Pakistan Automotive Engine Oils Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

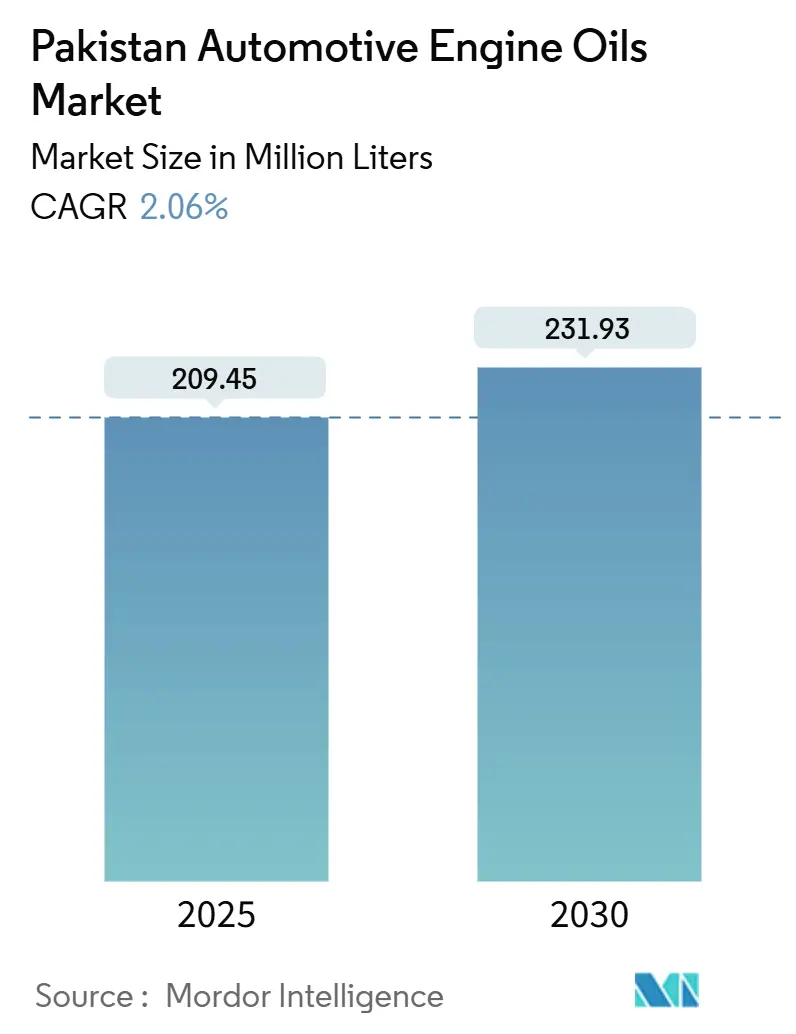

| Market Volume (2025) | 209.45 Million liters |

| Market Volume (2030) | 231.93 Million liters |

| Growth Rate (2025 - 2030) | 2.06% CAGR |

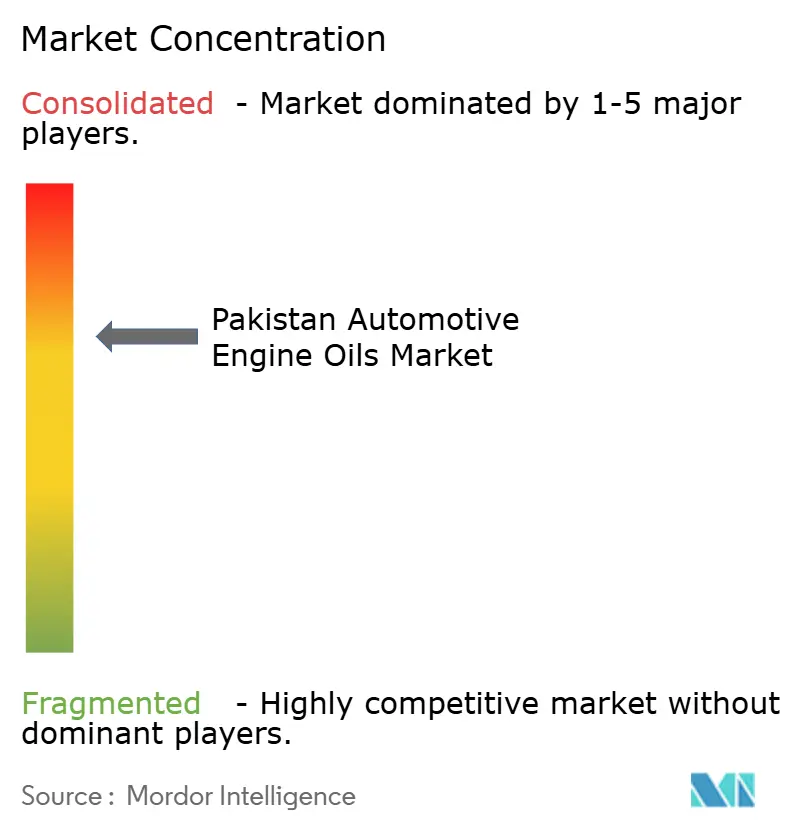

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Automotive Engine Oils Market Analysis by Mordor Intelligence

The Pakistan Automotive Engine Oils Market size is estimated at 209.45 million liters in 2025, and is expected to reach 231.93 million liters by 2030, at a CAGR of 2.06% during the forecast period (2025-2030). This growth outlook is underpinned by Pakistan’s expanding vehicle parc, macro-driven migration toward Euro-5 fuels, and sustained freight demand that keeps lubricant consumption structurally tied to road transport activity. Premiumisation is emerging as a parallel force, with domestic refineries channeling USD 5-6 billion into Euro-5 upgrades that will spur higher-value, low-SAPS formulations. Urban motorization, presently at 161 vehicles per 1,000 people, concentrates demand in Lahore, Karachi, and Islamabad, where stop-start usage intensifies drain cycles. Mineral oils still dominate retail shelves, yet synthetic blends post the quickest uptake as OEM mandates, ride-hailing mileage, and inter-city logistics fleets emphasize extended-drain efficiency. Competitive behaviour reflects moderate consolidation around brands with national pump networks and local blending assets that hedge currency exposure.

Key Report Takeaways

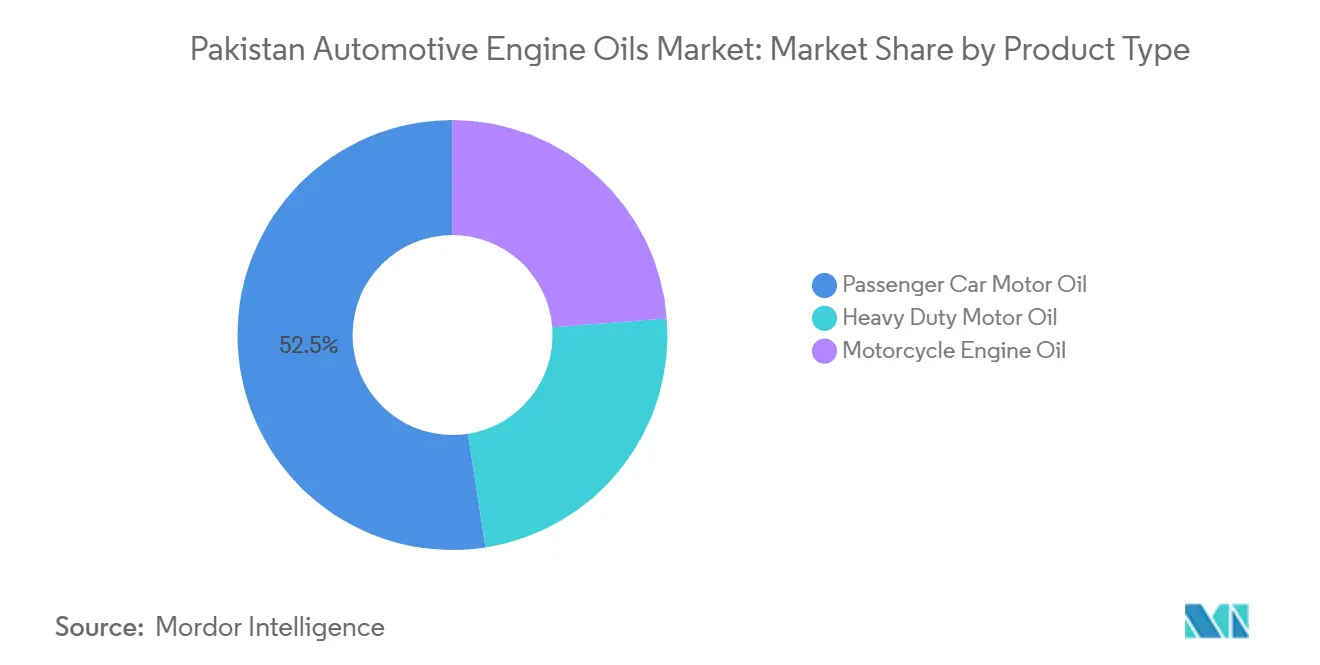

- By product type, passenger car motor oil led with a 52.46% share of the Pakistani automotive engine oils market in 2024. Motorcycle engine oil is forecast to expand at a 2.18% CAGR through 2030, the fastest among product types.

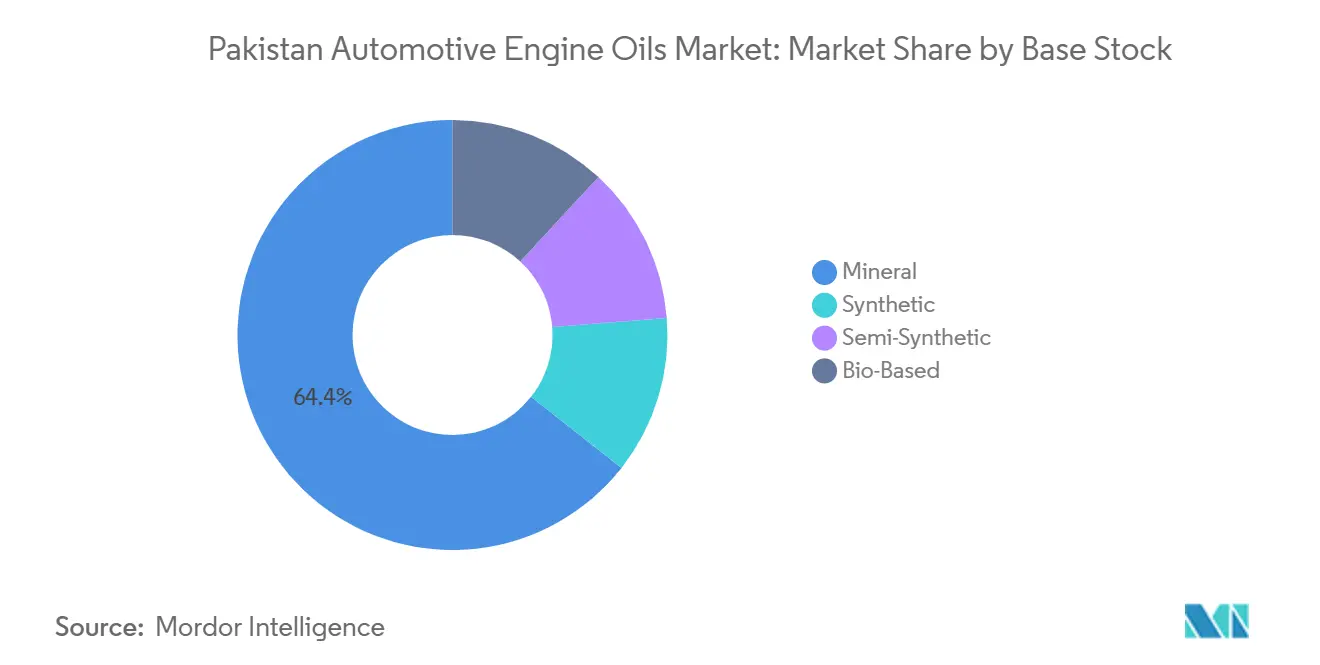

- Mineral base stocks captured 64.38% of the Pakistan automotive engine oils market size in 2024, while synthetic oils are projected to grow at a 2.31% CAGR, the quickest within base-stock categories.

Pakistan Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising two-wheeler and passenger-car parc in urban centers | +0.8% | Punjab and Sindh urban clusters; Islamabad | Medium term (2-4 years) |

| Expansion of inter-city logistics and ride-hailing fleets | +0.4% | Nationwide highway corridors | Short term (≤ 2 years) |

| OEM collaborations and local blending expansion | +0.3% | Karachi and Lahore industrial zones | Long term (≥ 4 years) |

| Government rebates on Euro-5-compliant lubricants | +0.2% | Nationwide | Medium term (2-4 years) |

| Remittance-fuelled used-car demand in tier-2 cities | +0.3% | Punjab tier-2 districts; KPK urban pockets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Two-Wheeler and Passenger-Car Parc in Urban Centers

Islamabad registered 1.3 million vehicles by April 2024 and continues to add 2,000-3,000 registrations monthly, a pattern mirrored across Lahore and Karachi[1]Pakistan Institute of Development Economics, “Urban vehicle statistics 2024,” pide.org.pk. High stop-start frequency in congested corridors shortens drain intervals, keeping lubricant demand sticky despite fuel-efficiency gains. Punjab’s 57% share of national road infrastructure funnels traffic through dense service clusters that favor organized lubricant retailers. Motorcycles, which already account for 78% of all vehicles, amplify volumes through frequent, low-capacity oil changes. OEM-recommended multigrades have gained traction in these cities, nudging consumers toward higher-margin synthetic and semi-synthetic lines.

Expansion of Inter-City Logistics and Ride-Hailing Fleets

Road transport accounts for 96% of Pakistan’s freight, and light commercial vehicles average 105,000 km per year, approximately triple the mileage of private cars. Heavy use drives 3-4 oil changes annually per vehicle, while fleet operators increasingly favor premium formulations that cut downtime. TCS, with a 43% national parcel share and 140,000 tons of annual freight, epitomizes these high-utilization fleets that standardize on extended-drain synthetics. Ride-hailing aggregators replicate this mileage intensity in the passenger-car segment, lifting demand for low-viscosity, fuel-saving oils.

OEM Collaborations and Local Blending Expansion

Gulf Oil International’s 2024 tie-up with OTO Pakistan embeds a premium global brand into a local retail network of lubricants and quick-service centers[2]Gulf Oil International, “Gulf partners with OTO Pakistan,” gulfoilinternational.com. Parallel investments by Shell and other multinationals in Karachi blending plants curb forex exposure and ensure supply amid Letter-of-Credit restrictions. Pakistan’s Auto Industry Development Policy targets 650,000 cars and 7 million two-wheelers annually, furnishing OEM-fill volumes that favor lubricant partners with factory approvals and synthetic portfolios.

Government Rebates on Euro-5-Compliant Lubricants

Under the Brownfield Refinery Policy, authorities levy 10% duty on motor spirit and 2.5% on high-speed diesel to fund Euro-5 upgrades. The program primes downstream demand for low-SAPS oils that protect after-treatment devices. OGRA oversight raises compliance costs for non-certified brands, effectively tilting share toward early adopters. Suppliers that secure Euro-5 attestations can capture price premiums and secure OEM endorsements in the domestic market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended oil-drain intervals with synthetics | -0.5% | Nationwide, especially metro areas | Long term (≥ 4 years) |

| Inflation and PKR depreciation impacting affordability | -0.4% | National, highest pressure in rural zones | Short term (≤ 2 years) |

| LC restrictions causing base-oil supply gaps | -0.3% | Nationwide importers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extended Oil-Drain Intervals with Synthetics

Synthetic and semi-synthetic formulations allow 10,000-15,000 km drain cycles, roughly double the 5,000 km norm for mineral oils. OEM service booklets are increasingly mandating these longer intervals, trimming per-vehicle volume even as revenue per liter rises by 40-60%. The effect is most pronounced in premium passenger-car and fleet segments that adopt synthetics early, tempering aggregate volume growth despite value gains.

Inflation and PKR Depreciation Impacting Affordability

PKR weakness inflates the landed cost of imported base oils and additives, forcing price hikes that pinch disposable incomes. Value-minded two-wheeler owners and owner-operators of small trucks either defer oil changes or shift to lower-grade monogrades. The squeeze is sharper in rural districts, where cash incomes lag behind urban levels, creating geographic segmentation in lubricant quality uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Passenger Car Oils Lead While Motorcycle Oils Accelerate

Passenger Car Motor Oil held 52.46% of Pakistan automotive engine oils market share in 2024, anchored by the rising urban car parc and the requirement for high-quality multigrades to meet Euro-5 fuel demands. The Pakistan automotive engine oil market size for PCMO is expected to grow steadily as consumer financing products keep car ownership within reach, despite macroeconomic pressures. High urban congestion, coupled with elevated ambient temperatures, favors 10W-XX and 15W-XX grades that strike a balance between cold-start fluidity and thermal stability. Dealers report that motorists are increasingly accepting synthetic top-ups during interim services, which improves brand upsell margins.

Motorcycle Engine Oil, serving 78% of the registered vehicle base, is projected to post the fastest growth at a 2.18% CAGR to 2030. The Pakistan automotive engine oil market benefits from the segment’s short 3,000-4,000 km drain norms, which sustain volume. Thinner 10W-40 multigrades gain share in branded retail packs, though bulk mineral CB-40 still dominates roadside mechanics. Two-wheeler OEMs are extending warranties that require branded synthetics, seeding gradual premiumisation.

Heavy Duty Motor Oil aligns with freight intensity that keeps 300,000+ registered trucks on the road. Fleet managers favor monograde SAE 40 for cost reasons yet test semi-synthetics for long-haul coastal routes. Euro-5 fuel adoption will push low-SAPS HDMO that protects after-treatment devices, especially among fleets serving Karachi-Lahore green-lane routes.

By Base Stock: Mineral Foundation Persists but Synthetics Gain Momentum

Mineral oils accounted for 64.38% of Pakistan automotive engine oils market share in 2024, reflecting price sensitivity and the dominance of older engines. The Pakistan automotive engine oils market size attached to mineral grades remains large but faces gradual erosion. Bulk drums sold through independent workshops offer cost advantages but also pose a counterfeit risk, prompting branded players to invest in tamper-evident packaging.

Semi-synthetic oils bridge the gap between affordability and performance, capturing owner-drivers who recognize that longer drain intervals reduce their lifetime costs. Blenders highlight a 5,000-7,000 km drain potential, compared to 4,000 km for their mineral peers. Semi-synthetics also provide a margin cushion in an inflationary setting because the performance narrative justifies a moderate price premium.

Synthetic oils are forecasted to grow at a 2.31% CAGR, driven by OEM specifications for new passenger cars and large fleets that track total cost of ownership through telematics. Castrol’s regional push of 0W-20 formulations illustrates how modern engines need low-viscosity synthetics to unlock fuel gains. As domestic blending capacities come online, synthetics will shed some of their foreign exchange cost burden, narrowing price differentials.

Bio-based formulations remain niche but receive policy attention under Pakistan’s climate commitments. Pilot supply to ride-sharing fleets in Lahore seeks ESG branding value rather than immediate economic payback, yet it seeds a future sub-segment that may scale once duty rebates emerge.

Geography Analysis

Lahore’s expanding Ring Road has increased commute volumes, supporting dense mechanic networks that stock branded multigrades. Karachi in Sindh continues to rely on its port-centric, heavy transport operations, which require HDMO suited for high-sulfur fuel blends. Both provinces host refinery assets, ensuring product availability and shorter supply chains.

Islamabad and Rawalpindi, despite having smaller population bases, register high per-capita lubricant use because the average household vehicle count exceeds national norms. The concentration of government and diplomatic fleets increases synthetic-grade uptake as procurement policies favor OEM-approved products. The Pakistan automotive engine oils market, therefore, exhibits premiumisation pockets even where total volumes remain modest.

Tier-2 cities such as Faisalabad, Sialkot, and Gujranwala emerge as growth hotspots. Remittance inflows fuel purchases of used cars and micro-vans, which often require immediate servicing. Local distributors expand their reach through van sales programs, offering 3-5-litre can packs designed for small workshop inventory needs. Highway corridors that knit these industrial towns to Karachi port experience high truck density, sustaining HDMO consumption. Rural districts lag in per-capita use, yet government road-building and farm mechanization slowly expand sump count, rendering these areas strategic for long-term volume capture.

Competitive Landscape

The Pakistan Automotive Engine Oils Market is concentrated. Shell and TotalEnergies utilize branded workshops and authorized dealers, focusing on synthetic segmentation where brand equity commands premium prices. Hi-Tech Lubricants broadened into fuel retailing with 50 company-owned stations, linking lubricant promotion to pump traffic and improving channel control. Competitive battlegrounds are shifting toward tier-2 cities, where branded synthetic penetration remains low but is on the rise. Brands vie to partner with ride-sharing fleets and logistics operators that demand certified oils with data-logged performance.

Pakistan Automotive Engine Oils Industry Leaders

Shell plc

Pakistan State Oil

TotalEnergies

Chevron Corporation

Attock Petroleum Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: American multinational company Chevron Corporation invested USD 30 million to set up an automated lubricants blending plant in Pakistan, the petroleum ministry announced.

- January 2023: Pakistan State Oil (PSO) launched the country’s first fully synthetic diesel engine oil, DEO MAX. DEO MAX, which meets the API CK-4 specifications, offers a longer oil drain interval, enhanced engine protection, and reduced emissions.

Pakistan Automotive Engine Oils Market Report Scope

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Resin Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

What is the current consumption level for Pakistan automotive engine oils?

Demand stands at 209.45 million litres in 2025 and is forecast to reach 231.93 million litres by 2030.

Which product category sells the most volume?

Passenger Car Motor Oil leads with 52.46% share of national engine-oil litres in 2024.

How fast are synthetic engine oils growing in Pakistan?

Synthetic formulations are projected to expand at a 2.31% CAGR through 2030, the quickest among base stocks.

How will Euro-5 fuel adoption affect lubricant demand?

Euro-5 fuels favor low-SAPS synthetic oils, shifting value mix toward premium SKUs while gradually trimming mineral-oil share.

What challenges do lubricant blenders face with imports?

Letter-of-Credit restrictions and PKR depreciation create supply gaps and cost inflation for imported base oils.

Page last updated on: