Smart Home Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

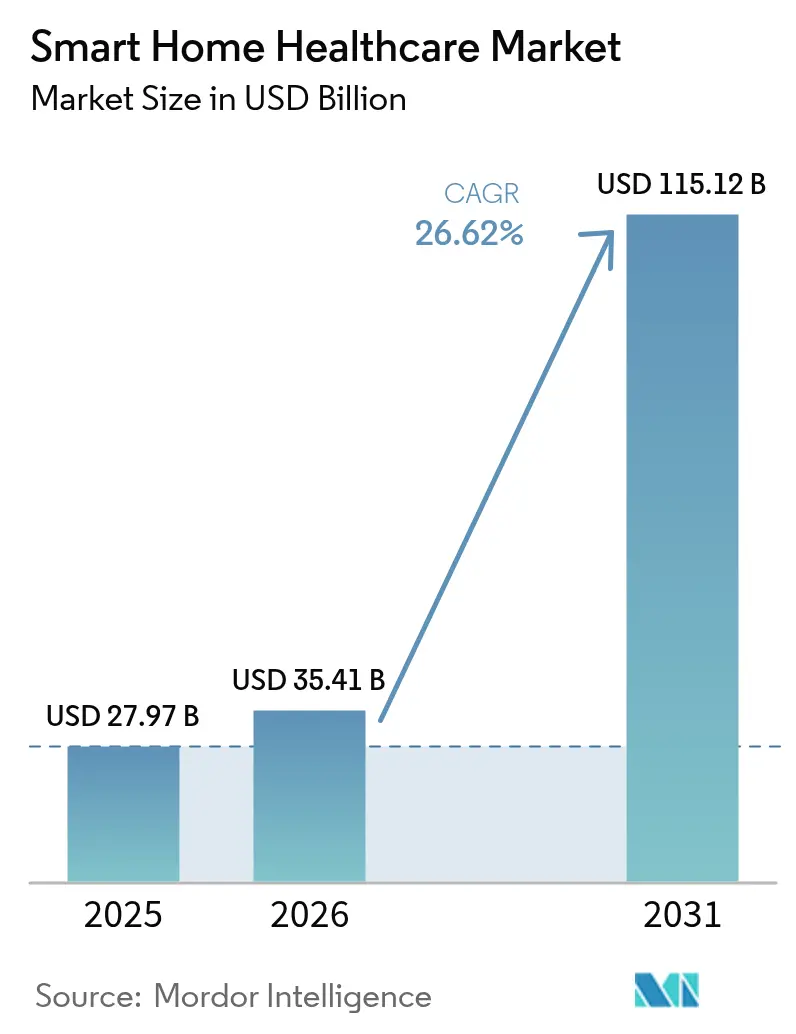

| Market Size (2026) | USD 35.41 Billion |

| Market Size (2031) | USD 115.12 Billion |

| Growth Rate (2026 - 2031) | 26.62% CAGR |

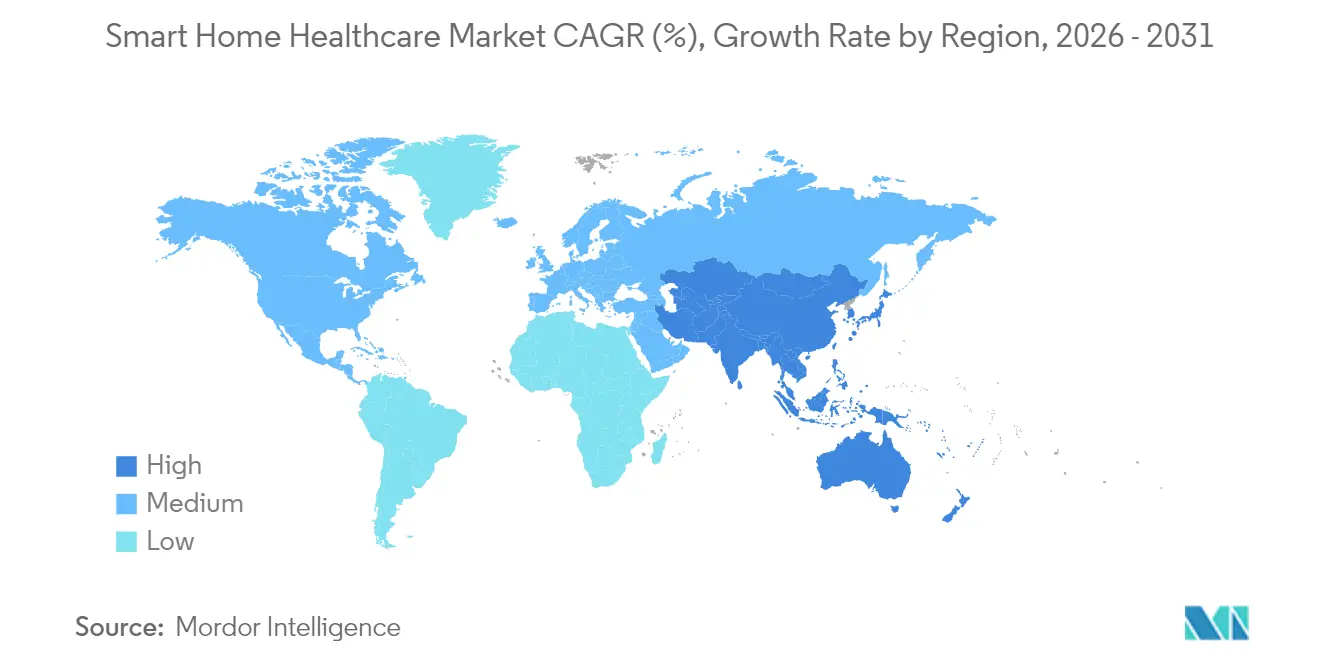

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Home Healthcare Market Analysis by Mordor Intelligence

The smart home healthcare market size was valued at USD 27.97 billion in 2025 and estimated to grow from USD 35.41 billion in 2026 to reach USD 115.12 billion by 2031, at a CAGR of 26.62% during the forecast period (2026-2031). Growing elderly and chronically ill populations, payer support for remote monitoring, and rapid 5G-plus connectivity upgrades place home-based care at the center of mainstream health-system strategy. Device makers focus on artificial-intelligence–driven analytics and seamless interoperability to turn once-episodic measurements into continuous decision support. Regulators now view cybersecurity as a core safety element, while supply-chain pressures push manufacturers toward localized production. Together these forces convert home healthcare from a convenience add-on to a structural pillar of modern care delivery.

Key Report Takeaways

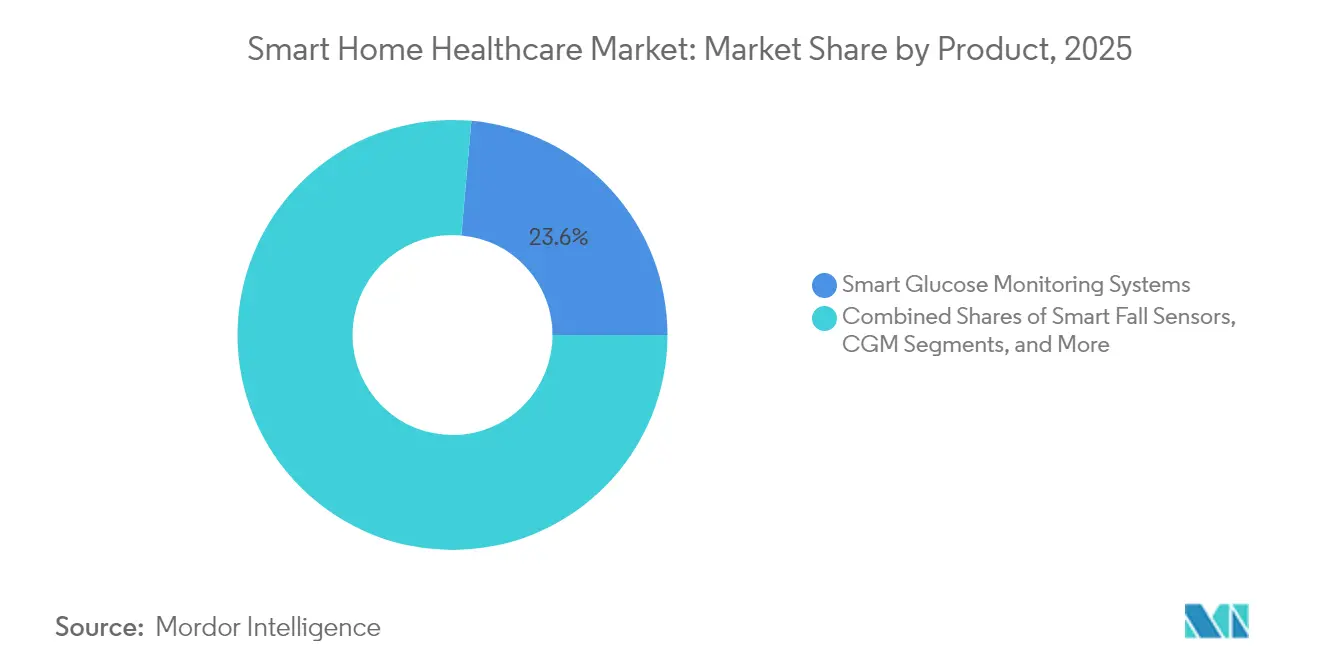

- By product category, Smart Glucose Monitoring Systems led with 23.60% revenue share in 2025; Continuous Glucose Monitoring is projected to advance at a 27.52% CAGR to 2031.

- By technology, wireless solutions held 60.25% of the smart home healthcare market share in 2025, while the segment is growing at 27.85% through 2031.

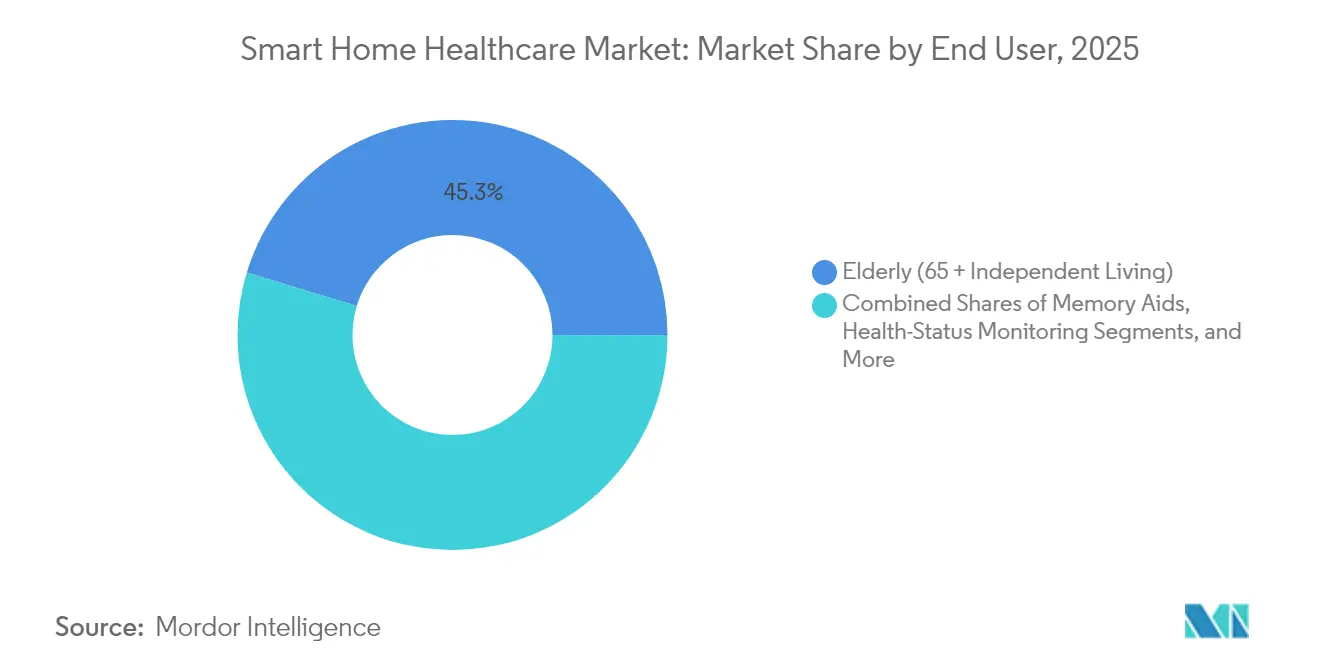

- By end user, the elderly segment accounted for 45.30% of the smart home healthcare market size in 2025; the disabled and mobility-impaired segment is expanding at 27.31% CAGR between 2026 and 2031.

- By application, health-status monitoring captured 27.10% of the smart home healthcare market size in 2025; remote patient management shows the fastest expansion at 27.22% CAGR through 2031.

- By geography, North America commanded 41.35% of the smart home healthcare market in 2025, while Asia Pacific is forecast to grow at 28.36% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Home Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic disease burden | +8.2% | Global, concentration in North America, Europe, Japan | Long term (≥ 4 years) |

| Accelerating IoT and AI integration in home-care devices | +6.8% | Global, led by North America and Asia Pacific | Medium term (2–4 years) |

| Shift to value-based reimbursement and telehealth coverage expansion | +5.4% | North America, Europe, emerging Asia Pacific | Medium term (2–4 years) |

| Cost advantage over facility-based care | +4.1% | Global, high-cost health markets | Long term (≥ 4 years) |

| Voice-assistant-enabled passive monitoring | +2.3% | North America, Europe, urban Asia Pacific | Short term (≤ 2 years) |

| Insurer wellness-IoT incentive programs | +1.8% | North America, select Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Chronic Disease Burden

One in five United States residents will be over 65 by 2030, and 85% of that cohort already lives with at least one chronic condition, pushing healthcare demand beyond existing facility capacity.[1]Nature Editorial Team, “The Demographic Time Bomb,” Nature, nature.com Japan already sees 29% of its citizens above 65, spurring pharmaceutical–technology collaborations that bring digital therapeutics into homes. Physician shortfalls projected at 139,000 by 2033 make smart devices an access necessity rather than a lifestyle upgrade. Programs such as Singapore’s Silver Infocomm Initiative pair tech-savvy youth with seniors, proving social support is a precondition for technology uptake. As demographics tighten, structural demand will keep the smart home healthcare market on an upward curve well past standard technology cycles.

Accelerating IoT and AI Integration in Home-Care Devices

Dexcom’s late-2024 launch of a generative-AI glucose platform demonstrates how machine learning contextualizes biosensor data into personalized insights.[2]Michael Smith, “Generative AI in Glucose Biosensing,” Dexcom Press Release, dexcom.com Samsung’s non-invasive glucose patents integrate predictive algorithms that address accuracy concerns flagged by the FDA, indicating AI now solves hardware limits rather than merely reporting data. Upcoming 6G networks promise near-instant bandwidth for large sensor arrays, giving clinicians seamless in-home visibility. Modular IoT nursing platforms already plug into existing electronic medical records through standardized APIs, suggesting that interoperability hurdles are easing. As each new device enriches shared data pools, value grows exponentially, reinforcing rapid adoption across multiple care pathways.

Shift to Value-Based Reimbursement and Telehealth Coverage Expansion

The 2025 Medicare Physician Fee Schedule keeps non-behavioral telehealth unfettered by geography through March 2025 and makes caregiver training billable, guaranteeing revenue for virtual chronic-care services. French national coverage for Dexcom ONE sensors extends continuous glucose monitoring to 100,000 basal-insulin users, the first such European reimbursement. Hypertension remote-monitoring pilots show a 22.2% ROI, which strengthens payer confidence in at-home models. With actuarial evidence showing USD 6,723 per-patient savings in heart-failure programs, payers and providers alike see connected devices as budget protectors. Reliable reimbursement removes a key barrier to scaling the smart home healthcare market.

Cost Advantage Over Facility-Based Care

UMass Chan Medical School’s “SNF at home” trials replace skilled-nursing beds with remote therapy, easing shortages and trimming per-episode costs. Hospitals leverage analytics platforms to optimize staffing and supply procurement, cutting operational expenses. Medtronic responds to chip inflation by shifting toward localized fabrication, maintaining price competitiveness while securing supply. Smart nursing-home retrofits lift build costs 18.35%, yet long-run savings from lower staff ratios and fewer safety incidents offset the premium.[3]Anna Miller, “Wearable Privacy Gaps,” MDPI Cryptography, mdpi.com Economies of scale and learning curves will keep driving device unit costs down, widening the cost gulf versus facility-centric care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cybersecurity concerns | -4.6% | Global, heightened in Europe and North America | Medium term (2–4 years) |

| Device-integration and interoperability gaps | -3.8% | Global, multi-vendor systems | Long term (≥ 4 years) |

| Care-giver digital-literacy barriers | -2.9% | Global, rural and underserved areas | Medium term (2–4 years) |

| Battery-life / maintenance burden for 24-7 sensors | -1.7% | Global, continuous monitoring | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cybersecurity Concerns

The FDA’s 2024 draft guidance now requires cybersecurity management plans and software bills of materials for every connected device submission, lengthening development cycles and raising compliance budgets. Consumer wearables that sit outside HIPAA still collect sensitive health data, leaving users exposed in grey regulatory zones. HIPAA’s safeguard rules and GDPR’s data-minimization mandates often pull in opposite directions, complicating AI model training. Edge-processing and end-to-end encryption mitigate risks yet increase computing overhead and cost. Each new IoT endpoint is another attack vector, requiring continuous security patching that inflates total cost of ownership, tempering adoption in the smart home healthcare industry.

Device-Integration and Interoperability Gaps

Fragmented data architectures keep valuable insights locked in silos; federated learning lets institutions co-train models without sharing raw patient data but demands advanced infrastructure. The 2025 Interoperability Standards Advisory endorses FHIR and terminologies like SNOMED CT and LOINC, though adoption remains uneven. Wireless Body Area Networks wrestle with protocol choices: IEEE 802.15.6 offers throughput, while LoRaWAN sacrifices speed for battery life. Proprietary ecosystems still give suppliers a competitive edge, clashing with providers who call for open architectures. True network effects for the smart home healthcare market will emerge only when standardized data exchange is universal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: CGM Technology Drives Glucose Monitoring Leadership

Smart Glucose Monitoring Systems held 23.60% of the smart home healthcare market in 2025, and Continuous Glucose Monitoring is set to climb at 27.52% CAGR, underscoring diabetes management as the entry point for connected care. Dexcom’s USD 1.114 billion Q4 2024 revenue, up 8% year on year, validates sustained demand. Smart cardiac monitors and blood-pressure devices ride telehealth adoption, while wearable sleep trackers spill over from consumer wellness into clinical protocols. Fall sensors deploy predictive algorithms to cut false alarms, though accuracy challenges hold back mass uptake. Medical device alert hubs act as command centers, linking multiple sensors for cohesive clinician dashboards. Smart inhalers align medication adherence with AI coaching, and robotic pill dispensers solve polypharmacy complexity. Product convergence signals that future offerings will package multi-parameter sensors under unified platforms rather than discrete gadgets.

The smart home healthcare market size for glucose monitoring dwarfs niche categories and supports heavy R&D budgets. Yet, competitive advantage is shifting toward software algorithms that translate raw data into actionable insights. Patent filings from Samsung show non-invasive optical glucose methods combined with contextual data layers to meet FDA accuracy thresholds. As reliability rises, CGM platforms will anchor broader chronic-care ecosystems, helping vendors cross-sell cardiac, respiratory, and sleep modules. Continuous feedback loops between device usage and clinical outcomes strengthen payer justification for wider reimbursement, reinforcing momentum across adjacent product lines.

By Technology: Wireless Dominance Accelerates Through 6G Integration

Wireless solutions commanded 60.25% of the smart home healthcare market share in 2025 and are advancing at 27.85% CAGR, pushed by 5G rollouts and early 6G pilots promising sub-millisecond latency. Wi-Fi 6 and Bluetooth Low Energy dominate short-range transmissions, while NB-IoT extends coverage to rural patients. Zigbee and Thread serve dense in-home mesh networks that need low power and self-healing signals. Wired connections persist in high-bandwidth imaging nodes but trend downward as encryption and reliability improve over airwaves.

By 2030 the smart home healthcare market size tied to wireless backbones will exceed wired channels by a broad margin, reflecting user demand for untethered mobility. Hybrid routers automatically shift traffic among cellular, Wi-Fi, and Ethernet to preserve quality of service during clinical events. LPWAN protocols such as LoRa prove ideal for battery-free wound sensors that broadcast occasional healing data, keeping maintenance minimal. As 6G matures, simultaneous transmission of thousands of sensor streams per household becomes feasible, opening doors to ambient intelligence that predicts clinical deterioration before symptoms appear.

By End User: Disability Segment Outpaces Traditional Elderly Focus

The elderly group controlled 45.30% of the smart home healthcare market in 2025, yet the disabled and mobility-impaired cohort is growing fastest at 27.31% CAGR. Predictive informing systems interpret user intent and adjust lighting, temperature, and medication schedules, enhancing autonomy. Chronic-disease patients remain a core base, relying on continuous metrics to manage conditions without frequent clinic visits. Post-acute and rehab patients use at-home sensors to document progress, cutting readmissions. Pregnant women adopt wearable fetal monitors that leverage deep-learning temperature models to forecast labor within two days.

Smart home healthcare industry vendors widen appeal by embedding universal-design principles, making interfaces usable by people with vision, hearing, or dexterity challenges. National Health and Aging Trends data show smart adaptations lower caregiver loads and delay institutionalization. Consumer wellness users form a feeder pipeline, graduating from basic fitness trackers to medical-grade gear as health needs evolve. Inclusion-driven design therefore doubles as a market-expansion engine.

By Application: Remote Patient Management Transforms Care Delivery

Health-status monitoring captured 27.10% of the smart home healthcare market size in 2025, while remote patient management is poised for 27.22% CAGR as payers reward proactive interventions. Safety and security nodes—fall detectors, smoke alarms, door sensors—form the first layer of protection for independent living. Machine-learning classifiers now differentiate genuine falls from routine movement, improving caregiver trust. Nutrition tracking pairs CGM readings with meal photos to quantify glycemic impact, tailoring dietary advice. Memory aids using voice prompts support medication adherence and daily routines for cognitive-decline sufferers.

Rehabilitation platforms combine motion sensors and gamified exercises, providing therapists with real-time recovery scores. The MONIT smart diaper system cut dermatitis severity among cognitively impaired users, illustrating niche-yet-high-impact use cases. Successful vendors map application design to specific clinical workflows, embedding analytics that convert raw sensor pulses into actionable tasks for nurses or family members. As remote management shows tangible outcome improvements, payer coverage will expand, further accelerating the smart home healthcare market.

Geography Analysis

North America generated 41.35% of 2025 revenue for the smart home healthcare market, thanks to established broadband, favorable reimbursement, and early IoT adoption. Government policy keeps momentum high as the FDA weaves cybersecurity into core safety rules and Medicare reimburses continuous remote monitoring. Provider networks integrate smart home data into clinical dashboards, giving clinicians near-real-time visibility across large patient cohorts.

Asia Pacific is on a steeper adoption curve and is projected to grow at 28.36% CAGR through 2031. Japan’s aging society propels pharmaceutical–technology alliances that bring monitoring to living rooms. China invests in national health-data lakes that feed AI decision engines, accelerating product approvals. South Korea earmarked USD 830 million to build AI-driven emergency systems and digital-care infrastructure. India emphasizes insurance-backed telehealth solutions that extend reach in rural districts, often using low-cost smartphones rather than dedicated hardware.

Europe posts steady growth under GDPR’s stringent privacy guardrails. National funding programs accelerate electronic medical-record harmonization, yet cross-border regulatory complexity slows multinational rollouts. Scandinavia pilots voice-assistant monitoring for dementia care, while France sets reimbursement precedent for CGM devices, expanding access for basal-insulin users.

The Middle East and Africa remain nascent but show promise where mobile health platforms overcome clinician shortages. Governments explore public-private partnerships to install community telehealth kiosks that interface with in-home devices. Latin America follows a similar path, leaning on low-bandwidth protocols that fit variable connectivity. Across all regions, policy alignment, broadband density, and digital-literacy programs determine adoption speed more than sensor availability alone.

Competitive Landscape

The smart home healthcare market features a mix of med-tech incumbents and consumer-tech challengers. Medtronic recorded 5.3% organic growth and 12.6% diabetes-segment expansion in FY25, fueled by MiniMed 780G automated insulin pumps. Abbott secured FDA and CE approvals for leadless pacemakers and expanded community health center partnerships to pair food security with chronic-care management. Dexcom merged biosensing with AI-driven analytics through ŌURA integration, broadening its wellness footprint while deepening clinical relevance.

Consumer giants build on existing device ecosystems. Apple layers health features onto Watch and iPhone, while Google leverages Fitbit data to feed proprietary AI coaching. Amazon’s Alexa Together uses voice cues to detect wellness changes and alert caregivers. Samsung’s push into optical glucose sensing shows the blurring line between wellness gadgets and regulated medical devices.

Start-ups attack white spaces such as battery-free wound monitors and federated-learning platforms that safeguard privacy without raw-data exchanges. Partnerships bloom across sectors: hospitals supply clinical validation, telecoms provide bandwidth, and insurers create incentive schemes. Competitive advantage is shifting toward firms mastering secure data orchestration rather than those focusing solely on hardware breakthroughs. With no single player above 15% market command, rivalry centers on speed of innovation and ecosystem breadth.

Smart Home Healthcare Industry Leaders

Sleepace

Awair Inc.

Eight Sleep

Encore Healthcare

Medtronic Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Dexcom reported Q4 2024 revenue of USD 1.114 billion, international sales up 17%, announced partnership with ŌURA, and unveiled generative-AI glucose insights.

- December 2024: Dexcom launched the first generative-AI platform for glucose biosensing, combining activity and sleep data for personalized advice.

- November 2024: Centers for Medicare & Medicaid Services finalized the 2025 Physician Fee Schedule, making caregiver tele-training reimbursable and setting the originating-site fee at 80% of USD 31.01.

- October 2024: South Korea earmarked USD 830 million through 2032 for AI emergency systems and integrated digital health under the Korean Advanced Research Projects Agency for Health.

Global Smart Home Healthcare Market Report Scope

Smart home healthcare is a home-based ecosystem that is equipped with sensors and technologies to provide in-home care for the elderly, outpatients, and individuals with disabilities.

The Smart Home Healthcare Market is segmented by Products (Medical Device Alert Systems, Smart Glucose Monitoring Systems, Smart Cardiac Monitoring Systems, and Others), Technology (Wireless and Wired), Application (Safety and Security Monitoring, Nutrition/Diet Monitoring, Memory Aids, Fall Prevention and Detection, Health Status Monitoring, and Others) and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Medical Device Alert Systems |

| Smart Glucose Monitoring Systems |

| Continuous Glucose Monitoring (CGM) |

| Smart Cardiac Monitoring Devices |

| Smart Blood-Pressure Monitors |

| Wearable Sleep and Vital-Sign Trackers |

| Smart Inhalers and Respiratory Monitors |

| Smart Fall Sensors |

| Medication-Dispensing Robots |

| Others |

| Wireless | Wi-Fi |

| Bluetooth | |

| Zigbee / Thread | |

| Cellular / NB-IoT | |

| Wired | |

| Hybrid Networks |

| Elderly (65 + Independent Living) |

| Chronic-Disease Patients |

| Disabled / Mobility-Impaired Individuals |

| Post-Acute and Rehabilitation Patients |

| Pregnant Women and New Mothers |

| General Wellness Users |

| Safety and Security Monitoring |

| Health-Status Monitoring |

| Fall Prevention and Detection |

| Nutrition / Diet Tracking |

| Memory Aids |

| Remote Patient Management |

| Rehabilitation and Chronic-Care Management |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Product | Medical Device Alert Systems | ||

| Smart Glucose Monitoring Systems | |||

| Continuous Glucose Monitoring (CGM) | |||

| Smart Cardiac Monitoring Devices | |||

| Smart Blood-Pressure Monitors | |||

| Wearable Sleep and Vital-Sign Trackers | |||

| Smart Inhalers and Respiratory Monitors | |||

| Smart Fall Sensors | |||

| Medication-Dispensing Robots | |||

| Others | |||

| By Technology | Wireless | Wi-Fi | |

| Bluetooth | |||

| Zigbee / Thread | |||

| Cellular / NB-IoT | |||

| Wired | |||

| Hybrid Networks | |||

| By End User | Elderly (65 + Independent Living) | ||

| Chronic-Disease Patients | |||

| Disabled / Mobility-Impaired Individuals | |||

| Post-Acute and Rehabilitation Patients | |||

| Pregnant Women and New Mothers | |||

| General Wellness Users | |||

| By Application | Safety and Security Monitoring | ||

| Health-Status Monitoring | |||

| Fall Prevention and Detection | |||

| Nutrition / Diet Tracking | |||

| Memory Aids | |||

| Remote Patient Management | |||

| Rehabilitation and Chronic-Care Management | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the smart home healthcare market?

The market is valued at USD 35.41 billion in 2026 and is expected to reach USD 115.12 billion by 2031.

Which region is expanding fastest in the smart home healthcare market?

Asia Pacific leads growth with a projected 28.36% CAGR through 2031, propelled by national digital-health investments.

Which product segment holds the largest smart home healthcare market share?

Smart Glucose Monitoring Systems account for 23.60% of 2025 revenue, driven by continuous glucose monitoring adoption.

How do reimbursement policies influence smart home healthcare adoption?

Expanded telehealth and remote-monitoring coverage create predictable revenue streams, accelerating device deployment and patient uptake.

What are the main barriers to smart home healthcare market growth?

Data-privacy concerns, interoperability gaps, and digital-literacy challenges remain key restraints despite rapid technology advances.

Who are the major players in the smart home healthcare industry?

Medtronic, Abbott, Dexcom, Apple, Google, and Amazon lead through a combination of medical-device expertise and consumer-tech ecosystems.

Page last updated on: