Slideway Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

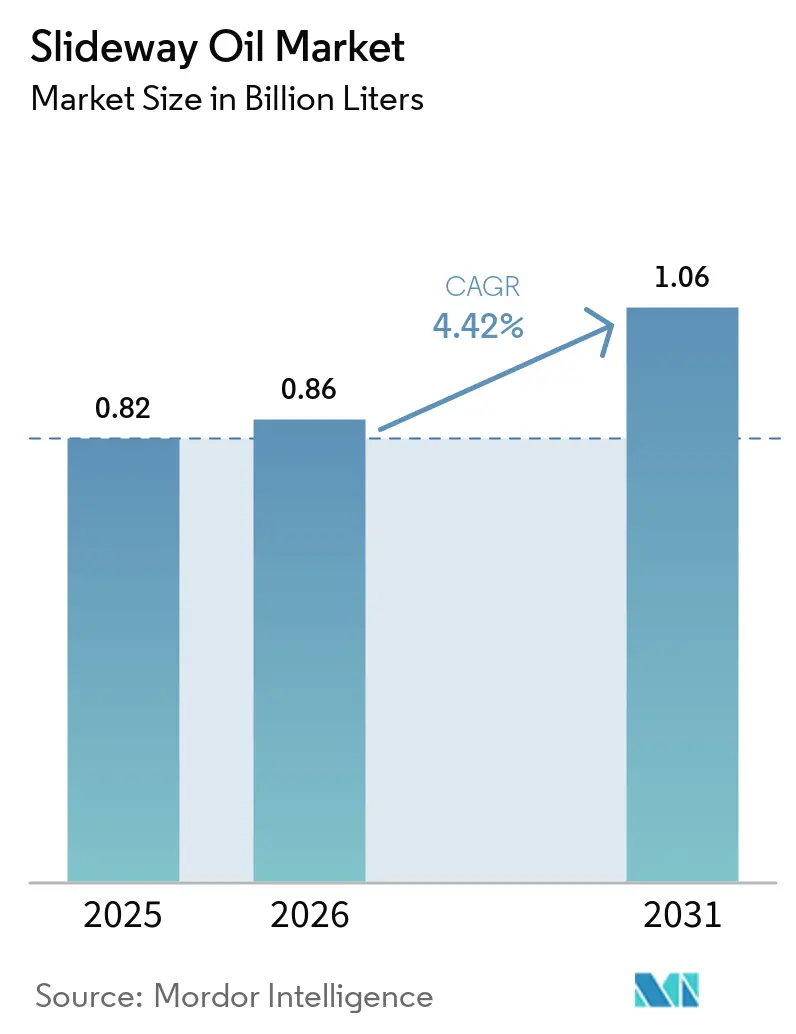

| Market Volume (2026) | 0.86 Billion liters |

| Market Volume (2031) | 1.06 Billion liters |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

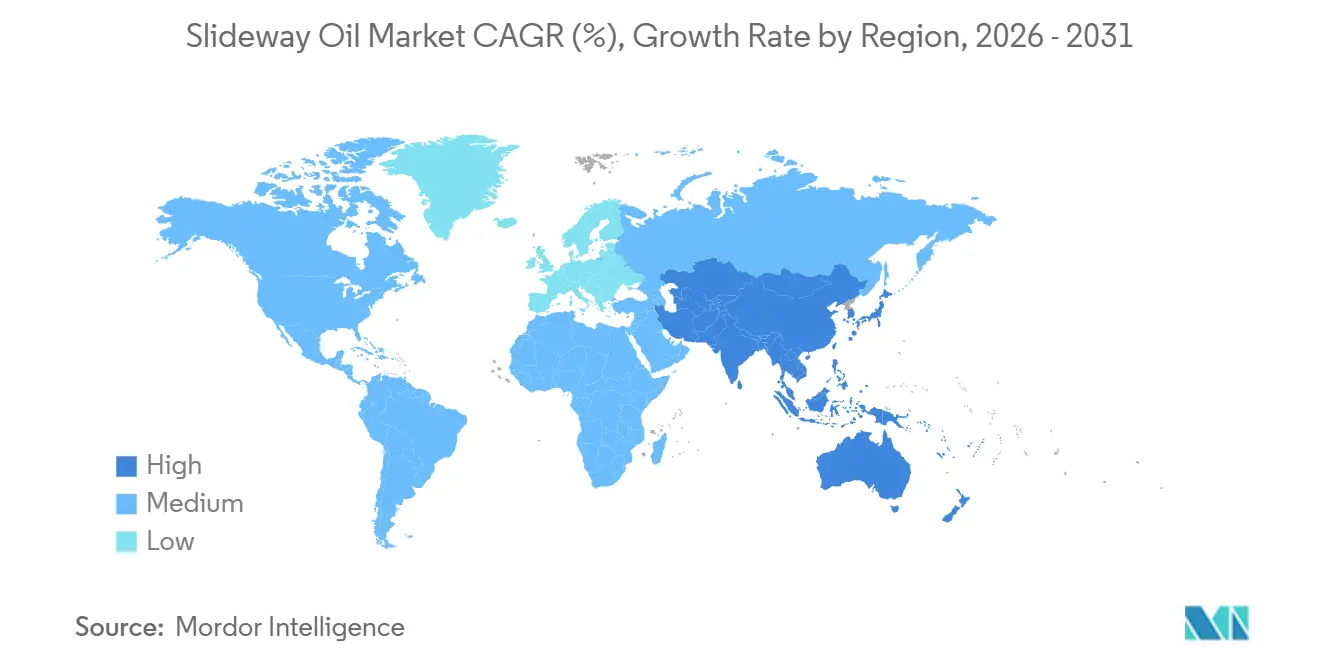

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slideway Oil Market Analysis by Mordor Intelligence

The Slideway Oil Market size was valued at 0.82 Billion liters in 2025 and is estimated to grow from 0.86 Billion liters in 2026 to reach 1.06 Billion liters by 2031, at a CAGR of 4.42% during the forecast period (2026-2031). Accelerating installation of five-axis machining centers across China, India, and Southeast Asia is driving baseline demand, while bio-based formulations are gaining traction as the European Chemicals Agency advances PFAS phase-out proposals. Integrated predictive-maintenance platforms are transforming competitive dynamics by shifting the focus from unit-price comparisons to total-cost-of-ownership discussions. Meanwhile, price-sensitive segments in Latin America and Africa continue to prefer Group II mineral blends, requiring global suppliers to balance high-value sustainability offerings with reliable low-cost supply.

Key Report Takeaways

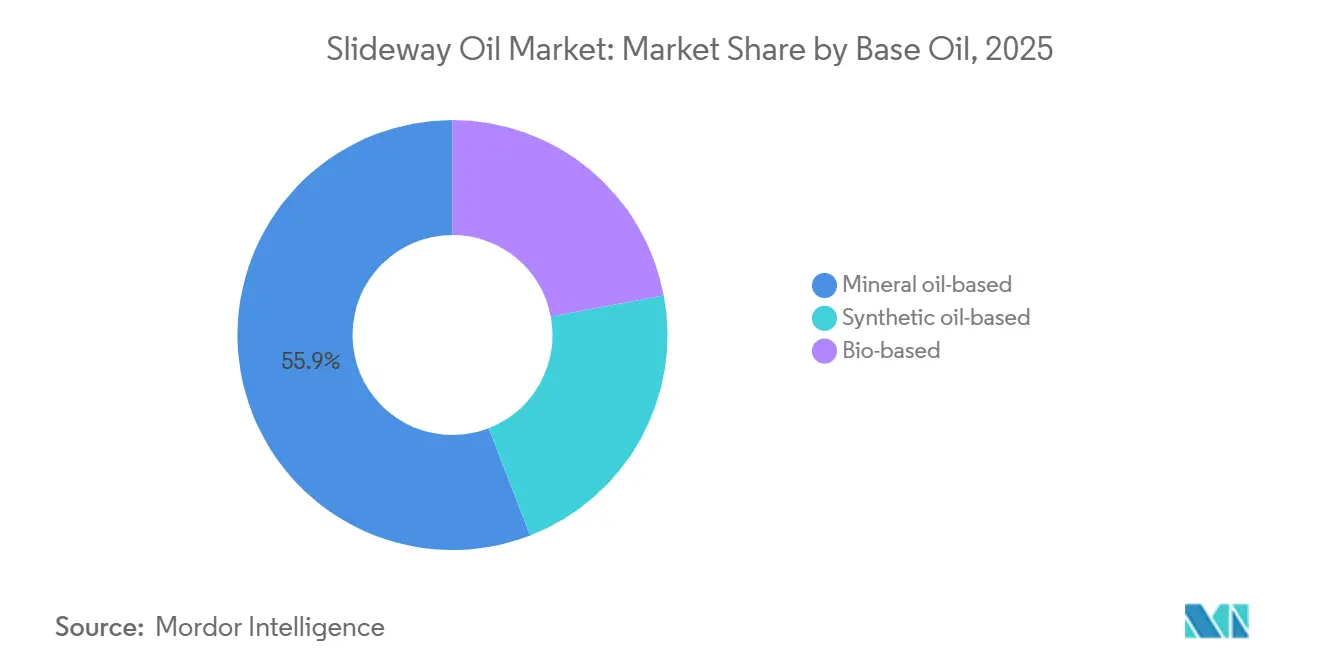

- By base oil, mineral oil-based commanded 55.89% of the slideway oil market share in 2025, while bio-based is set to expand at a 5.16% CAGR through 2031.

- By application, CNC machines captured 29.84% of the slideway oil market share in 2025 and will advance at a 5.05% CAGR through 2031.

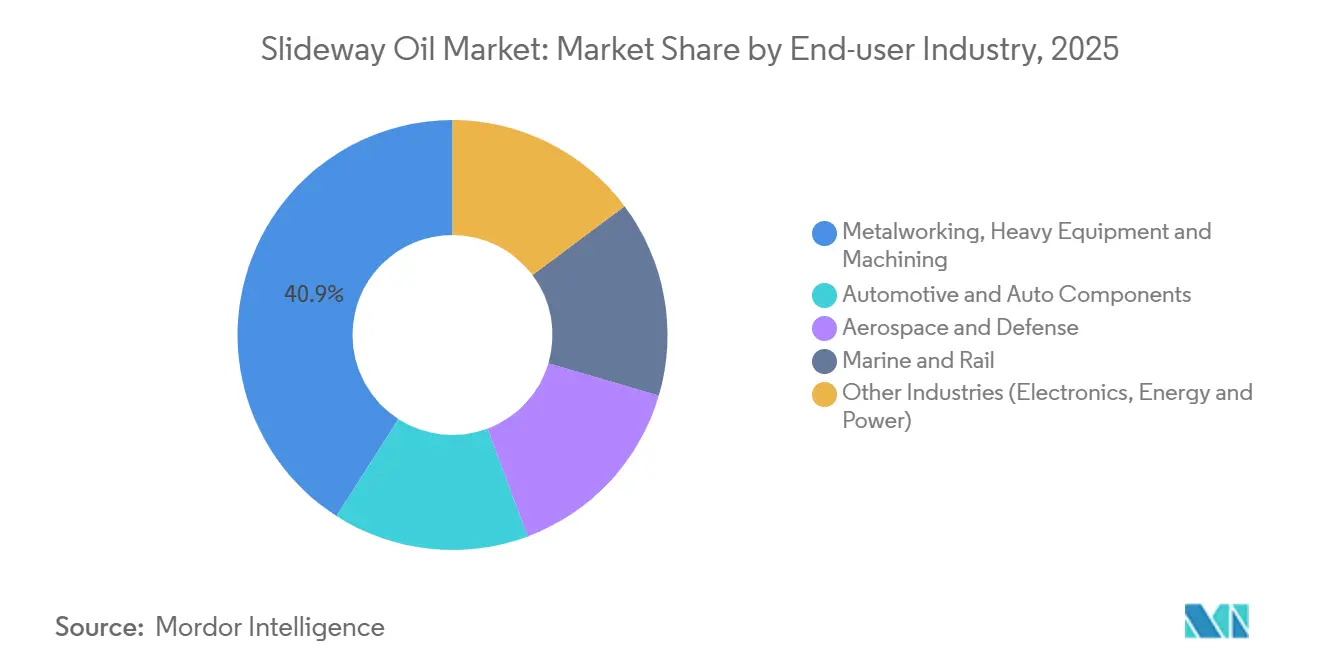

- By end-user industry, metalworking, heavy equipment and machining retained 40.92% of the slideway oil market share in 2025, while automotive and auto components are forecast to grow fastest at a 5.27% CAGR through 2031.

- By geography, Asia-Pacific held 47.57% of the slideway oil market share in 2025 and is projected to grow at a 5.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Slideway Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding precision machining and CNC penetration | +1.2% | Asia-Pacific core, spillover to North America and Europe | Medium term (2–4 years) |

| Accelerating metal-working output in emerging economies | +1.0% | Asia-Pacific (China, India, ASEAN), Mexico | Short term (≤ 2 years) |

| Industry 4.0 investments in automated tool rooms | +0.8% | Global, concentrated in Germany, Japan, United States, South Korea | Medium term (2–4 years) |

| Surge in retrofit/maintenance of ageing slideway beds | +0.6% | North America and Europe (legacy installed base), Japan | Long term (≥ 4 years) |

| Tightening VOC-emission rules favouring bio-based slideway fluids | +0.9% | Europe and North America, emerging in China | Long term (≥ 4 years) |

| IIoT-enabled smart-lubrication demand for condition-based dosing | +0.7% | Global, early adoption in automotive and aerospace clusters | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Expanding Precision Machining and CNC Penetration

China shipped 700,000 machine-tool units in 2024, setting a benchmark for future lubricant volumes as each new five-axis center requires low-migration slideway oil. FANUC’s USD 1.2 billion Chongqing expansion and TRUMPF’s Connecticut smart factory highlight similar growth trends in North America, reflecting the global demand for high-accuracy beds with closed-loop lubrication systems compatible with automated pallet changers. The increasing adoption of compact CNC lathes in Vietnam and Indonesia is further expanding the installed base, boosting replacement consumption, and encouraging suppliers to introduce synthetic-ester blends that extend drain intervals by 30–40%.

Accelerating Metal-Working Output in Emerging Economies

India’s INR 100 billion machine-tool production and Mexico’s USD 36 billion in nearshoring inflows are driving demand for slideway oils that ensure reliable film formation in humid, high-temperature environments. At the same time, China’s CNY 30.8 trillion machinery industry continues to rely on demulsifying formulations that prevent sump contamination in shared-fluid CNC cells. Suppliers offering oil-analysis services alongside product sales are securing multi-year maintenance contracts, insulating themselves from spot-price competition.

Industry 4.0 Investments in Automated Tool Rooms

Partnerships such as FUCHS-KCF integrate vibration analytics with customized dosing systems, enhancing lubricant performance from a cost consideration to a critical reliability factor. Castrol and Schaeffler are adopting similar approaches, embedding viscosity and contamination sensors directly into guide-rail circuits. Formulators unable to provide cloud dashboards or API feeds risk losing relevance regardless of the quality of their chemistry.

Tightening VOC-Emission Rules Favoring Bio-Based Slideway Fluids

The European Chemicals Agency’s 2026 PFAS evaluation targets 1,666 metric tons of fluorinated additives and accelerates the shift to ester-based chemistries[1]European Chemicals Agency, “Restriction Report on PFAS in Lubricants,” echa.europa.eu. Life-cycle studies by the Royal Society of Chemistry report 41–84% greenhouse-gas savings for bio-based lubricants, supporting OEM decarbonization mandates. TotalEnergies’ CARTER BIO 150, which meets EU Ecolabel thresholds, demonstrates how suppliers are translating regulatory changes into a competitive advantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-linked volatility in base-oil prices | -0.8% | Global, acute in regions dependent on Group I/II imports | Short term (≤ 2 years) |

| Chemical incompatibility with water-miscible metal-working fluids | -0.5% | Global, concentrated in CNC machining and grinding applications | Medium term (2–4 years) |

| Stringent disposal and REACH/EPA compliance costs | -0.4% | Europe and North America | Long term (≥ 4 years) |

| Adoption of dry/self-lubricating linear-motion polymers | -0.6% | Global, early adoption in clean-room and food-processing sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Linked Volatility in Base-Oil Prices

In the fourth quarter of 2025, the U.S. Producer Price Index for lubricants reached its lowest level since 2021. However, unplanned outages in the Middle-East subsequently tightened supply and drove up spot prices, squeezing margins for formulators without hedging programs. A 10% fluctuation in Brent crude prices translates to a 6–8% shift in base-oil costs, prompting Sinopec to invest in a 30,000 tpa metallocene PAO plant to reduce reliance on crude benchmarks for premium supply.

Chemical Incompatibility with Water-Miscible Metalworking Fluids

Even a small amount of water, such as 0.5% in slideway oil, can reduce tool life by 15–20%, while 2–3% oil in coolant increases bacterial growth and disposal costs. As a result, formulators prioritize demulsification times under 30 minutes per ASTM D1401 standards. FUCHS’s RENEP CGLP meets this requirement but requires careful additive balancing to maintain extreme-pressure performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base Oil: Bio-Based Formulations Gain Despite Mineral Dominance

Mineral oil-based represented 55.89% of the slideway oil market share in 2025, with synthetic PAO and ester blends serving high-temperature applications. The bio-based segment is anticipated to grow at a CAGR of 5.16% through 2031, surpassing all other base oil categories. Products such as Shell PANOLIN and TotalEnergies BIOHYDRAN illustrate that certified biodegradable oils can maintain extreme-pressure performance while reducing CO₂ life-cycle emissions by up to 84%.

Nevertheless, high feedstock costs and the limited availability of HEES-certified fluids above ISO VG 320 hinder adoption in heavy-duty vertical slideways. Expanding the production of epoxidized-soybean and tall-oil esters could help bridge the price gap with Group II mineral oils by 2029.

By Application: CNC Machines Drive Volumetric and Innovation Leadership

CNC machines accounted for 29.84% of the slideway oil market share in 2025 and are projected to grow at a CAGR of 5.05% through 2031. This growth is supported by retrofits that incorporate closed-loop lubrication systems and IIoT-based condition monitoring. Horizontal beds primarily utilize high-viscosity ISO VG 220–320 oils with tackifiers, while vertical slideways are increasingly adopting synthetic esters for improved performance at low temperatures.

Grinders require oils with strong demulsifying properties to operate effectively alongside high-velocity coolants, as demonstrated by Blaser’s Blasogrind GTS 15 case study, which achieved a 25% reduction in cycle time in Japan. Clean-room metrology tools demand PFAS-free, low-outgassing blends, creating a niche market for premium suppliers.

By End-user Industry: Automotive Components Outpace Metalworking Incumbents

Metalworking, heavy equipment and machining industry held a dominant 40.92% market share in 2025. However, the automotive and auto components segment is expected to grow at the fastest rate, with a CAGR of 5.27% through 2031, driven by the expansion of battery tray and motor housing production in Mexico and India. Aerospace applications offer high unit margins due to stringent OEM approval cycles and the challenges of superalloy machining, which require specialized lubricant clean-down processes. Marine and rail industries are increasingly adopting biodegradable grades to meet environmental compliance requirements near ports and waterways, supporting the growth of bio-based formulations despite their higher costs.

Geography Analysis

Asia-Pacific accounted for 47.57% of the slideway oil market share in 2025 and is projected to grow at a CAGR of 5.23% through 2031, supported by China’s machine-tool production of 700,000 units and India’s growing export machining clusters. North America benefits from USD 239 billion in U.S. manufacturing construction, with EPA Risk Management Plan revisions encouraging the adoption of bio-based products[2]U.S. Census Bureau, “Construction Spending Highlights 2024,” census.gov. Europe, while facing mixed machine-tool order volumes, leads in regulatory advancements, positioning it as a hub for PFAS-free innovations. The Middle-East and Africa, though starting from a smaller base, are attracting tailored solutions through partnerships like Quaker Houghton-Petrolube, which localizes blending for high-temperature environments.

Competitive Landscape

The slideway oil market is moderately fragmented, with integrated oil majors leveraging refining scale and specialty formulators focusing on application engineering and smart-maintenance solutions. BP’s 2025 review of Castrol highlights potential market consolidation, while FUCHS’s global capacity expansions and digital partnerships emphasize service-oriented differentiation. Entry barriers are increasing due to the high costs of REACH and EPA certifications, ranging from USD 50,000 to 200,000 per SKU, favoring established players with diversified portfolios capable of absorbing compliance costs.

Slideway Oil Industry Leaders

Chevron Corporation

FUCHS

Shell plc

Exxon Mobil Corporation

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: TotalEnergies acquired the Finnish company Tecoil to enhance the use of regenerated base oils (RRBOs) in premium lubricant formulations. This development contributed to the slideway oil market by increasing the availability of sustainable and high-performance base oils used in its production.

- September 2024: The XCMG and Shell plc formed a strategic partnership to introduce specialized lubricants aimed at enhancing machinery efficiency, extending equipment lifespan, and reducing downtime. This collaboration, which utilized Shell's advanced lubricant technology and production at their Derince facility, was relevant to the slideway oil market as it addressed the lubrication needs of heavy-duty machinery.

Global Slideway Oil Market Report Scope

Slideway oil is a specialized lubricant used for machine tool slideways, linear guides, and ball screws to ensure smooth and precise motion by preventing "stick-slip." It contains tackiness agents and friction modifiers, which help maintain a consistent lubricating film, even on vertical surfaces, thereby improving component longevity and precision.

The Slideway Oil Market is segmented into base oil, application, end-user industry, and geography. By base oil, the market is segmented into mineral oil-based, synthetic oil-based, and bio-based. By application, the market is segmented into CNC machines, horizontal slideways, vertical slideways, grinders, lathes, and other applications (e.g., clean-room tools). By end-user industry, the market is segmented into metalworking, heavy equipment and machining, automotive and auto components, aerospace and defense, marine and rail, and other industries (e.g., electronics, energy, and power). The report also covers the market size and forecasts for slideway oil in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

| Mineral oil-based |

| Synthetic oil-based |

| Bio-based |

| CNC Machines |

| Horizontal Slideways |

| Vertical Slideways |

| Grinders |

| Lathes |

| Other Applications (clean-room tools, etc.) |

| Metalworking, Heavy Equipment and Machining |

| Automotive and Auto Components |

| Aerospace and Defense |

| Marine and Rail |

| Other Industries (Electronics, Energy and Power) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Base Oil | Mineral oil-based | |

| Synthetic oil-based | ||

| Bio-based | ||

| By Application | CNC Machines | |

| Horizontal Slideways | ||

| Vertical Slideways | ||

| Grinders | ||

| Lathes | ||

| Other Applications (clean-room tools, etc.) | ||

| By End-user Industry | Metalworking, Heavy Equipment and Machining | |

| Automotive and Auto Components | ||

| Aerospace and Defense | ||

| Marine and Rail | ||

| Other Industries (Electronics, Energy and Power) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the slideway oil market?

The slideway oil market stands at 0.86 billion liters in 2026 and is projected to reach 1.06 billion liters by 2031.

How fast is bio-based sideways oil through 2031?

Bio-based sideways oil is projected to rise at a 5.16% CAGR through 2031.

Which region is showing the strongest demand growth through 2031?

Asia-Pacific leads with a 5.23% CAGR through 2031, thanks to expanding machine-tool output in China, India, and ASEAN countries.

How do IIoT-enabled lubrication systems reduce unplanned downtime?

Sensor-equipped pumps track vibration, temperature, and oil quality in real time, predict degradation up to two weeks in advance, and dose only what is needed, cutting unexpected stoppages that can cost up to USD 50,000 per production hour.

Page last updated on: