Gesture Recognition Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 37.41 Billion |

| Market Size (2031) | USD 104.16 Billion |

| Growth Rate (2026 - 2031) | 22.75% CAGR |

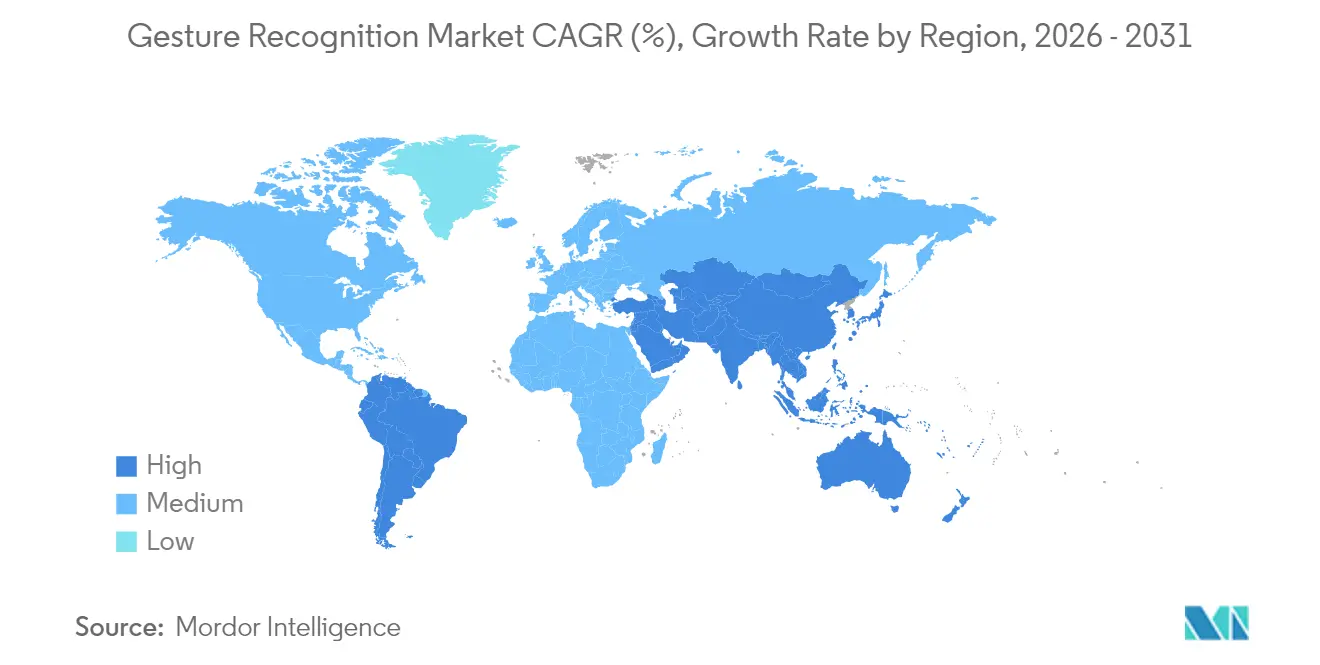

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

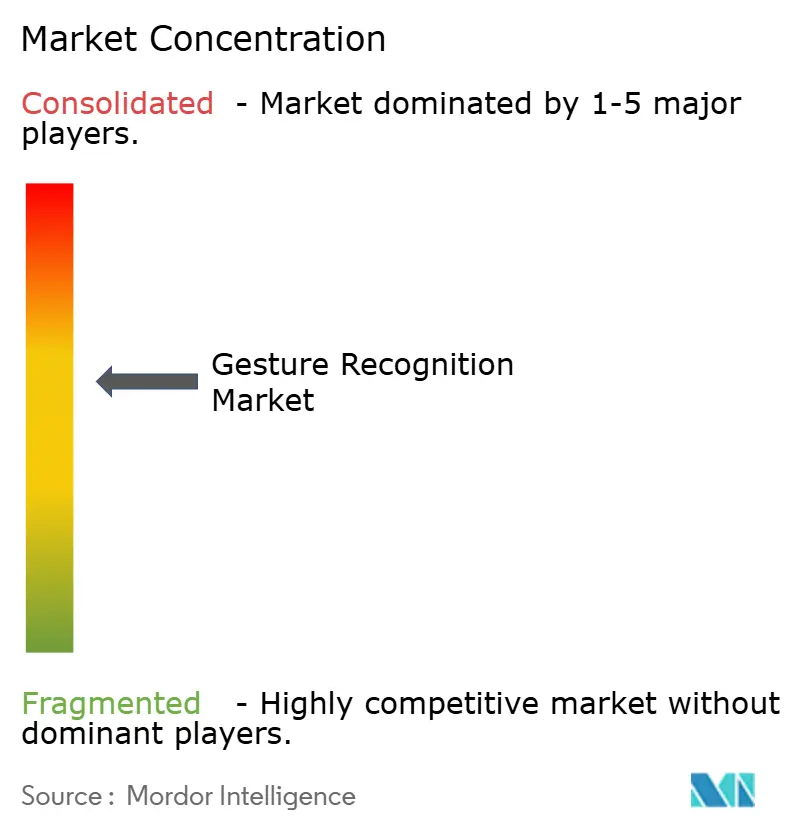

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gesture Recognition Market Analysis by Mordor Intelligence

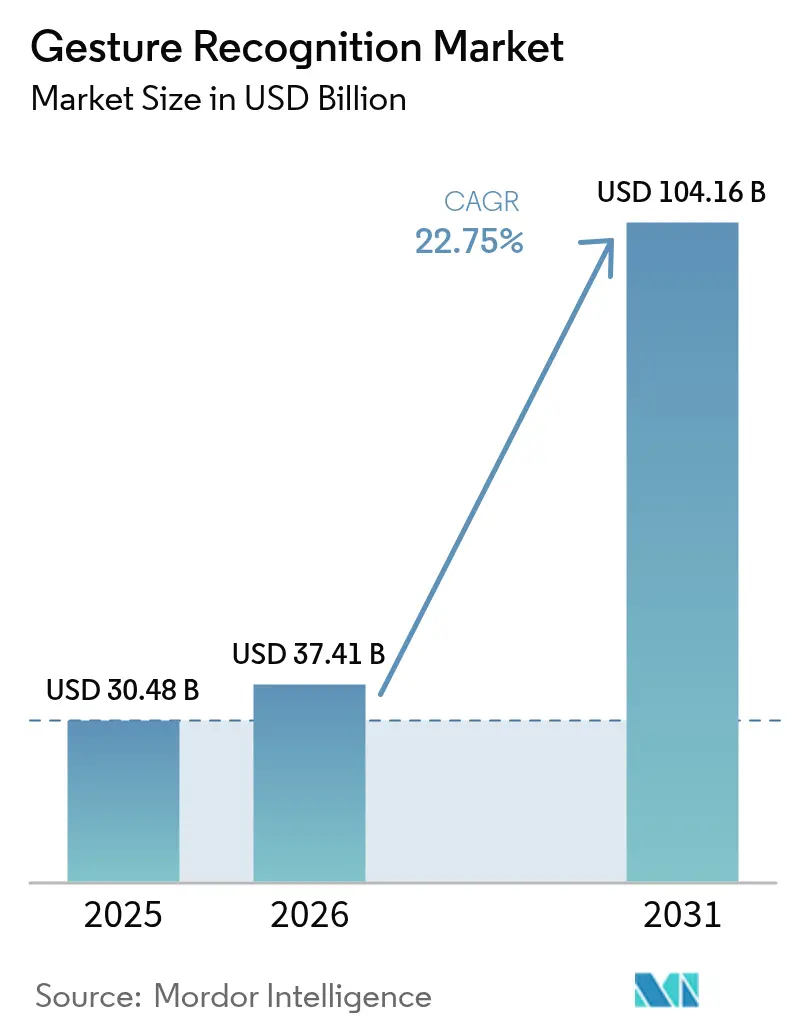

The Gesture Recognition market size is expected to grow from USD 30.48 billion in 2025 to USD 37.41 billion in 2026 and is forecast to reach USD 104.16 billion by 2031 at 22.75% CAGR over 2026-2031. This sustained expansion reflects the convergence of advanced millimeter-wave radar, multizone Time-of-Flight (ToF) sensors, and edge-AI algorithms that together enable responsive, low-latency human–machine interfaces across smartphones, vehicles, medical devices, and industrial equipment.[1]“Gesture Recognition,” st.com Accelerating sensor shipments in premium handsets, regulatory pressure on automotive safety systems, and infection-control imperatives in healthcare are jointly stimulating volume demand. At the same time, the gesture recognition market is witnessing a value shift from hardware-centric solutions toward software and AI stacks that personalize interactions, reduce false positives, and extend device longevity. Regional manufacturing incentives most notably the CHIPS Act in the United States and the European Chips Act are reshaping supply chains and creating new cost advantages for local component production. As these drivers converge, industry participants that integrate vertically across sensor, software, and cloud orchestration layers are positioned to capture disproportionate returns within the gesture recognition market.

Key Report Takeaways

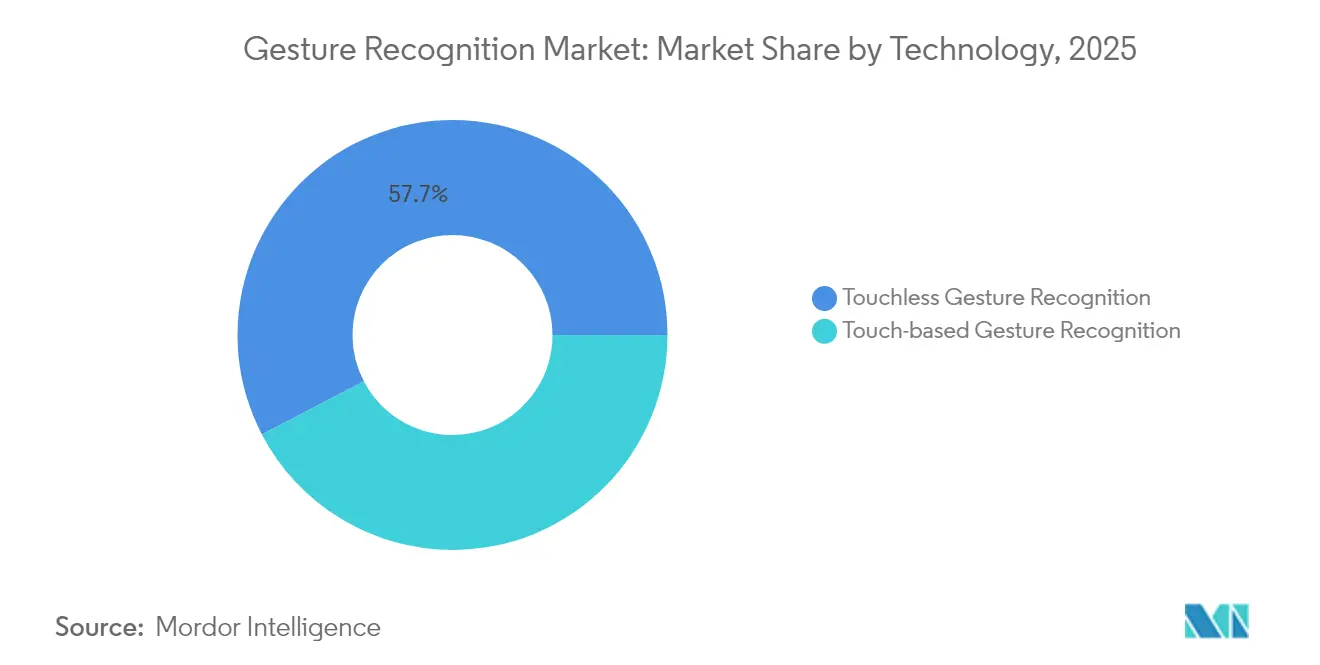

- By technology, touchless systems led with 57.65% revenue share of the gesture recognition market in 2025; 3-D depth and ToF solutions are projected to expand at a 23.65% CAGR through 2031.

- By component, hardware accounted for 70.85% of the gesture recognition market size in 2025, while software is set to record the fastest 23.1% CAGR to 2031.

- By end-user industry, consumer electronics commanded 42.05% of gesture recognition market share in 2025, whereas healthcare is the fastest-growing segment at 24.05% CAGR to 2031.

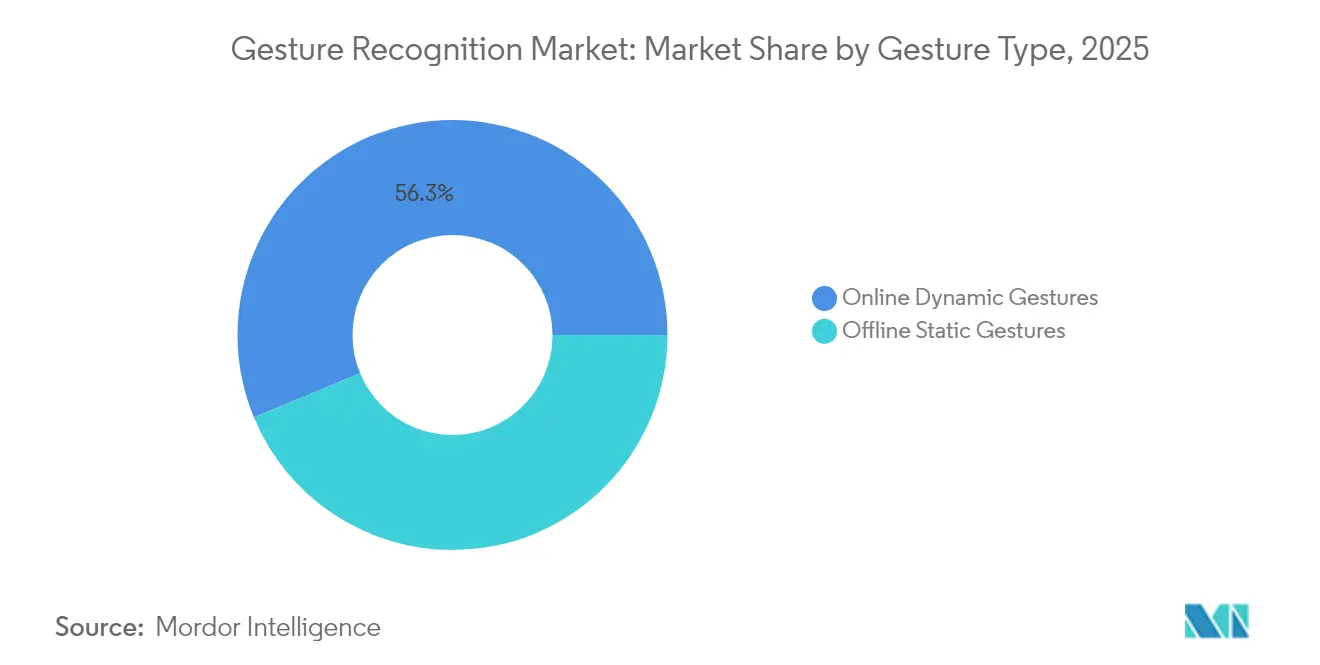

- By gesture type, dynamic gestures commanded 56.25% of gesture recognition market share in 2025, whereas it is the fastest-growing segment at 22.9% CAGR to 2031.

- By authentication, non-biometric (motion/pose) accounted for 80.35% of the gesture recognition market size in 2025, while biometric is set to record the fastest 23.55% CAGR to 2031.

- By geography, Asia Pacific held 38.05% of gesture recognition market share in 2025 and is forecast to advance at a 23.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gesture Recognition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of mm-wave and ToF sensors in flagship smartphones across Asia | +4.2% | Asia Pacific core, spill-over to global markets | Medium term (2-4 years) |

| Automaker adoption of in-cabin gesture HUDs to meet Euro NCAP distraction mandates | +3.8% | Europe primary, North America secondary | Short term (≤ 2 years) |

| Hospital demand for touch-free HMI to cut HAI risks in surgical suites | +3.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Integration into XR wearables to unlock 6-DoF control for industrial training | +2.9% | Global, with early gains in Japan, Germany, US | Long term (≥ 4 years) |

| Smart-TV vendors bundling air-gesture remotes to differentiate in price-eroding market | +2.1% | Global consumer markets | Short term (≤ 2 years) |

| Government smart-city grants driving public-kiosk gesture UI roll-outs | +1.8% | GCC primary, expanding to emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of mm-wave and ToF sensors in flagship smartphones across Asia

Asia-based handset OEMs now embed multizone ToF modules such as STMicroelectronics’ VL53L7CX to deliver millimeter-level depth accuracy without ambient-light restrictions, enabling reliable mid-air command input even under harsh illumination. The deployment extends to smart-TV handsets through Ceva’s MotionEngine Hex firmware, which integrates inertial and radar data to deliver spatial control of user interfaces.[2]“Ceva Launches MotionEngine Hex,” eejournal.com As the cost of ToF chipsets falls below USD 1 per unit in volume lots, gesture control is transitioning from a premium differentiator to a default feature in the gesture recognition market.

Automaker adoption of in-cabin gesture HUDs to meet Euro NCAP mandates

The July 2024 Advanced Driver Distraction Warning regulation obliges OEMs to mitigate cognitive load, propelling rapid integration of camera-based gesture hubs in European models.[3]“EU Regulation on Advanced Driver Distraction Warning Systems,” interregs.com BMW’s Level 2/3 certification on the 7 Series demonstrates commercial readiness, while Audi’s 3-D cockpit interface showcases multi-modal infotainment selection using above-console hand sweeps. Suppliers that can guarantee sub-150 ms response times and <3% false-trigger rates stand to win program awards, reinforcing the growth trajectory of the gesture recognition market.

Hospital demand for touch-free HMI to cut HAI risks in surgical suites

Clinical studies show 93% accuracy for mid-air MRI image manipulation, with contextual filtering reducing false positives to 2.3% in sterile environments. Neonode’s holographic displays eliminate high-touch surfaces in intensive-care units, addressing infection-control regulations and justifying higher ASPs.[4]“Holographic Displays,” neonode.com These hospital deployments create a premium sub-segment that values accuracy and regulatory compliance over bill-of-materials cost, expanding profit pools within the gesture recognition market.

Integration into XR wearables to unlock 6-DoF control for industrial training

Hitachi’s metaverse training platform allows journeyman technicians to shadow master operators in virtual settings, capturing tacit knowledge while using gesture sensing for machine interaction. Ultraleap and Prophesee combine event-based vision with low-power optics to sustain all-day AR sessions, reducing battery drain that previously limited adoption. These innovations position gesture recognition as the natural interface for immersive enterprise productivity, adding a long-tail growth vector to the gesture recognition market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High false-positive rates in sunlight for vision-based systems in tropical regions | -2.8% | APAC tropical regions, Middle East, parts of Africa | Short term (≤ 2 years) |

| Absence of open interoperability standards inflating OEM integration cost | -2.1% | Global, particularly affecting smaller OEMs | Medium term (2-4 years) |

| 'Always-on' gesture wake-word draining battery in sub-10 nm mobile SoCs | -1.9% | Global mobile device markets | Short term (≤ 2 years) |

| Data-privacy compliance hurdles for in-cabin video analytics under GDPR | -1.5% | Europe primary, with spillover to privacy-conscious markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High false-positive rates in sunlight for vision-based systems in tropical regions

Camera-centric algorithms struggle to resolve hand contours against high-lux backgrounds, driving error spikes in outdoor kiosks and ride-hailing vehicles. Research indicates radar-based alternatives maintain >90% precision independent of illumination, prompting system designers to adopt multi-sensor fusion in the gesture recognition market.

Absence of open interoperability standards inflating OEM integration cost

Fragmented SDKs force smaller manufacturers to invest in custom middleware, lengthening design cycles by up to six months. Synaptics’ open-source Astra platform seeks to harmonize APIs around its AI-native chipsets, but an industry-wide standard remains elusive, curbing the addressable volume available to entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Touchless systems drive premium applications

Touchless solutions generated 57.65% of 2025 revenue, reflecting end-market emphasis on hygiene, driver safety, and immersive entertainment. The touchless sub-segment will compound at 23.65% through 2031, outpacing the broader gesture recognition market as ToF, mm-wave radar, and ultrasonic arrays reduce bill-of-materials cost. In contrast, capacitive touch-based controls retain relevance in cost-sensitive consumer devices, yet their CAGR trails at single-digits. Kyocera’s depth sensor demonstrates 100 µm resolution within 10 cm, enabling robotic pick-and-place and orthopedic alignment tools that demand surgical-grade accuracy. The steady migration toward ambient interaction implies touchless modalities will ultimately hold a greater gesture recognition market share than their contact-dependent predecessors.

Touchless expansion is altering supplier power dynamics. Sensor vendors that historically commoditized silicon are now bundling AI firmware, data models, and developer portals, capturing recurring license fees on top of hardware margins. This re-bundling aligns with OEM priorities for field-upgradable over-the-air performance improvements and supports the scalable economics required for high-volume touchless adoption within the gesture recognition market.

By Component: Hardware dominance faces software disruption

Hardware contributed 70.85% of gesture recognition market size in 2025, driven by the intrinsic cost of lenses, radar front-ends, and MCUs. However, software platforms that deliver contextual awareness, user adaptation, and federated learning are forecast at a 23.1% CAGR—more than 350 bps above hardware growth. Infineon’s DEEPCRAFT Ready Models supply pre-trained neural networks for common gestures, cutting integration time by 40% and repositioning the firm higher on the value curve. Meanwhile, Imagimob’s visual graph-based ML tooling compresses model-development cycles to hours, democratizing AI optimization for mid-tier OEMs.

The revenue mix shift creates opportunities for service bundling: predictive maintenance, cloud-based analytics, and in-app monetization through gesture-initiated digital purchases. Suppliers able to orchestrate silicon, firmware, and lifecycle services are poised to command loyalty in the gesture recognition market as total cost of ownership eclipses component price considerations.

By End-user Industry: Healthcare disrupts consumer electronics leadership

Consumer electronics retained a 42.05% share in 2025, benefitting from smartphone replacement cycles and smart-TV attach rates that embed mid-air navigation as table-stakes functionality. Even so, surgical theaters, radiology labs, and cleanroom diagnostics will post a 24.05% CAGR, reflecting infection-prevention protocols and reimbursement incentives that justify higher system ASPs. Automotive adoption is accelerating, fueled by driver distraction mandates and Level 2+ autonomy roadmaps requiring intuitive fallback controls. Industrial cobots and hazardous-material robotics add incremental demand where glove-friendly interfaces are mandatory.

In healthcare, ROI materializes through shorter procedure times, lower surgical-site infection rates, and reduced consumable spend on sterile drapes. These quantifiable benefits underpin premium pricing and elevate medical OEM influence over component roadmaps, further diversifying revenue streams across the gesture recognition industry.

By Gesture Type: Dynamic gestures enable complex interactions

Dynamic gestures held a 56.25% revenue share in 2025 and will continue compounding at 22.9% as temporal recognition models mature. Researchers report 95.1% precision in ultra-long-distance detection up to 28 m by combining radar and vision data. Static pose recognition remains relevant for binary start-stop machine controls, yet user preference trends toward motion-rich commands that mirror natural language.

Attention-enhanced LSTM networks push real-time inference below 10 ms, supporting immersive gaming and remote-surgery use cases that demand latency-free feedback. Over time, dynamic modalities are expected to command an even larger slice of the gesture recognition market share as model compression aligns with edge-compute budgets.

By Authentication: Biometric security gains momentum

Non-biometric motion patterns represented 80.35% of 2025 implementations, thanks to lone-user consumer electronics scenarios that value convenience. Yet biometric gesture authentication combining finger-vein, iris, or impedance signatures with motion vectors is advancing at 23.55% CAGR.

Infineon’s SECORA Pay Bio cards fuse fingerprint and gesture confirmation to authorize contactless payments, closing the security gap without degrading user experience. Wearable patents that map muscular impedance hint at continuous authentication, ensuring only the registered user can execute privileged gestures during prolonged sessions. Such developments are elevating the security profile of the gesture recognition market, widening its addressable scope to regulated industries.

Geography Analysis

Asia Pacific’s dominance rests on vertically integrated supply chains, supportive government funding, and an immense installed base of early-adopter consumers. Regional handset brands release new flagship lines every 10–12 months, each iteration embedding higher-resolution ToF arrays, thereby expanding the gesture recognition market size for sensor vendors. Japanese conglomerates employ XR-based skill-transfer platforms in automotive welding and semiconductor lithography, reinforcing demand for high-precision gesture models. South Korea’s wafer capacity secures component continuity, while India’s smart-TV expansion introduces touchless remotes into middle-income households, broadening the revenue pyramid.

North America leverages healthcare spending power for surgical suites and diagnostic centers, generating premium revenue per unit. Hospitals adopting mid-air displays report significant reductions in cross-contamination incidents, translating into lower readmission penalties and bolstering ROI for gesture interfaces. Automotive OEMs integrate gesture-based driver monitoring to comply with post-2024 federal guidelines on distracted driving, pushing incremental sensor attach rates.

Europe acts as a regulatory pacesetter. Euro NCAP directives mandate distraction-mitigation technologies, accelerating deployment across both luxury and mass-market vehicle classes. German suppliers co-develop gesture modules with domestic automakers, cementing regional value capture despite globalized hardware sourcing. Meanwhile, GCC nations pursue AI sovereignty initiatives that fund public-service kiosks with touchless UIs, giving the Middle East an outsized growth profile relative to its current base.

Regulatory Landscape

Regulation increasingly hinges on how gesture recognition is implemented, particularly when paired with video analytics or biometric identification. In the European Union, Regulation (EU) 2024/1689 (AI Act) frames compliance requirements for AI systems in higher-risk contexts, while distinguishing readily apparent gesture or movement detection from emotion recognition unless the system is used to infer emotions.

For deployments that involve cameras in public or workplace settings, GDPR obligations and guidance such as the European Data Protection Board (EDPB) Guidelines 3/2019 on video devices reinforce privacy-by-design expectations (including data minimization and governance controls) that impact in-cabin monitoring, kiosks, and surveillance-adjacent gesture interfaces. Standards shaping assurance and procurement criteria across end users include ISO/IEC 30137-1:2024 addresses governance, privacy, and societal considerations for biometric video surveillance deployments, and ISO/IEC 19792:2025 updates requirements for security evaluation of biometric systems (including presentation attack considerations), both relevant when gesture is used as part of biometric or multi-factor access workflows. China also maintains specific technical requirements for gesture interaction systems (GB/T 38665.1-2020), adding a regional compliance layer for OEMs shipping gesture-enabled consumer devices and public-facing terminals into the country.

Competitive Landscape

The gesture recognition market remains moderately fragmented. Semiconductor majors Intel, Qualcomm, Infineon bundle CPU, GPU, and RF blocks that accelerate sensor fusion, leveraging scale advantages to defend gross margins. Specialist firms such as Ultraleap differentiate through high-fidelity hand tracking and mid-air haptics, targeting premium automotive and XR segments. Synaptics positions at the confluence of silicon and software, offering Astra AI-Native development stacks that shorten OEM integration timelines.

Strategically, consolidation centers on capability acquisition. Infineon’s new SURF division combines radar and sensor assets to expand automotive design-in depth, signaling a portfolio-management approach that aligns adjacent technologies under a common go-to-market. PreAct Technologies’ 2024 purchase of Gestoos AI added proprietary gesture datasets, enhancing model generalization across in-cabin and industrial robotics use cases. Competitive advantage now derives from vertically integrated reference designs, cloud-based model updates, and compliance toolkits that de-risk OEM audits.

White-space opportunities persist in hazardous-material handling, elder-care robotics, and accessibility tech for differently abled users. Entrants that can supply domain-specific training data and verification protocols stand to capture niche share pockets even as industry leaders lock down mainstream mobile and automotive sockets. Within this landscape, the gesture recognition market rewards firms that marry silicon roadmaps with AI model pipelines and certified reference flows.

Gesture Recognition Industry Leaders

Intel Corporation

Qualcomm Technologies Inc.

Apple Inc.

Microsoft Corp.

Sony Group Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity exists in security and surveillance-adjacent deployments that convert gesture understanding into real-time response, especially where phone calls are impractical or unsafe. Recent research prototypes demonstrate CCTV-linked hand-gesture risk assessment and alerting workflows that integrate common real-time vision stacks (e.g., OpenPose/MediaPipe-style pose pipelines) and notification APIs for geolocation-based messaging to responders, pointing to productizable patterns for schools, campuses, retail, and industrial sites that already operate camera networks. This pulls gesture recognition deeper into incident response platforms, not only as an HMI layer but also as an event trigger for alarms, access control actions, and guided evacuation messaging.

A second whitespace area is compliance-ready, on-device gesture inference for privacy-constrained environments, including vehicles in Europe (GDPR constraints on in-cabin video analytics are a cited hurdle) and healthcare sterile rooms that prioritize touch-free HMI. Market activity is also moving toward developer-ready toolchains and edge deployment: examples in the current landscape include Synaptics promoting Astra as an open-source pathway to harmonize APIs, and embedded model offerings such as Infineon DEEPCRAFT Ready Models that cut integration time for common gestures. These shifts support an ecosystem opportunity for interoperable SDKs, test harnesses, and verification workflows that reduce OEM integration friction while improving robustness in difficult conditions such as high-illumination outdoor scenes where vision-only systems can suffer false positives.

Recent Industry Developments

- March 2026: Oura acquired Doublepoint, adding gesture recognition and neural-input interaction know-how to its smart ring ecosystem. The deal signals consolidation around intent-based control in wearables, as established health-tracking platforms broaden into interaction and command workflows.

- April 2026: Synaptics promoted Astra as an open-source pathway to harmonize APIs, driving interoperable gesture SDKs and developer tooling across platforms and accelerating integration with gesture-enabled devices.

- November 2024: Infineon introduced the DEEPCRAFT edge-AI brand with pre-trained models aimed at accelerating embedded deployment of common AI tasks, including gesture-related inference. The release supports faster OEM integration and reinforces the shift toward packaged edge-AI software assets alongside sensor and MCU hardware.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the gesture recognition market covers revenue from hardware and software that detects, interprets, and responds to human gestures, including touch-based and touchless interaction across consumer, automotive, healthcare, industrial, and adjacent applications.

Scope exclusions: We exclude broader voice recognition-only interfaces and general camera modules that are not used for gesture interpretation.

Segmentation Overview

- By Technology

- Touch-based Gesture Recognition

- 2-D Multi-touch Panels

- Capacitive and Resistive Sensors

- Touchless Gesture Recognition

- 2-D Camera-based

- 3-D Depth and ToF

- Ultrasonic and mm-wave Radar

- Touch-based Gesture Recognition

- By Component

- Hardware (Sensors, Controllers, SoCs)

- Software (ML Algorithms, SDKs, Middleware)

- By Gesture Type

- Online Dynamic Gestures

- Offline Static Gestures

- By Authentication

- Biometric (Face, Iris, Palm-vein)

- Non-biometric (Motion, Pose)

- By End-user Industry

- Consumer Electronics

- Smartphones and Tablets

- Smart-TV and Set-top Boxes

- AR/VR and Wearables

- Automotive

- Driver Monitoring and Infotainment

- Aerospace and Defense

- Healthcare

- Surgical and Diagnostic Rooms

- Gaming and Entertainment

- Industrial and Robotics

- Other Industries

- Consumer Electronics

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- New Zealand and Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC (Saudi Arabia, UAE, Qatar)

- Turkey

- South Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work began by mapping the value chain and a typical bill-of-material split for gesture-enabled systems, so the model separates recognition software value from sensor and module value where the public record allows it. We leaned on public sources such as the US International Trade Commission and Federal Communications Commission equipment filings where relevant, ISO and IEC standards notes for sensing and safety, and research papers indexed through IEEE and NIST.

To ground demand signals, we also reviewed company annual reports and investor decks, product launch notes, reputable press coverage, and association websites tied to electronics, automotive safety, and medical devices. For pricing and supply-side checks, paid subscriptions were used only where appropriate for company financials and for patent databases to understand where commercialization was actually occurring. The desk sources listed here are not exhaustive, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews focused on validating what is monetized as gesture recognition versus adjacent sensing and UI features, since that boundary can change market totals quickly. We spoke with component suppliers, software providers, system integrators, and OEM-side teams across APAC, EMEA, and the Americas to confirm adoption timing, typical bundling, and price erosion patterns.

These discussions were also used to cross-check desk research assumptions, especially around attach rates in devices and vehicles, the split between touch-based and touchless deployments, and what drives software value over time.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 42% |

| Mid tier: 48% | Functional/Unit leaders: 32% | EMEA: 31% |

| Smaller Players: 20% | Managers: 56% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, reconstructing shipment and adoption signals first, then converting them into value using realistic pricing ladders. The top-down view used penetration-based demand pool assessment across major end-use areas (for example, gesture-enabled device shipments, in-vehicle system fitment, and healthcare and industrial interface rollouts), followed by mapping what portion of that stack is attributable to gesture recognition.

To keep the model practical, we used a small set of repeatable inputs such as sensor shipment trends (including ToF and radar where relevant), attach rates by device type, average selling price (ASP) ranges for hardware versus software value, regional mix shifts, and the pace of touchless adoption in safety and hygiene-led use cases. Results were corroborated with selective bottom-up checks, including sampled supplier revenue roll-ups, channel checks on typical module pricing, and sanity checks using ASP multiplied by implied volumes when disclosed.

For forecasting, scenario analysis was used because adoption varies by end market and design cycle timing. Scenarios were constrained by expert consensus on drivers like automotive feature uptake, consumer electronics refresh cycles, and typical price erosion, then reconciled back to the central case so the final path stays realistic.

Data Validation & Update Cycle

Outputs were stress-tested through triangulation across multiple indicators, followed by variance checks by region and end use to spot step changes that do not match the adoption story. When large gaps showed up, we rechecked unit assumptions, ASP ladders, and currency conversions before sign-off, and we re-contacted select experts when a discrepancy could not be explained by public signals.

The report is refreshed annually, and interim updates are made when material events occur, such as sharp sensor price movements, major platform launches, or regulatory shifts that change adoption pace. Before delivery, a final analyst pass is completed so clients receive the most up-to-date view consistent with the model logic and the latest validation.

Mordor Intelligence's Gesture Recognition Market Sizing Compared With Other Published Estimates

Published market numbers for gesture recognition often differ because the category boundary is easy to stretch, and because pricing assumptions move quickly as sensors and embedded software mature. Differences also come from whether the estimate treats gesture as a stand-alone revenue line, or as an add-on within larger HMI, sensing, or consumer device totals.

In practice, the biggest gap drivers are refresh cadence, currency timing for global revenues, and how ASP erosion is applied across touch-based versus touchless stacks. By refreshing ASP ladders in line with product cycle timing and rechecking conversions using consistent year-average rates, Mordor Intelligence keeps the estimate aligned to what is actually monetized as gesture recognition in the current base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 37.41 B (2026) | |

| Global Research Publisher A | USD 31.05 B (2025) | Uses a different base year and a longer forecast window, and the earlier-year value can be sensitive to how fast software versus hardware ASPs are assumed to decline. |

| Industry Research Publisher B | USD 25.44 B (2024) | Anchors estimates to an earlier historical base and may apply broader category grouping, which can undercount newer touchless deployments that scale after the base year. |

The spread across sources mainly reflects timing and scope handling rather than a single right or wrong answer. When the base year is aligned and the pricing logic is made consistent with device and vehicle refresh cycles, the totals tend to converge into a narrower band that is easier to track and explain over time.

Key Questions Answered in the Report

What is the current size of the gesture recognition market?

The gesture recognition market reached USD 37.41 billion in 2026 and is projected to grow to USD 104.16 billion by 2031.

Which region leads the gesture recognition market?

Asia Pacific holds the largest 38.05% share and is forecast to post the fastest 23.45% CAGR through 2031.

Why are touchless technologies expanding rapidly?

Hospitals, automakers, and consumer-electronics brands value hygienic and distraction-free interfaces, driving a 23.65% CAGR for touchless solutions.

How is software changing competitive dynamics?

AI-centric software platforms are growing faster than hardware, enabling continuous model updates and personalized experiences that raise switching costs.

What industries offer the highest growth opportunity?

Healthcare tops the expansion chart with a 24.05% CAGR to 2031 as surgical and diagnostic centers adopt sterile, mid-air controls.

How fragmented is the supplier landscape?

The top 10 players hold under 30% combined revenue, indicating ample space for new entrants with differentiated sensor or AI capabilities.

Page last updated on: