Market Overview

| Study Period | 2020 - 2031 |

|---|---|

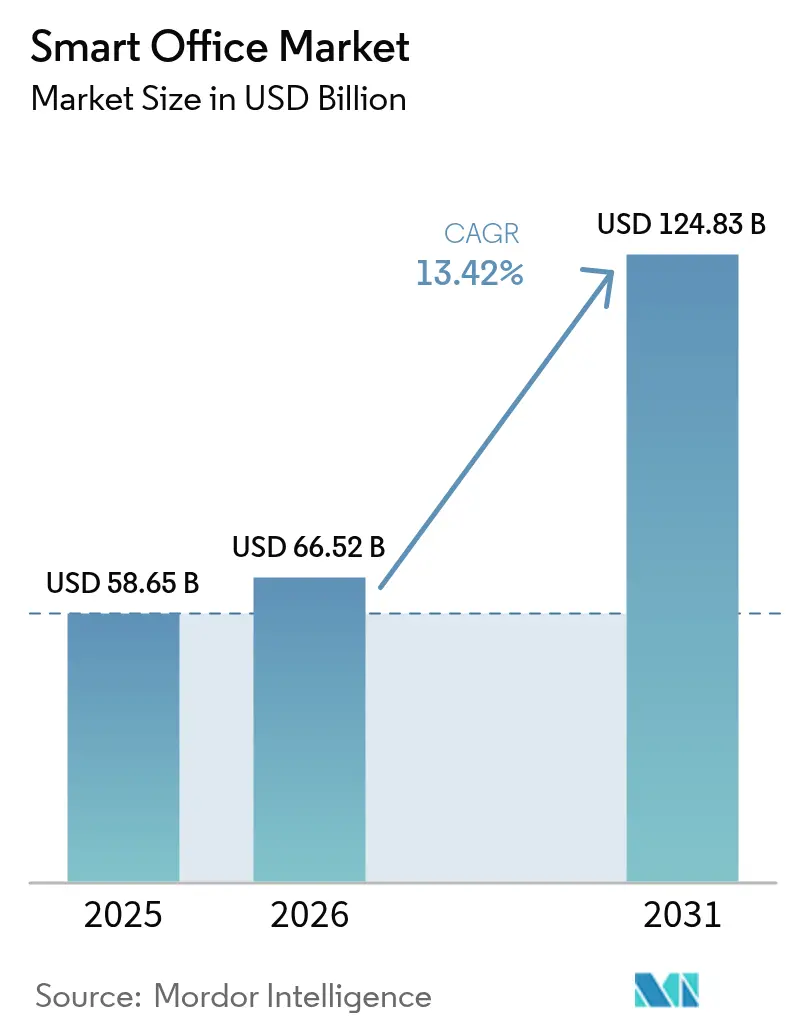

| Market Size (2026) | USD 66.52 Billion |

| Market Size (2031) | USD 124.83 Billion |

| Growth Rate (2026 - 2031) | 13.42% CAGR |

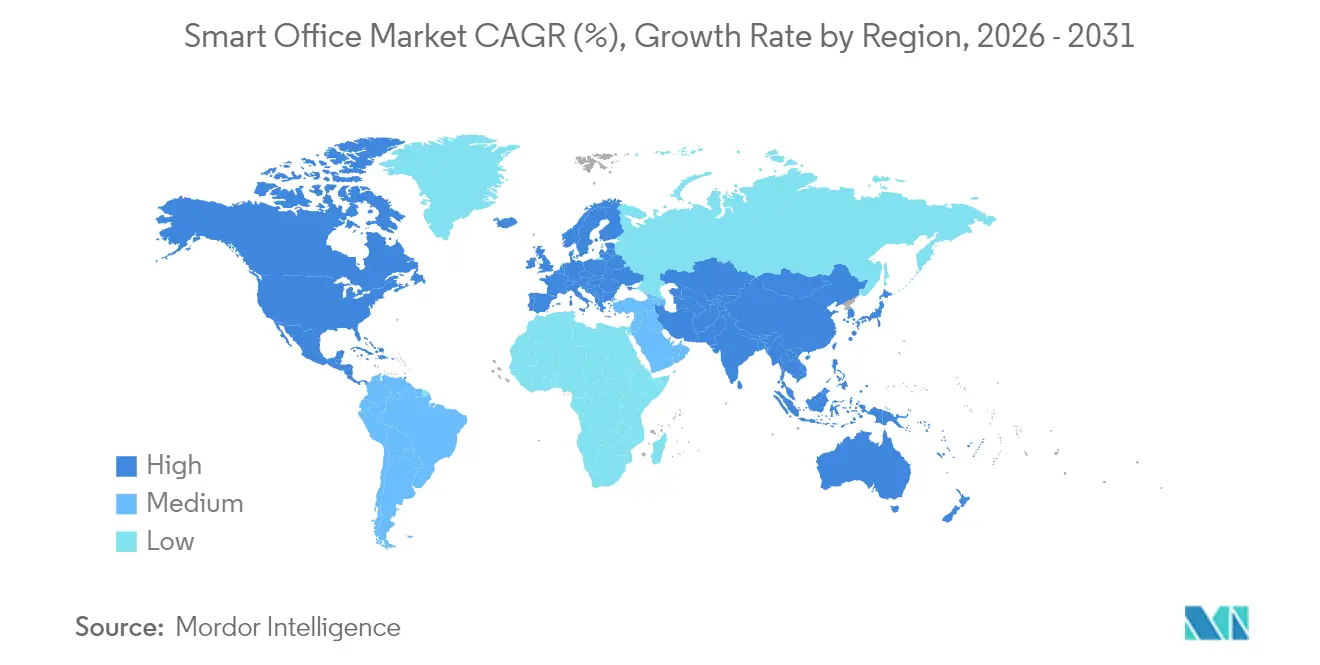

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

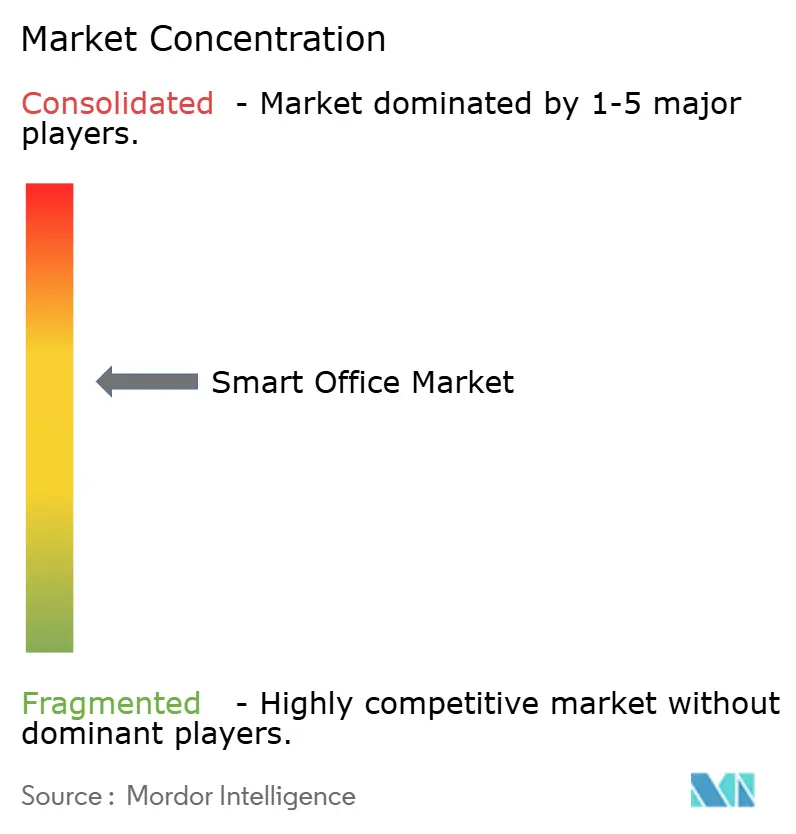

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Office Market Analysis by Mordor Intelligence

The smart office market size in 2026 is estimated at USD 66.52 billion, growing from 2025 value of USD 58.65 billion with 2031 projections showing USD 124.83 billion, growing at 13.42% CAGR over 2026-2031. Growth stems from permanent hybrid work patterns, tightening energy performance mandates, and falling IoT sensor costs, which together shift capital toward sensor networks, cloud platforms, and integration services. Corporate real-estate strategies now emphasize occupancy analytics and demand-responsive systems, redirecting budgets that once went to static fit-outs toward intelligent HVAC, lighting, and energy-management layers.[1]European Commission, “Directive 2024/1275 on the Energy Performance of Buildings (Recast),” eur-lex.europa.euModular, software-defined architectures are favored over proprietary hardware as the European Union, California, Singapore, and South Korea enact zero-emission or fault-detection standards that compel landlords to retrofit legacy assets with connected controls. Competitive intensity is rising as building-automation incumbents acquire software firms to defend installed bases, while network and cloud vendors bundle building-management features into switching and 5G portfolios. Retrofits dominate near-term spending because they deliver immediate energy savings and avoid the delays and cost inflation facing new construction.

Key Report Takeaways

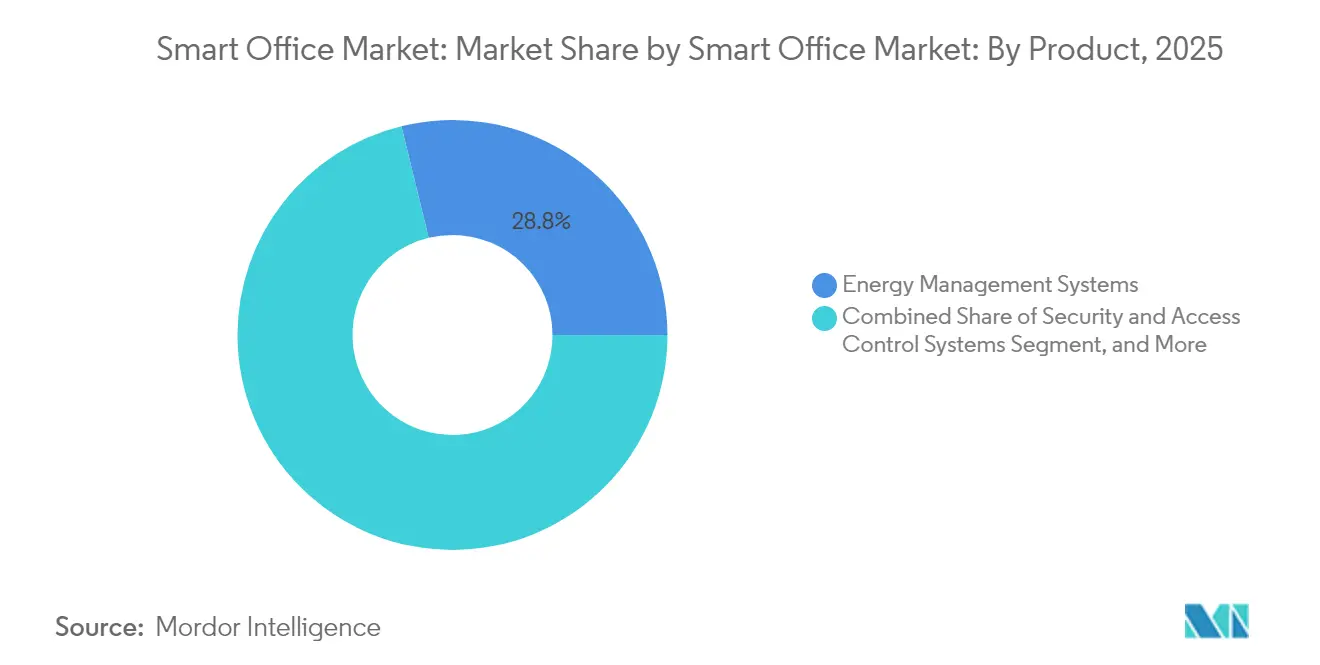

- By product, energy-management systems held 28.82% revenue share in 2025, while smart HVAC control systems are projected to expand at a 14.28% CAGR through 2031.

- By component, hardware led with 45.76% of 2025 revenue, whereas services are forecast to grow at a 14.57% CAGR to 2031.

- By building type, retrofits accounted for 63.72% of the 2025 value and are expected to advance at a 13.88% CAGR during the outlook period.

- By connectivity, Wi-Fi contributed 39.54% of revenue in 2025; however, cellular 4G and 5G are projected to grow at a 15.21% CAGR through 2031.

- By geography, North America accounted for 36.12% of 2025 revenue; the Asia Pacific is forecast to post the fastest CAGR of 14.05% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Office Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing hybrid and flexible working models | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Increasing focus on energy efficiency and sustainability mandates | +3.2% | Europe and Asia Pacific, spillover to North America | Long term (≥4 years) |

| Declining IoT sensor and connectivity module prices | +1.9% | Global | Short term (≤2 years) |

| Workplace wellness and indoor-air-quality regulations | +1.6% | North America and Europe, emerging in Asia Pacific | Medium term (2-4 years) |

| AI-based space utilization optimization | +2.3% | North America and Asia Pacific | Medium term (2-4 years) |

| Government-backed smart-building initiatives | +1.8% | Asia Pacific, Middle East, selective North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Hybrid and Flexible Working Models

Hybrid work is now the default operating model for large employers, raising demand for real-time occupancy analytics that match HVAC and lighting output to headcount. In 2024, 68% of Fortune 500 companies used flexible seating, up from 41% in 2020.[2]JLL Research, “Flexible Workspace Survey 2024,” jll.comReduced occupancy has pushed landlords to install granular monitoring that demonstrates efficiency to tenants and supports premium rents. Properties with certified smart-building credentials captured lease rates 8-12% above non-instrumented peers. The shift accelerates cloud-based building-management adoption that integrates with collaboration tools to synchronize cleaning, HVAC setpoints, and room availability.

Increasing Focus on Energy Efficiency and Sustainability Mandates

Climate policy has become the most durable demand driver. The EU’s Energy Performance of Buildings Directive recast mandates zero-emission status for new non-residential buildings by 2028 and sets renovation targets for 42% of existing stock by 2033. Germany requires an automation class B for buildings over 1,000 m². California’s 2024 Title 24 update requires fault detection in HVAC systems exceeding 54,000 BTU/h. South Korea’s expanded certification scope covers all commercial properties over 3,000 m². Such rules create a compliance floor that insulates the smart office market from macro cycles.

Declining IoT Sensor and Connectivity Module Prices

Rapid price deflation is democratizing adoption. Bluetooth Low Energy SOCs averaged USD 1.20 in Q1 2024, down from USD 2.10 in 2022.[3]Avnet Inc., “IoT Component Pricing Index Q1 2024,” avnet.com Wi-Fi 6E access points fell below USD 150 in volume buys, enabling whole-floor sensor meshes for buildings as small as 10,000 ft². Newly released 5G RedCap modules cost USD 8-12 per endpoint, half the price of legacy LTE Cat-1 units, allowing direct cloud connectivity without gateways. Lower hardware costs compress payback times from 48-60 months in 2020 to 24-36 months.

AI-Based Space Utilization Optimization

AI shifts space management from reactive scheduling to predictive allocation. Companies using AI-powered analytics reduce their real-estate footprints by 18% while maintaining steady employee satisfaction, saving USD 4,000-6,000 per employee in high-cost cities.[4]Microsoft Corp., “2024 Work Trend Index,” microsoft.comSiemens’ Enlighted deployments showed 23-29% energy savings compared to static schedules. Edge inference gains importance as latency-sensitive air-quality adjustments require sub-second response.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security concerns relating to IoT devices and data | –1.4% | Global, acute in Europe and North America | Medium term (2-4 years) |

| High retrofit costs for legacy buildings | –1.8% | North America and Europe | Short term (≤2 years) |

| Interoperability gaps across vendor ecosystems | –1.1% | Global | Medium term (2-4 years) |

| Slow decision cycles in commercial real estate | –0.9% | North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Security Concerns Relating to IoT Devices and Data

Intrusions into building-automation networks increased, with 37 confirmed incidents reported in the United States alone in 2023. The EU’s NIS2 directive classifies large commercial buildings as essential entities, imposing audit obligations that can exceed EUR 200,000 per year. Data-residency rules compel vendors to localize their cloud infrastructure, which can fragment service delivery and increase operating costs, particularly for tenants in financial services and healthcare.

High Retrofit Costs for Legacy Buildings

Buildings erected before 2000 often require extensive rewiring and controller replacement, which can push upgrade costs to USD 15-25 per square foot. A 2024 Urban Land Institute study found internal rates of return below 6% for full smart-retrofit programs in Class B and C offices. Limited access to green-financing instruments further constrains adoption in secondary markets, while rent-control regimes restrict pass-through of capital costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Energy Management Leads, HVAC Accelerates

Energy-management platforms accounted for 28.82% of 2025 revenue, the largest slice of the smart office market share. Demand-response incentives of USD 50-150 per curtailed kilowatt make participation financially attractive, and Johnson Controls reported 2 GW of commercial load enrolled under its OpenBlue platform in 2024. Smart HVAC controls are projected to expand at a 14.28% CAGR, the fastest among all products, aided by refrigerant phasedowns that trigger equipment upgrades compatible with lower global warming potential (GWP) gases. Security and access systems continue to benefit from the adoption of biometric and zero-trust technologies in regulated sectors. Fire and safety controls are incorporating NFPA 72-compliant wireless supervision, while smart lighting gains momentum through utility-backed LED rebate schemes that shorten paybacks to under 18 months.

Incremental demand is now tied to measurable outcomes, not just hardware counts. Energy dashboards that demonstrate kilowatt-hour savings help landlords justify premium service fees, and predictive maintenance modules embedded in HVAC controllers reduce unplanned downtime, which historically eroded tenant satisfaction. Combined, these factors solidify energy management and HVAC as twin growth engines within the larger smart office market.

By Component: Hardware Dominates, Services Surge

Hardware held 45.76% of 2025 revenue as sensors, controllers, and edge gateways remain foundational to any deployment. Services, however, are forecast to grow at a 14.57% CAGR, outpacing hardware as owners pivot toward outcome-based contracts. Schneider Electric’s EcoStruxure crossed 1 million connected devices in 2024, embedding ML models that optimize chiller staging without manual intervention. The smart office market size allocated to managed services is expanding as integrators package hardware, cloud licenses, and continuous commissioning into multi-year agreements.

Complexity fuels this service uptick. A typical enterprise footprint incorporates 8-12 discrete system categories, and few facility teams have the expertise to harmonize protocols across HVAC, lighting, metering, and conferencing. Systems integrators now carry performance risk, guaranteeing kilowatt-hour reductions or uptime, and recuperate costs through recurring fees that convert capex into opex. Meanwhile, hardware commoditization continues, but edge devices that host AI inference locally maintain pricing power due to latency and data-sovereignty needs.

By Building Type: Retrofit Economics Drive Majority Share

Retrofits generated 63.72% of 2025 revenue and are expected to log a 13.88% CAGR, underscoring the economic logic of upgrading existing stock. New-build projects typically embed connected controls by default; however, they often face longer development timelines, higher interest rates, and material-cost inflation, which limit near-term volume. Legislation such as New York City’s Local Law 97 charges carbon penalties starting in 2024, making energy-wasting buildings financially untenable. The smart office market size tied to retrofits, therefore, dominates budgets because energy savings and demand-response incentives start the moment systems come online.

Technical hurdles remain. Buildings with asbestos-laden ceilings or historic-preservation façades complicate sensor placement and conduit routing. Power over Ethernet offers an elegant retrofit path by combining data and power over existing structured cabling, reducing labor costs by up to 40%. Wireless sensor networks using Zigbee or Thread can bypass shaft drilling but may struggle in environments with dense steel. New buildings benefit from integrated design, yet the 2-4% premium on total construction budgets continues to be a negotiation point between developers and anchor tenants.

By Connectivity Technology: Wi-Fi Leads, Cellular Gains Momentum

Wi-Fi accounted for 39.54% of the 2025 value, leveraging the widespread adoption of enterprise LAN infrastructure and the maturity of Wi-Fi 6/6E standards, which provide deterministic latency under 10 ms. Cellular 4G and 5G are forecast to post the fastest 15.21% CAGR as private networks unlock on-premises data processing and guarantee QoS for latency-sensitive tasks. Carrier Global announced that 15% of its new controllers shipped with embedded cellular modems in 2024, a significant increase from negligible levels two years prior.

Bluetooth Low Energy dominates battery-powered sensors, offering multiyear autonomy. Zigbee and Thread, now unified under the Matter 1.2 spec, are winning lighting and shading projects where low power and local control trump cloud reach. Ethernet and Power over Ethernet continue to serve high-bandwidth devices, such as 4K PTZ cameras, aided by IEEE 802.3bt’s 90-watt power budget. As Wi-Fi 7 certification rolls out, multi-link operation that bonds 2.4, 5, and 6 GHz bands promises further gains in latency and reliability.

Geography Analysis

North America generated 36.12% of 2025 revenue and retains the largest smart office market share due to mature commercial real estate inventory, stringent coastal energy codes, and tenant demand for WELL and LEED certifications. Growth moderates to high single digits as the installed base deepens, but retrofit volume remains resilient thanks to New York’s carbon fines and California’s Title 24 updates. Federal tax incentives for high-efficiency HVAC under the Inflation Reduction Act further support ROI models, especially for campuses that pair heat-pump retrofits with solar power purchase agreements.

Asia Pacific is projected to record a 14.05% CAGR, the fastest regional pace, underpinned by China’s expansion of its Three-Star Green Building Standard to all public buildings over 20,000 m². India’s Smart Cities Mission continues to funnel capital toward connected infrastructure in Pune, Surat, and Ahmedabad, while Japan subsidizes up to 50% of BEMS installations for SMEs. The Middle East follows with gigascale projects, such as Saudi Arabia’s NEOM, which stipulates 100% renewable power and AI-driven building control, creating showcase opportunities for global vendors.

Europe sits between these poles. The Energy Performance of Buildings Directive imposes binding renovation quotas that pull forward demand for building automation, and Germany’s subsidy programs cover up to 40% of retrofit outlays. However, inflationary pressure and higher cost of capital temper volume, particularly in Southern Europe where real-estate yields remain compressed. South America grows modestly as multinationals enforce corporate sustainability standards on regional headquarters, but financing and technical-skills gaps slow uptake outside São Paulo, Mexico City, and Santiago.

Competitive Landscape

The smart office market remains moderately fragmented, with the top ten vendors holding a significant combined share, leaving room for regional integrators and software-first entrants. Building-automation leaders Johnson Controls, Siemens, Schneider Electric, and Honeywell are acquiring cloud-native firms to embed analytics into legacy controllers. Siemens paid USD 1.575 billion for Brightly Software in January 2024 to enhance its predictive maintenance and asset management features. Cisco and Huawei bundle building-management functions into their switching portfolios, leveraging network dominance to upsell smart-office capabilities.

Lighting specialists, such as Philips and Legrand, extend into occupancy sensing and space analytics, leveraging the ability of PoE to power both fixtures and data links. Smaller players carve niches: PointGrab supplies edge-AI occupancy chipsets, and Telit Cinterion focuses on cellular modules, feeding the broader ecosystem without competing head-to-head on full platforms. Patent filings in occupancy sensing surpassed 200 in 2024, signaling a shift in differentiation from sensor accuracy to software intelligence and multi-vendor interoperability.

Standards development is now a competitive lever. Firms that contribute to Matter, BACnet, and ONVIF gain early insight into protocol road maps that shape product architecture. Cybersecurity has also emerged as a deal-breaker in financial-services and healthcare verticals; Crestron’s XiO Cloud earned UL 2900-2-2 certification in February 2024. Vendors that can prove hardened security stacks win preferential access to risk-averse tenants, reinforcing a bifurcation between consumer-grade and enterprise-grade solutions.

Smart Office Industry Leaders

Johnson Controls International PLC

Cisco Systems Inc.

Siemens AG

Schneider Electric SE

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: IQVIA and Amazon Web Services announced a broad collaboration that positions AWS as IQVIA’s preferred cloud provider for AI-driven analytics.

- December 2025: The U.S. FDA deployed agentic AI across its workflows, automating label comparison and surveillance tasks.

- October 2025: Thermo Fisher Scientific closed its USD 8.9 billion acquisition of Clario Holdings, integrating eCOA and cardiac-safety tools into its PPD CRO division.

- January 2025: GlaxoSmithKline agreed to acquire IDRx for up to USD 1.15 billion, strengthening its oncology pipeline.

Global Smart Office Market Report Scope

The smart office systems deploy automated systems, sensors, and advanced communication infrastructure and networks, which provide centralized control and wireless data transfer for monitoring and analysis.

The Smart Office Market Report is Segmented by Product (Security and Access Control Systems, Energy Management Systems, Smart HVAC Control Systems, Audio-Video Conferencing Systems, Fire and Safety Control Systems, Other Products), Component (Hardware, Software Platforms, Services), Building Type (Retrofits, New Buildings), Connectivity Technology (Wi-Fi, Bluetooth Low Energy, Zigbee and Thread, Wired Ethernet/PoE, Cellular), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Product

| Security and Access Control Systems |

| Energy Management Systems |

| Smart HVAC Control Systems |

| Audio-Video Conferencing Systems |

| Fire and Safety Control Systems |

| Other Products |

By Component

| Hardware |

| Software Platforms |

| Services (Integration, Managed, Consulting) |

By Building Type

| Retrofits |

| New Buildings |

By Connectivity Technology

| Wi-Fi |

| Bluetooth Low Energy (BLE) |

| Zigbee and Thread |

| Wired Ethernet / PoE |

| Cellular (4G/5G) |

By Geography

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Mexico | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Product | Security and Access Control Systems | ||

| Energy Management Systems | |||

| Smart HVAC Control Systems | |||

| Audio-Video Conferencing Systems | |||

| Fire and Safety Control Systems | |||

| Other Products | |||

| By Component | Hardware | ||

| Software Platforms | |||

| Services (Integration, Managed, Consulting) | |||

| By Building Type | Retrofits | ||

| New Buildings | |||

| By Connectivity Technology | Wi-Fi | ||

| Bluetooth Low Energy (BLE) | |||

| Zigbee and Thread | |||

| Wired Ethernet / PoE | |||

| Cellular (4G/5G) | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Mexico | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Qatar | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the smart office market in 2026 and what growth is expected?

The smart office market size is USD 66.52 billion in 2026 and is projected to reach USD 124.83 billion by 2031 on a 13.42% CAGR.

Which product category currently generates the highest revenue?

Energy-management systems lead, accounting for 28.82% of 2025 revenue.

Which component is forecast to grow the fastest?

Services are expected to expand at a 14.57% CAGR through 2031 as owners favor outcome-based contracts.

Why are retrofits more attractive than new-build projects?

Retrofits deliver immediate energy savings and help avoid carbon penalties under rules such as New York City’s Local Law 97.

Page last updated on: