Smart Diaper Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

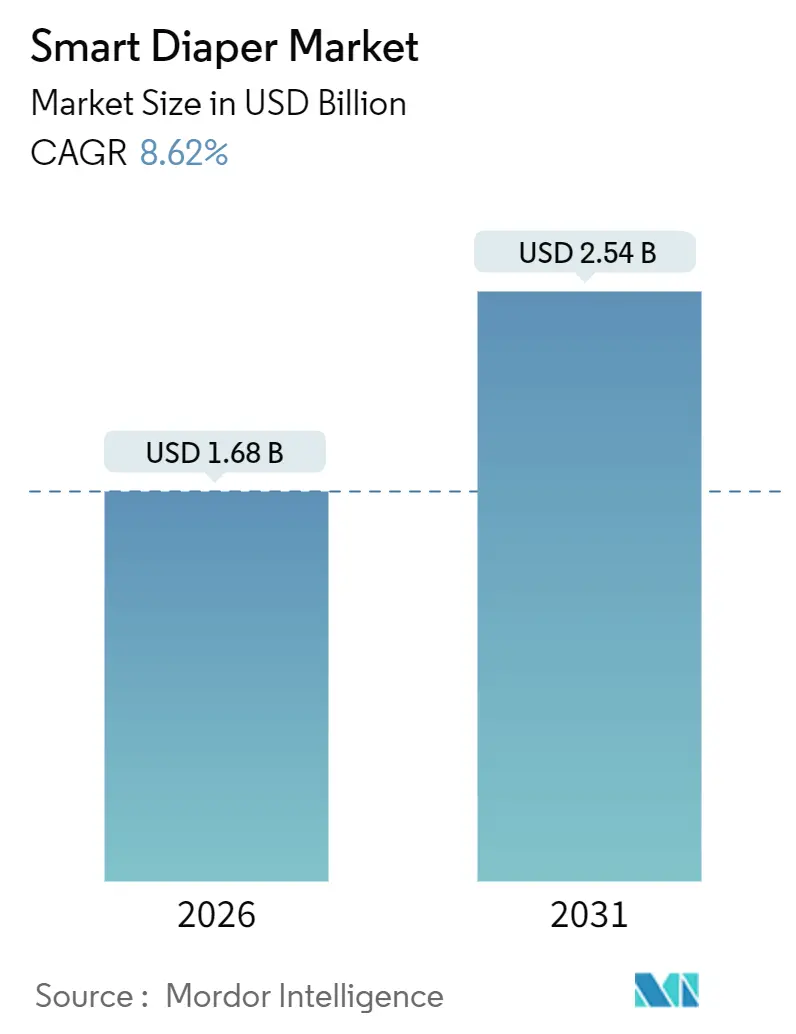

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Diaper Market Analysis by Mordor Intelligence

The Smart Diaper Market size is estimated at USD 1.68 billion in 2026, and is expected to reach USD 2.54 billion by 2031, at a CAGR of 8.62% during the forecast period (2026-2031).

Continued reimbursement expansion, sensor-cost deflation, and institutional labor shortages are prompting facilities to replace manual checks with predictive, connected briefs that lower nursing workload and pressure ulcer incidence. Japan’s fiscal-2025 subsidies for sensor-equipped continence products and the 2024 Centers for Medicare and Medicaid Services decision to reimburse continuous wetness monitoring have removed two of the largest adoption barriers. Vendors are therefore shifting from hardware-only sales to subscription bundles that combine diapers, analytics dashboards, and replenishment logistics, a move that secures recurring revenue and strengthens buyer lock-in. At the same time, long-term-care insurers in North America and Europe are piloting bundled-payment models that reward facilities for reductions in skin-integrity events, driving incremental demand for clinical-grade accuracy. On the supply side, polymer-sensor breakthroughs have cut inline integration costs by 30%, allowing incumbents to embed Bluetooth modules without re-tooling high-speed diaper lines.

Key Report Takeaways

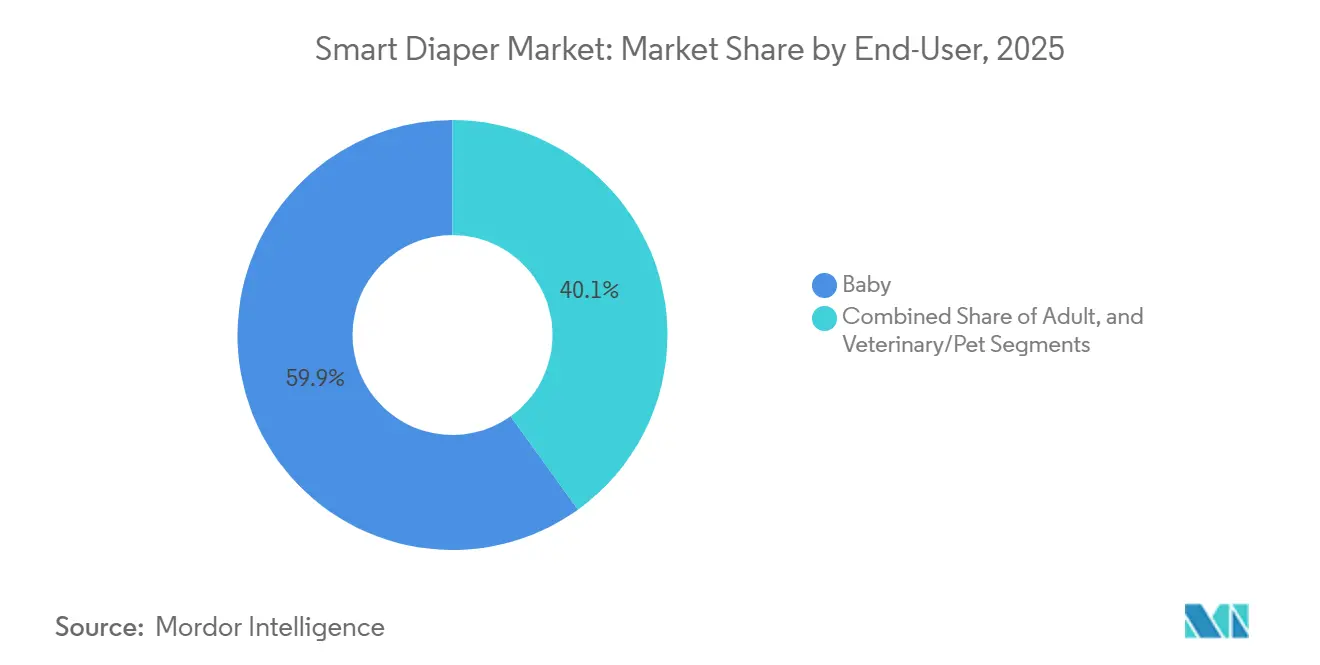

- By end-user, baby products led with 59.91% of smart diaper market share in 2025, while adult applications are forecast to advance at a 9.34% CAGR through 2031.

- By product type, disposable formats captured 74.22% of the smart diaper market size in 2025; reusable sensor patches are poised to grow at a 10.57% CAGR between 2026 and 2031.

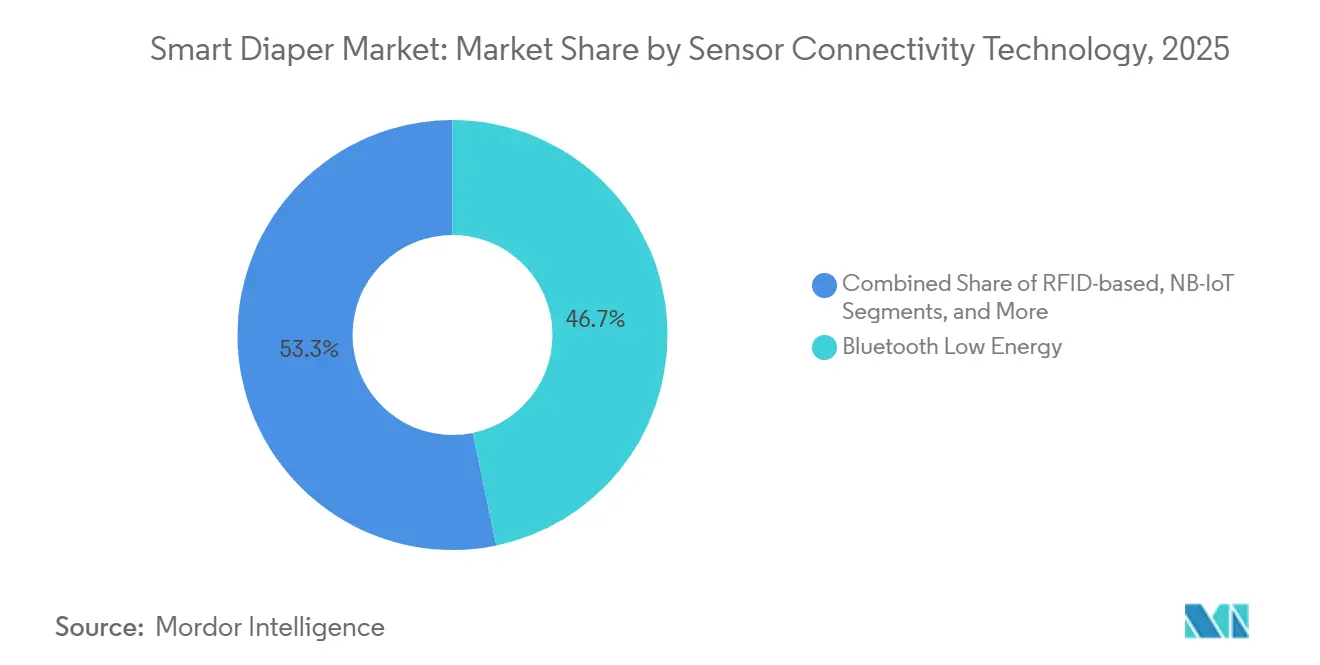

- By sensor connectivity, Bluetooth Low Energy commanded 46.74% revenue share in 2025, whereas NB-IoT and LTE-M are projected to register a 9.02% CAGR to 2031.

- By distribution channel, institutional purchasing represented 51.64% of the smart diaper market in 2025, whereas e-commerce platforms are expanding at a 10.88% CAGR over the forecast horizon.

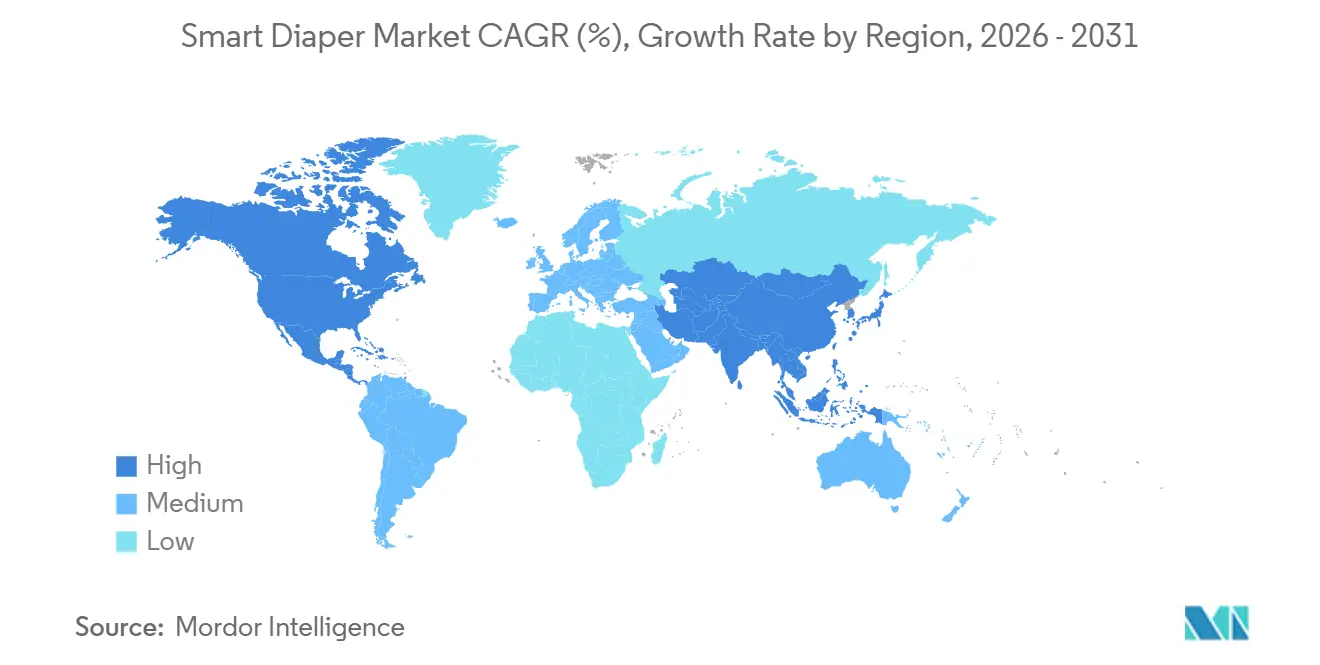

- By geography, North America accounted for a 35.83% smart diaper market share in 2025, but Asia-Pacific is anticipated to record the fastest 11.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Diaper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large geriatric population in developed countries | +2.1% | North America, Europe, Japan | Long term (≥ 4 years) |

| Rising birth rates and higher disposable income in emerging markets | +1.3% | Asia-Pacific (India, ASEAN), South America | Medium term (2-4 years) |

| Digital-health push by long-term-care insurers | +1.8% | North America, Europe | Short term (≤ 2 years) |

| IoT-enabled elderly-home platforms seeking integrated continence sensors | +1.6% | Global, with concentration in Japan, North America | Medium term (2-4 years) |

| AI-driven predictive analytics for urinary incontinence events | +1.2% | North America, Europe, Japan | Medium term (2-4 years) |

| Post-pandemic tele-nursing adoption accelerating smart diaper usage | +1.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Large Geriatric Population in Developed Countries

Population aging is shifting diaper demand from infants to seniors. Japan surpassed a 30% share of the 65-plus market in 2024, and adult briefs now outsell baby equivalents domestically.[1]Ministry of Health, Labour and Welfare, “Long-Term Care Insurance System,” mhlw.go.jp The United States expects more than 80 million seniors by 2040, magnifying labor pressure inside skilled-nursing facilities where turnover already exceeds 60%. Smart diapers reduce manual checks, cutting 15–20 minutes of staff time per resident each shift. National subsidy programs such as Japan’s Care Robot Support Office reimburse as much as 50% of device expenditure, further accelerating the smart diaper market.

Digital-Health Push by Long-Term-Care Insurers

CMS expanded Remote Patient Monitoring codes in 2024 to include continuous moisture sensing, opening a USD 50–100 monthly reimbursement stream for nursing-home operators. German and U.S. insurers have since piloted value-based contracts that bundle ulcer prevention, incentivizing facilities to deploy connected briefs. Early trials indicate a 40% decline in stage-1–2 pressure ulcers after implementing predictive change protocols. These financial incentives are reshaping capital budgets, allowing administrators to justify the premium smart diaper market price relative to conventional products.

IoT-Enabled Elderly-Home Platforms Seeking Integrated Continence Sensors

Long-term-care operators increasingly consolidate fall detection, bed-exit monitoring, and continence data on unified dashboards. Bluetooth Low Energy devices cover residential ranges, but campus-wide deployments favor NB-IoT, which offers direct-to-cloud transmission and 10-year battery life on AA cells.[2]STMicroelectronics, “NB-IoT and LTE-M Modules for Healthcare IoT,” st.com Essity’s TENA SmartCare integrates with electronic health records, automating supply orders and compliance reporting. Interoperability advantages therefore steer procurement toward manufacturers that publish standardized APIs, raising the competitive stakes in the smart diaper market.

AI-Driven Predictive Analytics for Urinary Incontinence Events

Algorithms that learn individual void patterns now forecast events 30-60 minutes ahead, enabling scheduled toileting and reducing resident discomfort. Verily Life Sciences filed multiple 2024 patents that separate urine from feces using impedance spectroscopy, bringing diagnostic potential to the smart diapers industry. A 2024 Korean nursing-home study showed 97.1% concordance between sensor alerts and physical checks, validating clinical reliability. Predictive accuracy grants access to higher reimbursement classes and differentiates premium platforms.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit cost versus conventional diapers | -1.9% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Infection and dermatitis risk from prolonged wear | -0.8% | Global | Medium term (2-4 years) |

| Data-privacy and cybersecurity concerns in connected devices | -0.7% | North America, Europe (GDPR jurisdictions) | Short term (≤ 2 years) |

| Short battery and adhesive sensor life limiting reuse cycles | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Unit Cost Versus Conventional Diapers

Sensor-equipped briefs cost USD 1-3 each, three to five times more than basic disposables, and reusable patches run USD 50-150. While institutions can amortize these expenses over labor savings, out-of-pocket payers in emerging economies view the premium as prohibitive. Subscription bundles that spread hardware charges across monthly deliveries have entered the smart diaper market, but uptake remains limited.

Infection and Dermatitis Risk From Prolonged Wear

Dermatitis affects up to half of nursing home residents, and delayed treatment may worsen skin integrity. Although sensors prompt timely replacement, staff may defer action until they are alerted, prolonging moisture exposure. The Wound, Ostomy and Continence Nurses Society recommends two-hour intervals independent of saturation, a guideline that partially offsets the labor-saving promise of the smart diapers industry.[3]Wound, Ostomy and Continence Nurses Society, “Clinical Practice Guidelines for Incontinence-Associated Dermatitis,” wocn.org Adhesive placement also introduces new allergen concerns, prompting stringent ISO and CE biocompatibility testing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Adult Care Surges Despite Baby Leadership

The baby category controlled 59.91% of the smart diaper market in 2025, buoyed by real-time sleep analytics embraced by affluent parents. Neonatal intensive-care units adopted preemie versions to track hydration, extending clinical credibility. Meanwhile, the adult segment is projected to register a 9.34% CAGR, the highest among all groups, as skilled-nursing operators combat projected caregiver shortages and rising ulcer-related litigation. The smart diaper market size for geriatric applications is therefore on a steeper expansion path than its pediatric counterpart.

Adult adoption is strongest in Japan, where adult briefs surpassed infant volume in 2024. Facilities there pair sensor alerts with staffing algorithms, freeing nurses for higher-acuity tasks. In the United States, CMS reimbursement is spurring trial programs across multistate chains. Special-needs adults and a nascent pet-care niche add incremental volume, hinting at diversification possibilities for the smart diapers industry.

By Product Type: Disposables Dominate but Reusables Gain Ground

Disposable formats held 74.22% of the smart diaper market share in 2025 as brands embedded low-cost printed circuitry directly into high-speed lines. Sensor integration costs fell after Toray’s 2024 polymer breakthrough, preserving incumbents’ scale advantages. Convenience and simple waste handling sustain household demand despite higher per-use cost.

Reusable patches, however, are expanding at a 10.57% CAGR. A USD 200 starter kit that survives 50 wash cycles lowers lifetime costs to USD 4 per use, undercutting disposables in high-volume institutional settings. Sustainability mandates in Europe elevate the appeal of reusables, aligning with circular-economy targets and reshaping procurement criteria in the smart diaper market.

By Sensor Connectivity Technology: Bluetooth Leads, Cellular IoT Accelerates

Bluetooth Low Energy accounted for 46.74% of 2025 revenue, thanks to its sub-USD 5 module cost and compatibility with caregiver smartphones. Retail-oriented offerings like Huggies Special Delivery exploit this ubiquitous connectivity, enriching the smart diaper market with app-based sleep dashboards.

Campus-scale deployments prefer NB-IoT and LTE-M, which are poised for a 9.02% CAGR. New modules support 10-year battery life and under USD 10 bill-of-materials pricing, enabling direct cloud uploads without gateways. RFID has receded to inventory tracking, while Wi-Fi and ultra-wideband remain niche.

By Distribution Channel: Institutional Contracts Lead as E-Commerce Climbs

Institutional buyers commanded 51.64% of 2025 sales, bundling connected diapers with facility-wide hygiene and analytics services. Multi-year contracts that fold in software support and staff training give established manufacturers a stronghold in the smart diaper market.

E-commerce is rising at a 10.88% CAGR as aging-in-place seniors value discreet home delivery and subscription replenishment. Amazon listings for reusable patches grew double digits in 2024, revealing latent consumer appetite. Brick-and-mortar pharmacies still satisfy urgent needs but lose ground to online variety and pricing transparency.

Geography Analysis

North America accounted for the largest regional share, at 35.83% of the smart diaper market in 2025. CMS reimbursement, high caregiver wages, and a 25 million adult-incontinence population underpin demand. Pilot studies showing 40% ulcer-reduction cement administrative confidence, and multistate operators are standardizing connected briefs across portfolios. Canada progresses cautiously under budget constraints, while Mexico’s uptake remains confined to private urban facilities.

Asia-Pacific is the fastest-growing territory with an 11.07% CAGR forecast through 2031. Japan’s demographic inversion and 50% government subsidy catalyze institutional rollouts. China’s CNY 73,000 crore (USD 10 billion) elderly-care allocation finances pilot deployments in Tier-1 cities, even as broad market penetration lags due to price sensitivity. India’s looming 230 million elder cohort offers strategic upside, but family-centric caregiving and limited insurance coverage curb near-term volumes. South Korea and select ASEAN nations show niche growth tied to middle-class expansion.

Europe, at 20% of the 2025 value, benefits from CE-certified products and long-term-care insurance schemes that reimburse assistive devices. Scandinavian facilities pioneered Essity’s integrated SmartCare platform, aligning with stringent GDPR data safeguards. German insurers now test outcome-based payments, while the United Kingdom’s budget pressures slow National Health Service adoption. Southern Europe and emerging Middle East and Africa markets remain nascent because of lower institutional capacity and high out-of-pocket costs.

Competitive Landscape

Global diaper incumbents - Kimberly-Clark, Procter & Gamble, Essity, and Unicharm - control supply chains and retail shelf space, allowing them to introduce sensor-enabled variants without overhauling distribution. Their collective scale amortizes the added cost of electronics at a fractional level, sustaining margins even in price-sensitive channels. Specialized entrants such as Simavita, Pixie Scientific, and Monit focus on software analytics and clinical validation, winning hospital pilots that demand granular predictive accuracy.

Partnerships are multiplying. Start-ups license firmware or data algorithms, while incumbents handle mass production and global logistics. Verily’s 2024 spectroscopy patents attracted interest from medical device majors eyeing diagnostic-grade expansion.[4]Alphabet Inc. (Verily Life Sciences), “Patent Application: Impedance Spectroscopy for Incontinence Monitoring,” patents.google.com Regulatory rigor is rising; the FDA now mandates cybersecurity bills of materials for connected devices, elevating compliance costs and raising entry barriers. As platform interoperability becomes a purchase criterion, vendors with open APIs and EHR integration strengthen their positioning in the smart diaper market.

Despite moderate concentration, white-space opportunities persist in direct-to-consumer aging-in-place segments and in hybrid institutional-home care models. Subscription logistics, remote-monitoring dashboards, and end-to-end supply automation represent differentiators beyond absorbency or sensor accuracy alone, suggesting that software sophistication will increasingly dictate competitive advantage.

Smart Diaper Industry Leaders

Abena Holding A/S

Kimberly-Clark Corporation

Essity Aktiebolag (publ)

First Quality Enterprises, Inc.

Monit Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Kimberly-Clark announced a USD 28.7 million Vietnam capacity expansion to produce sensor-equipped infant and adult briefs for ASEAN export.

- October 2025: Kimberly-Clark pledged USD 28.7 million toward Southeast-Asian maternal-and-infant programs that will pilot smart diapers in neonatal intensive-care units.

- June 2025: The U.S. FDA finalized cybersecurity guidance for connected medical devices, covering smart diapers entering clinical workflows.

- March 2025: Kimberly-Clark launched a restroom IoT suite combining dispensers, occupancy sensors, and connected continence monitors for institutional buyers.

- January 2025: Huggies released Special Delivery diapers featuring optional Bluetooth Low Energy sensors and a companion analytics app.

Global Smart Diaper Market Report Scope

Smart diapers are diapers integrated with sensors that enable effective care for babies and the elderly. Smart diapers are equipped with sensors that are connected to mobile applications that send out alerts as soon as they detect any leak.

The Smart Diaper Market Report is Segmented by End-User (Baby, Adult, Veterinary), Product Type (Disposable, Reusable and Sensor Patches), Sensor Connectivity Technology (RFID, Bluetooth Low Energy, NB-IoT/LTE-M, Others), Distribution Channel (Institutional, Retail, E-commerce), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Baby |

| Adult (Geriatric and Special-needs) |

| Veterinary / Pet |

| Disposable Smart Diapers |

| Reusable Smart Diapers and Sensor Patches |

| RFID-based |

| Bluetooth Low Energy (BLE) |

| NB-IoT / LTE-M |

| Others (Wi-Fi, Ultra-Wideband) |

| Institutional (B2B Hospitals, Nursing Homes) |

| Retail (B&M Pharmacies, Supermarkets) |

| E-commerce / Direct-to-Consumer |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By End-User | Baby | |

| Adult (Geriatric and Special-needs) | ||

| Veterinary / Pet | ||

| BY Product Type | Disposable Smart Diapers | |

| Reusable Smart Diapers and Sensor Patches | ||

| By Sensor Connectivity Technology | RFID-based | |

| Bluetooth Low Energy (BLE) | ||

| NB-IoT / LTE-M | ||

| Others (Wi-Fi, Ultra-Wideband) | ||

| By Distribution Channel | Institutional (B2B Hospitals, Nursing Homes) | |

| Retail (B&M Pharmacies, Supermarkets) | ||

| E-commerce / Direct-to-Consumer | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and growth trajectory of the smart diapers market?

The market stands at USD 1.68 billion in 2026 and is forecast to reach USD 2.54 billion by 2031, expanding at an 8.62% CAGR.

Which end-user segment offers the highest growth potential?

The adult segment (geriatric and special-needs) is growing at a 9.34% CAGR through 2031.

Why are reusable smart diapers gaining traction despite disposables' market dominance?

Reusable systems and sensor patches are expanding at a 10.57% CAGR as institutional buyers' total-cost-of-ownership analyses favor washable platforms that achieve USD 4 per-use costs after 50 cycles versus USD 1 to USD 3 per disposable unit.

Which geographic region presents the fastest growth opportunity?

Asia-Pacific is forecast to grow at an 11.07% CAGR through 2031.

What connectivity technology is displacing Bluetooth Low Energy in institutional settings?

NB-IoT and LTE-M cellular protocols are growing at a 9.02% CAGR as nursing homes deploy campus-wide networks that enable direct-to-cloud transmission.

How are reimbursement policies accelerating institutional adoption?

The Centers for Medicare and Medicaid Services' 2024 expansion of Remote Patient Monitoring billing codes permits USD 50 to USD 100 per patient per month reimbursement for continuous wetness monitoring.

Page last updated on: