Compressor Oil Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Volume (2026) | 494.38 Million liters |

| Market Volume (2031) | 609.33 Million liters |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

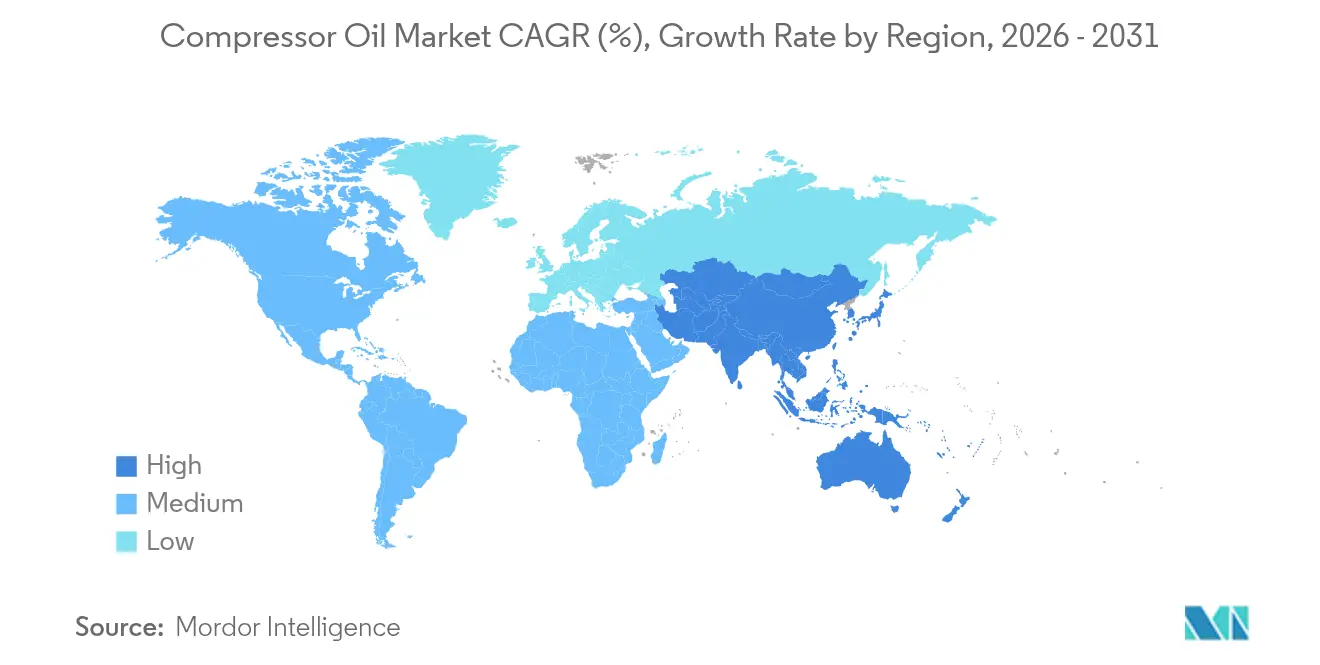

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

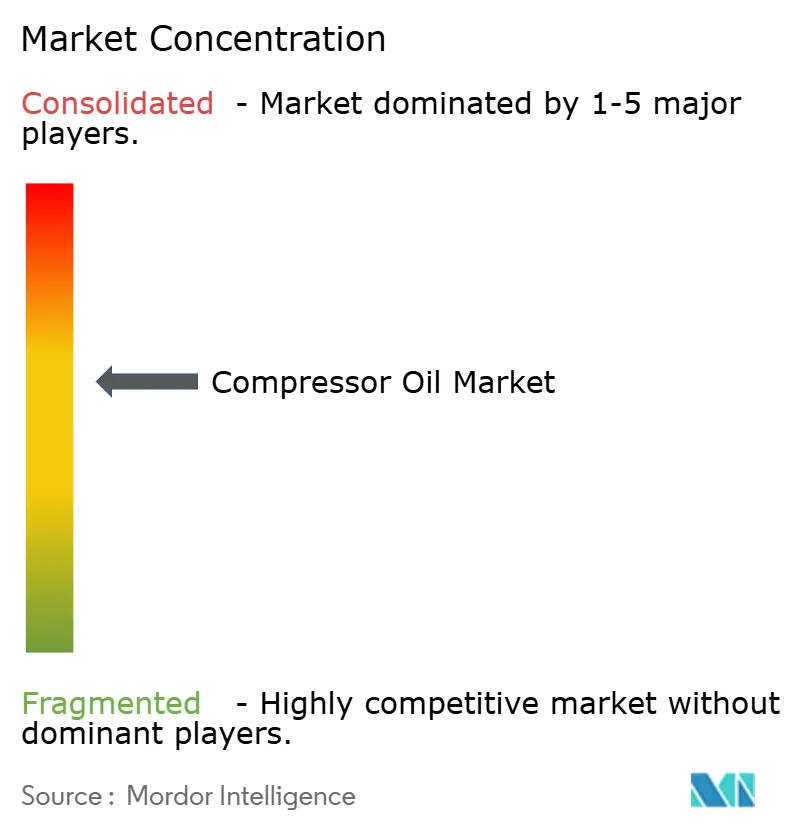

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compressor Oil Market Analysis by Mordor Intelligence

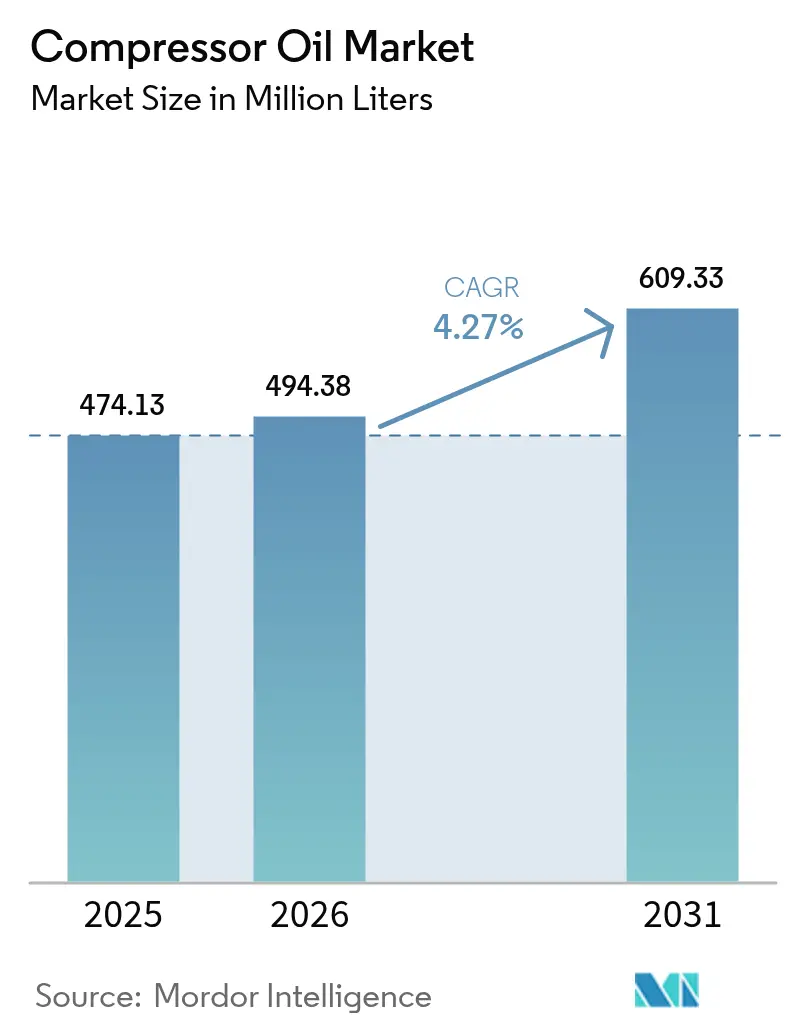

The Compressor Oil Market size was valued at 474.13 Million liters in 2025 and estimated to grow from 494.38 Million liters in 2026 to reach 609.33 Million liters by 2031, at a CAGR of 4.27% during the forecast period (2026-2031). The three strongest growth levers driving volume and value expansion are accelerated factory automation in Asia-Pacific, the pivot toward premium synthetic lubricants, and new hydrogen compression projects. Even though oil-free compressor technology is gaining momentum, most industrial users favor lubricated machines because extended-drain-interval synthetic oils now offset downtime costs and support rising efficiency mandates. Crude-linked base-oil price volatility remains a short-term headwind, yet suppliers are defending margins by emphasizing value-added formulations that lower the total cost of ownership. Overall, the compressor oils market is expected to preserve moderate concentration as multinational majors compete with niche regional providers focused on specialized applications.

Key Report Takeaways

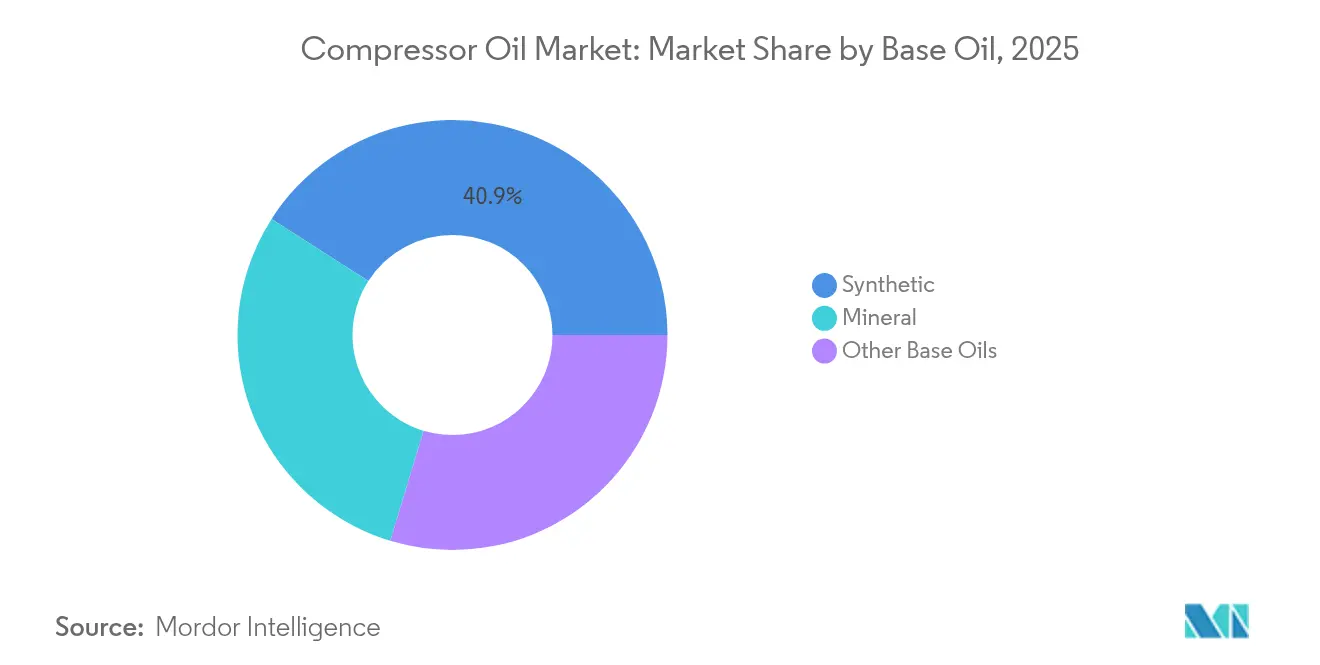

- By base oil, synthetic fluids captured 40.92% of the 2025 volume; other base oils are projected to expand at a 5.18% CAGR through 2031.

- By compressor type, positive displacement equipment held 64.05% of 2025 volume, whereas dynamic compressors are forecast to grow at 5.32% CAGR during the forecast period (2026-2031).

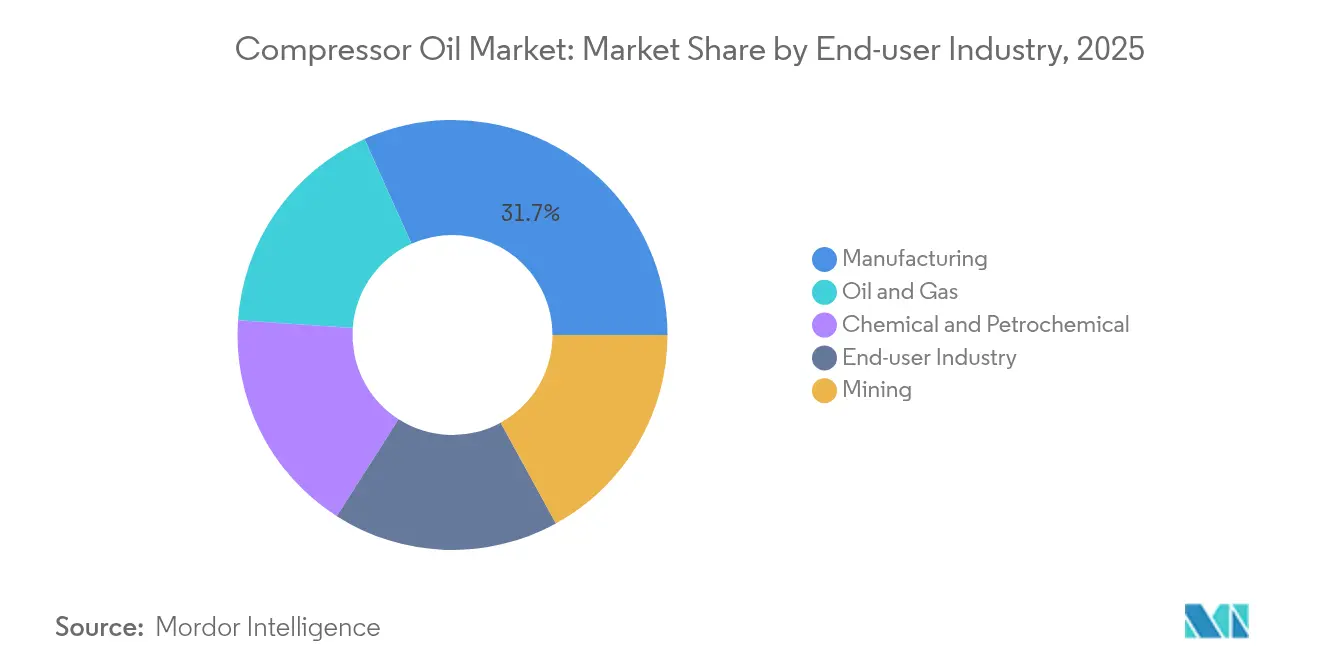

- By end-user industry, manufacturing accounted for 31.72% share in 2025, yet oil and gas is expected to record the fastest 5.11% CAGR to 2031.

- By application, air compressors dominated with a 75.62% share in 2025, while gas compressor demand should rise at a 5.14% CAGR through 2031.

- By geography, Asia-Pacific commanded 37.86% of the Compressor Oils market share in 2025 and is on track for the highest 5.03% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compressor Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Manufacturing Boom Boosting Compressed-air Systems | +1.2% | Global – APAC core | Medium term (2-4 years) |

| Shift to Synthetic Oils for Energy-efficient, High-temperature Operations | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Expansion of Oil and Gas Mid-stream Compression Capacity | +0.6% | North America, Middle East | Medium term (2-4 years) |

| Hydrogen Compression Projects Needing Embrittlement-Resistant Lubricants | +0.4% | EU & North America | Long term (≥ 4 years) |

| Ultra-low-viscosity Polyalphaolefin (PAO) Blends for EV Thermal-management Compressors | +0.3% | Global EV hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Manufacturing Boom Boosting Compressed-air Systems

Global industrial automation programs lift demand for variable-speed drive compressors that cut energy use while slashing maintenance costs, particularly across Asian production corridors. The United States Department of Energy’s new rotary air-compressor efficiency rule, effective January 2025, compels original equipment manufacturers (OEMs) to lift isentropic efficiency, indirectly raising lubricant performance requirements [1]U.S. Department of Energy, “Energy Conservation Standards for Air Compressors,” energy.gov. Factories deploying Internet of Things (IoT) monitoring platforms want oils with viscosity and film strength under fluctuating loads, encouraging migration to premium synthetics. Air compressor sales, forecast to escalate, have a one-to-one correlation with lubricant consumption, especially in the Internet of Things (APAC), where capital investment in manufacturing remains robust. The growing use of heat-recovery modules in compressor stations pushes bulk oil temperatures higher, necessitating oxidation-resistant formulations that preserve equipment life.

Shift to Synthetic Oils for Energy-efficient, High-temperature Operations

Polyalphaolefin (PAO) and ester fluids are gaining traction because longer drain intervals shrink downtime, even though the acquisition price is higher. ExxonMobil’s Singapore Resid Upgrade Project will commission EHC 340 MAX basestock in 2025, bolstering global supply security for premium-grade synthetics. Trials of tungsten-disulfide nano-additives in rotary screw units have recorded specific-energy cuts exceeding 5%, a gain that translates directly to lower Scope-1 emissions for industrial users. European Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) rules restrict high-sulfur aromatic constituents, nudging blenders toward cleaner synthetic chemistries that satisfy air-quality mandates. Hybrid additive packages with fullerene doses below 50 ppm are emerging, demonstrating marked friction reduction in refrigerant and process-gas compressors, which further accelerates the compressor oils market preference for synthetics.

Expansion of Oil and Gas Mid-stream Compression Capacity

A wave of North American gas-processing builds, typified by Phillips 66’s 300 MMcfd (million cubic feet per day) Iron Mesa plant in Texas, directly lifts lube demand for high-pressure screw and reciprocating units. Targa Resources’ Permian Basin network now totals 8.8 bcfd (billion cubic feet per day) across 43 plants, highlighting the scale of compression horsepower entering service and fueling the compressor oils market. Sour-gas streams accelerate corrosive wear, so operators adopt fortified additive systems that extend mean-time-between-overhauls from 2,000 hours to as high as 10,000 hours. Major Middle-East ethane crackers, such as QatarEnergy’s 2.08 million tpy (tons per year) Ras Laffan unit, reinforce global demand for continuous-duty centrifugal machines lubricated by high-VI synthetic blends. Novel compressed-air energy-storage facilities add another growth pocket because charge-discharge cycling requires oils with strong shear stability across repeated pressure swings.

Hydrogen Compression Projects Needing Embrittlement-resistant Lubricants

Emerging hydrogen corridors mandate fluids that resist hydrogen permeation under 1,000-bar discharge pressures, a niche that mineral oils cannot satisfy. Oil-free reciprocating packages with nitrogen barriers remove contamination risks, yet many projects still select lubricated technology, provided a specialty formulation prevents metal embrittlement. Fuel-cell electric-vehicle refueling stations need compact boosters whose crankcase oils must tolerate moisture ingress and elevated temperatures. Ionic-liquid prototypes show promise for oxygen-rich compression service where flammability is critical, signifying future competitive pressure on traditional base stocks. Anticipated hydrogen-specific standards inside the European Union (EU) framework will likely codify these performance thresholds, imposing entry barriers that favor high-end suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Oil-free Compressor Technology | -0.7% | Global, with faster adoption in pharmaceuticals and food processing | Medium term (2-4 years) |

| Crude-linked Volatility in Base-oil Prices | -0.4% | Global, with higher impact in price-sensitive markets | Short term (≤ 2 years) |

| Longer Drain-Interval Programs Lowering Lubricant Consumption Intensity | -0.6% | North America & EU primarily, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Oil-free Compressor Technology

Pharmaceutical and food plants accelerate oil-free purchases to meet International Organization for Standardization (ISO) 8573-1 Class 0 air specs, eliminating any contamination pathway. Variable-speed drives and active-magnetic bearings have lifted the reliability of dry machines, opening prospects in segments once dominated by lubricated designs. Mitsubishi Electric earmarked USD 143.5 million for a Kentucky heat-pump compressor factory targeting 1 million units per year by 2027, underscoring the scale potential for oil-less scroll and rotary models [2]Mitsubishi Electric Corporation, “Kentucky Heat Pump Compressor Plant Announcement,” mitsubishielectric.com. Rail-freight trials validate technical feasibility, yet mobile duty cycles present thermal-shock hurdles that keep lubricated units relevant in locomotives. Operators weigh higher capex against lifetime savings from filter replacements and oil purchase avoidance, creating a measured but steady drag on volumetric growth in the compressor oils market.

Crude-linked Volatility in Base-oil Prices

Base-oil postings mirror Brent swings, compressing blender margins and escalating procurement risk for price-sensitive buyers. Spot spikes prompt some operators to stretch change intervals, deferring consumption in the short term. Integrated majors partly hedge exposure through Group II and Group III slate diversity, but independent formulators face tighter working-capital strain. Renewed geopolitical tension has widened the crack spread for vacuum gas-oil, lifting feedstock costs that flow into compressor oils market prices. Distributors cushion volatility by converting clients to extended-life synthetics that smooth annual budgeting despite higher unit cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base Oil: Synthetic Dominance Drives Premium Positioning

The Compressor Oil market size tied to synthetic fluids accounted for 40.92% of the 2025 volume, owing to superior oxidation resistance that extends drain schedules and lowers unscheduled downtime. Mineral oils still hold bulk-volume leadership in cost-sensitive settings, yet their share erodes as lifecycle economics favor synthetics. Semi-synthetic blends offer a midway option and appeal in regions where upfront budget constraints remain acute but reliability demands are rising. Bio-based entrants achieve niche traction where biodegradability mandates exist, although cold-flow limitations restrict widespread substitution.

End-user trust in polyalphaolefin chains stems from consistent viscosity index near 140, safeguarding bearing films at 115°C discharge temperatures common in manufacturing automation lines. Nano-additive work with tungsten-disulfide and graphene platelets enhances thermal conductivity, shaving sump temperatures by 3°C during stress tests, directly supporting higher mean-time-between-overhaul targets. ExxonMobil’s Singapore expansion, adding 20,000 bpd (barrels per day) of premium basestock, signals a supply commitment that should stabilize pricing as synthetic demand scales. Other base-oil categories, especially advanced esters, are projected to record a 5.18% CAGR because environmental legislation steers fleets toward lower volatile organic compound (VOC) profiles.

By Compressor Type: Positive Displacement Maintains Industrial Leadership

Positive displacement machines, such as rotary screws and reciprocating designs, held 64.05% of 2025 shipments due to ubiquity in factory compressed-air loops that operate under fluctuating duty cycles. These systems require oils with robust anti-wear and demulsibility properties to protect internal rotors, gears, and seals. Reciprocating variants run on splash or pressure feed and endure elevated cross-head temperatures, making additive stability crucial to mitigate carbon deposits.

Given large process-gas volumes in petrochemical and liquefied natural gas (LNG) applications, dynamic compressors, predominantly centrifugal units, will grow the fastest at a 5.32% CAGR. Hydrodynamic bearings demand low foaming potential and high film strength under continuous full-load operation. Hybrid “integrally geared” architectures marry displacement attributes with dynamic staging, enabling operators to broaden turn-down ratios. Although oil-free centrifugal models cut lubricant consumption altogether, many high-pressure lines use flooded bearings where formulated synthetics guard against varnish under high-speed conditions.

By Application: Air Compressors Dominate Despite Gas Growth

Air-compressor application absorbed 75.62% of the total 2025 demand, as essentially every factory maintains one or more screw units for pneumatic tools and automation cylinders. Efficiency regulations promulgated by the United States Department of Energy require lubricants that sustain viscosity at reduced operating pressures and temperatures. Thermal-stable synthetics extend maintenance intervals, directly boosting productivity metrics for the compressor oils market.

Gas-compressor use will expand at 5.14% CAGR to 2031 as LNG terminals, midstream trunk lines, and hydrogen refueling stations scale. Fluids must confront higher discharge pressures and chemically aggressive gases, so formulators include robust anti-rust, anti-foam, and metal-deactivator packages. Compressor oils market size for gas service is poised to grow faster than air applications because each centrifugal train often holds hundreds of liters, magnifying volume pull with every new plant approval.

By End-user Industry: Manufacturing Leads While Oil & Gas Accelerates

Manufacturing retained 31.72% volume share in 2025, reflecting heavy dependence on compressed-air infrastructure for assembly, machining, and electronics fabrication. Digitally controlled variable-speed drives fine-tune output, but also require oils with shear-stable viscosity to preserve rotor clearances across dynamic loads.

The oil and gas sector is forecast for a 5.11% CAGR through 2031, the steepest among end-users, because midstream processors and petrochemical complexes are adding capacity that depends on both screw and centrifugal compression. Sour-gas handling intensifies additive demand for anti-corrosion inhibitors, and hydrogen-rich streams necessitate embrittlement-resistant chemistries. Mining, heating, ventilation, and air conditioning (HVAC), and refrigeration verticals remain solid secondary contributors: HVAC is shifting to A2L refrigerants, which need polar lubricants with dielectric strength, and mining machinery favors high-tack fluids that stay in place under shock loads in dusty environments.

Geography Analysis

Asia-Pacific commanded 37.86% of global 2025 volume and is forecast for the highest 5.03% CAGR owing to China’s automation push and India’s USD 87 billion petrochemical capex pipeline. Ongoing mega-projects such as BASF’s EUR 10 billion Zhanjiang complex and SABIC’s USD 6.4 billion Fujian venture inject sustained demand for synthetic lubricants to manage 24-hour duty cycles.

North America anchors substantial consumption owing to shale-gas processing developments like Phillips 66’s Iron Mesa plant and Targa Resources’ integrated Permian Basin network. Regulatory pressure from updated Department of Energy (DOE) compressor guidelines and Environmental Protection Agency (EPA) emissions caps accelerates synthetic adoption and supports the compressor oils market in this region. Mitsubishi Electric’s forthcoming Kentucky plant will lift the domestic supply of oil-less heat-pump scroll units, yet lubricated industrial lines still dominate heavy manufacturing.

Europe remains technologically progressive, leveraging stringent REACH limits and a green hydrogen roadmap that specifies embrittlement-resistant lubricant chemistry. Producers like FUCHS invest in Barcelona blending upgrades and acquisitions that broaden specialty portfolios. South America and the Middle East & Africa trail on volume but offer high upside where mining expansion and grassroots petrochemical ventures are ramping, albeit under tighter price discipline that preserves mineral-oil demand in the near term.

Mordor Intelligence provides coverage of the compressor oil market across other key regional markets, including North America and Asia, each with their regulatory frameworks and demand patterns.

Value Chain Analysis

The compressor oil value chain starts with feedstock and ingredient suppliers providing Group I-III mineral base oils and synthetic base stocks (PAO, PAG, and specialty esters), along with additive chemistries such as anti-wear, anti-oxidant, anti-foam, demulsifier, and corrosion-inhibitor packages. Lubricant majors and independent blenders then formulate and blend finished compressor oils, working with compressor OEMs and service organizations to pre-qualify products for specific rotary screw, reciprocating, and centrifugal compressor platforms. This specification-driven approach supports repeat purchasing tied to maintenance programs and warranty-compliant service intervals.

Finished products reach industrial users through direct industrial sales, authorized distributors, and industrial retailers, with offline channels staying dominant for many industrial lubricant categories. Technical services such as oil analysis, condition monitoring, drain-interval optimization, and contamination control increasingly accompany physical distribution, particularly for premium synthetics in continuous-duty manufacturing and process-gas applications. Supply-side constraints are concentrated around crude-linked base-oil price swings and access to higher-performance synthetic base stocks, which leads some buyers to favor longer drain intervals and pushes some suppliers toward regionalized blending and closer OEM alliances to limit qualification churn.

Competitive Landscape

The Compressor Oil market is moderately consolidated with the presence of major players, such as Shell, ExxonMobil Corporation, BP p.l.c., and TotalEnergies. Shell has led global lubricant sales for 18 consecutive years with about 11.6% share, leveraging an integrated supply chain and broad distributor coverage. ExxonMobil Corporation’s investment in Singapore synthetic basestock assures feedstock security for premium brands and fortifies a competitive moat against commodity suppliers. Saudi Aramco’s ongoing evaluation of BP p.l.c.’s Castrol unit could realign market dynamics by combining upstream crude with downstream specialty blending, thereby changing economies of scale. Companies investing in R&D for hydrogen-ready ester formulations or EV-thermal-management PAO blends will likely capture emerging revenue streams that balance any erosion in traditional screw-compressor consumption.

Compressor Oil Industry Leaders

BP p.l.c.

TotalEnergies

ExxonMobil Corporation

Shell

Sinopec Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is widening in high-value, specification-driven oils where operators focus on energy efficiency, extended drain intervals, and compatibility with harsher duty cycles, including higher discharge temperatures in automated manufacturing and chemically aggressive process gases in midstream and petrochemical service. Company activity in 2026 points to this split: Hitachi Industrial Equipment Systems introduced GREEN SCREW OIL (plant-based) for oil-flooded screw air compressors, while Repsol Lubricants launched Maker Synthetic Compressor, a 100% synthetic PAO-based line (ISO VG 46 and 68) with an ashless additive package. Together, these moves reinforce a market divide between higher-volume mineral and semi-synthetic products and higher-margin synthetics and alternative chemistries positioned around sustainability, cleanliness, and longer service life.

A second opportunity area is supply security and performance consistency for premium base stocks that support synthetic compressor oils. ExxonMobil started up technology in Singapore in September 2025 to upgrade lower-value crude streams into higher-value lubricant base stocks, including EHC 340 MAX, supporting feedstock needed for premium industrial formulations. On the demand side, Industry 4.0 maintenance practices create room for suppliers that bundle compressor oil with condition monitoring and OEM-approved service programs, using oil-health data to standardize drain intervals and reduce unplanned downtime across large manufacturing sites and high-horsepower gas compression assets.

Recent Industry Developments

- June 2026: PetroChina Lubricant Company advanced domestic substitution in high-end compressor lubricants by expanding its Kunlun ether-ester oil portfolio, with validation conducted across multiple sites in Yunnan. The move strengthens market position against premium synthetic competitors.

- September 2025: ExxonMobil started up a technology deployment in Singapore that converts bottom-of-the-barrel crude products into higher-value lubricant base stocks, including EHC 340 MAX at 6,000 barrels per day. The move strengthens supply assurance for premium industrial lubricants and improves feedstock flexibility for synthetic-leaning compressor oil portfolios.

- October 2024: RSC Bio Solutions launched FUTERRA Compressor Oils for rotary screw, reciprocating, and other high-performance air compressors, targeting industrial and marine users. The launch broadened the bio-based and alternative chemistry set available to operators seeking performance alongside sustainability attributes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers lubricating oils formulated for air and gas compressors that need lubrication, sealing, cooling, and wear protection during normal operation across industrial end uses and regions.

Scope exclusions: It excludes non-oil lubricants and oils used in unrelated equipment such as engines, gearboxes, hydraulics, and turbines.

Segmentation Overview

- By Base Oil

- Synthetic

- Mineral

- Other Base Oils (Semi-synthetic, Bio-based, etc.)

- By Compressor Type

- Positive Displacement

- Dynamic

- By Application

- Air Compressors

- Gas Compressors

- By End-user Industry

- Manufacturing

- Chemical and Petrochemical

- Oil and Gas

- Mining

- End-user Industry (HVAC and Refrigeration, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping how compressor oils are produced and sold, then linking those flows to compressor usage in key industries. We relied on public sources such as US Energy Information Administration data, US Geological Survey industrial indicators where relevant, UN Comtrade trade statistics for base oils and lubricants, and US EPA and European Chemicals Agency pages that discuss lubricant related compliance topics.

To keep assumptions realistic, we also reviewed company annual reports, investor presentations, and product technical data sheets that point to drain intervals and performance grades for common compressor types. Patent databases and an import and export shipment-level database were used selectively to sanity check innovation directions and cross-border movement patterns for lubricant categories. These examples are not exhaustive, and many other public and paid sources were referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to confirm how much oil is consumed per compressor over a service cycle, how fast end users are shifting toward synthetics, and how maintenance practices differ between air and gas compression. We spoke with a mix of lubricant suppliers, blenders, distributors, and large end users across APAC, EMEA, and the Americas, and we used follow-ups when desk signals and field inputs did not line up cleanly.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 39% |

| Mid tier: 48% | Functional/Unit leaders: 43% | EMEA: 34% |

| Smaller Players: 15% | Managers: 44% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built mainly from a top-down demand pool, where compressor population and activity indicators are translated into lubricant consumption using service intervals and typical fill volumes, then expressed in liters for the total market. To keep it grounded, we cross-check against selective bottom-up approximations such as sampled supplier volumes by region, distributor channel checks, and simple volume times average price logic for a few end-use pockets, which we then use to tune outliers.

Key inputs include compressor operating hours by industry, oil change intervals that shift with synthetic adoption, the split between air versus gas compressors, maintenance practices that affect top-up rates, and industrial output signals that drive compressor utilization. Forecasting uses scenario analysis supported by expert views on industrial activity, energy and gas processing investments, and the pace of premiumization. When bottom-up signals are missing in smaller countries, we fill gaps using proxy ratios tied to manufacturing intensity and compressor penetration, then validate totals through follow-up calls.

Data Validation & Update Cycle

Outputs are validated by checking consistency across regions, applications, and end users before the numbers are finalized. We run variance checks against independent signals such as compressor shipment trends, industrial production direction, and lubricant trade flows, then investigate any large jumps that cannot be explained by demand drivers. A second analyst review is completed, and re-contact is triggered when interview feedback conflicts with desk indicators or when assumptions move.

The model is refreshed annually, and interim updates are made when material events occur, such as sharp base oil price swings or major industrial slowdowns that change utilization. Before delivery, the dataset and calculations get a fresh pass so the final view reflects the most recent information available.

Mordor Intelligence's Compressor Oil Market Sizing Compared With Other Published Estimates

Published compressor oil market numbers often differ because the unit of measure, the point in the value chain being counted, and the inclusion of adjacent lubricant categories are not always aligned. Differences also show up when firms rely on one conversion factor for all regions, or when older assumptions are carried forward without fresh checks.

Industrial engine oils and hydraulic oils sit outside Mordor Intelligence's scope for this study, which is one reason value-based totals from broader lubricant baskets can look higher even when real compressor oil consumption is unchanged. The spread can also come from how pricing is handled, since average selling prices vary with synthetic share, drain interval behavior, and the mix of air versus gas compression, and not every publisher refreshes these inputs at the same frequency.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.49 B (2026) | |

| Industry Research House A | USD 4.92 B (2024) | Uses a revenue lens and may capture a wider lubricant value chain with price-based expansion, which can inflate totals versus a pure volume model in liters. |

| Global Consultancy B | USD 8.30 B (2023) | Includes sales-channel and end-use revenue aggregation that can fold in adjacent lubricant categories and broader pricing assumptions, creating a higher stated market value. |

The table indicates that the largest gaps come from unit choice and scope, since a liters-based consumption build will not match a revenue total that blends pricing and neighboring lubricant lines. By tying demand to compressor use intensity, service intervals, and product mix, our estimate stays traceable to inputs that can be checked and repeated year to year.

Key Questions Answered in the Report

What is the current Compressor Oil Market size?

The Compressor Oil market size stood at 494.38 Million liters in 2026 and is projected to reach 609.33 Million liters by 2031.

Which base-oil segment leads the Compressor Oil market?

Synthetic fluids command leadership, accounting for 40.92% of 2025 volume due to extended drain intervals and superior thermal stability.

Which end-user industry is growing the fastest?

Oil and gas applications are forecast to register the highest 5.11% CAGR through 2031 because of midstream processing expansions.

Why is Asia-Pacific the dominant regional market?

Asia-Pacific holds 37.86% share owing to rapid industrial automation in China and large-scale petrochemical investments in India, all of which expand compressor installations and lubricant demand.

How are oil-free compressors affecting lubricant demand?

Oil-free technology erodes fluid volumes in contamination-sensitive sectors, yet higher performance demands and new hydrogen applications create offsetting opportunities for specialty synthetic oils.

Page last updated on: