Spearmint Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

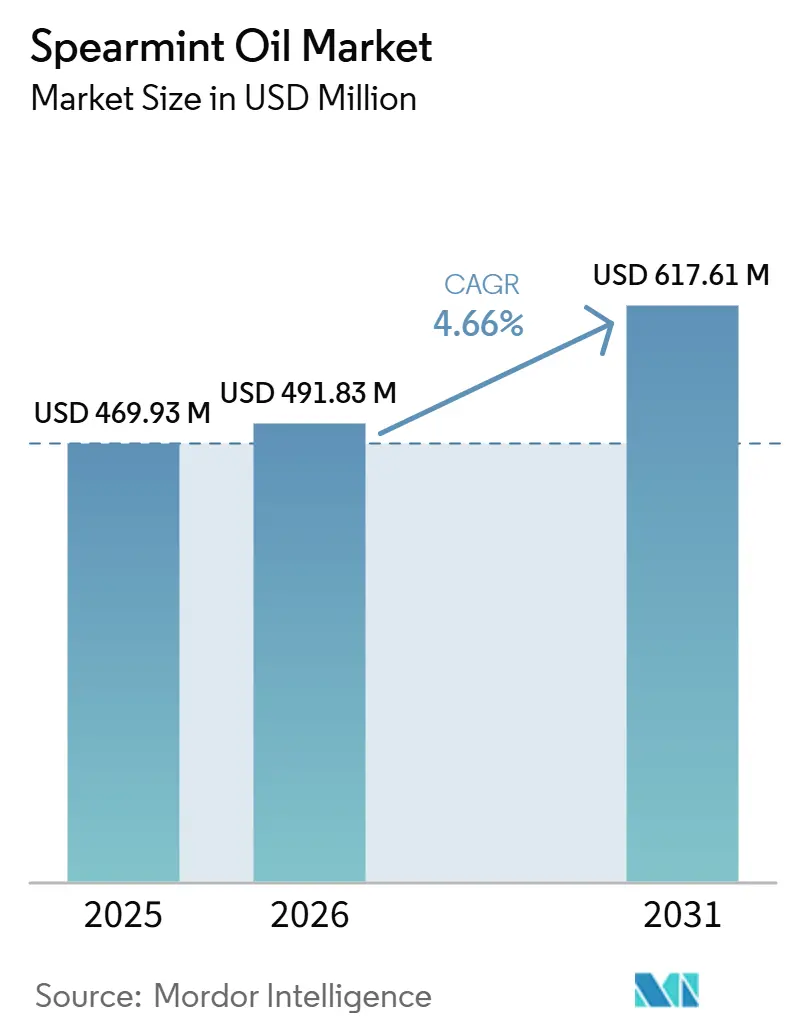

| Market Size (2026) | USD 491.83 Million |

| Market Size (2031) | USD 617.61 Million |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spearmint Oil Market Analysis by Mordor Intelligence

The Spearmint Oil Market size is projected to be USD 469.93 million in 2025, USD 491.83 million in 2026, and reach USD 617.61 million by 2031, growing at a CAGR of 4.66% from 2026 to 2031. Structural shifts are unfolding as regulators tilt preferences toward botanicals, allowing premium natural oils to advance even while synthetic menthol still dominates global tonnage. India’s 24% production drop between FY2020 and FY2024 has tightened feedstock, nudging prices higher for natural grades. North America benefits from the FDA (Food and Drug Administration) menthol-cigarette ban, which indirectly channels demand for natural cooling agents into consumer goods. At the same time, flavor houses and wellness brands are investing in blockchain traceability and micro-encapsulation to defend pricing in high-margin segments. Consolidation among the top five suppliers plus aggressive capacity additions in biotech-derived molecules signal an era of scale-driven competition.

Key Report Takeaways

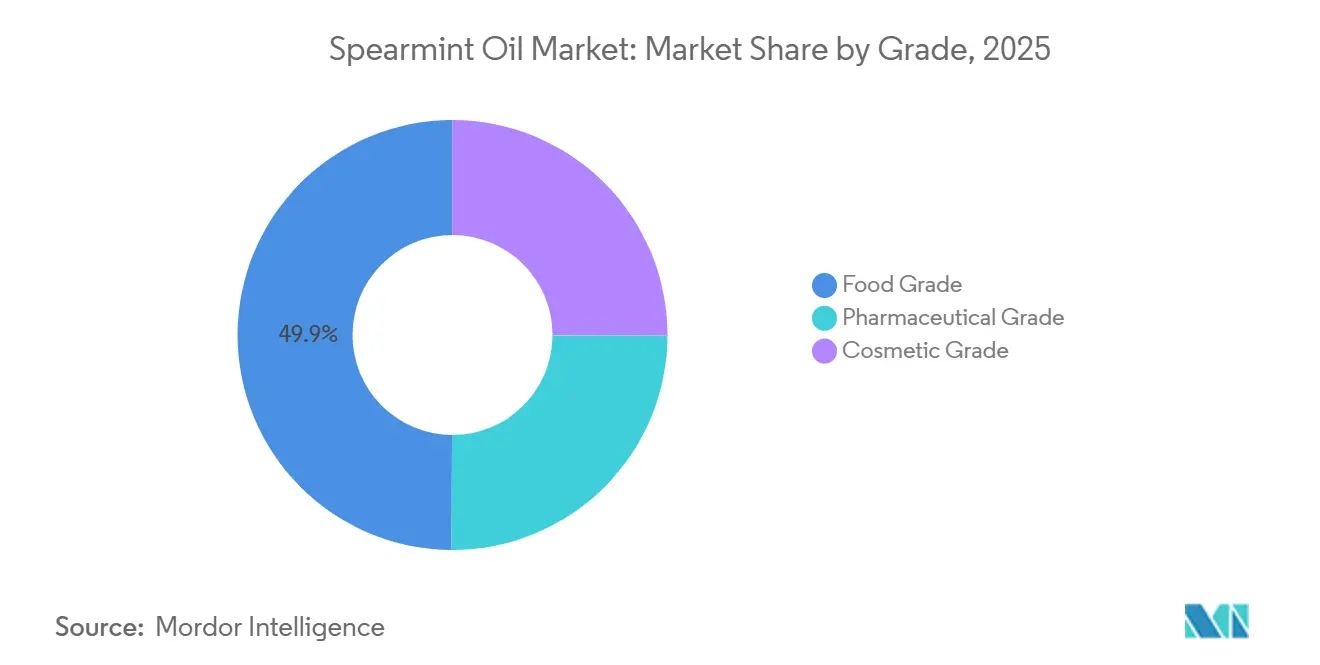

- By grade, food grade held 49.92% of the Spearmint Oil market share in 2025; pharmaceutical grade is forecast to expand at a 4.55% CAGR during the forecast period (2026-2031).

- By application, oral care and toothpaste accounted for 33.35% of the total value in 2025, whereas aromatherapy and personal care are advancing at a 4.78% CAGR to 2031.

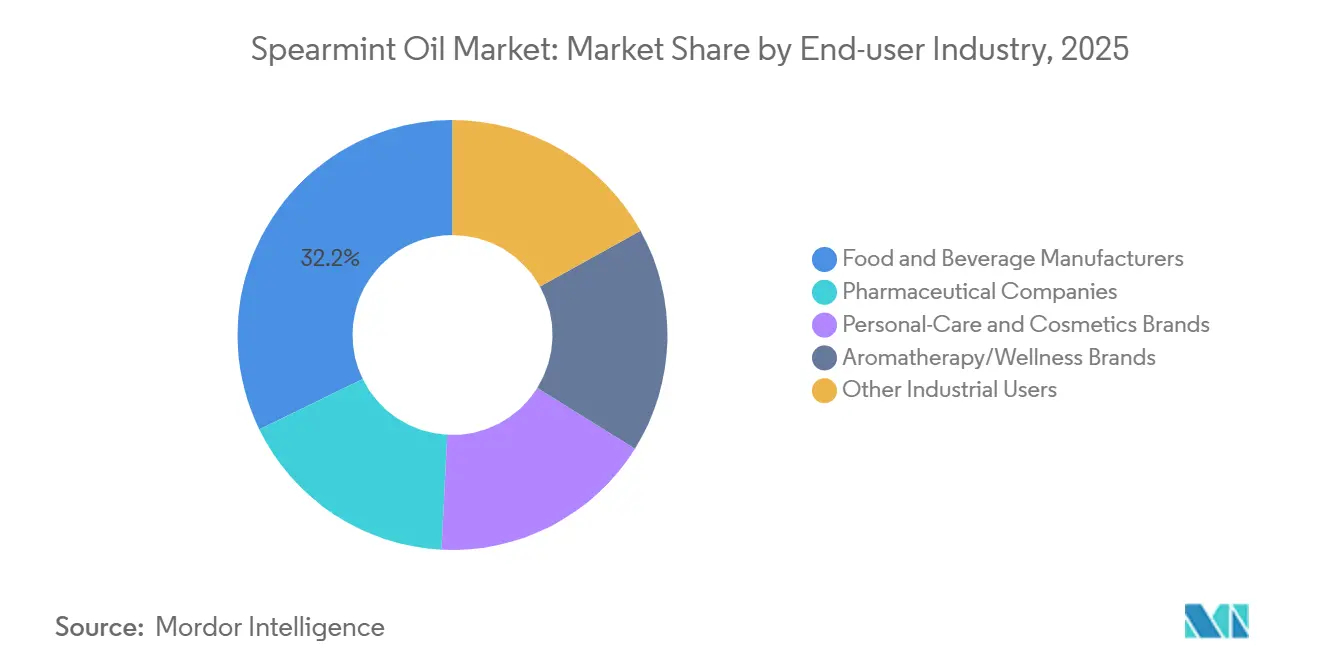

- By end-user industry, food and beverage manufacturers captured a 32.24% slice of revenue in 2025, while aromatherapy/wellness brands are poised for a 5.10% CAGR during the forecast period (2026-2031).

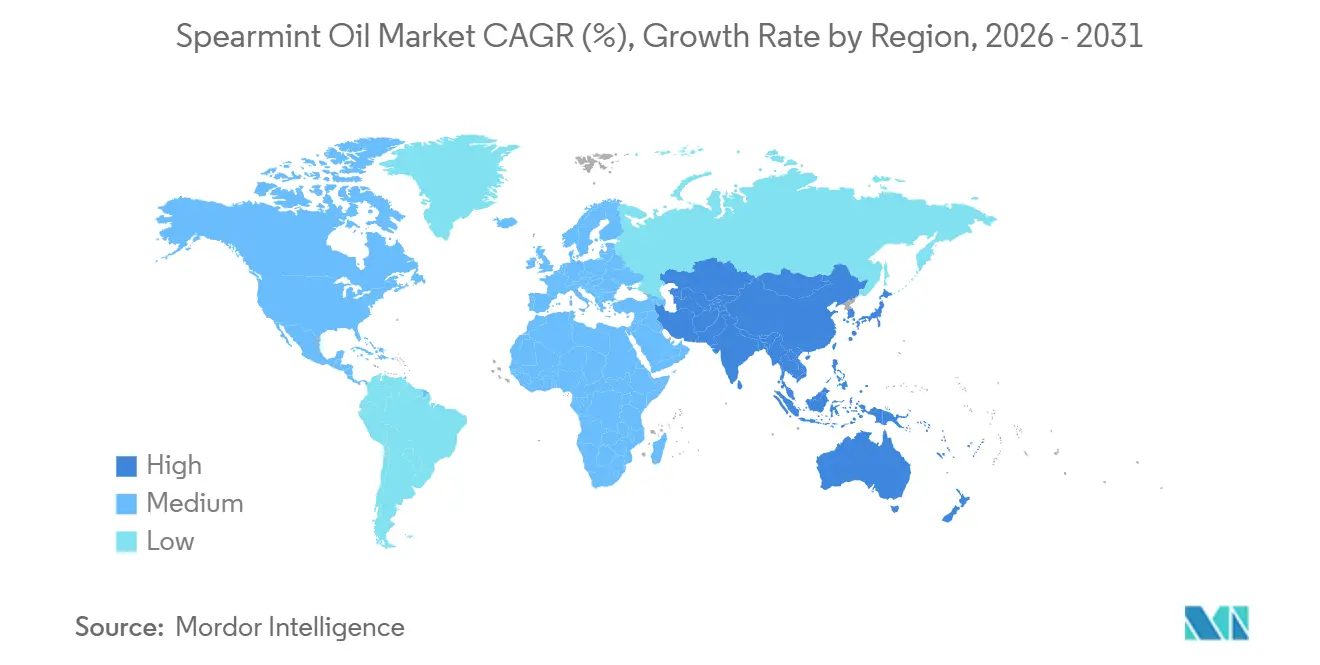

- By geography, North America commanded 38.11% of sales in 2025, yet Asia-Pacific is recording the quickest regional rise with a 5.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Spearmint Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural flavors and fragrances in food and beverage | +1.2% | Global, strongest in North America and EU | Medium term (2-4 years) |

| Increased use in oral-care and personal-care formulations | +0.9% | Global, concentrated in North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Clean-label and organic positioning of essential oils | +0.8% | North America, EU, Australia, emerging India and China | Medium term (2-4 years) |

| Functional confectionery needs (prolonged flavor release) | +0.4% | North America, Europe, Japan | Medium term (2-4 years) |

| Masking off-notes in plant-based meat analogues | +0.6% | North America, EU, spillover to urban APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural Flavors and Fragrances in Food and Beverage

Consumers favor short, recognizable ingredient lists, so formulators are swapping synthetic menthol for natural spearmint to meet clean-label mandates. The FDA treats natural menthol as GRAS (Generally Recognized as Safe), and FSSAI (Food Safety and Standards Authority of India) permits its use in food, giving botanicals a regulatory edge not enjoyed by many synthetic substitutes[1]U.S. Food and Drug Administration, “Generally Recognized as Safe (GRAS) Notices”, fda.gov. Spearmint’s modest 0.5-1% menthol content delivers a milder profile that fits fruit drinks and chewing gum, where the intense cooling of peppermint is unsuitable. Givaudan’s CHF 55 million (USD 66.38 million) Campus 52 hub in Grasse and IFF’s biotech molecules highlight long-term bets on botanical sourcing. Despite price gains from USD 19 per kg in 2020 to USD 24 per kg in 2023, demand in premium channels keeps outpacing synthetics.

Increased Use in Oral-Care and Personal-Care Formulations

Spearmint oil combines cooling with proven antimicrobial activity, which is prompting microbiome-friendly toothpaste and mouthwash launches. A 2025 study showed a 1% peppermint oil solution plus ultrasonication slashed bacterial load in chicken meat, illustrating preservative potential that oral-care brands now apply to natural preservative systems. EFSA’s July 2025 safety opinion on peppermint tincture in animal feed sets a blueprint for human applications[2]European Food Safety Authority, “Scientific Opinion on Peppermint Tincture”, efsa.europa.eu. The MIC of 1.8484 mg/mL against Streptococcus mutans elevates spearmint beyond simple flavoring. Brands leverage this dual function to market cavity defense without synthetic parabens.

Clean-Label and Organic Positioning of Essential Oils

Organic certification has become a basic ticket for premium retail placement. doTERRA joined the Union for Ethical BioTrade in October 2025, bringing 45 sourcing countries under traceability audits and creating 122,000 jobs. European Union (EU) rules cap non-approved pesticides at 0.01 mg/kg, forcing growers toward integrated pest management and driving consolidation among exporters with in-house labs. Blockchain pilots indicate a 40% fraud reduction in certified lots. Compliance costs are squeezing smaller farms, but vertically integrated suppliers recover premiums from U.S. and EU buyers.

Functional Confectionery Needs (Prolonged Flavor Release)

Long-lasting flavor is a competitive edge for gums and mints, and microencapsulated spearmint oil helps achieve that by releasing volatiles slowly during mastication. Flavor houses apply spray-drying and coacervation to stabilize monoterpenes that otherwise evaporate quickly. The controlled-release benefit lets brands claim extended freshness times versus standard formulas, an attribute consumers associate with product quality. The technology commands a 10-15% price premium yet maintains demand because synthetic menthol lacks comparable release profiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price pressure from synthetic menthol and other mint oils | -0.7% | Global, acute in Asia-Pacific price-sensitive segments | Short term (≤ 2 years) |

| Tightening trace-pesticide limits | -0.5% | EU, North America, export-oriented India and China | Medium term (2-4 years) |

| Rising land-use competition with higher-margin food crops | -0.3% | India (Uttar Pradesh, Barabanki), China (Jiangsu, Anhui) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Pressure from Synthetic Menthol and Other Mint Oils

Synthetic menthol averages USD 18,288 per ton in Asia-Pacific compared with USD 24,307 per ton for natural crystal menthol in Europe, driving a 25-30% cost gap. Exports from India dropped 60% in two years as buyers shifted to cheaper synthetics. BASF, ADM, Takasago, and Symrise run high-utilization plants that sustain oversupply, limiting any natural-oil price lift. Natural suppliers retain pricing power only in certified-organic or wellness channels where provenance carries a premium.

Tightening Trace-Pesticide Limits

EFSA lowered limits for acetamiprid and nicotine in plant oils during 2025, setting the de facto global benchmark. Growers must fund residue testing at USD 200-500 per shipment, a burden smallholders often cannot bear. Indian exporters face divergent domestic rules, so many dedicate organic acreage exclusively for EU orders, pushing up costs by as much as 20%. Preparatory work on pulegone and menthofuran toxicology suggests even tighter scrutiny ahead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Pharmaceutical Rigor Drives Premium Pricing

Food-grade oil dominated with 49.92% of Spearmint oil market share in 2025, anchored in beverages, confectionery, and gum formulations. The Spearmint oil market size for pharmaceutical-grade material is poised to rise at 4.55% CAGR through 2031 as topical analgesics, cough syrups, and GMP-compliant excipients seek reproducible purity. Higher testing for microbial load, heavy metals, and residual solvents justifies 40-60% price premiums that mid-tier producers are now chasing by upgrading distillation lines. Cosmetic-grade supply remains small but profitable because niche perfumery houses such as Jo Malone and Tom Ford value spearmint’s herbaceous top note. EFSA’s October 2025 opinion on rosemary tincture, which outlined occupational safety protocols, provides a framework for pharmaceutical-grade spearmint producers. Across all grades, traceability documentation has shifted from a differentiator to a hard requirement for multinational buyers.

In the medium term, synthetic menthol may cap upside on commodity grades, but premium certifications like USDA Organic and Fairtrade should shield margins. Export data show India’s CSV Pharmaceuticals scaling volumes under British Pharmacopeia monographs, signaling maturing supply capability. Producers that can couple pharmacopeial compliance with aromatic profile consistency are expected to win long-term contracts with global OTC brands, reinforcing a two-tier price structure inside the Spearmint oil market.

By Application: Oral Care Anchors Volume, Aromatherapy Captures Growth

Oral-care formulations held 33.35% share of the Spearmint oil market size in 2025 because the oil delivers cooling plus an MIC of 1.8484 mg/mL against Streptococcus mutans. Major toothpaste brands are shifting from triclosan to botanicals, opening incremental volume for natural oils. Aromatherapy and personal-care lines are growing the fastest at 4.78% CAGR to 2031, helped by MLM giants like doTERRA, which surpassed USD 2 billion revenue in 2024. Food and beverage remain substantial users but face tighter cost ceilings due to synthetic substitutes.

Pharmaceutical applications draw on established monographs, enabling spearmint to feature in topical gels and expectorants. Perfumery remains niche but influential in positioning the oil as a premium botanical. Industrial usage, such as veterinary products, is limited yet provides offtake for lower-grade fractions that do not meet food or pharma thresholds. Together, these dynamics encourage diversified demand that secures base-load consumption even as premium segments deliver margin.

By End-user Industry: Wellness Brands Outpace Traditional Manufacturers

Food and beverage manufacturers controlled 32.24% of the 2025 market demand, a testament to long-standing use in gum and drinks. However, aromatherapy/wellness brands are projected to expand at 5.10% CAGR through 2031, reflecting direct-selling models that capture the entire retail margin. doTERRA’s Co-Impact Sourcing now spans 45 countries and has injected USD 207,000 into community programs, strengthening supply-chain narratives. Young Living’s ISO/IEC 17025-accredited lab underpins purity claims that resonate with consumers.

Pharmaceutical corporations, though smaller in volume, value documented GMP (Good Manufacturing Practices) batches and secure multiyear agreements. Cosmetics firms pursue USDA (United States Department of Agriculture) Organic-certified lots, sometimes paying 45% premiums to support “clean beauty” messaging. Rising land-use competition in Uttar Pradesh and Jiangsu highlights a future in which vertically integrated wellness brands may increasingly contract farms outright to secure feedstock, reinforcing the evolution of the Spearmint oil market toward branded supply chains.

Geography Analysis

North America retained 38.11% of the Spearmint oil market in 2025, supported by the FDA menthol-cigarette ban and consumer readiness to pay for organic labels. Multi-level marketing networks enable doTERRA and Young Living to generate the majority of their combined USD 3.8 billion 2024 revenue domestically. Givaudan’s planned USD 110 million compounding site in Mexico will localize supply for U.S. clients, reflecting a nearshoring wave that also benefits Canadian buyers.

Asia-Pacific is projected to deliver a 5.22% CAGR through 2031, driven by China’s 150,000-ton domestic menthol demand and steady 4-5% compound growth. India supplies more than 70% of global natural menthol, yet output fell to 35,000 tonnes in FY2024 as growers switched to higher-margin crops. Takasago’s 3,000-ton-per-year l-Menthol capacity at Iwata and its Bengaluru taste center show the region’s dual role as producer and consumer. Japan and Korea add incremental oral-care and personal-care demand, while Australia’s certified-organic grades fetch premiums in export markets.

Europe, South America, and the Middle-East and Africa share the remaining demand. EFSA’s July 2025 opinion on peppermint tincture removes regulatory ambiguity and supports broader botanical adoption in feed and food. Givaudan’s CHF 55 million (USD 66.38 million) Campus 52 in Grasse cements Europe as an research and development nucleus for naturals though production seeking cost advantages relocates elsewhere. Brazil’s natural-products boom and Saudi diversification programs create future upside, but short-term growth is tempered by limited local distillation capacity and price sensitivity in several import-reliant economies.

Competitive Landscape

The Spearmint Oil market is moderately fragmented. White-space opportunities reside in microencapsulated spearmint for plant-protein meat and in GMP-grade APIs, areas where incumbent flavor houses have not yet locked up supply chains. The race to balance cost, purity, and transparency will shape competitive trajectories inside the Spearmint oil market during 2026-2031.

Spearmint Oil Industry Leaders

International Flavors & Fragrances Inc.

Givaudan

Symrise

Takasago International Corporation

Lebermuth, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: The USDA's Agricultural Marketing Service proposed a rule to revise the purchase limits for Class 3 (Native) spearmint oil. The changes affect handlers in Washington, Idaho, Oregon, and select areas in Nevada and Utah. The salable quantity of Native spearmint oil for the 2024-2025 marketing year would rise from 678,980 pounds to 731,220 pounds.

- June 2024: Nebraska Ag Connection highlighted research findings on optimized nitrogen management for mint production, demonstrating that polymer-coated urea significantly enhances yields while reducing greenhouse gas emissions. This can substantially benefit the Spearmint Oil Market.

Global Spearmint Oil Market Report Scope

Spearmint oil is an essential oil extracted via steam distillation from the leaves of the Mentha spicata plant. It is known for its sweet, refreshing, and minty aroma, containing high levels of carvone and low levels of menthol, making it a milder alternative to peppermint oil. It is commonly used in aromatherapy, oral care, and for promoting digestion.

The Spearmint Oil market is segmented by grade, application, end-user industry, and geography. By grade, the market is segmented into food grade, pharmaceutical grade, and cosmetic grade. By application, the market is segmented into food and beverages, pharmaceuticals, oral care and toothpaste, fragrances and cosmetics, aromatherapy and personal care, and other applications. By end-user industry, the market is segmented into food and beverage manufacturers, pharmaceutical companies, personal-care and cosmetics brands, aromatherapy/wellness brands, and other industrial users. The report also covers the market size and forecasts for spearmint oil in 18 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Food Grade |

| Pharmaceutical Grade |

| Cosmetic Grade |

| Food and Beverages |

| Pharmaceuticals |

| Oral Care and Toothpaste |

| Fragrances and Cosmetics |

| Aromatherapy and Personal Care |

| Other Applications |

| Food and Beverage Manufacturers |

| Pharmaceutical Companies |

| Personal-Care and Cosmetics Brands |

| Aromatherapy/Wellness Brands |

| Other Industrial Users |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Food Grade | |

| Pharmaceutical Grade | ||

| Cosmetic Grade | ||

| By Application | Food and Beverages | |

| Pharmaceuticals | ||

| Oral Care and Toothpaste | ||

| Fragrances and Cosmetics | ||

| Aromatherapy and Personal Care | ||

| Other Applications | ||

| By End-user Industry | Food and Beverage Manufacturers | |

| Pharmaceutical Companies | ||

| Personal-Care and Cosmetics Brands | ||

| Aromatherapy/Wellness Brands | ||

| Other Industrial Users | ||

| By Geography | Asia-Pacific | India |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the global spearmint category today?

The Spearmint oil market size stood at USD 491.83 million in 2026 and is projected to reach USD 617.61 million by 2031.

What is the forecast growth rate through 2031?

The market is expected to expand at a 4.66% CAGR during the forecast period (2026-2031), driven by clean-label demand and wellness applications.

Which segment is growing the fastest?

Aromatherapy and personal-care lines are advancing at a 4.78% CAGR during the forecast period (2026-2031) as direct-to-consumer brands gain share.

Why are natural grades priced higher than synthetic menthol?

Natural oils incur higher cultivation, residue testing, and certification costs, but earn premiums for organic and traceable supply chains.

Page last updated on: