Engine Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

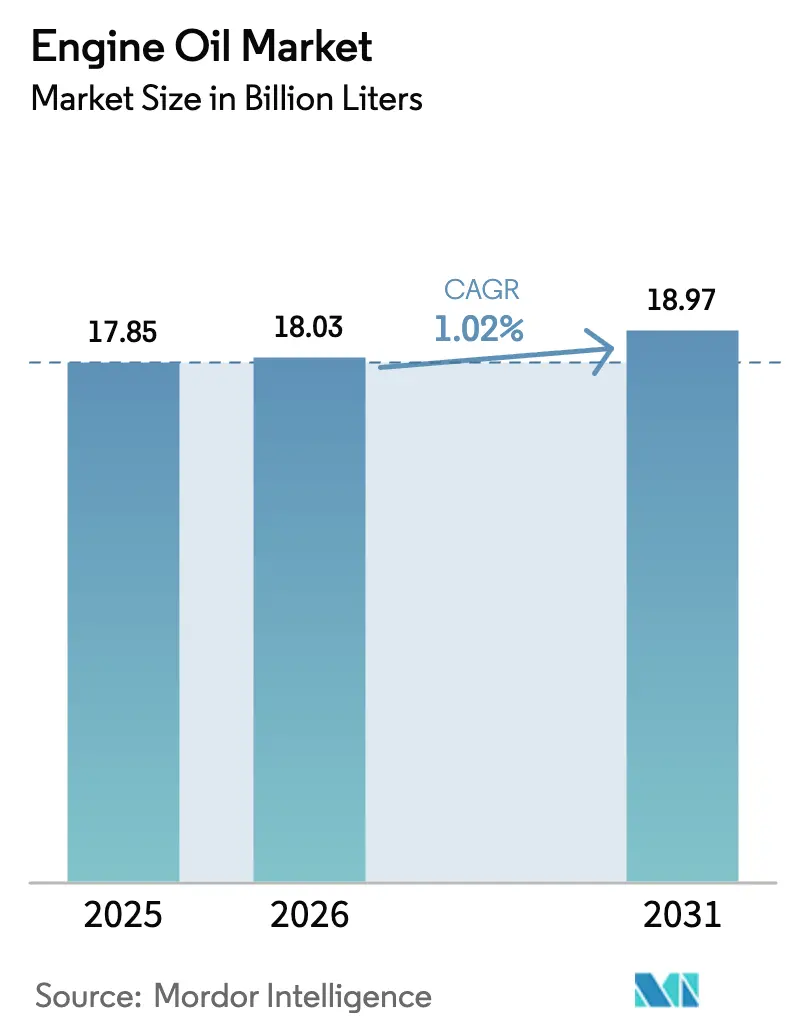

| Market Volume (2026) | 18.03 Billion liters |

| Market Volume (2031) | 18.97 Billion liters |

| Growth Rate (2026 - 2031) | 1.02% CAGR |

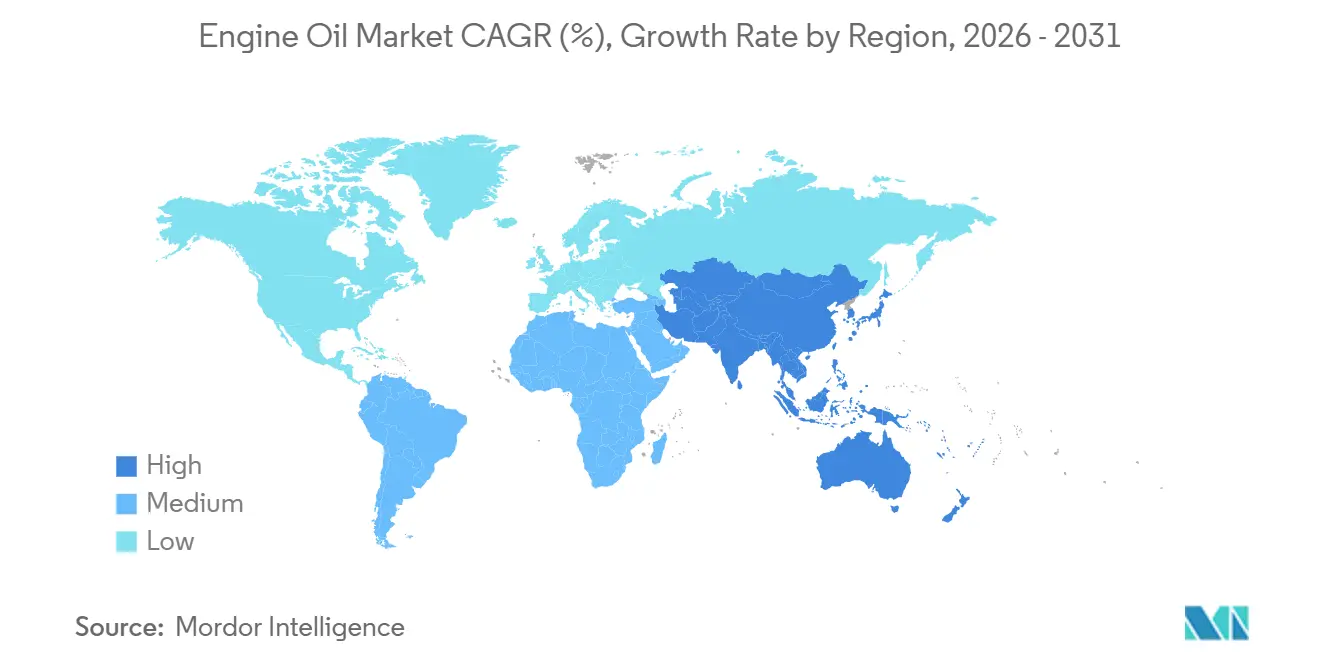

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Engine Oil Market Analysis by Mordor Intelligence

The Engine Oil Market size is expected to increase from 17.85 Billion liters in 2025 to 18.03 Billion liters in 2026 and reach 18.97 Billion liters by 2031, growing at a CAGR of 1.02% over 2026-2031. The engine oil market is feeling the drag of longer factory-fill drain intervals, accelerating battery-electric adoption, and wider use of sealed-for-life transmissions, even as the worldwide vehicle parc grows older. Asia-Pacific keeps volume leadership thanks to a sharp jump in Chinese output and a surge in Indian production during 2024, while Europe’s pending Euro 7 rule and the U.S. EPA Phase 3 standards are tilting demand toward low-viscosity synthetics. Bio-based formulations are picking up speed under EU Ecolabel mandates, and motorcycles are gaining ground as India’s Bharat Stage VI rules tighten sulfur and phosphorus caps. Competitive pressure remains intense, with global majors defending premium margins through Group III and Group III+ base-stock capacity while state-owned refiners in Asia chase domestic share.

Key Report Takeaways

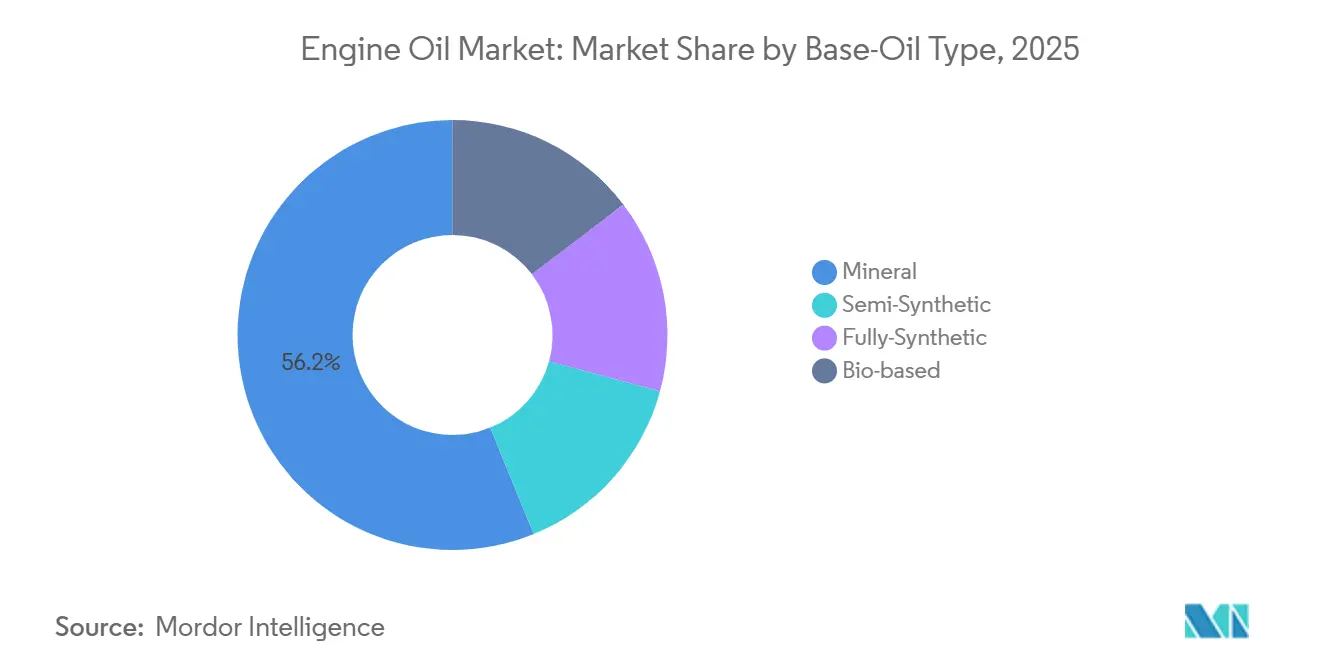

- By base-oil type, mineral oils led with 56.18% of 2025 volume, whereas bio-based oils are poised to expand at a 2.80% CAGR through 2031.

- By vehicle type, passenger cars captured 49.74% of 2025 demand, yet motorcycles and scooters are forecast to grow the fastest at 1.90% CAGR through 2031.

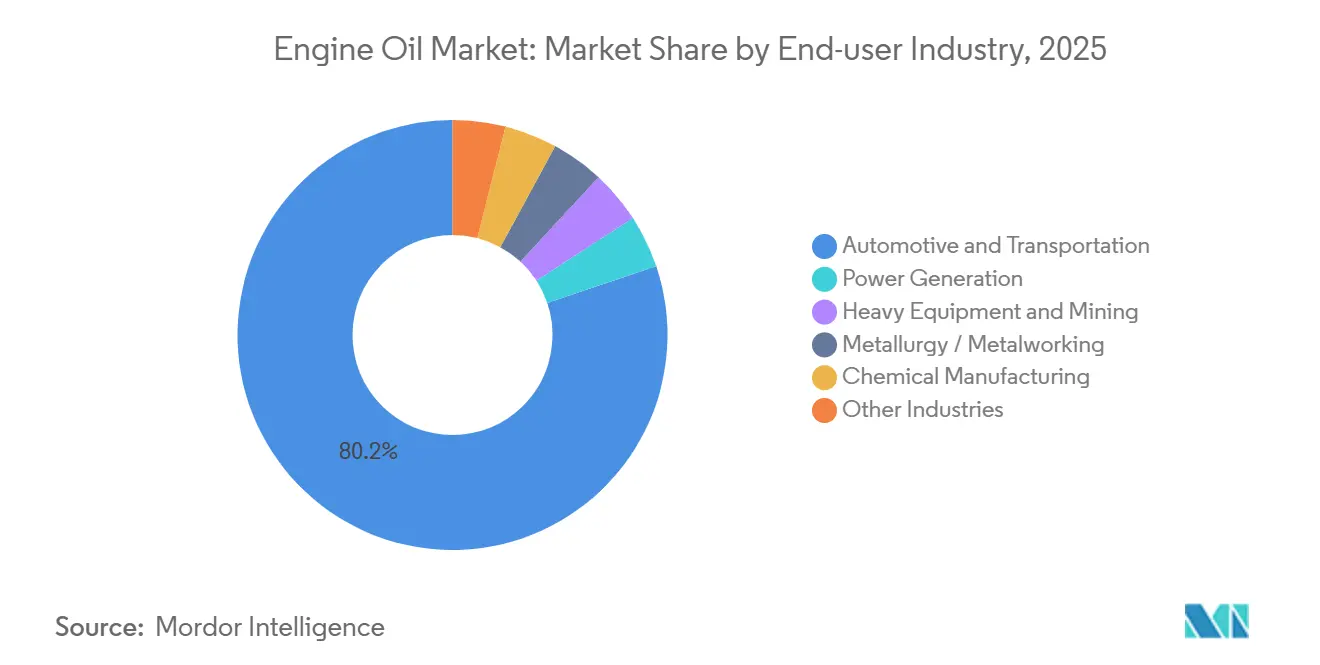

- By end-user industry, automotive and transportation accounted for 80.18% of 2025 consumption, while power generation is set to register the quickest 2.30% CAGR to 2031.

- By geography, Asia-Pacific dominated with a 58.17% share in 2025 and is expected to post a 1.30% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Engine Oil Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing automotive production in emerging economies | +0.4% | Asia-Pacific core, spillover to South America | Medium term (2-4 years) |

| Rising demand for high-performance synthetic lubricants | +0.3% | Global, with focus on North America and Europe | Long term (≥4 years) |

| Growing average vehicle age and miles-driven | +0.2% | North America, Europe, mature APAC markets | Long term (≥4 years) |

| Stricter CO₂/fuel-economy norms favoring low-viscosity oils | +0.3% | Global, led by EU, North America, China | Medium term (2-4 years) |

| Emergence of micro-mobility maintenance ecosystems | +0.1% | Urban centers in Europe and Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increasing Automotive Production in Emerging Economies

In 2024, global light-vehicle production increased, with Asia contributing significantly to the total output. China ramped up its production, while India, driven by a surge in SUV demand and bolstered by export hubs in Gujarat and Tamil Nadu, experienced notable growth. Mexico solidifies its position as the third key player in North America and acts as a re-export conduit to South America. This added capacity not only boosts factory-fill volumes but also ensures a robust aftermarket replenishment, especially in regions with service intervals under 10,000 kilometers. Looking to the future, the OICA projects that by 2028, the Asia-Pacific region will account for a significant share of the global output, signaling a continued strong demand for cost-sensitive mineral and semi-synthetic lubricant grades.

Rising Demand for High-Performance Synthetic Lubricants

As automakers increasingly turn to low-viscosity fluids to comply with fuel-economy standards, the share of fully synthetic engine oils in the global market has grown. In North America and Europe, Group III base oils now account for a significant portion of the supply, steadily displacing the older Group I stocks. The upcoming ILSAC GF-8A standard, set for 2028, mandates 0W-8 oils to maintain a high-temperature high-shear viscosity of 2.6 centipoise, further solidifying the demand for synthetics[1]International Lubricant Standardization and Approval Committee, “ILSAC GF-7 Standard,” ilsac.org. Mobil 1 from ExxonMobil and Shell's Helix Ultra have achieved notable success, bolstered by securing OEM co-approvals from automotive giants like Honda, Toyota, and Volkswagen.

Growing Average Vehicle Age and Miles-Driven

In 2025, the median age of light vehicles in the U.S. increased, surpassing the EU's average, signaling elongated replacement cycles. Older powertrains consuming oil ensure a consistent demand for top-ups in retail channels. In 2024, U.S. vehicle miles traveled increased, indicative of a rebound in both commuter and freight activities. Between 2020 and 2025, Japan experienced a rise in average odometer readings during inspections, counterbalancing the extended drain intervals of newer models.

Stricter CO₂/Fuel-Economy Norms Favoring Low-Viscosity Oils

In late 2024, Euro 7, set to be enforced in 2027, introduced a cap on crankcase emissions. It also mandates type-approval with market lubricants, shifting the durability risk onto blenders. Meanwhile, in the U.S., EPA Phase 3 is pushing for a significant CO₂ reduction in heavy-duty vehicles by 2032. This push is steering fleets towards FA-4 10W-30 oils, which offer fuel savings over the previously favored CK-4 15W-40. Over in China, 2024 saw a nationwide extension of the China VI-b limits, tightening caps on sulfur and phosphorus. This move has spurred a heightened demand for low-SAPS SAE 0W-20 and 5W-30 grades.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended drain intervals via OEM factory-fill long-life oils | -0.5% | Global, concentrated in Europe and North America | Medium term (2-4 years) |

| Accelerating EV penetration | -0.3% | Europe, China, North America | Long term (≥4 years) |

| OEM move toward sealed-for-life lubrication systems | -0.2% | Global, led by Europe and Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Extended Drain Intervals via OEM Factory-Fill Long-Life Oils

In North America, automakers have extended service windows, while in Europe, the limit is set at longer intervals. This extension is achieved by infusing factory fills with antioxidants and friction modifiers, ensuring they maintain viscosity for up to two years. Toyota's Camry Hybrid, using 0W-16 oil, adheres to a specific schedule. In contrast, Honda's 0W-20 Genuine Motor Oil follows a shorter interval. General Motors, with its Dexos1 Gen 3, focuses on endurance by incorporating molybdenum and boron chemistry.

Accelerating EV Penetration

In 2024, battery-electric models accounted for a significant share of total light-vehicle sales, leading to a reduction in crankcase oil demand per vehicle. Norway achieved an impressive share of electric vehicles (EVs) in 2025, while California's Advanced Clean Cars II initiative mandates 100% zero-emission sales by 2035[2]California Air Resources Board, “Advanced Clean Cars II,” arb.ca.gov . According to the IEA's Net Zero pathway, the adoption of EVs by 2030 could result in a notable decrease in engine oil demand compared to the 2026 baseline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base-Oil Type: Bio-Based Oils Gain Traction Amid Sustainability Mandates

Bio-based oils are the fastest-growing slice of the engine oil market, advancing 2.80% each year through 2031, even though mineral oils still dominate with 56.18% volume in 2025. The European Union's Ecolabel mandates a minimum of 25% renewable carbon and stipulates that biodegradability must exceed 60% within 28 days. This move is steering government fleets towards plant-ester blends. Similarly, the United States BioPreferred program is gaining traction, awarding federal contracts based on certified bio content. In Germany, RAVENOL is set to launch its 2024 BioSyntoLub, blending rapeseed and sunflower esters with Group III stock to align with ACEA C3 standards. This underscores the industry's pursuit of public-procurement budgets.

Price sensitivity maintains the mineral category's dominant share, particularly in South and Southeast Asia. Semi-synthetic blends, containing Group III or IV content, target API SN Plus standards for mainstream sedans. Fully synthetic oils, primarily derived from polyalphaolefin, enjoy premium OEM endorsements. However, they grapple with rising costs as mandates for low viscosity drive formulators towards enhanced Group III+ options. While the market for bio-based engine oils is currently modest, regulatory influences and corporate carbon objectives indicate a significant upward trend by 2031.

By Vehicle Type: Two-Wheelers Accelerate on Emission Compliance

Passenger cars generated 49.74% of 2025 volume, but motorcycles and scooters are forecast to log the highest 1.90% CAGR, underlining their expanding role in the engine oil market. India, Indonesia, Vietnam, and Thailand have tightened emission caps, leading to more frequent oil changes and a shift towards higher-spec JASO MA2 products. Bharat Petroleum’s MAK 4T Plus, Indian Oil’s Servo 4T Synth, and Hindustan Petroleum’s HP Racer dominate the market, controlling a significant share of organized two-wheeler lubricant sales through an extensive network of touchpoints.

Light commercial vans and pickups are reaping the rewards of e-commerce’s last-mile delivery demands. Giants like Amazon, FedEx, and UPS operate fleets requiring regular oil changes. Meanwhile, heavy-duty trucks and buses are transitioning to FA-4 and E9 low-viscosity grades. These grades not only reduce particulate emissions but also maintain wear protection. In the realm of off-road construction, equipment operators are turning to zinc-rich formulations, ensuring their hydraulic systems are safeguarded even in dusty conditions and under heavy loads. While the engine oil market for two-wheelers may lag behind that of passenger cars in size, its rapid growth and frequent service requirements render it a strategically vital segment for blenders.

By End-User Industry: Power Generation Drives Niche Growth

Automotive and transportation consumed 80.18% of global volume in 2025, but power generation stands out with the swiftest 2.30% CAGR, carving an attractive high-margin niche within the wider engine oil market. Gas gensets, dual-fuel engines, and backup turbines in data centers rely on low-ash oils, such as Caterpillar CG-4, to protect catalysts during stoichiometric combustion. Wärtsilä’s dual-fuel engines demand lubricants that maintain stability whether operating on heavy fuel oil or liquefied natural gas. Meanwhile, Cummins’ QSK95 engine consumes oil for every 1,000 hours of continuous operation.

Heavy equipment and mining, the second-largest industrial segment, rely on CI-4 Plus oils to safeguard turbochargers under heavy loads. In the realm of metalworking and metallurgy, ISO VG 68-150 oils serve a dual purpose, acting as both gear and hydraulic fluids. Chemical plants, on the other hand, opt for NSF-registered H1 or H2 grades to ensure optimal lubrication for compressors and pumps. While these sectors may hold a smaller market share, they consistently deliver volume and margin stability, countering the cyclical nature of the automotive industry and ensuring a balanced portfolio for the engine oil market.

Geography Analysis

Asia-Pacific delivered 58.17% of global demand in 2025 and is projected to grow at a 1.30% CAGR. This growth is bolstered by China's production, India's output, and ASEAN's combined assemblies. China's nationwide rollout of the China VI-b standard in 2024 led to a surge in demand for low-SAPS SAE 0W-20 and 5W-30 oils. Meanwhile, in India, lubricant consumption increased, driven by the proliferation of two-wheelers and a robust retail network.

North America experienced an annual contraction, coinciding with the adoption of electric vehicles (EVs) in the 2025 sales mix. Despite this, premium synthetic blends managed to maintain their value share. The EPA's 2024 sulfur cap necessitated additive reformulations, a move that benefitted suppliers like ExxonMobil, Chevron, and Valvoline. While Canada's federal zero-emission mandate has dampened demand in British Columbia and Quebec, Mexico's output is meeting the factory-fill needs for Dexos1 and Motorcraft-approved oils.

Europe saw an annual contraction, with countries like Norway and the Netherlands elevating their EV shares significantly. The region's regulatory intricacies - spanning Euro 7, ACEA sequences, and national CO₂ taxes - have escalated formulation costs, steering business towards integrated majors. By 2027, Germany's Federal Motor Transport Authority will mandate crankcase-emission testing with market lubricants, potentially increasing certification expenses. In the UK, initiatives by Safety-Kleen and Fuchs Petrolub's closed-loop programs have bolstered the share of re-refined base oils.

South America saw modest annual growth, spearheaded by Brazil's flex-fuel fleet, which necessitates corrosion-resistant oils. Petrobras' Lubrax brand, leveraging a network of company stations and independents, secured a dominant share in the aftermarket. In a strategic move, Argentina's YPF inaugurated a blending facility, catering to both Mercosur exports and the domestic agricultural machinery sector.

The Middle East and Africa recorded yearly growth. Demand was bolstered by assembly ventures funded by Saudi Arabia's PIF and a robust mining fleet in South Africa. In 2024, Aramco's Luberef expanded its Group II output, with a focus on markets in India and East Africa. Concurrently, Engen introduced its ACEA E9-approved 10W-40 oil, targeting heavy-duty trucks across the Southern African Development Community (SADC) region.

Competitive Landscape

The engine oil market is moderately fragmented in nature. Global players' strategies pivot on OEM partnerships, Group III+ base-stock integration, and direct-to-consumer e-commerce channels that preserve premium margins. State-owned refiners dominate their home turf by coupling crude supply, base-oil refining, and branded retail networks. White-space growth is unfolding in re-refined base oils and subscription models. Mobil 1 and Pennzoil have piloted direct-to-consumer programs that ship oil and filters on an annual cadence, capturing incremental share from traditional retail while building customer data. Additive innovation is another competitive lever. Molybdenum dialkyldithiocarbamate and boron dispersants slash friction and soot, respectively, while calcium sulfonate detergents extend total base number retention. Digital advances, such as in-sump oil-condition sensors and blockchain authenticity tags, aim to reduce counterfeit risks in emerging markets.

Engine Oil Industry Leaders

Shell PLC

Exxon Mobil Corporation

BP p.l.c

Chevron Corporation

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c began exploring a divestiture of its Castrol lubricants unit, valued near USD 10 billion, as part of a plan to raise USD 20 billion by 2027. The sale could reshape Castrol’s sizable global footprint in the engine oil market.

- May 2025: TotalEnergies released next-generation Quartz oils meeting API SQ and ILSAC GF-7 performance bars and designed for turbocharged gasoline direct-injection engines.

Global Engine Oil Market Report Scope

Engine oil is a lubricating system explicitly designed for use in engines. It decreases the friction between engine surfaces that come into contact with each other. It reduces energy waste caused by friction and is highly effective in cleaning, cooling, and protecting metal components from corrosion and rust. A good quality engine oil is critical for the proper operation of an engine as it enables smooth engine operations, prevents engine damage, and extends engine life.

The engine oil market is segmented by base-oil type, vehicle type, end-user industry, and geography. By base-oil type, the market is segmented into mineral, semi-synthetic, fully-synthetic, and bio-based. By vehicle type, the market is segmented into passenger cars, light commercial vehicles, heavy-duty trucks and buses, motorcycles and scooters, and off-road/construction. By end-user industry, the market is segmented into automotive and transportation, power generation, heavy equipment and mining, metallurgy/metalworking, chemical manufacturing, and other industries. The report also covers the market size and forecasts for the engine oil market in 17 countries across major regions. For each segment, the market sizing and forecasts are provided on the basis of volume (Liters).

| Mineral |

| Semi-Synthetic |

| Fully-Synthetic |

| Bio-based |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy-Duty Trucks and Buses |

| Motorcycles and Scooters |

| Off-Road / Construction |

| Automotive and Transportation |

| Power Generation |

| Heavy Equipment and Mining |

| Metallurgy / Metalworking |

| Chemical Manufacturing |

| Other Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Base-Oil Type | Mineral | |

| Semi-Synthetic | ||

| Fully-Synthetic | ||

| Bio-based | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy-Duty Trucks and Buses | ||

| Motorcycles and Scooters | ||

| Off-Road / Construction | ||

| By End-user Industry | Automotive and Transportation | |

| Power Generation | ||

| Heavy Equipment and Mining | ||

| Metallurgy / Metalworking | ||

| Chemical Manufacturing | ||

| Other Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global engine oil market size by 2031?

The engine oil market size is expected to reach 18.97 billion liters by 2031, rising at a 1.02% CAGR from 18.03 billion liters in 2026.

Which region holds the largest share of demand?

Asia-Pacific accounts for 58.17% of global volume in 2025 thanks to robust vehicle production in China, India, and ASEAN markets.

Which base-oil segment is growing the fastest?

Bio-based oils are forecast to expand at a 2.80% CAGR through 2031 as sustainability mandates strengthen.

Why are motorcycles an attractive growth pocket?

Motorcycles and scooters will post a 1.90% CAGR because stricter emission rules in India and Southeast Asia mandate higher-spec oils and more frequent changes.

How is electrification affecting lubricant demand?

Battery-electric vehicles consume less lubricant than internal-combustion models, trimming global engine oil volume as EV market share climbs.

Page last updated on: