Smart Hospital Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 96.61 Billion |

| Market Size (2031) | USD 218.19 Billion |

| Growth Rate (2026 - 2031) | 17.68% CAGR |

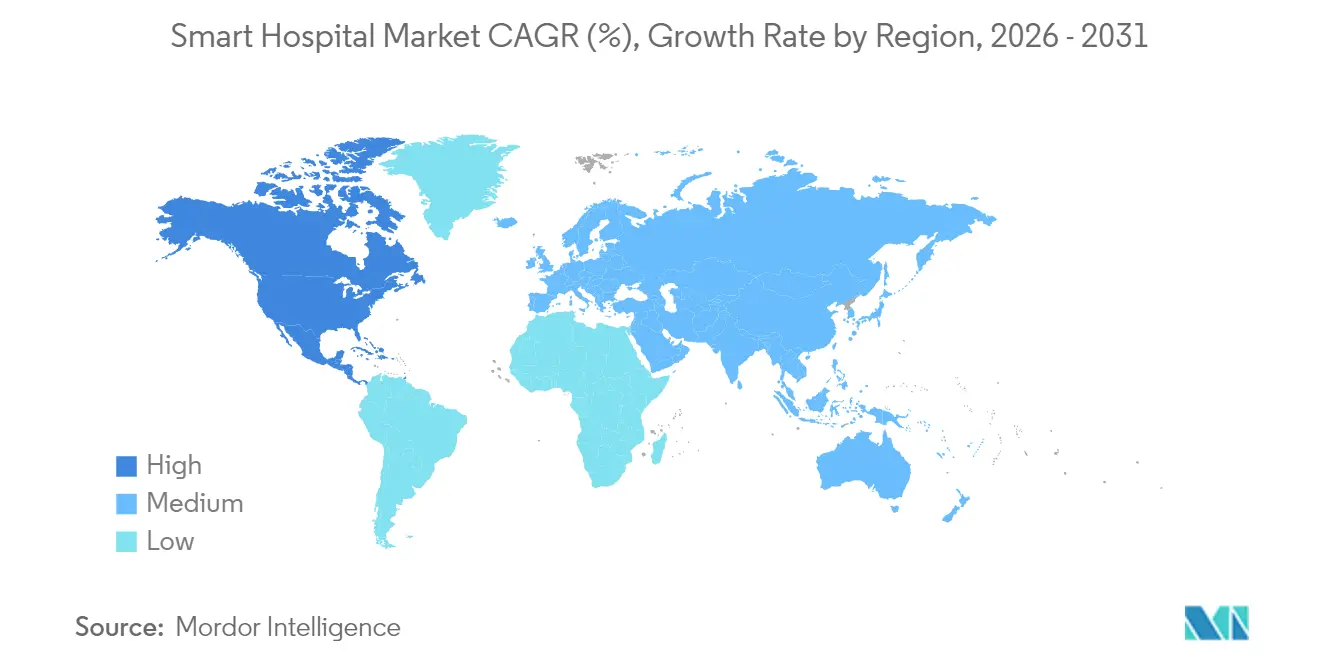

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

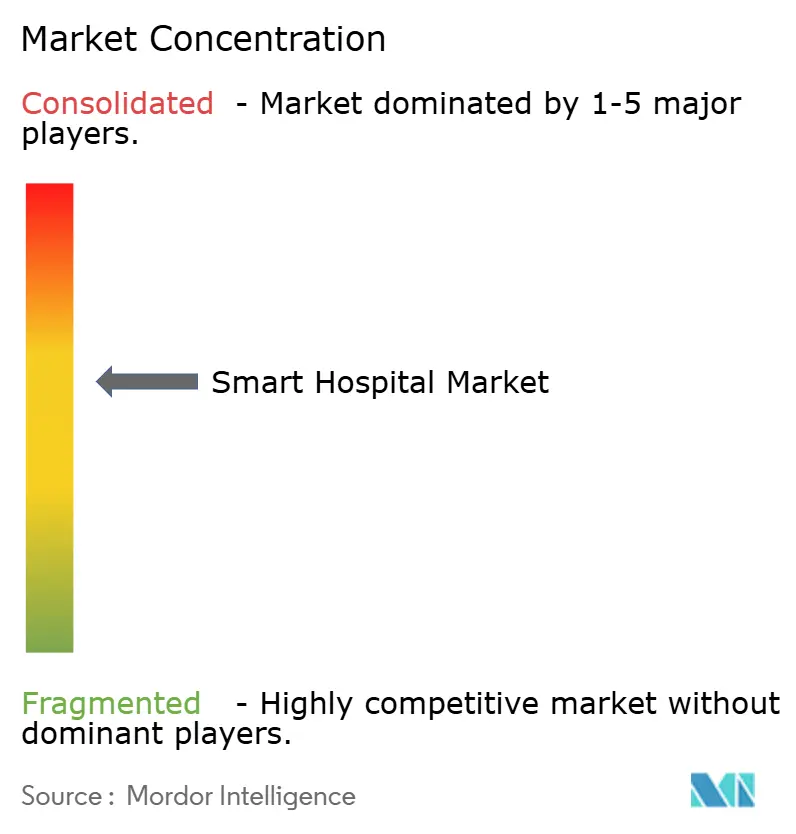

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Hospital Market Analysis by Mordor Intelligence

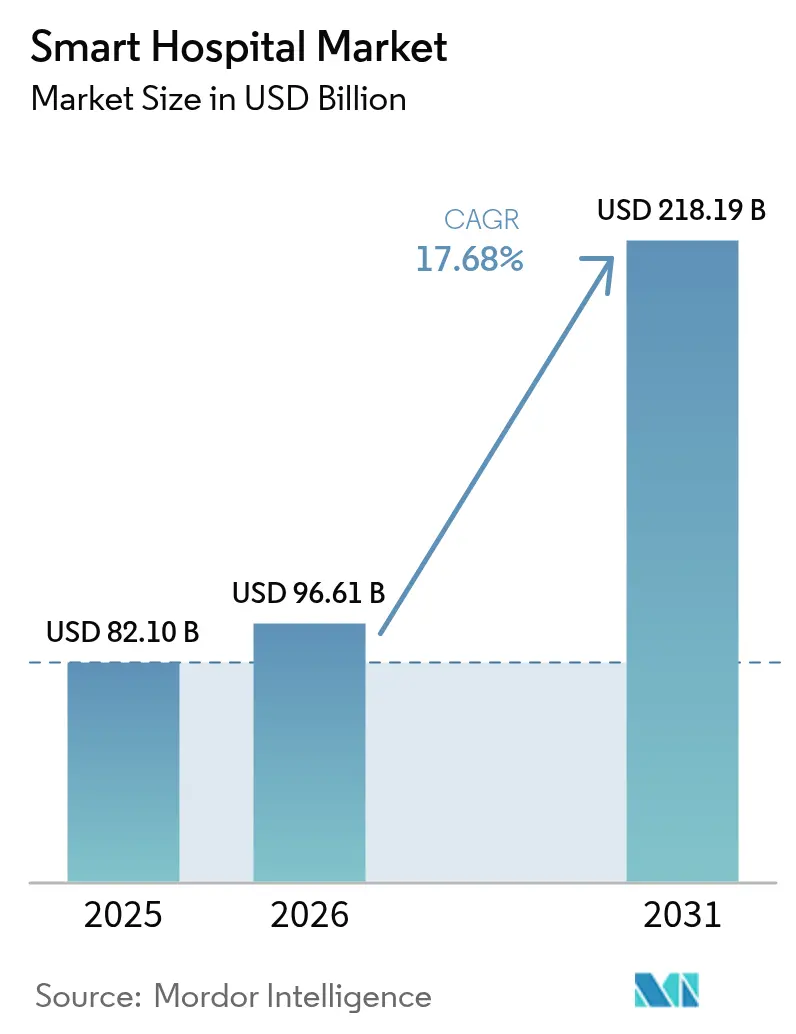

The Smart Hospital Market size was valued at USD 82.10 billion in 2025 and estimated to grow from USD 96.61 billion in 2026 to reach USD 218.19 billion by 2031, at a CAGR of 17.68% during the forecast period (2026-2031).

This expansion reflects accelerated digital transformation in healthcare, underpinned by infrastructure modernization and next-generation connectivity. Early 6G pilots reduce latency, permitting near-real-time analytics that reshape patient monitoring and clinical decision-making. [1]Frontiers in Medicine, “Clinical Applications of 6G Networks in Smart Hospitals,” frontiersin.orgHardware remains the largest component, yet services grow the fastest as hospitals shift from capital purchases to managed partnerships. Remote Patient Monitoring (RPM) outpaces Electronic Health Records (EHR) growth, signalling a move toward patient-centric, location-agnostic care. While North America leads in adoption, Asia-Pacific offers the most dynamic growth, driven by government stimulus and foundational digitisation efforts.

Key Report Takeaways

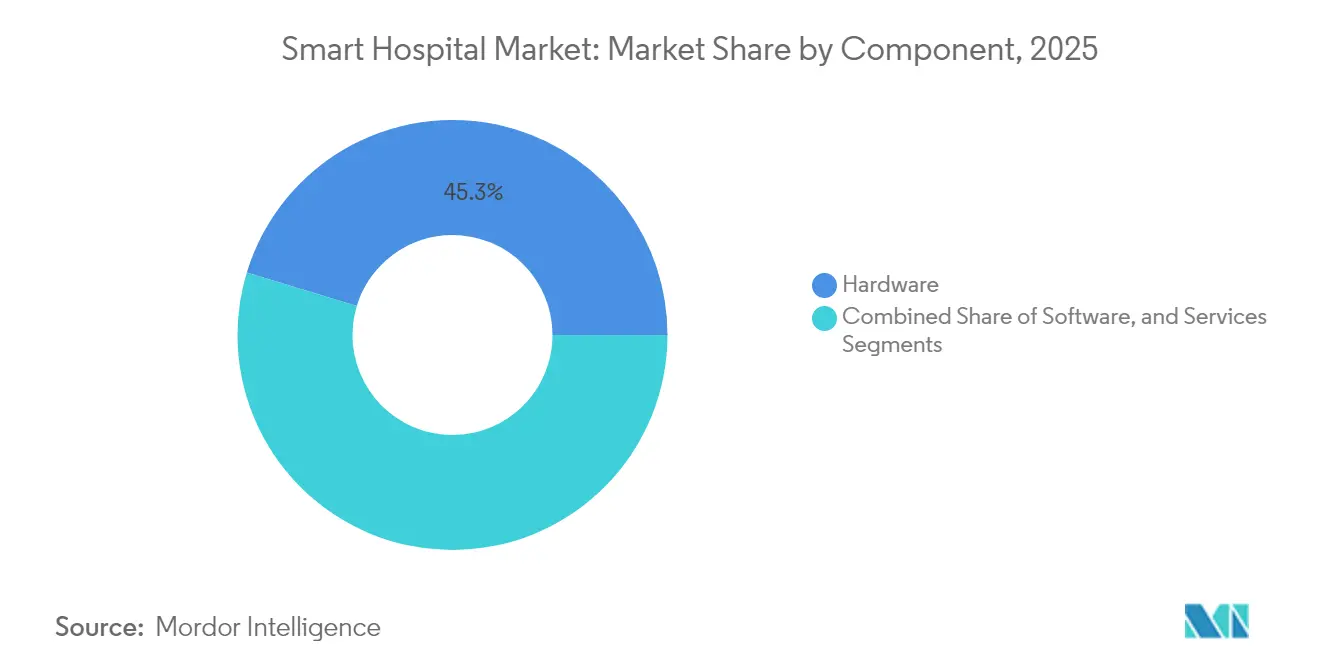

- By component, hardware held 45.30% of the smart hospital market share in 2025, whereas services are projected to expand at a 20.78% CAGR through 2031.

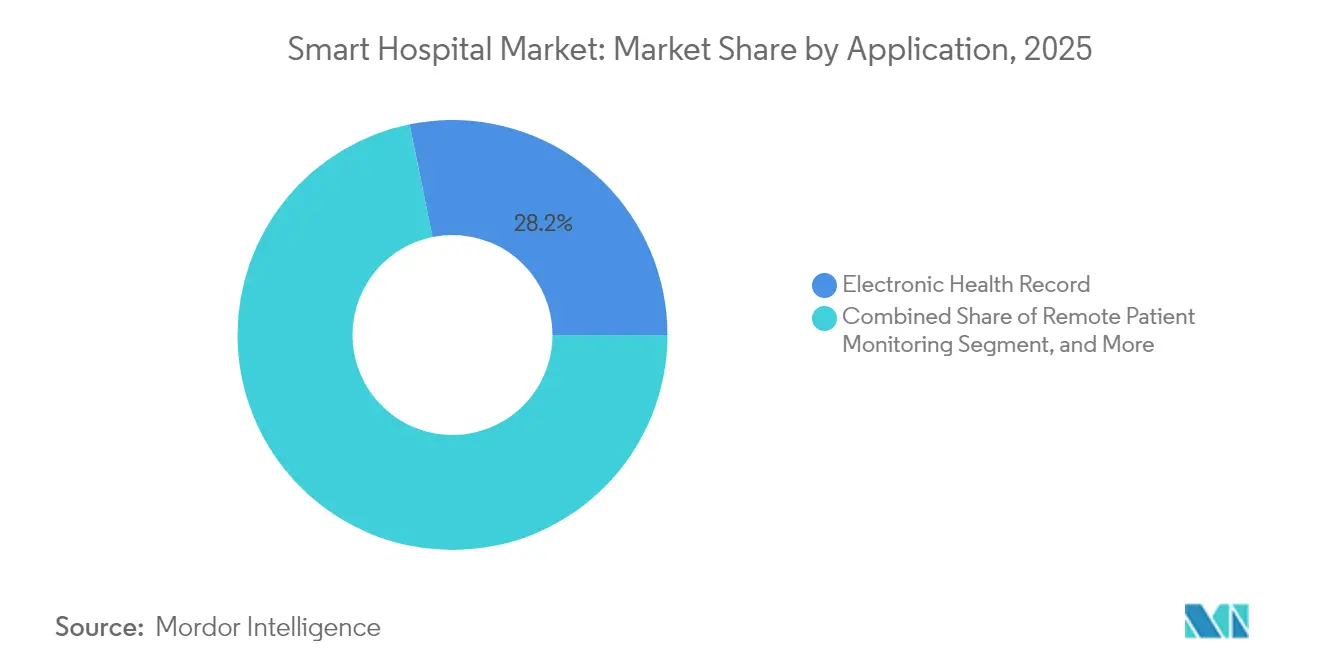

- By application, electronic health records led with a 28.20% revenue share in 2025 in the smart hospital market; remote patient monitoring is forecast to advance at a 22.05% CAGR to 2031.

- By geography, North America commanded 40.45% of the smart hospital market share in 2025 in the smart hospital market, while Asia-Pacific is set to grow at a 19.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Hospital Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Modernization of healthcare infrastructure | +4.2% | Global, with concentrated impact in North America and Europe | Medium term (2-4 years) |

| Surge in connected-device penetration | +3.8% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Government "smart-hospital" stimulus programs | +3.1% | Asia-Pacific core, particularly China, with spillover to emerging markets | Long term (≥ 4 years) |

| Corporate net-zero mandates driving smart-building retrofits | +2.4% | North America and EU, with selective adoption in APAC | Medium term (2-4 years) |

| Nursing-staff shortages accelerating virtual-care adoption | +2.9% | Global, most acute in North America and developed Asia-Pacific markets | Short term (≤ 2 years) |

| 6G-ready network pilots enabling near-real-time analytics | +1.6% | Limited to advanced markets: US, EU, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Modernisation of Healthcare Infrastructure

Modernisation funding anchors the current growth phase. The American Rescue Plan apportioned USD 1 trillion for healthcare facilities, including a USD 452 million North Texas State Hospital and a USD 855 million Utah medical campus. New York’s USD 188 million Safety Net Transformation Programme targets EHR integrations, confirming government reliance on technology-enabled upgrades.[2]Healthcare IT News, “New York Invests USD 188 Million in Hospital Tech Upgrades,” healthcareitnews.comHospitals also invest in digital backbones to handle sensor data, automated lighting, and predictive maintenance. These end-to-end upgrades displace piecemeal fixes, creating robust demand across the smart hospital market. Vendors able to bundle infrastructure, software, and services gain a competitive cost-of-ownership edge.

Surge in Connected-Device Penetration

Smart hospitals increasingly rely on IoT-enabled devices that produce high-volume clinical data. Samsung Medical Centre’s HIMSS Quadruple Stage 7 certification shows efficiency gains when device data integrates seamlessly. West Health Institute estimates that better device interoperability could save USD 30 billion each year by cutting redundant testing. This incentive drives hospital procurement toward platforms that unify data flows. While device proliferation raises interoperability hurdles, vendor consolidation and open protocols are easing integration. Accelerating device adoption, therefore, boosts the smart hospital market while spurring standards-based ecosystems.

Government Smart-Hospital Stimulus Programmes

China’s Trinity policy embeds smart medicine, services, and management into hospital build-outs, illustrating the economic scale achievable through cohesive national policy. The policy’s evaluation standards encourage unified electronic records, workflow optimisation, and skilled human resources. Similar momentum appears in Europe, where the incoming European Health Data Space could yield EUR 11 billion in savings. Coordinated stimulus quickens purchasing cycles, ensuring that the smart hospital market captures budgeted digital health outlays rather than competing with other capital projects.

Nursing-Staff Shortages Accelerating Virtual-Care Adoption

Acute workforce gaps quicken the shift to virtual nursing. At Guthrie Clinic, a virtual hub cut nurse turnover from 25% to 13% and saved USD 7 million in labour cost. Technology lets experienced nurses oversee multiple wards remotely, balancing workload and care quality. AI-ready EHR interfaces further streamline documentation, freeing bedside nurses for hands-on tasks. As staffing pressure intensifies, hospitals invest in tele-nursing platforms that scale expertise across facilities. This trend underpins sustained growth across the smart hospital market, especially for service providers offering turnkey virtual-care solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex of fully connected systems | -2.8% | Global, most pronounced in cost-sensitive emerging markets | Medium term (2-4 years) |

| Cyber-security and data-governance liabilities | -1.9% | Global, with heightened impact in regulated markets (US, EU) | Short term (≤ 2 years) |

| Inter-vendor interoperability gaps | -1.5% | Global, particularly acute in fragmented European markets | Medium term (2-4 years) |

| Limited digital-skills workforce in developing regions | -1.2% | Asia-Pacific emerging markets, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex of Fully Connected Systems

Comprehensive smart hospital roll-outs demand significant capital. Vendor-developed CPOE systems alone can cost USD 7.1 million to USD 19.3 million, with ROI horizons of eight years or more. Mid-sized hospitals struggle to meet these outlays amid margin pressure and supply chain inflation. Hardware, integration, training, and maintenance amplify total cost of ownership, favouring large networks that can amortise spending. Capital intensity thus slows adoption in emerging markets and rural facilities, tempering short-term growth in the smart hospital market.

Cyber-Security and Data-Governance Liabilities

Smart hospitals connect thousands of endpoints, each a possible attack vector. EU countries logged 309 major healthcare cyber incidents in 2023, highlighting systemic vulnerability. [3]European Commission, “Cybersecurity Incidents in EU Healthcare,” digital-strategy.ec.europa.eu Compliance with GDPR and HIPAA requires robust encryption, access control, and breach response capabilities. Security upgrades compete with clinical investments for budget share, and breach liabilities can exceed technology savings. As threat actors target high-value medical data, cybersecurity spending becomes an essential but growth-dampening cost for the smart hospital market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Services Disruption

Hardware generated the largest component revenue, securing 45.30% of the smart hospital market share in 2025 as hospitals installed servers, networking gear, imaging systems, and sensor arrays essential for digital operations. The smart hospital market size for hardware is projected to expand steadily, yet the services segment is growing faster at a 20.78% CAGR through 2031, reflecting demand for managed maintenance, analytics, and lifecycle support. Hospitals gravitate toward multi-year service contracts that convert capex to opex, ensuring predictable spend while accessing up-to-date expertise. Vendors such as Siemens Healthineers are expanding domestic manufacturing and service hubs to meet that need.

The services uptrend challenges hardware-centric revenue models. Providers bundle installation, remote monitoring, and AI-driven optimisation into outcome-linked agreements. This value shift boosts vendor lock-in yet lowers client operational risk. Software stands between the two, benefiting from cloud delivery that reduces onsite IT burden while enabling rapid feature deployment. Taken together, hardware reliability, smart software, and service depth create integrated propositions that shape competitive dynamics across the smart hospital market.

By Application: EHR Incumbency Challenged by RPM Innovation

Electronic Health Records retained a 28.20% revenue share in 2025, underlining their indispensable role in hospital digitisation. However, Remote Patient Monitoring recorded a 22.05% forecast CAGR, signalling a strategic pivot from internal process optimisation to patient-centric continuity of care. The smart hospital market size attached to RPM is expected to more than double from USD 16–17 billion in 2025 to more than USD 35 billion by 2031, aided by Medicare reimbursement codes.

RPM’s momentum arises from chronic disease prevalence, the aging population, and post-pandemic acceptance of home-based care. Hospital-at-home programmes have already cut inpatient costs by 30%, reinforcing the financial case for remote models. Meanwhile, EHR platforms add AI-powered tools to support diagnostics and workflow automation, defending incumbency. Pharmacy Automation and Medical Asset Tracking hold steady positions, yet emerging AI diagnostic platforms signal future growth pockets. Competition will intensify as device makers, cloud providers, and specialist startups vie for leadership across the smart hospital market.

Geography Analysis

North America captured 40.45% of the smart hospital market share in 2025, buoyed by mature infrastructure, federal stimulus, and strong vendor ecosystems. The American Rescue Plan’s USD 1 trillion healthcare allocation fuels facility upgrades, while programmes such as New York’s USD 188 million Safety Net Transformation advance EHR and emergency capabilities. Virtual nursing hubs, exemplified by Guthrie Clinic’s USD 7 million labour savings, demonstrate achievable returns on digital investments. Yet supply chain shortages cost an average of five-hospital networks USD 3.5 million, highlighting vulnerability.

Asia-Pacific is the fastest-growing region, projected at a 19.62% CAGR to 2031. China’s Trinity policy places smart medicine, services, and management at the core of hospital construction, with national smart healthcare value heading toward 150 billion yuan. Thailand’s Siriraj 5G Smart Hospital cut diagnosis time from 15 minutes to 25 seconds, showcasing the clinical impact of advanced connectivity. South Korea’s Samsung Medical Centre achieved HIMSS Quadruple Stage 7, setting a regional benchmark. Vendor collaborations, such as ZTE’s 5G IoT network with China Telecom, trimmed upgrade costs by 80% and build time by 90% ZTE.

Europe occupies a midway position, supported by the European Health Data Space, which could save EUR 11 billion over a decade. Cyber incidents remain a challenge, prompting a forthcoming Cybersecurity Support Centre. DIGITALEUROPE urges dedicated EU funding for digital health to ensure access to AI, telehealth, and interoperable data systems. With coordinated frameworks and funding, the region is poised for steady adoption, enhancing the long-term expansion of the smart hospital market.

Competitive Landscape

The smart hospital market displays moderate concentration anchored by diversified incumbents. Koninklijke Philips, GE Healthcare, and Siemens Healthineers merge hardware, software, and services into cohesive offerings that raise switching costs. EHR submarkets are consolidated around Epic Systems and Oracle Health, whereas RPM and AI diagnostics invite new entrants ranging from device manufacturers to tech giants. Large incumbents leverage scale to fund continuous R&D and regional service centers, securing relevance as hospitals demand integrated solutions.

Strategic alliances highlight AI as a differentiator. Philips and NVIDIA co-developed an MRI foundational model that enables zero-click scan planning. GE Healthcare partnered with AWS to inject generative AI into clinical workflows, aiming to streamline radiology interpretation. Siemens Healthineers’ USD 150 million US facility expansion strengthens local manufacturing for imaging and oncology devices.

Emerging players target niche gaps such as interoperability middleware, cybersecurity services, and specialty RPM platforms. Market entry barriers include regulatory certification, data-security compliance, and capital demand. Nonetheless, white-space innovations can scale rapidly through ecosystem partnerships. Competitive intensity is therefore poised to rise, promoting continual technology refresh cycles across the global smart hospital market.

Smart Hospital Industry Leaders

Koninklijke Philips N.V.

GE Healthcare ( General Electric)

Medtronic plc

Honeywell Life Care Solutions ( Honeywell International Inc)

Stanley Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Siemens Healthineers announced a USD 150 million investment in expanded US facilities, boosting imaging and oncology capacity.

- May 2025: Philips and NVIDIA unveiled an AI MRI foundational model that shortens scan times and automates image enhancement.

- April 2025: Tower Health and Siemens Healthineers formed a 10-year partnership to modernize diagnostic imaging across multiple sites.

- March 2025: GE Healthcare and NVIDIA expanded collaboration to develop autonomous ultrasound and X-ray solutions .

Global Smart Hospital Market Report Scope

The Smart Hospital market report provides detailed information regarding several segments of smart hospitals, such as hardware, software, and the solutions component. The report analyzes the smart hospital ecosystem and discusses Electronic Medical Records (EMRs), alarm management, research databases, and clinical decision support systems.

The Smart Hospital Market is Segmented by Component (Hardware, Software, and Services), Application (Electronic Health Record, Remote Patient Monitoring, Pharmacy Automation, Mobile Asset Tracking, and Other Applications), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

| Hardware |

| Software |

| Services |

| Electronic Health Record |

| Remote Patient Monitoring |

| Pharmacy Automation |

| Medical Asset Tracking |

| Other Applications |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Application | Electronic Health Record | |

| Remote Patient Monitoring | ||

| Pharmacy Automation | ||

| Medical Asset Tracking | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the smart hospital market?

The smart hospital market is valued at USD 96.61 billion in 2026.

Which component segment holds the largest share?

Hardware holds the largest component share at 45.30% in 2025.

Which application is growing the fastest?

Remote Patient Monitoring is projected to grow at a 22.05% CAGR between 2026 and 2031.

Which region is expected to grow most rapidly?

Asia-Pacific is forecast to expand at a 19.62% CAGR through 2031.

How do workforce shortages influence technology adoption

Nursing shortages accelerate investment in virtual-care platforms, which lower labour costs and maintain care quality.

What is a key restraint to smart hospital deployment?

High capital expenditure for fully connected systems slows adoption, particularly in cost-sensitive markets.

Page last updated on: