors despite higher costs. [3]Office of Community Oriented Policing Services, “FY24 COPS Technology and Equipment Program Invitational Solicitation,” cops.usdoj.gov

Insurance Premium Discounts for Homes with Verified Video Monitoring

Insurers now leverage camera-based verification to lower claims frequency, translating into premium rebates that offset device costs. Package-theft losses average USD 81.91, yet doorbell camera penetration among victims remains low, revealing headroom for insurer-driven adoption programs. [4]Matt Horwitz, “Package Theft Statistics,” Chamber of Commerce, chamberofcommerce.org The alignment of financial incentives with preventative technology expands the total addressable base for the home security camera market, particularly among risk-averse urban homeowners.

Rapid FTTH Roll-outs Enabling 24/7 Cloud Uploads in ASEAN

Fiber backbones across Southeast Asia eliminate bandwidth bottlenecks that previously capped cloud storage usage for high-resolution streams. Government smart-city grants fuel residential connectivity, allowing continuous recording and AI analytics that shift cameras from local devices to cloud-native platforms. Vendors that optimize codecs and edge processing for variable bandwidth environments stand to capture outsized growth in these emerging markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy Regulations Limiting Continuous Cloud Recording | -1.4% | Europe, California | Long term (≥ 4 years) |

| Saturation of Early-Adopter Segments in Developed Markets | -0.8% | North America and Europe | Medium term (2-4 years) |

| CMOS Image-Sensor Supply Volatility Creating Price Spikes | -1.1% | Global | Short term (≤ 2 years) |

| Rising Geopolitical Scrutiny on Chinese Brands | -0.9% | North America, Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Regulations Limiting Continuous Cloud Recording

European GDPR rules mandate data-protection impact assessments and curtail always-on recording, compelling manufacturers to invest in privacy-by-design architectures and local storage options. Compliance adds bill-of-materials cost and limits subscription revenue from cloud retention, dampening uptake among privacy-sensitive consumers.

CMOS Image-Sensor Supply Volatility Creating Price Spikes

Hurricane Helene’s disruption of high-purity quartz in North Carolina exposed the fragility of a critical node in the global semiconductor ecosystem, prompting manufacturers such as Axis to redesign platforms around diversified sourcing. Short-term shortages inflate component costs, narrowing margins and triggering staggered product launches that momentarily slow the home security camera market cadence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Doorbell Cameras Drive Innovation

Bullet cameras retained 37.55% share of the home security camera market in 2025, a position anchored in versatile indoor-outdoor use and cost-effectiveness. Doorbell units, while smaller in base, post the fastest 15.86% CAGR as households prioritize package-delivery verification and seamless smart-home integration. Dome and PTZ cameras occupy stable commercial niches, whereas box cameras remain specialized.

The 15.86% growth rate in doorbells reflects rising urban parcel theft and ecosystem incentives such as AI motion summaries from Ring that push adoption beyond early adopters. Insurance discounts accelerate demand, reinforcing the home security camera market trend toward entry-point visibility.

By Connectivity: Wireless Dominance Accelerates

Wireless devices captured 60.45% of the home security camera market share in 2025 and head toward a 15.62% CAGR to 2031. DIY-friendly installation and relocation agility improve the adoption curve, while proprietary long-range hubs such as Blink Sync Module XR extend coverage to 400 feet.

Wired systems maintain relevance for mission-critical commercial settings, yet slower growth reflects labor and cabling costs. As battery longevity improves, wireless penetration is expected to exceed two-thirds of the home security camera market by 2031.

By Power Source: Battery Solutions Gain Momentum

AC-powered units held a 71.20% share of the home security camera market size in 2025, yet battery and solar alternatives expand at 15.28% CAGR. Reolink’s Altas 20,000 mAh platform offers 96-hour 4K recording with solar topping, eliminating outlet dependency.

Energy-independent operation aligns with sustainability preferences and remote property use cases, establishing battery models as pivotal growth drivers for the home security camera market.

By Resolution: 4K Adoption Accelerates

HD models accounted for 45.40% of the home security camera market in 2025, but 4K units lead growth at 15.81% CAGR. Price deflation and better compression codecs make high-resolution streaming viable without escalating storage costs. Eufy’s 360-degree 4K LTE Cam S330 exemplifies premium positioning by bundling cellular uplinks and solar charging.

As costs decline, 4K is set to become the baseline, further elevating consumer expectations and raising competitive stakes across the home security camera market.

By Application: Outdoor Cameras Lead Market

Outdoor deployments represented 53.62% of the home security camera market size in 2025 due to perimeter protection priorities. Doorbell use cases exhibit the quickest 15.84% CAGR, merging visitor management with theft deterrence. Indoor cameras remain complementary for full coverage and pet monitoring.

Ring’s Pan-Tilt Indoor Cam at USD 79.99 shows how indoor devices evolve toward active 360-degree surveillance, positioning indoor adoption as an upsell to households that start with outdoor units.

By Sales Channel: Online Dominance Continues

E-commerce accounted for 64.25% of the home security camera market share in 2025, expanding at 14.88% CAGR. Direct-to-consumer strategies and rich virtual demonstrations reduce dependence on retail displays. Amazon’s bundling of hardware with Ring Protect subscriptions illustrates monetization beyond the initial sale.

Improved logistics and rising comfort with remote installation ensure that online sales retain momentum across all regions of the home security camera market.

Geography Analysis

North America commanded 37.60% of the home security camera market in 2025. High disposable income, suburban housing density, and insurer incentives sustain stable annual upgrades. The United States champions ecosystem lock-in through companies such as Amazon, while Canada’s colder climate elevates demand for energy-efficient models.

Asia Pacific posts the highest 16.34% CAGR through 2031. Regional FTTH expansion and smart-city grants in markets such as Singapore, Malaysia, and Thailand underpin cloud-centric adoption. China remains sizable despite external trade restrictions, driven by domestic demand and municipal safety initiatives. India’s rise of middle-class homeowners and e-commerce volumes fuels incremental unit sales. Japan and South Korea emphasize premium 4K and privacy-enhanced solutions, whereas Australia and New Zealand adopt high-end offerings supported by government rebates.

Europe records steady growth but at a moderated pace due to GDPR compliance costs. Germany and the United Kingdom show strong uptake of privacy-compliant hybrid storage models, while France, Italy, and Spain benefit from municipal subsidies that offset hardware prices. Manufacturers that localize data and offer on-premises video processing gain a competitive edge in the regional home security camera market.

Competitive Landscape

The competitive arena remains fragmented as technology conglomerates battle specialized entrants. Amazon (Ring) and Google (Nest) leverage AI and expansive cloud services to lock users into subscription ecosystems. Reolink and Arlo counter with battery innovation and lower total cost of ownership, eroding incumbents’ price premiums.

Acquisition activity accelerated in 2024. GardaWorld bought Stealth Monitoring, combining guarding services with AI video analytics to form a vertically integrated platform. Motorola Solutions added Silent Sentinel, expanding into long-range thermal vision for critical infrastructure. These moves demonstrate strategic convergence toward solutions-as-a-service, bundling hardware, cloud analytics, and manned monitoring.

Subscription economics gain prominence. Arlo ended 2024 with USD 210.1 million in annual recurring revenue and 2.8 million paid users, validating the pivot from unit sales to service annuities. Firms with pervasive ecosystems and diversified supply chains mitigate raw-material shocks, positioning themselves to capture share as the home security camera market matures.

Home Security Camera Industry Leaders

ADT Inc.

Hangzhou Hikvision Digital Technology Co. Ltd

Ring LLC (Amazon)

Lorex Technology Inc. (Flir)

Google LLC (Nest)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazon's Ring launched AI-generated security alerts that provide contextual summaries of motion activity captured by cameras and doorbells, representing a significant advancement in automated threat assessment capabilities.

- January 2025: Reolink introduced the Altas series of surveillance cameras capable of 24/7 recording without power outlets or internet connections, featuring 20,000 mAh batteries and ultra-low-power chipsets that enable nearly two years of operation in motion-triggered modes.

- January 2025: Ring partnered with Kidde to launch smart smoke and carbon monoxide alarms that integrate with the Ring app, expanding the company's ecosystem beyond security cameras to comprehensive home safety monitoring.

- January 2025: Amazon announced free 2K video resolution upgrades for Ring Floodlight Cam Pro and Spotlight Cam Pro models, along with new vehicle detection capabilities.

Global Home Security Camera Market Report Scope

A home security camera is a surveillance tool crafted to oversee and document activities around a residence, primarily for security reasons. Often integrated into comprehensive home security systems, these cameras bolster residential safety by delivering real-time video feeds, identifying potential intruders, and acting as a deterrent to criminal activities.

The study tracks the revenue accrued through the sale of the home security camera market by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The home security camera market is segmented by product type (bullet security camera, dome security camera, and IP security camera), connectivity (wired, and wireless), sales channel (online, and offline), application(doorbell camera, outdoor camera, and indoor camera), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Bullet Security Camera |

| Dome Security Camera |

| PTZ Security Camera |

| Box Security Camera |

| Doorbell (Video Doorbell) Camera |

| Wired |

| Wireless |

| AC-Powered |

| Battery / Solar-Powered |

| HD (≤1080p) |

| Full-HD (1080p) |

| 2K QHD |

| 4K UHD and Above |

| Indoor Camera |

| Outdoor Camera |

| Doorbell Camera |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Bullet Security Camera | ||

| Dome Security Camera | |||

| PTZ Security Camera | |||

| Box Security Camera | |||

| Doorbell (Video Doorbell) Camera | |||

| By Connectivity | Wired | ||

| Wireless | |||

| By Power Source | AC-Powered | ||

| Battery / Solar-Powered | |||

| By Resolution | HD (≤1080p) | ||

| Full-HD (1080p) | |||

| 2K QHD | |||

| 4K UHD and Above | |||

| By Application | Indoor Camera | ||

| Outdoor Camera | |||

| Doorbell Camera | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the home security camera market?

The market is valued at USD 27.37 billion in 2026 and is projected to climb to USD 55.17 billion by 2031.

Which segment is growing fastest within the home security camera market?

Doorbell cameras post the highest 15.86% CAGR through 2031, driven by parcel-theft deterrence and smart-home integration.

Why is Asia Pacific leading in growth?

Rapid fiber roll-outs, urbanization, and rising disposable incomes push the region to a 16.34% CAGR through 2031.

How are privacy regulations affecting adoption in Europe?

GDPR restrictions on continuous recording raise hardware costs and shift demand toward local storage models, slowing uptake.

What strategic trend defines competition among leading vendors?

A pivot from hardware margins to recurring service revenues—illustrated by Ring’s AI alerts and Arlo’s USD 210.1 million in annual recurring revenue—now shapes market positioning.

Page last updated on: