Smart Trash Bins Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

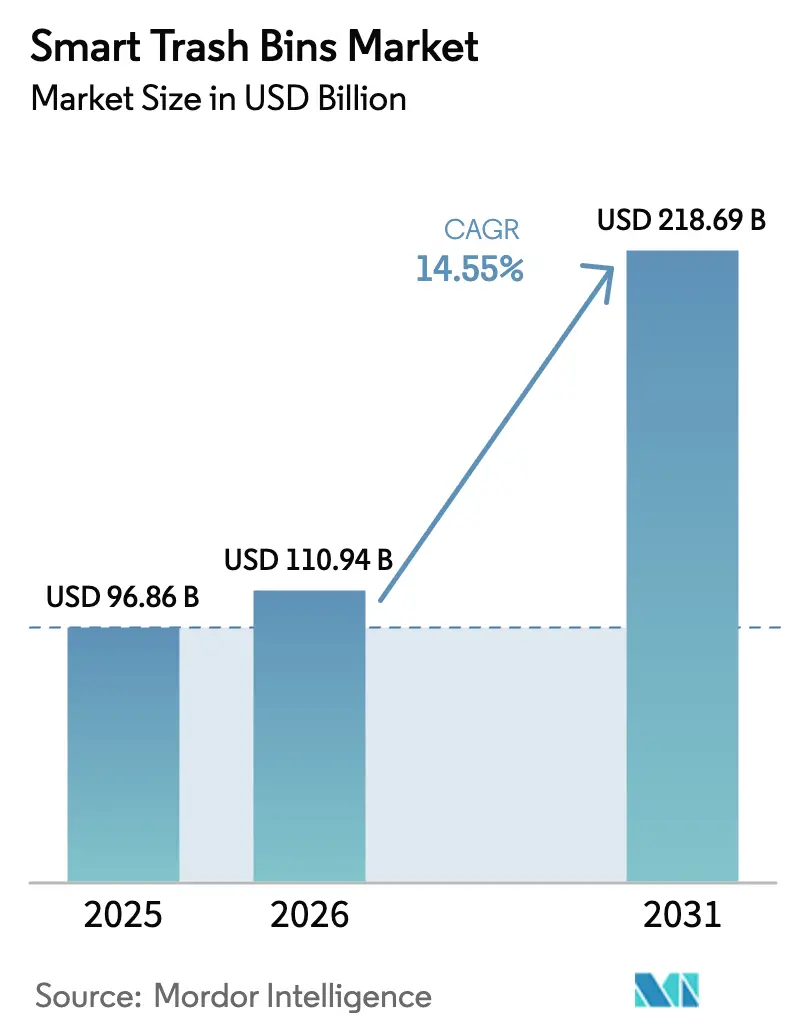

| Market Size (2026) | USD 110.94 Billion |

| Market Size (2031) | USD 218.69 Billion |

| Growth Rate (2026 - 2031) | 14.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Trash Bins Market Analysis by Mordor Intelligence

The smart trash bins market size was valued at USD 96.86 million in 2025 and estimated to grow from USD 110.94 million in 2026 to reach USD 218.69 million by 2031, at a CAGR of 14.55% during the forecast period (2026-2031). Solid waste authorities and commercial facilities are adopting intelligent collection systems because municipal digitization mandates, rapid sensor price erosion, and circular-economy regulations are now converging. North American cities adopted the technology first, demonstrating that optimized routes can cut collection costs by up to 50% while shrinking fleet-related emissions. Hardware remains the largest revenue contributor, yet demand is quickly shifting toward analytics platforms that monetize fill-level data for predictive planning. Market momentum is strongest in regions that pair smart-city grants with landfill-diversion targets, ensuring long-term budget allocations for connected bins.

Key Report Takeaways

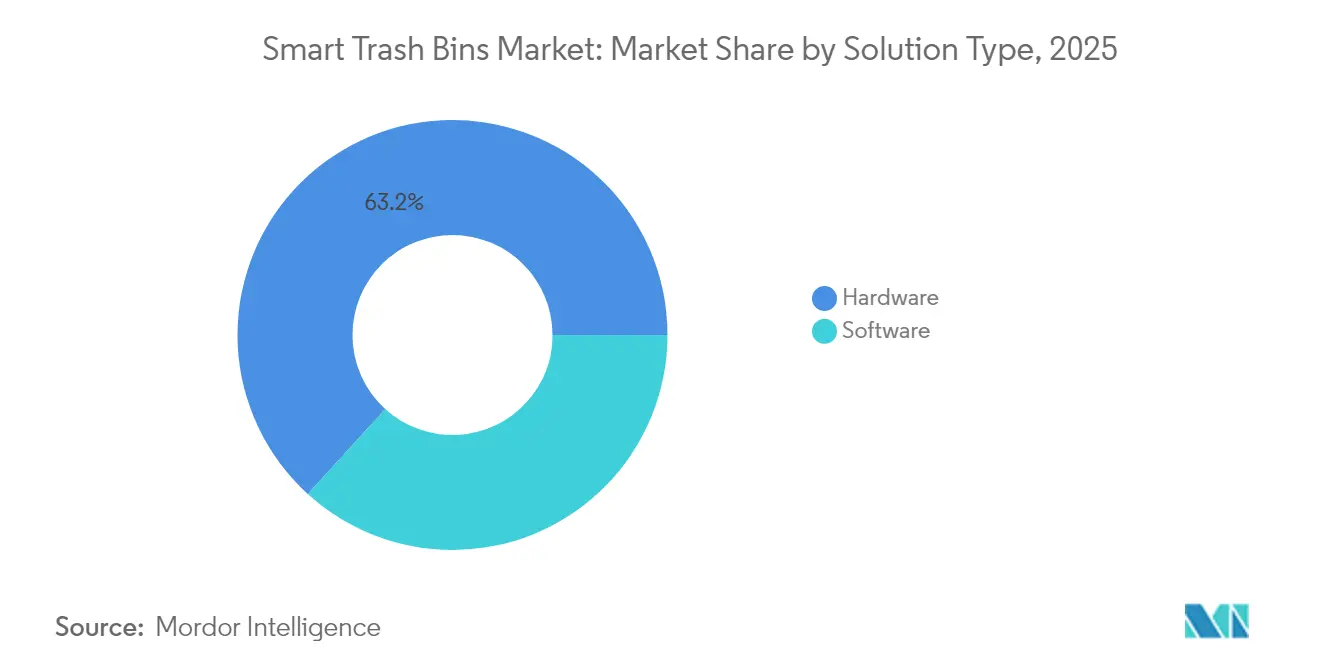

- By solution type, hardware held 63.25% of 2025 revenue, while software and analytics are set to grow at 15.78% CAGR through 2031.

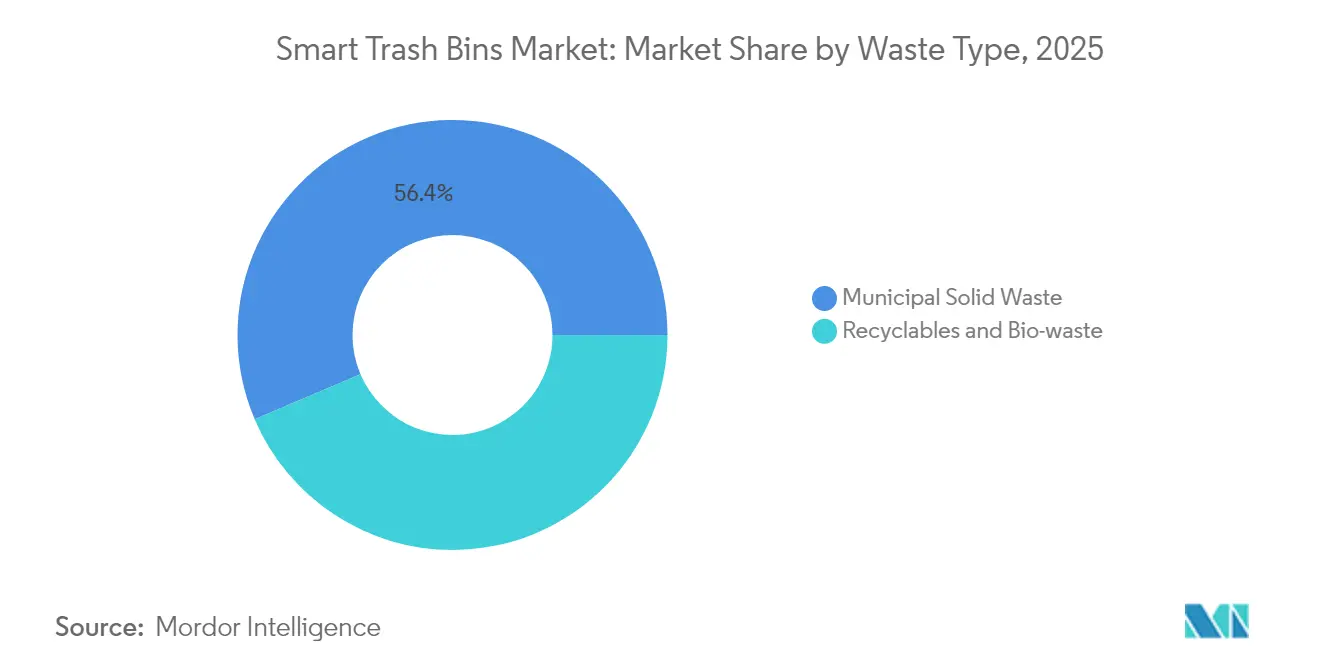

- By waste type, municipal solid waste led with 56.40% of the smart trash bins market share in 2025; organics collection is projected to expand at 15.02% CAGR to 2031.

- By end user, commercial sites captured 51.55% revenue in 2025, whereas municipal deployments are expected to progress at a 15.44% CAGR over the forecast.

- By sales channel, offline distribution controlled 57.35% of 2025 revenue; online channels are poised for a 15.61% CAGR to 2031.

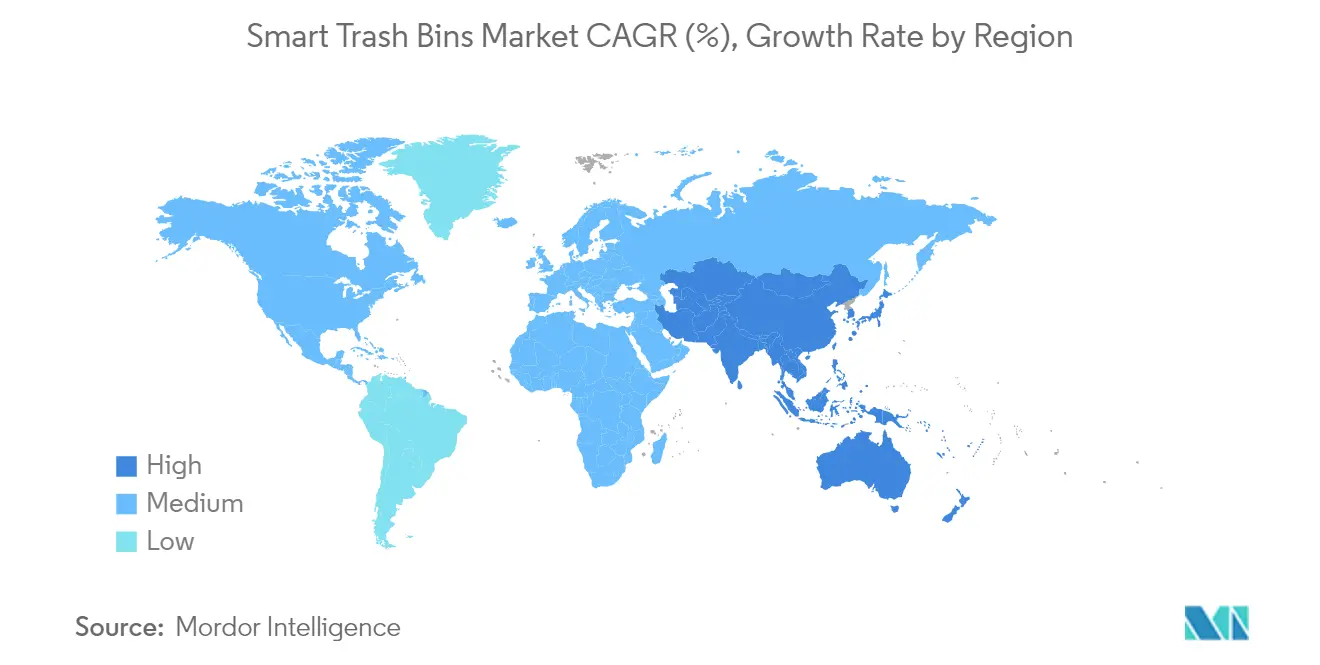

- By geography, North America accounted for 37.05% revenue in 2025; Asia-Pacific is set for the fastest 15.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Trash Bins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-city funding and mandates | +3.2% | North America, EU | Medium term (2-4 years) |

| IoT sensor cost decline | +2.8% | Asia-Pacific core | Short term (≤2 years) |

| Circular-economy landfill diversion rules | +2.1% | EU expanding to North America | Long term (≥4 years) |

| Edge-AI contamination detection | +1.9% | Developed markets | Medium term (2-4 years) |

| Urban population growth | +1.7% | Asia-Pacific, MEA | Long term (≥4 years) |

| Carbon-credit monetization | +1.4% | North America, EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Smart-City Funding and Mandate

Growing municipal budgets now earmark connected-waste infrastructure as a foundational data layer for wider urban analytics programs. Phoenix transitioned 418,000 collection points to digital monitoring that synchronizes route optimization with sustainability dashboards. Similar allocations appear in European and Canadian grant frameworks that treat sensorized bins as core utilities. Because city planners can overlay waste-generation data on traffic and demographic maps, funding streams have become recurrent. Suppliers benefit from predictable multi-year contracts that improve return on investment calculations, and the model is replicating in mid-tier US counties and Nordic municipalities.

Rapid IoT Sensor Cost Decline and Connectivity Rollout

Average fill-level sensor prices fell by more than 35% between 2023 and 2025, enabling large deployments in budget-constrained jurisdictions. Energy-efficient nodes now run 70 days on small batteries, while LPWAN backhaul eliminates the need for cellular subscriptions. Asian smart city pilots increasingly bundle LoRaWAN gateways with street-lighting upgrades, accelerating rollouts in Vietnam and Indonesia. The resulting network effect commoditizes basic telemetry and shifts competitive leverage to analytics brands that interpret bin-level data into preventive maintenance schedules.

Circular-Economy Regulations on Landfill Diversion

The EU Circular Economy Action Plan compels cities to verify diversion rates, and ISO 59000 provides measurement guidance that real-time bin telemetry can satisfy.[1]European Commission, “Circular Economy Action Plan,” European Commission, ec.europa.eu Early adopters in Belgium and the Netherlands now integrate bin data into compliance dashboards, reducing manual audit costs. North American provinces are drafting comparable landfill-levy rules, setting the stage for mandatory adoption of contamination-detection lids and blockchain traceability modules. Vendors that bundle compliance reporting into subscription tiers are securing premium margins.

Edge-AI-Enabled Contamination Detection Boosts ROI

AETECH’s battery-efficient neural networks identify recyclables with 99.3% precision, preventing costly processing of tainted loads while maintaining minimal power draw.[2]AETECH, “Edge-AI Sorting Solution Launch,” AETECH, aetech.ai The capability allows route adjustments in real time, sending contaminated bins to specialized facilities and raising tip-fee savings. The higher ROI shortens payback periods from four years to less than two in high-volume commercial districts. Competitive bids now score higher if platforms embed AI inference at the edge rather than the cloud.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and uncertain payback | -2.3% | Smaller municipalities worldwide | Short term (≤2 years) |

| Fragmented procurement and long bid cycles | -1.8% | North America, EU | Medium term (2-4 years) |

| Lack of interoperability standards | -1.2% | Global | Medium term (2-4 years) |

| Labor-union resistance | -0.9% | Unionized markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Payback Uncertainty

Connected bins cost USD 500–2,000 per unit depending on compaction and AI functions, straining budgets in towns under 100,000 residents. Although route optimization can cut fleet mileage by 25–50%, decision makers struggle to quantify secondary benefits such as reduced litter or methane avoidance. Budget cycles extend two to five years, creating mismatches with rapid hardware iteration. Vendors respond by offering lease-to-own models and performance-based contracts that tie monthly fees to verified diversion gains.

Fragmented Municipal Procurement and Long Bid Cycles

US Environmental Protection Agency guidelines recommend starting waste-service tenders years before award to align divergent objectives, prolonging sales funnels.[3]U.S. Environmental Protection Agency, “Sustainable Materials Management Procurement Guidelines,” U.S. Environmental Protection Agency, epa.gov Differing technical specs and privacy rules require vendors to customize proposals city by city, inflating pursuit costs. Smaller suppliers exit bids prematurely, reducing competitive intensity and slowing innovation. Cloud-native platforms that offer configurable APIs mitigate the fragmentation but need common data schemas to scale across borders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Hardware Dominance Faces Software Disruption

Hardware solutions still generate the bulk of smart trash bins market revenue, accounting for 63.25% in 2025. The segment includes fill-level sensors, solar compactors, RFID tags, and ruggedized communication modules that serve as the physical interface between waste streams and data clouds. Hardware sales formed the initial growth engine because municipalities required tangible assets to unlock grant disbursements, and procurement teams favored capital expenditure models that allocate devices to asset registers. Standardization is narrowing performance gaps among vendors, making price parity the norm for sensor payloads.

Software and analytics platforms now represent the fastest-growing revenue component at 15.78% CAGR to 2031. The shift repositions data rather than devices as the primary value driver, enabling suppliers to upsell predictive algorithms, dashboard subscriptions, and application-programming-interface access to third-party planners. As a result, recurring revenue share is expected to exceed 40% of the smart trash bins market size for leading vendors by 2028. Edge-AI upgrades further reduce haulage costs, securing budget approvals even in CAPEX-constrained municipalities. Service providers that combine firmware over-the-air updates with business-intelligence tools enjoy higher renewal rates and lower churn.

By Sales Channel: Digital Transformation Accelerates Online Growth

Offline integrators captured 57.35% of 2025 revenue because city engineering teams still rely on incumbents for installation, training, and multiyear maintenance. Local distributors navigate building codes, zoning rules, and collective-bargaining agreements that often dictate bin footprint and servicing schedules. Their field technicians also perform warranty repairs that safeguard service-level agreements.

Online platforms, however, are expanding fast at 15.61% CAGR as standardized, smaller-scale smart trash bins enter catalogues on industrial-procurement portals. Municipalities use e-tendering portals for pilot orders that evaluate proof-of-concept metrics before issuing citywide RFPs. Vendors leverage direct-to-customer storefronts to bypass distribution margins and to gather fleet-wide telemetry into centralized clouds without data-handoff delays. Over the forecast horizon, digital channels will likely claim double-digit revenue share increases, particularly for compact indoor units bought by private campuses.

By Waste Type: Organics Drive Specialized Collection Innovation

Municipal solid waste remains the dominant stream, holding 56.40% of 2025 revenue because every urban zone requires frequent residual collection. Smart lids that report fill status every two hours allow fleet dispatchers to reconfigure routes dynamically, avoiding half-empty pickups and lowering overtime expenses. The discipline of constant volume measurement also discourages illegal dumping, cutting cleanup budgets in central business districts.

Organics and bio-waste represent the most dynamic opportunity with a projected 15.02% CAGR. Composting mandates in Canada and Western Europe pay tipping-fee rebates for verified diversion tonnage, making sensorized organics carts financially attractive. Smart trash bins fitted with temperature probes and odor sensors prevent contamination that downgrades compost quality. Verified data streams qualify for carbon-credit issuance, creating an extra revenue lever for municipal treasuries. Recyclables remain a mature yet stable sub-segment; the addition of AI vision modules that achieve 99% material-type accuracy protects bale purity and sustains commodity prices.

By End User: Municipal Adoption Accelerates Sustainability Goals

Commercial facilities such as shopping malls, corporate campuses, and hotels led adoption, producing 51.55% of smart trash bins market revenue in 2025. Their condensed waste volumes magnify savings from compaction and real-time scheduling, and corporate ESG scorecards elevate visible technology investments. Private buyers also face fewer procurement barriers, shortening decision cycles to months rather than years.

Municipal deployments, however, are positioned to grow fastest at 15.44% CAGR because climate-neutrality pledges require verifiable diversion data. Cities are installing sensorized bins in parks and transit corridors to capture real-time litter trends, supporting public cleanliness indices that influence tourism and downtown revitalization budgets. Residential curbside pilots in the United Kingdom illustrate how neighborhood-level analytics can inform fleet right-sizing and capital-equipment deferrals. The public sector’s scale advantage will expand its share of the smart trash bins market through 2031.

Geography Analysis

North America held 37.05% of global revenue in 2025, reflecting early grant programs, robust IoT infrastructure, and established vendor ecosystems. Phoenix digitized weekly pickups across 418,000 locations, linking fill-level APIs to its climate dashboard for transparent performance monitoring. New York City’s plan for stationary curbside units underscores how dense urban footprints catalyze compactor adoption. Cloud-based platforms integrate seamlessly with 4G and low-power networks prevalent across US and Canadian metro areas, ensuring high uptime and rapid firmware updates.

Asia-Pacific will register a 15.92% CAGR through 2031, the swiftest worldwide. Rapid urbanization forces local governments to leapfrog legacy fleet models and invest directly in AI-enabled waste infrastructure. South Korea’s AETECH robots sort 96 items per minute, boosting recycling centers’ throughput without expanding labor rosters. Governments in Thailand, Vietnam, and Indonesia embed waste-data requirements in smart-city masterplans, triggering competitive tenders valued at tens of millions of USD. LPWAN coverage grows as utilities deploy network backbones, lowering operating costs compared with cellular telemetry.

Europe maintains steady expansion underpinned by rigorous diversion quotas in the EU Circular Economy Action Plan. Member states must record contamination incidents and recycling output, driving purchase orders for bins equipped with optical sensors and barcode scanners. The European Environment Agency validates technology pilots that demonstrate 30% reductions in residual collections after smart-bin rollout. Nordic cities capitalize on 0G networks from Heliot Europe to monitor rural containers where cellular signals are scarce. As ISO 59000 gains adoption, municipalities employ standardized APIs to transmit diversion metrics directly into environmental-audit platforms, cementing software-as-a-service renewals.

Competitive Landscape

The smart trash bins market is moderately fragmented. The top five suppliers collectively control an estimated 45% of 2025 revenue, while many regional start-ups concentrate on niche applications. Bigbelly remains the benchmark incumbent with more than 1,800 municipal and private clients in 60 nations, bundling hardware leasing with its CLEAN cloud that automates route sequences.[4]Bigbelly, “CLEAN Software Subscription Guide,” Bigbelly, bigbelly.com Its scale advantages include a global maintenance network and component purchasing power that sustains gross-margin leadership.

Disruptors differentiate through edge-AI capabilities that improve sorting accuracy and energy efficiency. AETECH raised 8.6 billion KRW in 2025 to commercialize compact robots that retrofit onto existing conveyor lines, delivering 99.3% purity even in mixed-material streams. SusGlobal monetizes verified organics diversion by selling carbon credits worth CAD 5-10 per ton, illustrating a revenue model that transcends hardware sales. Start-ups are also integrating blockchain ledgers that timestamp fill events, offering immutable audit trails for extended-producer-responsibility schemes.

Strategic moves center on vertical integration, with sensor makers acquiring data-analytics studios to secure full-stack portfolios. Partnerships between antenna specialists and bin manufacturers improve signal reliability in sub-basements and alleyways, unlocking new indoor applications. Suppliers are also exploring product-as-a-service contracts that shift CAPEX to operating budgets, addressing procurement hurdles in smaller jurisdictions. Because interoperability standards remain fluid, ecosystem control is emerging as a key battleground over the next five years.

Smart Trash Bins Industry Leaders

CleanRobotics

Ausko Pte Ltd

Evreka

Enevo Inc.

iTouchless Housewares and Products Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: AETECH commercialized AI waste-sorting robots achieving 99.3% accuracy and closed an 8.6 billion KRW Series A to build an unmanned recovery center doubling recycling rates in South Korea while planning Southeast Asian expansion.

- December 2024: Sensorita installed 2,500 radar-based sensors across Norway with Ragn-Sells to create digital twins of containers for contamination reduction.

- August 2024: New York City contracted Contenur for stationary curbside bins supporting its zero-waste roadmap.

- June 2024: SusGlobal Energy generated 105,000 verified emission reductions from its Belleville compost facility and sold credits at CAD 5-10 each

Global Smart Trash Bins Market Report Scope

Smart trash bins are basically sensor-based, touchless technology that reduces human effort. These automated garbage bins used for waste management or disposal enable the users to comprehensively control waste operations via one single platform by providing real-time data about the type of water being collected, location, current status, fill level, etc.

The study offers a comprehensive analysis of the smart trash bins market by considering current trends, demand patterns, technological innovations, and emerging opportunities that the market may offer. The study segments the market into various categories, including end-user and geography, to provide more insights into the demand and consumption patterns. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments. A chapter dedicated to the impact analysis of COVID-19 is also a part of the study.

| Hardware (Fill-level sensors, RFID, optical, compaction) |

| Software / Analytics Platforms |

| Offline (Distributors, System Integrators) |

| Online (Direct, E-commerce) |

| Municipal Solid Waste |

| Recyclables |

| Bio-waste / Organics |

| Residential |

| Commercial |

| Municipal / Public Spaces |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Solution Type (Value) | Hardware (Fill-level sensors, RFID, optical, compaction) | |

| Software / Analytics Platforms | ||

| By Sales Channel (Value) | Offline (Distributors, System Integrators) | |

| Online (Direct, E-commerce) | ||

| By Waste Type (Value) | Municipal Solid Waste | |

| Recyclables | ||

| Bio-waste / Organics | ||

| By End User (Value) | Residential | |

| Commercial | ||

| Municipal / Public Spaces | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the smart trash bins market?

The market stands at USD 110.94 million in 2026 and is projected to reach USD 218.69 million by 2031.

How fast is the marke growing?

It is expanding at a 14.55% compound annual growth rate (CAGR) during 2026-2031.

Which region holds the largest market share?

North America leads with 37.05% revenue share in 2025, reflecting early smart-city funding and mature IoT infrastructure.

Which region will grow the fastest through 2031?

Asia-Pacific is forecast to post the highest 15.92% CAGR, driven by rapid urbanization and government-backed smart-city programs.

What segment is growing more quickly—hardware or software?

Software and analytics platforms are advancing at a 15.78% CAGR, outpacing hardware as municipalities seek data-driven optimization.

What is the biggest barrier to adoption?

High upfront capital expenditure (USD 500–2,000 per unit) and uncertain payback periods remain the key obstacles for smaller municipalities.

Page last updated on: